Cybersecurity Skills Assessment And Talent Platforms Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

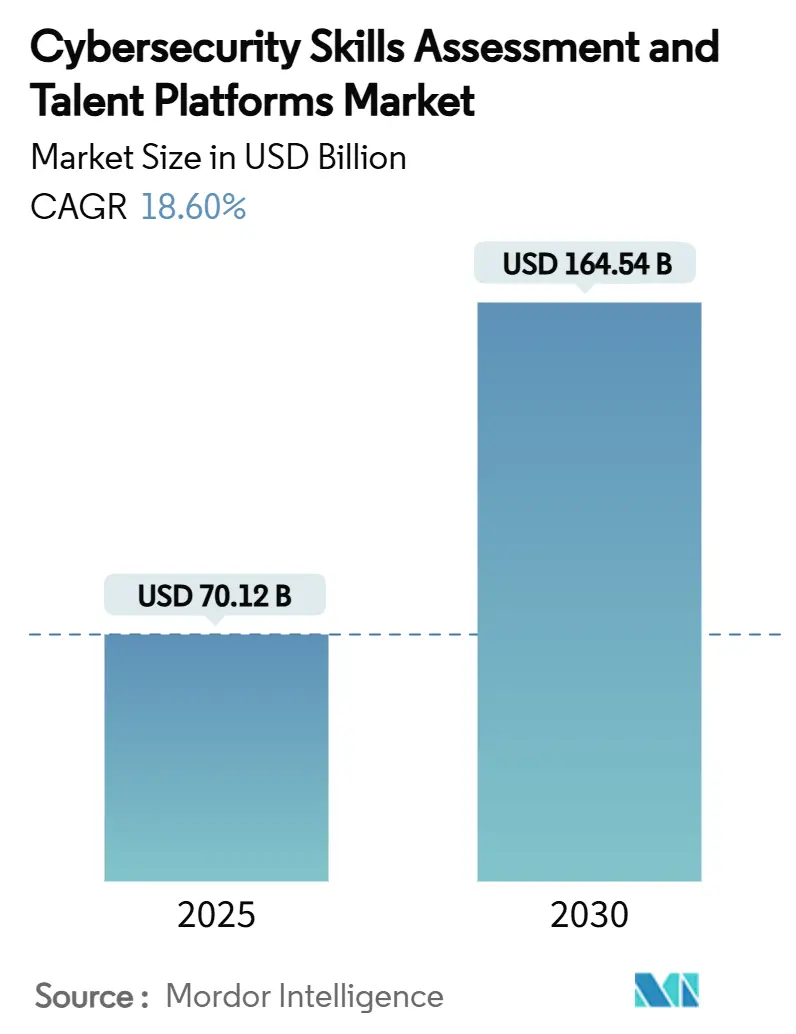

| Market Size (2025) | USD 70.12 Billion |

| Market Size (2030) | USD 164.54 Billion |

| Growth Rate (2025 - 2030) | 18.60% CAGR |

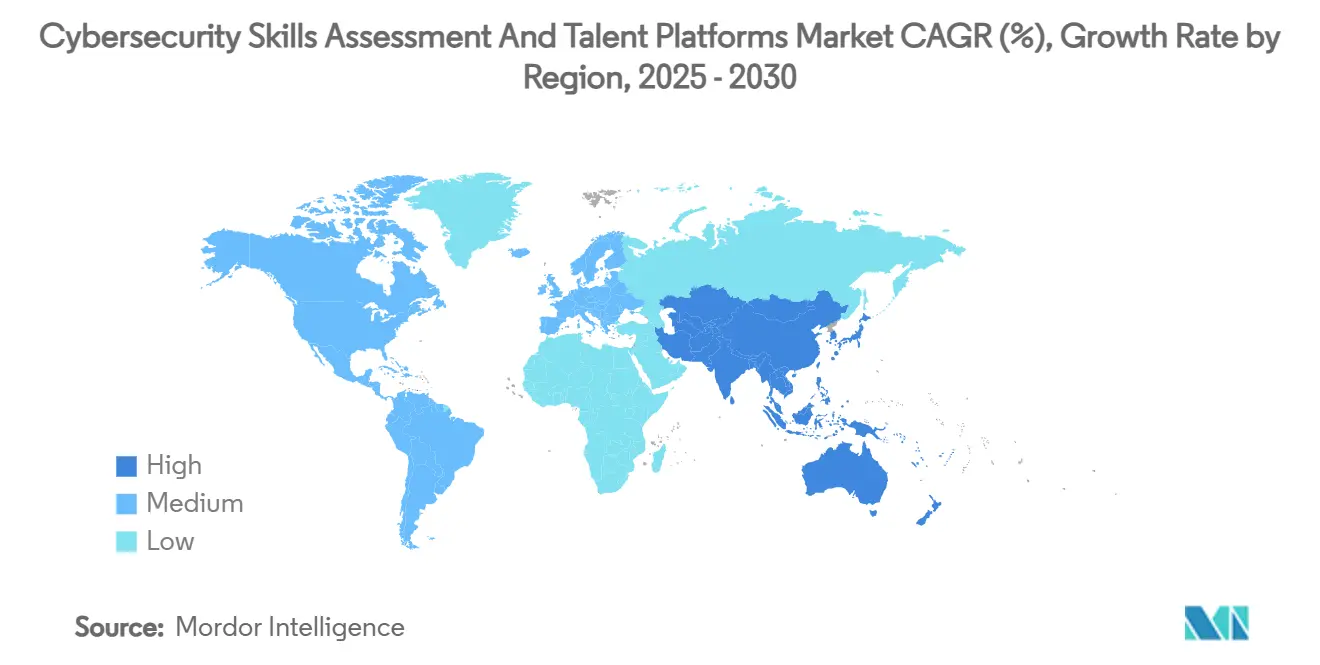

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cybersecurity Skills Assessment And Talent Platforms Market Analysis by Mordor Intelligence

The Cybersecurity skills assessment and talent platforms market size stood at USD 70.12 billion in 2025 and is expected to reach USD 164.54 billion by 2030, advancing at an 18.6% CAGR. Heightened cyber-insurance demands for documented workforce competency, mandatory zero-trust roll-outs, and AI-driven adaptive labs continue to expand the addressable user base and lower the total cost of ownership for assessment suites. Venture investment in cloud-native cyber-laboratory start-ups accelerates tool innovation, while the transition from static knowledge tests to dynamic skills verification reshapes competitive positioning. North America maintains leadership on the back of Department of Defense 8140 compliance, yet Asia-Pacific scales rapidly as regional governments embed workforce development into national cybersecurity strategies. Across all regions, platform vendors differentiate through purple-team simulations, real-time competency tracking, and hybrid deployment options that satisfy data-sovereignty rules.

Key Report Takeaways

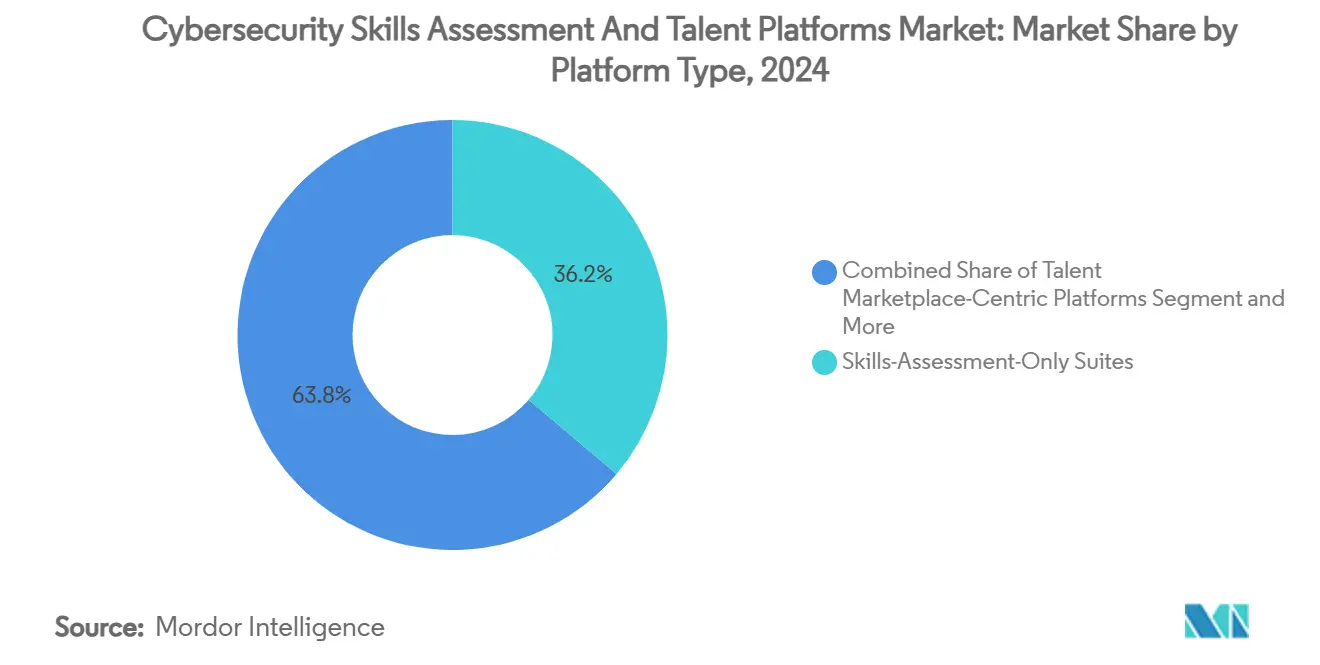

- By platform type, skills-assessment-only suites led with 36.2% revenue share of the cybersecurity skills assessment and talent platforms market in 2024, while talent marketplace-centric platforms are projected to expand at a 19.9% CAGR through 2030.

- By deployment mode, cloud-based solutions captured 57.3% of the cybersecurity skills assessment and talent platforms market size in 2024; hybrid architectures are forecast to grow at a 20.1% CAGR to 2030.

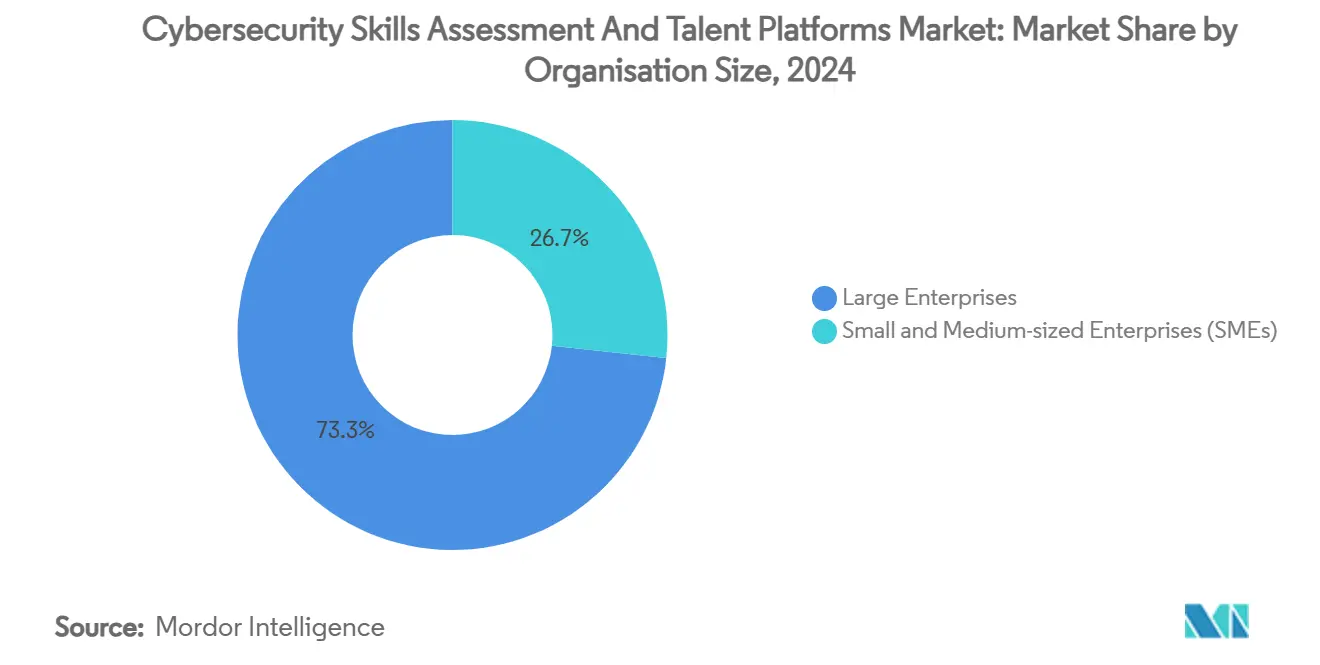

- By organisation size, large enterprises commanded a 73.3% share of the cybersecurity skills assessment and talent platforms market in 2024, whereas SMEs are expected to advance at a 20.3% CAGR between 2025-2030.

- By end-user industry, IT and telecom accounted for 29.4% of the cybersecurity skills assessment and talent platforms market revenue in 2024; government and defense are set to register the fastest growth at 19.7% CAGR through 2030.

- By geography, North America held a 38.2% share of the cybersecurity skills assessment and talent platforms market in 2024, while the Asia-Pacific is poised to rise at a 20% CAGR during the forecast period.

Global Cybersecurity Skills Assessment And Talent Platforms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-native adoption widens skills-gap urgency | +3.2% | North America, Europe | Medium term (2-4 years) |

| Escalating cyber-insurance prerequisites | +2.8% | North America, Europe, APAC | Short term (≤ 2 years) |

| Mandatory zero-trust roll-outs | +2.1% | North America, EU, Australia, Singapore | Medium term (2-4 years) |

| AI-driven adaptive labs | +1.9% | Global | Long term (≥ 4 years) |

| Venture funding surge in cyber-labs | +1.5% | North America, Europe, APAC | Short term (≤ 2 years) |

| Rise of offensive-security culture | +1.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-native adoption widens skills-gap urgency

Mass migration to containerised and serverless architectures exposes gaps in traditional perimeter-centric security skill sets. Enterprises discover that incumbent credentials do not validate practical competence in securing micro-services, prompting rapid uptake of labs that measure real-world cloud incident response. [1]Susana Barraza, “The Landscape of Performance-Based Assessments in Cybersecurity,” National Institute of Standards and Technology, nist.gov Platforms respond with scenario-based tasks mirroring multi-cloud breaches, reinforcing hands-on validation over theoretical exams. The capability to spin up ephemeral cloud labs on demand reduces hardware cost and supports geographically dispersed teams. Vendors leveraging automation to refresh cloud-specific challenge content every quarter sustain customer retention and differentiate on realism. As a result, the Cybersecurity skills assessment and talent platforms market benefits from continuous demand across both regulated and commercial sectors.

Escalating cyber-insurance prerequisites for validated workforce competency

Underwriters now penalise applicants who lack documented skills validation across key security roles. Frameworks from major brokers embed minimum certification matrices, compelling firms to institutionalise annual reassessments or face premium surcharges. Assessment suites with verifiable audit trails gain traction among finance and healthcare providers seeking to meet policy clauses efficiently. Insurance-driven urgency brings SMEs into the market as subscription-based platforms lower entry costs. This systemic linkage between insurance and workforce proof points sustains double-digit growth for vendors that can map platform outputs directly to underwriting templates.

Mandatory zero-trust roll-outs under new public-sector directives

Federal agencies must show proficiency in micro-segmentation, identity governance, and continuous verification before system accreditation, creating specialised demand for zero-trust assessment modules. Platforms embed government network topologies within test ranges, enabling staff to demonstrate capabilities under authentic constraints. Contractors supporting federal programmes adopt identical modules to maintain bid eligibility, extending the market beyond core agencies. Continuous refresh cycles, aligned with evolving zero-trust maturity models, lock in multi-year subscriptions and add recurring revenue streams for best-in-class vendors.

AI-driven adaptive labs reduce assessment cost and boost adoption

Generative algorithms craft unique exploit chains and tailor difficulty in real time, slashing manual content-development outlays while keeping challenges fresh. Personalised feedback loops accelerate learner progression, improving completion rates and platform stickiness. Cost savings enable vendors to price tiers competitively for mid-market customers without sacrificing content depth. Enterprises benefit from granular analytics that map adaptive performance to specific role competency matrices. Over the long term, AI-enabled scalability propels the Cybersecurity skills assessment and talent platforms market into adjacent training and certification niches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short shelf-life of challenge content | -2.4% | Global | Short term (≤ 2 years) |

| Skills-bias and test-fairness concerns | -1.8% | North America, Europe, APAC | Medium term (2-4 years) |

| Fragmented global certification standards | -1.2% | Global | Long term (≥ 4 years) |

| Data-sovereignty rules constrain cloud skills-labs | -0.9% | Europe, APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Short shelf-life of challenge content inflates platform OPEX

Attack vectors, tooling, and defensive controls iterate within months, making static challenges obsolete and forcing frequent content renewal. Smaller vendors struggle to amortise research costs, raising subscription fees or delaying updates, which erodes customer confidence. Large platforms mitigate with AI-assisted content generation and community-sourced scenario proposals, but still incur specialist review overhead. As a result, profitability hinges on balancing freshness with sustainable development cycles.

Skills-bias and test-fairness concerns slow HR adoption

Academic evidence shows recruiter gender can influence evaluation criteria, raising anxiety over unconscious bias embedded within assessments. [2]Joanne Hall and Asha Rao, “Gender of Recruiter Makes a Difference,” arXiv, arxiv.org Enterprises now request third-party fairness audits and demographic analytics before platform rollout. Vendors invest in inclusive content design and algorithmic transparency, lengthening product-development timelines. While necessary for equitable hiring, these safeguards temporarily slow deployment within risk-averse sectors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: Skills-Assessment-Only Suites retain leadership amid marketplace surge

Skills-Assessment-Only Suites commanded 36.2% of the Cybersecurity skills assessment and talent platforms market share in 2024, reflecting the enterprise's need for focused benchmarking independent of training workflows. [3]“Hiring Cybersecurity Professionals Services,” CyberTalents, cybertalents.com These suites emphasise proctored labs, role-based scoring, and audit-ready reporting, making them indispensable for regulated industries. Their lightweight integration with HR systems minimises change-management friction, sustaining high renewal rates. Conversely, Talent Marketplace-Centric Platforms are accelerating at 19.9% CAGR as firms tap gig-economy specialists for burst capacity. Artificial intelligence curates candidate pools, mapping verified lab scores to project requirements in near real time, which expedites staffing and lowers recruitment overhead. The Cybersecurity skills assessment and talent platforms market thus balances maturity in assessment-only offerings with disruptive marketplace innovation.

Integrated Assessment + Training Labs address mid-market customers that lack in-house learning content, bundling skill gaps analysis with adaptive coursework. Certification-Preparation Portals persist as entry points for professionals pursuing role-specific credentials, yet their share stabilises as employers privilege performance-based evidence over multiple-choice tests. Product road-maps increasingly converge: assessment-centric vendors embed micro-learning bites, while training-heavy providers add scored challenges, progressively blurring category boundaries inside the Cybersecurity skills assessment and talent platforms market.

By Deployment Mode: Cloud dominance meets hybrid expansion

Cloud deployments captured 57.3% of the Cybersecurity skills assessment and talent platforms market size in 2024 on the strength of rapid provisioning, elastic scaling, and zero capex. Multi-tenant architectures enable vendors to ship weekly feature updates without customer downtime, boosting user experience and reducing total ownership cost. However, national data-protection laws and critical-infrastructure mandates are steering a portion of demand toward hybrid models, which are forecast to grow at a 20.1% CAGR through 2030. Hybrid platforms place sensitive learner artefacts within sovereign borders while maintaining SaaS control planes in regional clouds, satisfying compliance without forfeiting scalability. On-premises installations persist within defense and intelligence communities that require air-gapped ranges; yet their share gradually declines as secure government clouds mature.

Vendor differentiation hinges on deployment flexibility, with modular architecture enabling customers to toggle between hosting models as regulatory environments evolve. Edge computing nodes decrease latency for global workforces, reinforcing hybrid value propositions. Consequently, the Cybersecurity skills assessment and talent platforms market increasingly rewards providers capable of orchestrating seamless workload portability across clouds, data centres, and tactical edge locations.

By Organisation Size: Enterprises dominate, SMEs accelerate

Large enterprises generated 73.3% of 2024 revenue by embedding assessments into strategic talent-management programs, regulatory audits, and cyber-maturity dashboards. Deep integration with HR information systems automates skill-gap analytics, enabling CISOs to align training spend with risk heat maps. Enterprises also purchase custom lab content mirroring proprietary tech stacks, driving high average-revenue-per-user within the Cybersecurity skills assessment and talent platforms market.

SMEs, constrained by limited security headcount, are now propelled into the market by cyber-insurance clauses that require periodic skills verification. Subscription models starting below USD 10,000 per year offer affordable compliance paths, and cloud delivery eliminates infrastructure hurdles. Research shows that up-skilling in-house staff costs USD 1,252 per employee annually versus USD 4,000 for external hires, reinforcing ROI narratives. Vendors capitalise by bundling templated assessments, automated reporting, and self-paced learning aligned to common SME pain points such as phishing defense and endpoint hygiene. As cyber-attacks increasingly target small businesses, SME adoption drives incremental growth across regions.

By End-user Industry: IT leadership faces government momentum

IT and telecom firms held a 29.4% share of the Cybersecurity skills assessment and talent platforms market in 2024, leveraging assessments to certify cloud engineers, DevSecOps teams, and SOC analysts against service-level obligations. Constant product releases and customer data custodianship compel continuous workforce validation, sustaining platform utilisation.

Government and defense agencies, however, are projected to grow at a 19.7% CAGR as zero-trust mandates and Department of Defense 8140 role-based requirements formalise assessment workflows. The Federal Virtual Training Environment supported over 139,000 users in 2024, showcasing scale and cost savings of USD 49 million. Healthcare, manufacturing, and retail sectors follow, driven by connected-device security, operational-technology threats, and payment-card data protection, respectively. BFSI maintains steady adoption as regulators tighten expectations on incident-response readiness and fraud countermeasures. Collectively, these dynamics diversify revenue streams within the Cybersecurity skills assessment and talent platforms industry and reduce dependence on any single vertical.

Geography Analysis

North America commanded 38.2% of 2024 revenue, underpinned by Department of Defense 8140 and Executive Order 13870, which institutionalized aptitude assessments across federal agencies. [4]U.S. Office of Personnel Management, “America’s Cybersecurity Workforce Executive Order 13870,” chcoc.gov Venture capital concentration accelerates product innovation, with deals such as OffSec’s acquisition fueling content expansion. Large financial and healthcare entities invest in Purple-Team Labs to meet cyber-insurance discounts, reinforcing regional platform spend. Mature cloud infrastructure and high breach awareness underpin premium acceptance of AI-enhanced offerings.

Asia-Pacific is the fastest-growing geography, on track for a 20% CAGR through 2030. Government skills academies in Singapore, Japan-ASEAN capacity programmes, and India’s burgeoning IT services sector form a compound growth engine. Local vendors partner with global platforms to localise content, while Western providers establish regional data centres to comply with sovereignty rules. Rising cyber-insurance penetration among mid-market enterprises broadens the user base beyond large conglomerates, boosting the Cybersecurity skills assessment and talent platforms market across the region.

Europe records solid mid-teens growth as the NIS 2 Directive and GDPR force organisations to validate workforce competence. ENISA’s 2024 study reveals that 89% of companies anticipate additional cyber staff needs, directly linking to assessment demand. Data residency laws encourage hybrid deployments hosted within EU borders, benefiting providers with local infrastructure. Public-private initiatives such as the EU Cybersecurity Skills Academy foster standardised competency models, streamlining platform adoption. Markets in Germany, France, and the United Kingdom lead spending, supported by robust manufacturing and finance sectors.

Competitive Landscape

The Cybersecurity skills assessment and talent platforms market is moderately fragmented. No single vendor exceeds 15% global revenue, yet the top five players collectively hold about 45%, positioning the market at a balanced midpoint between consolidation and fragmentation. Legacy certification bodies fortify their brands through hands-on labs, while digital-native start-ups introduce AI-driven marketplaces linking verified talent to outbound projects.

Strategic activity intensified in 2024-2025: KnowBe4 moved to acquire Egress, merging behavioural risk scoring with email threat protection. Leeds Equity Partners backed OffSec, financing the expansion of its 4,000-plus lab library. Hack The Box launched integrated purple-team content, while Immersive Labs unveiled an AI Scenario Generator, both elevating simulation realism. Vendors also integrate with HR systems, applicant-tracking software, and security-operations platforms, turning competency data into actionable workforce intelligence.

Platform differentiation pivots on adaptive content generation, predictive analytics that map skill gaps to threat intelligence, and flexible deployment architectures. Providers capable of demonstrating measurable cost savings—such as FedVTE’s USD 49 million annual reduction—gain procurement advantage in fiscally constrained agencies. Meanwhile, open standard APIs and microservice designs become table stakes for enterprise-wide orchestration.

Cybersecurity Skills Assessment And Talent Platforms Industry Leaders

Immersive Labs plc

Hack The Box Ltd.

RangeForce Inc.

OffSec Services Ltd.

Cybrary, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: KnowBe4 announced the acquisition of Egress to integrate email security with security-awareness training.

- November 2024: ENISA’s NIS Investments 2024 report highlighted 89% of firms needing extra cyber staff.

- October 2024: Leeds Equity Partners acquired OffSec, expanding hands-on certification offerings.

- August 2024: LP First Capital and Genesis Park launched the National Cyber Group to address workforce gaps.

Global Cybersecurity Skills Assessment And Talent Platforms Market Report Scope

| Skills-Assessment-Only Suites |

| Integrated Assessment + Training Labs |

| Talent Marketplace-Centric Platforms |

| Certification-Preparation Portals |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Small and Medium-sized Enterprises |

| Large Enterprises |

| BFSI |

| Government and Defense |

| IT and Telecom |

| Healthcare |

| Manufacturing |

| Retail and E-Commerce |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Platform Type | Skills-Assessment-Only Suites | ||

| Integrated Assessment + Training Labs | |||

| Talent Marketplace-Centric Platforms | |||

| Certification-Preparation Portals | |||

| By Deployment Mode | Cloud-Based | ||

| Hybrid | |||

| On-Premises | |||

| By Organisation Size | Small and Medium-sized Enterprises | ||

| Large Enterprises | |||

| By End-user Industry | BFSI | ||

| Government and Defense | |||

| IT and Telecom | |||

| Healthcare | |||

| Manufacturing | |||

| Retail and E-Commerce | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What growth rate is forecast for cybersecurity skills assessment platforms through 2030?

The Cybersecurity skills assessment and talent platforms market is projected to grow at an 18.6% CAGR, rising from USD 70.12 billion in 2025 to USD 164.54 billion by 2030.

Which platform type currently leads adoption?

Skills-Assessment-Only Suites held 36.2% market share in 2024, driven by demand for focused, audit-ready evaluations.

Why are cyber-insurance policies influencing platform uptake?

Insurers now require documented workforce competency; firms without validated skills face higher premiums, making assessment suites a cost-avoidance measure.

How do hybrid deployments address data-sovereignty rules?

Hybrid architectures store sensitive learner data inside national borders while using regional clouds for processing, satisfying compliance without sacrificing scalability.

Which region is growing fastest?

Asia-Pacific is forecast at 20% CAGR through 2030, supported by government skills academies and expanding cyber-insurance adoption.

How does AI improve assessment effectiveness?

AI-driven labs generate adaptive scenarios and personalised feedback, lowering content-development costs and improving learner engagement.

Page last updated on: