Glucagon Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

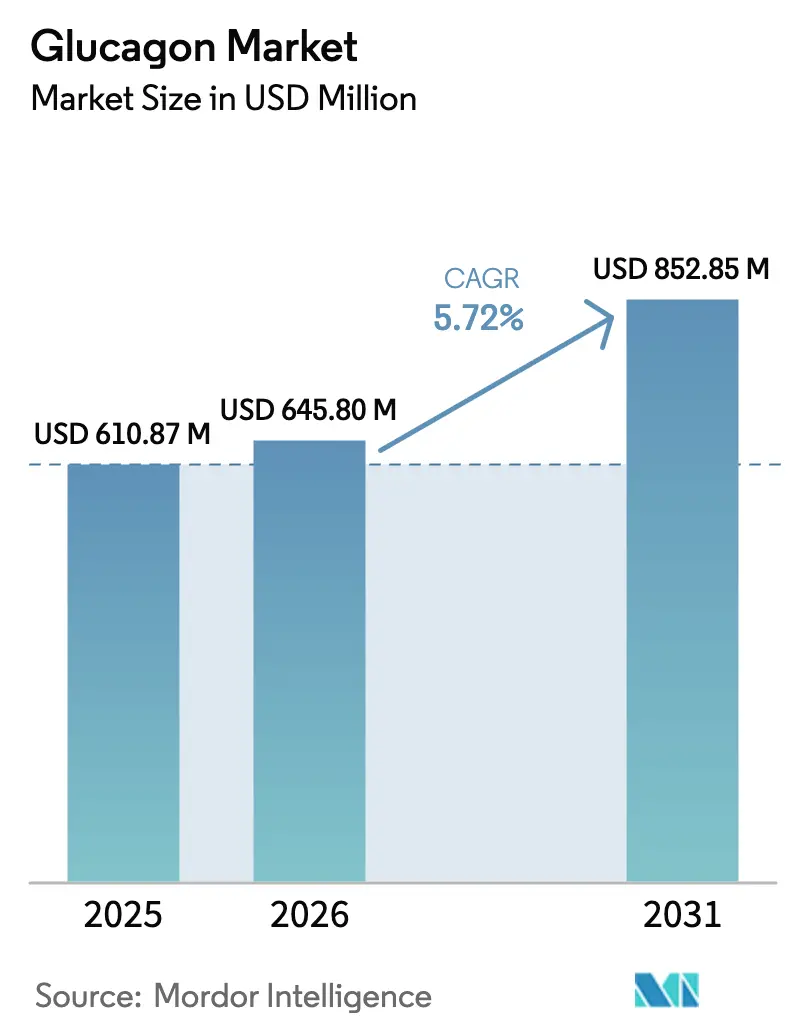

| Market Size (2026) | USD 645.8 Million |

| Market Size (2031) | USD 852.85 Million |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Glucagon Market Analysis by Mordor Intelligence

The glucagon market size is expected to grow from USD 610.87 million in 2025 to USD 645.8 million in 2026 and is forecast to reach USD 852.85 million by 2031 at 5.72% CAGR over 2026-2031. Robust expansion stems from the pivot away from multi-step reconstitution kits toward ready-to-use nasal powders, autoinjectors and dual-hormone pump cartridges that improve response times for severe hypoglycemia and broaden metabolic use cases. Supply-chain consolidation amplifies competitive stakes because a halt in pre-filled syringe availability forced Novo Nordisk to discontinue GlucaGen HypoKit, proving how a single component shortfall can suppress access. Rising pediatric diabetes incidence, guideline mandates that every insulin-treated patient receive glucagon, and employer-funded placement of kits in schools and workplaces further enlarge the addressable base. Meanwhile, technology alliances that embed liquid-stable glucagon in artificial-pancreas systems re-position the product from an episodic rescue drug to a daily therapeutic component.

Key Report Takeaways

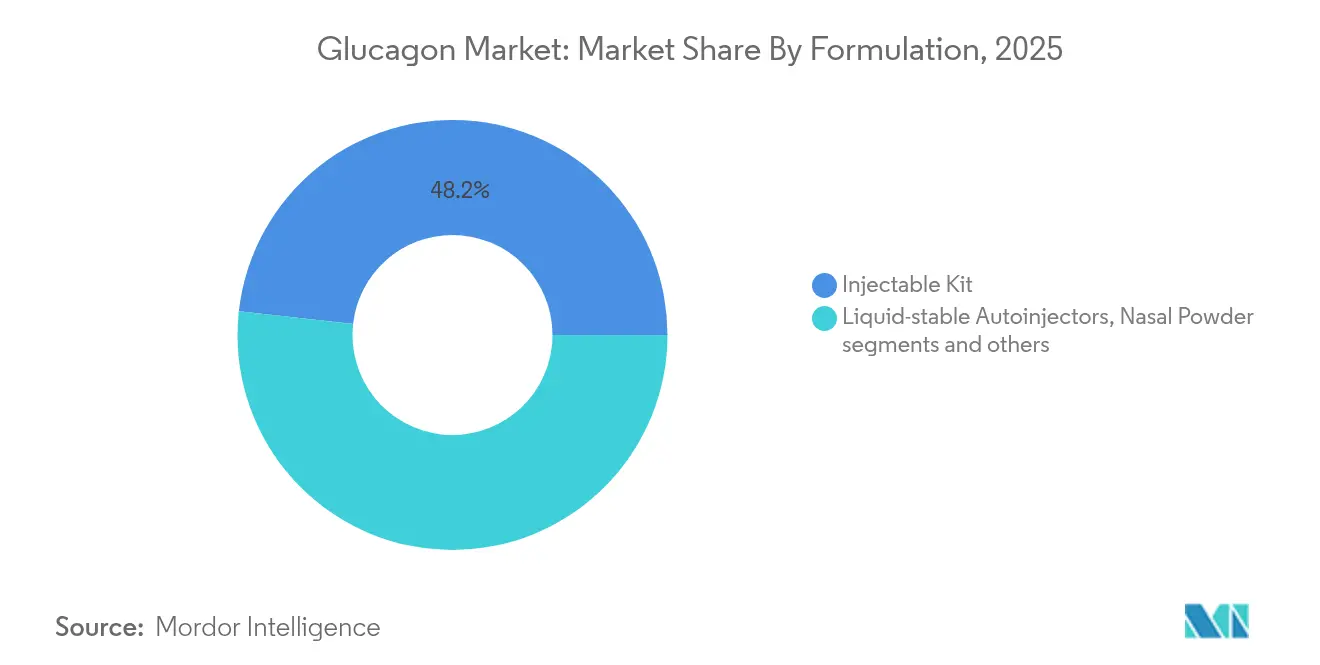

- By formulation, injectable kits led with 48.23% of glucagon market share in 2025, while nasal powder is projected to post a 6.55% CAGR through 2031.

- By route of administration, intramuscular delivery held 66.12% share of the glucagon market size in 2025; intranasal is set to grow at 6.78% CAGR to 2031.

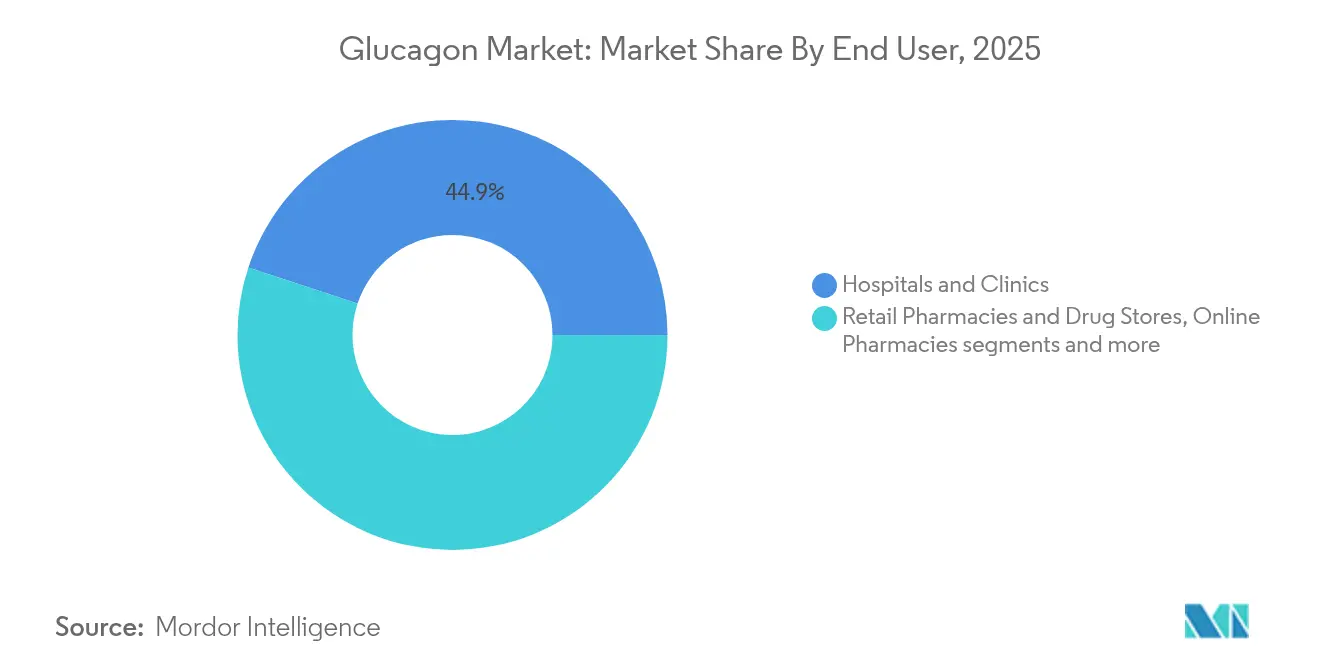

- By end-user, hospitals and clinics captured 44.92% revenue in 2025, whereas online pharmacies are forecast to expand at 8.01% CAGR.

- By indication, severe hypoglycemia dominated with 81.92% share in 2025; adjunct obesity trials will climb at 7.12% CAGR.

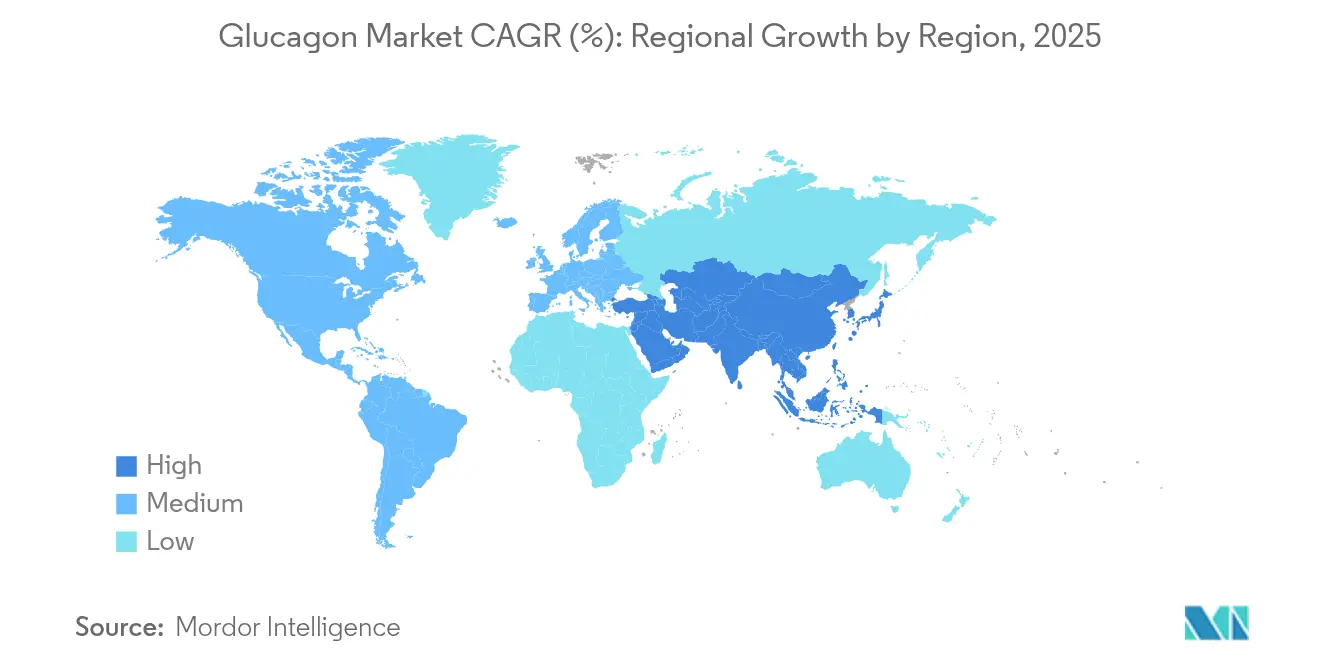

- By geography, North America commanded 38.41% of the glucagon market in 2025; Asia-Pacific is the fastest-growing region at 7.35% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Glucagon Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of insulin-treated diabetes and severe hypoglycemia | +1.2% | North America, Europe highest | Medium term (2-4 years) |

| Commercial rollout of ready-to-use nasal and autoinjector glucagon | +0.9% | North America, EU leading | Short term (≤ 2 years) |

| Inclusion of glucagon rescue kits in national diabetes guidelines | +0.7% | Developed markets first | Long term (≥ 4 years) |

| Employer-funded distribution in schools and workplaces | +0.5% | North America core | Medium term (2-4 years) |

| Integration of glucagon cartridges in dual-hormone pump systems | +0.8% | North America, EU core | Long term (≥ 4 years) |

| Bundled offerings with CGM and pump subscriptions | +0.6% | Global | Medium term |

| Source: Mordor Intelligence | |||

Rising Incidence of Insulin-Treated Diabetes and Severe Hypoglycemia

Intensive insulin therapy triples the likelihood of severe hypoglycemia compared with conventional regimens, expanding the pool that must keep emergency glucagon on hand[1]Source: ADA, “Standards of Medical Care in Diabetes 2024,” diabetesjournals.org. Nearly every US state now requires school staff to complete glucagon training, signalling institutional recognition of hypoglycemia as an urgent event. Pediatric type 1 diabetes is increasing 3-4% per year in developed economies, and children experience more frequent nocturnal hypoglycemia than adults. Continuous glucose monitoring sharpens awareness of low-glucose episodes, prompting physicians to prescribe multiple rescue kits per patient. These factors underpin sustained volume growth across both retail and institutional channels.

Commercial Rollout of Ready-to-Use Nasal and Autoinjector Glucagon

Needle-free and liquid-stable formats remove reconstitution errors that previously discouraged lay responders. Baqsimi’s nasal powder matched intramuscular bioavailability while cutting administration time below 30 seconds ema.europa.eu. Gvoke’s autoinjector recorded 99% adult treatment success and 100% in pediatric cohorts, driving broad clinician preference for ready-to-use devices[2]Source: Xeris Biopharma, “Gvoke Clinical Data,” xerispharma.com. Surveyed healthcare providers favored ready-to-use products 78% of the time because fewer steps improve confidence during emergencies. Hospitals anticipate that widespread adoption will trim door-to-drug intervals in ambulances and emergency departments.

Inclusion of Glucagon Rescue Kits in National Diabetes Guidelines

The 2024 ADA Standards of Care mandate that every insulin-treated patient receive a glucagon prescription, creating a de facto baseline of roughly 8 million US users. European guidelines echo this stance, especially for individuals with hypoglycemia unawareness. Japan integrated glucagon into national protocols alongside novel GLP-1 agents, extending coverage to patients newly diagnosed with obesity-related dysglycemia pharmajapan.com. Guideline alignment triggers automatic reimbursement in many single-payer systems, which lowers out-of-pocket costs. As standards spread to emerging markets, the guideline effect is poised to accelerate kit penetration well beyond historical levels.

Employer-Funded Distribution of Kits in Schools and Workplaces

Fortune 500 firms add glucagon to first-aid stations to mitigate liability and boost employee health confidence, with 34% of large US employers now providing diabetes emergency supplies. School districts emulate the approach to protect students and comply with state mandates. Institutions often purchase kits via group contracts, bypassing individual prescription hurdles. Employers report sharp reductions in ambulance calls after deploying onsite glucagon, offsetting device costs. Steady institutional volume therefore offers manufacturers a predictable, non-cyclical demand base.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing and patchy reimbursement versus insulin | -1.8% | Global, with highest impact in emerging markets | Short term (≤ 2 years) |

| API and fill-finish supply shortages | -1.1% | Global manufacturing hubs, affecting worldwide supply | Medium term (2-4 years) |

| Low patient & caregiver training rates | -0.7% | Global, with higher impact in rural and underserved areas | Medium term (2-4 years) |

| Pipeline of non-glucagon rescue biologics reducing addressable pool | -0.5% | North America & EU core, early adoption markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Pricing and Patchy Reimbursement Versus Insulin

Glucagon devices cost 15-20 times more than a single insulin vial, with Baqsimi’s cash price reaching USD 281, straining uninsured patients. Private payers often impose prior authorizations; 23% of US scripts encounter coverage gaps that delay pharmacy pickup. In low-income countries, the device price exceeds monthly healthcare budgets for middle-income households, curbing uptake. Reimbursement headwinds may intensify as insurers scrutinize spend on high-priced weight-loss therapies, prompting spill-over constraints on glucagon access.

API and Fill-Finish Supply Shortages

Peptide-hormone synthesis requires advanced facilities, and limited pre-filled syringe capacity led Novo Nordisk to halt GlucaGen HypoKit distribution, cutting global supply by double-digit percentages. Only a handful of sites can handle liquid-stable formulations, so any downtime cascades into worldwide back-orders. Geographic clustering of API plants adds geopolitical risk because trade disruptions can quickly choke output.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Formulation: Ready-to-Use Devices Redefine Emergency Response

Injectable kits accounted for 48.23% of glucagon market share in 2025, sustained by hospital familiarity and lower unit prices. Yet ready-to-use nasal powder leads growth at 6.55% CAGR, converting caregivers who value needle-free speed. Liquid-stable autoinjectors further accelerate uptake by eliminating the two-step mix process and halving training time. Collectively, these innovations enlarge the glucagon market size as non-medical responders gain confidence to carry the drug.

Development momentum favors formulations that extend beyond rescue use. Regulatory clearance for Baqsimi in 43 countries validated nasal delivery, while Phase 2 trials show long-acting analogs enabling weekly dosing in metabolic disorders ema.europa.eu. Radiology departments also integrate liquid vials to relax smooth muscle during imaging, opening niche volumes. Manufacturers that master stabilizing peptides at room temperature will command premium contracts across both emergency and chronic settings.

By Route of Administration: Intranasal Adoption Surges

Intramuscular injections held 66.12% of the glucagon market size in 2025 through entrenched clinical protocols, yet intranasal delivery is rising 6.78% annually on caregiver preference. Needle phobia and fear of dosing errors push families to pick sprays, especially for children. Pharmacokinetic data confirm plasma glucagon peaks within 10 minutes intranasally, matching injections without puncture risk.

Institutional buyers also pivot: US school districts report 89% staff preference for nasal kits, and workplace first-aid programs rapidly follow. Subcutaneous uses remain for diagnostic procedures that demand precise timing, but volume growth will center on nasal and autoinjector routes. Continued education plus broader reimbursement should tip mainstream protocols toward needle-free solutions by the end of the decade.

By End-User: Digital Pharmacies Propel Distribution

Hospitals and clinics generated 44.92% of 2025 revenue as prescribers dispensed kits during discharge and outpatient visits. Online pharmacies, however, post an 8.01% CAGR because telehealth consults integrate e-prescriptions and doorstep delivery. Automated refill reminders through digital platforms improve adherence and cut stock-out risk, especially for rural patients. Traditional retail chains maintain stable turnover due to walk-in convenience, while home-care uptake grows in tandem with CGM adoption that flags impending lows.

Digital channels represent a structural shift in the glucagon market because they reduce the friction of renewals and enable subscription bundles. Claims data show 34% higher on-time refills for patients using app-based pharmacies compared with brick-and-mortar stores. Manufacturers now negotiate directly with e-pharmacy operators for placement in diabetes-care bundles, bypassing wholesalers and securing real-time demand data.

By Indication: Metabolic Expansion Beyond Rescue

Severe hypoglycemia rescue sustained 81.92% of sales in 2025, anchoring the glucagon market. Yet adjunct obesity trials are climbing 7.12% annually as dual-agonist peptides such as survodutide deliver 14.9% weight loss in Phase 2 studies. Diagnostic imaging retains a specialized but steady niche where glucagon relaxes gastrointestinal muscle to sharpen visuals.

Therapeutic diversification repositions glucagon from a rarely used emergency tool to a chronic metabolic modulator. Investigators pairing glucagon receptor antagonists with SGLT2 inhibitors achieved 27% insulin-dose reductions in type 1 diabetes, highlighting synergy potential. As weight-management guidelines integrate glucagon-based agents, prescription volumes will increasingly reflect chronic, scheduled use rather than episodic rescues.

Geography Analysis

North America represented 38.41% of 2025 revenue owing to robust insurance mandates and mature emergency protocols that weave glucagon into diabetes self-management. FDA fast-track pathways aided rapid clearance of ready-to-use formats, and corporate wellness programs created recurring bulk purchases for on-site first-aid stations. The region’s growth now stems from optimizing distribution-especially online pharmacy channels-rather than dramatic user-base expansion.

Europe’s universal healthcare systems level cost barriers and create steady demand. BAQSIMI holds the top prescription rank across the bloc, and EMA continues approving new formulations such as Ogluo, illustrating regulatory enthusiasm for innovations that widen layperson access. Clinical guidelines across Germany, France and the Nordics oblige physicians to co-prescribe glucagon with intensive insulin, sustaining predictable volume. Eco-system integration with insulin pumps is also advancing through public health technology tenders.

Asia-Pacific logs the swiftest trajectory at 7.35% CAGR thanks to regulatory modernization, rapid diabetes prevalence growth and emergent obesity pharmacotherapy. Japan’s December 2024 approval of tirzepatide for weight loss signaled acceptance of broader hormonal interventions, opening labeling pathways for glucagon-centric agents. China’s pediatric trials showing 43.59% GLP-1 use in overweight cohorts point to rising acceptance of endocrine solutions beyond adult diabetes. India’s generic majors, preparing 15 GLP-1 products as patents lapse, will likely transfer pricing pressure to glucagon, expanding access but eroding margins.

Competitive Landscape

The glucagon market is moderately concentrated: three suppliers command roughly one third of global turnover, yet competitive intensity is climbing. Amphastar’s USD 1 billion acquisition of Baqsimi unified nasal formulations under a specialty-injectable leader, while Novo Nordisk’s exit from the reconstitution-kit segment reshaped share distribution. Xeris’s Gvoke attained 36% US retail share after deploying an extensive physician-education campaign and pharmacy stocking agreements that guarantee same-day availability.

Strategic alliances increasingly decide leadership. Xeris and Beta Bionics inked an exclusive pact to supply pump-compatible liquid glucagon, positioning both for first-mover advantage once dual-hormone systems clear regulators. Hanmi, Zealand and several generic houses pursue long-acting or small-volume analogs that attack obesity and fatty-liver indications, extending the competitive battlefield beyond emergency care.

Manufacturing prowess now differentiates winners because API syntheses and fill-finish lines remain constrained. Novo Nordisk and Eli Lilly each committed multi-billion-dollar US plant expansions to secure vertical control over injectables, while Amneal is building capacity in India to capture cost-sensitive export markets. Firms that assure uninterrupted supply will negotiate preferred-vendor status with large payers and technology partners, thereby reinforcing share gains.

Glucagon Industry Leaders

Amphastar Pharmaceuticals, Inc

Xeris Biopharma Holdings, Inc

Novo Nordisk A/S

Zealand Pharma A/S

Fresenius SE & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Novo Nordisk unveiled a USD 4.1 billion expansion of its North Carolina plant to boost injectable production, including glucagon lines

- December 2024: Eli Lilly committed USD 3 billion to expand injectable-drug output capacity for metabolic treatments that interact with glucagon signaling

- May 2024: Xeris Biopharma formed an exclusive partnership with Beta Bionics to co-develop pump-ready liquid glucagon for dual-hormone systems

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the glucagon market comprises every pharmaceutical-grade formulation, lyophilized rescue kits, liquid-stable autoinjectors, nasal powder sprays, and ready-to-use vials or prefilled syringes, indicated for severe hypoglycemia reversal or employed as a diagnostic adjunct in gastrointestinal imaging and metabolic research. The study measures revenue generated through hospitals, clinics, retail and online pharmacies, and home-care settings worldwide.

Scope exclusion: veterinary glucagon products and research-only peptide reagents are not covered.

Segmentation Overview

- By Formulation (Value)

- Injectable Kits (lyophilized)

- Liquid-stable Autoinjectors

- Nasal Powder

- Liquid-Stable Vials & Prefilled Syringes

- By Route of Administration (Value)

- Intramuscular

- Subcutaneous

- Intranasal

- By End-user (Value)

- Hospitals & Clinics

- Retail Pharmacies & Drug Stores

- Online Pharmacies

- Home-care Settings

- By Indication (Value)

- Severe Hypoglycemia Rescue

- Diagnostic Aid in Imaging

- Adjunct in Obesity / Metabolic Disease Trials

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted interviews with endocrinologists, diabetes nurse educators, hospital procurement managers, and pharmacy buyers across North America, Europe, and key Asian markets. These conversations validated kit utilization rates, channel mark-ups, and the accelerating shift toward nasal sprays, filling gaps left by desk research and guiding assumption ranges later used in modelling.

Desk Research

We first compiled public datasets that anchor demand, including IDF diabetes prevalence files, WHO essential medicine usage records, national hospital discharge abstracts, and customs shipment logs for HS code 3004.60 (hormone preparations). Supplemental insights were drawn from diabetes associations in the United States, Japan, and Germany, peer-reviewed journals tracking severe hypoglycemia incidence, and company 10-Ks that disclose unit sales of rescue kits. Our analysts then mined paid databases, D&B Hoovers for manufacturer financials and Dow Jones Factiva for product launch news, to cross-check volume and price assumptions.

Government price caps, reimbursement schedules, and patent expiry calendars were layered in to flag inflection points in average selling price. The listed sources illustrate our desk work; many additional references informed data collection, plausibility checks, and clarifications.

Market-Sizing & Forecasting

A top-down demand pool model started with treated Type 1 and insulin-using Type 2 diabetic counts, applied annual severe hypoglycemia incidence, and multiplied by verified rescue kit penetration rates; selective bottom-up cross-checks, supplier roll-ups and sampled ASP × volume, confirmed totals before adjustments. Key variables include: 1) prevalence of insulin-dependent diabetics, 2) emergency kit renewal frequency, 3) regulatory approvals for liquid-stable formulations, 4) reimbursement coverage ratios, and 5) regional channel mark-ups. Multivariate regression, supported by expert consensus on those drivers, underpins the 2025-2030 forecast, while any data gaps in bottom-up estimates were bridged through conservative interpolation from adjacent geographies.

Data Validation & Update Cycle

Outputs face variance tests against import values and hospital purchasing audits; anomalies trigger review by a second analyst layer. Reports refresh each year, and material events, such as a new intranasal approval, prompt interim updates. A final pre-publication pass ensures clients receive the latest view.

Why Mordor's Glucagon Market Baseline Commands Global Trust

Published estimates often differ; choice of formulations, channel coverage, and refresh cadence typically drive those gaps.

Key gap drivers include narrower scopes that omit nasal sprays, aggressive or outdated pricing curves, or models relying solely on diabetic headcounts without cross-checking real kit turnover. Mordor's disciplined scope selection, annual refresh, and dual-path validation reduce such variance.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 610.9 M (2025) | Mordor Intelligence | - |

| USD 297.8 M (2023) | Global Consultancy A | Excludes nasal and home-care channels; conservative ASP; older base year |

| USD 486.6 M (2020) | Industry Analyst Group B | Includes U.S. bias and partial device revenue; diabetic prevalence only driver |

| USD 621.3 M (2023) | Trade Journal C | Adds bulk peptide shipments to finished formulations; no channel mark-up adjustment |

The comparison shows that, by aligning scope with real clinical practice and validating prices against multi-channel audits, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can replicate and trust.

Key Questions Answered in the Report

What is the current size of the glucagon market?

The glucagon market generated USD 645.8 million in 2026 and is projected to reach USD 852.85 million by 2031, supported by a 5.72% CAGR.

Which formulation segment is expanding fastest?

Nasal powder glucagon is growing at a 6.55% CAGR because needle-free delivery shortens administration time and raises caregiver confidence.

Why is intranasal glucagon gaining adoption over intramuscular injections?

Intranasal sprays match injection bioavailability within 10 minutes, remove needle anxiety and simplify training for non-medical responders.

What geographic region offers the strongest growth opportunity?

Asia-Pacific leads at a 7.35% CAGR thanks to regulatory modernization, a rising diabetes population and expanding obesity-therapy pipelines.

How do dual-hormone artificial-pancreas systems affect demand?

Integration of pump-compatible liquid glucagon transforms the product from a rescue drug into a core component of automated glucose control, underpinning long-term volume expansion.

What years does this Glucagon Market cover, and what was the market size in 2025?

In 2025, the Glucagon Market size was estimated at USD 645.8 million. The report covers the Glucagon Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Glucagon Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: