Fume Hood Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

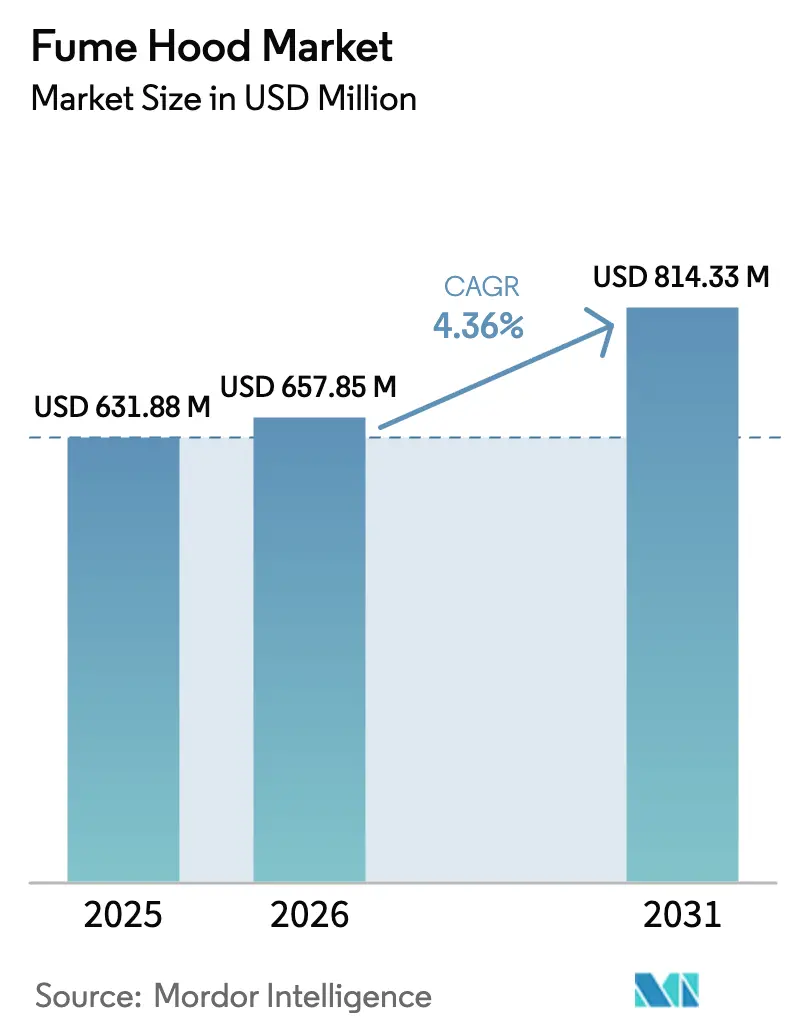

| Market Size (2026) | USD 657.85 Million |

| Market Size (2031) | USD 814.33 Million |

| Growth Rate (2026 - 2031) | 4.36% CAGR |

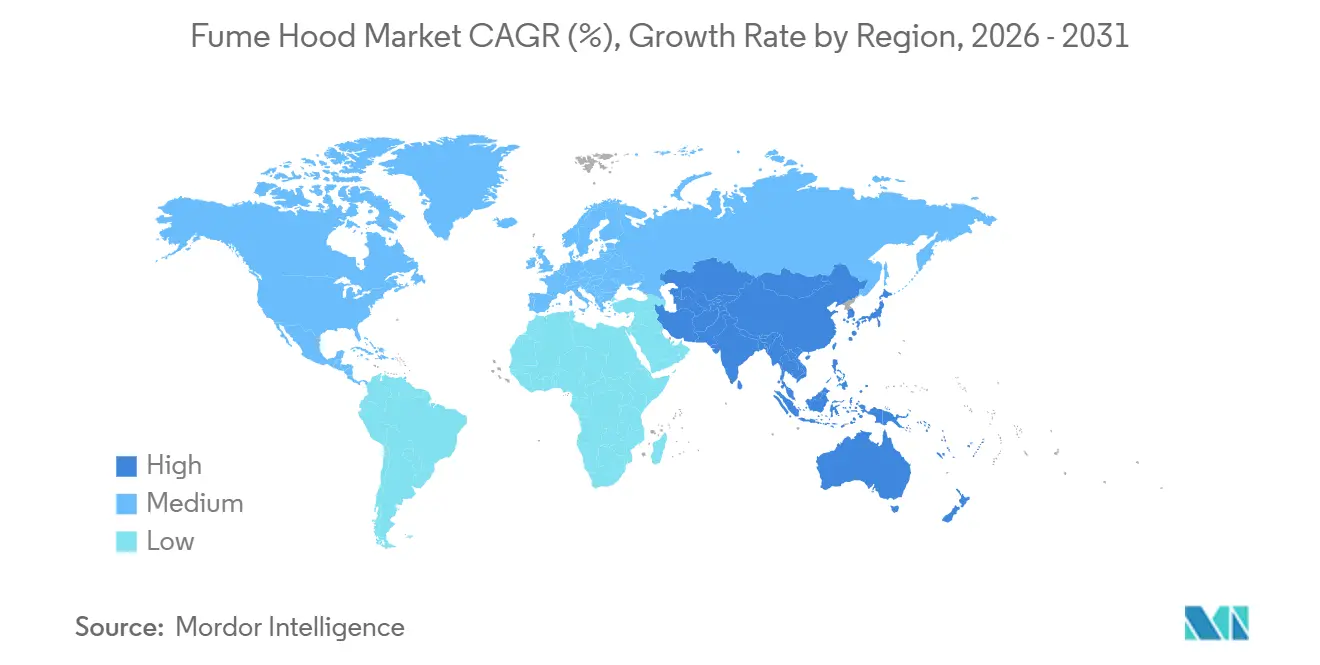

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fume Hood Market Analysis by Mordor Intelligence

The Fume Hood Market size is expected to grow from USD 631.88 million in 2025 to USD 657.85 million in 2026 and is forecast to reach USD 814.33 million by 2031 at 4.36% CAGR over 2026-2031.

Buyers now assign greater weight to lifetime energy and filter costs than to acquisition price, prompting vendors to emphasize variable-air-volume (VAV) designs and multi-stage filtration that lower operating expenses by 30-40% compared to legacy units. Pharmaceutical and biotechnology R&D budgets continue to anchor baseline demand. Yet, the fastest incremental growth arises from universities replacing outdated hoods with IoT-enabled models that satisfy both safety audits and campus-wide carbon-reduction mandates. Retrofit activity also benefits from building-code changes that cap permissible air changes per hour, effectively making older constant-air-volume hoods obsolete. On the supply side, specialty carbon and HEPA media constraints, though episodic, keep lead times volatile and favor manufacturers with vertically integrated filter production.

Key Report Takeaways

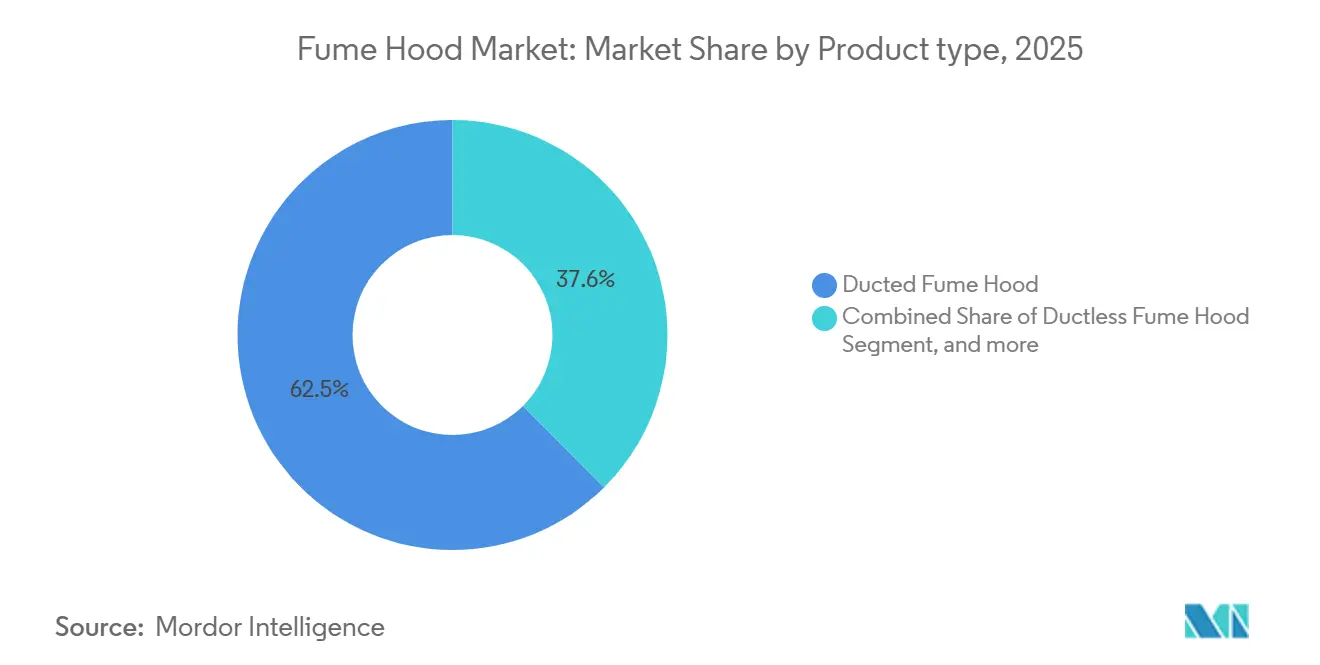

- By product type, ducted systems led with a 62.45% market share of the fume hood market in 2025, while ductless units are forecast to expand at a 6.65% CAGR through 2031.

- By mobility, bench-top configurations accounted for 66.43% of the Fume Hood market size in 2025; mobile/cart-mounted units are advancing at a 6.87% CAGR to 2031.

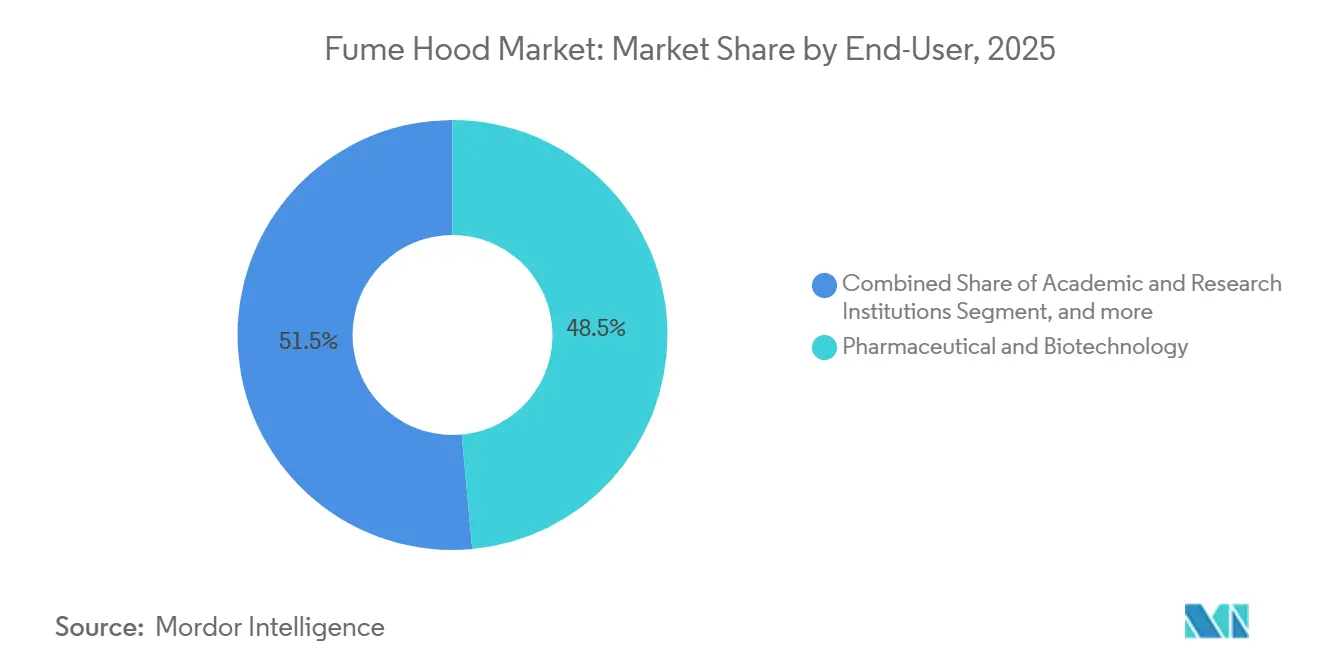

- By end-user, pharmaceutical and biotechnology labs captured 48.54% of the revenue in 2025, whereas academic and research institutions are projected to post the fastest growth of 7.65% CAGR through 2031.

- By material, stainless steel retained 41.34% share of the fume hood market size in 2025; polypropylene is rising at a 6.32% CAGR through 2031 on corrosive-chemistry demand.

- By geography, North America retained 42.34% share of the fume hood market size in 2025; Asia-Pacific is rising at a 5.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fume Hood Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Laboratory Safety Regulations | +0.9% | North America, Europe, spill-over to APAC | Medium term (2-4 years) |

| Expansion of Pharma & Biotech R&D Expenditure | +1.2% | Global hubs in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Energy-Efficiency Mandates Accelerating Retrofit Demand | +0.8% | North America, Europe, emerging in APAC | Short term (≤ 2 years) |

| Rapid Adoption of IoT-Enabled Smart Fume Hoods | +0.6% | Tier-1 cities across North America, Europe, APAC | Medium term (2-4 years) |

| Growing Demand from Emerging-Market Academic Labs | +0.5% | APAC core, Middle East, South America | Long term (≥ 4 years) |

| Rising Focus on Indoor Air Quality Certification in Green Buildings | +0.4% | North America, Europe, nascent in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Laboratory Safety Regulations

Global regulators now audit containment performance far more frequently. The U.S. Occupational Safety and Health Administration revised its Laboratory Standard in 2024, adopting quarterly face-velocity verification, which necessitates the early retirement of hoods that fail to meet the 80-120 feet-per-minute threshold[1]OSHA, “Laboratory Safety Guidance Update 2024,” osha.gov. In parallel, ANSI Z9.5 updates and Europe’s EN 14175 harmonization compel universities and pharmaceutical sites to budget for compliant replacements. The National Institutes of Health allocated USD 42.5 billion for FY 2025 infrastructure, earmarking 15% for environmental health and safety upgrades that include new fume hoods. Heightened litigation risk around occupational exposure now makes proactive hood replacement a board-level risk-mitigation measure. Collectively, these actions add 0.9 percentage points to the forecast CAGR.

Expansion of Pharma & Biotech R&D Expenditure

Life-science companies continue record capital outlays. Roche plans USD 50 billion in R&D for 2024-2026, allocating 8% to facility upgrades that include advanced containment. Novartis spent CHF 23 billion (approximately USD 26 billion) in 2024, prioritizing oncology suites that require HEPA-filtered, negative-pressure hoods. CBRE reported that North American lab space under construction reached 45 million square feet in Q4 2024, a 22% year-over-year surge, and most developers now specify energy-efficient hoods at the shell-and-core stage. Contract development and manufacturing organizations such as Catalent and Lonza likewise scale up, each requiring validated containment to secure FDA and EMA approvals. These investments increase long-run growth by 1.2 percentage points.

Energy-Efficiency Mandates Accelerating Retrofit Demand

Building codes are tightening fast. California’s Title 24 updates, effective 2025, require new labs to reduce HVAC energy use by 30% from 2019 baselines, which is achievable only with VAV fume hoods linked to occupancy sensors. The U.S. Department of Energy’s Better Buildings Lab Accelerator achieved electricity savings of 35-50% after VAV retrofits, often paying back in four years[2]U.S. Department of Energy, “Better Buildings Laboratory Accelerator Results,” energy.gov. Europe’s 2024 revision of the Energy Performance of Buildings Directive extends similar rules to renovations, creating a retrofit backlog across Germany, France, and the Nordics. Facility managers thus have both regulatory and financial incentives to replace constant-air-volume hoods promptly.

Rapid Adoption of IoT-Enabled Smart Fume Hoods

Smart containment converts static assets into data nodes. Kewaunee Scientific’s SmartFlow platform embeds sensors that report face velocity, sash position, and differential pressure in real-time, enabling predictive maintenance and up to 25% reduction in servicing costs. Siemens integrated similar telemetry into building-management systems in 2025, supporting campus-wide energy optimization for universities operating hundreds of hoods. Early adopters cite 15% energy savings from demand-controlled ventilation algorithms. With sustainability metrics now factoring into grant awards, especially in U.S. public universities, digital readiness of fume hoods becomes a funding prerequisite.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital and Operating Costs | -0.7% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Complex Multi-Standard Regulatory Compliance | -0.5% | Global, fragmented across jurisdictions | Medium term (2-4 years) |

| Emergence of Alternative Containment Technologies | -0.3% | North America, Europe | Long term (≥ 4 years) |

| Supply-Chain Volatility for Specialty Media | -0.4% | Global, episodic | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Operating Costs

A fully specified VAV ducted hood can cost USD 25,000 to install, while high-performance ductless units can start at around USD 18,000, which can squeeze budgets for small research labs. Annual energy outlays range from USD 3,500 to USD 5,000 for constant-air-volume models in North America, and ductless filter replacement averages USD 1,800, eroding operating funds. Indian universities, for example, face a 28% GST plus customs duties on imported hoods, which inflates prices by 40% over domestic but lower-spec options. These economic delays extend upgrade cycles, shaving 0.7 percentage points off growth.

Complex Multi-Standard Regulatory Compliance for Ductless Filters

Filter testing requirements diverge widely: the U.S. leans on OSHA self-certification, Europe mandates EN 14175-3 type tests, and France overlays AFNOR guidelines, forcing suppliers to maintain multiple SKUs and certification dossiers. Re-testing for new chemical classes, such as PFAS, adds cost and time to market. Smaller vendors struggle with this regulatory overhead, which limits product availability and dampens uptake by 0.5 percentage points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Retrofit Economics Propel Ductless Expansion

Ducted units dominated, accounting for 62.45% of 2025 revenue, reflecting entrenched installations in pharmaceutical QC labs where centralized exhaust is already in place. These customers value unlimited chemical throughput and straightforward regulatory audits. Yet ductless hoods are slated to outpace with a 6.65% CAGR through 2031. Modern multi-stage filters that meet ASHRAE 110 criteria have softened historical safety concerns, while avoiding ductwork can save USD 100,000 on a typical retrofit in 1950s-era university buildings. Accessories ranging from VAV controllers to IoT-ready sash sensors now account for a recurring aftermarket that suppliers bundle within service contracts.

Ductless adoption also benefits from application-specific niches, notably battery R&D and semiconductor wet benches where corrosive electrolytes or hydrofluoric acid would corrode stainless ductwork within years. Polypropylene cabinet construction and on-board filtration make these hoods plug-and-play, a feature prized by institutions operating within heritage architecture that restricts structural penetrations. As a result, the ductless portion of the Fume Hood market gains wallet share faster than headline unit volumes suggest, underpinning supplier gross-margin expansion.

By Mobility: Flexible Workflows Favor Portable Designs

Bench-top systems captured 66.43% of 2025 spending and remain the mainstay in fixed research suites that rarely reconfigure protocols. Their larger work surfaces and integration with casework make them irreplaceable in high-throughput analytical chemistry. The mobile/cart segment, however, is forecasted to grow at a 6.87% CAGR through 2031, driven by contract research organizations orchestrating multi-site clinical trials that require uniform containment across rented lab space. Battery-powered models introduced in 2024 further enhance portability by eliminating reliance on facility power outlets during short-term deployments.

Flexible lab layouts, including hot-desking for equipment, have gained traction in large pharmaceutical innovation centers and are being adopted by university incubators. Mobile hoods allow space planners to switch from organic synthesis one week to cell-culture prep the next without extensive HVAC rebalancing. The premium for mobility, typically 15-20% above bench-top equivalents, is offset by space-utilization gains that property managers now quantify in lease negotiations.

By End-User: Universities Post the Fastest Growth

Pharmaceutical and biotechnology firms held 48.54% of 2025 revenue, underpinned by strict containment standards and planned 15-year replacement cycles. Nonetheless, academic and government research institutions are projected to achieve a 7.65% CAGR to 2031, the fastest among end-users. U.S. federal stimulus under the CHIPS and Science Act and China’s Double First-Class University program channel billions into lab modernization, with fume hoods topping procurement lists because they confer immediate safety and energy wins. Partnerships where pharma outsources discovery work to universities further shift capital budgets toward academia.

Diagnostics laboratories and hospital pathology suites form the smallest slice yet sustain modest growth tied to healthcare infrastructure upgrades begun during the pandemic. They require compact hoods primarily for handling formalin and xylene, rather than broad-spectrum chemical containment, making them attractive targets for ductless suppliers that can pre-qualify filter matrices for typical reagent sets.

By Material: Corrosion Concerns Elevate Polypropylene

Stainless steel retained 41.34% of 2025 demand thanks to its longevity and compatibility with most disinfectants. However, polypropylene cabinets are expected to post a 6.32% CAGR on the back of battery and semiconductor research that involves corrosive chemistries intolerant of metal. Polypropylene also reduces weight, a significant advantage in mobile configurations where cart maneuverability is crucial. Mixed-material designs are emerging—stainless steel work surfaces paired with polypropylene side panels—to strike a balance between durability, corrosion resistance, and cost.

Powder-coated mild steel remains a budget option in cash-constrained public colleges, although its share is gradually being ceded to composite and fiberglass variants in ultra-corrosive environments. Material choice has thus become application-specific, a shift that suppliers accommodate through on-demand fabrication and the selection of modular bill-of-materials, enabled by digital twins.

Geography Analysis

North America commanded 42.34% of the 2025 global revenue, supported by OSHA and ANSI Z9.5 enforcement, deep pharmaceutical pipelines, and a vibrant life-science real estate sector that embeds high-efficiency hoods in spec builds. NIH infrastructure grants further bolster replacement cycles as universities race to meet quarterly velocity audits. Despite a maturing installed base, continued construction—45 million ft² in progress as of Q4 2024—keeps the regional Fume Hood market expanding, albeit below the global average.

The Asia-Pacific region is forecasted to be the fastest-growing territory, with a 5.43% CAGR through 2031, accounting for over one-third of the incremental units added worldwide. China’s self-sufficiency drive in pharmaceuticals and India’s biosimilar scale-up underwrite a wave of new laboratory construction. Government subsidies that cover 30% of energy-efficient equipment costs in Japan and South Korea also stimulate the replacement of constant-air-volume models with VAV hoods. Suppliers that pair local manufacturing with EN 14175 and ANSI certifications stand to outcompete import-only rivals.

Europe is experiencing slower top-line growth, constrained by a mature asset base and modest expansion of its R&D pipeline. Even so, the European Union’s 2024 revision of the Energy Performance of Buildings Directive has turned energy efficiency into a compliance requirement for renovations, catalyzing a retrofit market from Germany to the Nordics. Meanwhile, Middle Eastern research universities, such as KAUST and the UAE’s Masdar Institute, create beachheads for premium suppliers, although annual volumes remain relatively small. South America experiences episodic demand spikes linked to public university stimulus, but is hindered by currency volatility and import duties.

Competitive Landscape

Thermo Fisher Scientific, Esco Group, and Labconco collectively generated just over 45% of the global revenue in 2025, contributing to a moderate concentration in the Fume Hood market. Their competitive edge lies in global service footprints, bundled maintenance contracts, and the ability to provide end-to-end laboratory furniture suites that simplify vendor management for large R&D campuses. The integration of IoT telemetry into product lines has become a key differentiator. Esco’s 2025 alliance with Siemens enables facility-wide energy dashboards that competing mid-tier suppliers cannot yet match.

Challengers exploit regional footholds and niche offerings. Kewaunee Scientific’s battery-powered mobile hood targets clinical trial logistics, while Terra Universal’s modular CleanPro platform serves pop-up research centers that proliferated during pandemic response. Local manufacturers in India and Vietnam often undercut prices, prompting multinationals to open regional plants to avoid tariffs and shorten lead times, as evidenced by Esco’s 2024 Vietnam facility.

Regulatory expertise acts as a soft barrier to entry; maintaining parallel compliance tracks for OSHA, EN 14175, and country-specific addenda requires in-house testing chambers and seasoned documentation teams. Incumbents leverage this capability to fast-track customer validation, while smaller entrants often rely on white-label filters that may delay approvals. The rise of robotics as an alternative containment route has spurred incumbents to explore hybrid biological-chemical safety cabinets, such as NuAire’s FDA-cleared NU-540.

Fume Hood Industry Leaders

Flow Sciences, Inc.

ThermoFisher Scientific

NuAire

Hemco Corporation

Erlab

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Clean Air, one of the United Kingdom's leaders in fume management solutions, launched its Discovery fume cupboard at Lab Innovations. The product emphasizes safety, sustainability, and affordability, having been notably developed without the use of harmful SF₆ gas. It was designed and validated using advanced CFD modelling to ensure optimal fume containment.

- November 2024: The Franke Group has announced the successful acquisition of WESCO Group, a leading supplier of extractor hoods and ventilation systems in Switzerland and Germany. The transaction has received approval from the relevant competition authorities.

Global Fume Hood Market Report Scope

As per the scope of the report, a fume hood is a ventilator device built for performing hazardous experiments by drawing toxic air through ducts or filters.

The Fume Hood Market is Segmented by Product Type (Ducted Fume Hood, Ductless Fume Hood, and Accessories & Consumables), Mobility (Bench-Top and Mobile/Cart-Mounted), End-User (Pharmaceutical & Biotechnology, Academic & Research Institutions, and Healthcare & Diagnostics), Material (Stainless Steel, Polypropylene, Mild Steel & Powder-Coated Alloys, and Composite & Other Materials), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Ducted Fume Hood |

| Ductless Fume Hood |

| Accessories & Consumables |

| Bench-Top |

| Mobile / Cart-Mounted |

| Pharmaceutical & Biotechnology |

| Academic & Research Institutions |

| Healthcare & Diagnostics |

| Stainless Steel |

| Polypropylene |

| Mild Steel & Powders-Coated Alloys |

| Composite & Other Materials |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East And Africa | GCC |

| South Africa | |

| Rest Of Middle East And Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Product Type | Ducted Fume Hood | |

| Ductless Fume Hood | ||

| Accessories & Consumables | ||

| By Mobility | Bench-Top | |

| Mobile / Cart-Mounted | ||

| By End-User | Pharmaceutical & Biotechnology | |

| Academic & Research Institutions | ||

| Healthcare & Diagnostics | ||

| By Material | Stainless Steel | |

| Polypropylene | ||

| Mild Steel & Powders-Coated Alloys | ||

| Composite & Other Materials | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East And Africa | GCC | |

| South Africa | ||

| Rest Of Middle East And Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

How large is the Fume Hood market in 2026?

The Fume Hood market size is USD 657.85 million in 2026.

What CAGR is expected for global demand through 2031?

Demand is projected to advance at a 4.36% CAGR to 2031.

Which end-user segment will grow fastest?

Academic and research institutions are forecast to register a 7.65% CAGR through 2031 on the back of government stimulus.

Why are ductless hoods gaining popularity?

They cut retrofit costs by eliminating ductwork, achieve ASHRAE 110 containment with multi-stage filters, and now integrate IoT monitoring for predictive maintenance.

Which region will add the most incremental units?

Asia-Pacific, propelled by laboratory construction booms in China and India, is projected as the fastest-growing territory.

Who are the leading suppliers?

Thermo Fisher Scientific, Esco Group, and Labconco together account for just over 45% of global revenue, giving the market a moderate concentration profile.

Page last updated on: