Carrier Screening Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.76 Billion |

| Market Size (2031) | USD 6.56 Billion |

| Growth Rate (2026 - 2031) | 11.79% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

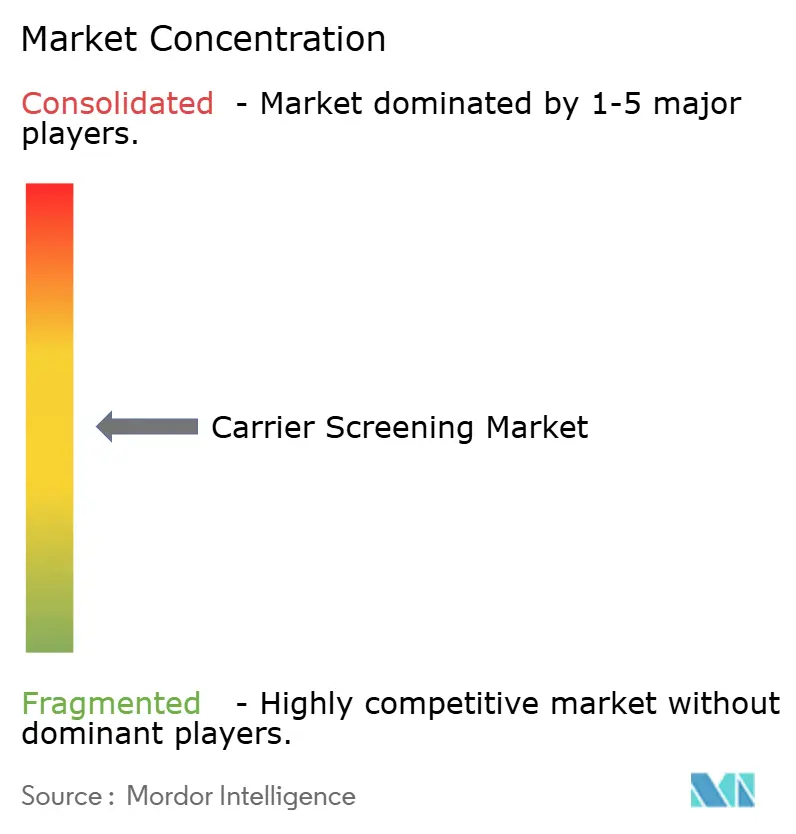

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Carrier Screening Market Analysis by Mordor Intelligence

The global carrier screening market size in 2026 is estimated at USD 3.76 billion, growing from 2025 value of USD 3.36 billion with 2031 projections showing USD 6.56 billion, growing at 11.79% CAGR over 2026-2031. Growth stems from falling next-generation sequencing prices, tightening but clearer Laboratory Developed Test rules, and deeper integration of genetic screening across fertility medicine. Providers now weave carrier testing into routine reproductive decision-making, while employer genetic-benefit programs, wider insurance coverage, and population pilots boost test volumes. Consolidation among reference laboratories accelerates scale advantages, and multi-gene panel uptake signals a shift from single-gene assays toward broad, cost-effective genomic screens. At the same time, shortages of trained genetic counselors and uneven reimbursement temper near-term expansion, pressing stakeholders to adopt tele-genetics and AI-supported result interpretation.

Key Report Takeaways

- By test type, molecular screening captured 62.74% revenue share in 2025; biochemical assays trail yet remain clinically relevant.

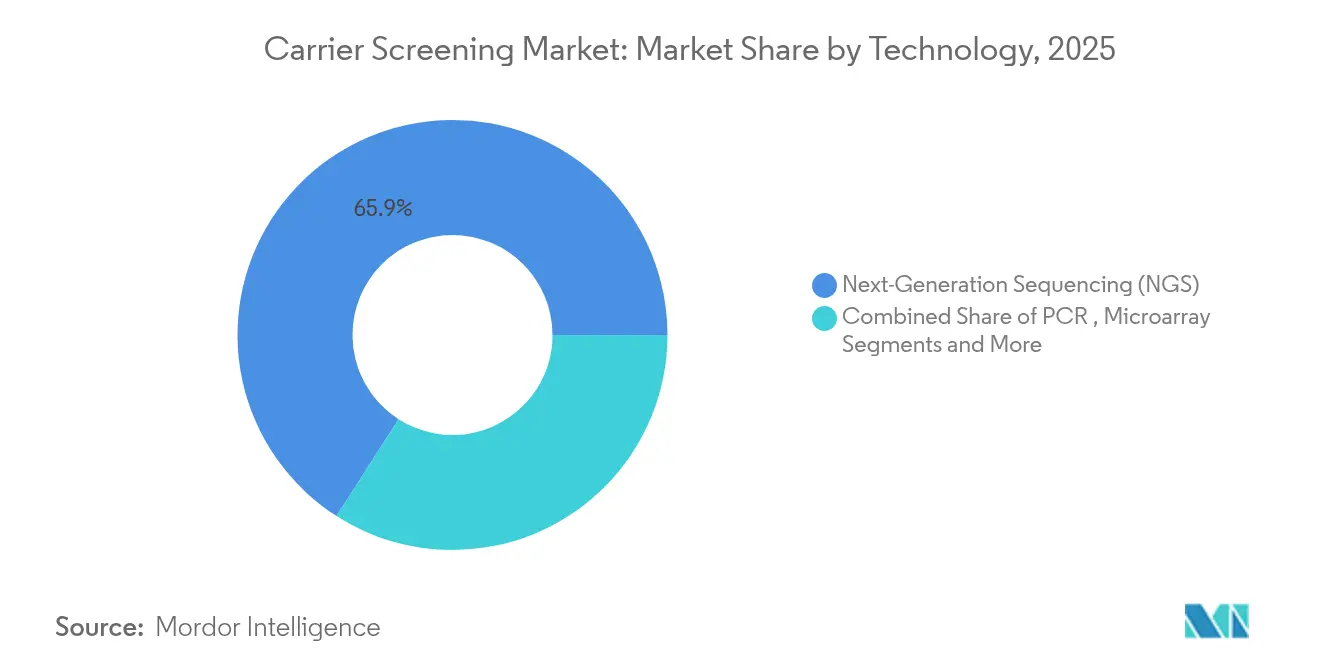

- By technology, next-generation sequencing led with 65.93% share in 2025 and is projected to advance at 14.98% CAGR to 2031.

- By disease, cystic fibrosis held 58.96% of the carrier screening market share in 2025, while spinal muscular atrophy posts the highest projected CAGR at 12.41% through 2031.

- By panel breadth, targeted single-gene tests claimed 46.12% of the carrier screening market size in 2025, but expanded multi-gene panels are set to expand at 13.95% CAGR.

- By end user, diagnostic laboratories accounted for 41.03% of the carrier screening market size in 2025 and are tracking 12.62% CAGR through 2031.

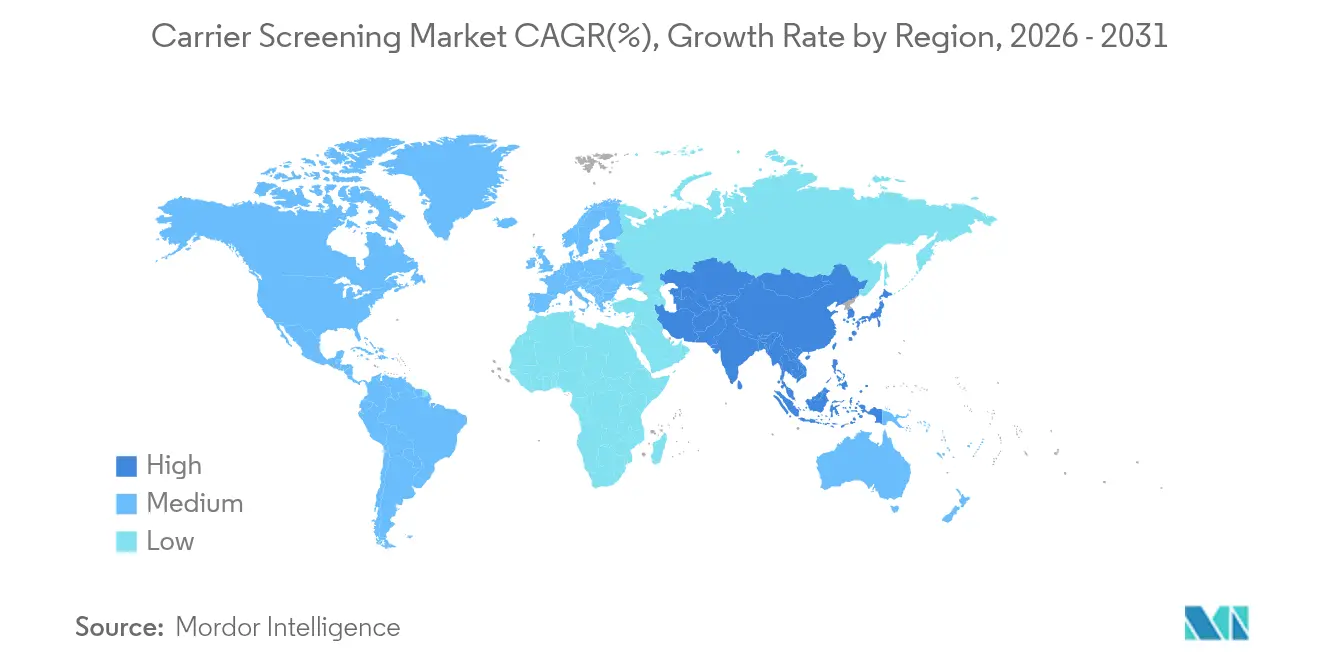

- By geography, North America dominated with 43.88% share in 2025; Asia-Pacific is the fastest-growing region with 13.32% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Carrier Screening Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing emphasis on early disease detection and prevention | +2.8% | North America and Europe with strong global spillover | Medium term (2-4 years) |

| Rising demand for personalized reproductive medicine | +2.1% | Developed markets worldwide | Long term (≥ 4 years) |

| Declining NGS costs enabling expanded panels | +3.2% | Fast uptake in Asia-Pacific with global relevance | Short term (≤ 2 years) |

| Integration of carrier screening in IVF and ART protocols | +1.9% | North America and Europe and emerging Asia-Pacific | Medium term (2-4 years) |

| Employer-sponsored genetic-benefit programs | +1.1% | Predominantly North America | Medium term (2-4 years) |

| Payer mandates tied to population pilots | +1.4% | North America and select European and Australian markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Emphasis on Early Disease Detection and Prevention

Payers and public-health agencies increasingly see comprehensive genomic screening as a cost-saving path rather than a discretionary service. Australia’s microsimulation of 569 recessive disorders predicted 2,067 affected births avoided at 50% test uptake, dwarfing outcomes from limited panels.[1]Tamar Nov-Klaiman, Ruth Horn & Aviad Raz, “More of the Same? Israel's Expanded Carrier Screening for Cystic Fibrosis,” Nature, nature.comLarge newborn initiatives in the United Kingdom and New York City covering 200,000 infants further spotlight the pivot toward preventive genomics.[2]Jocelyn Kaiser, “Sequencing Projects Will Screen 200,000 Newborns for Disease Genes,” Science, science.orgGeisinger’s MyCode program found clinically actionable results in 1 in 30 participants, most of whom were unaware of inherited risks. These demonstrations of clinical and fiscal value propel wider adoption of broad multi-gene carrier screening, cementing preventive genomics as routine care.

Rising Demand for Personalized Reproductive Medicine

Assisted reproduction now defaults to genetic scrutiny for both partners. Johns Hopkins Fertility Center recommends expanded panels covering more than 400 recessive conditions for every patient regardless of ancestry. Non-invasive embryo assays allow preimplantation genetic assessment without biopsy-related viability concerns, easing patient acceptance. Australia’s Medicare reimbursement for reproductive carrier screening underscores official endorsement of such proactive planning. Couples now desire genomic clarity before pregnancy, pushing clinics to embed carrier testing into routine fertility workflows and lifting test volumes within the carrier screening market.

Declining NGS Costs Enabling Expanded Panels

Whole-genome sequencing has fallen from USD 100 million in 2001 to just over USD 500 in 2023.[3]WIPO Global Health Unit, “Measuring Genome Sequencing Costs and Its Health Impact,” World Intellectual Property Organization, wipo.intIllumina’s USD 600 genome and Ultima’s USD 100 genome now make comprehensive multi-gene panels as affordable as legacy single-gene tests. The University of Minnesota processes 320 whole genomes weekly on the UG 100, expanding capacity for population pilots. Cheap sequencing lowers per-condition costs and incentivizes payers to reimburse broader panels, intensifying growth of the carrier screening market.

Integration of Carrier Screening in IVF and ART Protocols

Professional societies have broadened panel requirements; the American College of Medical Genetics now recommends testing 100 CFTR variants instead of 23. IVF centers embed screening into cycle planning to choose optimal gametes or embryos. Belgium’s BabyDetect pilot screened 165 disorders at birth with 90% parental acceptance, showing high receptivity to genomic data. The seamless alignment of genetic counseling, laboratory workflows, and reproductive decisions deepens clinical demand and fortifies the carrier screening market trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High costs and inconsistent reimbursement | −1.8% | Most acute in emerging nations | Short term (≤ 2 years) |

| Ethical and psychosocial concerns over incidental findings | −0.9% | Markets with established bioethics regulation | Long term (≥ 4 years) |

| Limited genetic-counseling workforce capacity | −1.4% | Global with rural concentration | Medium term (2-4 years) |

| Data-privacy regulations limiting secondary data use | −0.7% | Europe and North America and expanding Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Costs and Inconsistent Reimbursement

UnitedHealthcare explicitly excludes carrier tests from Medicare Advantage coverage, and limited CPT codes complicate claims for novel panels. Belgium recorded EUR 365 per newborn genomic test, well above conventional screens, challenging health-system budgets. Fragmented policies slow the spread of comprehensive screening in lower-income regions.

Limited Genetic-Counseling Workforce Capacity

Acceptance rates for genetic-counseling graduates fell to 30% by mid-2024, underscoring supply shortages. The US projects only 600 new counselors this decade, insufficient for soaring demand. Limited counseling delays result disclosure, prolongs care pathways, and could dampen the pace at which the carrier screening market scales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Dominance Drives Innovation

Molecular assays commanded 62.74% of 2025 revenue and are advancing at 12.98% CAGR, eclipsing biochemical methods in sensitivity and multiplexing scope. This dominance propels the carrier screening market as providers prefer direct variant detection over indirect metabolite proxies. The Comprehensive Analysis of Thalassemia Alleles protocol in southern China illustrates the efficacy of ultra-high-throughput sequencing where carrier prevalence exceeds 16%.

Biochemical screens still matter for enzyme or protein conditions and blend well with genomic assays in newborn programs such as Belgium’s BabyDetect. Economic analyses confirm tandem mass spectrometry’s value in certain metabolic scenarios, ensuring that diversified testing menus persist alongside molecular expansion.

By Disease Type: Cystic Fibrosis Leadership Amid SMA Surge

Cystic fibrosis retained 58.96% share in 2025 thanks to universal guidelines and payer familiarity, securing a large slice of the carrier screening market share. Expanded 100-variant CFTR panels raise detection rates in multiethnic populations.

Spinal muscular atrophy, projected at 12.41% CAGR, benefits from transformative therapies and inclusion in most newborn panels. Ancestry-driven programs for Tay-Sachs, Gaucher, and sickle cell disease continue, while rare autosomal recessive conditions gain traction as sequencing costs fall.

By Panel Type: Expansion Beyond Targeted Approaches

Targeted single-gene panels still held 46.12% of the carrier screening market size in 2025, yet expanded multi-gene panels are scaling at 13.95% CAGR on the back of sub-USD 200 genome economics. LabCorp’s Inheritest product suite exemplifies broad panels that streamline risk stratification across heterogeneous ancestry groups.

Ethnicity-specific panels persist where founder mutations dominate, but the march toward universal expanded screening is clear. Thailand’s exome-wide carrier survey found pathogenic variants in 34% of individuals, proving comprehensive panels expose clinically actionable risks otherwise unrecognized.

By Technology: NGS Acceleration Transforms Market Dynamics

Next-generation sequencing contributed 65.93% of revenue in 2025 and is growing fastest at 14.98% CAGR as system throughput soars. Illumina’s NovaSeq X processes 64 genomes per flow cell, while its 5-base chemistry merges genomic and epigenomic reads for richer insights.

Polymerase chain reaction retains value for rapid confirmatory testing, and microarrays continue for structural variation analysis. Third-generation platforms shine in repeat-rich or structurally complex loci; China’s application in thalassemia underscores future hybrid approaches.

By End User: Laboratory Consolidation Reshapes Service Delivery

Diagnostic labs comprise 41.03% of the carrier screening market size with 12.62% growth projected, aided by M&A that pools bioinformatics, wet-lab, and counseling assets. LabCorp’s USD 239 million Invitae purchase and subsequent alliance with Ultima Genomics typify a push toward population-scale sequencing services.

Hospitals and clinics increasingly bring carrier screening in-house, bolstered by guidelines from health systems such as Penn Medicine. IVF centers and physician offices remain pivotal in preconception workflows, while academic consortia like Virginia’s PrIMeD demonstrate research-driven community outreach. Tele-genetics vendors offer scalable counseling, alleviating workforce constraints and broadening the carrier screening market reach.

Geography Analysis

North America secured 43.88% revenue in 2025 on the strength of employer genetic benefits, robust counseling networks, and an FDA framework that balances oversight with innovation. Geisinger’s MyCode enrollment surpassed 175,000 individuals, evidencing appetite for population genomics. South Carolina’s In Our DNA initiative recruited 50,000 participants toward a 100,000 goal, reinforcing state-level momentum.

Asia-Pacific exhibits the strongest growth at 13.32% CAGR. China’s iHope project assisted 513 rare-disease families by mid-2024 and targets 1,800 by 2026, while national thalassemia screening addresses carrier rates up to 24% in southern provinces. Australia’s Medicare-funded panels set a regional precedent for reimbursement.

Europe records balanced expansion. The UK aims to sequence 100,000 newborn genomes, while Belgium’s 90% parental acceptance rates for genomic newborn screening prove public trust. Israel’s Ministry of Health funds a 650-variant program comprising 290 genes, underlining governmental support for broad panels.

Regulatory Landscape

Carrier screening is regulated through a mix of rules covering assay systems and laboratory quality requirements that shape how tests are validated and delivered. In the United States, autosomal recessive carrier screening gene mutation detection systems are regulated by the FDA under 21 CFR 866.5940 as Class II devices with special controls, which sets expectations around analytical performance, labeling, and use in CLIA-regulated laboratory settings.

In other regions, regulators and accreditation bodies are tightening standardization around genomic service delivery and NGS testing quality. In November 2025, European Accreditation published EA-4/24 G to harmonize assessment of NGS-based genetic testing laboratories, and the Singapore Accreditation Council issued MED 002 (5 November 2025) for clinical labs performing genetic and genomic testing. In the Middle East, the Dubai Health Authority issued Standards for Genomic Services effective 28 February 2026, aligning genomic services with ISO 15189 and CAP/CLIA frameworks and increasing compliance emphasis across end-to-end genomic workflows, from consent and reporting to laboratory operations.

Value Chain Analysis

The carrier screening value chain starts with upstream instrument and assay inputs, including sequencing systems and reagents and consumables supplied by companies such as Illumina, Thermo Fisher Scientific, Roche, QIAGEN, Bio-Rad, Danaher, Agilent, and Oxford Nanopore. These inputs support assay design and validation, bioinformatics pipeline configuration, and quality management aligned with medical laboratory accreditation (commonly ISO 15189) and country-specific requirements.

Midstream, diagnostic laboratories and reference labs operate as the execution hub, receiving samples from hospitals, physician offices, and IVF centers and running high-throughput workflows that combine wet-lab processing with variant interpretation and clinical reporting. Sample access and logistics are key differentiators because carrier screening is often centralized, requiring reliable collection networks and temperature-controlled transport. Reported turnaround times vary by provider, for example 10 to 21 days for Labcorp and about 15 business days for Centogene. Downstream, results are delivered to ordering clinicians and patients alongside genetic counseling support (in-person or tele-genetics), with growing integration into EMR and LIS systems to streamline ordering, consent documentation, and follow-up pathways.

Competitive Landscape

The carrier screening market is moderately consolidated. LabCorp’s asset acquisition and Natera’s USD 52.5 million reproductive portfolio purchase reconfigure competitive hierarchies. Quest Diagnostics added digital pathology through PathAI to bolster AI analytics amid pathologist shortages. Myriad Genetics secured a foundational patent for molecular residual disease assays, reinforcing its IP moat.

Technology differentiation thrives. Illumina readies spatial transcriptomics and combinatorial multiomic workflows, and Roche earned FDA Breakthrough status for an Lp(a) assay targeting hereditary cardiovascular risk, showcasing a pivot to integrated risk profiling. AI-powered variant interpretation tools aim to counter counseling bottlenecks and expedite result delivery.

White-space opportunities include employer benefits, low-and-middle income population pilots, and AI tele-counseling platforms. As payer mandates expand and sequencing costs decline, integrated firms able to couple laboratory throughput with digital counseling and analytics hold competitive advantage within the carrier screening market.

Carrier Screening Industry Leaders

Illumina Inc.

Thermo Fisher Scientific Inc.

Abbott Laboratories

F.Hoffmann-La Roche Ltd

Danaher Corporation (Cepheid)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The biggest whitespace in carrier screening sits at the intersection of standardized universal screening models and scalable service delivery. Clinical direction has shifted toward more consistent pan-ethnic approaches, including ACMG guidance on universal tiered screening models, but there is still no unified industry standard for expanded panel gene content. That gap leaves room for laboratories and kit providers to align panel design, variant classification, and reporting language to widely referenced clinical criteria. Quality frameworks are also tightening, including EA-4/24 G in Europe and national accreditation technical notes such as Singapore SAC MED 002, which increases demand for validated workflows, auditable bioinformatics, and interoperable reporting.

National and population-scale programs add further commercial pathways for vendors able to provide turnkey digital delivery, counseling, and registry-ready data handling. Australia has published work through Australian Genomics on expanding reproductive genetic carrier screening toward a national screening program model, including centralized and integrated online service delivery and registry systems, which benefits providers with patient-facing platforms and robust consent, privacy, and follow-up infrastructure. At the provider-network level, partnerships that embed carrier screening inside IVF workflows also expand access in underpenetrated geographies, including collaborations with large IVF networks and Middle East laboratory expansions that bring localized testing capacity closer to care pathways.

Recent Industry Developments

- July 2026: Centogene acquired ownership of Pearl Medical Analysis Laboratory in Abu Dhabi to expand access to genetic testing services, including carrier screening, prenatal diagnostics, and preimplantation genetic testing. The move adds in-region laboratory capacity and supports faster sample-to-result workflows for providers serving the Middle East.

- September 2025: Pacific Biosciences entered the high-throughput carrier screening market by expanding its PureTarget offering into formats designed for higher sample volumes (including 24- and 96-sample kits). This broadened the set of sequencing and enrichment options available to laboratories scaling expanded carrier screening panels.

- October 2024: Myriad Genetics and JScreen announced a strategic partnership focused on expanding access to preventive genetic testing and carrier screening in higher-risk communities. The collaboration strengthens community-based outreach and funnels testing demand into clinical workflows that include education and appropriate follow-up.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the revenue generated from carrier screening tests that identify whether an individual carries gene variants linked to inherited disorders, mainly used before conception or in early pregnancy. The scope includes screening delivered through clinical laboratories and test-kit revenue when bundled with the screening offering.

Scope exclusions: research-only genetic screening, newborn metabolic screening panels, and direct-to-consumer ancestry testing are excluded from this sizing.

Segmentation Overview

- By Test Type

- Molecular Screening Tests

- Biochemical Screening Tests

- By Disease Type

- Cystic Fibrosis

- Tay-Sachs Disease

- Gaucher Disease

- Sickle Cell Disease

- Spinal Muscular Atrophy

- Other Autosomal Recessive Disorders

- By Panel Type

- Targeted Single-Gene Panels

- Ethnicity-Specific Panels

- Expanded Multi-Gene Panels

- By Technology

- Next-Generation Sequencing (NGS)

- Polymerase Chain Reaction (PCR)

- Microarrays

- Others

- By End-User

- Hospitals & Clinics

- Diagnostic Laboratories

- Physician Offices & IVF Centers

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by grounding the demand pool and testing cadence in public, repeatable sources, before any commercial assumptions are added. We typically reference sources such as CDC reproductive health and genetics pages, NIH and NLM resources (including PubMed summaries), FDA safety communications and test-related updates, and OECD health indicators for cross-country comparability.

To keep the revenue model realistic, we also review payer and coverage signals from public CMS references, plus peer-reviewed utilization studies that report ordering patterns for preconception and prenatal testing. Company filings, earnings call transcripts, investor decks, and reputable press help validate pricing direction, service mix, and where volume is shifting (for example, toward expanded panels). For company financials and broader news coverage, we also use select paid subscriptions without relying on them as the only source of truth. These desk sources are illustrative, and many other public references were used for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary inputs are used to confirm what is actually being ordered and paid for, and to pressure-test assumptions that cannot be cleanly read from public data alone. We covered views from clinical laboratory leadership, test developers, genetic counselors, and hospital and clinic stakeholders across APAC, EMEA, and the Americas, then aligned those inputs to one set of pricing and volume rules.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | APAC: 51% |

| Mid tier: 41% | Functional/Unit leaders: 41% | EMEA: 29% |

| Smaller Players: 22% | Managers: 45% | Americas: 20% |

Market-Sizing & Forecasting

Market totals are built using top-down logic that reconstructs the addressable testing pool from reproductive health activity and genetics utilization, and then converts that pool into revenue using pricing and mix assumptions. In practice, we start with indicators such as annual births and pregnancies, share of pregnancies receiving prenatal care, carrier screening adoption rates by care pathway (preconception versus prenatal), the split between targeted and expanded panels, and typical re-test patterns when a partner screen is triggered.

Once the demand base is formed, average selling price is applied using a ladder that separates test type, panel breadth, and care setting, and then adjusts for expected price compression and reimbursement shifts over time. Results are corroborated with selective bottom-up approximations, such as sampled provider volume checks, lab capacity and throughput discussions, and channel feedback on average order values, so totals can be corrected when the first pass appears too high or too low. For forecasting, scenario analysis is used around a central case because policy changes, guideline updates, and payer behavior can shift adoption faster than a single trend line would suggest.

Data Validation & Update Cycle

Validation is done by triangulating the modeled revenue against independent signals, such as test utilization trends reported in medical literature, broad healthcare spending context, and qualitative checks from providers and laboratories. Any sharp jumps are reviewed for real-world triggers, such as a guideline change, expanded panel uptake, or reimbursement tightening, and then the assumptions are reworked and rechecked.

Before sign-off, outputs go through multiple analyst reviews, with variance checks across regions and with prior-year estimates, followed by re-contact if a key input looks inconsistent. Reports are refreshed annually, and interim updates are done when material events occur that can move volumes or pricing. Right before delivery, an analyst performs a fresh pass so clients receive the most current version of the numbers and assumptions.

Mordor Intelligence's Carrier Screening Market Size Compared Against Other Published Estimates

Published market sizes for carrier screening can look far apart because the underlying count of tests, the price logic, and the included revenue components are not always aligned. In this category, differences often come from whether kit revenue and lab services are both included, how expanded panels are treated versus targeted tests, and how quickly pricing is assumed to decline as volume scales.

Some publishers start from broad genetic testing totals and then allocate a share to carrier screening, while others lean heavily on faster growth assumptions without documenting what changes in utilization or reimbursement drive the step-up. The spread also comes from currency timing and which year is treated as the anchor, plus whether clinical-only testing is separated from adjacent offerings. Some estimates fold in adjacent areas like newborn screening or ancestry-related consumer tests, and Mordor Intelligence counts only clinical carrier screening used for reproductive planning in preconception and early pregnancy.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.76 B (2026) | |

| Trade Publisher A | USD 2.72 B (2024) | Uses an earlier anchor year and a different growth window, which can understate later adoption effects that show up as expanded panel ordering increases. The write-up is less explicit on separating clinical carrier screening from newborn screening and consumer ancestry-related testing, which can shift what gets counted. |

| Industry Publisher B | USD 1.70 B (2025) | The inclusions are not clearly broken out between laboratory services and test-kit revenues, so totals can land lower if only one side of the value chain is captured. A longer horizon and a lower stated CAGR also implies slower uptake of expanded panels than many providers plan for in the near term. |

Taken together, the table shows that year selection and what gets counted in the revenue stack do most of the work behind the gap. By tying volumes to pregnancies and care pathways, then applying a clear price and mix structure that can be checked in interviews, we keep the final number traceable and easier to reproduce.

Key Questions Answered in the Report

What is the current value of the carrier screening market?

The carrier screening market is valued at USD 3.76 billion in 2026 and is forecast to reach USD 6.56 billion by 2031 at an 11.79% CAGR.

Which technology drives the fastest growth within the carrier screening market?

Next-generation sequencing holds 65.93% revenue share and is expanding at 14.98% CAGR, making it the market’s primary growth driver.

Why are expanded multi-gene panels gaining momentum?

Sequencing costs have fallen below USD 600 per genome, allowing laboratories to offer comprehensive panels that detect hundreds of conditions at prices comparable to legacy single-gene tests.

How does the shortage of genetic counselors affect market growth?

Limited counselor availability lengthens result-turnaround times and may slow adoption in regions without tele-genetic solutions, creating operational bottlenecks.

Which region is growing fastest and why?

Asia-Pacific is pacing the market with 13.32% CAGR as China, Australia, and Japan fund large-scale screening programs and clarify laboratory-test regulations.

What are the main reimbursement challenges?

Coverage varies widely; some US Medicare Advantage plans exclude carrier testing, and limited CPT codes complicate billing, deterring labs from rolling out new panels in certain markets.

Page last updated on: