Full-Body Scanner Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

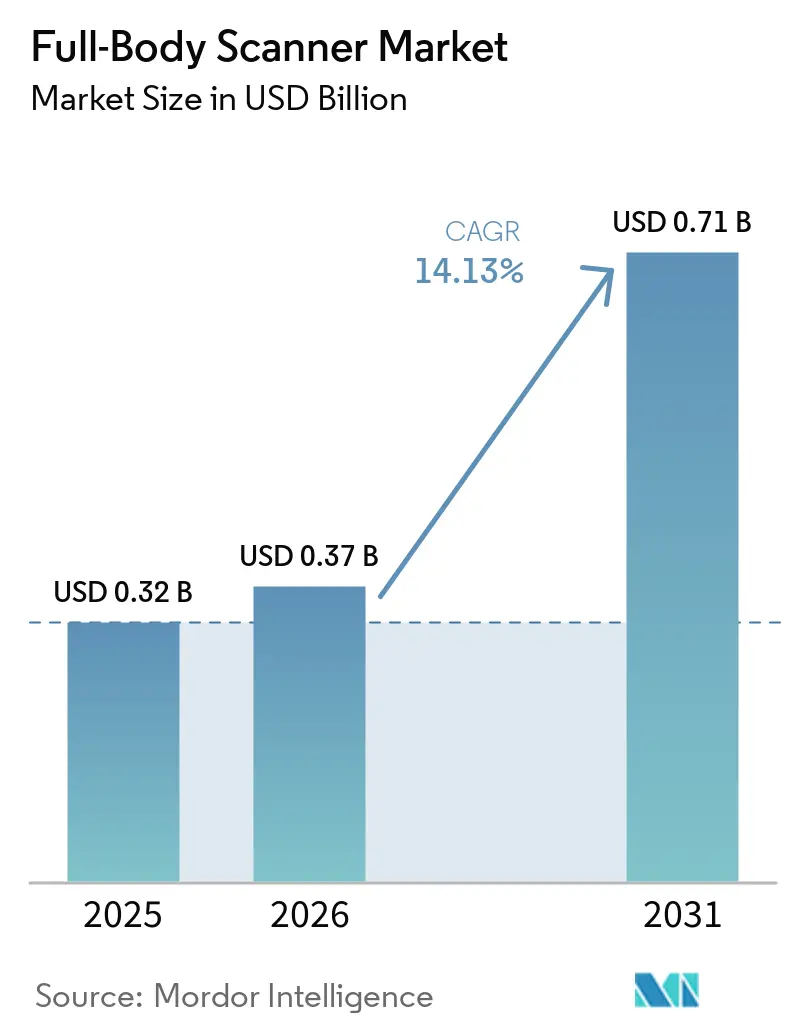

| Market Size (2026) | USD 0.37 Billion |

| Market Size (2031) | USD 0.71 Billion |

| Growth Rate (2026 - 2031) | 14.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Full-Body Scanner Market Analysis by Mordor Intelligence

The full-body scanner market size is expected to increase from USD 0.32 billion in 2025 to USD 0.37 billion in 2026 and reach USD 0.71 billion by 2031, growing at a CAGR of 14.13% over 2026-2031. Rapid recovery in global passenger traffic, rising adoption of millimeter-wave and terahertz imaging, and escalating security mandates are sustaining high equipment-refresh rates across aviation and non-aviation checkpoints. Funding pipelines already earmarked by border agencies and airport operators are anchoring procurement visibility, while software-centric upgrades are enlarging recurring-revenue pools for service vendors. Export-control tensions and privacy litigation remain structural headwinds, yet their drag is outweighed by throughput-driven replacement cycles and the need to detect non-metallic threats that legacy metal detectors routinely miss. As a result, the full-body scanner market continues to exhibit double-digit expansion opportunities across both mature and greenfield geographies.

Key Report Takeaways

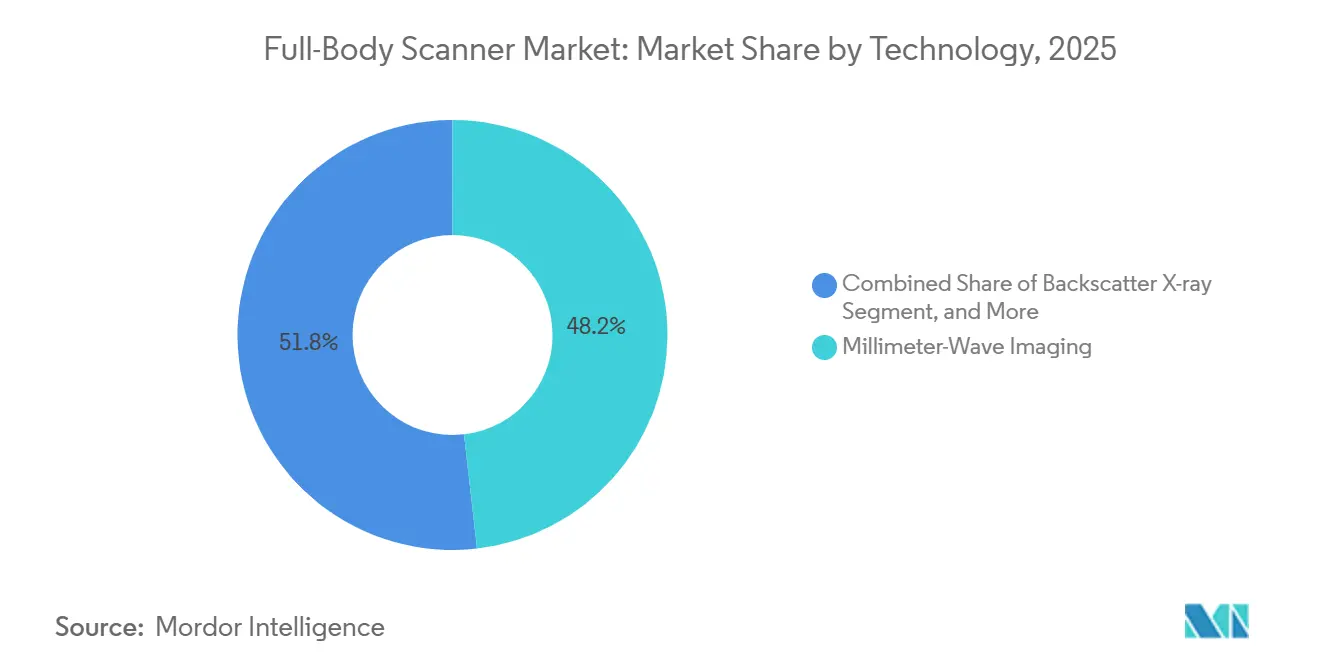

- By technology, millimeter-wave imaging led with 48.18% of the full-body scanner market share in 2025; terahertz imaging is projected to expand at a 14.78% CAGR through 2031.

- By application, airport security checkpoints accounted for 57.52% of the market revenue share in 2025, while public venues and events are forecast to grow at a 14.59% CAGR through 2031.

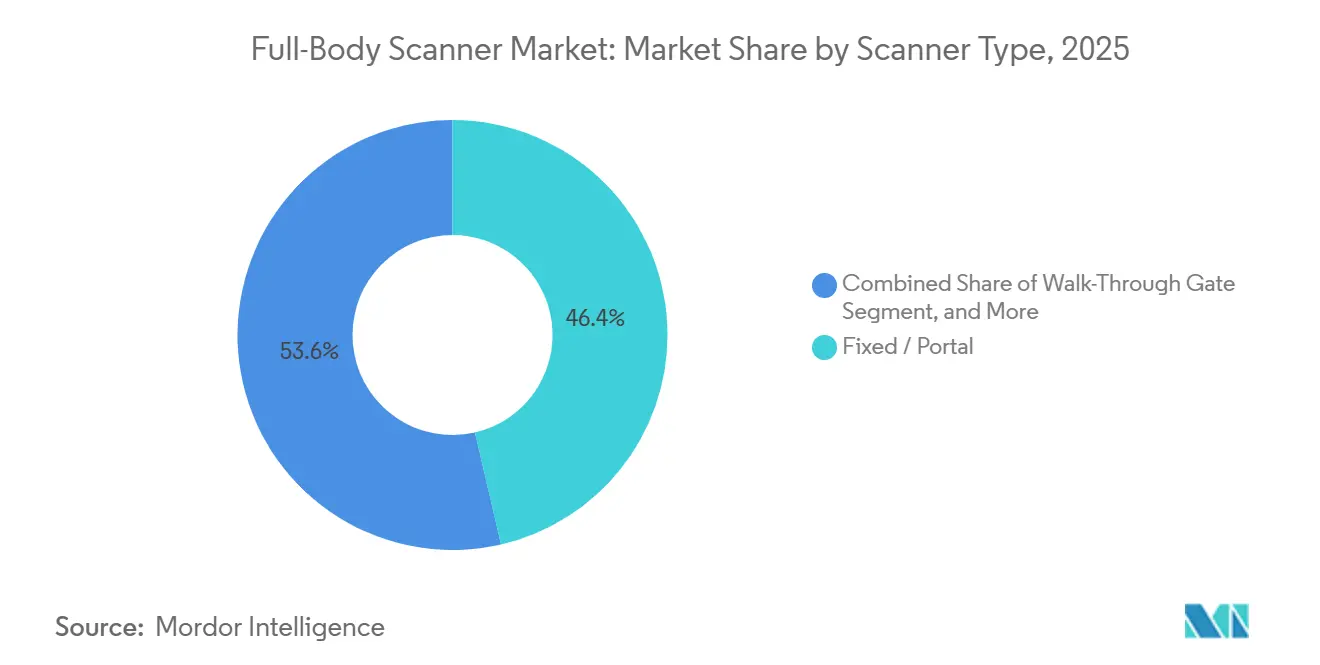

- By scanner type, fixed portal scanners accounted for 46.38% of the market revenue share in 2025, whereas portable rapid-deploy units are advancing at a 14.98% CAGR through 2031.

- By component, hardware accounted for 54.73% of the full-body scanner market in 2025, and software and analytics are poised to grow at a 14.65% CAGR between 2026 and 2031.

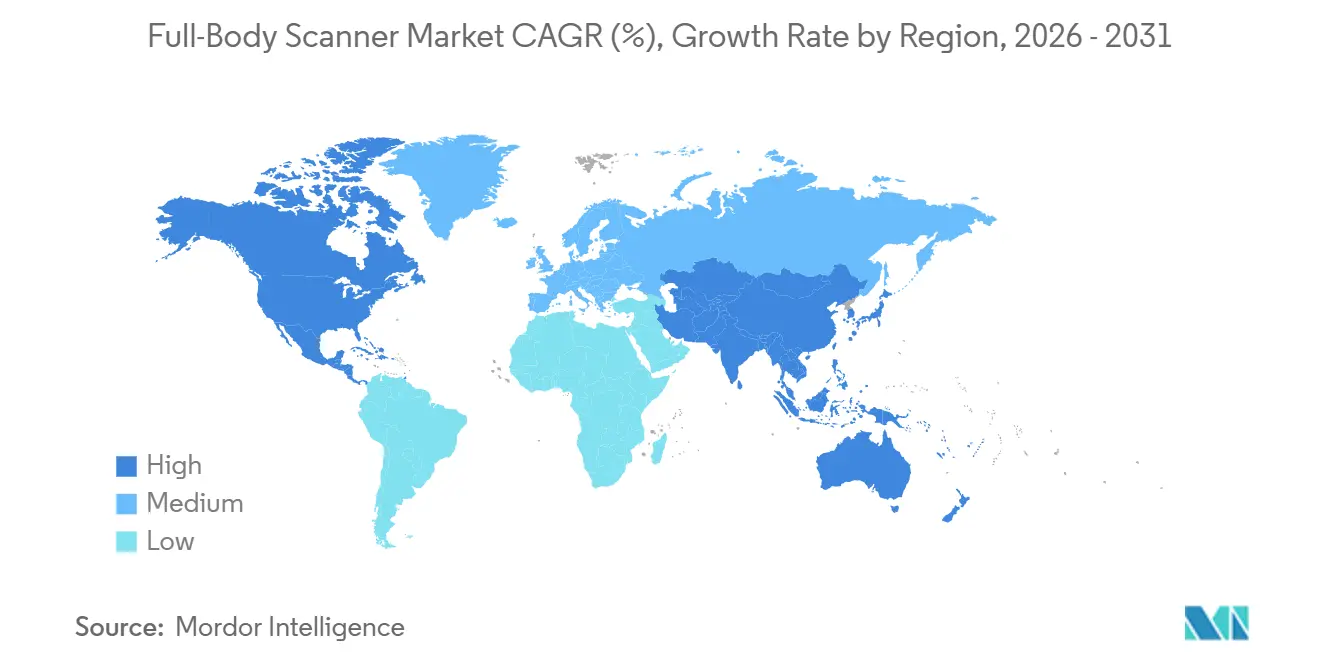

- By geography, North America commanded 37.49% share of the full-body scanner market in 2025, while Asia-Pacific is set to register the fastest 14.71% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Full-Body Scanner Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aviation Passenger-Volume Rebound | +3.2% | Global, led by North America and the Asia-Pacific | Short term (≤ 2 years) |

| Tightening Global Anti-Terrorism Regulations | +2.8% | Global, strongest in Europe and the Middle East | Medium term (2-4 years) |

| Rapid Decline in Millimeter-Wave Cost Curve | +2.1% | Asia-Pacific core, spill-over to the Middle East and Africa | Medium term (2-4 years) |

| Digital Twin-Enabled Checkpoint Optimization | +1.9% | North America and Europe, early adoption in the Asia-Pacific | Long term (≥ 4 years) |

| Rise of Pop-Up Event Security Contracts | +1.7% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Emerging Cargo-Plus-People Hybrid Screening | +1.4% | North America and Europe border crossings | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aviation Passenger-Volume Rebound

Single-day throughput at US checkpoints reached 3.13 million travelers in November 2025, surpassing pre-pandemic peaks and validating multi-year capital allocations for advanced imaging equipment.[1]Transportation Security Administration, “Monday Holiday Travel Numbers,” tsa.gov Brisbane Airport’s eight-lane computed-tomography checkpoint, inaugurated in December 2025, doubled screening capacity and trimmed wait times by 30%, underscoring airlines’ preference for high-throughput lanes during long-haul bank periods.[2]Brisbane Airport Corporation, “New CT Lanes Double Capacity,” bne.com.au South Korea’s Incheon International Airport introduced a fully automated remote baggage-screening link with the US Customs and Border Protection in August 2025, shortening passenger connections by up to 20 minutes and showcasing cross-border collaboration made possible by next-generation scanners.[3]U.S. Customs and Border Protection, “Low-Energy Portal X-Ray Expansion,” cbp.gov Similar surge-demand dynamics will arise around the FIFA World Cup 2026, where pre-placed contracts for millimeter-wave portals at host-city airports highlight the full-body scanner market’s event-driven upside. Across the Asia-Pacific, immigration agencies are pursuing upgrades to e-gates and body scanners in tandem, signaling convergent growth in people- and baggage-screening infrastructure.

Tightening Global Anti-Terrorism Regulations

India’s Bureau of Civil Aviation Security now obliges airports handling ≥ 10 million annual passengers to install full-body scanners, catalyzing live trials of 70-80 GHz portals at Delhi Indira Gandhi International Airport that can process 1,200 scans per hour. Australia mandated the adoption of computed tomography at primary gateways by mid-2026, prompting nationwide retrofits that hardwire advanced imaging into domestic security codes. In the United States, Section 44925 of Title 49 codifies advanced imaging as the preferred primary screening modality, reinforcing the Transportation Security Administration’s multi-billion-dollar fleet-refresh roadmap. Europe’s Civil Aviation Conference continues to tighten Standard 3.1 image-quality benchmarks, pushing operators to retire legacy backscatter units in favor of millimeter-wave portals certified to the latest specification. Collectively, these statutes lock in a compliance-driven replacement wave that shields volumes against cyclical capex fluctuations.

Rapid Decline in Millimeter-Wave Scanner Cost Curve

The global installed base of millimeter-wave portals surpassed 2,000 units by January 2026, driving scale efficiencies that lowered average selling prices to below USD 170,000 and widened the addressable market among mid-tier airports. Semiconductor advances are further compressing bill-of-materials costs, while terahertz prototypes have achieved sub-millimeter resolution at 220 GHz, paving the way for sub-USD 100,000 handheld systems by 2028. Correctional facilities such as Jackson County, Michigan, justified capital outlays for scanners once pricing fell under USD 180,000, demonstrating cost-curve elasticity in non-aviation verticals. Contract awards for trace-detection add-ons that leverage quartz-crystal microbalance sensors illustrate how hardware de-pricing coincides with the upsell of high-margin ancillary modules. These price trajectories collectively expand the full-body scanner market’s total addressable install base over the medium term.

Digital Twin-Enabled Checkpoint Optimization

Dublin Airport applied discrete-event simulation to model queue dynamics and recommended deploying Rapiscan 620XR, thereby reducing the risk of under-capacity or stranded capital outlays. A 2025 Journal of Air Transport Management study at Paris Charles de Gaulle Airport trimmed wait times by 12% through digital-twin-guided lane allocation, validating virtual prototyping as a capex-light lever for checkpoint efficiency. ICAO frameworks now encourage airports to feed real-time sensor data from body scanners into predictive-maintenance engines that minimize downtime, an imperative underscored by more than 400,000 inoperable hours logged on US border scanners in 2025.[4]International Civil Aviation Organization, “Digital Twin for Airport Resilience,” icao.int Map-based indoor-positioning overlays are being stitched into digital twins to simulate passenger flow under dynamic flight banks, helping operators stress-test scanner throughput before construction. As software licensing becomes the vehicle for delivering these insights, digital twins reshape the value proposition from gear-centric procurement to analytics-as-a-service.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy and Data-Protection Litigation Risk | -1.6% | North America and Europe | Medium term (2-4 years) |

| High Capital Expenditure for Mid-Tier Airports | -1.3% | Asia-Pacific, Middle East, Africa, South America | Short term (≤ 2 years) |

| Cyber-Vulnerabilities in Connected Scanners | -0.9% | Global, heightened in North America and Europe | Long term (≥ 4 years) |

| Export-Control Restrictions on Dual-Use Tech | -0.8% | Europe, Asia-Pacific, Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Privacy and Data-Protection Litigation Risk

The 2025 Muir v. Department of Homeland Security filing alleges disproportionate false positives among passengers with disabilities, potentially forcing recalibration protocols that lengthen certification lead-times. A parallel settlement obliges the Transportation Security Administration to publish quarterly deletion-compliance reports, adding administrative overhead to fleet operations. Europe’s General Data Protection Regulation pushes airports toward explicit-consent workflows, diverging from US opt-out norms and complicating multinational equipment rollouts. The Privacy and Civil Liberties Oversight Board now recommends six-month algorithm-bias audits for biometric integrations, elevating ongoing compliance costs for vendors. As airports weigh litigation exposure against throughput gains, procurement cycles risk elongation, tempering near-term momentum in the full-body scanner market.

High Capital Expenditure for Mid-Tier Airports

Walk-through metal detectors still cost barely USD 10,000, while millimeter-wave portals average USD 170,000, a ratio that mid-tier gateways processing < 1 million passengers struggle to absorb in the absence of a subsidy or mandate. Site-readiness work, ranging from floor reinforcement to HVAC retrofits, adds incremental costs that can eclipse the cost of the scanner itself, as evidenced by 43 US border systems worth USD 96 million sitting idle in storage during 2025 due to infrastructure delays. India’s security code exempts smaller airports from the full-body-scanner requirement, reinforcing a two-tier security architecture that slows the growth of passenger volumes in regional hubs. Maintenance backlogs, leading to 166 systems being inoperative for extended periods, underscore the long-term burden on operating budgets, especially when technician pools are thin. These economics compel smaller operators to defer adoption, shaving topline potential from the full-body scanner market in the short term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Terahertz Imaging Accelerates Beyond Benchmark Modalities

Millimeter-wave imaging accounted for 48.18% of revenue in 2025, anchored by certifications from the Transportation Security Administration and the European Civil Aviation Conference. Terahertz systems, however, are on track for a 14.78% CAGR, buoyed by sub-millimeter resolution breakthroughs at 220 GHz that enable video-rate concealed-object detection without motion controllers. The full-body scanner market size for millimeter-wave portals is expanding steadily, yet terahertz’s ability to detect non-metallic contraband positions it for rapid share gains once certification paths mature. In applied trials, prototype handheld terahertz devices weighing under 5 kg expanded effective aperture by over 50 times, pointing to field-ready deployments in border patrol scenarios where portability dictates form-factor choices. Backscatter X-ray platforms remain confined to specialty use cases, such as drive-by vehicle inspection, while dual-energy transmission scanners are gaining traction in cargo applications.

Artificial-intelligence fusion that pairs computed tomography with threat-detection algorithms further differentiates high-resolution terahertz modalities. Certification remains the gating item; millimeter-wave incumbents enjoy entrenched compliance status, and terahertz vendors must navigate multi-year testing cycles before aviation adoption crystallizes. Second-order effects reinforce terahertz ascendance. Semiconductor advances are eroding unit cost, and the larger silicon photonics ecosystem is migrating know-how from 5G millimeter-wave components into security imaging. Major primes such as Smiths Detection are integrating DICOS 3.0-compliant interfaces that allow remote analysis of high-capacity data streams, a prerequisite for terahertz imagery. These intersecting technology arcs hint at a plateau for millimeter-wave share before the end of the decade and a gradual pivot toward hybrid deployments that mix mature portals with targeted terahertz add-ons.

By Application: Event-Driven Demand Diversifies Revenue Mix

Airport checkpoints accounted for 57.52% of revenue in 2025, underscoring their role as the centerpiece of the full-body scanner market. Yet public venues and events are projected to log a 14.59% CAGR as stadiums migrate away from walk-through metal detectors to high-throughput weapons-detection lanes. The full-body scanner market size for sports and entertainment facilities is expanding on the back of contract wins for mobile trailers fitted with millimeter-wave portals capable of screening crowds at 2,500 people per hour. High-profile rollouts at the FIFA Club World Cup 2025, SoFi Stadium, and Rugby World Cup proved that pop-up deployments could blend security with fan-experience imperatives.

Secondary use cases deepen diversification. Correctional facilities now procure portals to interdict narcotics and improvised weapons, while land-border agencies integrate low-energy X-ray portals that rotate between vehicle and pedestrian inspection modes. Corporate campuses are piloting scanners during elevated threat windows or executive events, leasing units for days or weeks rather than purchasing outright. Such variability in contract length invites outcome-based pricing, where vendors charge per scan or per day, thereby smoothing utilization across a traditionally lumpy aviation-centric order book.

By Scanner Type: Portability Reshapes Procurement Logic

Fixed portals retained 46.38% revenue in 2025 because certification frameworks continue to favor standardized walk-through lanes at large airports. Still, portable units are set for a 14.98% CAGR as trailer-mounted and handheld devices open greenfield demand in border security, events, and commercial real estate. Contracts for 2,000-plus QPS201 fixed portals across global hubs illustrate sustained baseline demand, yet every marquee sports event since 2023 has featured rapid-deploy trailers that can be craned in and out within hours. Thruvision’s walk-through thermal systems, supplied under a USD 0.6 million airport worker-screening order in March 2026, demonstrate cost-effective penetration into secondary gateways where permanent infrastructure is impractical.

Portability also mitigates regulatory risk. Operators can relocate mobile units as threat landscapes shift, a strategic hedge against under-utilization that fixed portals cannot offer. Border agencies in the US and Europe increasingly favor mixed fleets that include drive-through X-ray systems on the road network and trailer-mounted millimeter-wave scanners for pedestrian crossings. Handheld terahertz devices in the prototype phase promise to extend mobility to last-mile interdiction points, further fragmenting the fixed-portal monopoly.

By Component: Software and Analytics Capture Expanding Wallet Share

Hardware still accounted for 54.73% of revenue in 2025, but the software and analytics lines are forecast to grow at a 14.65% CAGR as value migrates toward algorithm updates, remote diagnostics, and predictive maintenance. Remote screening platforms, such as the International Remote Baggage Screening System at Incheon Airport, illustrate how software unlocks cross-border operational efficiencies. The full-body scanner market share attributed to software-centric revenue will grow as agencies sign multi-year service contracts; one US airport service deal for 486 scanners outstripped prior hardware orders in total dollar value.

Predictive-maintenance modules already monitor scan counts, motor vibration, and image-quality drift in real time, allowing field teams to intervene before devices fail. At land borders, maintenance backlogs valued at nearly USD 100 million have led to idle assets, catalyzing demand for analytics to safeguard uptime. Vendors are shifting to subscription tiers that bundle algorithm refreshes with cybersecurity patches, positioning software as a perpetual revenue annuity layered onto a slowly depreciating hardware base.

Geography Analysis

North America accounted for 37.49% of revenue in 2025, thanks to the Transportation Security Administration’s USD 220.6 million capital plan to refresh 1,065 advanced imaging units. Incremental demand now pivots to mega-events such as the FIFA World Cup 2026, where QPS201 portals will address surge throughput. Border agencies complement aviation demand, such as low-energy X-ray portals, which are rolling out at southern crossings under a program exceeding USD 200 million, reflecting a broader homeland-security budget that spans people and cargo. Canada is phasing out Chinese-origin scanners from future tenders, aligning supply chains with allied vendors, while Mexico’s multi-year Rapiscan backlog illustrates sustained replacement momentum even in emerging-market fiscal environments.

Asia-Pacific is on track for a 14.71% CAGR, driven by greenfield airport construction, regulatory mandates, and tech-forward screening pilots. South Korea’s remote baggage screening link with US authorities compresses minimum connection windows and positions Incheon as a template for trans-Pacific transfers. Australia’s mid-2026 computed-tomography deadline is accelerating equipment rollouts in Brisbane, Sydney, and Melbourne. India’s mandate for full-body scanners at Tier-1 airports triggers trials at Delhi and will cascade to Bengaluru and Hyderabad as passenger counts climb. Japan is gearing up for Expo 2025 Osaka via phased CT installations at Fukuoka and other airports, aligning with its 60-million-visitor target by 2030. China’s digital-twin crowd-management rollouts reveal how data-layer integration can amplify scanner throughput, a model under evaluation in Singapore and Hong Kong.

Europe follows close behind, buoyed by London Heathrow’s GBP 1 billion (USD 1.35 billion) CT upgrade and Dubai’s 100-scanner order that cements the Gulf Cooperation Council’s leadership within the extended European travel corridor. Export-control scrutiny on Chinese equipment, illustrated by Poland’s removal of Nuctech portals, is redirecting tenders toward domestic European or allied US vendors. Middle Eastern hubs, especially Dubai and Riyadh, are scaling up CT lanes in anticipation of tourism diversification goals. South America and Africa remain nascent but show green shoots. Brazil’s biometric e-gate deployments in 2025-2026 lay the foundation for advanced imaging to be layered on later. Overall, geographic diversification cushions the full-body scanner market against any single-region budget shock.

Competitive Landscape

Industry concentration is moderate. OSI Systems Rapiscan, Smiths Detection, and Leidos collectively hold a near-60% share through entrenched contracts with the Transportation Security Administration and US Customs and Border Protection. Life-cycle service awards, such as Leidos’ potential USD 2.63 billion maintenance pact, illustrate how incumbents leverage installed base to secure annuity revenue well beyond the initial sale. Private equity’s USD 2.2 billion acquisition bid for Smiths Detection demonstrates capital-market confidence in the sector’s resilience.

Challenger firms are capturing whitespace. Evolv Technologies surpassed 8,000 global deployments across stadiums and arenas by 2025, demonstrating that differentiated pedestrian-flow form factors can circumvent aviation certification barriers. Thruvision’s lightweight thermal portals gained traction at secondary US airports and corporate campuses, supported by worker-screening contracts valued at under USD 1 million. Micro-X is advancing self-screening kiosks under a US Department of Homeland Security contract valued at up to USD 14.1 million, signaling the government's appetite for passenger-led workflows.

Technology roadmaps are converging on software differentiation. Leidos’ alliance with Quadridox embeds XRDI algorithms into its 3DX CT line, reducing false positives and operator workload. Smiths Detection’s rollout of DICOS-compliant SDX 10080 SCT scanners positions the firm for data-sharing mandates that accompany remote-screening models. Export-control friction around Chinese vendors is fragmenting market share in Europe and North America, funneling incremental demand toward allied suppliers such as Rohde and Schwarz and Dimark-Anglosec. Cyber-hardening credentials and algorithm-audit transparency are emerging as critical bid-score criteria, recalibrating competitive dynamics away from price-only evaluations.

Full-Body Scanner Industry Leaders

OSI Systems, Inc. (Rapiscan Systems)

Smiths Detection Group Ltd.

Leidos Security Detection & Automation, Inc.

Nuctech Company Limited

Rohde & Schwarz GmbH & Co KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Thruvision won a USD 0.6 million contract from Greater Orlando Aviation Authority for five 81-Series walk-through systems, expanding its US airport presence to five sites.

- January 2026: The Transportation Security Administration placed a multi-million-dollar order with Rohde and Schwarz for QPS201 portals at FIFA World Cup 2026 host-city airports.

- January 2026: MS Tech secured a contract to install DUOSCAN trace detectors at Adani Navi Mumbai International Airport, designed for 90 million passengers annually.

- January 2026: Smiths Detection finalized the deployment of the International Remote Baggage Screening System at Incheon Airport Terminal 2, enabling remote US screening of checked baggage.

Global Full-Body Scanner Market Report Scope

The Full-Body Scanner Market encompasses advanced security screening devices designed to detect concealed objects, weapons, or threats on and within a person's body without physical contact or the need to remove clothing. These scanners primarily use technologies such as millimeter-wave, backscatter X-ray, and transmission X-ray to generate detailed 3D images, enabling rapid identification of metallic and non-metallic contraband in high-security environments such as airports, border checkpoints, correctional facilities, and public venues.

The Full-Body Scanner Market Report is Segmented by Technology (Millimeter-Wave Imaging, Backscatter X-Ray, Terahertz Imaging, Dual-Energy Transmission, and Emerging AI-Fusion Methods), Application (Airport Security Checkpoints, Land and Sea Border Crossings, Correctional and Detention Facilities, Corporate and Critical Infrastructure, and Public Venues and Events), Scanner Type (Fixed/Portal, Walk-Through Gate, and Portable/Rapid-Deploy), Component (Hardware, Software and Analytics, and Maintenance and Integration Services), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Millimeter-Wave Imaging |

| Backscatter X-ray |

| Terahertz Imaging |

| Dual-Energy Transmission |

| Emerging AI-Fusion Methods |

| Airport Security Checkpoints |

| Land and Sea Border Crossings |

| Correctional and Detention Facilities |

| Corporate and Critical Infrastructure |

| Public Venues and Events |

| Fixed / Portal |

| Walk-Through Gate |

| Portable / Rapid-Deploy |

| Hardware |

| Software and Analytics |

| Maintenance and Integration Services |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Millimeter-Wave Imaging | |

| Backscatter X-ray | ||

| Terahertz Imaging | ||

| Dual-Energy Transmission | ||

| Emerging AI-Fusion Methods | ||

| By Application | Airport Security Checkpoints | |

| Land and Sea Border Crossings | ||

| Correctional and Detention Facilities | ||

| Corporate and Critical Infrastructure | ||

| Public Venues and Events | ||

| By Scanner Type | Fixed / Portal | |

| Walk-Through Gate | ||

| Portable / Rapid-Deploy | ||

| By Component | Hardware | |

| Software and Analytics | ||

| Maintenance and Integration Services | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the full-body scanner market today and where is it headed by 2031?

It totaled USD 0.37 billion in 2026 and is projected to reach USD 0.71 billion by 2031, reflecting a 14.13% CAGR as per Mordor Intelligence.

Which imaging technology is advancing fastest?

Terahertz imaging is expected to grow at 14.78% CAGR through 2031 on the back of sub-millimeter resolution breakthroughs as per Mordor Intelligence.

Why are public-venue operators adopting body scanners?

High-throughput, portable systems cut queue times during sports and entertainment events, meeting safety goals without disrupting visitor experience.

What is driving Asia-Pacific demand?

Government mandates, greenfield airport projects, and automated remote-screening pilots are together producing a 14.71% CAGR for the region as per Mordor Intelligence.

How are vendors monetizing beyond hardware sales?

Recurring software licenses for remote screening, predictive maintenance, and algorithm updates now form a growing share of revenue, backed by multi-year service contracts.

What privacy issues should executives watch?

Litigation over image retention and algorithmic bias is prompting quarterly deletion audits and six-month bias reviews, adding compliance costs and lengthening procurement cycles.

Page last updated on: