Body Area Network Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

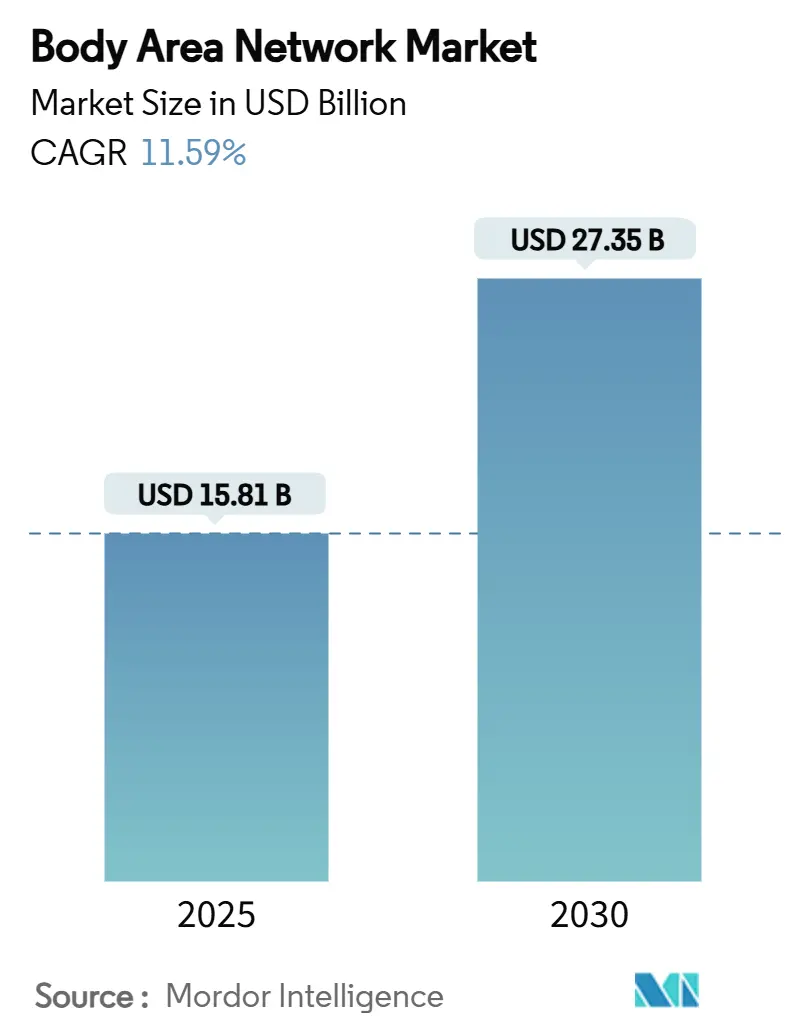

| Market Size (2025) | USD 15.81 Billion |

| Market Size (2030) | USD 27.35 Billion |

| Growth Rate (2025 - 2030) | 11.59% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Middle East and Africa |

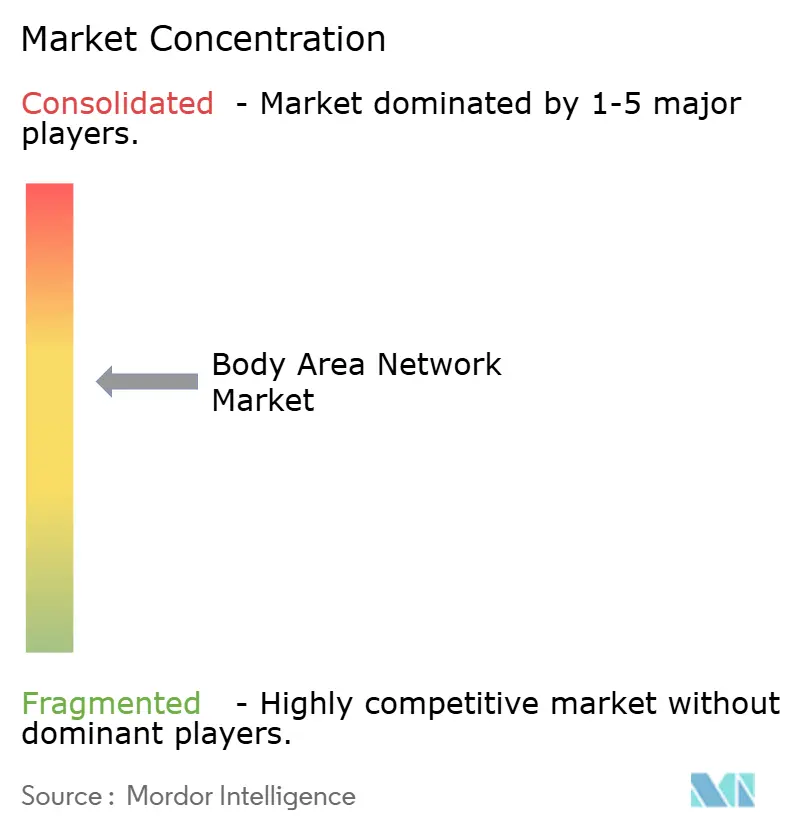

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Body Area Network Market Analysis by Mordor Intelligence

The body area network market size stands at USD 15.81 billion in 2025 and is forecast to reach USD 27.35 billion by 2030, reflecting an 11.59% CAGR that illustrates how connected sensors, edge analytics, and cloud platforms are becoming core to precision care. Expedited U.S. regulatory approvals, broader Medicare reimbursement for remote patient monitoring, and accelerating 5G rollouts have combined to move the body area network market from pilot projects to enterprise-scale deployments. Continuous glucose monitors, leadless pacemakers, and cardiac inserts approved by the FDA in 2024 alone demonstrate clinical validation of the technology. Semiconductor miniaturization has cut sensor cost curves, while AI-enabled software transforms raw biosignals into actionable care plans. Investment momentum is equally strong in consumer health, entertainment, and military safety programs, giving companies multiple demand vectors. Heightened cybersecurity requirements, battery limitations, and interoperability gaps temper growth but also foster innovation in on-device processing and energy harvesting.

Key Report Takeaways

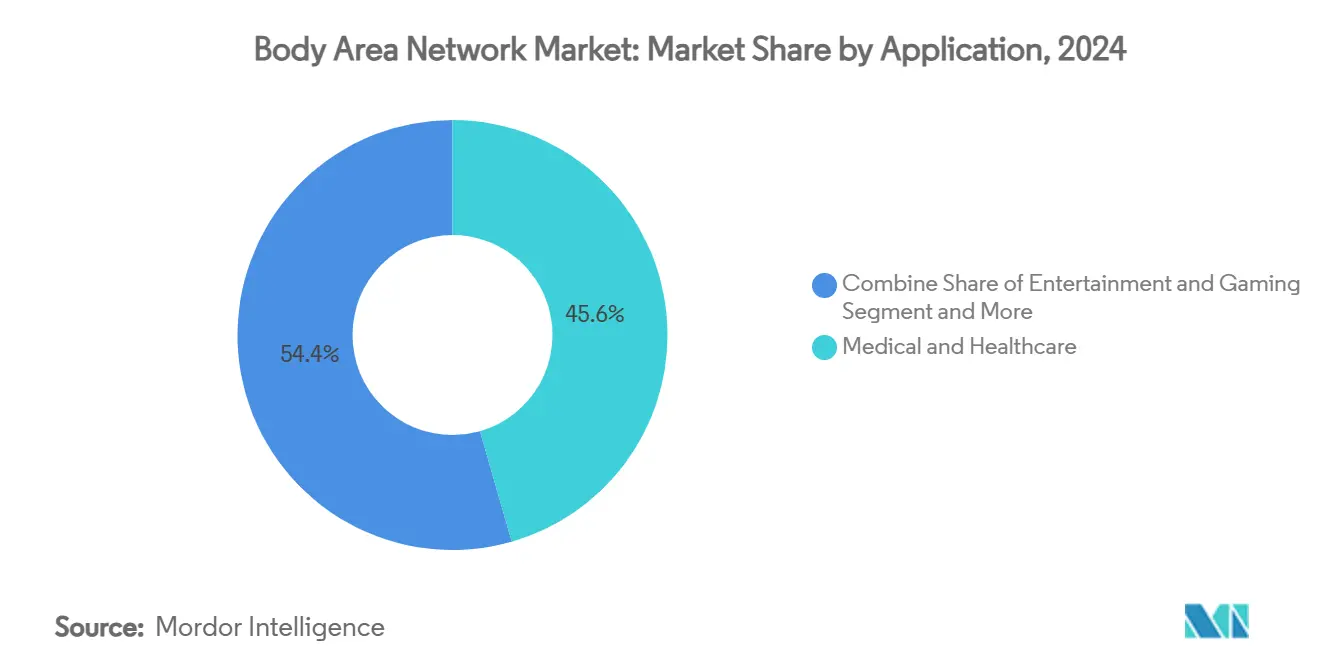

- By application, healthcare held 45.56% of the body area network market share in 2024, while entertainment and gaming applications are advancing at a 14.84% CAGR through 2030.

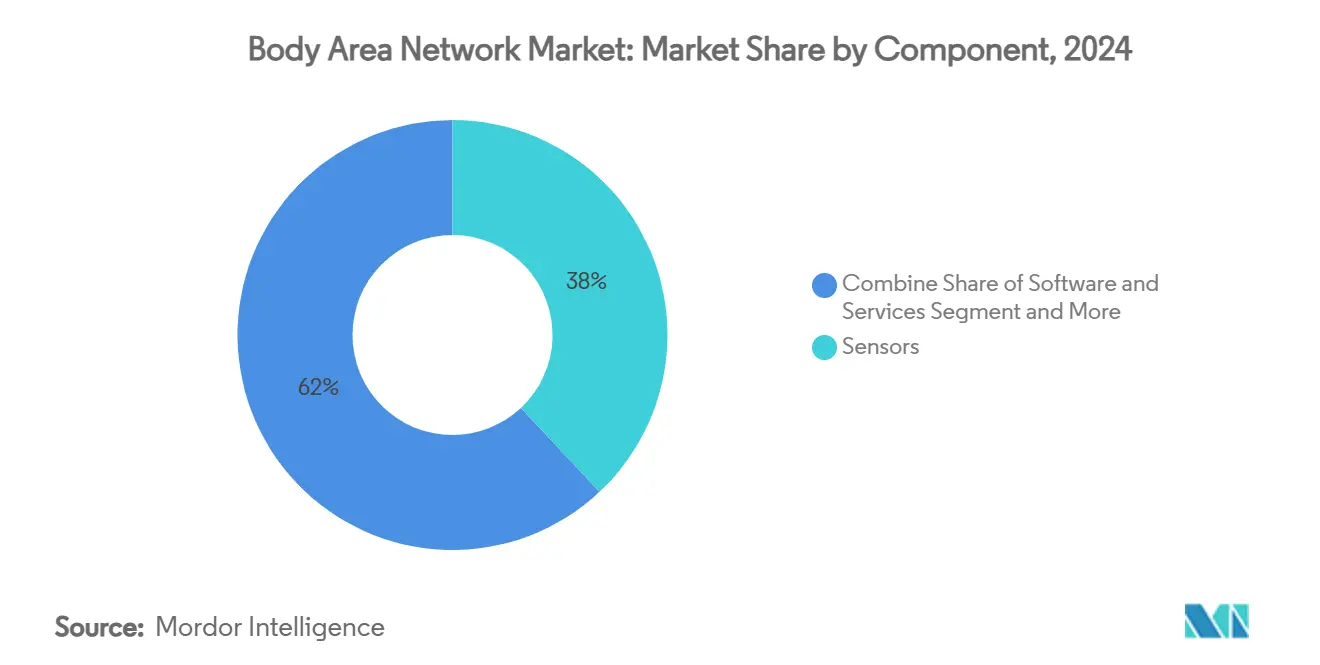

- By component, sensors accounted for 38.01% of the body area network market size in 2024, whereas software and services are projected to expand at a 14.56% CAGR through 2030.

- By connectivity technology, Bluetooth/BLE led with 44.76% revenue share in 2024; 5G and LPWAN solutions are forecast to grow at 15.02% CAGR to 2030.

- On-body communication held 54.87% of the body area network market share in 2024, while off-body communication is projected to grow at a 13.67% CAGR through 2030.

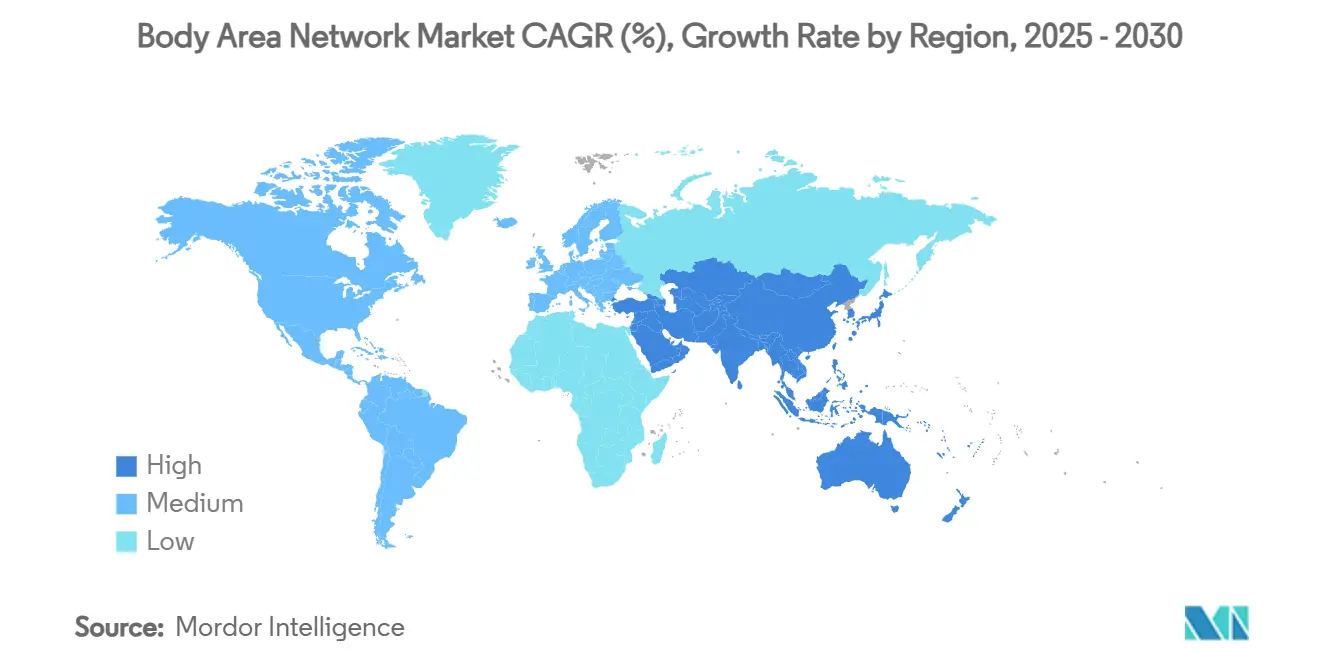

- By geography, North America commanded 38.44% of the body area network market in 2024, while the Middle East and Africa region is projected to accelerate at a 15.34% CAGR through 2030.

Global Body Area Network Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of chronic diseases and reimbursement for RPM | +2.8% | North America, Europe | Medium term (2-4 years) |

| Consumer wearables and fitness tracking culture | +1.9% | North America, Asia-Pacific | Short term (≤ 2 years) |

| Sensor miniaturization and cost decline | +2.1% | Global, manufacturing in Asia-Pacific | Long term (≥ 4 years) |

| Regulatory push for remote-care adoption | +1.7% | North America, Europe, emerging markets | Medium term (2-4 years) |

| Precision digital-therapeutics integration | +1.2% | North America, Europe, select Asia-Pacific | Long term (≥ 4 years) |

| Smart-textile-enabled invisible BANs | +0.8% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing prevalence of chronic diseases and reimbursement for RPM

Rising diabetes, hypertension, and heart-failure caseloads are prompting providers to adopt continuous monitoring programs that lower readmissions and improve outcomes. Frederick Health cut hospital readmissions by 83% and saved USD 5.1 million after deploying connected devices. NYU Langone enrolled 8,000 patients in home monitoring and recorded a 532.5% jump in resolved episodes after integrating remote alerts.[1]Singh et al., “Developing and Scaling Remote Patient Monitoring,” NEJM Catalyst, nejm.org Starting in 2025, new Advanced Primary Care Management billing codes allow U.S. clinicians to bundle sensor data, coaching, and telehealth into one reimbursable service, transforming cash-flow dynamics. Similar payer reforms are emerging in Europe and parts of Asia, reinforcing recurring demand for connected devices and analytics.

Proliferation of consumer wearables and fitness tracking culture

Mainstream gadgets are training users to expect 24/7 health insights, a shift that funnels qualified leads toward certified medical devices. Samsung’s 2024 Galaxy Ring launch bridged lifestyle tracking with oxygen saturation and sleep apnea screening in a USD 399.99 form factor. The U.S. wearable medical devices market is projected to hit USD 112.67 billion by 2033, confirming steady consumer appetite. As athletic enthusiasts demand more granular metrics, sports-science labs and pro teams are piloting body area networks that unite cardiac, metabolic, and biomechanical feeds in real time. This cultural normalization lowers adoption barriers for hospital-grade BAN platforms configured for chronic care.

Sensor miniaturization and cost decline

Breakthroughs in flexible substrates, piezoelectric harvesters, and system-on-chip design have produced lighter, cheaper sensors with integrated memory and AI cores. A Korean team demonstrated a 280-fold boost in energy efficiency from a stretchable harvester that powers vital-sign monitors. MIT’s fiber computers weave processing units directly into textiles, opening garment-based diagnostics for extreme environments. [2]Daegu Gyeongbuk Institute of Science and Technology, “Wearable energy harvester achieves 280 times efficiency boost,” techxplore.com These advances shrink bill of materials costs and prolong device life, making large-scale rollouts economically viable for payers and employers.

Regulatory push for remote-care adoption

The FCC reserved spectrum between 2360 MHz and 2400 MHz solely for medical body area network use, eliminating interference risk and giving device firms greater design certainty. The FDA cleared breakthrough devices such as Abbott’s Simplera CGM, validating calibration-free continuous sensing. IEEE ratified 802.15.6 updates and published 2933-2024 guidelines covering security and interoperability, helping vendors converge on common radio stacks. Collectively, harmonized rules cut time-to-market and raise investor confidence, stimulating additional R&D.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and cyber-security concerns | -1.4% | Europe, North America | Short term (≤ 2 years) |

| Limited battery life and energy-harvesting gaps | -0.9% | Global, stronger in low-resource settings | Medium term (2-4 years) |

| RF interference in crowded ISM bands | -0.7% | Dense urban hospitals | Short term (≤ 2 years) |

| Fragmented edge-level interoperability standards | -0.6% | Multi-vendor health systems | Long term |

| Source: Mordor Intelligence | |||

Data-privacy and cyber-security concerns

High-profile ransomware attacks on hospital networks have elevated scrutiny of every connected device. The FDA now requires detailed cyber risk assessments in pre-market submissions, adding engineering overhead and delaying launches. IEEE’s 2621 and 2933-2024 standards outline encryption and key-exchange guidelines, yet smaller firms often lack the resources to embed multi-layer defenses. European GDPR penalties further increase liability, pushing providers to demand on-device analytics that limit cloud exposure.

Limited battery life and energy-harvesting gaps

Most medical wearables still rely on lithium-ion coin cells that last 7–14 days, a replacement cadence that frustrates patients and inflates service costs. TDK analysis shows ambient-energy harvesting covers only 10–30% of typical load profiles, leaving a sizeable deficit. [3]TDK, “Battery Solutions for Wearable Devices,” tdk.com Thermoelectric and triboelectric prototypes yield promising lab efficiencies but struggle with humidity, temperature swings, and scalable manufacturing. The gap constrains use cases such as 24-hour multi-lead ECG streaming where power budgets remain tight.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Analytics Drive Value Creation

Sensors retained a 38.01% share of the body area network market in 2024 by acting as the primary data conduit between the human body and digital infrastructure. Recent magnetoreceptive e-skin prototypes add magnetic-field mapping without bulky coils, widening diagnostic reach. Yet the fastest-growing revenue stream comes from software and services, which are projected to deliver a 14.56% CAGR as providers demand analytic dashboards and AI decision engines. Power-management ICs are benefiting from flexible organic photovoltaics that achieve 16.18% efficiency, increasing deployment feasibility in low-resource geographies.

The software layer now orchestrates data curation, compliance logging, and therapeutic recommendations inside hospital workflows. Dexcom’s generative AI upgrade illustrates how cloud engines transform sensor feeds into predictive alerts with minimal clinician input. Processors with integrated neural accelerators keep personal data on the edge, aligning with new privacy mandates. Over the forecast horizon, modular firmware updates are expected to extend device lifecycles and support subscription-based revenue, intensifying competition across analytics vendors in the body area network industry.

By Connectivity Technology: 5G Networks Enable Advanced Applications

Bluetooth and BLE controlled 44.76% of 2024 revenue, giving the body area network market a familiar install base across smartphones and tablets. Hospitals use ZigBee mesh topologies to maintain redundant pathways in operating theaters, while Wi-Fi supports high-bandwidth transfers inside existing LANs. The arrival of dedicated medical 5G slices eliminates latency bottlenecks, enabling telesurgery demonstrations that synchronize Orlando, Dubai, and Shanghai with sub-20 ms round-trip times.

5G and LPWAN connections are forecast to expand at a 15.02% CAGR because they combine ultra-reliable low-latency performance with energy-efficient profiles for implantables. Private 5G hospital networks in China illustrate the security and QoS benefits of isolated cores. ANT+ and UWB fill niche needs in sports analytics and asset tracking, respectively, while NFC remains popular for secure pairing. As regional regulators free more mid-band spectrum, the body area network market will diversify its radio stack options and mitigate ISM congestion.

By Device Type: Wearables Dominate Through Consumer Acceptance

Wearable devices such as smartwatches, patches, and rings captured 70.23% of 2024 revenue thanks to their non-invasive nature and daily-use appeal. Apple, Samsung, and Google have expanded biosensor arrays to include blood-pressure estimation, non-invasive glucose trending, and stress biomarkers. Ear-worn and hearable devices are predicted to log a 13.46% CAGR through 2030 as micro-electromechanical microphones and photoplethysmography merge inside earbuds for discreet monitoring. Implantables address critical cardiac and neuro applications, with Abbott’s AVEIR DR setting a precedent for dual-chamber leadless pacing.

Smart garments integrate conductive yarns and haptic actuators to deliver biofeedback without visible hardware. A self-healing electronic skin prototype restored 80% conductivity within 10 seconds of damage, demonstrating resilience for occupational safety deployments. As production costs fall, multi-modal sensor placement across wrists, chest, and thighs will improve algorithmic accuracy, reinforcing wearable dominance within the body area network market.

By Application: Entertainment and Gaming Drive Innovation

Healthcare retained 45.56% share in 2024 as reimbursement and clinical evidence underpin device purchases, yet immersive media leads innovation velocity. Streaming platforms and VR studios are embedding real-time biometric triggers that adapt game difficulty and narrative arcs, a feature that is pushing a 14.84% CAGR in entertainment-focused deployments. Military programs deploy rugged BAN kits that relay vitals and location to commanders, reducing casualty response times.

Chronic disease programs record tangible benefits: unified care models that integrate remote monitoring have lowered systolic blood pressure by 11.9 mmHg and HbA1c by 1.4% in multi-center trials. Elderly-care providers layer fall detection with medication reminders, extending independence for seniors. Sports franchises equip athletes with inertial sensors and metabolic trackers to fine-tune training loads, creating performance benchmarks later commercialized for consumer gear. These cross-sector successes feed a virtuous cycle of component demand and cloud-analytics subscriptions inside the body area network industry.

By Communication Type: Off-Body Connectivity Enables Cloud Integration

On-body links—typically Bluetooth or intra-body capacitive couplings—managed 54.87% of 2024 traffic due to their reliability over short ranges. Off-body hand-offs to smartphones, gateways, or 5G routers are forecast to climb at a 13.67% CAGR as healthcare shifts toward integrated electronic records and predictive population health models. IEEE research on software-defined networking and blockchain-anchored identity layers shows how providers can maintain audit trails while shuttling encrypted packets to cloud AI engines.

Intra-body ultrasonic telemetry remains the choice for deeply implanted neuro-stimulators because RF absorption in tissue is high. Visible light communication is being trialed inside surgical theaters to reduce electromagnetic hazards, and early tests meet 6G deterministic latency targets. As edge accelerators proliferate, more preprocessing will occur on the body, lowering data volumes and accommodating stricter privacy statutes across the body area network market.

Geography Analysis

North America accounted for 38.44% of 2024 revenue, supported by Medicare reimbursement, FCC spectrum allocations, and mature EHR infrastructures. More than 8,000 patients at NYU Langone Health transmit vitals daily, yielding a 58.7% uptick in actionable data, which showcases provider readiness. The U.S. FDA’s expedited review of Simplera and other CGMs keeps innovation cycles short, while Canadian regulators streamline device licensing to align with cross-border supply.

The Middle East and Africa region is projected to record a 15.34% CAGR through 2030. Saudi Arabia’s Vision 2030 earmarks AI as a linchpin for public-sector care modernization, giving the body area network market an anchor customer base. The UAE’s Malaffi interoperability exchange links hospitals and clinics, opening APIs for remote monitoring platforms. Private equity commitments such as Al Khair Capital’s USD 50 million healthcare fund highlight investor confidence in regional rollouts.

Asia-Pacific blends populous emerging economies with tech-heavy incumbents. The GSMA counts 1.8 billion mobile subscribers, providing an addressable channel for tele-consults and BAN data. India’s digital-health roadmap targets USD 25 billion in value by 2025, driven by the ABHA patient-ID initiative. China’s private 5G wards and Japan’s surgical robotics clusters draw on domestic semiconductor ecosystems. Collectively, these programs fuel volume growth and encourage local manufacturing, reducing regional import dependency and reinforcing the long-term competitiveness of the body area network market.

Competitive Landscape

The body area network market shows moderate fragmentation. Abbott, Medtronic, Dexcom, Samsung, and Apple lead in installed units and IP portfolios. Abbott’s August 2024 alliance with Medtronic bundles FreeStyle Libre CGMs with MiniMed insulin pumps, targeting 11 million intensive-therapy diabetics. Medtronic filed 510(k) submissions in April 2025 for an interoperable pump algorithm to formalize that tie-up. Samsung broadened its wellness ecosystem at CES 2025, integrating Galaxy Ring data into SmartThings telehealth channels.

Hardware makers face supply-chain strain from semiconductor shortages, prompting some to vertically integrate or pre-book foundry capacity. Patent filings reveal aggressive experimentation: Google’s electrical-impedance tomography wearables reconstruct full-hand movement for AR interfaces, while Apple patents sweat-wicking cushion assemblies to improve skin-sensor fidelity. Smaller firms pivot toward niche segments such as neonatal monitors or veterinary wearables, positioning themselves for M&A exits. Standard-setting participation has become a strategic tool; early compliance with IEEE 2933-2024 lets vendors influence hospital procurement checklists and differentiate through security certifications.

Across the forecast horizon, software will exert outsized influence on revenue as SaaS layers deliver decision support, cohort analytics, and firmware-as-a-service. Firms that merge secure cloud operations with ergonomic industrial design are expected to command premium pricing, reinforcing a barbell structure where a handful of global platforms coexist alongside regional specialists.

Body Area Network Industry Leaders

Apple Inc.

Samsung Electronics Co., Ltd.

Google LLC

Koninklijke Philips N.V.

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Abbott started the ASCEND CSP pivotal trial to evaluate its conduction system pacing ICD lead after securing FDA breakthrough designation.

- April 2025: Medtronic filed 510(k) applications for an interoperable MiniMed 780G pump integrated with Abbott CGM technology.

- March 2025: Abbott’s TRILUMINATE Pivotal trial data showed TriClip therapy reduced heart-failure hospitalizations to 0.19 events per patient-year.

- January 2025: Samsung presented Galaxy Ring and Galaxy Watch integrations at CES 2025, showcasing end-to-end wellness services.

Global Body Area Network Market Report Scope

| Sensors |

| Processors and Micro-controllers |

| Power-management ICs and Energy-harvesting |

| Transceivers / Communication ICs |

| Software and Services |

| Bluetooth / BLE |

| ZigBee |

| Wi-Fi |

| ANT+ |

| UWB |

| NFC |

| 5G / LPWAN |

| Wearable Devices | Smartwatches and Fitness Bands |

| Smart Patches and E-skin | |

| Smart Clothing and E-textiles | |

| Implantable Devices | |

| Ear-worn / Hearables | |

| Others (on-body monitors) |

| Medical and Healthcare | Remote Patient Monitoring |

| Chronic Disease Management | |

| Elderly and Assisted Living | |

| Sports and Fitness | |

| Military and Defense | |

| Workplace Safety and Industrial | |

| Entertainment and Gaming |

| Intra-body Communication |

| On-body Communication |

| Off-body Communication (to exernal devices/cloud) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Sensors | ||

| Processors and Micro-controllers | |||

| Power-management ICs and Energy-harvesting | |||

| Transceivers / Communication ICs | |||

| Software and Services | |||

| By Connectivity Technology | Bluetooth / BLE | ||

| ZigBee | |||

| Wi-Fi | |||

| ANT+ | |||

| UWB | |||

| NFC | |||

| 5G / LPWAN | |||

| By Device Type | Wearable Devices | Smartwatches and Fitness Bands | |

| Smart Patches and E-skin | |||

| Smart Clothing and E-textiles | |||

| Implantable Devices | |||

| Ear-worn / Hearables | |||

| Others (on-body monitors) | |||

| By Application | Medical and Healthcare | Remote Patient Monitoring | |

| Chronic Disease Management | |||

| Elderly and Assisted Living | |||

| Sports and Fitness | |||

| Military and Defense | |||

| Workplace Safety and Industrial | |||

| Entertainment and Gaming | |||

| By Communication Type | Intra-body Communication | ||

| On-body Communication | |||

| Off-body Communication (to exernal devices/cloud) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large will the body area network market be by 2030?

Forecasts show the body area network market size reaching USD 27.35 billion in 2030, driven by an 11.59% CAGR underpinned by chronic-care demand and 5G rollouts.

Which application area is growing fastest?

Entertainment and gaming deployments are expanding at a 14.84% CAGR because immersive experiences rely on real-time biometric feedback.

What is the leading component segment today?

Sensors hold the largest 2024 revenue share at 38.01%, though software and services are projected to grow faster at 14.56% CAGR.

Why is North America ahead of other regions?

Medicare reimbursement, FDA fast-track approvals, and dedicated FCC spectrum have accelerated adoption, giving North America 38.44% share in 2024.

What key restraint should vendors address first?

Data privacy and cybersecurity carry the highest negative weight (-1.4% impact on CAGR), making end-to-end encryption and on-device analytics top priorities.

Which connectivity technology shows the strongest upside?

5G and LPWAN links are expected to log a 15.02% CAGR because they meet low-latency medical requirements and support hospital private networks.

Page last updated on: