Fruit And Vegetable Processing Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 8.72 Billion |

| Market Size (2031) | USD 11.8 Billion |

| Growth Rate (2026 - 2031) | 6.24% CAGR |

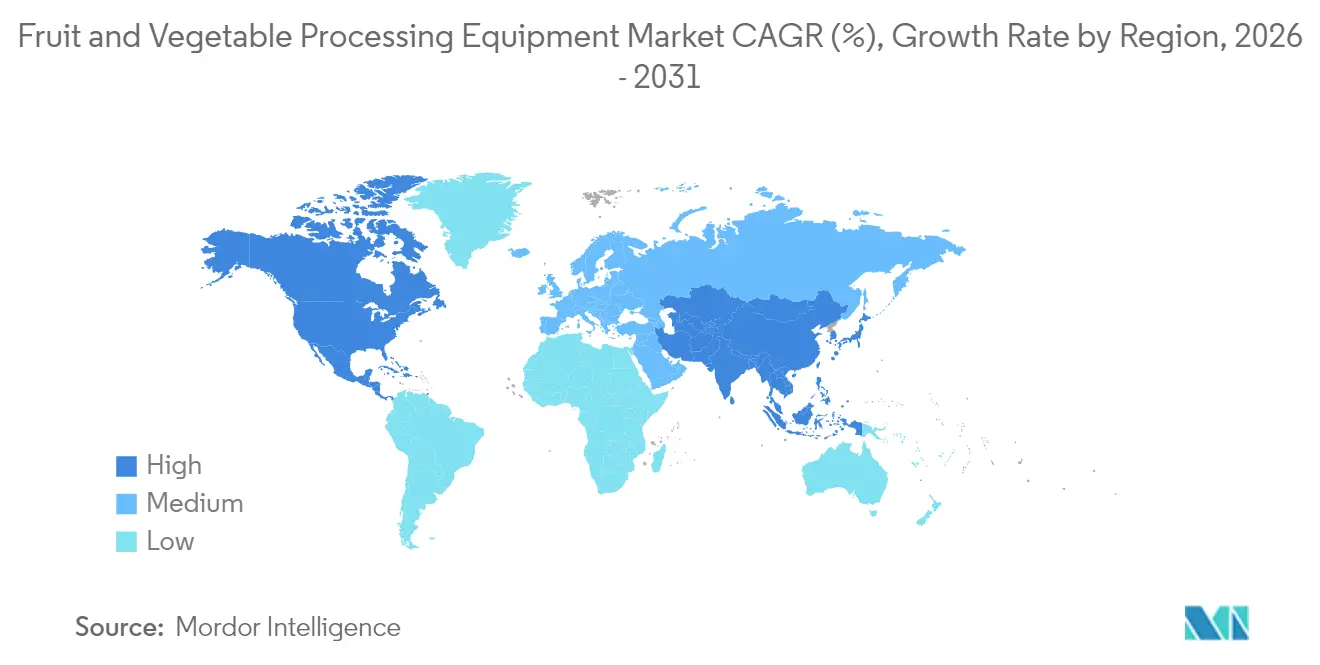

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

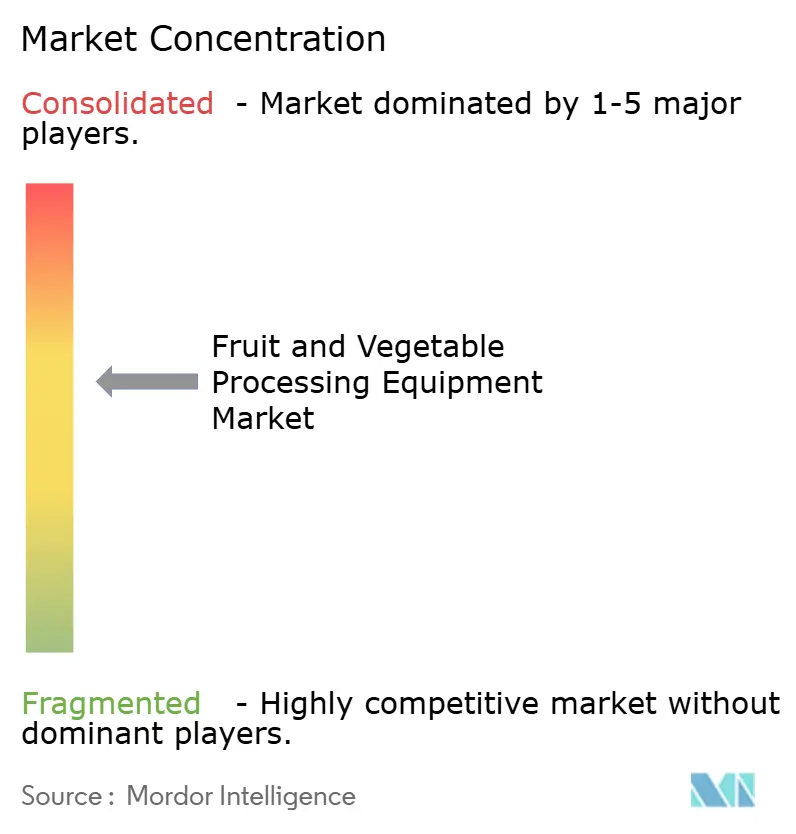

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fruit And Vegetable Processing Equipment Market Analysis by Mordor Intelligence

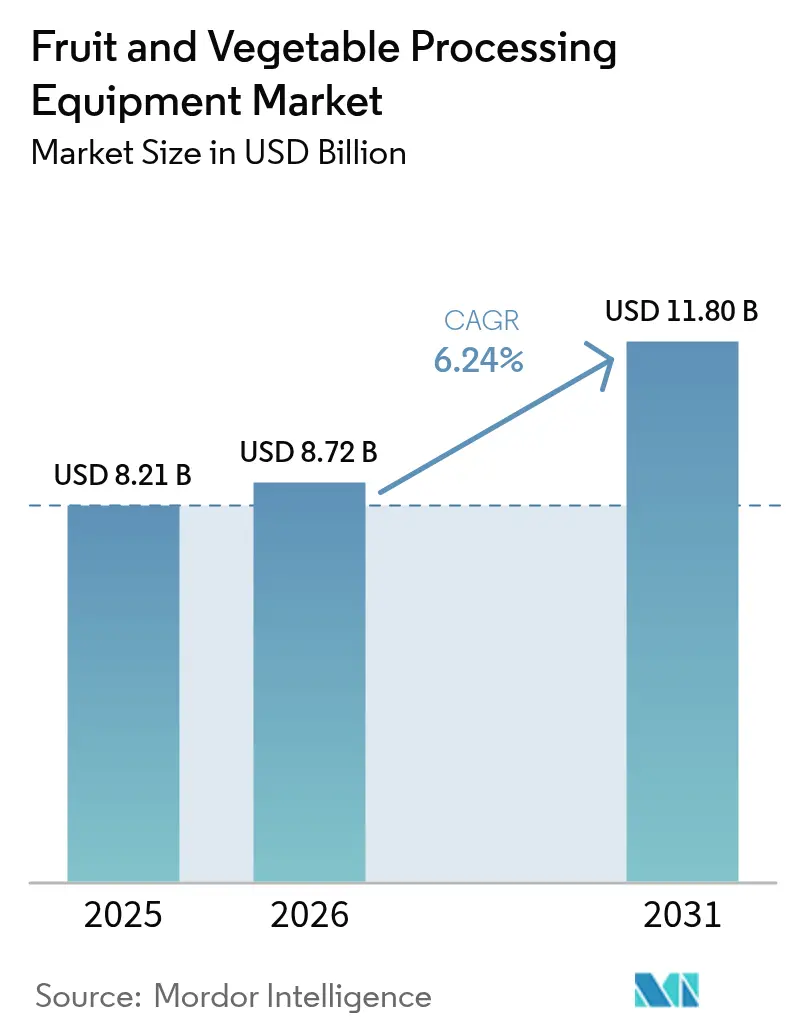

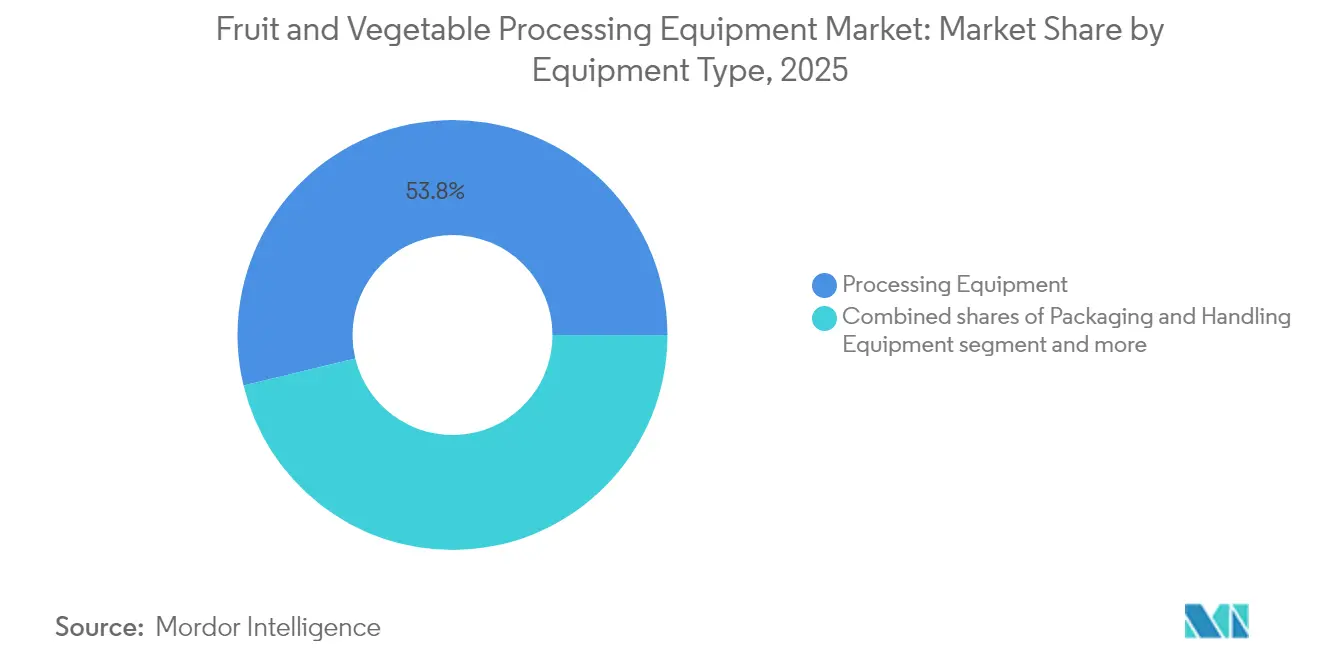

The fruit and vegetable processing equipment market size was valued at USD 8.21 billion in 2025 and estimated to grow from USD 8.72 billion in 2026 to reach USD 11.8 billion by 2031, at a CAGR of 6.24% during the forecast period (2026-2031). This trajectory reflects accelerating capital deployment into automated processing lines, cold chain infrastructure, and multifunctional systems that reduce labor dependency while meeting tightening food safety standards. Processing Equipment commands 54.41% of the 2024 market, yet Packaging and Handling Equipment is projected to grow at 7.84% annually through 2030, signaling a strategic pivot toward end-of-line automation as processors seek to compress time-to-market and comply with modified atmosphere packaging requirements [1]Source: Agriculture and Agri-Food Canada, "Modified atmosphere packaging requirements", agriculture.canada.ca. Government-backed modernization programs, including Canada's Agri-Innovation Program, India's Rs. 10,000 crore (USD 1.2 billion) PMFME scheme, and China's 14th Five-Year Plan cold chain targets, are channeling subsidies and low-interest loans into processing capacity, particularly in the Asia-Pacific, which held 31.24% of the market in 2024[2]Source: Government of India, "Government-backed modernization programs", pib.gov.in.

Key Report Takeaways

- By equipment type, processing equipment held 53.78% of the fruit and vegetable processing equipment market share in 2025, and packaging and handling is forecast to expand at a 7.71% CAGR to 2031.

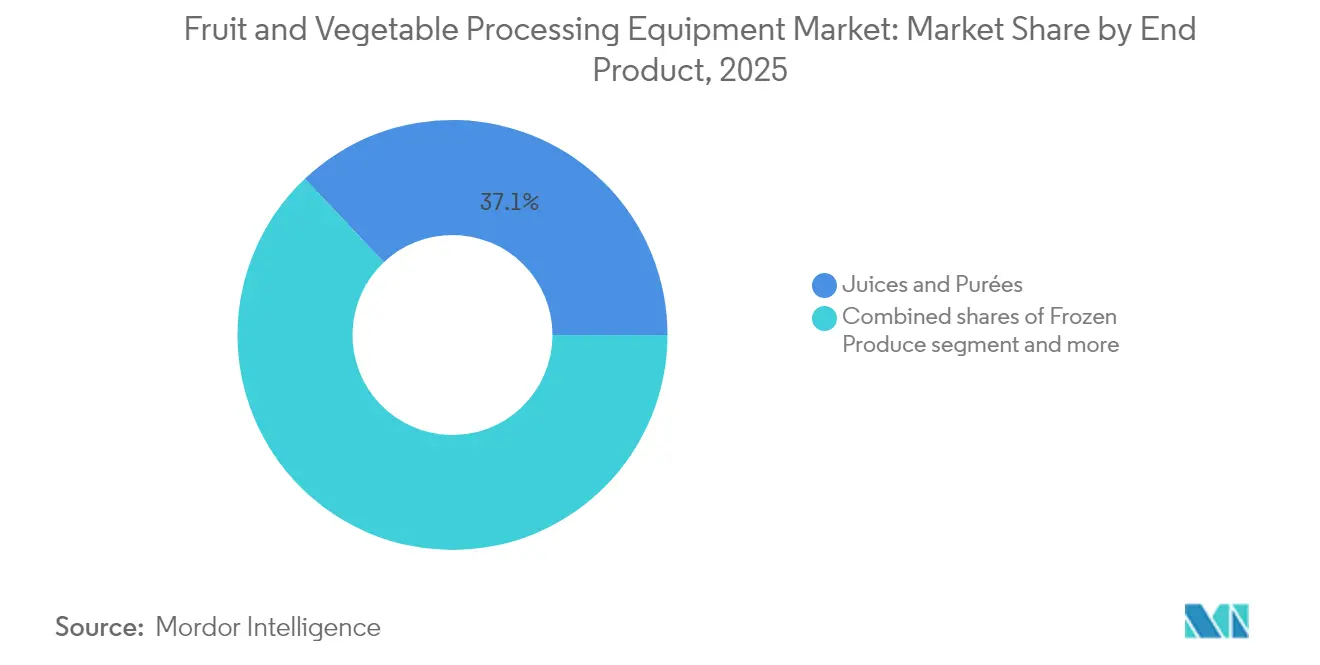

- By end-product type, juices and purées captured 37.05% share of the fruit and vegetable processing equipment market size in 2025, and frozen produce is advancing at an 8.52% CAGR through 2031.

- By geography, Asia-Pacific led with a 31.05% share in 2025, while the Middle East and Africa recorded the highest projected CAGR at 7.92% to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fruit And Vegetable Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing adoption of cold chain and preservation technologies | +1.2% | Global, with a concentration in Asia-Pacific and the Middle East | Medium term (2-4 years) |

| Technological advancements in automated and high-efficiency processing equipment | +1.5% | North America, Europe, Asia-Pacific core | Short term (≤ 2 years) |

| Growing consumer preference for minimally processed and fresh-tasting products | +0.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| Government initiatives promoting food processing and agri-tech modernization | +1.1% | Asia-Pacific, Middle East, select Latin American markets | Long term (≥ 4 years) |

| Development of multifunctional equipment reducing processing time and labor costs | +0.8% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Rising awareness about food safety and hygiene standards | +0.7% | Global, regulatory pressure is strongest in North America and the EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Cold Chain and Preservation Technologies

Cold chain infrastructure is expanding at an unprecedented pace, driven by government mandates to reduce post-harvest losses and extend shelf life for export markets. India approved 399 cold chain projects under the Pradhan Mantri Kisan Sampada Yojana in 2024, targeting integrated pack-houses with pre-cooling, ripening chambers, and refrigerated transport links. This creates derived demand for blast freezers, individual quick freezing tunnels, and modified atmosphere packaging equipment that lock in quality at the point of harvest. Singapore's 30 by 30 food security initiative similarly mandates cold storage capacity for domestic produce, compelling vertical farms and controlled-environment agriculture operators to install post-harvest processing lines[3]Source: Singapore Food Agency, "Key Strategies for Ensuring Food Security", sfa.gov.sg. The strategic implication is that cold chain investments are no longer confined to distribution; they now encompass processing, blurring the line between farm-gate and factory-floor equipment.

Technological Advancements in Automated and High-Efficiency Processing Equipment

Automation is migrating from repetitive tasks like sorting and cutting to cognitive functions such as defect detection and yield optimization. Bühler's LumoVision optical sorters deploy hyperspectral imaging and machine learning algorithms to identify internal defects invisible to human inspectors, reducing false rejects by 15% and improving throughput. JBT Corporation's Frigoscandia GYRoCOMPACT spiral freezers integrate IoT sensors that adjust belt speed and refrigerant flow in real time, cutting energy consumption by 20% compared to legacy systems. These advancements matter because they shift the value proposition from labor replacement to data-driven process control, enabling processors to guarantee consistent quality and traceability, prerequisites for retail private-label contracts and export certifications. Equipment suppliers that embed predictive maintenance and remote diagnostics are capturing premium pricing, as unplanned downtime costs processors USD 50,000 to USD 200,000 per day in lost production and spoilage.

Growing Consumer Preference for Minimally Processed and Fresh-Tasting Products

Health-conscious consumers are gravitating toward products with clean labels and short ingredient lists, pressuring processors to adopt non-thermal preservation methods. High-pressure processing, which applies 87,000 psi to inactivate pathogens without heat, has become standard for premium cold-pressed juices and guacamole, with installed capacity doubling since 2024. Fresh-cut salads and vegetable trays, which require modified atmosphere packaging to maintain crispness, now represent a USD 4 billion segment in North America alone, driving demand for vertical form-fill-seal machines with gas flushing capabilities. The paradox is that "minimally processed" products often require more sophisticated equipment than traditional canning or freezing, as processors must control microbial load, enzymatic activity, and respiration rates without chemical preservatives. This is reshaping capital allocation, with processors investing in pulsed electric field systems, ultraviolet-C light chambers, and edible coatings, technologies that were niche five years ago but are now mainstream.

Government Initiatives Promoting Food Processing and Agri-Tech Modernization

Sovereign food security concerns are translating into direct subsidies and tax incentives for processing infrastructure. Canada's Agri-Innovation Program allocated CAD 150 million (USD 110 million) in 2024 to co-fund automation projects, covering up to 50% of capital costs for small and medium processors according to the Agriculture and Agri-Food Canada. China's 14th Five-Year Plan mandates 70% cold chain coverage for perishable agricultural products by 2025, prompting provincial governments to offer land subsidies and preferential loans for processing parks according to the National Development and Reform Commission, China. These programs are not neutral, they favor domestic equipment manufacturers through local-content requirements, creating bifurcated markets where imported machinery faces tariff and certification barriers. The strategic takeaway is that equipment suppliers must localize production or form joint ventures to access subsidy-driven demand, particularly in Asia-Pacific and Middle East markets where government procurement dominates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capital investment required for advanced processing equipment | -0.6% | Global, acute in emerging markets and the SME segment | Short term (≤ 2 years) |

| Complexity and maintenance requirements of automated machinery | -0.4% | Global, more pronounced in regions with limited technical support | Medium term (2-4 years) |

| Shortage of skilled workforce to operate sophisticated equipment | -0.5% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Strict regulatory compliance and certification requirements in different regions | -0.3% | Global, the highest burden in North America and the EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Investment Required for Advanced Processing Equipment

Processing lines with integrated automation, spanning washing, sorting, cutting, blanching, and packaging, demand USD 2 million to USD 5 million in capital, a threshold that excludes most small and medium enterprises from upgrading legacy equipment. Return-on-investment calculations hinge on throughput gains and labor savings, yet processors in emerging markets face 12% to 18% interest rates on equipment loans, extending payback periods beyond 7 years, and eroding net present value. Leasing and equipment-as-a-service models remain underdeveloped outside North America and Europe, leaving processors to self-finance or rely on government subsidies that are often delayed or capped at 30% of project costs. This capital constraint bifurcates the market: large processors amortize investments across high-volume contracts, while smaller operators defer upgrades, perpetuating quality inconsistencies and limiting access to export markets that mandate traceability and HACCP compliance.

Shortage of Skilled Workforce to Operate Sophisticated Equipment

The U.S. manufacturing sector reported 2.1 million unfilled positions in 2024, with food processing facing acute shortages of technicians trained in programmable logic controllers, industrial robotics, and predictive maintenance platforms. Equipment suppliers are responding by embedding remote diagnostics and augmented reality interfaces that guide operators through troubleshooting, yet these solutions assume reliable internet connectivity and digital literacy, conditions absent in many rural processing facilities. The strategic implication is that automation intended to reduce labor dependency paradoxically creates new skill bottlenecks, as a single malfunctioning sensor or misconfigured recipe can halt production for hours. Processors are partnering with community colleges and equipment manufacturers to develop certification programs, but training cycles span 6 to 12 months, lagging the pace of technology deployment and leaving a persistent gap between installed capacity and operational uptime.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Automation Drives Packaging Surge

Processing Equipment held 53.78% of the market in 2025, reflecting its role as the core value-add stage where raw produce is transformed into consumer-ready formats through blanching, pasteurization, extraction, and concentration. However, Packaging and Handling Equipment is expanding at 7.71% annually through 2031, the fastest growth among all equipment types, as processors prioritize end-of-line automation to meet modified atmosphere packaging standards and reduce contamination risks during final handling. Vertical form-fill-seal machines, robotic case packers, and inline checkweighers are displacing manual labor in facilities pursuing Safe Quality Food and British Retail Consortium certifications, which mandate documented controls at every packaging touchpoint. Pre-processing Equipment, encompassing washers, peelers, and destoners, remains essential but commoditized, with differentiation limited to water recirculation efficiency and sanitary design features that comply with 3-A and EHEDG hygiene standards.

The shift toward Packaging and Handling reflects a broader strategic reorientation: processors recognize that product quality established during processing can be compromised by inadequate packaging, particularly for fresh-cut and minimally processed items with 7- to 14-day shelf lives. GEA's robotic pick-and-place systems, integrated with vision-guided sorting, enable mixed-SKU packing at speeds exceeding 120 units per minute, a capability critical for e-commerce fulfillment and retail variety packs. Compliance frameworks such as ISO 22000 now extend packaging line validation requirements to include allergen cross-contact prevention and tamper-evident sealing, driving capital allocation toward equipment with automated changeover and clean-in-place functionality. Pre-processing Equipment, while foundational, offers limited margin expansion unless suppliers incorporate optical sorting or defect rejection, technologies traditionally associated with processing stages, creating convergence between equipment categories.

By End-Product Type: Frozen Gains on Juice Dominance

Juices and Purées commanded 37.05% of the market in 2025, sustained by high-pressure processing and aseptic filling technologies that deliver fresh taste without refrigeration, a format favored by premium brands and health-focused consumers. Yet Frozen Produce is projected to grow at 8.52% annually through 2031, the fastest rate among end-product segments, as individual quick freezing and cryogenic systems enable year-round availability of berries, tropical fruits, and vegetable medleys for foodservice and retail. This divergence reflects distinct value propositions: juice equipment prioritizes nutrient retention and microbial safety, while frozen lines optimize ice crystal size and freezing speed to preserve texture and color. Processors investing in dual-purpose facilities, capable of switching between juice extraction and IQF freezing, are capturing margin premiums by aligning production with seasonal supply gluts and demand cycles.

Canned Produce, historically the largest segment, is stagnating as consumers associate thermal processing with nutrient loss and metallic off-flavors, despite modern retort systems that reduce cook times by 40% through steam-air mixtures and rotational agitation. Dried and Dehydrated products occupy a niche, with freeze-drying equipment commanding USD 300,000 to USD 1 million per unit, limiting adoption to high-value applications like instant soups and backpacking meals. Fresh and Fresh-Cut segments are converging, as modified atmosphere packaging extends shelf life to 10 to 14 days, blurring the line between whole produce and convenience formats. Processors targeting Fresh-Cut are deploying chlorine dioxide wash systems and edible coatings to suppress enzymatic browning, technologies that require FDA Generally Recognized as Safe approvals and add USD 0.05 to USD 0.10 per kilogram in processing costs, a margin squeeze that favors vertically integrated operators with retail distribution leverage.

Geography Analysis

Asia-Pacific captured 31.05% of the market in 2025, driven by China's cold chain mandates, India's PMFME subsidies, and Japan's labor-shortage-induced automation. China's 14th Five-Year Plan allocated USD 15 billion for cold chain logistics, including processing hubs in Shandong, Guangdong, and Sichuan provinces that consolidate smallholder output into export-grade volumes according to the National Development and Reform Commission, China. Japan's labor force contraction, manufacturing employment fell 8% from 2019 to 2024, is accelerating the adoption of collaborative robots and AI-driven quality inspection in vegetable processing facilities supplying convenience stores and ready-meal manufacturers. Australia's focus on export-oriented horticulture, particularly berries and stone fruit destined for Southeast Asia, is driving investments in optical sorters and modified atmosphere packaging lines that meet phytosanitary standards. The region's growth is uneven: multinational processors dominate in coastal China and urban India, while inland and rural areas rely on manual processing, creating a dual market where premium equipment suppliers compete on technology and local manufacturers compete on price.

The Middle East and Africa are expanding at 7.92% annually, the fastest regional growth rate, propelled by food security imperatives and import substitution policies. UAE's National Food Security Strategy 2051 mandates 70% self-sufficiency in perishable produce, prompting vertical farm operators and controlled-environment agriculture projects to install post-harvest processing lines for leafy greens and tomatoes according to the Government of the United Arab Emirates. Saudi Arabia's Vision 2030 allocated USD 3.2 billion for agri-processing infrastructure, including date processing facilities in Al-Ahsa and vegetable packing houses in Jizan that reduce reliance on imports from Egypt and Jordan, according to the Government of Saudi Arabia. South Africa's citrus and grape export sector, valued at USD 2.5 billion annually, is upgrading sorting and packing lines to meet European Union traceability requirements and Global GAP certification.

Europe and North America, while mature, continue to invest in sustainability-focused equipment upgrades. Europe's Farm to Fork Strategy mandates a 50% reduction in food waste by 2030, driving adoption of AI-powered sorting systems that salvage cosmetically imperfect produce for juice and purée production according to the European Commission. North America's focus on labor cost mitigation, minimum wages in California and Washington exceeding USD 15 per hour, is accelerating robotic harvesting and automated packing, with equipment suppliers offering turnkey solutions that integrate field machinery with processing lines. South America, led by Brazil and Argentina, is expanding frozen fruit exports to North America and Europe, requiring IQF tunnels and blast freezers that meet HACCP and Kosher certification standards. Compliance influence from bodies such as the FDA, EFSA, and Codex Alimentarius shapes equipment specifications across all geographies, with sanitary design and traceability features becoming non-negotiable for processors targeting export markets.

Regulatory Landscape

Food safety, hygiene, and traceability rules remain the primary compliance drivers shaping equipment specifications for fruit and vegetable processors selling into regulated retail and export channels, including sanitary design, clean-in-place validation, and digital recordkeeping. In the United States, FDA actions around the Food Traceability Rule included a draft guidance issued in February 2026 and a stakeholder listening session held on March 6, 2026, shifting near-term emphasis toward implementation planning, pilots, and systems readiness rather than only enforcement deadlines.

In the European Union, Commission Implementing Regulation (EU) 2023/2430 became applicable from January 2025 for marketing standard conformity checks relevant to processed fruit and vegetable products, reinforcing documentation and quality-control requirements that extend to inspection-ready processing and packing lines. At the international level, Codex Alimentarius Commission decisions from its 49th Session (July 7, 2026) adopting standards for vanilla and large cardamom add to the global reference standards used in cross-border trade, which processors and equipment suppliers use to align quality and safety expectations when configuring processes and verification protocols.

Competitive Landscape

The market exhibits moderate consolidation, as established European integrators, Bühler, GEA, and Alfa Laval, compete against specialized regional suppliers and niche technology providers. Large players pursue turnkey strategies, bundling pre-processing, processing, and packaging modules into single contracts that lock in multi-year service agreements and spare parts revenue. This approach resonates with multinational food companies seeking single-source accountability and standardized equipment across global facilities, yet it leaves openings for smaller suppliers that offer best-in-class single-function machines at 30% to 40% lower capital costs.

Patent activity in optical sorting, energy-efficient heat exchangers, and AI-driven quality control has intensified since 2024, with Bühler filing 12 hyperspectral imaging patents and JBT securing 8 patents for cryogenic freezing innovations. The strategic battleground is shifting from mechanical throughput to digital intelligence: suppliers embedding IoT sensors, predictive maintenance algorithms, and cloud-based recipe management are capturing premium pricing and recurring software revenue, while those offering standalone hardware face commoditization pressure.

Modular designs that allow processors to add capacity in USD 200,000 increments, rather than USD 2 million greenfield investments, are gaining traction among small and medium enterprises constrained by capital access. Emerging disruptors include robotics specialists partnering with food technologists to develop vision-guided systems that handle delicate produce like berries and leafy greens without bruising, a capability that traditional mechanical conveyors cannot match. Compliance with ISO 22000, HACCP, and FDA FSMA preventive controls is table stakes, with equipment suppliers offering validation protocols and documentation packages that streamline third-party audits, a service differentiation that matters as processors face increasing scrutiny from retailers and regulators.

Fruit And Vegetable Processing Equipment Industry Leaders

-

GEA Group Aktiengesellschaft

-

ALFA LAVAL

-

Bühler AG

-

JBT

-

KRONEN GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Automation and inspection intelligence are becoming a more defined purchase priority for lines handling fresh, fresh-cut, and frozen formats, where yield loss and foreign-material risk translate into direct operating cost and audit exposure. In 2026, multiple suppliers expanded optical and AI-enabled capabilities for produce operations, including Key Technology launching the COMPASS optical sorter for fresh and IQF vegetables (wet or dry environments) and UNITEC showcasing its VISION 4.0 AI platform with UNIQ CHERRY for internal quality parameter detection at Macfrut 2026. Together, these releases support demand for integrated solutions that bring gentle handling, sorting and classification, and packaging verification into one data layer that can support traceability, specification compliance, and reduced giveaway.

Sustainability-driven equipment upgrades are also creating buying triggers where water, chemicals, and energy are constrained or increasingly costed into operations. In 2026, TOMRA Food launched the DPS-16 Dry Peel Separator, which performs water-free separation at high throughput (70 tons per hour, potatoes), and published R&D focused on non-chemical peeling approaches such as pulsed electric fields, cold plasma, and catalytic infrared to reduce effluent load and energy use versus lye/steam processes. Line debottlenecking and labor substitution are likewise extending beyond cutting and washing into more complex tasks, as seen in Wyma Solutions launching the Optical Vege-Trimmer (optical recognition with IP69K-rated components) and Natural Processing Solutions introducing the Pluckr system for gentle automated detachment of clustered produce, which supports investment in automation where manual dexterity has constrained scale.

Recent Industry Developments

- July 2026: GEA announced a EUR 4 million investment in a German biotech pilot center focused on accelerating food production scale-up. The added pilot capability supports faster validation and transfer of processing concepts into industrial equipment packages, shortening customer development cycles for new produce-based formulations and processes.

- January 2025: Buhler Group acquired puffing technology from CEREX, adding capabilities positioned around higher yields and lower energy consumption in grain and pulse processing. The move strengthens Buhler's process portfolio for plant-based and ingredient applications that can extend into fruit and vegetable-derived formulations requiring texturization and controlled expansion steps.

- May 2024: Alfa Laval introduced the Hygienic WideGap heat exchanger for liquid foods containing fibers and particles, targeting higher energy efficiency versus conventional systems. For fruit and vegetable processors handling pulpy streams (juices, purees, soups), this type of hygienic thermal equipment supports throughput upgrades while aligning with tighter sanitation and sustainability requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers machinery and systems used to prepare, process, handle, and pack fruits and vegetables into finished formats, as they move from raw intake to an output that is ready for storage, shipment, or sale.

Scope exclusions: We exclude farm-level harvesting tools, primary cold storage buildings, and retail backroom food prep equipment that is not designed for industrial processing lines.

Segmentation Overview

-

By Equipment Type

- Pre-processing Equipment

- Processing Equipment

- Packaging and Handling Equipment

-

By End-Product Type

- Juices and Purées

- Frozen Produce

- Canned Produce

- Dried and Dehydrated

- Fresh

- Fresh Cut

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the demand backdrop and to keep the model tied to measurable food processing activity. We reviewed public sources such as FAOSTAT, USDA Economic Research Service releases, Eurostat food manufacturing statistics, UN Comtrade trade flows for relevant machinery categories, and World Bank macro indicators to understand production, trade, and investment cycles.

On the supply side, we also relied on accessible company filings, annual reports, investor presentations, reputable press coverage, and association websites linked to food processing and packaging. Select paid subscriptions that support company financials and intelligence, news and financials, and import/export shipment-level views were used to speed up cross-checking of installed base signals and revenue directionally by region. These examples are not exhaustive, and other public and paid sources were reviewed to support data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on speaking with equipment manufacturers, distributors, system integrators, and processing plant stakeholders who manage line upgrades and capex timing. These discussions helped confirm what gets counted as processing equipment versus adjacent handling and cold chain assets. We also used respondent input to validate average selling price movement, lead times, and regional mix across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 15% | APAC: 43% |

| Mid tier: 55% | Functional/Unit leaders: 40% | EMEA: 34% |

| Smaller Players: 15% | Managers: 45% | Americas: 23% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where food processing equipment demand is reconstructed using production and trade signals, and then allocated into fruit and vegetable lines based on processing intensity across key end products (juices and purees, frozen, canned, dried, and fresh-cut). Once the demand pool is formed, it is converted into value using price bands by equipment families and automation level, which are adjusted for regional sourcing patterns.

To keep the totals realistic, we corroborated the outcome with selective bottom-up approximations, including sampled supplier revenue exposure to fruit and vegetable applications, distributor channel checks, and a simple volume times ASP check for commonly installed line modules. Inputs that matter in this market include processed fruit and vegetable output growth, plant capacity additions and modernization cycles, trade movement for industrial food machinery, energy and labor cost pressure that pushes automation, and regulatory and hygiene-driven retrofit frequency. Forecasts were developed using scenario analysis supported by expert views on capex cycles, with assumptions refreshed for inflation, currency timing, and mix shifts where gaps existed in country-level reporting.

Data Validation & Update Cycle

Outputs are checked against independent signals such as processed food production trends, machinery trade direction, and commentary on plant expansions and shutdowns. When variances appear, the assumptions are reviewed, and follow-up calls are triggered to confirm whether the change is a one-off project, a pricing move, or a genuine demand shift.

Before sign-off, numbers pass through multi-step analyst review where unit economics, regional splits, and growth rates are tested for internal consistency. Reports are refreshed annually, and interim updates are made when material events occur, such as major policy changes, sharp currency moves, or large capex announcements. Right before delivery, we run a final update pass so the view aligns with the latest available information.

Mordor Intelligence's Fruit and Vegetable Processing Equipment Market Estimate Compared With Other Published Estimates

Published market values for fruit and vegetable processing equipment can look far apart because the counting boundaries are not always the same, and update timing also varies. Differences usually come from what is treated as processing equipment versus adjacent plant assets, and from how price increases and currency conversion are applied.

If average selling prices are refreshed at different points in the year, the same shipment outlook can convert into different USD totals, especially when regional mix changes. The spread also widens when some estimates include broader packaging lines or general food processing machines, or when older base-year assumptions are carried forward without re-checking plant upgrade activity. In that context, the annual refresh and currency timing applied by Mordor Intelligence can shift the 2026 value relative to other figures.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.72 B (2026) | |

| Global Consultancy A | USD 7.10 B (2025) | Uses an earlier base year and typically reflects a tighter equipment scope, with less visible adjustment for ASP progression and the currency conversion timing used to report the USD value. |

| Industry Publisher B | USD 6.80 B (2024) | Anchored to a prior-year snapshot, which can understate the market when plant modernization accelerates, and it may not fully separate fruit and vegetable lines from broader food processing equipment in mixed-use facilities. |

The table shows that year selection and the equipment boundary are the two biggest drivers of the gap. By keeping the scope tied to fruit and vegetable processing lines and by updating pricing and currency assumptions on a consistent cadence, the model stays traceable to real activity signals and can be repeated when new data appears.

Key Questions Answered in the Report

How fast is global demand for fruit and vegetable processing equipment growing?

The fruit and vegetable processing equipment market is expanding at a 6.24% CAGR from 2026 to 2031, reaching USD 11.8 billion by the end of the forecast period.

Which equipment type is projected to see the strongest growth through 2031?

Packaging and handling lines lead growth with a 7.71% CAGR as processors automate end-of-line operations to meet modified-atmosphere packaging and retailer hygiene standards.

What product segment offers the highest upside for equipment suppliers?

Frozen produce lines are advancing at an 8.52% CAGR thanks to IQF and cryogenic technologies that enable year-round supply of berries and vegetables.

Which region is expanding the fastest in equipment investment?

Middle East and Africa post the highest regional CAGR at 7.92% as UAE and Saudi Arabia invest heavily in post-harvest infrastructure to boost food self-sufficiency.

Page last updated on: