Non-Thermal Processing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.24 Billion |

| Market Size (2031) | USD 3.36 Billion |

| Growth Rate (2026 - 2031) | 8.43% CAGR |

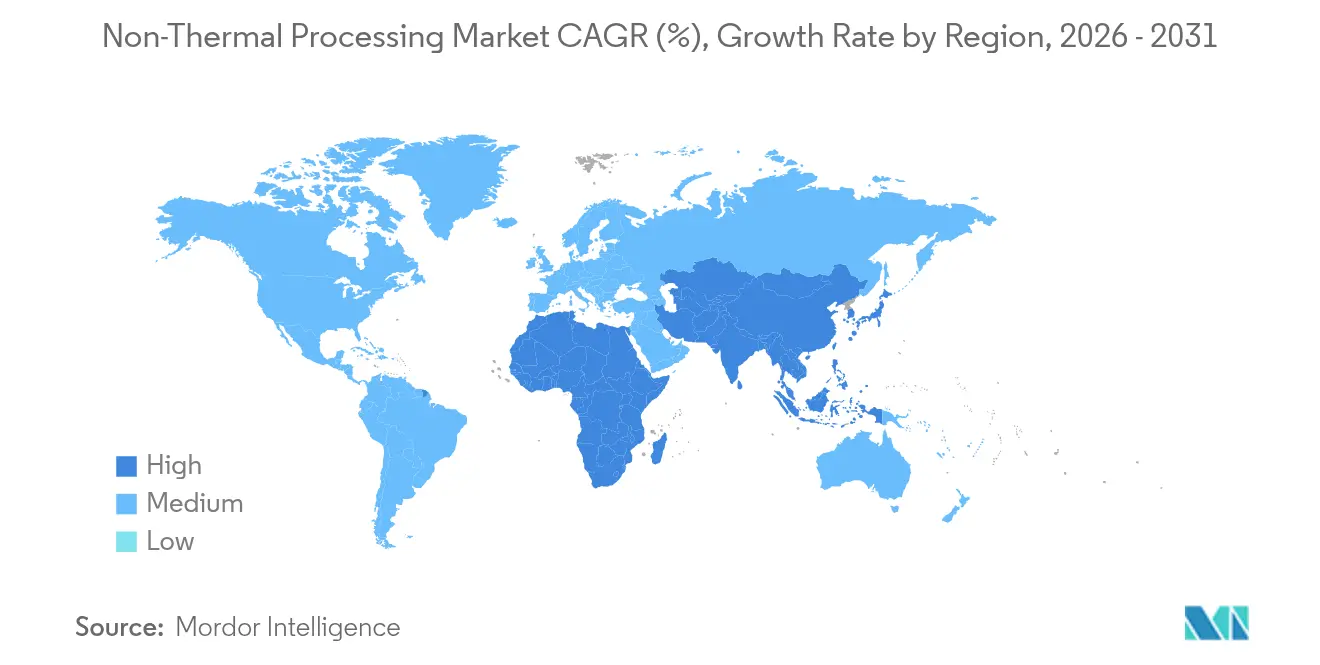

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

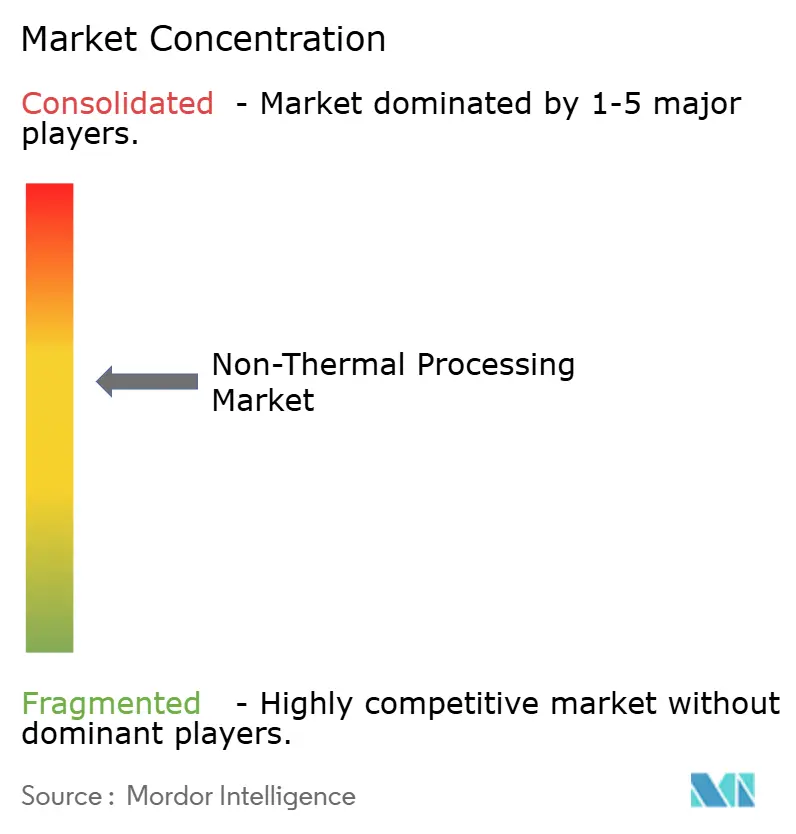

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-Thermal Processing Market Analysis by Mordor Intelligence

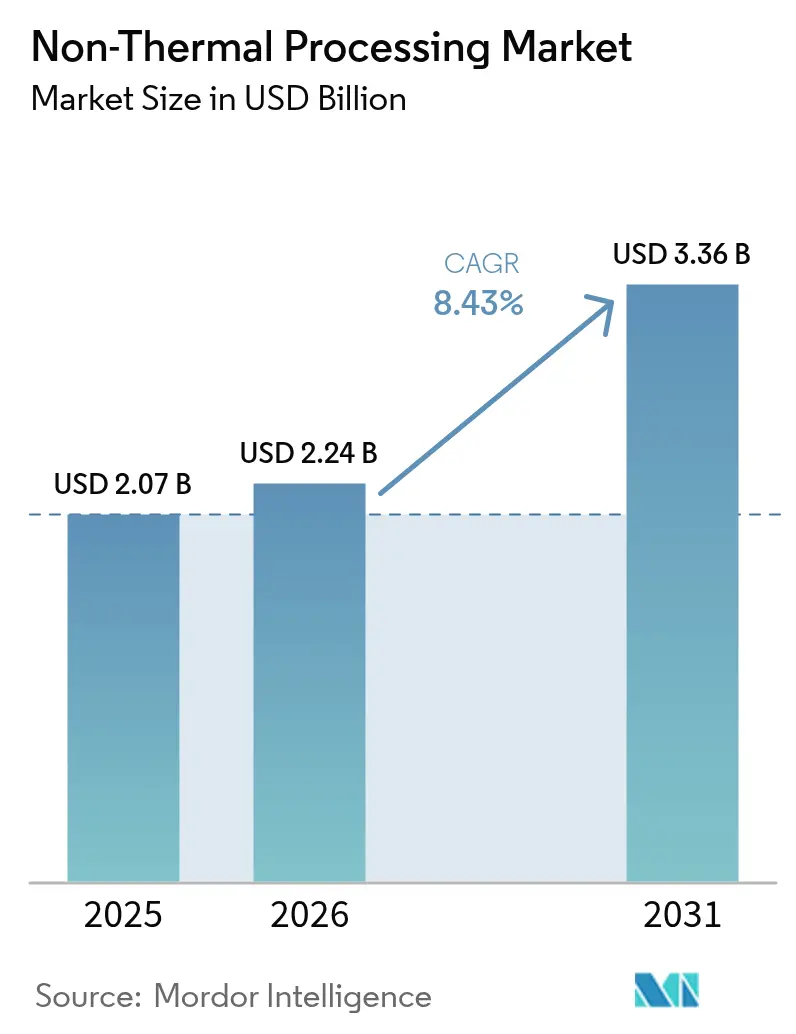

The non-thermal processing market size was valued at USD 2.07 billion in 2025 and estimated to grow from USD 2.24 billion in 2026 to reach USD 3.36 billion by 2031, at a CAGR of 8.43% during the forecast period (2026-2031). This trajectory reflects rising demand for clean-label foods, stricter global food-safety mandates, and proven commercial success of high-pressure processing in premium beverages. Regulatory updates such as the FDA’s 2024 Food Code supplement and the USDA’s declaration of Salmonella as an adulterant in poultry have accelerated technology uptake across meats, juices, and pet nutrition [1]Source: U.S. Food and Drug Administration, “Food Code Supplement 2024,” fda.gov. Equipment suppliers have responded with modular, fully automated systems that lower labor needs and enable predictive maintenance. Sustainability goals further reinforce adoption, as pulsed electric field and ultrasonic solutions cut energy use while safeguarding nutrients. Competitive intensity stays moderate, creating room for regional specialists and start-ups to partner with established leaders and widen the Non-Thermal Processing market footprint.

Key Report Takeaways

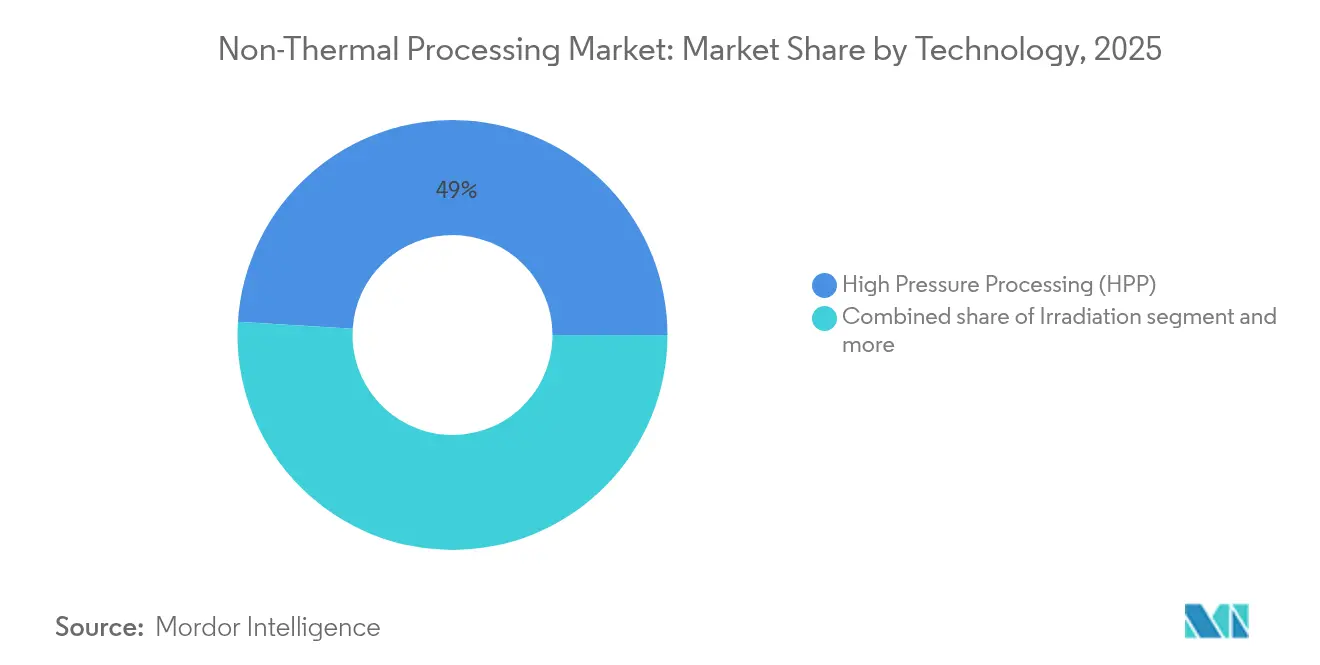

- By technology, high-pressure processing (HPP) led with 49.02% of the 2025 non-thermal processing market, while pulsed electric field (PEF) posts the fastest 10.12% CAGR through 2031.

- By application, food and beverages held a 94.88% share in 2025; pet food is projected to grow the quickest at 10.28% CAGR to 2031, especially in North America.

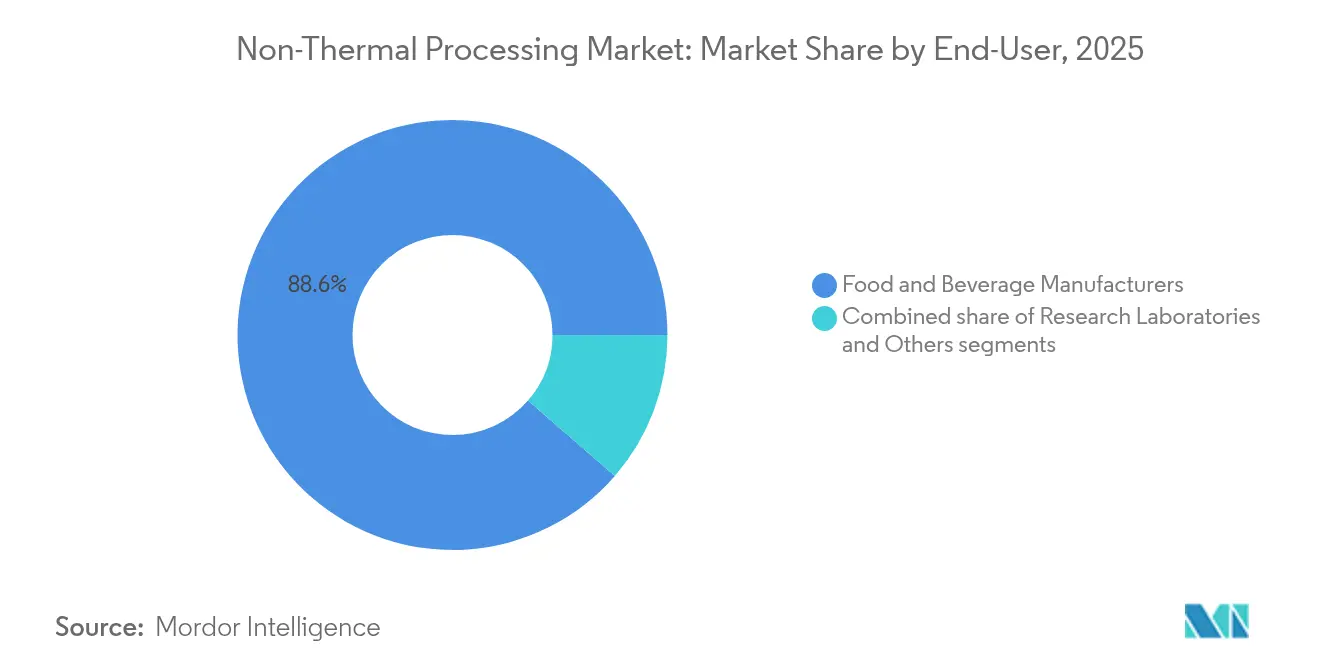

- By end-user, food and beverage manufacturers controlled 88.62% demand in 2025, whereas research laboratories are set to expand at 9.74% CAGR as governments fund process-validation work.

- By region, North America accounted for 40.78% of the non-thermal processing market size in 2025, and Asia-Pacific is forecast to register the highest 9.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Non-Thermal Processing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean-label and minimally processed items | +2.1% | North America, Europe strongest | Medium term (2-4 years) |

| Preservation of nutritional and sensory properties | +1.8% | Asia-Pacific emerging markets | Long term (≥ 4 years) |

| Growing focus on food safety and extended shelf life | +2.3% | Regulatory-driven in developed markets | Short term (≤ 2 years) |

| Technological advancements in equipment and automation | +1.5% | North America, Europe core; spill-over to Asia-Pacific | Medium term (2-4 years) |

| Rapid commercialization in beverages and meats | +1.2% | Early gains in North America, Europe | Short term (≤ 2 years) |

| Expansion of functional foods and nutraceuticals | +0.9% | Strongest in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for clean-label and minimally processed items

Food manufacturers are responding to consumers who want to know exactly what goes into their food, leading to higher prices for clean-label products in developed markets. The food industry has found success with pulsed electric field technology for clean-label production, which uses 90% less energy and water than traditional blanching methods while removing the need for chemical preservatives [2]Source: DLG, “Energy-Efficient Pulsed Electric Field Applications,” dlg.org. As regulations tighten and consumers continue to demand cleaner products, food companies are increasingly adopting non-thermal processing methods, especially in premium food categories. Manufacturers are finding that the investment in non-thermal processing equipment makes business sense, particularly when producing high-margin products like organic beverages and specialty meats, where clean-label positioning helps justify the costs.

Preservation of nutritional and sensory properties

Food manufacturers are increasingly adopting non-thermal processing technologies as these methods better preserve heat-sensitive vitamins, antioxidants, and bioactive compounds compared to traditional thermal methods. This advancement helps solve the long-standing challenge of nutritional loss during industrial food processing. Companies benefit from this technology's ability to maintain food taste and texture while extending product shelf life. For instance, baby food manufacturer GroGro implemented High-Pressure Processing (HPP) to produce products that taste homemade without using preservatives. As more consumers seek functional foods and nutraceuticals, food processors who utilize non-thermal technologies gain a competitive advantage by offering products with enhanced nutritional value.

Growing focus on food safety and extended shelf life

Regulatory agencies worldwide have strengthened pathogen control requirements. The USDA's 2024 framework classifies poultry products with Salmonella levels above 10 CFU/g as adulterants, increasing the demand for non-thermal processing solutions that reduce pathogens while maintaining product quality [3]Source: Food Safety and Inspection Service, “Salmonella Framework for Raw Poultry Products,” fsis.usda.gov. High-pressure processing achieves a 4-log reduction in Listeria monocytogenes and a 6-log reduction in Salmonella enterica, surpassing regulatory requirements. This technology also extends product shelf life by 2-4 times compared to untreated products. The combination of strict regulatory enforcement and liability concerns creates consistent demand for non-thermal processing technologies, especially in high-risk food categories where pathogen control affects brand reputation and market access. The food safety benefits, along with extended shelf life, allow manufacturers to minimize waste, expand distribution networks, and implement premium pricing for products with longer freshness periods.

Technological advancements in equipment and automation

Food processing equipment manufacturers continue to enhance operational efficiency and accessibility through improved systems. Hiperbaric's HPP systems now include automated material handling features that minimize labor needs and ensure consistent throughput. Pulsemaster has developed modular PEF systems with processing capacities from 1 to 60 tons per hour, allowing flexible implementation across different production settings while meeting hygiene requirements. In ultrasonic technology, Herrmann Ultraschall acquired exclusive rights to seal uncoated paper without adhesives, reducing environmental impact in packaging. The adoption of Industry 4.0 capabilities enables equipment monitoring and maintenance prediction, as demonstrated by Dukane's ultrasonic cutting systems that operate between 20-40 kHz for improved precision and reduced waste. These automation improvements have simplified operations and reduced technical expertise requirements, making non-thermal processing more accessible to small and medium-sized processors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital investment | -1.8% | Global, particularly impacting emerging markets | Medium term (2-4 years) |

| Limited packaging compatibility | -0.9% | Global, with stronger impact in developing regions | Short term (≤ 2 years) |

| Labelling and consumer-communication ambiguity | -0.7% | Global, particularly in consumer-direct segments | Medium term (2-4 years) |

| Scale-up challenges for particulate and solid foods | -1.1% | Global, with emphasis on industrial processing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High capital investment

Non-thermal processing equipment demands significant capital investment, with industrial-scale HPP systems and PEF installations requiring substantial funding. These high costs create barriers for small and medium-scale processors who dominate emerging markets. The capital requirements increase further when accounting for facility modifications, specialized packaging requirements, and operator training, which can significantly impact the total implementation investment. Research laboratories face additional constraints due to the high costs of pilot-scale equipment for comprehensive non-thermal processing capabilities, limiting technology validation and scale-up opportunities. Limited financing options specifically designed for food processing technology further compound the investment barrier, as traditional equipment financing models do not adequately address the specialized nature and extended payback periods of non-thermal processing systems. Market penetration remains constrained in price-sensitive segments where processors prioritize immediate cost reduction over long-term quality and safety benefits.

Limited packaging compatibility

Non-thermal processing technologies require specific packaging materials, which restrict options and increase costs, particularly affecting processors in developing regions where flexible packaging is prevalent due to cost considerations. High-pressure processing (HPP) requires materials that can withstand pressures up to 600 MPa, which eliminates rigid containers and limits design options. UV processing efficiency depends on packaging transparency and thickness, which restricts the use of multilayer barrier films commonly used for extended shelf life. This creates a trade-off between processing effectiveness and product protection. Export-oriented processors face additional challenges in balancing non-thermal processing requirements with international shipping standards that require robust, multi-barrier packaging. In emerging markets, limited access to specialized packaging materials affects technology adoption, despite favorable economic conditions for food processing investment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Established HPP Leadership Meets PEF Momentum

The food processing industry has witnessed significant adoption of high-pressure processing (HPP), which captured a substantial 49.02% market share in 2025. This technology has proven its worth across various food applications, while pulsed electric field (PEF) technology is emerging as a promising solution with a projected growth rate of 10.12% CAGR through 2031. The success of HPP can be attributed to its strong regulatory standing and widespread implementation in premium food segments, particularly in juices and ready-to-eat meals, where manufacturers can justify premium pricing through improved food safety and longer shelf life.

Despite a proven safety record, irradiation technology grapples with consumer resistance, limiting its application primarily to spice and herb processing. The market showcases a divide: while established players in High Pressure Processing (HPP) focus on enhancing operational efficiencies through advancements in equipment and process optimization, those pioneering Pulsed Electric Field (PEF) technology are venturing into plant-based protein processing and bioactive compound extraction. This exploration includes improving the extraction of nutrients and functional compounds, which are increasingly in demand due to the growing focus on health and wellness. These developments collectively signal a vibrant and transformative evolution within the industry.

By Application: Food and Beverages Maintain Dominance Amid Pet Food Surge

In 2025, the food and beverages industry dominates non-thermal processing applications, commanding a significant 94.88% market share. Within this realm, meat processing leads the charge, adapting to stringent regulations aimed at pathogen reduction and catering to a rising consumer appetite for minimally processed proteins. The adoption of non-thermal processing technologies in meat processing ensures compliance with food safety standards while retaining the natural texture and flavor of the products, which is increasingly important to health-conscious consumers. Meanwhile, the beverage sector has adeptly harnessed these technologies, especially in crafting HPP-treated cold-pressed juices and functional drinks, achieving a balance of commercial sterility and nutritional integrity. These advancements have allowed beverage manufacturers to meet consumer preferences for fresh, nutrient-rich products with extended shelf life.

Emerging as the industry's most vibrant segment, pet food is set to witness a robust CAGR of 10.28% extending to 2031. This surge is largely attributed to the industry's vigilant stance on food safety, especially in raw pet food production. By increasingly adopting HPP technology, manufacturers are not only curbing pathogens but also preserving the nutritional standards that discerning pet owners prioritize. The use of HPP in pet food production also aligns with the growing trend of premiumization in the pet food market, as consumers seek high-quality, minimally processed options for their pets. This demonstrates a dual commitment to safety and quality, ensuring that the products meet both regulatory requirements and consumer expectations.

By End-User: Manufacturers Lead While Research Labs Drive Innovation

In 2025, the food and beverage manufacturing industry commands a dominant 88.62% share of the non-thermal processing market. This stronghold is largely attributed to the industry's entrenched production infrastructure and commercial operations, which enable efficient scaling and consistent product quality. The sector's ability to integrate advanced non-thermal technologies into existing systems further reinforces its leadership position. On the other hand, research laboratories are rapidly gaining ground, emerging as the fastest-growing end-user segment with a projected CAGR of 9.74% through 2031. This growth is fueled by these labs bolstering their expertise in process optimization and technology validation, as they increasingly focus on developing innovative applications and enhancing the efficacy of non-thermal processing methods.

Large-scale food processors remain the primary adopters of HPP technology, as they can effectively justify the capital investment through volume-based economics. This has created opportunities for companies like JBT's Avure division, which reports growing demand for tolling services that help smaller manufacturers access HPP technology. In the research sector, laboratories are expanding their involvement through investments in bioprocessing scale-up and technology validation, particularly focusing on emerging applications such as cultivated meat production and alternative protein processing. Government initiatives, including NIST's investment in measurement science for manufacturing robotics, continue to support the adoption of HPP technology in research environments .

Geography Analysis

The North American market holds a commanding 40.78% share in 2025, establishing itself as the global leader in non-thermal processing technology. This dominance stems from well-established regulatory frameworks and widespread adoption of HPP technology across premium food segments. In the United States, clear FDA guidelines and USDA requirements for pathogen control have created a favorable environment for non-thermal processing adoption. The region's commitment to innovation is evident in developments such as Believer Meats' construction of large-scale cultivated meat facilities in North Carolina. Canada complements this growth through robust government support for food technology advancement and benefits from its strategic proximity to the United States' food processing hubs.

Asia-Pacific emerges as the frontrunner, eyeing a robust 9.98% CAGR through 2031. This surge is fueled by relentless industrialization and hefty investments in food processing infrastructure, which are driving advancements in production efficiency and product quality. China, with its government-backed initiatives, is bolstering its market stance, zeroing in on food safety and tech upgrades to meet both domestic and international demand. Japan, with its seasoned market, is pivoting towards premium applications, focusing on high-value products that cater to evolving consumer preferences. Meanwhile, Vietnam is making waves, highlighted by partnerships such as OctoFrost's collaboration with the Mekong Delta, which showcases the country's growing capabilities in adopting innovative processing technologies.

Europe, a bastion of stability, boasts a mature market underpinned by regulatory frameworks that champion non-thermal processing. The region shines brightest in the organic and premium food sectors, where consumers willingly pay a premium for advanced processing technologies that align with sustainability and health-conscious trends. The European Commission, with its progressive stance on novel food approvals, thinks UV-treated insect proteins are paving the way for broader non-thermal processing applications. This regulatory support, combined with a strong focus on innovation, positions Europe as a key player in driving the adoption of cutting-edge food processing methods.

Regulatory Landscape

Non-thermal processing adoption is shaped more by outcome-based food-safety requirements than by technology-specific licensing. In the United States, FDA updates such as the 2024 Food Code Supplement reinforce expectations around safe handling and validated controls, while FSIS oversight for meat and poultry emphasizes verified pathogen-reduction performance under HACCP-based systems, including verification activities for interventions such as high pressure processing and irradiation. The USDA-FSIS 2024 Salmonella framework for raw poultry, which treats products above defined contamination levels as adulterated, further raises the value of validated non-thermal lethality steps in poultry and other high-risk categories.

In Europe, foods and ingredients processed via novel methods can fall under the Novel Food framework, with EFSA and the European Commission applying Regulation (EU) 2015/2283 and related administrative guidance (updated through November 2025) when an authorization pathway is triggered. At the same time, many deployments of HPP, PEF, UV, and ultrasound proceed under general hygiene and food-safety rules (for example, HACCP and good hygiene practice requirements under Regulation (EC) No 852/2004). That approach pushes manufacturers to document microbial inactivation equivalency and maintain robust validation packages, rather than rely on a single harmonized, technology-specific approval.

Competitive Landscape

The non-thermal processing industry displays moderate concentration. Technology leaders in the non-thermal processing market hold their competitive positions through strong patent portfolios and deep customer relationships, while newer players carve out their market share by specializing in niche applications and expanding into different regions. Companies that provide end-to-end technology solutions and comprehensive service capabilities have an advantage, as customers increasingly look for complete solutions that bring together equipment, process improvements, and ongoing technical assistance.

With its well-established HPP equipment base and extensive tolling network, JBT Corporation continues to lead the market. Meanwhile, Hiperbaric builds its presence through innovation and worldwide expansion, supported by strategic partnerships and advanced automation solutions. Companies are differentiating themselves by developing more energy-efficient, automated, and flexible technologies. A good example is Pulsemaster, which has introduced modular PEF systems that can be easily scaled across different production settings.

Hybrid processing technologies, which blend various non-thermal methods, are unveiling fresh prospects, particularly in burgeoning sectors such as cultivated meat processing and alternative protein production. These technologies offer innovative solutions to address challenges like energy efficiency, product quality, and scalability in food production. A notable example is GEA's collaboration with Believer Meats, which is accelerating the adoption of bioreactor technology enhancements for cultivated meat production. This partnership highlights how cooperation between equipment manufacturers and food processors drives technological advancements and facilitates the swift market embrace of these innovations.

Non-Thermal Processing Industry Leaders

JBT Corporation

Hiperbaric

Thyssenkrupp Uhde GmbH

Nordion (Canada) Inc.

Universal Pure, LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Tolling and contract processing capacity expansion is a straightforward commercialization pathway for brands that want clean-label shelf-life extension but do not justify a full in-house line, and the latest large-format HPP deployments reinforce that gap. American Pasteurization Company installed a Hiperbaric 525 at its Milwaukee facility in February 2026, and Universal Pure added a Hiperbaric 525i system at its Malvern, Pennsylvania, site in November 2025. These additions indicate continued investment in shared-capacity models for refrigerated beverages, prepared foods, and emerging pet nutrition formats.

Beyond established HPP use cases, opportunities center on energy-efficient processing and control automation that help non-thermal methods work across more complex matrices. Recent work on SCADA-based PEF systems for seafood processing points to instrumented, real-time controllable non-thermal lines that target lower energy consumption and tighter process verification, matching manufacturer needs for repeatable lethality and quality retention. In Asia, supplier-backed localization also supports new greenfield installations, illustrated by Quintus Technologies supplying a QIF 600L press for WakeFresh in Anhui Province with an April 2026 installation timeline, which highlights the role of regional beverage and fresh food hubs in widening non-thermal processing footprints.

Recent Industry Developments

- February 2026: American Pasteurization Company installed a new Hiperbaric 525 high pressure processing system at its Milwaukee, Wisconsin, facility to expand HPP capacity for clean-label food and beverage customers. The added system increases available throughput for brands that outsource processing, supporting faster commercialization without immediate in-house capex.

- October 2025: Hiperbaric reported installing 30 HPP machines globally during 2025 and highlighted expansion of its tolling network through new partnerships. Higher installed base and service network density strengthen after-sales support and reduce adoption friction for processors standardizing HPP across multiple plants and regions.

- October 2024: Quintus Technologies launched the QIF 600L high pressure processing system featuring a 600-liter cycle capacity and an 18.5-inch pressure vessel diameter to improve load efficiency and throughput. Larger-batch capability and productivity gains support cost-per-unit reductions, helping HPP expand beyond premium niches into higher-volume processing lines.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers non-thermal processing solutions used to improve food and beverage safety and shelf life without using high heat. Spending is captured as the value of equipment and related solutions sold into end users.

Scope exclusions: Basic thermal pasteurization and standard heating or cooking steps are not counted. Downstream packaging-only services that do not include a non-thermal treatment are also excluded.

Segmentation Overview

- By Technology

- High Pressure Processing (HPP)

- Pulsed Electric Field (PEF)

- Ultraviolet (UV) Processing

- Ultrasonic Processing

- Irradiation

- Others

- By Application

- Food and Beverages

- Fruits and Vegetables

- Bakery and Confectionery

- Meat, Poultry, and Seafood

- Dairy and Dairy Alternatives

- Beverages

- Others

- Pet Food

- Others

- Food and Beverages

- By End-User

- Food and Beverage Manufacturers

- Research Laboratories

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- France

- United Kingdom

- Spain

- Netherlands

- Italy

- Sweden

- Poland

- Belgium

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

- Middle East and Africa

- United Arab Emirates

- South Africa

- Nigeria

- Saudi Arabia

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with locking the coverage boundaries, then building a clean list of demand signals that can be checked year after year. Public sources such as USDA and FDA references on food safety and processing controls, FAO food production series, UN Comtrade trade flows for relevant machinery categories, and World Bank macro indicators that explain food processing investments are reviewed first.

To convert these reference points into a workable model, we also use company annual reports, investor presentations, plant expansion announcements, and publications from industry associations focused on high pressure processing and comparable non-thermal methods. A paid subscription for company financials and news is used mainly to standardize revenue timing and reduce gaps in privately held disclosures. Patent databases are scanned to track where newer methods are being commercialized. These examples are not exhaustive, and other public sources were reviewed for collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test what the desk signals imply, especially around adoption pace and pricing movement across technologies such as high pressure processing and PEF. We interview equipment suppliers, integrators, food and beverage manufacturers, and technical experts across APAC, EMEA, and the Americas, and then adjust assumptions on utilization, replacement cycles, and service attachment where the responses differ from initial estimates.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 14% | APAC: 48% |

| Mid tier: 46% | Functional/Unit leaders: 37% | EMEA: 32% |

| Smaller Players: 15% | Managers: 49% | Americas: 20% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach, where regional food and beverage processing activity is reconstructed and then filtered through the realistic share of lines that can adopt non-thermal steps. Those demand pools are translated into market value using the technology mix and average selling price ranges validated through interviews.

We corroborate results with selective bottom-up approximations, including sampled supplier revenue roll-ups, channel checks, and installed base replacement logic. Market fingerprints are tracked closely because they show up directly in demand, for example packaged food and beverage production growth, capacity additions in high throughput processing plants, product-type adoption for heat-sensitive categories, typical equipment replacement cycles, and service and maintenance attach rates.

Where supplier disclosure is incomplete, gaps are handled by using comparable peer ranges, then narrowing them with regional shipment signals and interview feedback. Forecasts are produced using scenario analysis supported by regression-based checks on the main demand drivers, then adjusted based on expert expectations for regulatory scrutiny, clean label demand, and energy and cost pressures. Before finalizing, we check that the CAGR implied by the model aligns with practical capacity build-out and adoption constraints.

Data Validation & Update Cycle

Validation is done by triangulating model totals against independent signals such as regional food processing investment trends, trade movements for relevant machinery, and implied installed base growth needed to support the forecast. Outliers are flagged early, and when variance cannot be explained by scope or timing, we re-check assumptions and reconnect with selected respondents for clarification.

A multi-step review is then followed to ensure calculations, currency conversions, and price progression logic are internally consistent before sign-off. Reports are refreshed annually, and interim updates are triggered when major plant announcements, regulatory shifts, or sharp currency and inflation changes could move market value meaningfully. Just before delivery, an additional pass is completed so clients receive the latest view based on the most recent information available.

Mordor Intelligence's Global Non Thermal Processing Market Size Compared Against Other Published Estimates

Published market numbers for non-thermal processing can differ widely even when they cover similar technologies. Timing and pricing choices can change the reported value because studies vary in end-use coverage, how equipment prices are carried forward, and whether they model a nearer-term equipment cycle or a longer-term adoption story.

In this study, the refresh cadence and currency timing are handled conservatively, so year-to-year changes better reflect actual purchasing patterns rather than exchange-rate swings. ASP movement is checked against interview feedback before totals are locked, which is why the market size aligns the way it does for Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.24 B (2026) | |

| Industry Publisher A | USD 2.84 B (2025) | Uses a different base year and a longer forecast window, and it also appears to include adjacent applications beyond food processing, which can inflate the near-term total. |

| Market Advisory B | USD 2.55 B (2025) | Scope detail is less explicit in public extracts, and the value can shift based on how technology bundles and services are treated, along with the currency conversion timing used for global totals. |

Overall, the spread is mainly explained by year selection, what is counted around adjacent applications, and how pricing and currency are carried through the model. By keeping assumptions linked to observable adoption signals and re-validating ASP ranges during updates, the final figure remains traceable to steps that can be repeated as new data arrives.

Key Questions Answered in the Report

What is the current value of the Non-Thermal Processing market?

The market is valued at USD 2.24 billion in 2026 and is projected to climb to USD 3.36 billion by 2031 on an 8.43% CAGR.

Which technology leads the Non-Thermal Processing market?

High Pressure Processing commands 49.02% share, backed by widespread regulatory acceptance and commercial installations in beverages and meats.

Why is Asia-Pacific the fastest-growing region?

Rapid industrialization, improving food-safety regulations, and expanding middle-class demand for premium fresh foods drive a 9.98% CAGR in Asia-Pacific through 2031.

Which application segment is growing fastest?

Pet Food shows the highest momentum with 10.28% CAGR as premium raw diets require pathogen control without cooking.

Page last updated on: