Food Processing Machinery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 88.21 Billion |

| Market Size (2031) | USD 116.18 Billion |

| Growth Rate (2026 - 2031) | 5.67% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Food Processing Machinery Market Analysis by Mordor Intelligence

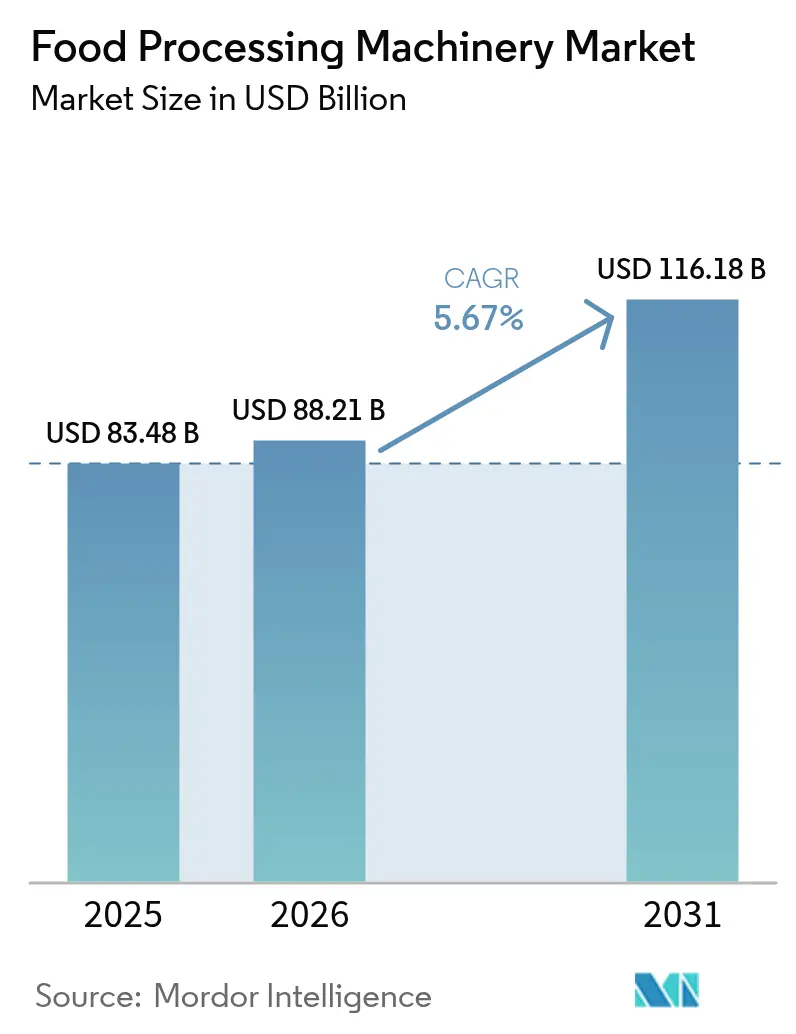

Food processing machinery market size in 2026 is estimated at USD 88.21 billion, growing from 2025 value of USD 83.48 billion with 2031 projections showing USD 116.18 billion, growing at 5.67% CAGR over 2026-2031. Steady modernization of plant floors, stricter hygiene regulations, and rising consumption of packaged foods underpin this growth trajectory. Processing machinery continues to command the largest revenue share because manufacturers view primary transformation equipment as the surest route to throughput gains and consistent product quality. Asia-Pacific’s industrial build-out, coupled with expanding middle-class purchasing power, accelerates regional demand for advanced systems that comply with evolving food-safety mandates. Automation remains pivotal; semi-automatic lines dominate current installations, yet smart and AI-enabled equipment records the fastest uptake as firms pursue predictive maintenance, resource efficiency, and real-time quality monitoring[1]Agriculture and Agri-Food Canada, “Ready Meals – United States,” agriculture.canada.ca. Competitive intensity stays moderate in a fragmented supplier base, enabling technology disruptors to win share with specialized, connected solutions.

Key Report Takeaways

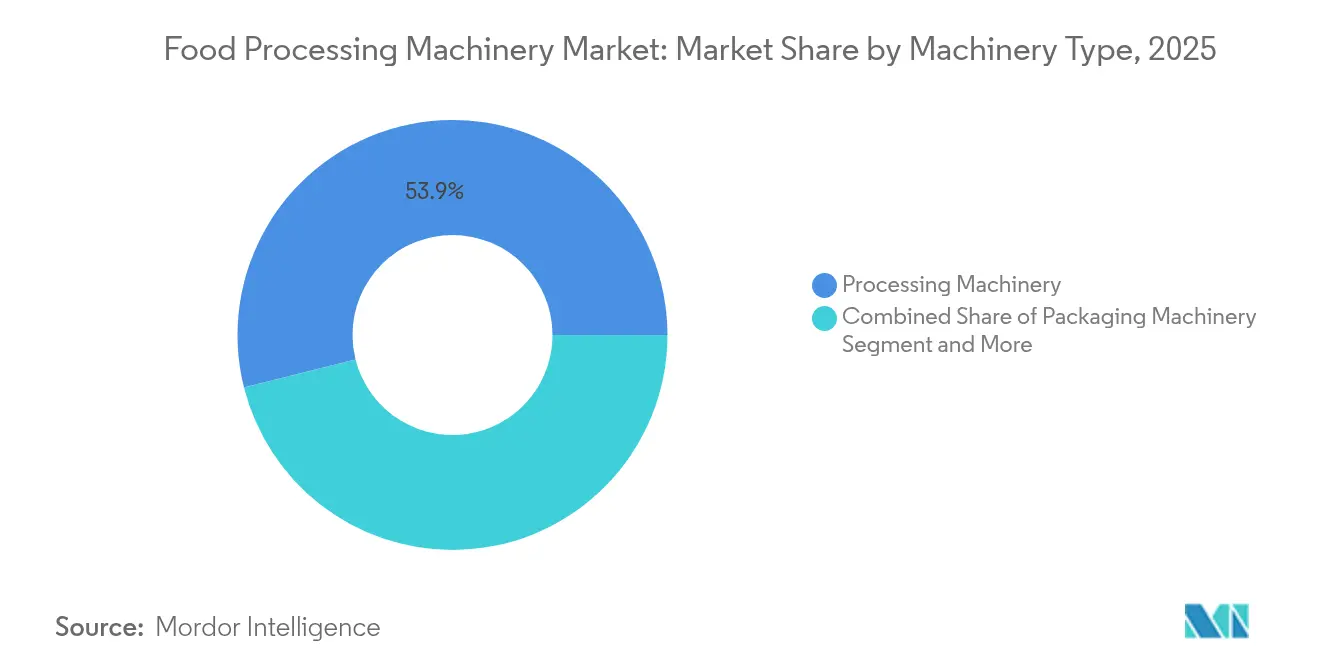

- By machinery type, processing equipment led the food processing machinery market with 53.92% market share in 2025 and is advancing at a 5.04% CAGR through 2031.

- By automation level, smart and AI-enabled systems are the fastest-growing segment with a 7.24% CAGR to 2031, while semi-automatic lines retained 46.73% of the 2025 revenue.

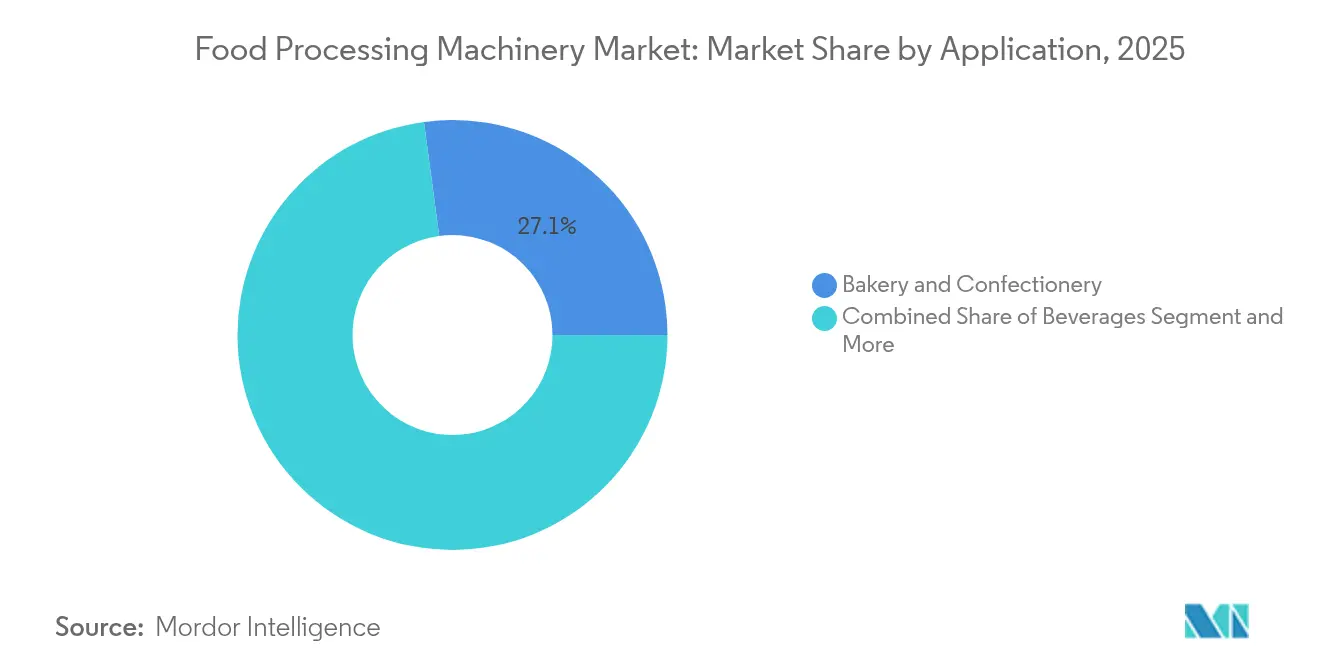

- By application, bakery and confectionery accounted for 27.12% of 2025 revenue, whereas meat, seafood, and meat-alternative processing is forecast to expand at a 6.12% CAGR through 2031.

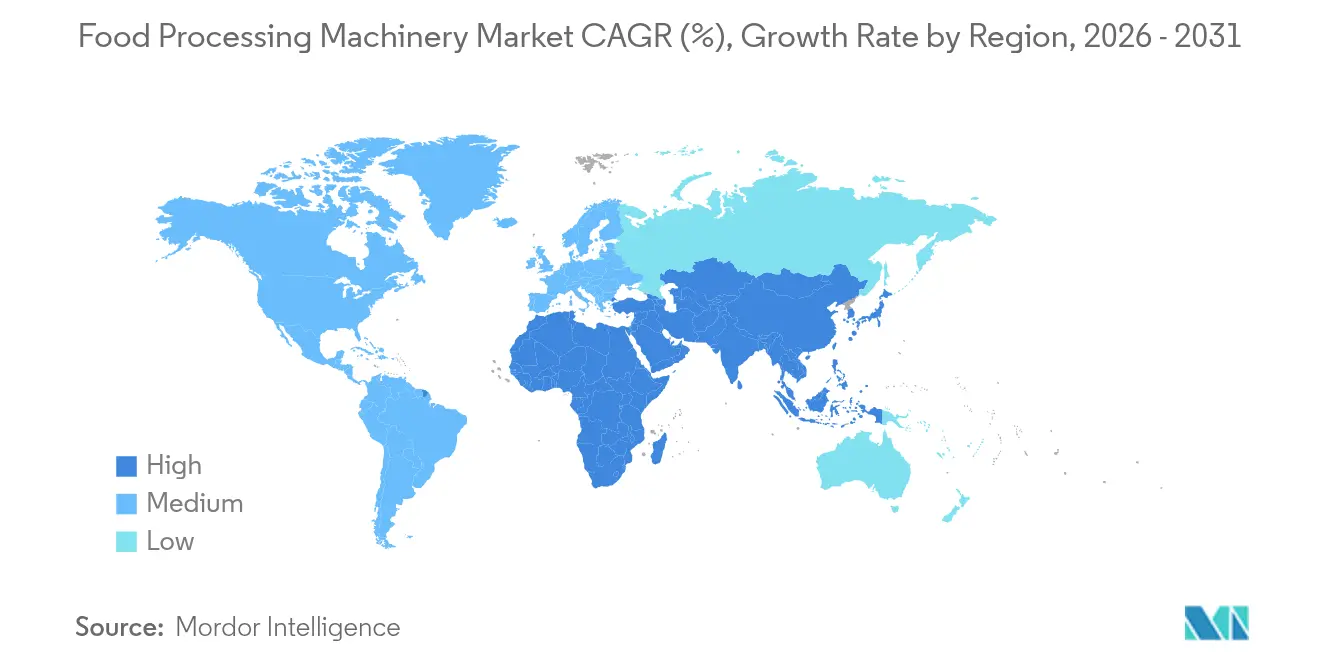

- By geography, Asia-Pacific accounted for 38.21% of 2025 sales and is set to grow at a 5.33% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Food Processing Machinery Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for processed and convenience foods | +1.2% | Global, with strongest impact in APAC and North America | Medium term (2-4 years) |

| Rapid automation and IIoT integration in plant floors | +0.9% | North America & EU leading, APAC following | Long term (≥ 4 years) |

| Stricter global food-safety and hygiene regulations | +0.8% | Global, with varying enforcement timelines | Short term (≤ 2 years) |

| Expanding food manufacturing capacity across APAC | +0.7% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Shift toward flexible small-batch lines for D2C and ghost kitchens | +0.6% | North America & EU urban centers | Short term (≤ 2 years) |

| Near-shoring incentives & tariff regimes in U.S./EU | +0.5% | North America & EU, with supplier impact in Mexico and Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Processed and Convenience Foods

Consumer lifestyle shifts toward convenience-oriented consumption patterns drive sustained equipment investment across processing and packaging segments. The U.S. ready meals market reached USD 63.3 billion with a 9.1% CAGR growth, creating upstream demand for flexible processing lines capable of handling diverse product formulations and packaging formats. This trend particularly benefits manufacturers offering modular systems that accommodate rapid product changeovers without extensive reconfiguration. Ghost kitchen operators increasingly specify compact, ventless equipment solutions that maximize space utilization while enabling multi-concept food preparation, as demonstrated by Alto-Shaam's Vector H Series Multi-Cook Oven powering Virtual Chef Hall's seven-concept operations[2]Alto-Shaam, “Ghost Kitchen Solutions,” alto-shaam.com. The convergence of delivery-focused business models with advanced processing technology creates new market segments for equipment suppliers targeting urban commissary operations.

Rapid Automation and IoT Integration in Plant Floors

Manufacturing intelligence platforms transform food processing from reactive maintenance toward predictive operational models that optimize equipment utilization and product quality. Rockwell Automation's FactoryTalk Analytics platform enables real-time monitoring of processing parameters, reducing unplanned downtime by up to 30% while improving overall equipment effectiveness. This technological shift particularly impacts high-volume processing environments where marginal efficiency gains translate to significant cost savings. Smart processing equipment increasingly incorporates edge computing capabilities that enable local decision-making without relying on cloud connectivity, addressing latency concerns in time-sensitive operations. The integration of artificial intelligence in food processing machinery, exemplified by Chef Robotics' AI-enabled depositing systems achieving greater than 30% improvement in consistency and yield, demonstrates how machine learning algorithms optimize portion control and reduce food waste[3]Chef Robotics, “AI-Enabled System,” chefrobotics.ai.

Stricter Global Food-Safety and Hygiene Regulations

Regulatory frameworks increasingly mandate equipment design standards that prioritize contamination prevention and traceability throughout processing operations. The FDA's Food Safety Modernization Act (FSMA) Preventive Controls Rule requires food facilities to implement hazard analysis and risk-based preventive controls, driving demand for equipment with built-in monitoring and documentation capabilities. FSIS directive 5000.6 mandates enhanced sanitation standard operating procedures, compelling meat and poultry processors to invest in equipment designed for efficient cleaning and sanitization cycles. Equipment manufacturers respond by incorporating features like automated cleaning-in-place (CIP) systems and hygienic design principles that eliminate potential contamination points. The convergence of regulatory compliance with operational efficiency creates market opportunities for suppliers offering integrated solutions that simultaneously address safety requirements and productivity objectives.

Expanding Food Manufacturing Capacity Across APAC

Infrastructure investment across Asia-Pacific markets creates substantial demand for processing equipment as multinational food companies establish regional production capabilities. Cargill's expansion of its Gresik, Indonesia, facility with new cocoa production lines exemplifies the strategic capacity additions occurring throughout Southeast Asia. FPS Food Process Solutions' establishment of a 463,000-square-foot Asia Pacific headquarters in China demonstrates the company's commitment to supporting regional manufacturing growth. This geographic expansion coincides with rising domestic consumption and export-oriented production strategies that require advanced processing capabilities. Local content requirements and import substitution policies in key APAC markets favor equipment suppliers with regional manufacturing and service capabilities, creating a competitive advantage for companies that invest in a local presence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex and opex of advanced hygienic machinery | -1.1% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Escalating energy and skilled-labor costs | -0.8% | North America & EU primarily | Medium term (2-4 years) |

| Semiconductor & sensor shortages delaying deliveries | -0.6% | Global supply chain impact | Short term (≤ 2 years) |

| Cyber-security risks in connected processing equipment | -0.4% | Developed markets with high connectivity adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex and Opex of Advanced Hygienic Machinery

Investment barriers for sophisticated processing equipment create market segmentation between large-scale manufacturers and smaller operators seeking cost-effective automation solutions. Advanced hygienic design requirements, including 316L stainless steel construction and specialized surface finishes, significantly increase equipment costs compared to standard industrial machinery. GEA's introduction of entry-level thermoforming machines specifically targets small and medium-sized companies seeking advanced packaging capabilities without the capital commitment of high-end systems. Operating expenses compound initial investment challenges, as specialized cleaning chemicals, validation procedures, and maintenance protocols require ongoing financial commitments. This cost structure particularly impacts emerging market manufacturers who must balance automation benefits against capital constraints, creating opportunities for equipment suppliers offering flexible financing and leasing models.

Escalating Energy and Skilled-Labor Costs

Rising operational expenses force manufacturers to prioritize equipment investments that deliver measurable returns through energy efficiency and labor reduction. Australian food manufacturers face electricity price increases of 22-50%, compelling investment in energy-efficient processing technologies that reduce per-unit production costs. Skilled technician shortages across developed markets create additional pressure for automated systems that reduce dependency on specialized labor while maintaining operational consistency. Equipment manufacturers respond by incorporating energy management features and simplified operation interfaces that enable less-experienced operators to manage complex processing tasks. The convergence of energy and labor cost pressures accelerates the adoption of smart equipment that optimizes resource utilization through predictive algorithms and automated parameter adjustment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Processing Dominance Drives Innovation

Processing equipment captured 53.92% of 2025 revenue within the food processing machinery market, reflecting manufacturers’ focus on core value generation. Thermal, non-thermal, and extrusion technologies form the backbone of capacity expansions and recorded a 5.04% CAGR outlook. Bühler’s SmartLine release, including the DirectBake Smart oven produced in India, tailors high-end combustion and recipe controls to local price points. Packaging machinery ranks second in revenue yet increasingly integrates with upstream processes through unified controls that synchronize fill rates, sealing temperatures, and label feeds. Utilities such as CIP skids, waste-handling units, and HVAC systems tie into overarching plant-wide dashboards that analyze water, energy, and chemical consumption. This linkage illustrates how the food processing machinery market is moving from machine-level performance to holistic line optimization.

Demand for flexible, small-batch thermal systems rises alongside D2C brands and ghost kitchens that prioritize rapid changeovers. At the other end of the scale, mega-plants order high-throughput evaporators, UHT units, and aseptic fillers to serve export channels. Suppliers that modularize heat exchangers, pumps, and valve manifolds allow processors to phase investments over multiple budget cycles, keeping adoption on track even when cash flows fluctuate. As cyber-secure PLCs and industrial Ethernet become standard, equipment interoperability becomes a competitive requirement rather than a luxury.

By Automation Level: Smart Systems Reshape Operations

Semi-automatic lines held 46.73% of 2025 global revenue, mirroring the installed base in medium-sized bakeries, breweries, and meat plants that still depend on operators for inspection and adjustment. Nonetheless, smart and AI-enabled equipment is forecast to grow at 7.24% annually, outpacing every other automation segment. Chef Robotics’ AI portioning platform, which lifted yield by more than 30%, signals the performance leap achievable when machine learning algorithms guide depositor stroke length and speed.

Manual workstations survive in craft chocolate, artisanal cheese, and microbrewery settings where tactile quality cues are impossible to automate. Fully automatic systems dominate high-volume snack, beverage, and dairy plants thanks to synchronized conveyors, pick-and-place robotics, and inline QC sensors. Retrofit-ready sensors, vision cameras, and cloud gateways enable older semi-automatic units to feed data to central dashboards without full replacement. This path lowers capital hurdles and sustains the food processing machinery market by lengthening product life cycles. As predictive algorithms spot wear patterns early, maintenance windows shrink and overall equipment effectiveness rises.

By Application: Protein Processing Accelerates Growth

Bakery and confectionery applications led 2025 revenue with a 27.12% share, underscoring the maturity of bread, biscuit, and chocolate lines worldwide. High-output tunnel ovens, continuous tempering machines, and rotary molders keep this segment attractive because standardized recipes lend themselves to automation. Bühler’s Mondomix batch cooker illustrates the advanced thermal control now typical in confectionery cookers. Meanwhile, meat, seafood, and meat-alternative processing is projected to post a 6.12% CAGR as consumers diversify protein intake. Specialized equipment such as low-pressure forming dies for plant-based burgers, high-pressure pasteurization units for deli meats, and intelligent portion cutters for fish loins anchors this surge.

Dairy and dairy-alternative lines benefit from shared technologies such as membrane filtration and enzymatic texturizing, while beverage processors emphasize aseptic cold-fill and carbonation precision. Ready-meal facilities deploy multi-zone cooking kettles and rapid-cool spiral freezers to meet foodservice deadlines. The expanding product mix generates opportunity for multi-purpose cook-chill, mixing, and packaging centers that can swing between proteins, sauces, and plant-based analogues with minor adjustments.

Geography Analysis

In 2025, the Asia-Pacific region is projected to contribute 38.21% to global revenue and is set to grow at a CAGR of 5.33%. This underscores the region's pivotal role in global capacity expansion. Factors such as surging food exports, urban consumption, and government incentives for modernizing domestic processing bolster the region's growth. Multinational giants, including Cargill in Indonesia and Lonza in India, are broadening their localized manufacturing to cater to both domestic markets and nearby export corridors. Procurement teams in the region are increasingly favoring machinery suppliers who offer shorter lead times, local spare parts, and swift after-sales service. This trend fuels demand for modular systems, automated inspection technologies, and continuous processing lines, all tailored to the region's unique crop and livestock profiles.

North America is focusing on optimizing its existing infrastructure instead of pursuing greenfield expansions. Processors are channeling investments into digital retrofits, predictive maintenance systems, and energy-efficient upgrades. Rising tariffs on steel and aluminium, leading to a 25% spike in equipment fabrication costs—are nudging buyers to turn to regional OEMs or global firms with U.S.-based assembly units. The market is witnessing a robust adoption of robotics for tasks like portioning, packaging, and sanitation. This shift is largely driven by labor shortages, stringent hygiene standards, and the challenge of managing production variability across diverse product SKUs.

In South America, the Middle East, and Africa, there's a concerted push to establish foundational food processing infrastructure. This initiative aims to bolster food security, curtail post-harvest losses, and invigorate rural agro-industrial value chains. Innovations like mobile fruit processing units, containerized dairy lines, solar-powered dehydrators, and low-pressure poultry scalders are being deployed. These technologies are especially beneficial in areas with limited cold-chain access and inconsistent grid connectivity. While government-backed modernization grants and public-private partnerships are aiding small and mid-sized processors in upgrading their equipment, challenges like foreign exchange volatility and a reliance on imports are causing delays in machinery orders. Nevertheless, the overarching goal in these regions remains clear: to bridge critical capacity gaps, enhance local value addition, and align supply with the growing domestic demand.

Competitive Landscape

The food processing machinery market, with a concentration score of 3 out of 10, reflects high supplier fragmentation, as many players hold single-digit market shares. Leading multinationals like Bühler AG, GEA Group, and Tetra Laval leverage their global reach, extensive portfolios, and life-cycle services to dominate tier-one processors. Mid-tier competitors are consolidating, exemplified by the January 2025 JBT-Marel merger, which created a USD 3 billion entity focused on protein capabilities.

Digital differentiation has become a critical competitive factor, with vendors offering predictive-maintenance dashboards, OEE benchmarking, and secure remote assistance to reduce downtime and service costs. Additionally, the adoption of cyber-secure designs aligned with IEC 62443 standards has gained traction following high-profile ransomware incidents.

Energy-efficient platforms are increasingly positioned as premium offerings. For instance, Tetra Pak's 2025 protein mixer line claims 25% energy savings through heat-recovery coils, addressing rising utility tariffs. Meanwhile, niche players are integrating robotics, AI vision, and 3D printing for change parts to serve small-batch, high-value segments such as plant-based cheese and functional beverages. These advancements highlight the industry's focus on innovation to meet evolving consumer demands and operational challenges.

Food Processing Machinery Industry Leaders

Bühler AG

Tetra Laval

GEA Group AG

John Bean Technologies

Krones AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The Rolinson Group has announced its official launch, with the slogan "Food Processing from Start to Finish." Led by Graeme Rolinson, the company aims to deliver top-tier industrial food processing equipment to food businesses in the UK.

- June 2024: Tummers Food Processing Solutions and Kiron Food Processing Technologies have launched a new joint venture, Tummers Kiron India Pvt. Ltd., based in Mumbai, India. The venture was announced at Inter Food Tech in New Delhi and will initially function as a sales office and warehouse to serve the Indian market with equipment and spare parts.

- March 2024: GEA launched a real-time monitoring solution for food processing technology at the Anuga FoodTec trade show, scheduled to take place in Cologne, Germany, from March 19 to 22, 2024. The solution has been designed to support all food processing and packaging plants in achieving key production goals, including maximizing machine availability, minimizing downtime, preventing unplanned shutdowns, and managing resources efficiently.

Global Food Processing Machinery Market Report Scope

The food processing machinery market is a large and complicated market that includes all of the machines and equipment used in commercial food production and packaging. The global food processing machinery market is segmented by type, application, and geography. By type, the market studied is segmented into processing machinery and equipment, packaging machinery and equipment, and utilities. By application, the market studied is segmented into dairy and dairy alternatives, meat/seafood and meat/seafood alternatives, bakery and confectionery, beverages, fruits, vegetables and nuts, and other applications. The report also provides an analysis of the emerging and established geographical regions by covering regions such as North America, Europe, Asia-Pacific, South America, and the Middle East and Africa.

The report offers market size and forecasts in value in USD terms for the abovementioned segments.

| Processing Machinery | Primary Processing |

| Thermal Processing | |

| Non-Thermal Processing | |

| Extrusion and Forming Systems | |

| Packaging Machinery | Primary Packaging |

| Secondary Packaging | |

| End-of-Line packaging | |

| Vacuum / MAP / Aseptic Systems | |

| Utilities and Ancillary Systems |

| Manual |

| Semi-Automatic |

| Fully Automatic |

| Smart and AI-Enabled |

| Bakery and Confectionery |

| Meat/Seafood and Meat-Alternative |

| Dairy and Dairy-Alternative |

| Beverages |

| Fruits, Vegetables & Nuts |

| Ready Meals and Meal Kits |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Machinery Type | Processing Machinery | Primary Processing |

| Thermal Processing | ||

| Non-Thermal Processing | ||

| Extrusion and Forming Systems | ||

| Packaging Machinery | Primary Packaging | |

| Secondary Packaging | ||

| End-of-Line packaging | ||

| Vacuum / MAP / Aseptic Systems | ||

| Utilities and Ancillary Systems | ||

| By Automation Level | Manual | |

| Semi-Automatic | ||

| Fully Automatic | ||

| Smart and AI-Enabled | ||

| By Application | Bakery and Confectionery | |

| Meat/Seafood and Meat-Alternative | ||

| Dairy and Dairy-Alternative | ||

| Beverages | ||

| Fruits, Vegetables & Nuts | ||

| Ready Meals and Meal Kits | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Food Processing Machinery Market?

The Food Processing Machinery Market size is expected to reach USD 88.21 billion in 2026 and grow at a CAGR of 5.67% to reach USD 116.18 billion by 2031.

Which is the Largest Application for Food Processing Machinery Market?

Bakery and confectionery is the largest application segment for the Food Processing Machinery Market with 27.12% market share in 2025.

Who are the key players in Food Processing Machinery Market?

Bühler AG, Tetra Laval, GEA Group AG, John Bean Technologies, and Krones AG are the major companies operating in the Food Processing Machinery Market.

Which is the fastest growing region in Food Processing Machinery Market?

Asia Pacific is estimated to grow at the highest CAGR of 5.33 % over the forecast period (2026-2031).

Page last updated on: