Market Overview

| Study Period | 2021 - 2031 |

|---|---|

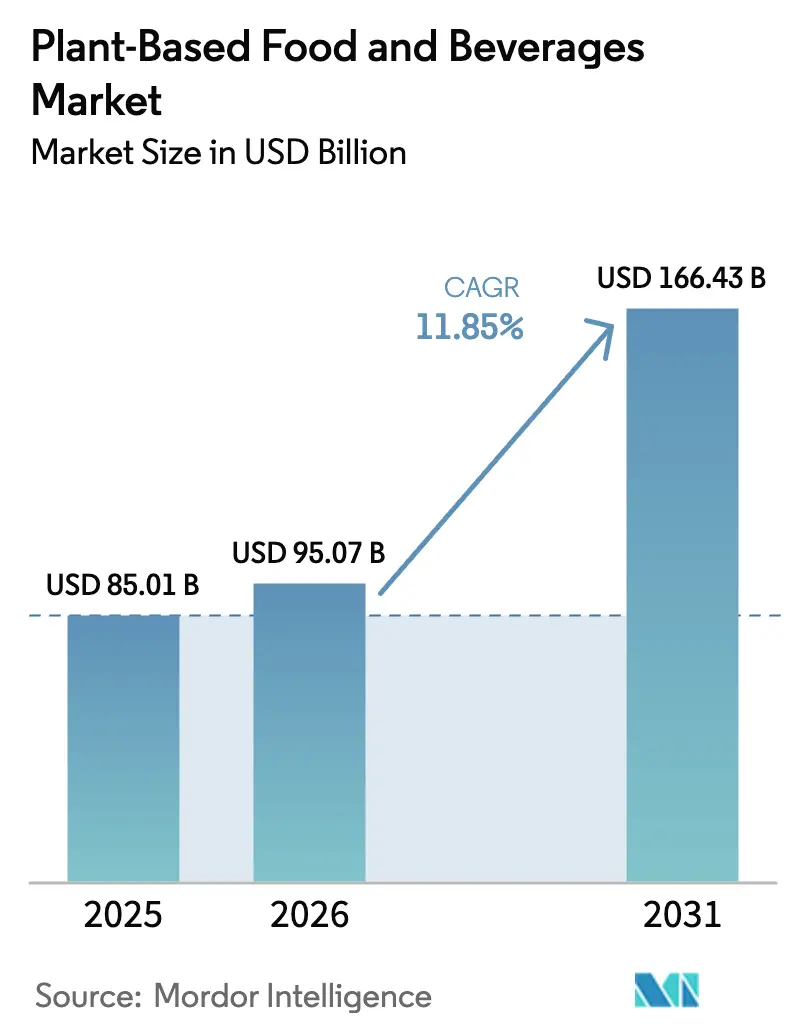

| Market Size (2026) | USD 95.07 Billion |

| Market Size (2031) | USD 166.43 Billion |

| Growth Rate (2026 - 2031) | 11.85% CAGR |

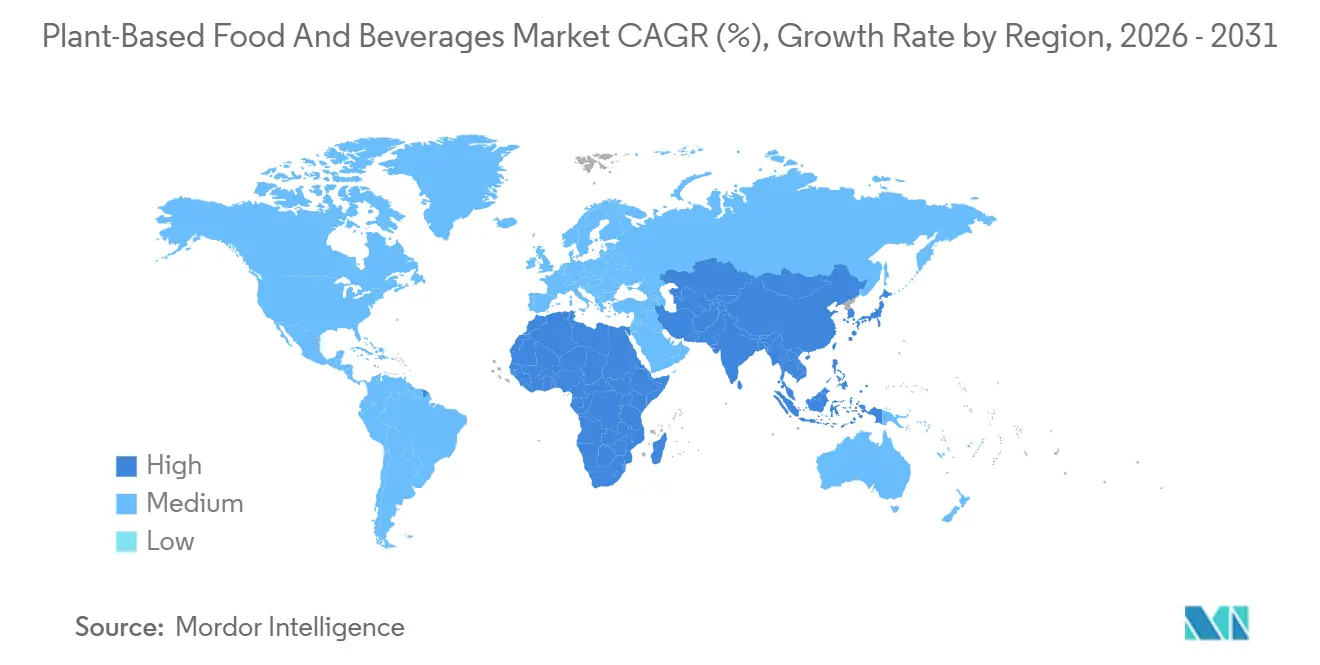

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

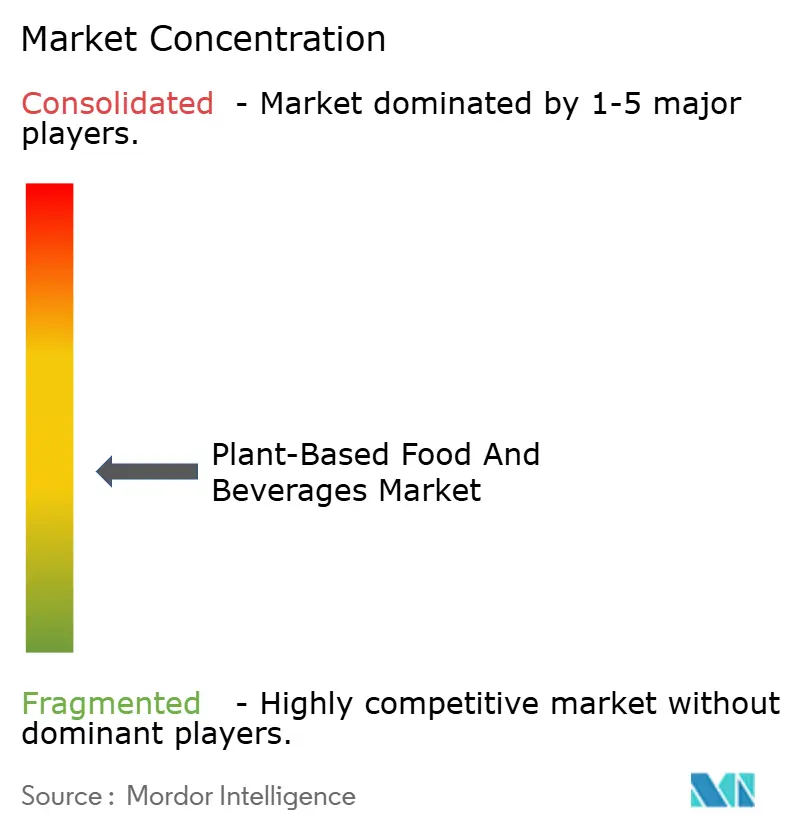

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Plant-Based Food And Beverages Market Analysis by Mordor Intelligence

The plant-based food and beverages market size is projected to expand from USD 85.01 billion in 2025 and USD 95.07 billion in 2026 to USD 166.43 billion by 2031, registering a CAGR of 11.85% between 2026 to 2031. The growing adoption of flexitarian diets in North America and Europe is significantly driving market growth. In the Asia-Pacific region, the increasing prevalence of lactose intolerance is boosting demand for plant-based alternatives. The Gulf states are witnessing a surge in halal-certified product launches, further contributing to market expansion. Innovations in ingredients, such as precision-fermented heme and barista-grade oat emulsions, are improving taste profiles, encouraging repeat purchases. Supermarkets are reorganizing shelves to place plant-based products alongside conventional dairy and meat, making them more accessible to consumers. Furthermore, quick-service restaurant chains are reintroducing plant-based options, creating more opportunities for consumers to try these products. The market remains fragmented.

Key Report Takeaways

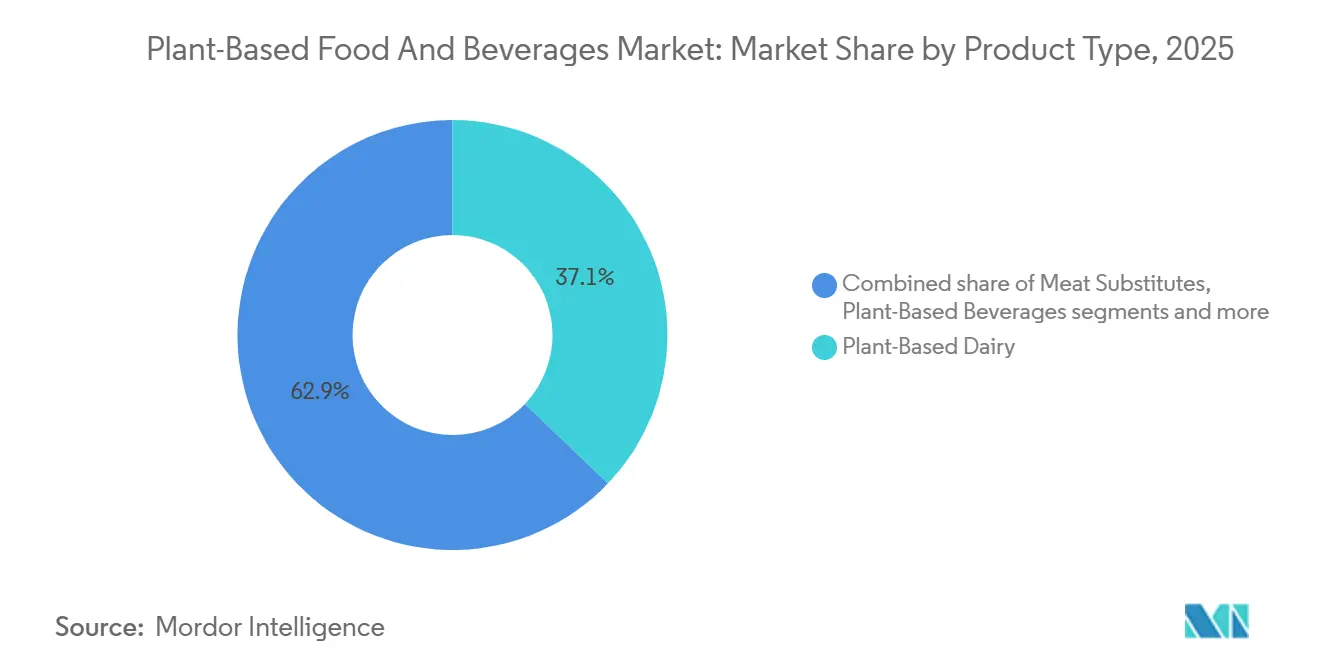

- By product type, plant-based dairy led with 37.12% revenue share in 2025; meat substitutes are projected to expand at a 12.61% CAGR through 2031.

- By ingredient source, soy accounted for 39.55% of 2025 revenue, whereas oat is set to grow at a 13.03% CAGR through 2031.

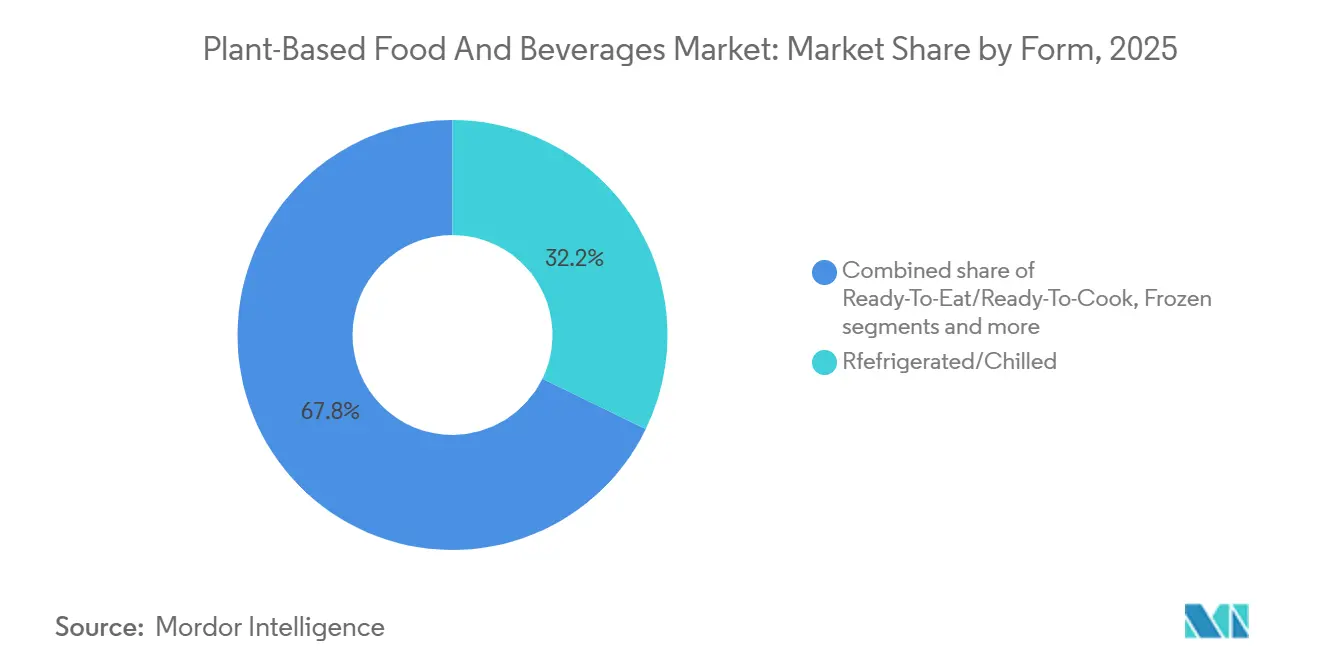

- By form, refrigerated and chilled items accounted for 32.21% of 2025 sales, yet ready-to-eat and ready-to-cook formats are forecast to grow at a 13.46% CAGR through 2031.

- By distribution channel, off-trade accounted for 71.82% of 2025 revenue, while on-trade is expected to rise at a 13.13% CAGR to 2031.

- By geography, Asia-Pacific held 35.84% of the 2025 turnover; the Middle East and Africa are poised for the fastest 12.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Plant-Based Food And Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of flexitarian and vegetarian lifestyles | +2.8% | Global, with highest penetration in North America and Europe | Medium term (2-4 years) |

| Increasing prevalence of lactose intolerance and food allergies | +2.1% | Asia-Pacific core (68% population lactose intolerant), spill-over to global markets | Long term (≥ 4 years) |

| Rising ethical concerns related to animal welfare supporting long-term adoption | +1.6% | North America, Europe, Australia | Long term (≥ 4 years) |

| Continuous innovation in plant-based formulations improving taste, texture, and nutritional profiles | +2.4% | Global, led by Research and Development hubs in North America and Europe | Short term (≤ 2 years) |

| Growing awareness of environmental impact of animal agriculture | +1.9% | Europe, North America, with emerging awareness in Asia-Pacific | Medium term (2-4 years) |

| Consumer focus on health and wellness increasing demand for foods perceived as lower in cholesterol, saturated fat, and artificial ingredients | +2.2% | Global, strongest in high-income markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of flexitarian and vegetarian lifestyles

The rise in flexitarian and vegetarian lifestyles has become a key driver of the plant-based food and beverage market. More consumers are now choosing to include plant-based options in their daily diets without completely giving up meat. In 2024, ProVeg International reported that approximately 40% of Europe’s population identified as flexitarian, highlighting a growing trend of reduced meat consumption[1]Source: ProVeg International, "Capture Europe’s Biggest Flexitarian Audience by Understanding German Consumers", proveg.org. This shift has pushed retailers and foodservice providers to broaden their plant-based product offerings, integrating them into mainstream categories rather than restricting them to niche sections. For example, well-known quick-service restaurant chains and retail brands have begun adding permanent plant-based menu items and expanding their product ranges to meet this changing demand. Increasing consumer awareness about health benefits, environmental sustainability, and the need for dietary variety continues to fuel the growth of plant-based food and beverage consumption worldwide.

Increasing prevalence of lactose intolerance and food allergies

The increasing prevalence of lactose intolerance and food allergies is a major driver of the global plant-based food and beverage market. In 2025, data from the World Population Review showed that some countries, including the Democratic Republic of Congo, Vietnam, South Korea, Yemen, and Mozambique, reported lactose intolerance rates of up to 100%[2]Source: World Population Review, "Lactose Intolerance by Country 2025", worldpopulationreview.com. This highlights a significant demand for dairy-free alternatives. Plant-based beverages like oat milk, almond milk, and soy milk have become popular choices as they provide similar functionality to dairy products without causing digestive issues. To meet this growing demand, manufacturers are developing fortified, allergen-friendly products to cater to consumers with dietary sensitivities. Increasing health awareness and the rising preference for dairy alternatives are further boosting the adoption of plant-based food and beverages worldwide.

Rising ethical concerns related to animal welfare are supporting long-term adoption

Concerns about animal welfare are becoming a major driver of the plant-based food and beverage market. Many consumers are now actively seeking cruelty-free food options that align with their ethical beliefs. The American Humane Farm Survey 2024 found that 72% of respondents are worried about the treatment of animals on farms, showing a clear demand for more humane and ethical practices in food production[3]Source: American Humane Org, "American Humane Farm Survey", americanhumane.org. This growing awareness has led to a noticeable shift toward plant-based alternatives, as these products do not involve animal exploitation and are considered more ethical. In response to this trend, retailers and food manufacturers are increasing their focus on plant-based product offerings. They are introducing a wider range of options to cater to consumers who prioritize animal welfare and ethical considerations in their purchasing decisions.

Continuous innovation in plant-based formulations is improving taste, texture, and nutritional profiles

Advancements in product formulation are playing a key role in improving the taste and texture of plant-based food and beverages, making them more appealing to consumers. A 2025 blind tasting conducted by the NECTAR consortium found that only about one-third of plant-based alternatives matched the taste and texture of traditional animal-based products. This finding underscores the need for continuous research and development in the sector. Companies like Impossible Foods are using innovative techniques, such as precision fermentation, to create heme and casein analogs. These ingredients help mimic the savory umami flavor and melting properties found in animal-based foods. Additionally, improvements in texturized vegetable protein technology now enable the creation of fibrous, whole-muscle alternatives for a variety of applications beyond plant-based burgers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited consumer awareness and understanding of plant-based nutrition | -1.4% | Emerging markets in Asia-Pacific, Middle East and Africa, and Latin America | Medium term (2-4 years) |

| Rising incidence of soy, nut, and gluten allergies limiting consumer adoption | -1.2% | Global, with highest impact in North America and Europe | Long term (≥ 4 years) |

| Higher prices of plant-based products compared to conventional animal-based alternatives | -2.1% | Global, most acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Regulatory ambiguity around labeling terms such as milk, cheese, and meat | -0.9% | North America, Europe, with emerging debates in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited consumer awareness and understanding of plant-based nutrition

Low consumer awareness of plant-based nutrition remains a major challenge, especially in emerging markets, where these products are often seen as foreign or Western imports rather than natural extensions of traditional protein sources like lentils, chickpeas, or tofu. Many consumers still hold misconceptions about the protein quality and completeness of plant-based diets, even though the Academy of Nutrition and Dietetics confirmed in 2024 that well-planned plant-based diets can provide all essential nutrients for people at every stage of life. Furthermore, plant-based products are often placed in premium or specialty health sections in stores, which reinforces the idea that they are niche or luxury items rather than everyday food options. This perception limits their appeal to the broader market. Efforts such as placing plant-based products alongside conventional items on shelves and using QR codes to educate consumers about their nutritional benefits are helping to address these issues.

Rising incidence of soy, nut, and gluten allergies limits consumer adoption

The increasing number of allergies to common plant-based ingredients, such as soy and tree nuts, is creating challenges for the plant-based food and beverages market. These allergies make it difficult for sensitive consumers to access certain products and reduce their trust in using plant-based options as regular substitutes for traditional foods. Although alternatives like oat- and rice-based products are gaining popularity as safer options, they often have lower protein content, which limits their appeal in segments such as sports nutrition and pediatric diets, where higher protein intake is essential. Furthermore, producing allergen-free products requires specialized manufacturing processes and strict labeling, which increases costs and operational challenges, especially for smaller companies. Retailers also tend to focus on stocking high-demand products, which can result in fewer allergen-free options being available on shelves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dairy Still Dominates Revenue

In 2025, plant-based dairy products contributed 37.12% of the plant-based food and beverages market revenue, making it the largest segment. The growing demand for alternatives to traditional dairy products is driven by factors such as lactose intolerance, the rise in vegan lifestyles, and increasing environmental awareness. Products such as plant-based milk, yogurt, cheese, and creamers have become popular among consumers, both in retail stores and in foodservice outlets. Companies are focusing on improving the taste and quality of these products while ensuring they are widely available in supermarkets. This segment continues to thrive due to its loyal consumer base and the frequent use of plant-based dairy in daily diets.

The meat substitutes segment is expected to grow at a CAGR of 12.61% from 2026 to 2031, reflecting the increasing shift toward plant-based protein options. Consumers are becoming more aware of health benefits, sustainability issues, and animal welfare, which is driving the demand for plant-based meat products. Manufacturers are using advanced technologies to enhance the texture, flavor, and nutritional content of these products, making them more appealing to a broader audience. Additionally, the availability of plant-based meat in quick-service restaurants and packaged food categories is expanding its reach. As global acceptance grows, this segment is poised to become one of the fastest-growing areas in the plant-based food and beverages market.

By Ingredient Source: Soy Leads but Oat Accelerates

Soy is expected to account for 39.55% of the plant-based food and beverages market revenue by ingredient source in 2025, maintaining its dominance as a key raw material. This is largely due to its high protein content, affordability, and versatility, which make it suitable for a range of products such as plant-based milk, meat substitutes, and tofu. The well-established supply chains and large-scale soy cultivation ensure consistent availability and cost efficiency. Its long-standing use in plant-based diets and strong consumer familiarity further contribute to its widespread adoption, solidifying its leading position in the market.

Oat-based ingredients are projected to grow at a CAGR of 13.03% through 2031, driven by increasing consumer demand for allergen-friendly and clean-label options. Oats are naturally free from common allergens like soy and nuts, making them appealing to a wider range of consumers. Their mild flavor and creamy texture make them ideal for dairy alternatives, such as plant-based milk and yogurt. The growing preference for sustainable, minimally processed ingredients has also boosted oats' popularity. Continued product innovation and improved retail availability are expected to support the steady growth of this segment.

By Form: Refrigerated Lines Still Largest

Refrigerated and chilled products accounted for 32.21% of plant-based food and beverage sales in 2025, driven by growing preference for fresh, less-processed options. These include plant-based milk, yogurt, meat substitutes, and ready-to-eat meals that require refrigeration to maintain quality and shelf life. Consumers often perceive chilled products as fresher and tastier, boosting their popularity. The expansion of cold storage facilities and their increasing availability in supermarkets and specialty stores have further supported this segment. The introduction of premium and functional plant-based products has contributed to the growth of refrigerated options.

Ready-to-eat and ready-to-cook plant-based products are expected to grow at a CAGR of 13.46% through 2031, reflecting rising demand for quick, convenient meal solutions. As urbanization increases and lifestyles become busier, more consumers are turning to easy-to-prepare plant-based options. Companies are responding by offering a wider range of products, such as frozen meals, ready-made snacks, and precooked meat substitutes, to meet these needs. Innovations in product development, improved taste profiles, and better retail availability are driving this segment forward. The focus on convenience is expected to remain a key factor in the continued growth of this category.

By Distribution Channel: Supermarkets Command

Off-trade channels, such as supermarkets, hypermarkets, specialty stores, and e-commerce platforms, accounted for 71.82% of the plant-based food and beverage market revenue in 2025. These channels are popular because they offer a wide variety of products, easy accessibility, and strong visibility for plant-based options. Supermarkets dominate due to their established cold-storage infrastructure and ability to stock diverse product ranges. E-commerce is also growing rapidly, providing consumers with direct access to products and a broader selection of niche and premium brands. The continuous growth of organized retail and online grocery platforms is expected to keep off-trade channels as the leading distribution method for plant-based products.

On-trade channels, including restaurants, cafes, and foodservice outlets, are expected to grow at a CAGR of 13.13% through 2031. This growth is driven by the growing availability of plant-based menu options as foodservice providers adapt to consumer demand for healthier, more sustainable meals. Quick-service restaurants and casual dining chains are introducing plant-based alternatives to attract a wider range of customers. The rising trend of dining out and growing consumer awareness about plant-based diets are boosting demand in this segment. As a result, plant-based products are becoming more prominent in foodservice channels, further expanding their market presence.

Geography Analysis

Asia Pacific accounted for 35.84% of the plant-based food and beverage market revenue in 2025, making it the leading region. This growth is fueled by increasing consumer interest in plant-based diets, driven by health consciousness and the rising popularity of flexitarian lifestyles. Countries like China, Japan, and India are experiencing significant demand driven by large populations and growing urbanization. Local manufacturers are creating products that cater to regional tastes, thereby improving acceptance and accessibility. Investments in production facilities and supply chain networks are further solidifying the region’s dominance in the market.

The Middle East and Africa region is expected to grow at a CAGR of 12.05% through 2031, emerging as one of the fastest-growing markets. This growth is supported by increasing awareness of health benefits, a rising need for alternative protein sources, and government initiatives promoting food diversification. Improved retail infrastructure and the availability of plant-based products are making these options more accessible to consumers. Younger generations and urban populations are increasingly interested in plant-based diets, further driving demand. The entry of both global and regional players into the market is expected to accelerate growth in this region.

Europe and North America are mature markets with steady demand, driven by strong consumer awareness of sustainability and established plant-based eating habits. Consumers in these regions are increasingly motivated by environmental concerns, ethical sourcing, and preferences for clean-label products. Retailers are expanding their offerings, including affordable private-label plant-based products, to cater to a wider audience. In Latin America, countries like Brazil and Mexico are experiencing gradual growth due to urbanization and rising consumer awareness of plant-based options. Continued innovation in product development and the expansion of retail distribution channels are expected to support long-term growth in these regions.

Competitive Landscape

The plant-based food and beverages market is moderately fragmented, with both large multinational corporations and smaller innovative brands competing for market share. Major companies like Danone SA, Nestlé SA, Beyond Meat Inc., Oatly Group AB, and Conagra Brands Inc. dominate the market due to their strong product portfolios and extensive global distribution networks. These companies cater to a wide range of consumer preferences by offering a diverse product line, including plant-based dairy, meat substitutes, and beverages. Their ability to produce on a large scale and continuously invest in new product development helps them maintain a competitive edge. However, the presence of numerous regional and emerging brands further fragments the market, creating a dynamic competitive environment.

Leading manufacturers are actively expanding their product offerings and improving supply chain efficiency to meet growing consumer demand. They are heavily investing in research and development to enhance the taste, texture, and nutritional value of their products, which helps in attracting repeat customers. These companies are forming strategic partnerships and entering new geographic markets to strengthen their global presence. Retail expansion and collaborations with foodservice providers are also key strategies to make plant-based products more accessible to consumers. These efforts allow major players to maintain their market position while addressing the evolving needs of the plant-based food and beverages market.

Smaller and regional players are gaining momentum by focusing on niche markets and offering premium or locally tailored plant-based products. Many of these companies emphasize clean label ingredients, sustainability, and unique formulations to stand out in the competitive landscape. Private label brands are also increasing their presence by providing cost-effective alternatives, which adds to the competitive pressure. Success in this market depends on efficient supply chains, reliable ingredient sourcing, and effective brand positioning. As competition continues to grow, companies must prioritize innovation and differentiation to achieve long term success in the plant-based food and beverages market.

Plant-Based Food And Beverages Industry Leaders

-

Danone SA

-

Beyond Meat Inc.

-

Nestlé SA

-

Oatly Group AB

-

Conagra Brands Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Ota Tofu introduced Frozen Seasoned Tofu Crumbles, offering a flavorful, convenient plant-based option for everyday cooking. This launch marked a significant step in expanding their product portfolio to meet the growing demand for versatile, ready-to-use plant-based ingredients.

- September 2025: United Kingdom plant-based food producer THIS collaborated with the German startup Omami to introduce a new range of chickpea-based tofu. This partnership aimed to diversify plant-based protein options by utilizing chickpeas as an alternative ingredient, catering to consumers seeking soy-free choices.

- July 2025: Seoul Dairy Cooperative (led by Chairman Moon Jin-seop) previously announced that it had introduced a plant-based yogurt named 'Cocogurt.' This product was designed to embody the sweetness and richness of coconut, aligning with the growing vegan trend observed in the market.

- July 2025: Alpro, a plant-based brand owned by Danone, launched a new product line specifically designed for children, addressing parental concerns regarding healthier food choices. This product range featured a chocolate-flavored oat-based drink, a strawberry-flavored soya drink, and soya-based yogurt alternatives available in vanilla and strawberry flavors.

Global Plant-Based Food And Beverages Market Report Scope

Plant-based food and beverages are primarily products made from plants, vegetables, grains, nuts, legumes, and fruit sources, which provide nutrients including iron, magnesium, folic acid, vitamin C, vitamin E, and dietary fiber. The plant-based food and beverage market is segmented by product type, ingredient source, form, distribution channel, and geography. The market is segmented by product type into plant-based dairy, meat substitutes, plant-based nutrition/snack bars, plant-based bakery products, and plant-based beverages. Based on ingredient source, the market is segmented into soy, almond, pea, oat, wheat, rice, coconut, and others. Based on form, the market is segmented into refrigerated/chilled, frozen, shelf-stable/ambient, and ready-to-eat/ready-to-cook. By distribution channel, the plant-based food and beverages market is segmented into on-trade and off-trade. Geographically, the report provides an analysis of emerging and established economies worldwide, including North America, Europe, South America, Asia-Pacific, and the Middle East and Africa. For each segment, market sizing and forecasts have been conducted on a value basis (USD million).

By Product Type

| Plant-Based Dairy | Yogurt |

| Cheese | |

| Frozen Desserts and Ice Creams | |

| Others | |

| Meat Substitutes | Tofu |

| Tempeh | |

| Textured Vegetable Protein | |

| Others | |

| Plant-Based Nutrition/Snack Bars | |

| Plant-Based Bakery Products | |

| Plant-Based Beverages | Packaged Milk |

| Packaged Smoothies | |

| Coffee | |

| Tea | |

| Others | |

| Other Product Types |

By Ingredient Source

| Soy |

| Almond |

| Pea |

| Oat |

| Wheat |

| Rice |

| Coconut |

| Others |

By Form

| Refrigerated/Chilled |

| Frozen |

| Shelf-Stable/Ambient |

| Ready-To-Eat/Ready-To-Cook |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Stores | |

| Other Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Plant-Based Dairy | Yogurt |

| Cheese | ||

| Frozen Desserts and Ice Creams | ||

| Others | ||

| Meat Substitutes | Tofu | |

| Tempeh | ||

| Textured Vegetable Protein | ||

| Others | ||

| Plant-Based Nutrition/Snack Bars | ||

| Plant-Based Bakery Products | ||

| Plant-Based Beverages | Packaged Milk | |

| Packaged Smoothies | ||

| Coffee | ||

| Tea | ||

| Others | ||

| Other Product Types | ||

| By Ingredient Source | Soy | |

| Almond | ||

| Pea | ||

| Oat | ||

| Wheat | ||

| Rice | ||

| Coconut | ||

| Others | ||

| By Form | Refrigerated/Chilled | |

| Frozen | ||

| Shelf-Stable/Ambient | ||

| Ready-To-Eat/Ready-To-Cook | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Stores | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the plant-based food and beverages market by 2031?

The plant-based food and beverages market size is forecast to reach USD 166.43 billion by 2031.

Which region accounts for the largest revenue share today?

Asia-Pacific holds 35.84% of 2025 global revenue, making it the largest regional market.

Which segment is expected to grow fastest within the category?

Meat substitutes are projected to post a 12.61% CAGR through 2031 as whole-muscle textures improve.

Why is oat gaining ground against soy in plant-based drinks?

Oat offers neutral flavor, lower allergen risk, and a smaller water footprint, driving a 13.03% CAGR through 2031.

Page last updated on: