Fresh Figs Market Size and Share

Fresh Figs Market Analysis by Mordor Intelligence

The fresh figs market is projected to grow from USD 2.20 billion in 2025 to USD 2.35 billion in 2026, and is forecasted to reach USD 3.30 billion by 2031, with a CAGR of 7.0% during 2026-2031. Growth is primarily driven by increasing consumer demand for nutrient-rich fruits, the rising popularity of Mediterranean diet trends, and advancements in post-harvest technologies. The expansion of e-commerce platforms has further improved access to imported fruits. Investments in climate-resilient cultivars and precision irrigation systems are helping producers reduce yield fluctuations and strengthen their competitive position. Moreover, innovations in blockchain-enabled traceability and breathable packaging are extending shipping ranges and lowering rejection rates, contributing to better unit margins.

Key Report Takeaways

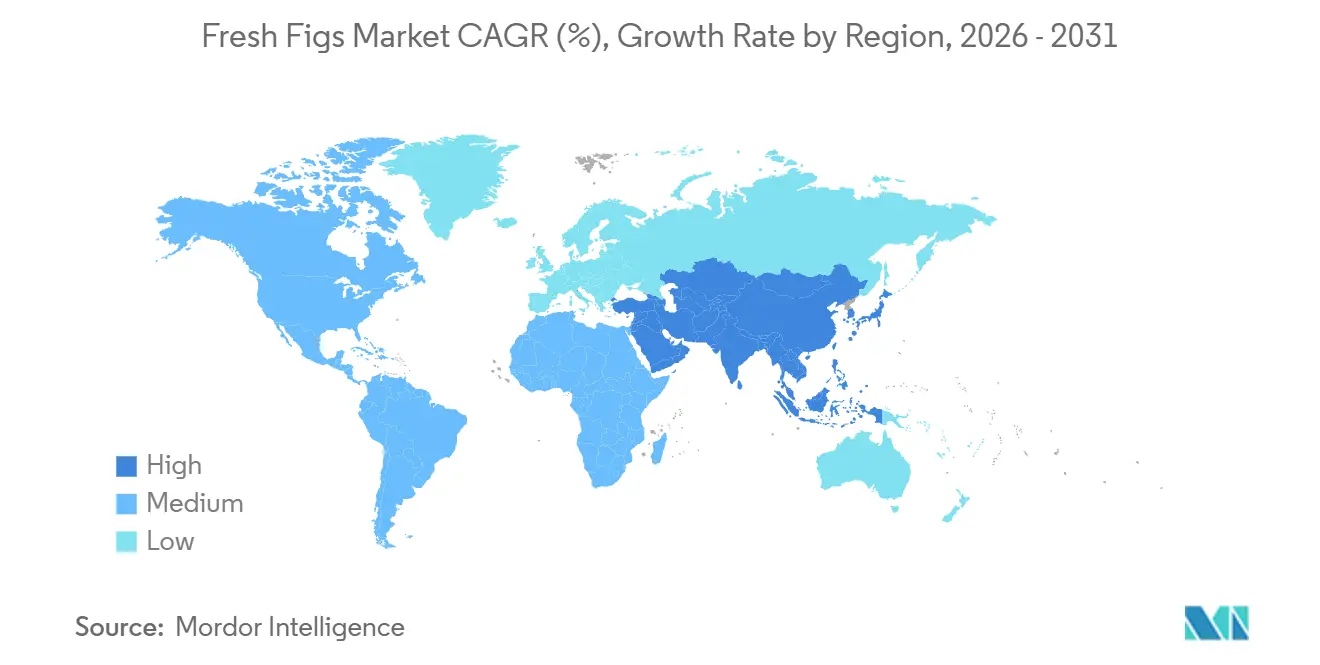

- By geography, Asia-Pacific held the largest fresh figs market share at 37.0% in 2025, and the market size for Asia-Pacific is projected to grow at the fastest 6.0% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fresh Figs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding health-conscious consumer base | +1.3% | Global, premium uptake in North America, European Union, and Asia-Pacific urban markets | Medium term (2-4 years) |

| Premiumization of exotic fruits in urban centers | +1.0% | Asia-Pacific (Tokyo, Shanghai, Hong Kong), North America (New York, Los Angeles), and Middle East (Dubai) | Medium term (2-4 years) |

| Rapid growth of Mediterranean-style diets | +1.1% | Global, led by North America, European Union, and emerging Asia-Pacific adoption | Long term (≥ 4 years) |

| Climate-smart cultivation incentives | +0.9% | Mediterranean basin and North Africa | Long term (≥ 4 years) |

| Rising demand from natural sweetener industry | +1.0% | North America and European Union, spillover to Asia-Pacific processing hubs | Medium term (2-4 years) |

| E-commerce penetration in fresh produce trade | +1.2% | Asia-Pacific, North America, European Union, and strongest in tier-2 and tier-3 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Health-Conscious Consumer Base

Consumers are increasingly opting for functional foods that provide clear physiological benefits, elevating fresh figs from a Mediterranean specialty to a globally recognized superfood. A 100-gram serving of figs contains approximately 162 milligrams of calcium, making it a nutrient-dense option that supports bone health and mineral intake[1]Source: U.S. Department of Agriculture (USDA), FoodData Central – Figs, Dried, fdc.nal.usda.gov. Mainstream sellers are increasing seasonal stock-keeping units, and nutraceutical companies are exploring fig extracts for use in functional beverages, creating additional revenue opportunities. Furthermore, peer-reviewed studies have identified antimicrobial and antioxidant properties in figs, expanding their potential applications in the cosmetic and pharmaceutical industries.

Premiumization of Exotic Fruits in Urban Centers

Affluent consumers in cities such as Tokyo, Shanghai, Dubai, New York, and Los Angeles perceive premium figs as lifestyle products, willingly paying a premium over mainstream berries. Social media trends, including charcuterie boards and fig-topped flatbreads, have increased the visibility of figs. Direct-to-consumer channels allow growers to bypass wholesalers, capturing higher margins while offering blockchain-verified provenance, which commands additional pricing. In China, tier-2 cities are reflecting this trend, with fig imports growing as e-commerce platforms expand refrigerated fulfilment networks.

Rapid Growth of Mediterranean-Style Diets

The World Health Organization (WHO) advocates for Mediterranean dietary patterns to mitigate chronic diseases, encouraging the inclusion of figs in meal planning. Surveys indicate that around half of urban households in North America incorporate Mediterranean elements into their meals weekly, while adoption in the Asia-Pacific region is increasing through fusion cuisine. Figs provide natural sweetness without added sugar, along with potassium and antioxidants, aligning with clean-label guidelines. Figs meet year-round pantry needs, while fresh figs are available seasonally, peaking from July to October in the Northern Hemisphere and December to March in the Southern Hemisphere, aligning with seasonal wellness campaigns.

Climate-Smart Cultivation Incentives

Governments are supporting precision irrigation, drought-tolerant crop varieties, and integrated pest management to address the Mediterranean basin's warming, which is occurring 20% faster than the global average[2]Source: United Nations Environment Programme, “Mediterranean Climate Outlook,” unep.org. A 2025 study revealed that drip irrigation reduces water consumption by 30–50% while maintaining or enhancing crop yields. This makes it particularly suitable for high-value fruit crops, such as figs, grown in semi-arid climates. These efficiency improvements help ensure consistent fruit quality, optimize resource utilization, and promote the adoption of sustainable orchard practices amid growing climate variability [3]Source: Rahman A., “Effectiveness of Drip Irrigation Systems in Agriculture,” agroresearchjournal.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High perishability and cold-chain gaps | -1.6% | Global, acute on Mediterranean to Asia-Pacific and South America to European Union routes | Short term (≤ 2 years) |

| Susceptibility to fungal diseases | -1.1% | Mediterranean basin and North Africa | Medium term (2-4 years) |

| Volatile farm-gate prices in producing countries | -0.9% | South America, North Africa, and Asia-Pacific | Medium term (2-4 years) |

| Trade disruptions from phytosanitary barriers | -0.8% | Cross-border trade subject to United States Department of Agriculture, European Commission, and China Customs rules | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Perishability and Cold-Chain Gaps

Fresh figs have a shelf life of approximately seven days at ambient temperatures, with post-harvest losses remaining high on routes lacking stable refrigeration. The use of honeycomb trays and breathable valves can extend the shelf life to 21 days under controlled conditions. However, reefer capacity remains inconsistent in emerging markets. In Argentina, the wholesale price of figs increased significantly due to supply shocks, demonstrating cost pass-through to buyers. Smallholders without access to on-farm cold storage are compelled to make distress sales during peak harvest periods, limiting their ability to reinvest in orchard improvements.

Susceptibility to Fungal Diseases

Fig rust, anthracnose, and aflatoxin-producing Aspergillus pose significant threats to fig yields and are major contributors to export rejections. The European Union's strict limits on aflatoxin B1 and total aflatoxins to ensure food safety have also been followed by South Africa. Compliance with these regulations incurs additional costs for producers, as meeting the required standards involves significant investment in monitoring and control measures. Organic growers face even greater challenges, as biological fungicides, while environmentally friendly, are less effective compared to synthetic alternatives. This often results in notable yield losses, further impacting their profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

In 2025, the Asia-Pacific region accounted for the largest share of the fresh figs market at 37.0%. The market size in this region is projected to grow at the fastest CAGR of 6.0% from 2026 to 2031. This growth is supported by China’s imports of 16.3 million kilograms and the increasing role of e-commerce distribution channels. Urban households in cities such as Shanghai, Tokyo, and Mumbai consider premium figs as status symbols, often paying higher prices during Mediterranean harvest seasons. However, domestic production in regions like Sichuan and Maharashtra is expanding slowly, leading to continued reliance on imports from Turkey, Spain, and California.

Production declined due to late frost, with forecasts suggesting further reductions unless the widespread adoption of The Full International and Global Accounts for Research in Input-Output Analysis (FIGARO) precision irrigation mitigates moisture stress. Spain ranked second, producing in Extremadura, supported by increasing organic acreage that commands retail premiums. Greece and Italy contribute smaller volumes but face challenges such as drought-induced orchard losses and aging tree stock.

In North America, California produced a significant crop in 2025, with Mexico supplying the October to May window. Canada imports fresh fig to meet the demand. Argentina, Brazil, Egypt, and Morocco remain cost-competitive but face challenges such as aflatoxin controls and cold-chain infrastructure gaps, which hinder their ability to access premium European Union and Asia-Pacific markets. In 2025, Saudi Arabia purchased a substantial quantity for Ramadan, while the United Arab Emirates utilized rapid delivery apps to boost urban consumption. These diversified supply chains help stabilize the global market against localized climate-related disruptions.

Competitive Landscape

Production in the fig industry is predominantly managed by smallholder orchards, typically spanning less than five hectares. Export operations are overseen by cooperatives and integrated traders who handle cold storage, packing, and certification processes. Valley Fig Growers markets brands such as Blue Ribbon and Orchard Choice, processing a significant portion of California’s figs into paste and diced formats to stabilize revenues amidst fluctuations in the fresh market. In Turkiye, FIGY coordinates sourcing activities across the Aydın province, while Litras Fresh maintains year-round supply contracts with European retailers.

Companies like Aksun are enhancing their operations by utilizing advanced sorting, grading, and packaging technologies to ensure consistent quality and extend shelf life for export markets. The Full International and Global Accounts for Research in Input-Output Analysis (FIGARO) project demonstrated that precision irrigation technologies achieved water savings of 20–30% in pilot orchards. Exporters are increasingly implementing blockchain-based traceability systems, such as Hyperledger Fabric, to ensure compliance with cold-chain requirements, which are becoming a standard demand from large retail buyers.

Innovation efforts are increasingly directed toward utilizing processing by-products, as fig processing generates significant residual material, including peels and pomace. These by-products are rich in valuable compounds such as pectin and polyphenols. Incorporating fig by-products into livestock feed can contribute to sustainability objectives. Premium fig varieties, such as Emerald from California, achieve higher prices in niche markets. Additionally, leading exporters account for nearly 40% of the global trade volume, presenting opportunities for emerging players to enter and compete in the market.

Recent Industry Developments

- February 2026: The European Commission has upheld the aflatoxin B1 limit at 6 µg/kg. Additionally, it has removed the fig mosaic agent from the Regulated Non-Quarantine Pests list, simplifying intra-European Union trade compliance for countries such as Spain, Greece, and Italy.

- May 2025: The India–UAE Comprehensive Economic Partnership Agreement (CEPA) and the proposed India–Middle East–Europe Economic Corridor (IMEC) have expanded agricultural export opportunities, including for fresh fruits such as figs. These agreements are facilitating improved tariff conditions and optimizing cross-border logistics for exporters.

Global Fresh Figs Market Report Scope

Fresh figs are ripened, soft fruits consumed in their natural, unprocessed state, appreciated for their sweet flavor and high nutritional value. Due to their perishable nature, they are typically consumed fresh or with minimal handling, necessitating careful harvesting and storage to preserve quality. The global fresh figs market report is segmented by geography (North America, Europe, Asia-Pacific, and more). The report includes production analysis (volume), consumption analysis (value and volume), export analysis (value and volume), import analysis (value and volume), wholesale price trend analysis and forecast, regulatory framework, list of key players, logistics and infrastructure and seasonality analysis. The market forecasts are provided in terms of value (USD) and volume (metric tons).

| North America | United States | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Canada | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Rest of North America | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| South America | Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Rest of South America | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Europe | Spain | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Greece | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Russia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Rest of Europe | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Asia-Pacific | China | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| India | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Japan | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Australia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Rest of Asia-Pacific | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Middle East | Turkey | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Saudi Arabia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| United Arab Emirates | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Rest of Middle East | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Africa | Egypt | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Rest of Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| By Geography | North America | United States | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Canada | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Rest of North America | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| South America | Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Rest of South America | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Europe | Spain | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Greece | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Russia | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Rest of Europe | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Asia-Pacific | China | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| India | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Japan | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Australia | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Rest of Asia-Pacific | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Middle East | Turkey | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Saudi Arabia | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| United Arab Emirates | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Rest of Middle East | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Africa | Egypt | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Rest of Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

Key Questions Answered in the Report

How large will the global fresh figs category be by 2031?

The fresh figs market size is projected to reach USD 3.30 billion by 2031.

Which region currently drives the greatest share of demand?

Asia-Pacific held the largest regional share at 37.0% in 2025, fueled by urbanization and e-commerce growth in China, Japan, and India.

What growth rate is Asia-Pacific posting through 2031?

Asia-Pacific is advancing at a 6.0% CAGR during 2026-2031, the fastest among all reporting regions.

Why are processors interested in fig-based sweeteners?

Fig paste and syrup offer natural sweetness, a mid-range glycemic index, and minerals that satisfy clean-label goals while reducing reliance on refined sugar.

Page last updated on: