Pistachio Market Size and Share

Pistachio Market Analysis by Mordor Intelligence

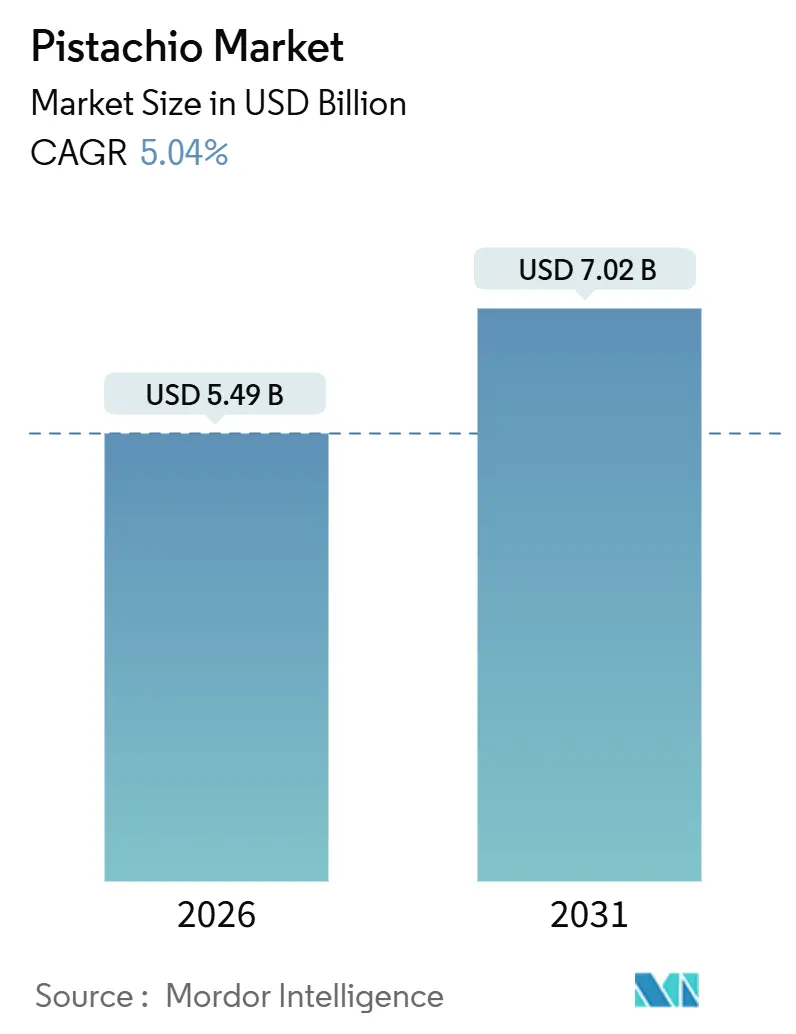

The pistachio market size is estimated at USD 5.49 billion in 2026 and is projected to reach USD 7.02 billion by 2031, reflecting a 5.04% CAGR during the forecast period. Robust consumer demand for plant-based proteins, the premiumization of snack nuts, and sustained acreage growth in drought-resilient regions support this expansion. Vertically integrated processors scale capacity to secure grower loyalty and capture value through branded retail channels, while blockchain traceability platforms ease retailer compliance requirements in North America and Europe[1]Source: United States Department of Agriculture Foreign Agricultural Service, “Tree Nuts Annual_Beijing_China,” fas.usda.gov. Precision irrigation and drone-enabled input mapping reduce water and fertilizer use, shielding growers from the impact of tightening groundwater regulations and labor scarcity. Counter-seasonal supply from Argentina and Australia provides a hedge against climate risk in California and Iran, although alternate-bearing cycles and volatile water allocations continue to inject variability into the pistachio market.

Key Report Takeaways

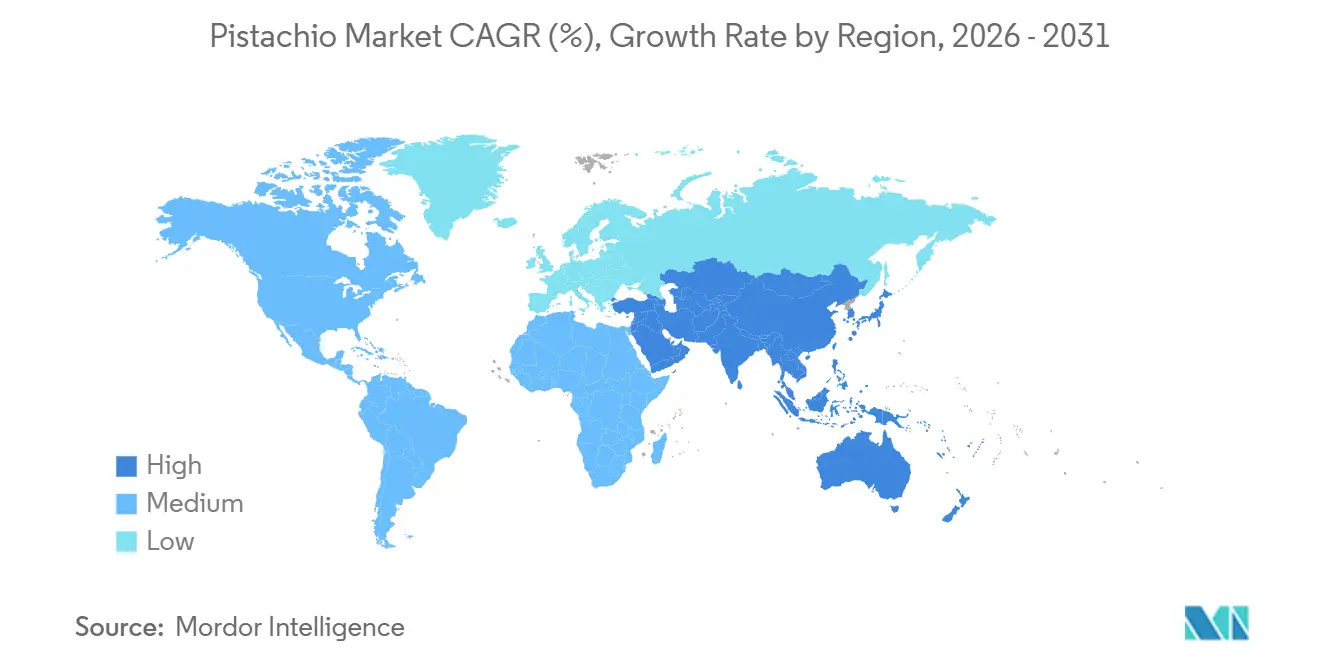

- By geography, North America led the pistachio market share with 42% in 2025, while the Asia-Pacific region is projected to post the fastest CAGR of 5.1% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pistachio Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding acreage under drought-resistant rootstocks | +0.8% | North America, Middle East, and South America | Medium term (2-4 years) |

| Short-cycle cultivars enabling double-harvest regimes | +0.7% | North America, Australia | Long term (≥ 4 years) |

| Increasing demand for plant-based proteins | +0.9% | Global, with concentration in Asia-Pacific and North America | Short term (≤ 2 years) |

| Premiumization of snack nuts in bulk and ingredient channels | +0.6% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Advent of blockchain grower-to-roaster traceability | +0.3% | North America, Europe | Short term (≤ 2 years) |

| Drone-enabled yield mapping optimizing inputs | +0.4% | North America, Australia, and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Acreage under Drought-Resistant Rootstocks

Drought-tolerant rootstocks are being increasingly adopted to expand pistachio cultivation into semi-arid zones previously considered unsuitable. Trials indicate that these rootstocks maintain strong yield performance even under deficit irrigation, making them valuable in regions facing water scarcity. Government funding programs are supporting breeding initiatives to enhance salinity tolerance, particularly in areas with poor groundwater quality[2]Source: National Institute of Food and Agriculture, “Specialty Crop Research Initiative,” nifa.usda.gov. Countries in South America, the Middle East, and Oceania are also adopting these rootstocks, diversifying global production bases. Growers report that drought‑resistant rootstocks enable mechanical harvesting, lower input costs, and drive acreage growth while stabilizing supply in major producing regions.

Short-Cycle Cultivars Enabling Double-Harvest Regimes

Early-maturing cultivars are transforming pistachio production by reducing the time required to reach commercial harvests. These varieties help mitigate alternate-bearing cycles, enabling growers to plan sequential plantings that stabilize output. Processing facilities are adapting with flexible shelling systems that can handle multiple cultivars without downtime, supporting premium pricing for differentiated lots. In regions prone to early autumn rains, shorter harvest windows reduce contamination risks and improve product quality. Short‑cycle cultivars deliver heavier kernel weights and more reliable yields during peak years, playing a larger role in balancing supply with demand while improving profitability.

Increasing Demand for Plant-Based Proteins

Pistachios are gaining recognition as a complete source of plant-based protein, providing all the essential amino acids that the body needs. Ingredient buyers in the meat alternative, dairy substitute, and sports nutrition sectors are increasingly incorporating pistachio protein into their formulations. Growing consumer interest in health and sustainability has elevated pistachios as a premium choice among plant proteins. Imports into major Asian and Latin American markets continue to rise, reflecting strong demand growth. Domestic research is exploring opportunities for local cultivation to reduce dependence on imports, while pistachio protein is increasingly recognized as a driver of demand, positioning the crop as a central ingredient in plant-based nutrition.

Premiumization of Snack Nuts in Bulk and Ingredient Channels

Premium pistachio segments, including organic, flavored, and single-origin varieties, are commanding significant price premiums over commodity grades. Acreage dedicated to organic production is expanding, while flavored pistachios are gaining popularity in North American and European markets[3]Source: National Agricultural Statistics Service, “California Pistachio Reports,” nass.usda.gov. Large processors are investing in roasting and flavoring facilities to capture value through branded retail channels. Single-origin pistachios from traditional producing regions are marketed for their provenance and kernel quality, appealing to niche consumer segments. Premiumization boosts grower returns and strengthens consumer loyalty to specific brands, with organic, flavored, and single‑origin pistachios projected to remain key growth areas as preferences evolve.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from emerging desert nuts | -0.5% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Volatile water allocations in major origins | -0.6% | North America (California) and Middle East (Iran) | Short term (≤ 2 years) |

| Alternate-bearing supply swings inflating inventory costs | -0.5% | Global | Short term (≤ 2 years) |

| Labor scarcity amid stricter immigration policies | -0.4% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Emerging Desert Nuts

Alternative desert crops such as sacha inchi, tigernuts, and mongongo are entering the market with comparable nutritional profiles. These nuts are often marketed at lower prices, creating competitive pressure on pistachio ingredient margins. Sacha inchi is promoted for its high protein content, while tigernuts are positioned as allergen-free options that bypass labeling constraints. Emerging origins in Latin America are exploring pistachio cultivation alongside these alternatives, diversifying protein sources. Alternative desert crops appeal strongly to health‑conscious consumers seeking diversity in plant‑based diets, and this competition is projected to shape pricing strategies while encouraging innovation in pistachio products.

Volatile Water Allocations in Major Origins

Water availability remains a critical challenge for pistachio growers in major producing regions. In California, state water allocations fluctuate significantly, leading to an increased reliance on groundwater, which is subject to growing regulation. In Iran, declining aquifers have reduced productive acreage, creating uncertainty for growers in key provinces. While Australia provides some counter-seasonal relief, its volumes remain limited compared to traditional suppliers. Uncertain water supplies raise production costs and complicate long‑term planning, with volatility in allocations likely to remain a defining challenge that influences investment decisions and shapes the stability of pistachio supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

North America accounted for 42% of the pistachio market share in 2025, highlighting its position as the largest regional supplier. California remains central to production, supported by vertically integrated processors that enhance capacity and returns through premiumization strategies. The adoption of precision irrigation and blockchain traceability improves supply stability and strengthens retailer confidence. Mexico and Canada significantly contribute to regional trade flows, with favorable duty structures that facilitate the import of goods. North America is projected to maintain its leadership in global pistachio supply, although groundwater restrictions emphasize the need for sustainable practices. The region’s scale, infrastructure, and established consumer base ensure its continued dominance in both domestic and export markets.

The Asia-Pacific region is projected to achieve a 5.1% CAGR through 2031, making it the fastest-growing area in the pistachio market. Increasing demand in China and India drives imports, supported by tariff adjustments and tax reforms that enhance the affordability of these products. Expanding e-commerce penetration and health awareness campaigns further boost consumption, positioning pistachios as a preferred plant-based protein. Australia contributes counter-seasonal supply, while South Africa’s emerging production adds diversification. The Asia-Pacific region is projected to steadily expand its market size, driven by structural demand growth and rising middle-class consumption. This momentum highlights the region’s pivotal role as a key driver of global pistachio trade growth.

Europe continues to grow steadily, with countries such as Greece, Spain, and Italy increasing plantings to reduce reliance on imports. Turkey’s confectionery industry consumes the majority of its domestic production, occasionally necessitating imports from neighboring regions to maintain a stable supply. European Union aflatoxin limits favor exporters from regions with advanced post-harvest handling and traceability systems. Europe is anticipated to maintain moderate growth, driven by rising demand for premium snack nuts and ingredient applications. While not the largest or fastest-growing region, Europe’s focus on quality standards and sustainability ensures it remains a critical market for exporters seeking differentiation and compliance.

Competitive Landscape

Companies such as Wonderful Pistachios and Setton Pistachio play a significant role in shaping the pistachio industry. These firms manage extensive orchards, advanced processing facilities, and integrated logistics networks to streamline the delivery from farm to market. Their strategies focus on premiumization, operational efficiency, and sustainability, strengthening their leadership in both domestic and export markets. Investments in infrastructure and branding enhance grower loyalty while capturing value through differentiated retail offerings. By setting benchmarks in pricing, quality, and innovation, these companies influence the broader market and establish standards that smaller players often follow. Their scale and adoption of advanced technologies position them as key drivers of long-term industry growth.

Smallholder growers remain essential to the pistachio supply chain and pistachio market share, often collaborating through cooperatives and associations to manage exports and uphold quality standards. Despite challenges such as water scarcity and fragmented production structures, their collective efforts ensure continued participation in global trade. Counter-seasonal producers, such as SolFrut, capitalize on timing advantages by supplying markets during off-years, securing premiums, and stabilizing their supply. Organic certification provides opportunities for differentiation, though the transition period can be financially challenging for smaller growers. These stakeholders demonstrate the diversity of production models, where collaboration and timing strategies are critical for maintaining market presence and competitiveness.

Technological advancements are transforming the pistachio market. Innovations such as blockchain traceability, drone-guided agronomy, and mechanical harvesting are increasingly adopted by stakeholders with the resources to invest in modern infrastructure. These technologies reduce labor dependency, enhance throughput, and ensure compliance with retailer requirements. Family-owned processors often face challenges in adopting such technologies, while newly established orchards by companies like Setton Pistachio and SolFrut integrate advanced systems from the outset. This positions them for cost parity with established suppliers as they grow. Stakeholders that embrace innovation enhance their resilience and secure long-term growth, while those that lag behind risk marginalization in a market increasingly driven by efficiency, sustainability, and technological progress.

Recent Industry Developments

- December 2025: Canada is experiencing an increasing salmonella outbreak associated with imported pistachios and pistachio-based products, with over 150 laboratory-confirmed cases reported across several provinces. In response, the Canadian Food Inspection Agency (CFIA) has initiated multiple product recalls and enforced import restrictions, along with mandatory testing for pistachios originating from Iran, to reduce the risk of further contamination. This outbreak, along with the subsequent product recalls, is impacting market confidence and influencing the supply dynamics of pistachio imports and retail sales within Canada.

- May 2025: Wonderful Pistachios launched its "The Don’t Hold Back Snack" integrated marketing campaign in the United States in anticipation of a record California pistachio harvest. This comprehensive initiative includes TV advertisements, out-of-home promotions across nine major markets, and celebrity-hosted podcast appearances aimed at increasing consumer demand and enhancing brand visibility. The campaign highlights the growing consumer preference for pistachios as a flavorful, protein-rich snack and aligns with the broader market growth driven by rising global demand for pistachio products.

- January 2025: California Pistachios introduced the Better Nut initiative in India to position pistachios as a healthier snacking choice. This expansion highlights the benefits of plant‑based protein and aims to build stronger consumer awareness in a rapidly growing market segment.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global pistachio market as commercial sales of in-shell and shelled nuts, raw or roasted, moving through retail, food-service, ingredient, and bulk export channels. According to Mordor Intelligence, we track both conventional and certified-organic volumes originating from producing orchards in the United States, Türkiye, Iran, and other minor growers, and then follow the nuts through processing, packaging, and distribution until their first point of final sale.

Scope exclusion: Pistachio-based oils, cosmetic derivatives, and blended multi-nut products fall outside this assessment.

Segmentation Overview

- By Geography

- North America

- United States

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Canada

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Mexico

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- United States

- Europe

- Greece

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Spain

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Italy

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Germany

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- France

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Germany

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Greece

- Asia-Pacific

- China

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- India

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Australia

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- China

- South America

- Brazil

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Argentina

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Brazil

- Middle East

- Turkey

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Iran

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Syria

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Turkey

- Africa

- Egypt

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- South Africa

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Egypt

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with orchard owners, processors, bulk traders, ingredient buyers, and category managers across North America, Europe, the Middle East, and Asia-Pacific help us validate yield assumptions, average selling prices, quality differentials, and emerging demand pockets. Insights from these conversations close gaps that published statistics leave open.

Desk Research

Our analysts begin with authoritative public datasets such as USDA NASS bearing acreage reports, FAOSTAT crop statistics, ITC Trade Map shipment values, Eurostat COMEXT import flows, and International Nut & Dried Fruit Council supply balances. Company filings, investor presentations, and government customs data enrich the baseline, while paid resources like D&B Hoovers and Questel supplement financials and patent trends where relevant. These sources establish production, trade, and average price corridors that underpin the model. The desk-research list cited here is illustrative rather than exhaustive, and many additional references informed the final build.

Market-Sizing & Forecasting

A top-down harvested-acreage × yield reconstruction is first built country by country. Export and domestic disappearance are then aligned with consumption coefficients derived from nutrition survey data and snack penetration rates. Bottom-up cross-checks, sampled processor throughput, channel audits, and averaged in-shell-to-kernel price spreads adjust totals where discrepancies appear. Key variables fed into the model include alternate-bearing cycle patterns, bearing-acre expansion, average kernel recovery, per-capita snack consumption, and wholesale price trends. Forecasts employ multivariate regression that links those drivers to macro indicators such as disposable income and urbanization, a technique our experts confirm mirrors real-world purchasing dynamics.

Data Validation & Update Cycle

Model outputs pass variance checks against independent trade tallies and Statista production benchmarks before senior review. Reports refresh each year, with mid-cycle updates triggered by material events like drought shocks or tariff changes. A final analyst pass occurs just before delivery to ensure clients receive the latest view.

Why Mordor's Pistachio Baseline Earns Buyer Confidence

Published estimates often diverge because firms choose different product scopes, pricing anchors, and update cadences. We acknowledge those gaps upfront.

Key gap drivers include: some studies lump flavored value-added items or wider tree-nut categories into totals; others apply uniform farm-gate prices across regions or roll forward older baseline years without accounting for the 2024 U.S. acreage jump. Mordor Intelligence reports only edible nut forms, refreshes annually, and factors in regional yield swings, which keeps our 2025 base figure balanced and traceable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.67 billion | Mordor Intelligence | Mordor Intelligence reports only edible nut forms, refreshes annually, and factors in regional yield swings, which keeps our 2025 base figure balanced and traceable. |

| USD 4.58 billion | Global Consultancy A | Narrower product coverage and minimal informal-trade mapping |

| USD 5.79 billion | Trade Journal B | Tree-nut aggregation with uniform price assumptions |

These comparisons show that Mordor's disciplined scope selection and regular data refresh create a dependable baseline clients can rely on for strategic decisions.

Key Questions Answered in the Report

What is the current pistachio market size and its growth outlook?

The pistachio market size stands at USD 5.49 billion in 2026, with a forecast to reach USD 7.02 billion by 2031.

How fast is the pistachio market growing?

The market is expanding at a 5.04% CAGR through 2031.

Which region holds the largest share in the pistachio market?

North America commands 42% market share in 2025.

Which region shows the fastest consumption growth?

Asia-Pacific posts the fastest CAGR at 5.1% through 2031, driven by imports in China and India.

What technologies are improving pistachio production efficiency?

Drone-enabled input mapping, blockchain traceability, and drought-resistant rootstocks lower costs and raise compliance levels.

Page last updated on: