Europe Non-Destructive Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

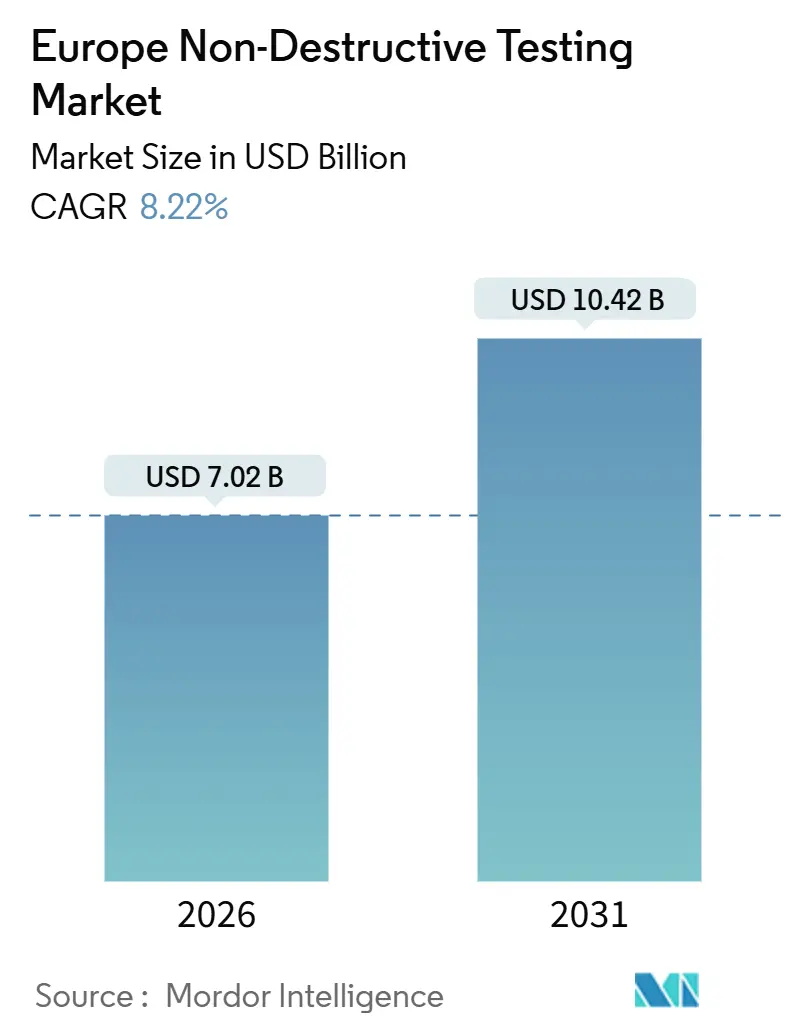

| Market Size (2026) | USD 7.02 Billion |

| Market Size (2031) | USD 10.42 Billion |

| Growth Rate (2026 - 2031) | 8.22% CAGR |

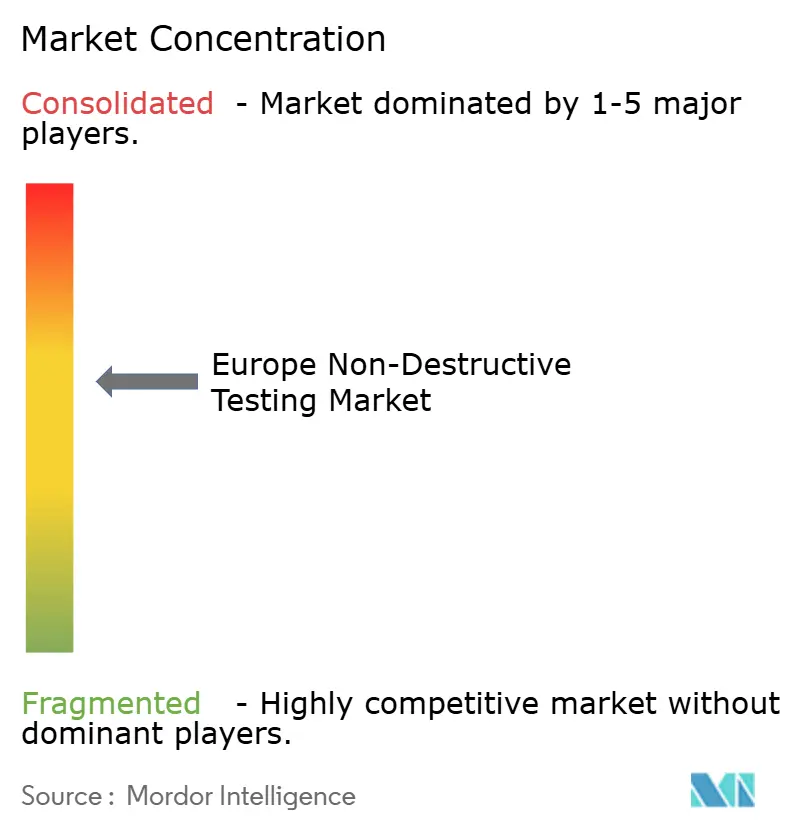

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Non-Destructive Testing Market Analysis by Mordor Intelligence

The Europe Non-Destructive Testing Market size is estimated at USD 7.02 billion in 2026, and is expected to reach USD 10.42 billion by 2031, at a CAGR of 8.22% during the forecast period (2026-2031).

Robust regulatory enforcement, heavy aerospace and defense maintenance activity, and life-extension programs for North Sea energy assets are sustaining inspection volumes while digitization pushes operators toward data-rich ultrasonic, radiographic, and eddy-current platforms. Outsourcing remains the dominant service model, yet rental arrangements and cloud analytics subscriptions are widening access to advanced technologies. German automotive electrification, United Kingdom nuclear new-builds, and additive-manufacturing part qualification are among the highest-growth demand pockets, encouraging vendors to bundle portable hardware with artificial-intelligence analytics for faster defect classification. Competitive intensity is moderate as five multinational service providers hold just under 40% share, but specialized equipment makers are expanding niches in phased-array ultrasonics and portable computed-tomography solutions, reshaping value capture along the inspection workflow.

Key Report Takeaways

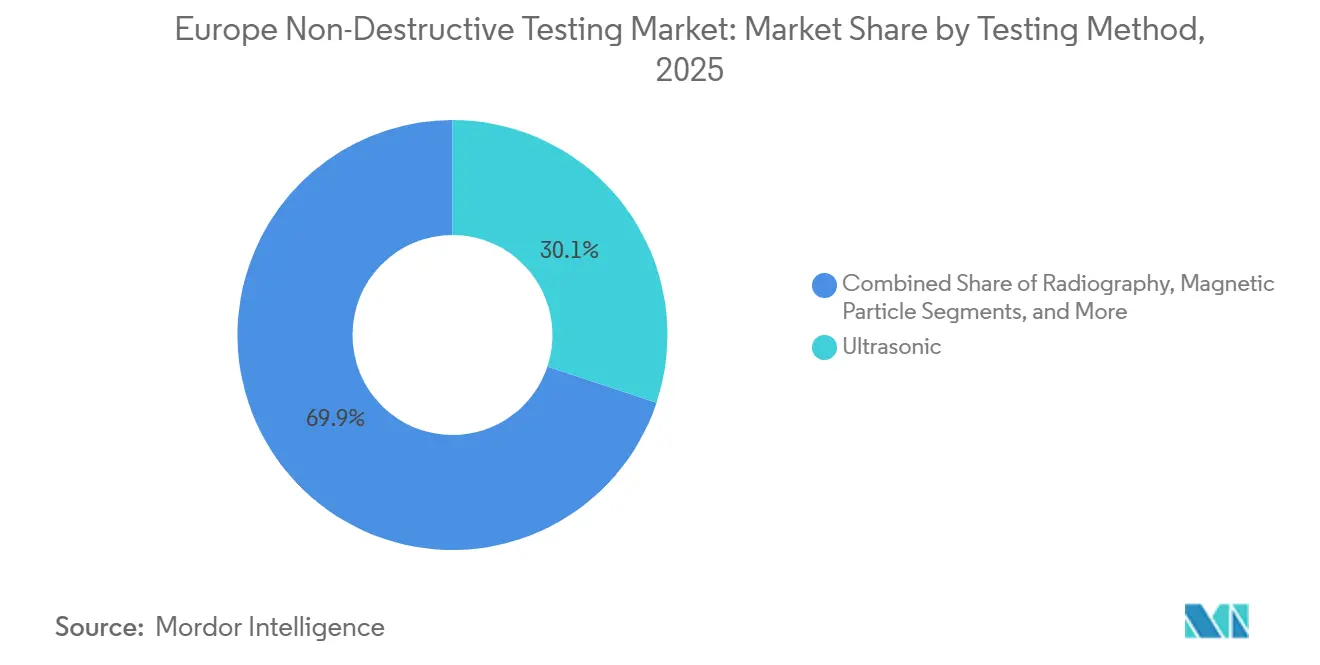

- By testing method, ultrasonic techniques led with 30.11% of Europe Non-Destructive Testing market share in 2025, while emerging techniques are forecast to expand at an 8.92% CAGR through 2031.

- By component type, services held 49.57% share of the Europe Non-Destructive Testing market size in 2025, whereas software and analytics platforms are projected to grow at 9.14% CAGR to 2031.

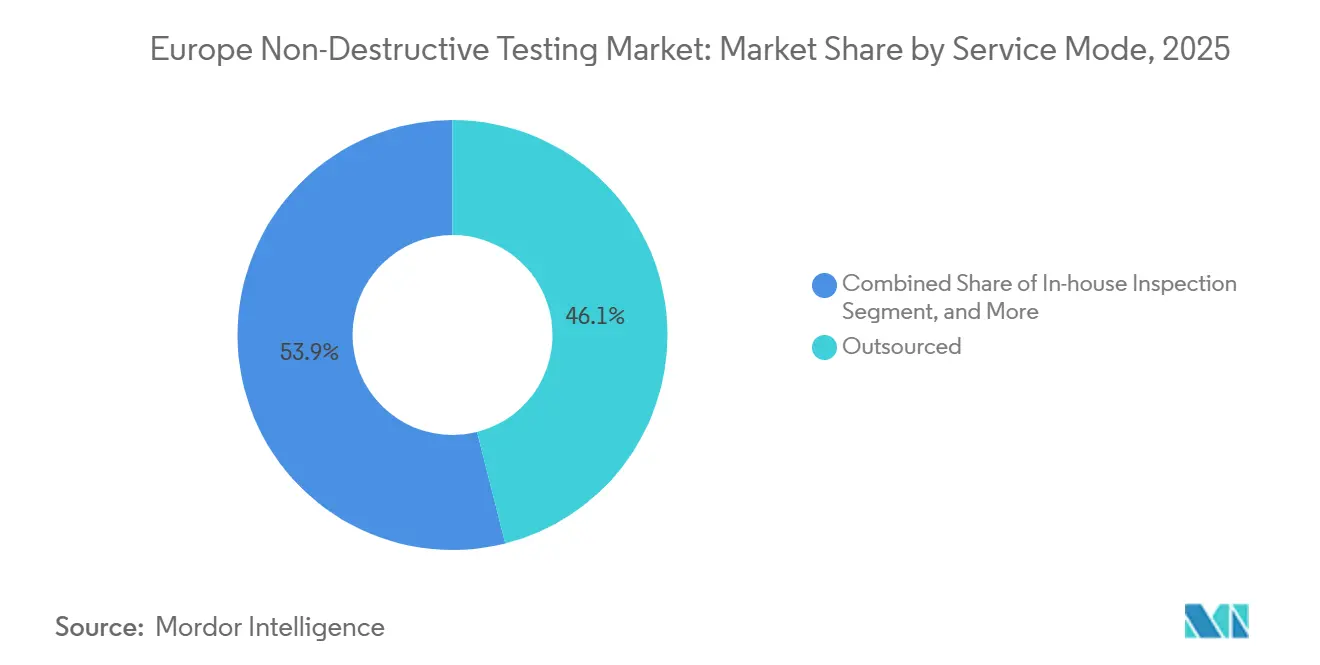

- By service mode, outsourced inspection captured 46.06% of Europe Non-Destructive Testing market size in 2025; rental and leasing are the fastest segment at an 8.52% CAGR.

- By end-user, oil and gas accounted for 23.92% share of the Europe Non-Destructive Testing market size in 2025, while industrial manufacturing is advancing at a 9.01% CAGR through 2031.

- By country, Germany commanded 23.88% share of the Europe Non-Destructive Testing market size in 2025, and the United Kingdom is poised for the quickest expansion at a 9.63% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Non-Destructive Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EU Directives On Industrial Safety and Product Liability | +1.8% | Pan-European, with concentrated enforcement in Germany, France, United Kingdom | Medium term (2-4 years) |

| Rising Capital Expenditure In European Aerospace and Defence MRO Facilities | +1.5% | United Kingdom, France, Germany, with spill-over to Spain and Italy | Medium term (2-4 years) |

| Ageing Oil and Gas Assets In The North Sea Demanding Life-Extension Inspections | +1.3% | United Kingdom, Norway (North Sea basin), with indirect demand in Netherlands | Long term (≥ 4 years) |

| Mandatory Periodic Testing Of On-Road Commercial Vehicles Under EU Roadworthiness Package | +1.2% | Pan-European, with early adoption in Germany, France, Spain | Short term (≤ 2 years) |

| Surge In Additive-Manufacturing (AM) Part Qualification Requiring Novel NDT Protocols | +1.0% | Germany, United Kingdom, France (aerospace and industrial hubs) | Medium term (2-4 years) |

| Investments In Small Modular Nuclear Reactors (SMRs) Driving Advanced In-Service Inspection | +0.9% | United Kingdom, France, with exploratory projects in Czech Republic, Romania | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent EU Directives on Industrial Safety and Product Liability

Revisions to the Pressure Equipment Directive, Machinery Regulation, and the Roadworthiness Package have widened the scope and tightened the cadence of mandatory inspections. Commercial vehicles older than 12 years now face annual structural checks, adding roughly 1.2 million inspections across Germany, France, and Spain each year.[1]European Commission, “Roadworthiness Testing and Technical Roadside Inspections,” ec.europa.eu Updated product-liability rules shift the burden of proof onto manufacturers, compelling the creation of auditable, non-destructive testing records in aerospace and medical-device production lines. As compliance becomes non-negotiable, Europe Non-Destructive Testing market demand remains insulated from macro-economic slowdowns and pricing pressure on legacy techniques.

Rising Capital Expenditure in European Aerospace and Defense MRO Facilities

Between 2024 and 2026, GE Aerospace, Safran, and other maintenance organizations committed more than USD 1.25 billion to expand ultrasonic and computed-tomography capacity, shortening engine overhaul cycles and enabling same-shift re-inspection of additive-manufactured parts. The spending wave aligns with Airbus forecasts indicating USD 130 billion in cumulative European MRO outlays to 2031, with NDT accounting for 8% of total costs.[2]Airbus, “Global MRO Forecast 2024-2031,” airbus.com High throughput facilities that integrate inspection data into enterprise asset-management systems now enjoy preferential contract terms, accelerating software adoption and pushing the Europe Non-Destructive Testing market toward predictive analytics.

Ageing Oil and Gas Assets in the North Sea Demanding Life-Extension Inspections

More than 60% of United Kingdom Continental Shelf platforms had served for 30 years or more in 2024, prompting intensified ultrasonic thickness surveys and intelligent-pigging campaigns under revised safety-case regulations. Operators have extended decommissioning timelines by up to 15 years, particularly where carbon-capture retrofits are viable, anchoring long-run inspection workloads. Updated pipeline guidelines from the Energy Institute recommend dual techniques - inline pigs plus external corrosion mapping - shifting spending toward remotely operated vehicle-mounted phased-array probes.

Mandatory Periodic Testing of On-Road Commercial Vehicles under EU Roadworthiness Package

Directive 2014/45/EU has evolved from spot visual checks to compulsory ultrasonic or magnetic-particle examinations of brake systems and chassis components. Germany, France, and Spain adopted the tighter schedules first, raising aggregate annual inspection volume and heightening demand for portable flaw detectors that can deliver pass-or-fail decisions within minutes at roadside stations.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Shortage Of Level-III Certified NDT Personnel | -1.1% | Pan-European, acute in United Kingdom, Germany, France | Short term (≤ 2 years) |

| High Ownership Cost Of Phased-Array Ultrasonic and DR Systems For SMEs | -0.8% | Spain, Italy, Eastern European member states | Medium term (2-4 years) |

| Fragmented EU Standards Harmonisation Delaying Cross-Border Acceptance Of Results | -0.6% | Pan-European, with friction at Germany-Poland, France-Belgium borders | Medium term (2-4 years) |

| Limited Field-Use Robustness Of Emerging Terahertz NDT Solutions | -0.3% | Research-intensive regions: Germany, United Kingdom, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Shortage of Level-III Certified NDT Personnel

Pan-European demand for Level-III ultrasonic and radiographic specialists outstrips supply by 15%, pushing day rates near USD 870 and delaying complex weld inspections.[3]British Institute of Non-Destructive Testing, “NDT Personnel Shortage Report 2024,” bindt.org The five-year experiential requirement embedded in ISO 9712 prolongs the talent gap, while competition from the nuclear sector intensifies scarcity. Automation mitigates routine tasks, but regulatory frameworks still mandate human sign-off, constraining throughput and nudging Europe Non-Destructive Testing market participants to invest in internal academies.

High Ownership Cost of Phased-Array Ultrasonic and Digital Radiography Systems for SMEs

Portable phased-array units start at USD 130,000 and require annual maintenance equaling up to 12% of purchase value. For small firms generating less than EUR 2 million in test revenue, capital intensity is prohibitive, forcing reliance on dated film radiography or subcontracting. Rental programs are expanding, yet the lack of favorable financing in Southern and Eastern Europe sustains a technology gap and caps the addressable base for high-margin software upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Testing Method: Ultrasonic Techniques Retain a One-Third Hold

Ultrasonic solutions accounted for 30.11% of Europe Non-Destructive Testing market share in 2025, favored for detecting subsurface flaws in thick welds, composites, and aged pipeline walls. Large aerospace shops now scan turbine disks in 12 minutes using 128-element phased-array heads, down from 45 minutes with legacy pulse-echo probes.[4]Safran, “Phased-Array Ultrasonic Efficiency Gains,” safran-group.com Radiography remains indispensable for nuclear welds and additive-manufactured parts, while computed tomography is gaining traction to meet EASA Part 21 volumetric mandates. Emerging techniques - terahertz imaging, laser ultrasonics, and AI-assisted thermography - are forecast at an 8.92% CAGR, making them the fastest slice of the Europe Non-Destructive Testing market.

Increasingly, inspection protocols combine modalities. A single wind-turbine tower campaign might deploy drone-based visual surveys, ultrasonic spot checks, and eddy-current arrays for bolt-thread inspections. Vendors able to integrate data from these sources into unified dashboards stand to capture the expanding software layer of the Europe Non-Destructive Testing market.

By Component Type: Services Still Dominate but Software Grabs Margins

Services delivered 49.57% of 2025 revenue as asset owners continued to outsource compliance and liability to accredited providers. Bureau Veritas alone logged USD 1.3 billion in European NDT services during 2024. However, software and analytics platforms are rising at 9.14% CAGR, even as the broader Europe Non-Destructive Testing market advances at 8.22%. Instruments such as Evident’s OmniScan X4 ship with embedded neural networks that classify weld flaws with 92% accuracy, reducing Level-III sign-off time. Gross margins on subscription analytics hover near 70%, double those of labor-intensive services, incentivizing incumbent service giants to acquire niche software firms.

When software is bundled with rental hardware- an approach championed by Zetec and Olympus- customers sidestep upfront capital, while vendors lock in recurring revenue. This inversion of the traditional equipment-sale model is reshaping the profit pool within the Europe Non-Destructive Testing market.

By Service Mode: Outsourcing Remains the Anchor While Rental Gains Momentum

Outsourced inspection services commanded 46.06% of Europe Non-Destructive Testing market share in 2025 as asset owners continued to shift liability for regulatory compliance toward accredited third parties, a strategy that lets operators focus scarce capital and internal talent on core production targets. Multinational providers have reinforced this preference by embedding indemnity clauses and performance dashboards into framework contracts, providing customers with transparent defect-detection metrics across multiple facilities. In-house inspection models persist inside large aerospace and petrochemical groups, yet even these vertically integrated players increasingly subcontract peak-load work to avoid idle equipment during maintenance lulls. Outsourced specialists also leverage dense regional office footprints that cut mobilization costs for offshore campaigns and bridge rehabilitation projects, an advantage unattainable for single-site in-house teams. This structural edge stabilizes pricing power and underpins the services slice of the Europe Non-Destructive Testing market size through the forecast horizon.

Rental and leasing programs are the fastest growing service mode, expanding at an 8.52% CAGR to 2031 as small and medium enterprises in Spain, Italy, and Eastern Europe sidestep six-figure equipment investments and pay weekly or monthly fees instead. Olympus, Zetec, and TÜV Rheinland now bundle rental hardware with cloud analytics subscriptions, transforming one-off equipment hires into recurring revenue streams while giving users access to the newest phased-array and digital-radiography platforms without ownership risk. The model is particularly attractive for episodic projects such as offshore platform decommissioning or high-speed rail weld surveys, where utilization drops sharply after completion. As more suppliers copy this hybrid approach, rental penetration is expected to lift the recurring-revenue mix within the Europe Non-Destructive Testing market size and reduce technology gaps between tier-one contractors and regional specialists.

By End-User Industry: Energy Assets Underpin Demand While Manufacturing Accelerates

Oil and gas applications retained 23.92% of Europe Non-Destructive Testing market share in 2025, buoyed by North Sea life-extension campaigns that mandate ultrasonic wall-thickness checks and intelligent-pig runs every five to seven years to satisfy updated safety-case rules. Subsea pipeline operators are layering external phased-array corrosion mapping onto inline data to refine corrosion-growth models, increasing the inspection spend per kilometer of pipe. Refinery turnarounds reinforce baseline volumes by requiring radiographic weld examinations and ultrasonic nozzle scans each maintenance cycle, even when crude prices soften. This entrenched workload gives service providers predictable revenue and justifies offshore logistics hubs in Aberdeen, Stavanger, and Rotterdam, locking in a resilient core for the Europe Non-Destructive Testing market size.

Industrial manufacturing is projected to grow at a 9.01% CAGR as additive-manufacturing part qualification, electric-vehicle battery-weld integrity, and Industry 4.0 traceability mandates embed non-destructive testing directly on production lines. Automotive plants in Germany now run inline phased-array checks on every battery-pack enclosure, in response to stricter fire-safety scrutiny following several high-profile incidents in 2024. Aerospace suppliers must document computed-tomography scans of powder-bed fusion parts to meet EASA Part 21 requirements, pushing inspection demand beyond traditional MRO cycles into day-to-day fabrication. Together with steady contributions from power generation, transportation, and infrastructure rehabilitation, these drivers diversify revenue streams and lessen reliance on the cyclical oil and gas segment within the broader Europe Non-Destructive Testing market.

Geography Analysis

Germany held 23.88% of the Europe Non-Destructive Testing market size in 2025, underpinned by battery-pack weld inspection across Bavarian and Baden-Württemberg automotive plants and stringent TÜV requirements that embed third-party testing in machinery certification. Fraunhofer’s laser-ultrasonic breakthroughs lifted scan speeds tenfold, positioning domestic vendors for export opportunities.

The United Kingdom is forecast to grow at a 9.63% CAGR through 2031 on the back of Rolls-Royce small modular reactor investments and 5 GW of offshore wind projects that rely on remotely operated vehicle-mounted phased-array probes. Nuclear Advanced Manufacturing Research Centre partnerships are fastening laser-ultrasonic protocols onto compact reactor vessels, carving out a high-margin niche.

France’s 56-reactor nuclear fleet enforces a drumbeat of pressure-vessel and steam-generator tube inspections, anchoring demand for eddy-current and ultrasonic techniques. Safran’s EUR 1 billion MRO upgrade consolidates computed-tomography capacity in Toulouse and Villaroche, accelerating turnaround times for composite fan blades.

Italy and Spain see episodic spikes tied to bridge rehabilitation and high-speed rail expansion, yet smaller industrial footprints temper sustained growth. Poland, Czech Republic, and Romania offer lower labor costs and ISO 17020 accreditation, attracting cross-border contracts but also dispersing qualified personnel, which intensifies the already acute Level-III shortage across the Europe Non-Destructive Testing market.

Competitive Landscape

Multinational service houses- Bureau Veritas, Intertek, SGS, Applus, and TÜV Nord- collectively hold just under 40% share, translating to a moderate concentration score. Their edge rests on multi-country accreditation, site density that reduces mobilization costs, and proprietary digital platforms that integrate ultrasonic, radiographic, and eddy-current data. Equipment specialists such as Eddyfi Technologies are vertically integrating through acquisitions, including Magnifi, to merge phased-array and eddy-current portfolios.

Smaller innovators exploit white spaces. Sonatest’s 1.8 kg handheld phased-array device reaches confined spots in offshore rigs, while NOVO DR’s lightweight digital panels fit wing-box inspections where standard detectors cannot. The Europe Non-Destructive Testing market thus balances scale players with agile specialists, and differentiation is shifting from hardware features to software-driven, real-time defect analytics.

Europe Non-Destructive Testing Industry Leaders

Baker Hughes Company

Bureau Veritas SA

Applus Servicios Tecnológicos S.L.U.

Intertek Group plc

Olympus Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Bureau Veritas commissioned three additional computed-tomography systems in Rotterdam, doubling its digital radiography throughput for additive-manufactured aerospace parts.

- October 2025: Bureau Veritas installed Yxlon MU2000-D CT systems in Rotterdam, cutting AM part inspection turnaround from six days to 18 hours.

- September 2025: Rolls-Royce received a GBP 210 million (USD 268 million) contract for small modular reactors, embedding advanced ultrasonic and radiographic requirements in procurement specs.

- July 2025: Eddyfi Technologies released Lyft 2.0 software, raising phased-array flaw-classification accuracy to 94% and slashing Level-III review labor by 65%.

- June 2025: GE Aerospace completed an USD 85 million expansion at Prestwick, adding automated ultrasonic cells that process 120 turbine blades per shift.

Europe Non-Destructive Testing Market Report Scope

The Europe Non-Destructive Testing Market Report is Segmented by Testing Method (Radiography, Ultrasonic, Magnetic Particle, Liquid Penetrant, Visual and Remote Visual, Electromagnetic and Eddy-Current, Emerging Techniques), Component Type (Equipment, Software and Analytics Platforms, Services), Service Mode (In-house, Outsourced, Rental and Leasing), End-User Industry (Oil and Gas, Aerospace and Defense, Automotive and Transportation, Power Generation, Industrial Manufacturing, Construction and Infrastructure, Other End-User Industries), and Geography (United Kingdom, Germany, France, Italy, Spain, Other Countries). The Market Forecasts are Provided in Terms of Value (USD).

| Radiography (Film, Digital, CT) |

| Ultrasonic (Conventional, PAUT, TOFD) |

| Magnetic Particle |

| Liquid Penetrant |

| Visual and Remote Visual |

| Electromagnetic and Eddy- Current |

| Emerging Techniques |

| Equipment |

| Software and Analytics Platforms |

| Services |

| In-house Inspection |

| Outsourced/Third-Party Inspection |

| Rental and Leasing |

| Oil and Gas |

| Aerospace and Defense |

| Automotive and Transportation |

| Power Generation |

| Industrial Manufacturing |

| Construction and Infrastructure |

| Other End-User Industries |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Other Countries |

| By Testing Method | Radiography (Film, Digital, CT) |

| Ultrasonic (Conventional, PAUT, TOFD) | |

| Magnetic Particle | |

| Liquid Penetrant | |

| Visual and Remote Visual | |

| Electromagnetic and Eddy- Current | |

| Emerging Techniques | |

| By Component Type | Equipment |

| Software and Analytics Platforms | |

| Services | |

| By Service Mode | In-house Inspection |

| Outsourced/Third-Party Inspection | |

| Rental and Leasing | |

| By End-User Industry | Oil and Gas |

| Aerospace and Defense | |

| Automotive and Transportation | |

| Power Generation | |

| Industrial Manufacturing | |

| Construction and Infrastructure | |

| Other End-User Industries | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Other Countries |

Key Questions Answered in the Report

How large is the Europe Non-Destructive Testing market in 2026?

The market reached USD 7.02 billion in 2026 and is forecast to rise to USD 10.42 billion by 2031 at an 8.22% CAGR.

Which testing method commands the biggest share?

Ultrasonic techniques held 30.11% of 2025 revenue, thanks to their versatility in aerospace, pipeline, and composite inspections.

What end-user sector is growing fastest?

Industrial manufacturing is expanding at a 9.01% CAGR as additive-manufacturing part qualification and battery-pack weld testing accelerate demand.

Why is the United Kingdom the fastest-growing country market?

Nuclear new-build projects, offshore wind foundation monitoring, and Rolls-Royce small modular reactor manufacturing drive a 9.63% CAGR through 2031.

How are vendors addressing the Level-III inspector shortage?

Service providers are investing in internal academies and deploying AI-enabled instruments that automate defect classification, reducing reliance on scarce experts.

Page last updated on: