Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

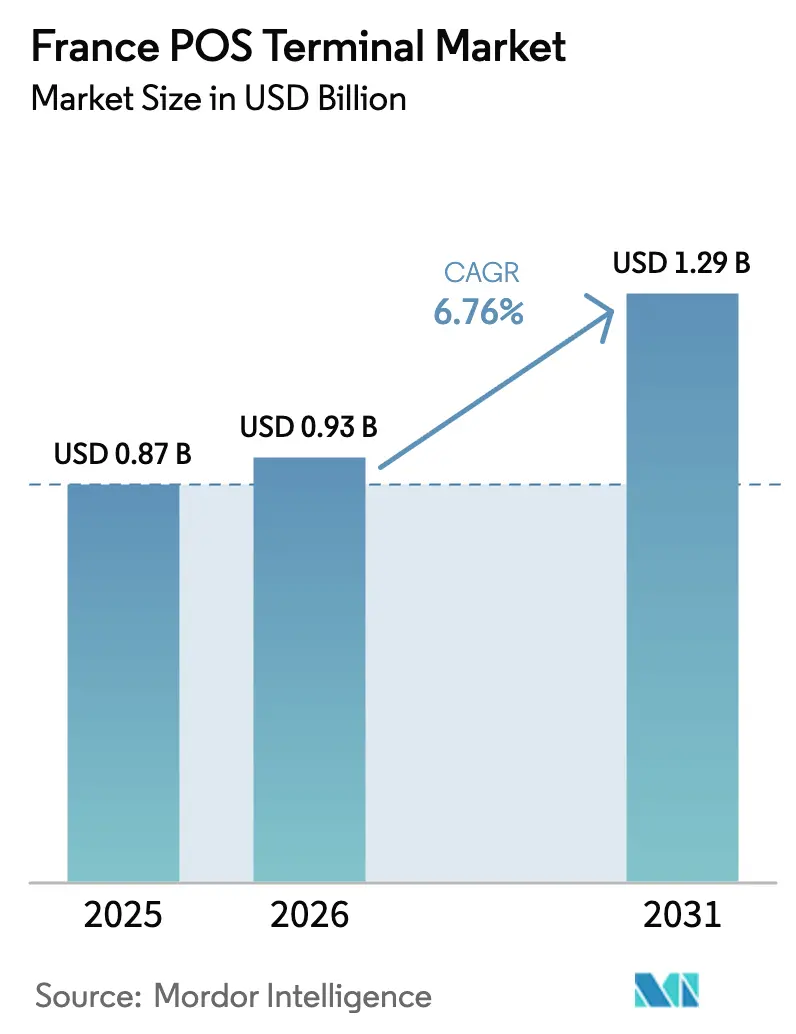

| Base Year Market Size (2025) | USD 0.87 Billion |

| Market Size (2026) | USD 0.93 Billion |

| Market Size (2031) | USD 1.29 Billion |

| Growth Rate (2026 - 2031) | 6.76% CAGR |

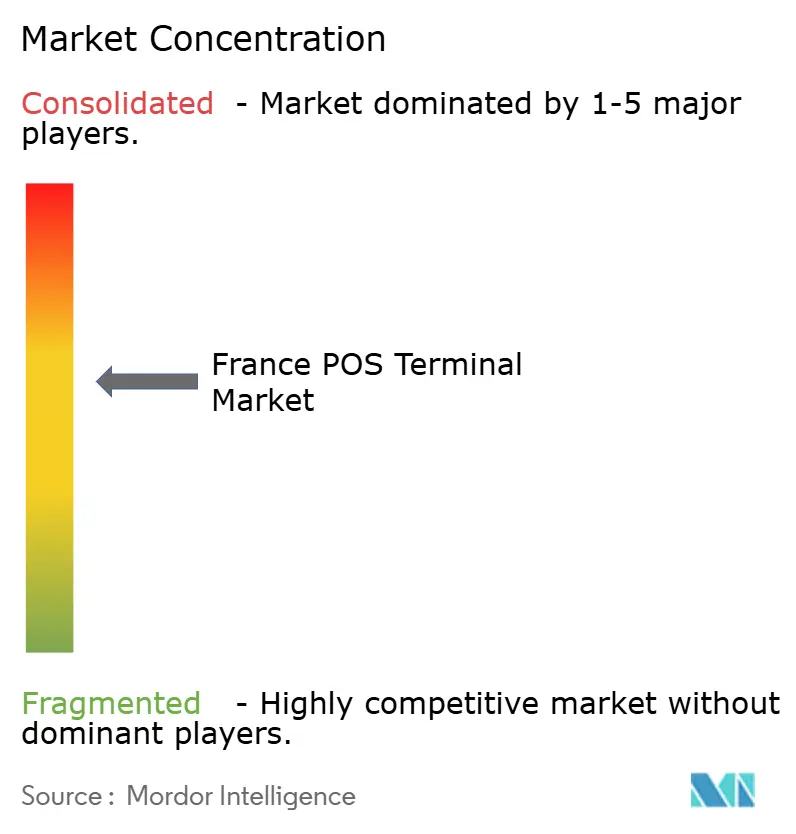

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France POS Terminal Market Analysis by Mordor Intelligence

The France POS Terminal Market size is expected to grow from USD 0.87 billion in 2025 to USD 0.93 billion in 2026 and is forecast to reach USD 1.29 billion by 2031 at a 6.75% CAGR over 2026-2031. The expansion reflects a structural pivot toward cash-lite commerce as card payments overtook cash for the first time in 2024, while contactless transactions already account for more than two-thirds of in-store card activity. Regulatory mandates such as PSD2-driven strong customer authentication, the transition to NF525 third-party certification, and early preparations for a digital euro are compressing upgrade timelines and compelling acquirers to prioritize crypto-agile hardware that can be patched over-the-air. Retailers are synchronizing terminal refresh cycles with broader store-digitalization programs that bundle electronic shelf labels, computer-vision cameras, and real-time inventory feeds.

Meanwhile, micro-merchants are migrating to SoftPOS and tap-to-pay applications that remove the capital barrier of dedicated hardware, reshaping competitive dynamics across the France POS terminal market. Key secular forces include omnichannel retail adoption, the rise of mobile-first consumer journeys, and emerging sustainability procurement rules that reward energy-efficient, modular devices. Strategic responses range from cloud device-management suites that slash truck-roll costs to open-API Android terminals that let merchants embed loyalty, digital ID, and dynamic pricing apps at the point of sale. Although France is a mature card market, the looming post-quantum cryptography transition and stricter PCI DSS v4.0 obligations will continue to stoke replacement demand, sustaining mid-single-digit growth even as traditional checkout lanes see lower foot traffic.

Key Report Takeaways

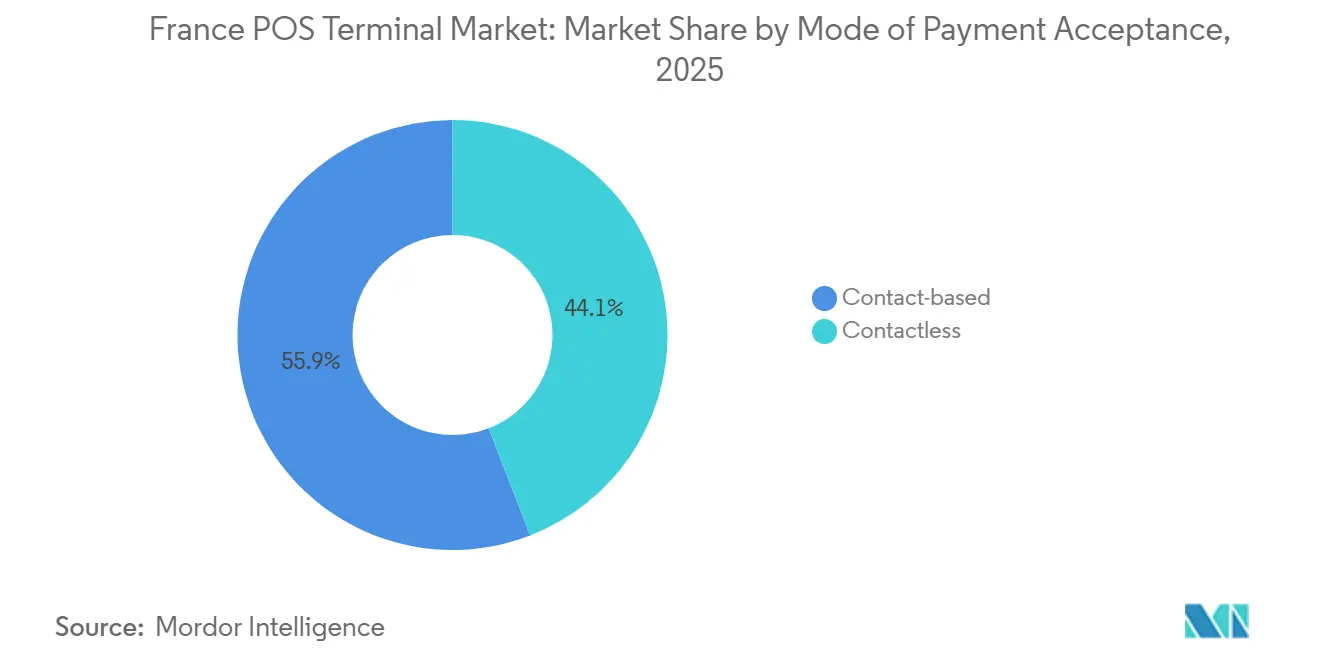

- By mode of payment acceptance, contact-based terminals led with 55.89% of the France POS terminal market share in 2025, while contactless systems are advancing at a 7.43% CAGR through 2031.

- By POS type, fixed systems captured 61.97% of the France POS terminal market size in 2025, yet mobile and portable terminals are projected to expand at an 8.04% CAGR between 2026-2031.

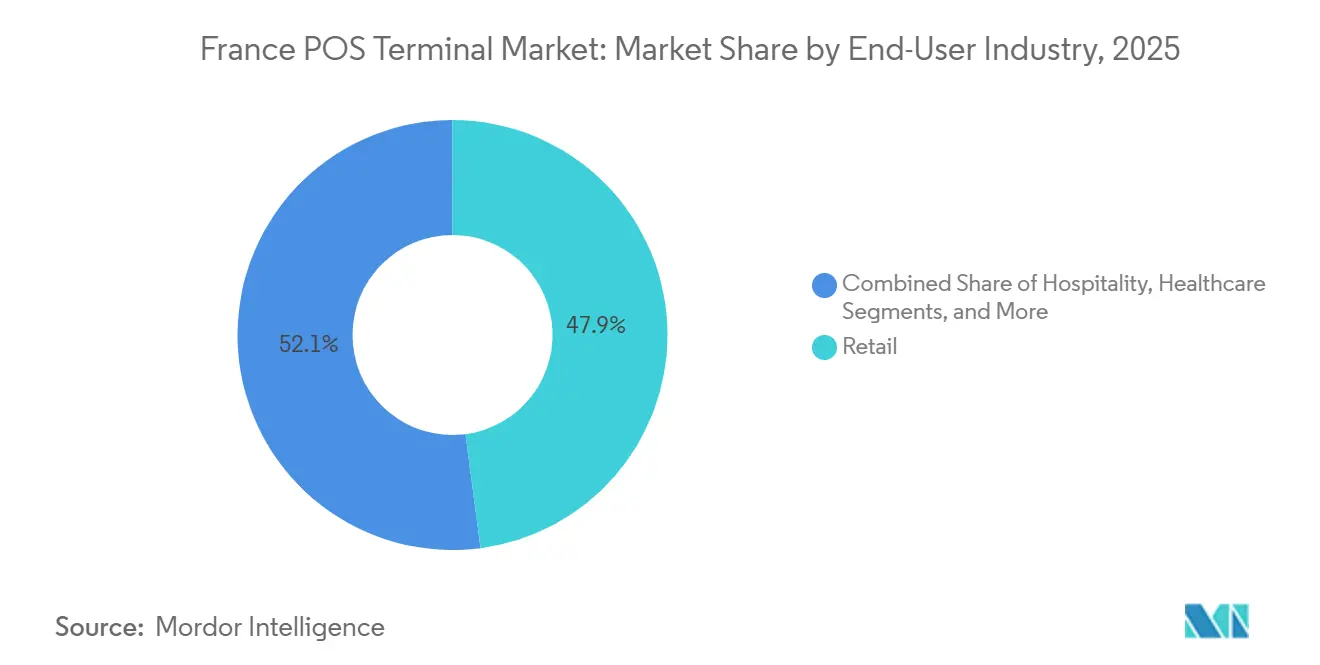

- By end-user industry, retail dominated with 47.92% share of the France POS terminal market size in 2025, but healthcare is forecast to record the fastest 7.27% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France POS Terminal Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Contactless-Payment Penetration | +1.8% | Île-de-France, Auvergne-Rhône-Alpes, Provence-Alpes-Côte d’Azur | Short term (≤ 2 years) |

| Omnichannel Retail Digitalization | +1.5% | Hypermarket chains in metropolitan areas | Medium term (2-4 years) |

| Cash-Lite Policies and PSD2 Security Upgrades | +1.2% | National, aligned with EU directives | Medium term (2-4 years) |

| SoftPOS and Tap-to-Pay Adoption | +1.0% | Sole traders and micro-enterprises nationwide | Short term (≤ 2 years) |

| Carbon-Neutral Procurement Mandates | +0.4% | CAC 40 retailers and cooperative groups | Long term (≥ 4 years) |

| In-Person Digital ID Verification | +0.6% | Tobacco, alcohol, and pharmacy retail | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Contactless-Payment Penetration Among French Consumers

Contactless activity already represented 68% of in-store card payments in 2023, and velocity limits imposed by the Banque de France now require dual-interface NFC chipsets for every new terminal. Consumers embraced tap-and-go during the pandemic, and the behavioral shift has persisted as card payments surpassed cash for 48% versus 43% of transaction value in 2024. The rollout of the Wero wallet in 2024 and the sunset of Paylib in 2025 widen the addressable base for wallets that demand smartphone-friendly acceptance flows. Hardware vendors are responding with Android 14 terminals that feature dual screens and EMV Level 3 certification, letting merchants push loyalty offers while processing tap transactions. As mobile-initiated payments are projected to exceed 15% of in-store volume by 2027, the France POS terminal market participants that embed crypto-agile firmware and QR-ready optics today stand to capture outsized upgrade spend.

Omnichannel Retail Digitalization Accelerating POS Refresh Cycles

Grocery and hypermarket operators lifted IT capex by 13.9% between 2021-2023, channeling funds into edge-computing pilots that synchronize shelf labels, cameras, and smart rails. Carrefour’s EdgeSense store integrates 70,000 electronic labels and 500 cameras, a topology that demands terminals capable of sub-second inventory calls and remote configuration of apps. Mergers such as Auchan’s EUR 1.3 billion (USD 1.47 billion) acquisition of Casino stores have further complicated estate management, incentivizing acquirers to standardize on cloud-connected devices that can be patched centrally. Vendors that deliver Manage-360-style device orchestration reduce truck-roll costs by up to 40%, a saving that resonates with retailers juggling razor-thin grocery margins. As French operators replicate Dutch blueprints for digital-first supermarkets, the France POS terminal market will lean heavily toward Android, edge-native hardware capable of running multiple micro-services in-store.[1]VusionGroup, “Carrefour and VusionGroup Unveil EdgeSense,” vusiongroup.com

EU and National Policies Promoting Cash-Lite Economy and PSD2-Driven Security Upgrades

The revised PSD2 cut online fraud by 40% between 2018-2024 and is now cascading into brick-and-mortar environments via dynamic linking requirements. France’s NF525 rules migrated from self-declaration to compulsory third-party audits in February 2025, setting off a scramble among merchants to certify before the March 2026 deadline. The European Central Bank’s October 2025 digital-euro blueprint introduces offline, privacy-preserving payments that will require terminal firmware capable of dual-ledger settlement. Compliance layers such as PCI DSS v4.0, EU Instant Payments Regulation, and the EU Accessibility Act collectively drive hardware to evolve in lockstep with cybersecurity and inclusivity norms. Vendors that secured PTS POI 7.0 certification early are best positioned to capitalize on France POS terminal market refresh cycles as acquirers chase audit deadlines.

SoftPOS and Tap-to-Pay on Smartphones Slashing Hardware TCO for Micro-Merchants

Apple’s 2024 launch of Tap to Pay on iPhone and similar Android SoftPOS solutions remove upfront hardware costs that previously ranged from EUR 200-700 (USD 226-791). Transaction-fee-only models resonate with France’s 3.9 million SMEs, many of which balk at rental charges of EUR 15-80 (USD 17-90) per month for a traditional terminal. SumUp’s 2025 all-in-one device priced at EUR 199 (USD 226) with 0.9% fees underscores a secular push toward sub-2% acquiring economics. The three-year total cost of ownership for SoftPOS can fall 30-50% below legacy devices when factoring in maintenance, recertification, and compliance. As more acquirers white-label tap-to-pay apps, the addressable French estate of 2.6 million terminals is poised for cannibalization, yet incremental micro-merchant adoption keeps overall unit shipments in positive territory.[2]SumUp, “SumUp Card Readers,” sumup.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Terminal and Maintenance Costs | -0.9% | Sole traders and micro-enterprises nationwide | Short term (≤ 2 years) |

| Heightened PCI-DSS and SCA Compliance Burden | -0.7% | Independent retailers across France | Medium term (2-4 years) |

| Post-Quantum Cryptography Upgrade Pressure | -0.5% | All terminal vendors and acquirers nationwide | Long term (≥ 4 years) |

| Foot-Traffic Shift Toward E-Commerce | -0.6% | Urban centers and suburban malls | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Terminal and Maintenance Costs for French SMEs

Purchase prices span EUR 50-700 (USD 57-791), or EUR 15-80 (USD 17-90) monthly on rental plans, placing a heavy burden on France’s fragmented SME landscape. Annual PCI DSS compliance can add USD 1,000-10,000 for small firms once encryption, tokenization, and quarterly scans are factored in. NF525 third-party audits now cost EUR 500-2,000 (USD 565-2,260) per terminal model every three years, tightening cash flow for businesses that operate on slim margins. While SoftPOS can neutralize hardware outlay, per-transaction fees near 2% remain prohibitive for low-ticket sectors such as cafés and bakeries. As a result, cost remains the chief drag on the France POS terminal market's CAGR, especially outside dense urban corridors.[3]Stripe, “PCI DSS Compliance Costs,” stripe.com

Heightened PCI-DSS and SCA Cybersecurity Compliance Burden

Mandatory PCI DSS v4.0 implementation has introduced 64 new control points, from multi-factor admin access to quarterly vulnerability scanning, raising compliance workloads by 30%. Network segmentation and SIEM subscriptions can exceed USD 50,000 annually for multi-location retailers. PSD2’s dynamic-linking rules extend strong customer authentication to in-store payments, forcing acquirers to deploy secure-element chips and tamper sensors. Vendors must now juggle separate firmware branches for each EU jurisdiction, inflating development costs by up to 20%. The compounded burden slows rollouts and discourages independents from upgrading, shaving 70 basis points off the France POS terminal market growth outlook.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment Acceptance: Contactless Ascends as Dual-Interface Default

Contact-based units still generated the largest slice of revenue in 2025 with 55.89% France POS terminal market share, yet their dominance is eroding as consumers flock to tap-and-go convenience. Contactless-ready shipments are forecast to register a 7.43% CAGR through 2031, fueled by OSMP velocity caps that penalize chip-and-PIN retries and by the phasing-out of single-interface hardware. The France POS terminal market size for contactless devices is therefore on course to leapfrog contact-based models well before the forecast horizon.

Emerging use cases such as the Wero wallet, QR-driven age verification, and offline digital-euro payments require terminals to toggle seamlessly between NFC, QR, and chip. Vendors are embedding dual screens and Android open APIs to let merchants run loyalty or inventory apps side-by-side with payment flows. As SoftPOS proliferates, dedicated hardware demand concentrates in high-throughput lanes - fuel, grocery, mass transit - where rapid tap processing and ruggedized form factors remain indispensable.

By POS Type: Mobile and Portable Units Chip Away at Fixed-Lane Supremacy

Fixed systems captured 61.97% of 2025 revenue, anchoring checkout counters in France’s dense hypermarket network. However, mobile and portable terminals are projected to expand at an 8.04% CAGR, reflecting a structural shift toward tableside and curbside fulfillment. The France POS terminal market size for mobile devices will be lifted by public-transport deployments such as RATP’s EUR 100 million (USD 113 million) contactless bus initiative and by the growth of outdoor events, pop-ups, and quick-service restaurants.

Edge-native pilots show handhelds slashing average queue time by 25% and enabling staff to upsell while roaming the aisles. SoftPOS lowers the entry point further, letting micro-merchants accept EUR 29-199 (USD 33-226) hardware with embedded 4G connections, or zero-cost phone-based acceptance models. Fixed lanes will persist for bulk-basket grocery and self-checkout, yet estate growth skews decisively toward portable devices over the forecast window.

By End-User Industry: Digital Vitale Ignites Healthcare Outlays

Retail remained the largest buyer in the France POS terminal market in 2025, with a 47.92% share, but healthcare is the clear growth engine, posting a projected 7.27% CAGR through 2031. The mandatory Digital Vitale smartphone app that launched in November 2025 forces every French pharmacy, clinic, and hospital to install NFC or QR code readers to stay eligible for reimbursement, unlocking a multi-year refresh wave across more than 21,000 pharmacies alone.

Hospitals are layering QR-based patient check-ins and on-premise meal payments onto the same hardware, further expanding terminal counts. Hospitality also logs strong momentum as restaurants and cafés streamline tableside service with portable terminals that sync automatically to cloud POS suites. Transportation, fueled by contactless ticketing rollouts, rounds out the roster of fast-growing adopters and keeps the France POS terminal market squarely geared toward vertical-specific feature sets.

Geography Analysis

France’s demand concentrates in Île-de-France, which hosts the nation’s densest retail footprint, the largest transit network, and headquarters of top acquirers. The region’s early adoption of SoftPOS and digital ID initiatives accelerates hardware churn cycles. Auvergne-Rhône-Alpes ranks second, buoyed by tourism inflows to Lyon and the Alpine resorts, where hospitality venues embrace mobile terminals for tableside settlement. Provence-Alpes-Côte d’Azur follows, with luxury retail and cruise-port volumes sustaining premium Android terminal deployments.

The Grand Est and Hauts-de-France corridors display moderate growth, propelled by cross-border commerce with Germany and Belgium, respectively, which incentivizes merchants to support multi-currency wallets and dynamic currency conversion. Occitanie and Nouvelle-Aquitaine see upticks driven by agrifood cooperatives digitizing farmers-market sales through low-cost SoftPOS apps. Brittany and Normandy trail due to a higher proportion of cash-reliant micro-businesses, though transit pilots such as Worldline’s Titre Unique program signal future upside.

Corsica and the overseas departments represent niche opportunities where acquirers bundle satellite connectivity with ruggedized wireless terminals to overcome patchy broadband. Overall, urban density, tourism intensity, and regional subsidy programs for digitalization determine the pace of hardware replacement, creating a layered demand profile across the France POS terminal market.

Competitive Landscape

The France POS terminal market is moderately concentrated: the top three incumbents—Ingenico, Verifone, and PAX Technology—command roughly 60% combined share, while a long tail of regional specialists addresses vertical micro-niches. Competition sharpened in 2025 when SoftPOS newcomers such as Apple Tap to Pay, Worldline, SumUp, and Zettle slashed entry costs and shifted revenue pools from hardware margin to per-transaction fees. Incumbents retaliated with modular Android devices, higher recycled-content thresholds, and cloud orchestration platforms like Ingenico Manage 360 that trim truck-roll by 40%.

Certification agility is emerging as a moat. Newland’s early PCI PTS POI 7.0 accreditation and Castles' compliance whitepaper position both to win audit-driven refresh deals, especially as ANSSI urges crypto-agile firmware ahead of post-quantum deadlines. Partnerships also matter: Verifone’s biometric tie-up with PopID embeds age verification at the terminal, sidestepping CNIL’s clampdown on standalone AI cameras, while Castles and nexo’s rollout across 7,000 TotalEnergies forecourts highlights the value of open-standard stacks.

Market entry barriers remain moderate because rental financing, white-label SoftPOS, and Android developer ecosystems compress time-to-market. Nonetheless, switching costs rise once merchants integrate loyalty, inventory, and analytics apps, tilting renewals toward incumbents that keep device APIs backward-compatible. Sustainability weighting in retailer tenders gives an edge to suppliers that certify recycled plastics, lower idle-power draw, and run circular take-back programs. On balance, the France POS terminal market is expected to remain a battleground between hardware incumbents moving up the software stack and fintech entrants aiming to commoditize acceptance.

France POS Terminal Industry Leaders

Diebold Nixdorf

Zettle (Paypal)

PAX Technology

Ingenico Group SA (Worldline)

SumUp Payments Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Castles Technology released its “POS Compliance in 2026” whitepaper outlining firmware-branching needs under new EU regulations.

- October 2025: The European Central Bank published a digital euro progress report that will require crypto-agile terminal upgrades.

- September 2025: Ingenico introduced Manage 360, a cloud device-management suite promising 40% truck-roll savings.

- July 2025: SumUp launched its EUR 199 (USD 226) all-in-one terminal with 0.9% card fees.

France POS Terminal Market Report Scope

The France POS Terminal Market Report is Segmented by Mode of Payment Acceptance (Contact-based, Contactless), POS Type (Fixed Point-of-Sale Systems, Mobile and Portable Point-of-Sale Systems), End-User Industry (Retail, Hospitality, Healthcare, Transportation and Logistics, Other End-User Industries), and Geography (France). The Market Forecasts are Provided in Terms of Value (USD).

By Mode of Payment Acceptance

| Contact-based |

| Contactless |

By POS Type

| Fixed Point-of-Sale Systems |

| Mobile and Portable Point-of-Sale Systems |

By End-User Industry

| Retail |

| Hospitality |

| Healthcare |

| Transportation and Logistics |

| Other End-User Industries |

| By Mode of Payment Acceptance | Contact-based |

| Contactless | |

| By POS Type | Fixed Point-of-Sale Systems |

| Mobile and Portable Point-of-Sale Systems | |

| By End-User Industry | Retail |

| Hospitality | |

| Healthcare | |

| Transportation and Logistics | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the expected compound annual growth rate for France POS terminals between 2026-2031?

The France POS terminal market is projected to grow at a 6.76% CAGR from 2026 to 2031.

Which payment-acceptance mode is growing fastest?

Contactless systems are advancing at a 7.43% CAGR, outpacing contact-based devices.

Why is healthcare the fastest-growing vertical?

The nationwide rollout of the Digital Vitale smartphone app mandates NFC or QR-equipped readers at pharmacies and clinics, pushing a 7.27% CAGR for healthcare terminals.

How are SoftPOS solutions affecting hardware demand?

SoftPOS and tap-to-pay apps remove upfront device costs, cutting total ownership by up to 50% and expanding acceptance among 3.9 million French SMEs.

What regulatory deadlines should merchants watch?

Key timelines include NF525 third-party certification by March 1 2026 and full PCI DSS v4.0 compliance already in force since 2024.

Which companies lead the market today?

Ingenico, Verifone, and PAX Technology together hold about 60% share, with SumUp, Zettle, and Apple Tap to Pay driving new competitive pressure.

Page last updated on: