CBD Edibles Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

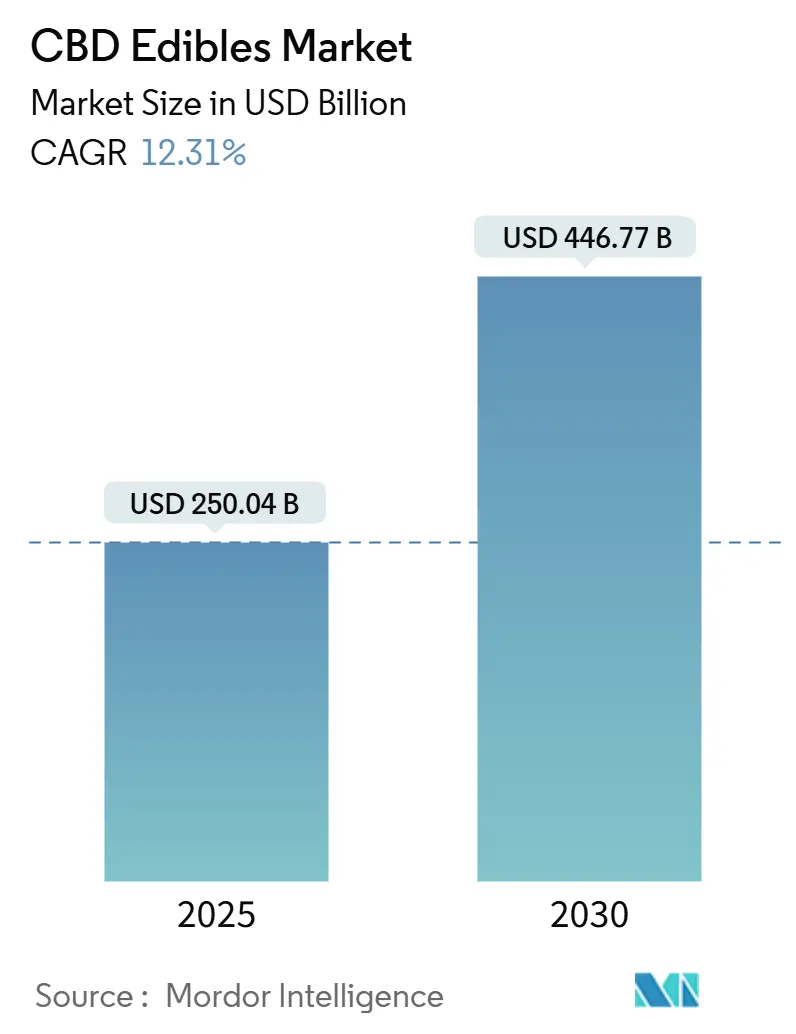

| Market Size (2025) | USD 250.04 Billion |

| Market Size (2030) | USD 446.77 Billion |

| Growth Rate (2025 - 2030) | 12.31% CAGR |

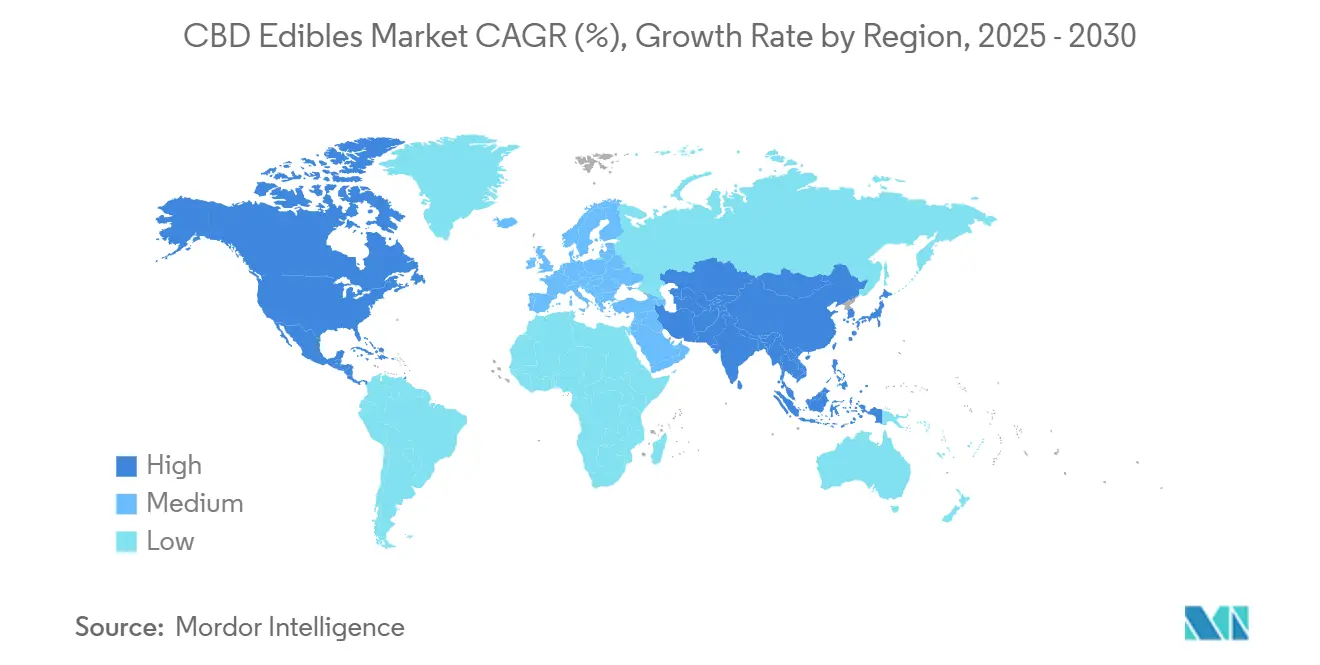

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

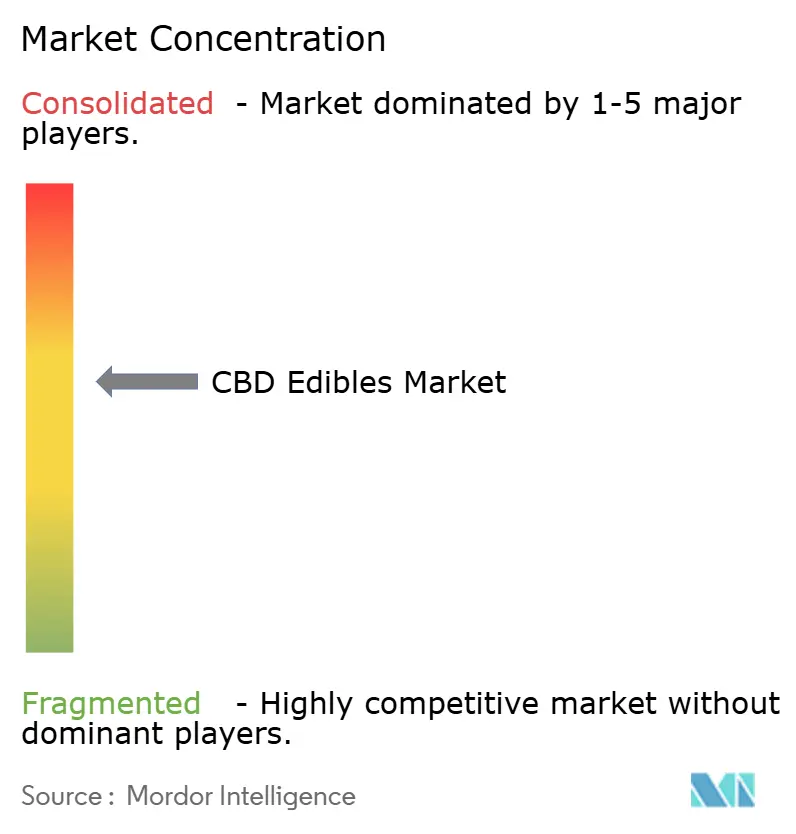

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

CBD Edibles Market Analysis by Mordor Intelligence

The CBD Edibles Market size is estimated at USD 250.04 billion in 2025, and is expected to reach USD 446.77 billion by 2030, at a CAGR of 12.31% during the forecast period (2025-2030). his growth trajectory positions CBD (Cannabidiol) edibles as a pivotal segment within the broader wellness and nutraceutical landscape, driven by evolving regulatory frameworks and shifting consumer preferences toward plant-based therapeutic alternatives. The market's resilience stems from increasing scientific validation of cannabidiol's therapeutic properties, with peer-reviewed research highlighting its efficacy in managing anxiety, chronic pain, and sleep disorders. North America remains the primary revenue hub, yet the Asia-Pacific region is the fastest mover thanks to landmark rule changes in Japan and broader policy softening across Southeast Asia. Product innovation—from nanotechnology-enabled chocolate miniatures to child-resistant paperboard packs—broadens use cases and drives premiumization. At the same time, enhanced age-verification tools in e-commerce channels unlock incremental reach while satisfying compliance requirements.

Key Report Takeaways

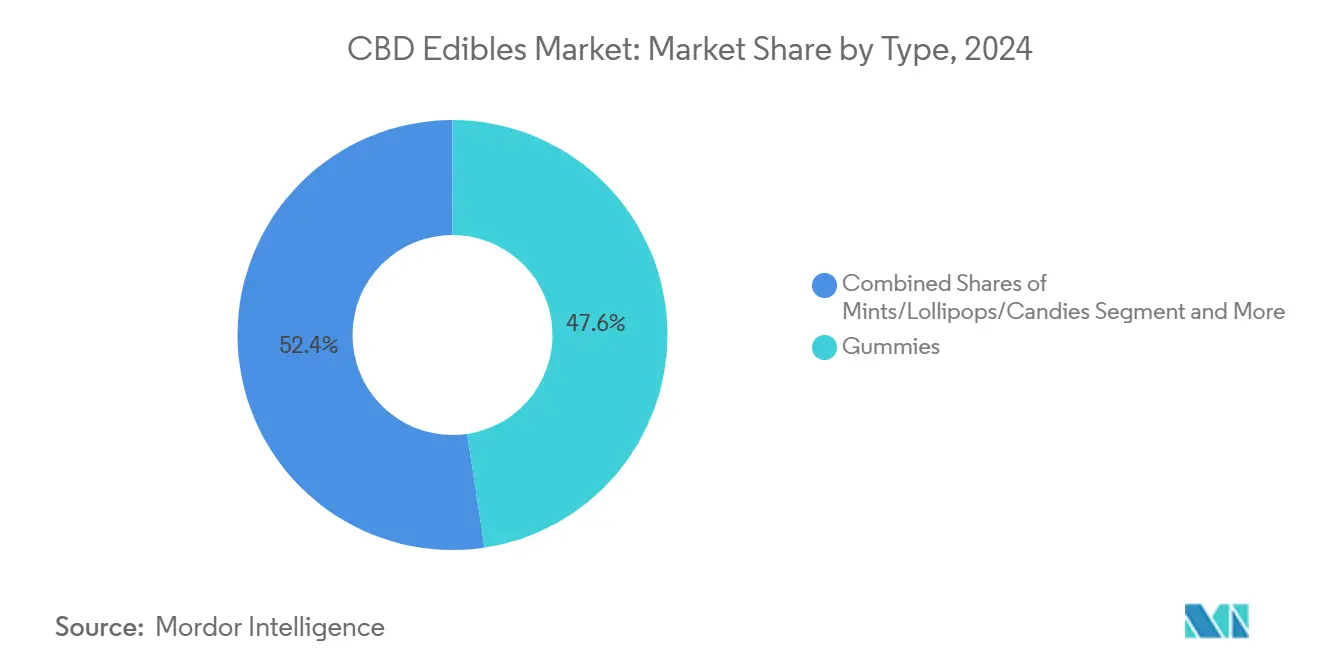

- By type, gummies led with 47.63% revenue share in 2024, whereas mints/lollipops/candies are projected to expand at a 14.33% CAGR through 2030.

- By category, conventional items held 75.22% of the CBD edibles market share in 2024; certified-organic formats are on track for a 12.78% CAGR to 2030.

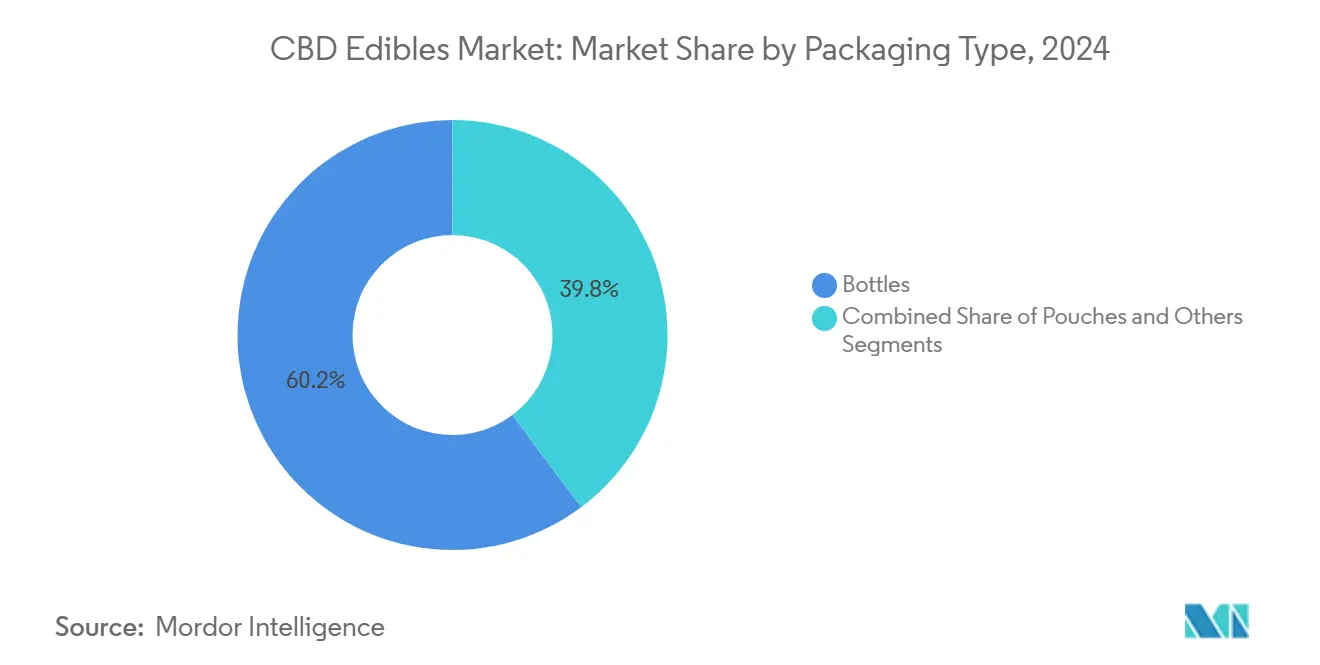

- By packaging, bottles accounted for 60.21% share of the CBD edibles market size in 2024, while pouches are advancing at a 13.21% CAGR during the forecast horizon.

- By distribution channel, offline stores captured 63.74% of 2024 sales; online platforms register the highest projected CAGR at 12.65% to 2030.

- By geography, North America generated 39.09% of 2024 revenues, whereas Asia-Pacific is forecast to record a 13.76% CAGR through 2030.

Global CBD Edibles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer awareness about therapeutic and wellness benefits of CBD edibles | +2.8% | Global, with strongest adoption in North America & Europe | Medium term (2-4 years) |

| Increasing legalization and decriminalization of cannabis products globally | +3.2% | Asia-Pacific core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Expanding product innovation and diversification | +2.1% | North America & EU leading, with rapid adoption in Asia-Pacific | Short term (≤ 2 years) |

| Growing online sales channels offering convenience and wider availability | +1.9% | Global, with accelerated penetration in urban markets | Short term (≤ 2 years) |

| Increasing preference for natural and plant-based wellness products | +1.7% | North America & Europe, expanding to Asia-Pacific markets | Medium term (2-4 years) |

| Growing social acceptance and reduced stigma among younger demographics | +1.4% | Global, with fastest adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Awareness About Therapeutic and Wellness Benefits

Scientific validation of CBD's therapeutic mechanisms drives mainstream adoption beyond recreational consumption patterns. Peer-reviewed research demonstrates CBD's interaction with the endocannabinoid system, showing measurable efficacy in treating epilepsy, chronic pain, and anxiety disorders, with the FDA's approval of Epidiolex establishing regulatory precedent for cannabinoid-based therapeutics. Consumer surveys indicate 20.6% of U.S. adults used CBD in 2022, with higher prevalence among women and individuals with chronic health conditions, suggesting targeted therapeutic applications rather than broad recreational use. Healthcare provider education programs and patient advocacy initiatives accelerate professional endorsement, while third-party clinical trials provide the evidence base necessary for insurance coverage discussions. The shift from anecdotal testimonials to peer-reviewed efficacy data fundamentally alters consumer purchasing decisions, with 71.4% of users prioritizing third-party testing results over marketing claims. This evidence-based approach creates sustainable demand growth independent of regulatory volatility or market speculation.

Increasing Legalization and Decriminalization Globally

Regulatory harmonization across jurisdictions creates unprecedented market access opportunities, with 47 U.S. states and Washington D.C. implementing some form of cannabis legalization by 2024. Japan's December 2024 cannabis law amendments represent the most significant regulatory shift in 75 years, transitioning from component-based to residue-limit regulations with specific THC thresholds for different product categories [1]Source: Japan Cannabis Industry Association, "Formulation and publication of voluntary guidelines for cannabinoid-containing foods", prtimes.jp. The European Union's novel food classification creates standardized safety assessment protocols, though the European Commission's proposal to classify flower-derived CBD as narcotic substances introduces regulatory uncertainty that could fragment market access. Canada's Cannabis Act amendments streamline licensing requirements and expand production thresholds for micro-class operators, reducing barriers to market entry while maintaining quality standards [2]Source: Canada Gazette, "Canada's Cannabis Act", gazette.gc.ca. International treaty obligations under UN conventions continue constraining cross-border trade, yet bilateral agreements and regional harmonization initiatives suggest gradual liberalization trajectories that will unlock global supply chain efficiencies.

Expanding Product Innovation and Diversification

Expanding product innovation and diversification serve as crucial drivers for the CBD edibles market, fueling both consumer interest and sustained market growth. Companies are continually introducing new edible formats—ranging from classic gummies and chocolates to emerging categories like teas, coffees, and functional snacks—catering to a wide spectrum of tastes and wellness needs. Innovations extend beyond just formats and flavors; there is also increasing emphasis on clean-label ingredients, organic certifications, vegan or gluten-free options, and even targeted formulations combining CBD with supportive botanicals or vitamins. This wave of product diversification not only broadens consumer choice but also addresses evolving regulatory demands and helps brands carve out unique identities amid intense competition. With consumers seeking novel, enjoyable ways to incorporate CBD into their daily routines, ongoing innovation ensures the market remains dynamic, responsive, and positioned for robust growth.

Growing Social Acceptance and Reduced Stigma Among Younger Demographics

Growing social acceptance and reduced stigma among younger demographics are significant drivers boosting the global CBD edibles market. Younger consumers, particularly Millennials and Gen Z, increasingly view CBD as a natural, wellness-oriented supplement rather than a controlled or taboo substance. This demographic shift is fueled by widespread education, social media influence, celebrity endorsements, and a broader cultural trend towards holistic health and self-care. As stigma around cannabis-derived products diminishes, these consumers are more willing to try CBD edibles as part of their daily routines for stress relief, anxiety management, and overall wellness. Their openness encourages innovation in product flavors, formats, and branding tailored to youthful preferences, further propelling market penetration. This growing acceptance among younger buyers is expanding the consumer base and driving sustained revenue growth in the CBD edibles sector, contributing to a market projected to grow at a CAGR of approximately 13-15% from 2025 through 2030

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competitive pressure from alternative cannabinoid products and other supplements | -1.8% | Global, with intensified competition in mature markets | Short term (≤ 2 years) |

| Illicit or counterfeit products flooding some markets, harming trust and safety | -2.3% | Developing markets and regions with weak enforcement | Medium term (2-4 years) |

| Supply chain disruptions including raw material sourcing and production bottlenecks | -1.4% | Global, with acute impact on import-dependent regions | Short term (≤ 2 years) |

| Persistent stigma and misconceptions about cannabis-derived products among some consumers | -1.1% | Conservative markets and older demographic segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Illicit or Counterfeit Products Flooding Markets

Regulatory enforcement gaps enable unscrupulous operators to distribute substandard products that undermine consumer confidence and legitimate market development. The FDA's joint action with the FTC against companies selling copycat Delta-8 THC products demonstrates the scope of enforcement challenges, with over 300 adverse events reported between 2021 and 2023 leading to hospitalizations [3]Source: U.S Food & Drug Administration, "FDA, FTC Continue Joint Effort to Protect Consumers Against Companies Illegally Selling Copycat Delta-8 THC Food Products", fda.gov. California's revocation of testing laboratory licenses for falsifying results exposes systemic quality control failures that compromise product safety and market integrity. Counterfeit products often contain undisclosed synthetic cannabinoids, pesticide residues, or incorrect potency levels, creating health risks that generate negative media coverage and regulatory backlash affecting the entire industry. International supply chains lack standardized quality protocols, enabling contaminated raw materials to enter legitimate manufacturing processes without detection. The proliferation of unregulated online marketplaces facilitates distribution of non-compliant products, while inadequate consumer education makes it difficult for buyers to distinguish between legitimate and counterfeit offerings, perpetuating market confusion and safety concerns.

Supply Chain Disruptions Including Raw Material Sourcing

Global hemp cultivation constraints and processing bottlenecks create supply volatility that impacts pricing stability and product availability. The USDA's 2021 Final Rule requiring pre-harvest THC testing within 30 days of harvest, with mandatory DEA-registered laboratory testing by 2025, increases compliance costs and creates processing delays. International shipping restrictions and varying import regulations complicate cross-border raw material sourcing, while climate change impacts on agricultural production create seasonal supply fluctuations. Manufacturing capacity limitations in specialized extraction and formulation facilities constrain production scaling, particularly for companies seeking to meet organic certification requirements that limit processing options. Quality control requirements necessitate extensive testing protocols that extend production timelines, while regulatory changes can suddenly render existing inventory non-compliant, forcing costly reformulation or disposal. Banking restrictions on cannabis-related businesses limit working capital availability for inventory management and supply chain optimization, creating cash flow challenges that compound supply disruption impacts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Gummies Dominate While Mints Drive Innovation

Gummies command 47.63% market share in 2024, leveraging consumer familiarity and precise dosing capabilities that appeal to both therapeutic and recreational users. The format's success stems from manufacturing scalability and flavor masking properties that eliminate cannabis taste profiles, while portion control addresses dosing anxiety among new consumers. Mints, lollipops, and candies accelerate at 14.33% CAGR through 2030, driven by discrete consumption preferences and rapid onset characteristics that appeal to professional users seeking workplace-appropriate formats. Capsules and softgels serve the pharmaceutical-oriented segment with standardized dosing and extended shelf life, while tea and coffee products target wellness-conscious consumers seeking ritualistic consumption experiences.

The emergence of nanotechnology in chocolate miniatures demonstrates format innovation beyond traditional categories, with companies like KANHA developing 4mg THC chocolates that achieve faster absorption and more predictable effects. Honey sticks, lozenges, and specialty chocolates represent niche opportunities within the "Others" category, often commanding premium pricing through artisanal positioning and organic certifications. Manufacturing advances in starch-free gummy production using plant-based gelling agents address clean-label demands while improving production efficiency and reducing allergen concerns.

By Category: Conventional Leads as Organic Accelerates

Conventional products maintain 75.22% market share in 2024, reflecting cost advantages and established supply chains that enable broader market penetration. However, organic CBD edibles accelerate at 12.78% CAGR, indicating consumer willingness to pay premiums for certified organic ingredients and sustainable production methods. The organic segment benefits from USDA certification programs, with Cornbread Hemp achieving the first USDA-certified organic hemp THC gummy designation, demonstrating regulatory pathway viability. OCal Cannabis Certification provides additional organic verification specifically for cannabis products, creating differentiated positioning opportunities.

Organic certification requires pesticide-free cultivation, non-synthetic processing methods, and third-party verification protocols that increase production costs but enable premium pricing strategies. Companies like Aspen Green expand organic offerings with full-spectrum gummies that combine therapeutic efficacy with clean ingredient profiles. The conventional segment's resilience stems from price sensitivity among mainstream consumers and limited organic hemp cultivation capacity that constrains supply expansion. Hybrid approaches emerge where companies offer both conventional and organic product lines to capture different consumer segments while optimizing production efficiency across shared manufacturing infrastructure.

By Packaging Type: Bottles Prevail While Pouches Innovate

Bottles secure 60.21% market share in 2024 through child-resistant compliance, extended shelf-life protection, and consumer familiarity that reduces purchase hesitation. The format's dominance reflects regulatory requirements for child-resistant packaging and consumer preference for resealable containers that maintain product freshness over extended periods. Pouches accelerate at 13.21% CAGR, driven by sustainability initiatives, portion control innovations, and cost-effective manufacturing that appeals to environmentally conscious consumers and value-oriented segments. Sachets and tin boxes serve specialized applications, with sachets enabling single-serve convenience and tin boxes providing premium presentation for gift markets.

Packaging innovation focuses on smart technologies that enhance consumer engagement and regulatory compliance, with QR codes linking directly to certificates of analysis and dosing guidance. Child-resistant paperboard solutions address environmental concerns while maintaining safety standards, with companies developing recyclable alternatives to traditional plastic bottles. Mylar pouches gain traction for gummy products through superior barrier properties and customizable printing options that enable brand differentiation. The packaging evolution reflects broader sustainability trends while addressing functional requirements for product protection, regulatory compliance, and consumer convenience across diverse consumption contexts.

By Distribution Channel: Offline Dominance Meets Online Growth

Offline stores maintain 63.74% market share in 2024, leveraging consumer preference for product inspection, immediate availability, and expert consultation that builds confidence in CBD purchases. Physical retail provides educational opportunities through knowledgeable staff, product sampling, and brand demonstrations that address consumer uncertainty about dosing and effects. Online stores accelerate at 12.65% CAGR, driven by convenience, privacy, and expanded product selection that appeals to experienced users and geographically dispersed consumers. The digital channel benefits from subscription models, personalized recommendations, and direct-to-consumer relationships that enable higher margins and customer lifetime value optimization.

E-commerce platform sophistication improves through enhanced age verification systems, regulatory compliance automation, and integration with mainstream delivery services like DoorDash. Edible Brands' launch of Edibles.com demonstrates traditional retail expertise application to cannabis e-commerce, leveraging established logistics capabilities for same-day delivery and trusted brand curation. Omnichannel strategies emerge as companies integrate online and offline touchpoints, using digital platforms for education and discovery while maintaining physical locations for immediate fulfillment and customer service. The distribution evolution reflects changing consumer behaviors and regulatory adaptations that enable broader market access while maintaining compliance and safety standards.

Geography Analysis

North America commands 39.09% market share in 2024, benefiting from established regulatory frameworks, consumer acceptance, and mature distribution infrastructure across 47 states with some form of cannabis legalization. The region's leadership stems from early adoption, extensive clinical research, and sophisticated manufacturing capabilities that enable premium product development and quality assurance. Canada's regulatory streamlining through Cannabis Act amendments reduces compliance burdens while maintaining safety standards, supporting continued market expansion.

Asia-Pacific emerges as the fastest-growing region at 13.76% CAGR through 2030, driven by regulatory liberalization and expanding consumer acceptance across key markets. Japan's landmark cannabis law reforms in December 2024 establish specific THC residue limits for CBD products, creating unprecedented market access after 75 years of prohibition. Thailand's comprehensive legalization framework spawned over 10,000 dispensaries, demonstrating rapid infrastructure development and consumer adoption. South Korea's Health Functional Food Act provides regulatory pathways for dietary supplements, while nutraceutical regulations across Asian countries create opportunities for CBD edibles positioned as wellness products.

Europe balances between progressive policies and regulatory caution, with Germany's adult-use legalization in April 2024 allowing personal cultivation and possession while maintaining quality standards. However, the European Commission's proposal to classify flower-derived CBD as narcotic substances creates uncertainty that could fragment market access across member states. The UK maintains separate regulatory pathways that may provide competitive advantages for British companies, while Switzerland's established CBD market offers lessons for broader European adoption. Middle East and Africa show emerging opportunities in Israel and South Africa, where medical cannabis programs create regulatory precedents for CBD edibles, though market development remains constrained by conservative social attitudes and limited infrastructure in many countries.

Competitive Landscape

The CBD edibles market exhibits moderate concentration, indicating emerging consolidation pressures as established players acquire smaller competitors and expand geographic reach. Strategic partnerships dominate competitive dynamics, exemplified by The Cannabist Company's collaborations with Flower by Edie Parker and COAST Cannabis Co., which expand artisan chocolate and premium gummy offerings across multiple states while leveraging complementary brand positioning. Vertical integration strategies emerge as companies seek supply chain control and margin optimization, with firms like Tilray Brands expanding from cultivation through retail distribution to capture value across the entire production cycle.

Innovation is a critical factor distinguishing competitors in this space. Brands compete by introducing novel edible formats beyond traditional gummies, such as capsules, mints, teas, and infused beverages, alongside clean-label, organic, vegan, and functionally targeted formulations. This product diversification helps companies appeal to evolving consumer preferences and wellness trends, enhancing customer loyalty and capturing niche segments. Additionally, the rise of online retail channels has intensified competition on convenience, pricing, and brand differentiation. Smaller and newer entrants frequently specialize in organic or premium edibles to carve out tangible market share against the giants, contributing to a dynamic and fragmented market environment.

Geographically, North America remains the largest and most competitive market due to favorable legislation and high consumer awareness, but regions like Asia-Pacific are emerging as key battlegrounds with rapid market growth forecasts. As regulatory frameworks evolve globally, firms investing heavily in compliance, quality assurance, and transparent marketing gain a competitive edge. Furthermore, strategic partnerships, mergers, and acquisitions play a vital role in consolidating market positions and expanding geographic reach, with large multi-state operators and cannabis conglomerates actively acquiring promising CBD edible brands. Altogether, the competitive landscape in 2025 is characterized by consolidation among leaders, vigorous innovation, and expanding global footprints amid robust consumer demand.

CBD Edibles Industry Leaders

-

CV Sciences, Inc

-

HempLucid

-

Dixie Brands

-

Medterra

-

Charlotte's Web, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Tilray Brands Inc., a global lifestyle and consumer packaged goods company, unveiled its latest offering: Charlotte's Web CBD gummies, in Canada. Tailored for daily CBD enthusiasts, the newly introduced Charlotte’s Web CBD Rest Gummies and CBD Life Gummies provided a tasty and convenient method to seamlessly integrate CBD into daily wellness routines.

- October 2024: CBD Life Sciences Inc. set a new industry standard with its launch of a high-performance line of mushroom-infused gummies, designed to meet the surging demand for wellness products in a projected USD 20 billion market. Focused on energy, sleep, and sexual wellness, these unique formulations offered CBDL shareholders and new investors an unprecedented growth opportunity in an exploding sector.

- April 2024: Building on the success of their versatile Melt and Pour gummy base, Candy Pros had launched another groundbreaking product, the Naked Gold Sugar Free Hard Candy Mix. This innovative formula was specifically designed for crafting both THC hard candies and CBD-infused edibles, offering a new way for confectioners to meet the growing demand for healthier, customizable cannabis products.

Global CBD Edibles Market Report Scope

| Gummies |

| Capsules and Softgels |

| Mints/Lollipops/candies |

| Tea and Coffee |

| Others |

| Organic |

| Conventional |

| Bottles |

| Pouches |

| Others |

| Offline Stores |

| Online Stores |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Switzerland | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | Japan |

| South Korea | |

| Thailand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Israel | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Colombia | |

| Rest of South America |

| By Type | Gummies | |

| Capsules and Softgels | ||

| Mints/Lollipops/candies | ||

| Tea and Coffee | ||

| Others | ||

| By Category | Organic | |

| Conventional | ||

| By Packaging Type | Bottles | |

| Pouches | ||

| Others | ||

| By Distribution Channel | Offline Stores | |

| Online Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Switzerland | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | Japan | |

| South Korea | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Israel | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Colombia | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the CBD edibles market be by 2030?

It is projected to reach USD 446.77 million, growing at a 12.31% CAGR from 2025.

Which product format currently dominates sales?

Gummies hold 47.63% of 2024 revenue due to flavor masking and precise dosing.

Which region is expanding the fastest?

Asia-Pacific is set to grow at a 13.76% CAGR through 2030, propelled by new Japanese and Thai regulations.

What packaging trend is gaining momentum?

Child-resistant, recyclable pouches are advancing at a 13.21% CAGR as brands pursue sustainability.

Page last updated on: