Foot Care Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

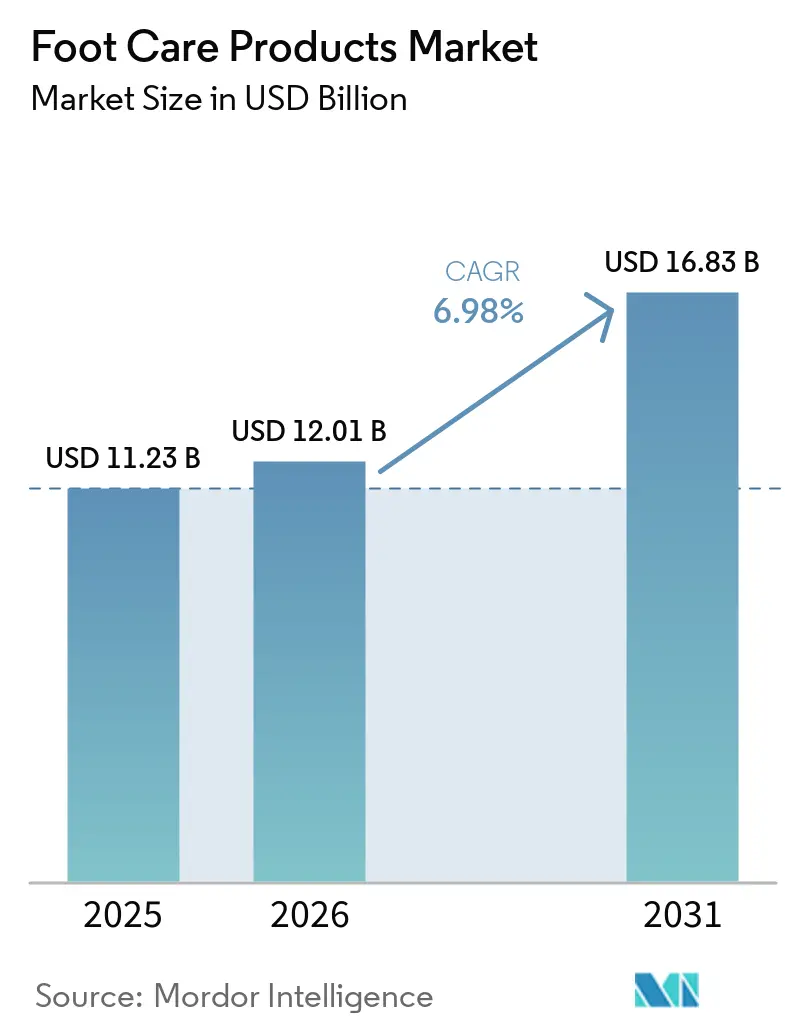

| Market Size (2026) | USD 12.01 Billion |

| Market Size (2031) | USD 16.83 Billion |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Foot Care Products Market Analysis by Mordor Intelligence

The Foot Care Products Market size was valued at USD 11.23 billion in 2025 and is estimated to grow from USD 12.01 billion in 2026 to reach USD 16.83 billion by 2031, at a CAGR of 6.98% during the forecast period (2026-2031).

The foot care products market is growing faster than many personal care categories, driven by rising diabetes rates, an aging population, and increased spending on preventive care. By 2025, 589 million adults are expected to have diabetes, with related health expenditures reaching USD 1.015 trillion in 2024.[1]International Diabetes Federation, “IDF Diabetes Atlas, 11th Edition,” IDF, diabetesatlas.org This demand supports recurring-use products like insoles, antifungal solutions, and heel repair creams. The market is also benefiting from a shift toward OTC purchases, pharmacy sales, and digital discovery, reducing reliance on clinician-led pathways and encouraging frequent replenishment. Major consumer health companies leverage pharmacy reach, compliance, and brand trust, while specialists attract high-value customers through 3D scanning, digital fitting tools, and premium materials. This dynamic fosters growth in preventive care, premium repair regimens, and digitally-assisted orthotics across mature and emerging markets.

Key Report Takeaways

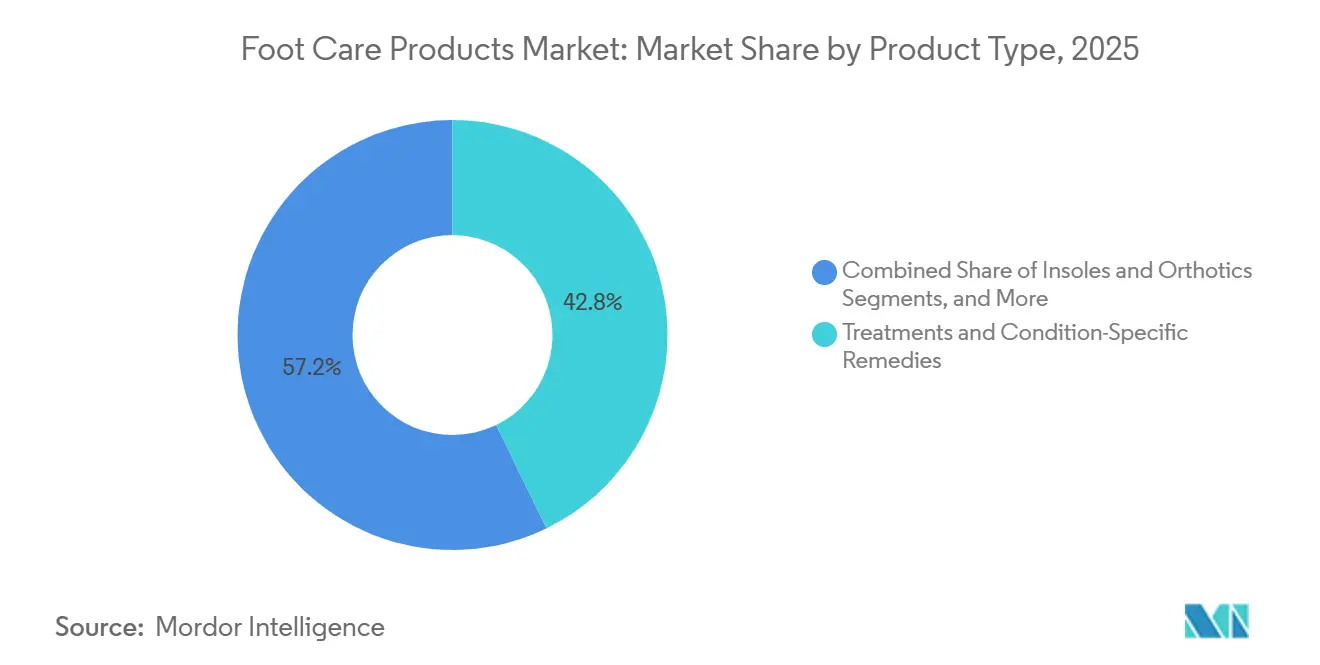

- By product type, treatment & condition-specific remedies led with 42.80% share in 2025, while insoles & orthotics are projected to expand at an 8.10% CAGR through 2031.

- By product form, cream held 34.40% share in 2025, while spray is expected to grow at a 7.20% CAGR through 2031.

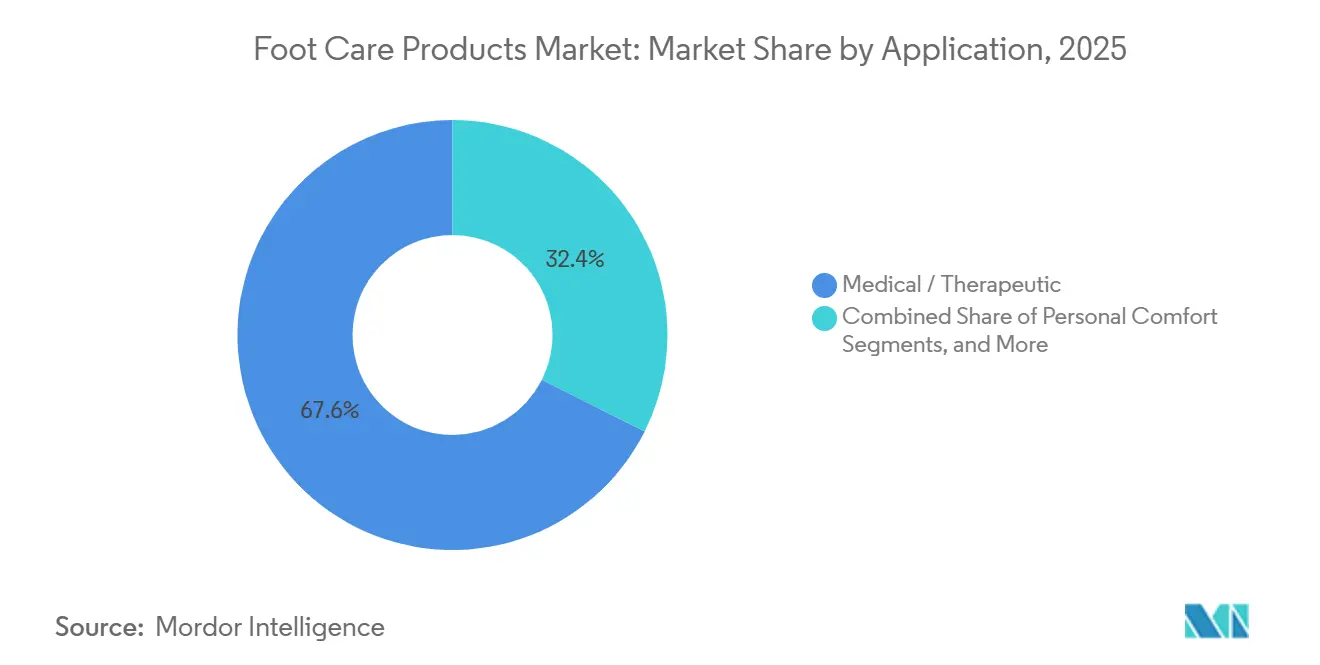

- By application, medical/therapeutic accounted for 67.60% share in 2025, while personal comfort is projected to grow at an 8.95% CAGR through 2031.

- By distribution channel, pharmacies & drug stores held 37.90% share in 2025, while online/e-commerce recorded the highest projected CAGR at 7.25% through 2031.

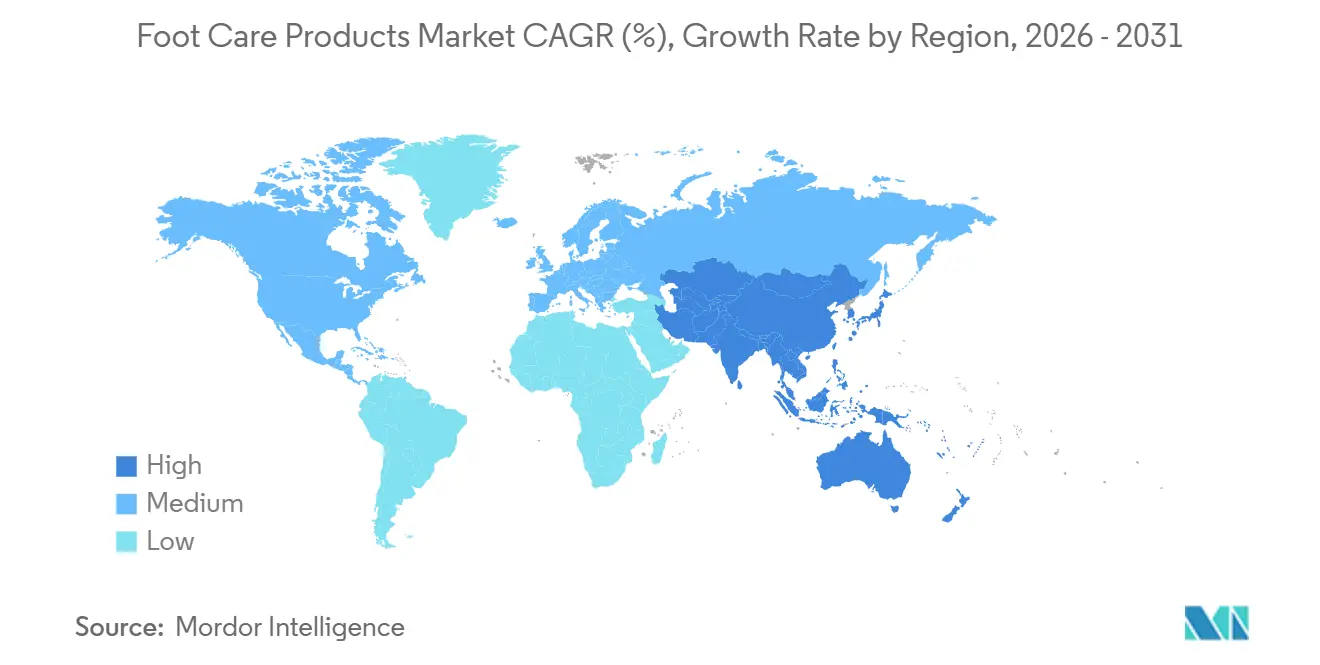

- By geography, North America held 40.12% share in 2025, while Asia-Pacific is projected to expand at a 9.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Foot Care Products Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising diabetic and aging-foot burden | +2.1% | Global, highest intensity in North America, South Asia, and APAC | Long term (≥ 4 years) |

| OTC shift toward preventive foot health | +1.3% | North America and Europe, with emerging traction across APAC | Medium term (2-4 years) |

| Premium foot repair and antifungal regimens | +1.1% | North America, Europe, South Korea, and Japan | Medium term (2-4 years) |

| Pharmacy-led and e-commerce discovery | +0.9% | Global, fastest adoption in China, India, and Latin America | Short term (≤ 2 years) |

| Retail scan-to-fit orthotics scaling | +0.7% | North America and Western Europe | Medium term (2-4 years) |

| Climate-linked fungal and sweat burden | +0.6% | APAC, South America, and MEA, with spillover into temperate European zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Diabetic and Aging-Foot Burden

The foot care products market benefits from a growing long-term patient base, with 589 million adults aged 20 to 79 living with diabetes in 2025, representing 1 in 9 adults globally. Of these, 43% or 252 million remained undiagnosed, and 81% resided in low- and middle-income countries, indicating a delayed entry into preventive care pathways. Diabetes-related health expenditure reached USD 1.015 trillion in 2024, a 338% increase over 17 years, highlighting the significant impact of chronic foot-risk conditions on healthcare spending and self-care purchasing.[2]International Diabetes Federation, “IDF Diabetes Atlas, 11th Edition,” IDF, diabetesatlas.org Globally, 6.3% of adults with diabetes experience diabetic foot ulcers, with North America showing a higher prevalence of 13.0%.[3]International Diabetes Federation, “Diabetes-Related Foot Complications,” IDF, idf.org This drives consistent demand for products like plantar-pressure insoles, medicated creams, antifungal treatments, and protective skin regimens, emphasizing preventive care. Additionally, the aging population sustains demand, with studies supporting the use of arch-support and pressure-redistribution insoles for managing common foot pain.

OTC Shift Toward Preventive Foot Health

The market is witnessing a shift from reactive purchases to planned preventive use, particularly in developed regions where consumers increasingly invest in therapeutic foot products before symptoms worsen. This trend is evident in premium insoles, foot repair creams, and antifungal treatments, which are now positioned closer to daily wellness items. This shift creates a middle tier between low-cost commodities and prescription products, enabling clinically positioned brands to expand their price range while maintaining accessibility. Independent endorsements, such as the American Podiatric Medical Association Seal of Acceptance for ARRIS Composites’ AURORRA carbon fiber insoles, are becoming more valuable. Regulatory frameworks also favor established players with robust product testing and compliance systems.

Premium Foot Repair and Antifungal Regimens

Consumers increasingly approach heel repair, antifungal care, and skin recovery as structured regimens rather than standalone purchases. O’Keeffe’s launched the Healthy Feet Heel Repair Kit in November 2025, combining concentrated foot cream with application tools, promoting bundled use cases. Similarly, Beiersdorf’s Health Care division reported 6.1% organic sales growth in 2024, reaching approximately USD 296 million, driven by blister prevention plasters. Enhanced formulations and delivery systems improve treatment adherence and reduce recurrence risks, enabling companies with advanced research capabilities to defend premium pricing against private-label competitors.

Pharmacy-Led and E-Commerce Discovery

Pharmacies remain a key distribution channel, accounting for 37.90% of the market in 2025, as pharmacist guidance is crucial for fungal treatments, heel repair products, and plantar fasciitis solutions. Meanwhile, online channels are projected to grow at a 7.25% CAGR through 2031, driven by search-led acquisition, subscription replenishment, and digital tools that match products to conditions. Digital platforms are expanding access to smaller cities and converting occasional buyers into regular users through repeat orders.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Low reimbursement for routine foot care | -0.4% | North America, especially the United States, and parts of Europe | Long term (≥ 4 years) |

| Evidence gaps across OTC claims | -0.3% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Regulatory scrutiny on orthotics and claims | -0.2% | North America, Europe, and Australia | Medium term (2-4 years) |

| PFAS and material-compliance pressure | -0.2% | Europe and North America, with expansion into APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Low Reimbursement for Routine Foot Care

In the U.S., the foot care products market faces structural challenges due to reimbursement policies. Medicare Part B excludes most routine foot care services unless a qualifying systemic condition is properly documented. Consequently, a significant portion of preventive spending becomes out-of-pocket, even for products addressing critical risks like diabetic skin breakdown or fungal recurrence. A 2025 audit revealed that 49% of sampled claims for routine foot care tied to systemic conditions did not meet Medicare requirements. This drives a large segment of the market toward over-the-counter and retail channels, where consumers often prioritize price over long-term value. Expanding coverage for preventive diabetic footwear or related services could significantly impact market growth beyond current forecasts.

PFAS and Material-Compliance Pressure

Material compliance is an increasing challenge for the foot care products market, particularly for insoles and moisture-management accessories that rely on fluorinated treatments. Denmark’s 2025 regulation bans the import and sale of footwear with total fluorine levels above 50 mg F/kg starting July 2026, directly affecting material choices. In the U.S., state-level regulations like Minnesota’s Amara’s Law and New Mexico’s PFAS Protection Act, both effective in 2025, add further compliance pressures. Consumer-grade insoles sold in mass retail face greater reformulation demands compared to FDA-regulated prosthetic or orthotic products. Smaller brands are disproportionately affected due to limited resources for material substitution, testing, and supplier qualification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Orthotics Innovation Reshapes a Treatments-Led Market

In 2025, Treatment & Condition-Specific Remedies held 42.80% of the foot care products market share, driven by recurring conditions like athlete’s foot, fungal nails, and plantar fasciitis. These products benefit from strong shelf visibility, symptom-led merchandising, and ease of selection without formal diagnosis. Foot Skincare & Cosmetic Care has expanded its audience by attracting wellness-focused consumers who integrate foot masks, balms, and exfoliants into regular self-care routines.

Insoles & Orthotics is projected to grow at a CAGR of 8.10% through 2031, supported by the shift from clinic-based customization to digitally accessible retail options. Advanced insole designs, such as lattice-based structures, enhance plantar pressure redistribution, offering brands a strong value proposition for comfort, prevention, and performance. Foot Hygiene & Odor Control remains stable, with probiotic deodorant formats signaling innovation through formulation science.

By Product Form: Spray Gains as Delivery Science Meets Lifestyle Convenience

Cream led the market with a 34.40% share in 2025, owing to its versatility in addressing cosmetic hydration and medicinal treatments. Lotion remains popular for daily moisturization, while gel formats cater to cooling and recovery needs. Patch/Pad/Tape products maintain strong credibility in Europe due to their association with visible protection and symptom relief.

Spray is forecast to grow at a CAGR of 7.20% through 2031, driven by convenience, quick-drying features, and improved suitability for interdigital application. Enhanced propellant systems and carrier technology have enabled sprays to expand into clinically relevant uses. Device and tool formats, such as electronic foot files, create new growth opportunities by linking hardware with consumable products.

By Application: Medical Dominance Meets Wellness Demand From Below

Medical/Therapeutic applications accounted for 67.60% of the market in 2025, reflecting the segment's focus on managing conditions like diabetes-related prevention, pressure relief, and fungal control. The growing diabetic population reinforces the demand for preventive foot care, while retail and online channels are increasingly influencing purchasing decisions.

Personal Comfort is expected to grow at a CAGR of 8.95% through 2031, driven by factors like daily fatigue, prolonged standing, and commuting. Sports & Athletics remains a key segment, with demand for blister prevention and moisture control. These segments often serve as entry points for consumers transitioning to therapeutic products.

By Distribution Channel: AI-Powered Retail and the Online Shift Redefine Discovery

Pharmacies & Drug Stores held a 37.90% share in 2025, reflecting consumer trust in pharmacist-guided product selection. Supermarkets & Hypermarkets remain relevant for general-use creams and hygiene products, while Specialty Stores cater to premium insoles and performance-oriented solutions requiring in-store support.

Online/E-Commerce is projected to grow at a CAGR of 7.25% through 2031, driven by search-led traffic and subscription models for repeat purchases. Convenience Stores play a smaller role, focusing on travel-related hygiene needs and quick purchases for events or commuting. Channel competition now emphasizes trust, speed, and digital engagement over shelf presence.

Geography Analysis

In 2025, North America accounted for 40.12% of the foot care products market, with the U.S. as the leading center for OTC therapeutic foot care. This dominance is driven by a high disease burden, as 13.0% of adults with diabetes in the region experience diabetic foot ulcers compared to the global average of 6.3%. The region benefits from a strong pharmacy network, high product awareness, and consumer willingness to invest in advanced formulations and insoles. Canada mirrors U.S. purchasing trends in pharmacist-led and self-care categories, while Mexico contributes to volume growth through expanding retail and pharmacy infrastructure.

Europe ranked as the second-largest regional market, with Germany, the U.K., France, Italy, and Spain as key demand centers. Germany stands out due to reimbursement structures and a pharmacy culture that supports a stronger therapeutic mix. Beiersdorf’s Health Care division, including Hansaplast, reported growth. Europe is also adapting to material compliance changes, favoring brands transitioning to PFAS-free inputs without compromising performance or pricing.

Asia-Pacific is the fastest-growing region in the foot care products market, with a projected CAGR of 9.35% from 2026 to 2031. China and India lead due to large diabetic populations and growing preventive foot care adoption. By late 2024, China’s population aged 60 and above reached nearly 297 million, driving demand for products focused on pressure relief, skin care, and circulation support. Japan follows a mature model, promoting foot care as part of routine health management. The Middle East and Africa benefit from high obesity and diabetes rates in GCC countries, while South America sees growth in antifungal and hygiene products as retail networks expand.

Competitive Landscape

The foot care products market operates through a two-tier structure, combining large consumer health groups with specialized brands. The first tier includes multinational companies leveraging pharmacy distribution, marketing scale, manufacturing efficiency, and compliance to lead in treatment and skincare categories. Kenvue reported USD 15.1 billion in net sales for fiscal year 2025, strengthening its consumer health portfolio and retail leverage, including foot care-adjacent product lines. Perrigo capitalizes on store-brand capabilities and OTC expertise, while Beiersdorf benefits from Hansaplast’s established medical credibility in Europe. These players focus on clinical-strength positioning, premium kits, and cross-category placement to protect margins.

The second tier is led by specialist orthotics and therapeutic footwear brands like Bauerfeind, Aetrex, and Superfeet. Their strengths include personalized fitting, digital manufacturing, scanning technology, and clinician endorsements, which are difficult for mass-market brands to replicate. Aetrex’s FitAI platform surpassed 2 million personalized fit recommendations in March 2026 across 500 retail locations, achieving in-store engagement rates of 45% to 60%. Such innovations help specialist brands convert store traffic into premium orthotics demand while building proprietary data assets for improved merchandising decisions.

White space is evident in mid-market personalization and preventive product bundles for newly diagnosed diabetic users, especially in emerging markets where awareness is growing faster than access to specialist services. Coats Group’s USD 770 million acquisition of OrthoLite Holdings LLC in October 2025 highlights the growing importance of premium insoles as a significant growth platform. The deal also targets USD 20 million in joint annualized cost synergies by 2028, emphasizing scale and manufacturing efficiency. Superfeet introduced the Run Pacer Elite in October 2025, a performance insole offering 39% more responsiveness than conventional insoles.

Foot Care Products Industry Leaders

Aetrex, Inc.

Bayer AG

O’Keeffe’s Company

Perrigo Company plc

Superfeet Worldwide, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Aetrex Inc.'s FitAI technology surpassed 2 million personalized fit recommendations across 500+ global retail locations, including ASICS, PUMA, DSW, and Foot Locker, achieving a 45–60% in-store engagement rate and strengthening its dataset of over 50 million unique foot scans.

- March 2026: Scholl's Wellness Company Japan launched "Surari-npa" daytime compression and "Yururi-npa" nighttime lymphatic care foot support products nationwide, targeting the 60+ demographic with patented circulatory comfort technology.

- March 2026: Dr. Scholl's Shoes, Caleres, and Wrangler introduced a limited-edition capsule collection priced at USD 80–200, combining orthopedic comfort technology with Western heritage-inspired designs.

- October 2025: Superfeet Worldwide LLC launched the Run Pacer Elite, a performance insole featuring Carbitex carbon fiber and SuperRev foam, offering a 39% improvement in responsiveness over conventional insoles.

Global Foot Care Products Market Report Scope

As per the scope of the report, foot care products are specialized formulations and tools designed to cleanse, moisturize, exfoliate, and protect the skin and nails on your feet. They target common issues like dryness, cracking, fungal infections, and odor, promoting overall hygiene and comfort.

The foot care products market is segmented by product type, product form, application, and distribution channel. By product type, the market includes insoles & orthotics (athletic/performance insoles, gel insoles, foam insoles, orthotic insoles, heel cups & arch supports), treatments & condition-specific remedies (athlete’s foot treatments, anti-blister products, corn & callus treatments, fungal nail treatments, plantar fasciitis relief products), foot skincare & cosmetic care (foot creams, foot lotions & moisturizers, foot masks & peels, foot files & exfoliators, foot balms), foot hygiene & odor control (foot powders, sprays & deodorants, sanitizing solutions), and protective pads & accessories (shoe pads, toe separators & sleeves, cushions & tapes). By product form, the market is segmented into cream, lotion, gel, spray, powder, patch/pad/tape, insole/insert, and device/tool. By application, the market is categorized into medical/therapeutic, sports & athletics, personal comfort, and beauty/grooming. By distribution channel, the market is segmented into pharmacies & drug stores, supermarkets & hypermarkets, online/e-commerce, specialty stores, hospitals & clinics, and convenience stores. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Insoles & Orthotics | Athletic / Performance Insoles |

| Gel Insoles | |

| Foam Insoles | |

| Orthotic Insoles | |

| Heel Cups & Arch Supports | |

| Treatments & Condition-Specific Remedies | Athlete's Foot Treatments |

| Anti-blister Products | |

| Corn & Callus Treatments | |

| Fungal Nail Treatments | |

| Plantar Fasciitis Relief Products | |

| Foot Skincare & Cosmetic Care | Foot Creams |

| Foot Lotions & Moisturizers | |

| Foot Masks & Peels | |

| Foot Files & Exfoliators | |

| Foot Balms | |

| Foot Hygiene & Odor Control | Foot Powders |

| Sprays & Deodorants | |

| Sanitizing Solutions | |

| Protective Pads & Accessories | Shoe Pads |

| Toe Separators & Sleeves | |

| Cushions & Tapes |

| Cream |

| Lotion |

| Gel |

| Spray |

| Powder |

| Patch / Pad / Tape |

| Insole / Insert |

| Device / Tool |

| Medical / Therapeutic |

| Sports & Athletics |

| Personal Comfort |

| Beauty / Grooming |

| Pharmacies & Drug Stores |

| Supermarkets & Hypermarkets |

| Online / E-commerce |

| Specialty Stores |

| Hospitals & Clinics |

| Convenience Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Insoles & Orthotics | Athletic / Performance Insoles |

| Gel Insoles | ||

| Foam Insoles | ||

| Orthotic Insoles | ||

| Heel Cups & Arch Supports | ||

| Treatments & Condition-Specific Remedies | Athlete's Foot Treatments | |

| Anti-blister Products | ||

| Corn & Callus Treatments | ||

| Fungal Nail Treatments | ||

| Plantar Fasciitis Relief Products | ||

| Foot Skincare & Cosmetic Care | Foot Creams | |

| Foot Lotions & Moisturizers | ||

| Foot Masks & Peels | ||

| Foot Files & Exfoliators | ||

| Foot Balms | ||

| Foot Hygiene & Odor Control | Foot Powders | |

| Sprays & Deodorants | ||

| Sanitizing Solutions | ||

| Protective Pads & Accessories | Shoe Pads | |

| Toe Separators & Sleeves | ||

| Cushions & Tapes | ||

| By Product Form | Cream | |

| Lotion | ||

| Gel | ||

| Spray | ||

| Powder | ||

| Patch / Pad / Tape | ||

| Insole / Insert | ||

| Device / Tool | ||

| By Application | Medical / Therapeutic | |

| Sports & Athletics | ||

| Personal Comfort | ||

| Beauty / Grooming | ||

| By Distribution Channel | Pharmacies & Drug Stores | |

| Supermarkets & Hypermarkets | ||

| Online / E-commerce | ||

| Specialty Stores | ||

| Hospitals & Clinics | ||

| Convenience Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the foot care products space in 2026?

The foot care products market stands at USD 12.01 billion in 2026 and is projected to reach USD 16.83 billion by 2031 at a CAGR of 6.98%.

Which region leads global demand for foot care products?

North America led in 2025 with a 40.12% share, supported by high diabetes-related foot risk, strong pharmacy networks, and consumer willingness to pay for therapeutic solutions.

Which product category is growing the fastest in foot care products?

Insoles & Orthotics is the fastest-growing product type, with a projected CAGR of 8.10% through 2031, helped by digital fit tools and stronger clinical support.

Why are pharmacies still important in foot care product sales?

Pharmacies & Drug Stores held 37.90% share in 2025 because many buyers still rely on pharmacist advice for antifungal products, diabetic foot creams, and support solutions.

What is driving faster online demand for foot care products?

Online/E-Commerce is projected to grow at 7.25% CAGR because digital shoppers often search for specific conditions, and subscriptions improve repeat purchasing for creams, antifungals, and insoles.

Which application area dominates demand in foot care products?

Medical/Therapeutic led with 67.60% share in 2025, although Personal Comfort is growing faster at an 8.95% CAGR as routine wellness and fatigue relief gain more attention.

Page last updated on: