Foot Orthotic Insoles Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

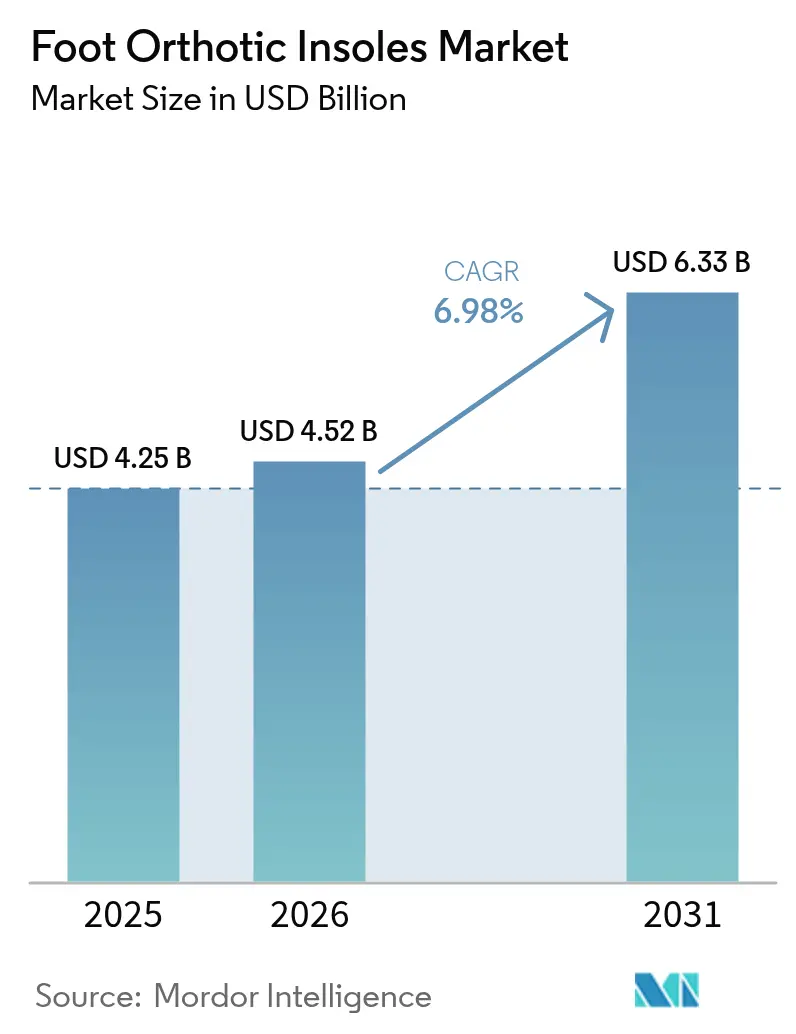

| Market Size (2026) | USD 4.52 Billion |

| Market Size (2031) | USD 6.33 Billion |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

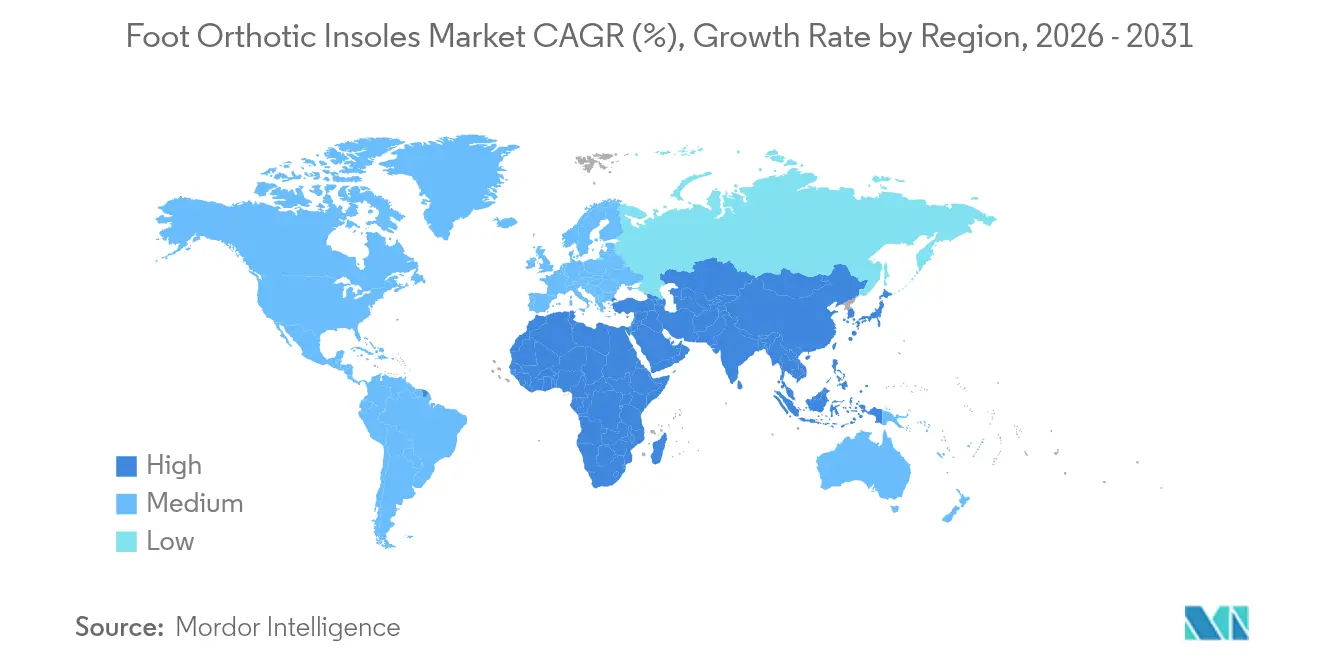

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

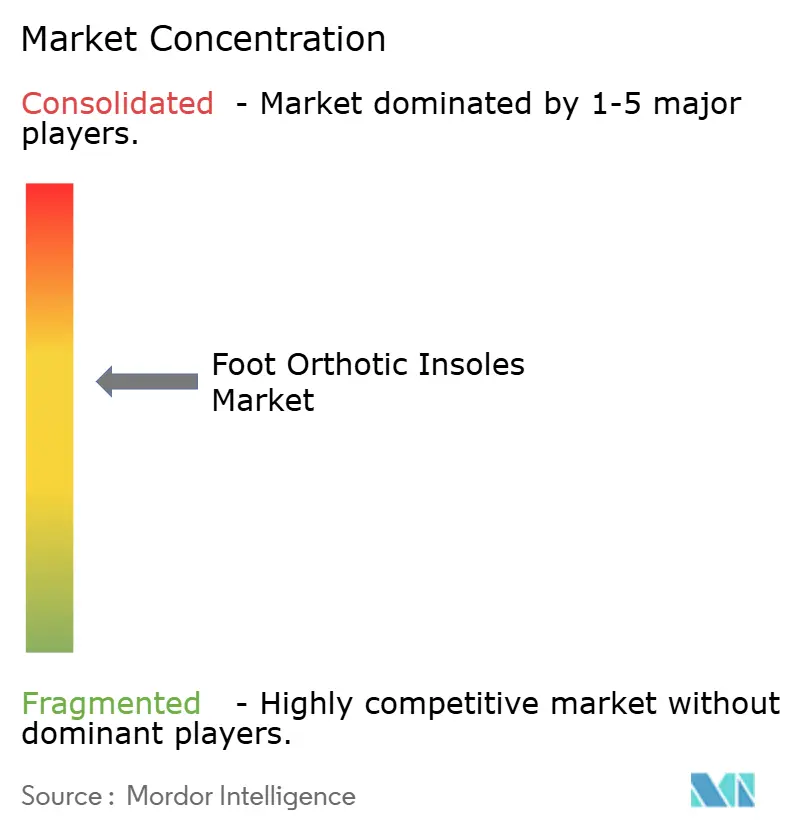

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Foot Orthotic Insoles Market Analysis by Mordor Intelligence

The Foot Orthotic Insoles Market size was valued at USD 4.25 billion in 2025 and is estimated to grow from USD 4.52 billion in 2026 to reach USD 6.33 billion by 2031, at a CAGR of 6.98% during the forecast period (2026-2031).

Consistent demand stems from an aging population, escalating diabetes prevalence, and the rapid arrival of consumer-friendly scanning tools that compress fitting times and lower costs. Retailers now deploy AI kiosks that convert roughly one-third of walk-ins by matching real-time gait data with stocked SKUs, while smartphone LiDAR applications enable sub-millimeter home scans that feed the same design engines. These tools divert purchases away from clinic-only channels toward mass retail and direct-to-consumer sites, reshaping the competitive playbook. Material innovation adds momentum: carbon-fiber plates have proven energy-return benefits that resonate with runners, and thermoplastics support in-store heat molding that satisfies shoppers who refuse multi-week waits. Supply chains are adapting as well; EVA remains cost-efficient, yet composite inputs and lattice printing reduce scrap by up to 40%, helping brands protect margin against resin price swings.

Key Report Takeaways

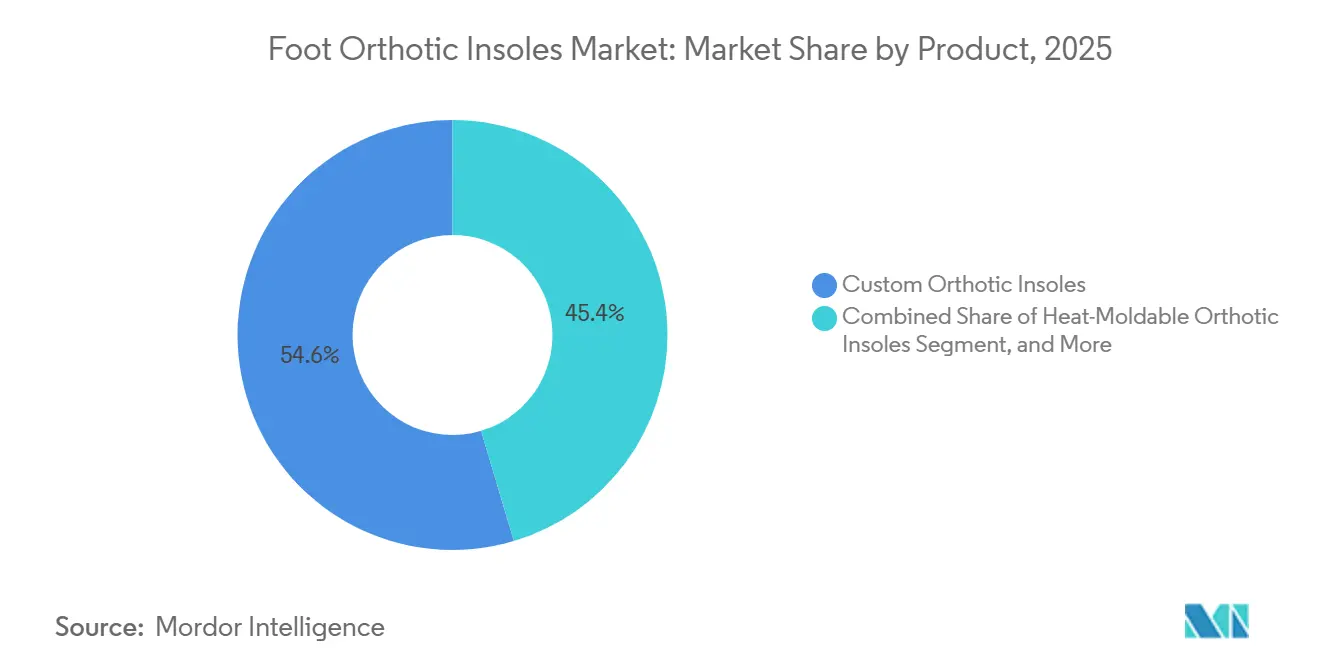

- By product type, custom orthotic insoles held 54.62% of foot orthotics insoles market share in 2025, while heat-moldable variants are expanding at a 7.52% CAGR to 2031.

- By material, EVA foam retained 28.91% share of the foot orthotics insoles market size in 2025; composite carbon fiber is forecast to grow at an 8.24% CAGR through 2031.

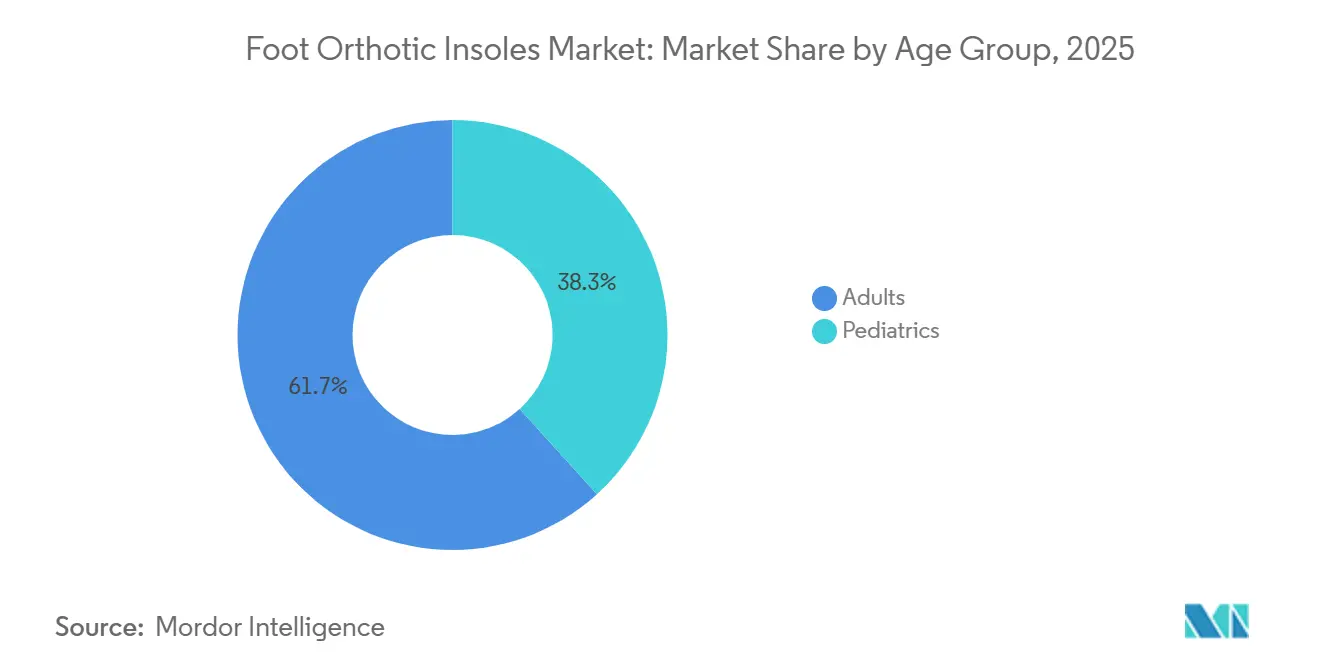

- By age group, adults accounted for 61.72% of 2025 revenue, whereas the pediatric segment is projected to advance at an 8.72% CAGR between 2026-2031.

- By application, medical indications dominated with 57.84% share in 2025, yet sports and athletics are on track for a 9.05% CAGR to 2031.

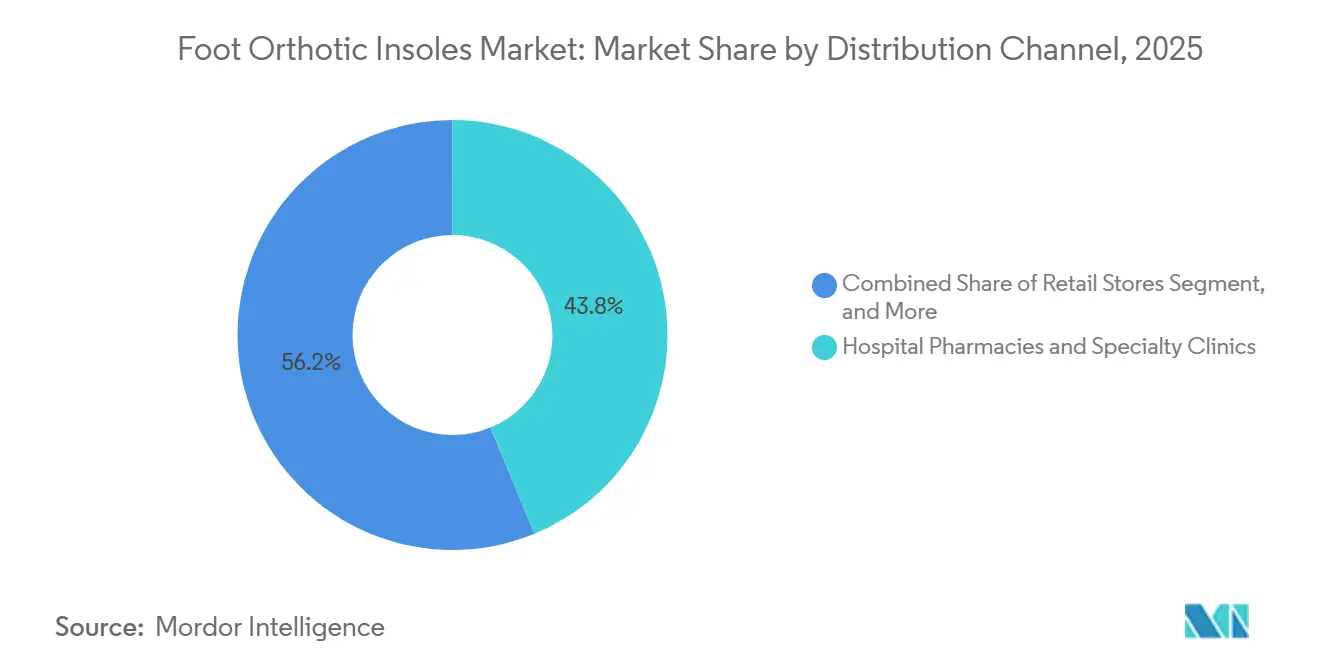

- By distribution channel, hospital pharmacies and specialty clinics captured 43.78% of 2025 sales, but online pharmacies are poised for an 11.99% CAGR over the same horizon.

- By geography, North America accounted for 39.18% of the value in 2025; Asia-Pacific is the fastest-growing region, with a 7.99% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Foot Orthotic Insoles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing Demographic & Diabetes Prevalence | +1.8% | North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Sports & Recreational Participation Boom | +1.2% | North America, Europe, expanding Asia-Pacific | Medium term (2-4 years) |

| Rapid Adoption of 3-D Scanning/Printing | +1.5% | North America, Europe early; Asia-Pacific scaling | Medium term (2-4 years) |

| AI-Enabled Retail Foot-Scan Kiosks | +0.9% | North America, Europe, pilot Asia-Pacific | Short term (≤ 2 years) |

| Employer-Funded Anti-Fatigue Programs | +0.6% | North America, Western Europe | Medium term (2-4 years) |

| Smartphones’ LiDAR Foot-Scan APIs | +1.0% | Digitally mature markets worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ageing Demographic & Diabetes Prevalence

Global residents aged 60 and older are projected to reach 1.4 billion by 2030, and many experience plantar fasciitis, arthritis, or neuropathy that restricts mobility.[1]World Health Organization, “Ageing and Health,” who.int Diabetes prevalence is expected to hit 1.3 billion cases by 2050, intensifying pressure to prevent foot ulcers through pressure-redistributing insoles.[2]Institute for Health Metrics and Evaluation, “Forecasting Future Diabetes Burden,” healthdata.org Medicare Part B covers 80% of allowable costs for custom orthoses prescribed for diabetic patients, effectively underwriting U.S. demand. Because older adults with diabetes face compounded gait challenges, insurers and clinicians align on early orthotic intervention, turning this demographic trend into a structural pull for the foot orthotics insoles market. As national health systems elsewhere follow the reimbursement template, baseline growth continues through 2031.

Sports & Recreational Participation Boom

Strava recorded 135 million users posting 15.3 billion activities in 2024, proof that running, cycling, and hiking have become daily habits across age brackets.[3]Strava Inc., “Year in Sport 2024,” strava.com Athletes proactively pursue orthoses to delay fatigue and protect joints, a pattern reinforced by peer-reviewed studies showing that carbon-fiber inserts reduce energy loss during gait by nearly 10%. Superfeet and Brooks embed carbon plates at the factory, repositioning insoles as performance components rather than aftermarket add-ons. Margins improve because shoppers accept footwear package premiums instead of stand-alone device surcharges. As sports normalization rises in emerging Asia-Pacific metros, retailers replicate North American merchandising practices, widening the demand funnel for foot orthotic insoles.

Rapid Adoption of 3-D Scanning and Printing

Volumental’s cloud engine completes a foot scan in under 1 minute and integrates directly with point-of-sale software, eliminating the plaster cast entirely. Aetrex priced its Zoe Pro scanner at USD 1,995, a level accessible to mid-tier shoe stores, enabling instant personal recommendations. On the production side, Formlabs stereolithography lines print lattice midsoles that mirror EVA stiffness but cut material waste by 40%. Retailers, therefore, pivot to just-in-time custom output that shortens wait times from weeks to days and lets consumers co-design color or arch height. Clinical trials confirm biomechanical equivalence between 3-D-printed and conventionally milled orthoses, sweeping aside the final quality objection.

AI-Enabled Retail Foot-Scan Kiosks

In-store kiosks powered by machine-vision algorithms interpret pressure maps and suggest SKUs in less than 120 seconds. U.S. pharmacy chains deploying these systems record conversion lifts of 30% because the recommendation appears authoritative and instant. Early adopters in Europe report similar gains, especially when kiosks print a digital voucher redeemable online. Low hardware costs and cloud-based updates encourage rapid rollout across athletic specialty and pharmacy formats. For the foot orthotics insoles market, kiosks dissolve the referral bottleneck and hand retailers a credible biomechanical service without podiatrists on staff.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited consumer awareness in low-income regions | -0.9% | Emerging Asia, Latin America, Africa | Long term (≥ 4 years) |

| High cost of fully custom devices & weak reimbursement | -1.2% | Global, price-sensitive markets | Medium term (2-4 years) |

| Biomechanical risks from DTC comfort-only inserts | -0.6% | Developed markets | Short term (≤ 2 years) |

| Supply volatility in EVA & specialty polymers | -0.8% | Global; Asia-Pacific supply hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost & Limited Reimbursement

Custom pairs sell for USD 200-800, a bracket far above cash-pay comfort inserts. Medicare reimburses only diabetic indications, excluding sports or general wellness uses, and private insurers mirror those rules. Outside North America and Western Europe, insurance penetration is low, so consumers compare custom quotes to USD 50 drugstore alternatives. Margins compress, and vendors experiment with vertical integration to shave lead times and bill to flexible spending accounts, as seen in the Bilt Labs-Health-E Commerce partnership, which accesses 70 million FSA/HSA members. Until broader reimbursement arrives, the pricing gap restrains the foot orthotic insole market, particularly in middle-income economies.

Counterfeit/Low-Quality Products

Online marketplaces list imitation insoles priced under USD 10 that mimic branded packaging without biomechanical testing. These products underperform, sometimes aggravating foot pain, which erodes trust in legitimate brands. Authorities in China and India have stepped up border seizures, yet enforcement remains uneven. Recognized labels use serialized QR codes and warranty registration to authenticate inventory, but consumer education lags. Persistence of gray imports therefore drags on perceived value and slows upgrade cycles within the foot orthotics insoles market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Heat-Moldable Gains on Custom’s Convenience Gap

Custom orthotic insoles accounted for 54.62% of 2025 revenue, yet heat-moldable models are projected to post a 7.52% CAGR, the highest among product types, as shoppers substitute immediate in-store fitting for multi-week lab waits. The foot orthotics insole market, which is attached to custom formats, still benefits from diabetic reimbursement, but convenience-oriented buyers tilt toward thermoplastic units that personalize in minutes.

Thermoplastics soften at 80-100 °C, so footwear associates can shape arches on the sales floor, and loyalty apps then store fit data for re-order prompts, reinforcing brand lock-in. Prefabricated insoles plug the value gap at USD 30-80 and enjoy pharmacy impulse placement, while hybrid lines such as Aetrex Lynco L2200 merge prefab arches with heat-moldable heel cups. As the category blurs, regulators continue to group all versions under the same Class I umbrella, leaving marketing language around “custom” loosely defined, intensifying the branding race in the foot orthotics insoles market.

By Material: Carbon Fiber Disrupts EVA’s Cost Dominance

EVA foam held 28.91% of 2025 revenue thanks to its low unit cost, but composite carbon fiber is set to advance at an 8.24% CAGR as elite and recreational runners pursue weight savings and rebound. Carbon’s premium positioning raises average selling price, expanding the foot orthotics insoles market size even when pair counts stay flat.

Biomechanics research shows carbon inserts trim energy loss during running stride by nearly a tenth, a measurable edge that justifies USD 80-150 ticket prices for performance models. Thermoplastic sheets supply heat-moldable lines, while gel and silicone dominate diabetic care for pressure redistribution. Leather remains a dress-shoe niche, valued for breathability more than support. Brand acquisitions of material suppliers, as OttoBock accomplished in 2024, signal a pivot toward upstream control that shields gross margin and accelerates prototyping in the foot orthotics insoles market.

By Age Group: Pediatric Segment Gains Clinical Validation

Adults accounted for 61.72% of 2025 consumption, but pediatric pairs are forecast to grow at an 8.72% CAGR after randomized trials confirmed that orthoses ease pain in flexible flatfoot cases. Growth in children forces shorter replacement cycles, injecting recurring volume into the foot orthotics insoles market share equation.

Subscription models bundle scans with periodic refits, helping parents budget for natural foot growth and giving vendors predictable revenue. Colorful finishes and low-profile molds address compliance hurdles by ensuring devices fit school and athletic shoes. Evidence that prefabricated designs achieve results comparable to bespoke pairs in many pediatric cases also broadens access among budget-constrained households.

By Application: Sports Segment Outpaces Medical’s Reimbursement Advantage

Medical indications controlled 57.84% of receipts in 2025, yet the sports and athletics lane is on track for a 9.05% CAGR, the swiftest among applications. Factory-installed plates in Brooks Glycerin exemplify how brands bake orthotic tech into mainstream footwear, pulling unit demand into first purchases rather than aftermarket add-ons.

Occupational safety programs are seeing steady uptake as human resources teams link anti-fatigue gear with reduced injury claims, and personal-comfort inserts appeal to clerical and service staff who stand for long hours. Lacking reimbursement, these cash-pay segments compel brands to foreground visible benefits, such as copper-infused antimicrobial linings or carbon-rebound metrics. The diverse use cases are expanding the foot orthotics insole market while challenging firms to segment their messaging precisely.

By Distribution Channel: Online Pharmacies Disrupt Clinic-Centric Model

Hospital pharmacies and specialty clinics captured 43.78% of 2025 sales, but online pharmacies are projected to grow at an 11.99% CAGR as platforms combine at-home impression kits with FSA/HSA eligibility. Seamless checkout without insurance pre-authorization resonates with younger buyers who view clinic visits as a source of friction.

Retail stores still matter for discovery; Dr. Scholl’s foot-mapping kiosks in 5,000 Walgreens locations upsell custom inserts in minutes, while sporting-goods chains pair Aetrex scanners with loyalty-app coupons. The most resilient brands cover all three routes: clinic credibility, retail trial, and e-commerce replenishment, so customers can stay within one ecosystem through life stages, sustaining volume inside the foot orthotics insoles market.

Geography Analysis

North America retained 39.18% of 2025 revenue, as Medicare reimbursement for diabetic orthoses under HCPCS codes A5512-A5513 covered 80% of allowable charges, effectively subsidizing the core at-risk group. A deep innovation cluster, anchored by Volumental, Aetrex, and Superfeet, nurtures fast deployment of scanners and AI kiosks across pharmacy and sporting channels. Canada’s provincial health plans reimburse custom devices for medical diagnoses, though coverage stops at sports or comfort, keeping cash-pay niches lively. Mexico has early-stage but rising disposable income, and more running events push premium athletic insoles, despite limited diabetic reimbursement frameworks.

Europe sits second by value, propelled by Germany, the United Kingdom, and France, where podiatric density and social-insurance schemes normalize orthotic prescriptions. The EU Medical Device Regulation classifies custom insoles as Class I, so entry barriers stay modest while post-market surveillance safeguards quality. German players Bauerfeind and OttoBock leverage vertical integration to speed heat-moldable launches, and Birkenstock’s 2024 investment in 3-D printing extends footbed expertise into therapeutic niches. NHS-backed trials showing prefab efficacy influence payer panels across the continent, nudging purchasing from custom to mid-priced alternatives and widening consumer choice in the foot orthotics insole market.

Asia-Pacific is forecast to post a 7.99% CAGR to 2031, the fastest regional pace. China hosts 140.9 million adults with diabetes, forming a vast preventive-care addressable base. Yet out-of-pocket spending dampens immediate uptake outside urban centers. Japan’s aging demographics spur integration of orthotic plates into walking shoes, while India’s domestic brand Tynor scales value prefabs through pharmacy chains. Australia blends a strong sports culture with universal health coverage, driving early adoption of carbon composites. Middle East & Africa and South America lag because of price sensitivity and lower clinician coverage, but pilot e-commerce programs with smartphone scanning hint at future catch-up once awareness and payment options improve.

Competitive Landscape

No single vendor exceeds a mid-teens share of revenue, so rivalry centers on scanning accuracy, materials science, and omnichannel reach. Aetrex’s Albert 3D Pro device captures 16-foot dimensions and feeds dynamic arch profiles straight to point-of-sale cash desks, lifting conversion rates by 30% for partner stores. Volumental processes more than 1 million cloud scans each month, and its AI engine pinpoints shoe recommendations that cut online return rates by 20%. Brands that can make this data portable across in-store, web, and mobile win higher lifetime value because a shopper’s digital foot twin unlocks frictionless re-orders across seasons.

Material leadership also differentiates. Superfeet’s carbon platform underpins Brooks Running’s Glycerin and Ghost models, embedding orthotic features at the factory and redirecting margin from aftermarket retailers to footwear OEMs. OttoBock’s acquisition of a thermoplastic plant secures substrate supply for heat-moldable lines and trims, resulting in a 10-day to 3-week lead time. Direct-to-consumer newcomers such as Bilt Labs and Upstep unbundle the clinic visit through phone scanning, delivering custom pairs at USD 199 with satisfaction guarantees that overcome first-purchase hesitancy.

Legacy medical-device firms face a strategic fork: double down on reimbursed diabetic channels or pivot into retail and digital arenas that demand marketing heft and UX design rather than physician outreach. The FDA’s Class I exemption levels regulatory hurdles, allowing rapid SKU refresh but also inviting fashion brands like Vionic to integrate arch support into apparel-driven silhouettes. As a result, the foot orthotics insoles market rewards agility over scale, and alliances between scanner software, material innovators, and lifestyle labels form the new center of gravity.

Foot Orthotic Insoles Industry Leaders

DJO Global Inc.

Acor Orthopedic, Inc.

Aetrex Worldwide, Inc.

Algeo Limited

Dr. Scholl's

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Zimmer Biomet announced a definitive agreement to acquire Paragon 28, broadening its footprint in foot-and-ankle solutions.

- January 2025: Hike Medical unveiled an AI-powered browser tool that converts camera phone images into 3-D foot models for quick custom insole manufacturing.

- February 2024: Hanger completed its acquisition of Fillauer, combining manufacturing depth with data-rich clinical networks.

Global Foot Orthotic Insoles Market Report Scope

As per the report's scope, foot orthotic insoles are shoe inserts designed to cure foot deformities and stabilize the biomechanical misalignment of the foot. These are used to reduce pain. These orthotics are custom-made as prescribed by physicians to provide comfort and support to the patients. Many are adopting specially designed orthotic insoles for personal comfort and pain reduction.

The Foot Orthotics Insoles Market Report is Segmented by Product Type (Custom, Prefabricated, Heat-Moldable), Material (EVA Foam, Thermoplastics, Composite Carbon Fiber, Foam & Memory Foam, Gel & Silicone, Leather, Other), Age Group (Adults, Pediatrics), Application (Medical, Sports & Athletics, Personal Comfort, Occupational Safety), Distribution Channel (Hospital Pharmacies & Specialty Clinics, Retail, Online), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Value (USD).

| Custom Orthotic Insoles |

| Prefabricated Orthotic Insoles |

| Heat-Moldable Orthotic Insoles |

| Ethyl-Vinyl Acetate (EVA) Foam |

| Thermoplastics |

| Composite Carbon Fiber |

| Foam & Memory Foam |

| Gel & Silicone |

| Leather |

| Other Materials |

| Adults |

| Pediatrics |

| Medical |

| Sports & Athletics |

| Personal Comfort |

| Occupational Safety |

| Hospital Pharmacies & Specialty Clinics |

| Retail Stores |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Custom Orthotic Insoles | |

| Prefabricated Orthotic Insoles | ||

| Heat-Moldable Orthotic Insoles | ||

| By Material | Ethyl-Vinyl Acetate (EVA) Foam | |

| Thermoplastics | ||

| Composite Carbon Fiber | ||

| Foam & Memory Foam | ||

| Gel & Silicone | ||

| Leather | ||

| Other Materials | ||

| By Age Group | Adults | |

| Pediatrics | ||

| By Application | Medical | |

| Sports & Athletics | ||

| Personal Comfort | ||

| Occupational Safety | ||

| By Distribution Channel | Hospital Pharmacies & Specialty Clinics | |

| Retail Stores | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the foot orthotics insoles market by 2031?

It is forecast to reach USD 6.33 billion, expanding at a 6.98% CAGR from 2026-2031.

Which product category currently leads revenue?

Custom orthotic insoles captured 54.62% of 2025 sales thanks to clinical efficacy and diabetic reimbursement support.

Which application will grow the fastest through 2031?

Sports and athletics are projected to register a 9.05% CAGR as performance footwear brands integrate carbon-fiber plates.

Why are online pharmacies gaining share?

Platforms that combine smartphone scans, at-home kits, and FSA/HSA payments remove clinic visits and are forecast to grow at 11.99% CAGR.

Which material is gaining popularity among athletes?

Composite carbon fiber is advancing at an 8.24% CAGR because it reduces energy loss during operation and enhances durability.

Page last updated on: