Foot Ulcer Sensors Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

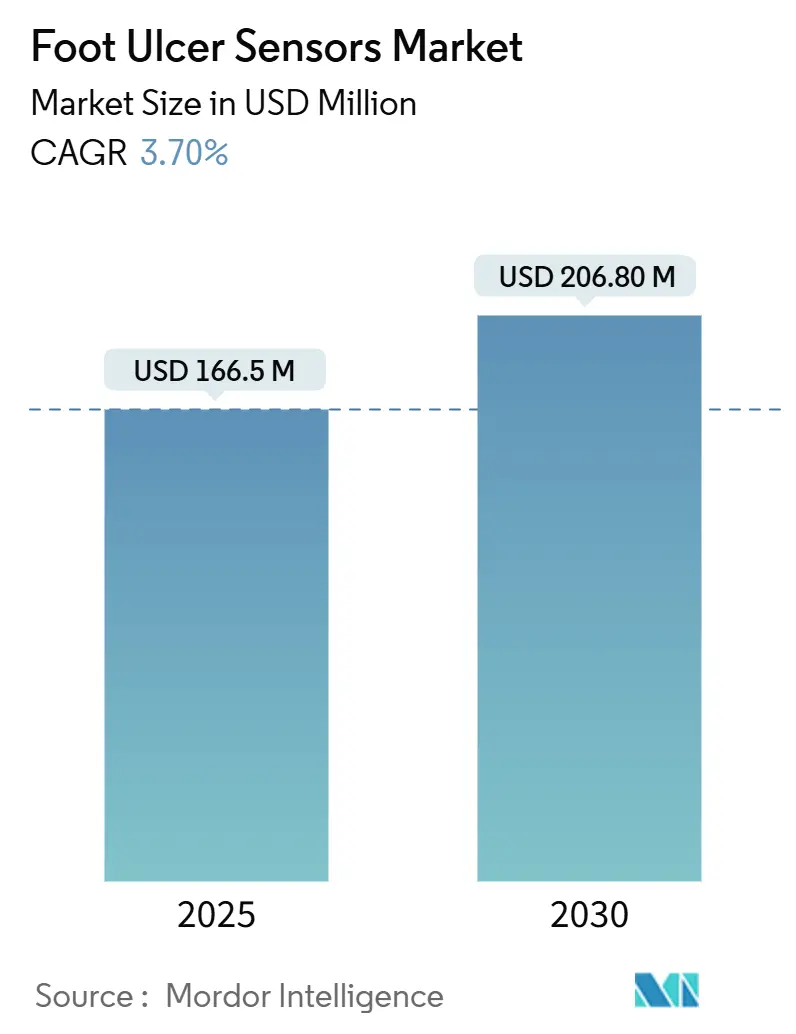

| Market Size (2025) | USD 166.5 Million |

| Market Size (2030) | USD 206.80 Million |

| Growth Rate (2025 - 2030) | 3.70% CAGR |

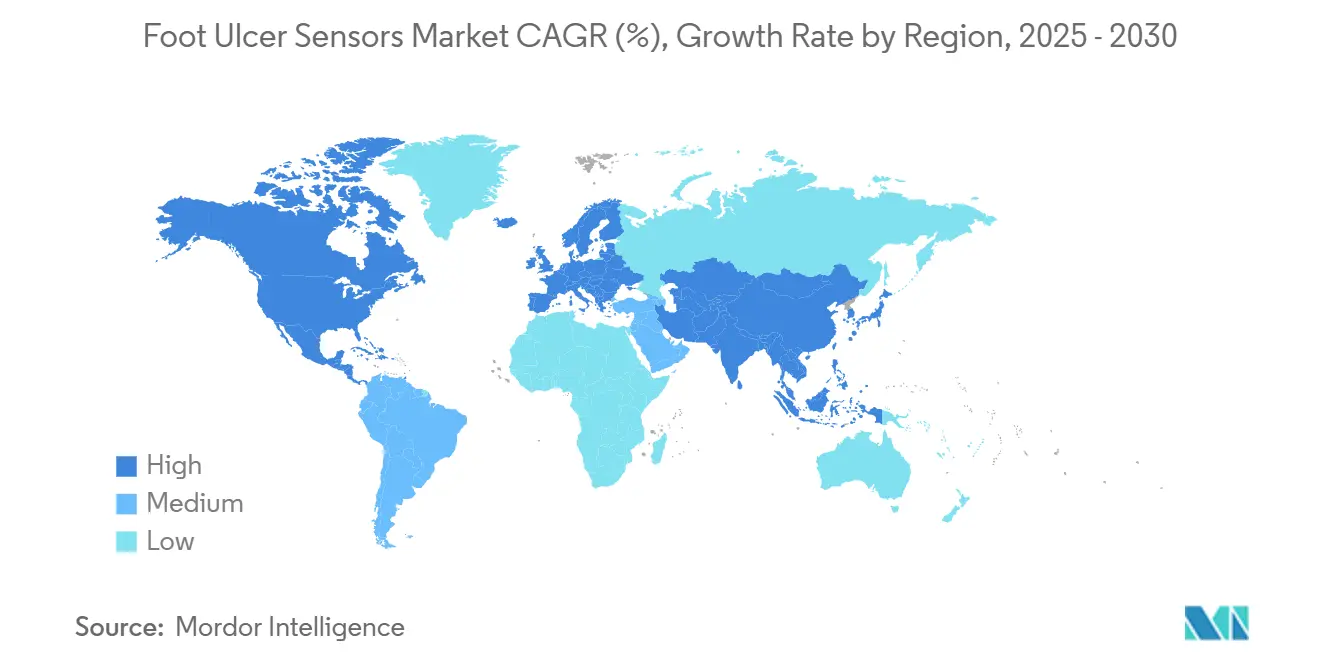

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Foot Ulcer Sensors Market Analysis by Mordor Intelligence

The foot ulcer sensors market size reached USD 166.5 million in 2025 and is projected to expand to USD 206.8 million by 2030, advancing at a 3.7% CAGR. Growing clinical proof that continuous monitoring lowers major amputations by up to 86% and drives direct cost savings of USD 38,593 for every ulcer prevented anchors demand in the period ahead. Adoption momentum is further strengthened by artificial-intelligence platforms that classify ulcer status with 95% accuracy and by reimbursement reforms that treat remote monitoring as a covered benefit under Medicare and allied payers. These clinical and economic incentives, paired with multi-sensor miniaturization, have shifted procurement budgets from experimental pilots to standard-of-care roll-outs, allowing the foot ulcer sensors market to sustain steady, mid-single-digit growth through 2030.

Key Report Takeaways

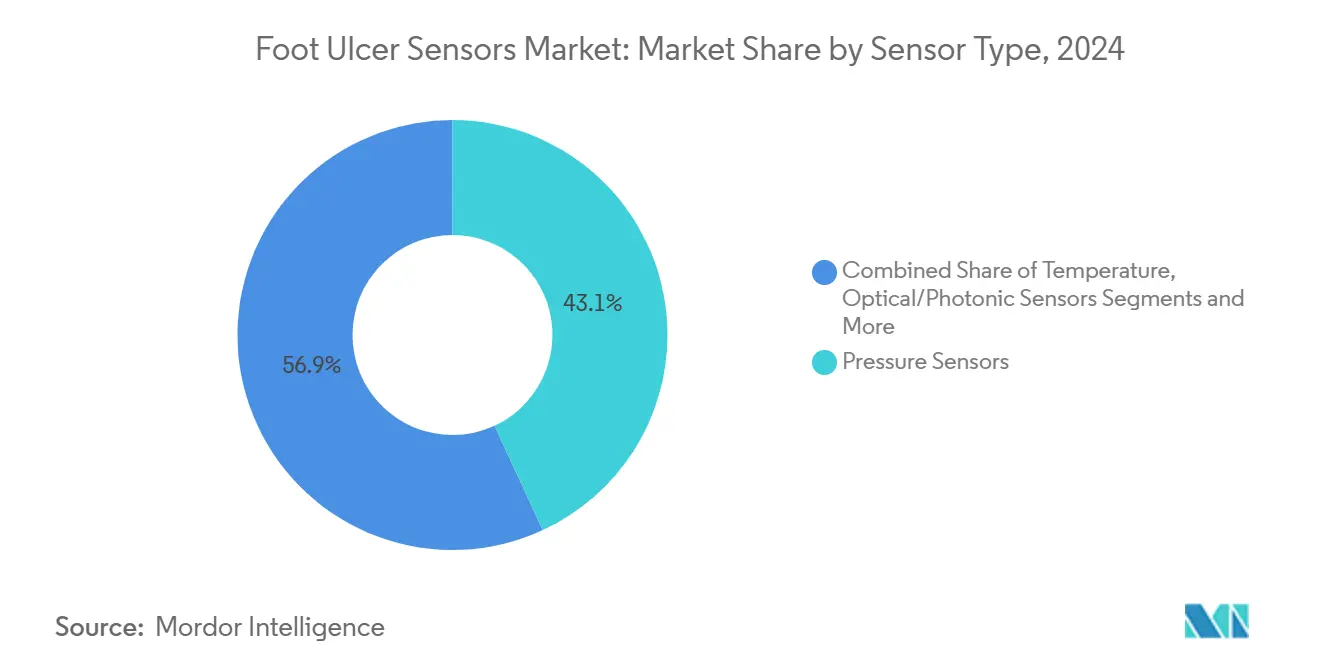

- By sensor type, pressure sensors held 43.1% of foot ulcer sensors market share in 2024, while optical/photonic sensors are forecast to grow at a 4.8% CAGR to 2030.

- By form factor, smart insoles led with 37.2% of the foot ulcer sensors market size in 2024; smart socks are advancing at a 5.4% CAGR through 2030.

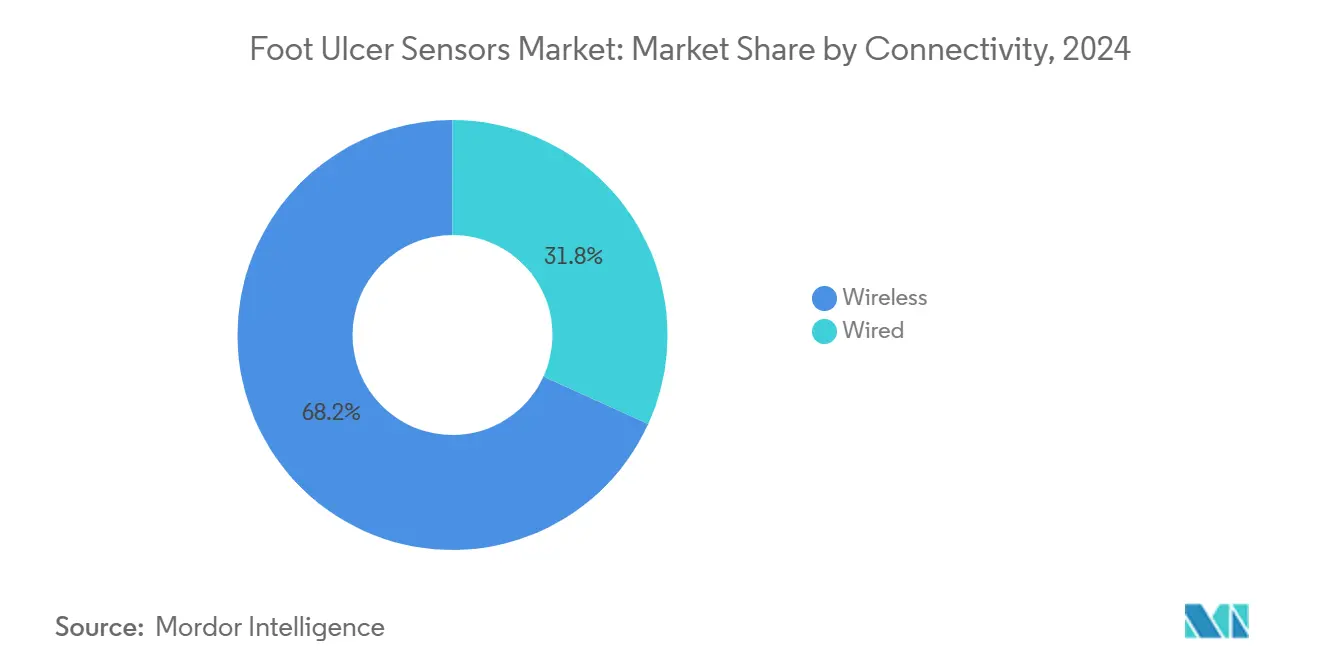

- By connectivity, wireless solutions captured 68.2% revenue in 2024 and are projected to rise at a 7.2% CAGR, reflecting hospital interoperability priorities.

- By end user, hospitals and wound-care centers accounted for 42.7% of 2024 revenue, whereas home-care settings are the fastest-growing channel at a 3.6% CAGR to 2030.

- By geography, North America commanded 38.1% of 2024 revenue; Asia Pacific is projected to register the highest regional CAGR at 4.7% through 2030.

Global Foot Ulcer Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-powered predictive analytics integration | +1.20% | Global; early uptake in North America and EU | Medium term (2-4 years) |

| Rising diabetes prevalence & aging population | +0.80% | Global; strongest in Asia Pacific & North America | Long term (≥ 4 years) |

| Reimbursement expansion for remote monitoring devices | +0.60% | North America & EU core markets | Short term (≤ 2 years) |

| Shift to value-based care & hospital readmission penalties | +0.50% | North America, expanding to EU | Medium term (2-4 years) |

| Miniaturization of multi-modal sensor arrays | +0.30% | Global technology hubs | Medium term (2-4 years) |

| Surge in home-based wound-management programs | +0.40% | North America & EU; emerging in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI-Powered Predictive Analytics Integration

Artificial-intelligence engines now detect ischemia with high accuracy and infections effectively, enabling timely interventions that avert escalating care episodes.[1]Varun Sendilraj, “DFUCare: Deep Learning Platform for Diabetic Foot Ulcer Detection, Analysis, and Monitoring,” Frontiers in Endocrinology, frontiersin.orgDeep-learning algorithms accurately forecast hospital readmissions in diabetic cohorts, allowing care teams to re-allocate resources toward high-risk patients and curb avoidable costs. Vision-transformer models deliver near-perfect precision when identifying ulcer boundaries on smartphone images, democratizing access to specialist-level diagnostics for rural or mobility-limited patients. Explainable-AI frameworks provide transparency for clinicians, building trust and accelerating protocol adoption. Taken together, these gains reposition the foot ulcer sensors market from reactive detection to proactive disease-course modification, reinforcing steady device replacement cycles.

Rising Diabetes Prevalence & Aging Population

More than 422 million people live with diabetes worldwide, and 15% will develop a foot ulcer during their lifetime. Peripheral neuropathy affects roughly 60% of this base, creating a large at-risk population that benefits from continuous biomechanical and thermographic surveillance. Asia Pacific shows the sharpest epidemiological uptick; China alone is on track to host 147 million diabetics by 2030, prompting public-sector investments in smart-footwear reimbursement and tele-wound platforms.[2]Zhikui Tian, “Predicting the Diabetic Foot from Tongue Images and Clinical Information,” Frontiers in Physiology, frontiersin.orgPopulation aging magnifies ulcer incidence because vascular elasticity declines with age, a parameter now factored into machine-learning risk models that predict amputation likelihood. Sustained prevalence and demographic momentum guarantee a sizable, durable customer pool for foot ulcer sensor market participants.

Reimbursement Expansion for Remote Monitoring Devices

The United States finalized local-coverage determinations that reimburse therapeutic shoes equipped with embedded sensors as well as standalone temperature-monitoring platforms, reducing provider uncertainty around claims submission. Medicaid beneficiaries in states offering podiatric coverage experienced lower major-amputation risk, validating the fiscal logic behind preventive monitoring.[3]Abdul Rahaman Wahab Sait, “Diabetic Foot Ulcers Detection Model Using Hybrid CNN–Vision Transformers,” Diagnostics, mdpi.com In Europe, reimbursement programs fast-track AI-driven diabetes devices into statutory insurance. These payment reforms shorten payback periods and spur bulk-buy tenders, feeding predictable revenue into the foot ulcer sensors market.

Shift to Value-Based Care & Hospital Readmission Penalties

U.S. hospitals face readmission penalties when ulcers progress to infection or require surgical debridement within 30 days of discharge. Remote patient-monitoring programs cut ulcer-related readmissions by 30–40%, shielding providers from fiscal penalties and supporting capitated risk contracts. Bundled-payment pilots reimburse the entire ulcer episode, incentivizing health systems to deploy sensor-equipped footwear and cloud dashboards that spot early tissue stress. Digital communication aids counter poor post-discharge comprehension, which otherwise doubles readmission odds. As more systems pivot to value-based billing, sensorized footwear and mats move from niche pilots into formulary staples across the foot ulcer sensors market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy & cybersecurity concerns | −0.7% | Global; peaks in EU under GDPR | Short term (≤ 2 years) |

| Limited clinical validation across diverse ethnic foot morphologies | −0.4% | Global; notable in Asia Pacific & MEA | Medium term (2-4 years) |

| High upfront cost versus conventional dressings | −0.5% | Emerging markets & resource–constrained sites | Medium term (2-4 years) |

| Interoperability gaps with hospital EHR ecosystems | −0.3% | North America & EU health systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-Privacy & Cybersecurity Concerns

Device interconnectivity widens the attack surface for patient-identifiable data, drawing regulatory scrutiny from authorities. Encryption, multifactor authentication, and zero-trust architectures are mandatory but add cost and prolong approval timelines. Recent breaches involving wearables eroded patient confidence, encouraging some hospital compliance teams to delay procurement until vendors certify independent audits. Non-covered entities that sell direct-to-consumer devices fall outside regulation, leaving gaps in recourse if data are mishandled. Until global security standards mature, cyber-risk will weigh on adoption rates.

High Upfront Cost Versus Conventional Dressings

Smart insole kits command price tags several multiples above off-the-shelf offloading footwear, challenging payers in resource-limited settings. The economic case hinges on the avoidance of catastrophic complications, yet longitudinal savings materialize over multi-year horizons, exceeding typical budget cycles. Insurance coding for emerging devices sometimes lags innovation, forcing patients to self-pay and depressing volume. As component prices fall and pay-for-performance contracts proliferate, financial barriers should gradually loosen, but near-term capital constraints remain a headwind for the foot ulcer sensors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Pressure Leads While Optics Accelerate

Pressure sensors generated the most significant slice of revenue in 2024, accounting for 43.1% of the foot ulcer sensors market share, thanks to decades of clinical use that link elevated plantar stress directly to ulcer onset. Investments in thin-film MEMS and real-time analytics preserve their dominance. Yet, optical/photonic sensors are gaining momentum, clocking a forecast 4.8% CAGR to 2030 on the strength of infrared thermography and spectroscopic tissue-oxygen mapping. The foot ulcer sensors market size tied to hybrid designs that marry pressure and thermal inputs is projected to climb steadily as clinicians favor multi-modal risk profiling.

Thermal imagers that detect subcutaneous hotspots 2–3 weeks before skin breakdown are already clearing regulatory pathways, broadening clinical utility beyond pressure-centric protocols. Future gains hinge on validating optical algorithms across varied skin pigmentation and on refining calibration routines that compensate for ambient temperature swings. Suppliers that synchronize data streams from pressure mats, NIR optics, and galvanic-skin-response electrodes could raise switching costs and secure multi-year maintenance contracts.

By Form Factor: Insoles Dominate, Socks Surge

Smart insoles captured 37.2% of 2024 revenue because they overlay seamlessly onto clinicians’ long-standing offloading workflows and require minimal patient behavior change. This form factor also permits sensor density high enough to map localized pressure gradients in real time, aligning with reimbursement criteria that demand objective risk documentation. On the horizon, smart socks are on track to post the fastest unit growth at a 5.4% CAGR, leveraging conductive yarns that embed thermistors and strain gauges directly into textile weaves.

Siren-branded prototypes report alert accuracy exceeding 90% when plantar temperatures diverge by more than 2 °C between feet. Continuous-knit production lines cut unit costs, making textile-integrated wearables attractive for capitated care organizations. Smart shoes that couple inertial sensors with embedded force plates remain in pilot phases but promise full-gait analytics that could shift ulcer prevention toward whole-limb biomechanics. Niche scanner platforms that deliver high-resolution 3-D morphology models retain value for complex cases but will not materially dent the overall foot ulcer sensors market size.

By Connectivity: Wireless Integration Prevails

Hospital CIOs gravitate toward Wi-Fi and Bluetooth LE endpoints that plug straight into electronic health-record data brokers. Consequently, wireless architectures commanded 68.2% of 2024 revenue and are predicted to log a 7.2% CAGR through 2030. The upside rests on energy-frugal microcontrollers and edge AI compression that curbs data-plan fees. Wired devices retain pockets of demand in high-acuity wards, where uninterrupted power and deterministic latency trump mobility.

Initiatives that standardize HL7 FHIR bidirectional APIs are dismantling integration barriers, and pilots using piezo-electric harvesting show promise for battery-free footwear inserts. As hospitals consolidate vendor panels, suppliers able to certify end-to-end cybersecurity and deliver real-time HL7-FHIR hand-offs will enjoy a competitive moat in the foot ulcer sensors market.

By End User: Hospitals Anchor, Home Care Expands

Hospitals and wound-care centers generated 42.7% of 2024 sales, reflecting entrenched referral pathways and the availability of multidisciplinary teams to interpret sensor outputs. However, the home-care channel is pacing the field with a 3.6% CAGR, propelled by reimbursement parity for remote physiologic monitoring and by mounting evidence that outpatient programs accelerate healing.

Ambulatory surgical centers deploy scanners mainly for pre-operative planning, while long-term care facilities are beginning to trial smart socks bundled with mobile nurse dashboards to slash transfer admissions. Future share gains hinge on simplifying patient onboarding and automating alert triage so that overburdened home-health nurses can act at the right moment without alert fatigue.

Geography Analysis

North America controlled 38.1% of 2024 revenue, aided by Medicare policy that reimburses both sensorized footwear and remote-monitoring codes, effectively collapsing payer resistance. FDA guidance on diabetic foot infection drugs and digital health submissions further streamlines market clearance, shrinking the time to launch for novel form factors. Robust venture capital pipelines and collaboration between academic wound centers and sensor start-ups sustain a dynamic ecosystem that regularly refreshes clinical evidence.

Asia Pacific is the fastest-growing region, with a projected 4.7% CAGR through 2030, underpinned by rapid urbanization, lifestyle shifts, and government-funded tele-endocrinology networks in China and India. Public-private investments in semiconductor and textile manufacturing lower bill-of-materials costs, enabling local brands to serve price-sensitive health systems while complying with domestic procurement rules. Pilot programs in India’s tier-2 cities show uptake when devices integrate multilingual coaching apps that mitigate cultural and literacy barriers.

Europe maintains steadier but meaningful growth supported by universal health coverage and pan-EU initiatives to harmonize real-world-evidence data sets. Privacy mandates elevate vendor selection criteria, encouraging providers to choose platforms with on-device encryption and patient-centric consent flows. The European Medical Device Regulation’s rigorous clinical evaluation rules prolong launch timelines but confer market trust once approvals are obtained, positioning cleared devices for cross-border scale within the foot ulcer sensors market.

Competitive Landscape

The foot ulcer sensors market is moderately fragmented, with no single supplier surpassing a double-digit revenue share. Podimetrics has expanded its SmartMat platform and is partnering with integrated-delivery networks to bundle data dashboards and nurse coaching. Mölnlycke’s strategic stake in Siren validates textile-based temperature sensing and underscores incumbents’ push to couple wound dressings with diagnostic wearables.

Orpyx continues to publish long-term data showing an 86% reduction in ulcer recurrence, a clinical credential that helps win group-purchasing contracts among U.S. hospital chains. Start-ups such as IR-MED are advancing optical biomarkers that provide biochemical insight into tissue perfusion, aiming to leapfrog purely mechanical sensors.

Established wound-care companies leverage broad sales channels and regulatory experience, while digital natives differentiate through AI-driven triage and subscription analytics. The competitive edge increasingly hinges on evidence-backed outcomes, integration APIs, and cybersecurity certifications rather than on sensor hardware alone.

Foot Ulcer Sensors Industry Leaders

Podimetrics

Siren Care

Sensoria Health

Orpyx Medical Technologies

FeetMe

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Mölnlycke Health Care invested USD 8 million in Siren to accelerate temperature-sensing textile roll-outs and expand global distribution partnerships.

- January 2025: AlexiGen, Sensoria Health, Defender, and Anderson Medical Supplies formed a Footwear-as-a-Service consortium to embed remote monitoring in offloading footwear for high-risk patients.

- November 2024: Diabetis JSC secured FDA registration for Feetsee, an infrared thermography device that applies machine-learning analysis to foot temperature maps.

Global Foot Ulcer Sensors Market Report Scope

| Pressure Sensors |

| Temperature Sensors |

| Optical/Photonic Sensors |

| Electromagnetic/Impedance Sensors |

| Multi-modal Hybrid Sensors |

| Smart Insoles |

| Smart Socks |

| Smart Shoes |

| Wearable Patches & Strips |

| External Scanner Devices |

| Wireless (Bluetooth, Wi-Fi, NFC) |

| Wired |

| Hospitals & Specialty Wound-Care Centers |

| Home-care Settings |

| Ambulatory Surgical Centers |

| Long-term Care Facilities |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Sensor Type | Pressure Sensors | |

| Temperature Sensors | ||

| Optical/Photonic Sensors | ||

| Electromagnetic/Impedance Sensors | ||

| Multi-modal Hybrid Sensors | ||

| By Form Factor | Smart Insoles | |

| Smart Socks | ||

| Smart Shoes | ||

| Wearable Patches & Strips | ||

| External Scanner Devices | ||

| By Connectivity | Wireless (Bluetooth, Wi-Fi, NFC) | |

| Wired | ||

| By End User | Hospitals & Specialty Wound-Care Centers | |

| Home-care Settings | ||

| Ambulatory Surgical Centers | ||

| Long-term Care Facilities | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is global demand for foot ulcer sensors today?

The foot ulcer sensors market size reached USD 166.5 million in 2025 and is on track to exceed USD 206.8 million by 2030 at a 3.7% CAGR.

Which sensor technology holds the biggest share?

Pressure sensors lead with 43.1% foot ulcer sensors market share thanks to decades of clinical validation.

What region offers the fastest growth opportunity?

Asia Pacific is projected to expand at a 4.7% CAGR, propelled by rising diabetes prevalence and large-scale health-infrastructure investments.

Why are wireless devices preferred in diabetic foot monitoring?

Wireless connectivity captures 68.5% revenue because it streams data directly into electronic health records, enabling real-time clinician action.

How do monitoring devices reduce healthcare costs?

Continuous temperature and pressure tracking prevents ulcers that would otherwise cost USD 38,593 each to treat, generating a positive return on investment for providers.

What is the main barrier to wider adoption?

Data-privacy and cybersecurity concerns remain the top restraint, carrying a ?0.7% drag on forecast CAGR until global standards mature.

Page last updated on: