Compression Bandages Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.43 Billion |

| Market Size (2031) | USD 1.86 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Compression Bandages Market Analysis by Mordor Intelligence

The Compression Bandages Market size is estimated at USD 1.43 billion in 2026, and is expected to reach USD 1.86 billion by 2031, at a CAGR of 5.42% during the forecast period (2026-2031).

Growing preference for multilayer wraps that sustain therapeutic pressure, accelerating demand in Asia-Pacific, and the uptake of smart-bandage prototypes that promise remote monitoring are also expanding the compression bandages market. Home-healthcare providers are capturing volume as Medicare Advantage enrollment climbs, while military field-medicine kits and sports-injury protocols add incremental growth lanes. Competitive strategies now revolve around product differentiation through pressure-regulating laminates, vertical integration that bundles supplies with home-equipment delivery, and targeted M&A to secure manufacturing scale in cost-sensitive regions. Together, these forces create a durable tailwind that should keep the compression bandages market on a mid-single-digit growth trajectory through the forecast period.

Key Report Takeaways

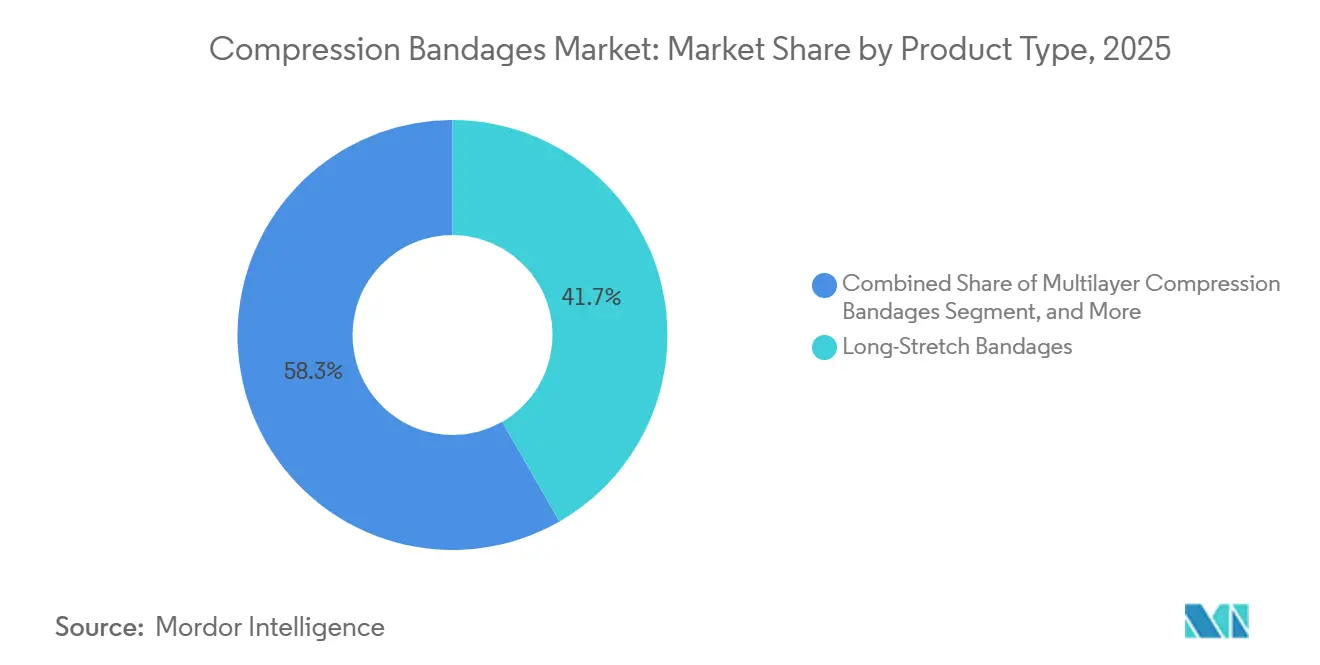

- By product type, long-stretch bandages led with 41.71% of the compression bandages market share in 2025, whereas multilayer systems are forecast to grow at a 7.09% CAGR to 2031.

- By application, venous leg ulcers accounted for 37.57% of the compression bandages market in 2025, while lymphedema treatment is advancing at a 7.78% CAGR through 2031.

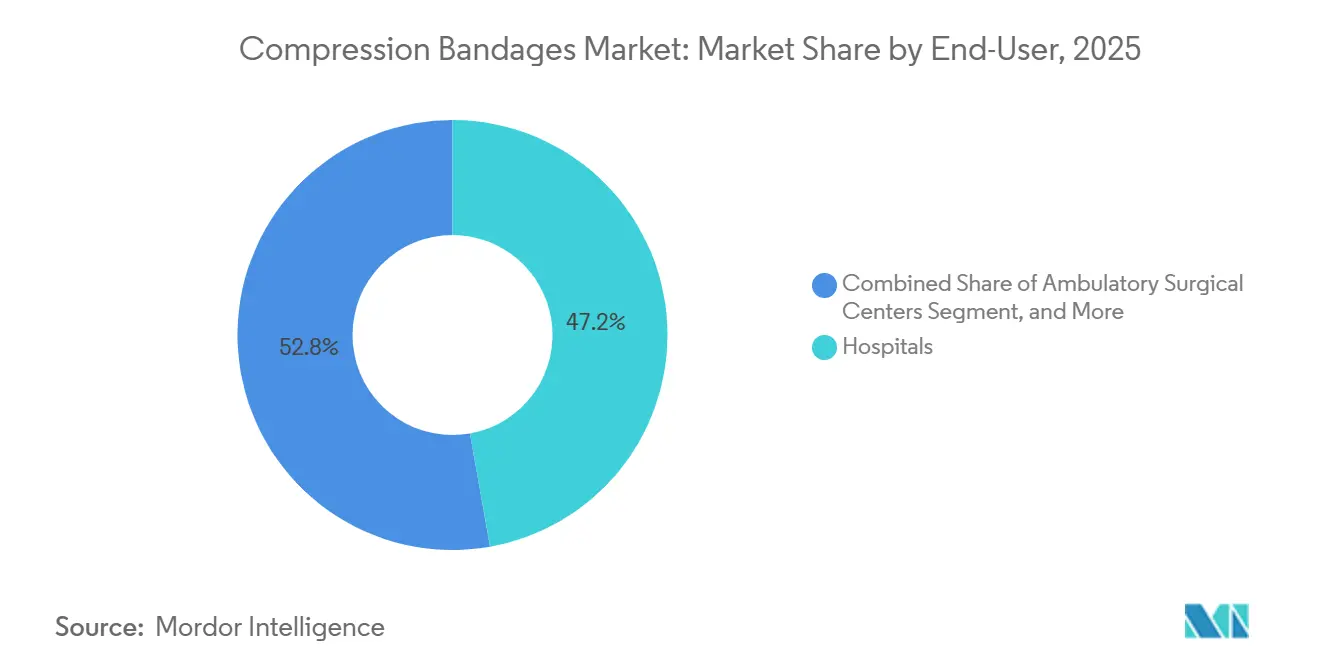

- By end user, hospitals accounted for 47.22% of spending in 2025, yet home healthcare settings are expanding at a 9.69% CAGR through 2031.

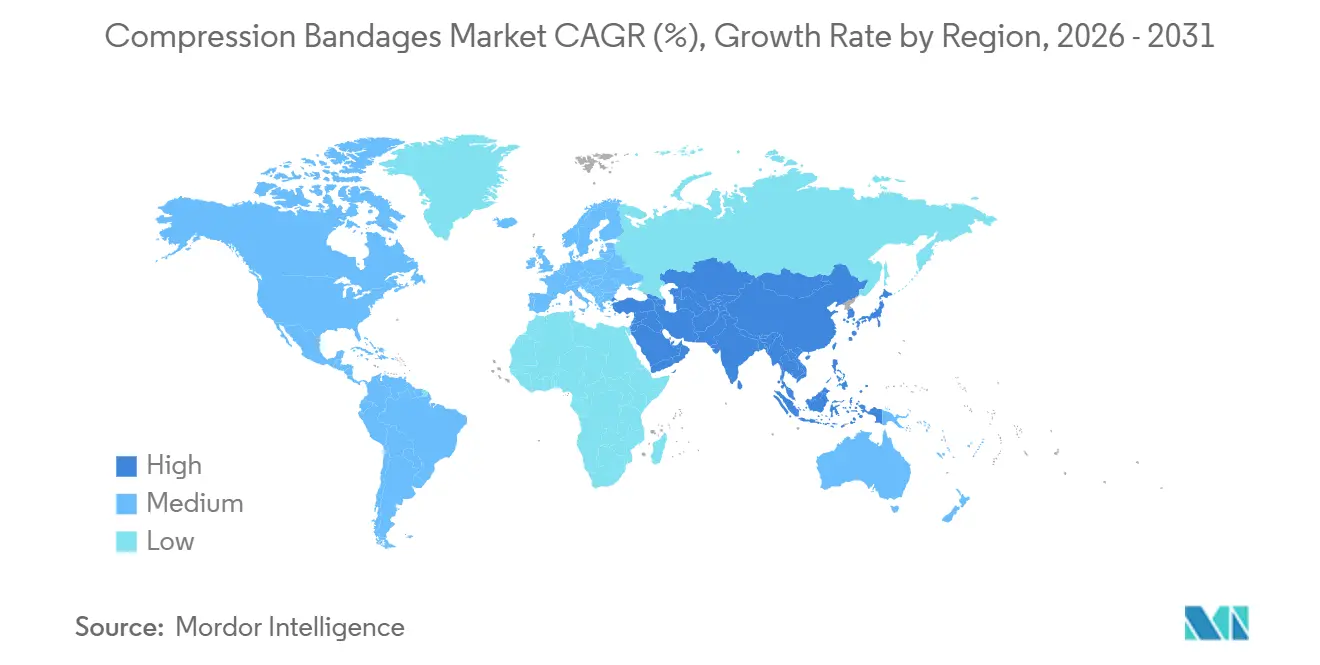

- By geography, North America accounted for 38.83% of revenue in 2025, but Asia-Pacific is poised to outpace with a 10.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Compression Bandages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population and chronic venous disorders surge | +1.2% | Global, concentrated in North America, Europe, Japan | Long term (≥ 4 years) |

| Rising diabetic foot-ulcer prevalence | +0.8% | Global, acute in India, Middle East, US Sun Belt states | Medium term (2-4 years) |

| Post-surgical edema-management protocols tightening | +0.6% | North America, EU, early adoption in Australia | Short term (≤ 2 years) |

| Increasing sports-injury incidence among millennials | +0.5% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Growing use in compression-assisted drug-delivery patches | +0.3% | North America, EU clinical-trial hubs | Long term (≥ 4 years) |

| Military adoption of field hemorrhage-control kits | +0.2% | United States, NATO members, Middle East conflict zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population and Chronic Venous Disorders Surge

The share of the global population aged 65 and above will reach 1.6 billion by 2050, and 25-30% of that cohort already lives with chronic venous insufficiency, pushing sustained demand for compression therapy.[1]Organisation for Economic Co-operation and Development, “Ageing Population Statistics,” OECD.org Japan’s super-aging profile has driven per-capita bandage consumption to levels 40% higher than the OECD average, a pattern that South Korea and Taiwan are now replicating. China’s Healthy China 2030 plan steers CNY 16 trillion (USD 2.3 trillion) toward community clinics that dispense compression supplies, expanding access for 280 million citizens aged 60 and older. Rising obesity, which doubles venous-reflux risk, further amplifies prevalence. Payers are codifying compression as first-line therapy before authorizing surgery, as reflected in the 2024 NICE guidelines, and this reimbursement preference is anchoring the baseline for future growth.

Rising Diabetic Foot-Ulcer Prevalence

Roughly 15-25% of the 537 million adults with diabetes will develop a foot ulcer, and clinical data now validate graduated compression as an adjunct that expedites granulation. India’s Ayushman Bharat scheme added compression wraps to its essential medicines in 2024, tripling demand in tier-2 cities. The International Diabetes Federation forecasts 783 million global cases by 2045, concentrating unmet need in low- and middle-income regions.[2]International Diabetes Federation, “IDF Diabetes Atlas,” IDF.org Adjustable-pressure devices such as the ARTAIRA system, cleared by the FDA in late 2024 for patients with ankle-brachial indices as low as 0.5, allow clinicians to safely titrate to 20-40 mmHg, expanding eligibility when arterial disease co-exists. These technological gains and payer incentives together drive sustained growth in the compression bandages market.

Post-Surgical Edema-Management Protocols Tightening

Enhanced-recovery guidelines now require compression within two hours of orthopedic and vascular surgery in 60% of U.S. hospitals. A 2024 Journal of Vascular Surgery study linked multilayer wraps to 35% shorter hospital stays and 50% lower readmission rates. The American College of Surgeons formalized compression as a required element in its 2025 ERAS update, affecting 4 million annual U.S. procedures. Procurement teams, therefore, bundle multilayer kits into case carts, guaranteeing volume commitments to suppliers that can meet just-in-time delivery schedules. Ambulatory surgical centers, managing 28 million procedures in 2024, favor single-use cohesive wraps that reduce infection-control overhead, widening product segmentation.

Increasing Sports-Injury Incidence Among Millennials

High-impact recreational sports participation among adults aged 25-40 rose 18% between 2020 and 2025 and produced 2.7 million U.S. ankle sprains in 2024 alone. Elastic cohesive bandages that self-adhere without clips have become a standard because they maintain compression during dynamic movement; a 2025 British Journal of Sports Medicine meta-analysis found a 25% faster return-to-play with elastic cohesive bandages versus crepe wraps. Direct-to-consumer brands exploit social media to market subscription deliveries of fresh wraps, bypassing pharmacy markups. The U.S. Army’s Holistic Health and Fitness initiative, rolled out in 2024, issues compression wraps to all active-duty personnel for injury prevention, legitimizing broader civilian uptake.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity in low-income regions | -0.4% | Sub-Saharan Africa, South Asia, Latin America | Medium term (2-4 years) |

| Reimbursement gaps for home-care products | -0.3% | United States, emerging markets | Short term (≤ 2 years) |

| Allergic dermatitis to synthetic elastic yarns | -0.2% | Global, higher in humid climates | Long term (≥ 4 years) |

| Sustainability push away from single-use wraps | -0.2% | European Union, California, selected Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity in Low-Income Regions

Unit prices of USD 5-15 keep compression wraps beyond reach for households earning under USD 2 daily. China’s volume-based procurement policy now mandates 50-70% price cuts for devices included in tenders, squeezing imported margins and encouraging local production.[3]National Healthcare Security Administration of China, “Volume-Based Procurement Policy,” NHSA.gov.cn India levies 10-20% import tariffs to spur domestic manufacturing, thereby delaying the entry of premium products. Brazil’s SUS allocates less than USD 0.50 per capita per year for wound care, restricting reimbursement to low-cost crepe wraps. Limited cold-chain capacity for temperature-sensitive adhesives further complicates tiered pricing, dampening penetration and slowing the growth of the compression bandages market.

Reimbursement Gaps for Home-Care Products

Medicare caps annual compression reimbursement at USD 600, covering only half the supplies needed for intensive lymphedema therapy. Private-insurance parity remains mixed; a 2025 National Lymphedema Network survey found just 40% of commercial plans reimbursed home-use wraps without prior authorization. Multilayer kits, which cost three times as much as single-layer wraps, are often rejected as “convenience items.” Only 18 U.S. states extend Medicaid coverage, and inconsistent billing codes obscure use data, complicating manufacturer-payer negotiations. These frictions cap upside even as policy momentum trends positive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Multilayer Systems Accelerate on Clinical Proof

Long-stretch wraps maintained 41.71% of the compression bandage market share in 2025, thanks to their elastic recoil, making them the sport-medicine staple. Multilayer kits, however, are projected to expand at a 7.09% CAGR, driven by evidence that four-layer systems heal venous ulcers 30% faster than single-layer systems. The compression bandages market size attributed to multilayer products is expected to expand as discharge kits increasingly specify pre-marked systems like 3M’s Coban 2 Lite, which reduces application time to 3 minutes. Hybrid solutions pair foam padding with short-stretch exteriors to balance high working and low resting pressures, making them suitable for mixed arterial-venous cases. Regulatory reclassification of many multilayer wraps to Class I in 2024 removed premarket-notification hurdles, encouraging incremental innovations and speeding their impact on the compression bandages market.

Therapist-preferred short-stretch wraps retain a niche among lymphedema clinics due to their superior lymphatic drainage during muscle pump cycles, yet they scale slowly because certified fitters are in short supply. Elastic cohesive wraps dominate sports and military use for their self-adhering convenience, and tubular wraps continue to serve pediatrics and digit care. Collectively, ongoing product diversification will sustain competitive churn while reinforcing mix-shift in the compression bandages industry upward.

By Application: Lymphedema Surges Past Traditional Venous Indications

Venous leg ulcers still represented 37.57% of use cases in 2025, but lymphedema uptake is growing fastest at a 7.78% CAGR following Medicare coverage that took effect in 2024. The compression bandages market size linked to lymphedema is rising as earlier diagnosis becomes mainstream and telehealth platforms teach patients self-bandaging.

Roughly 10 million Americans live with lymphedema, 40% of them breast-cancer survivors, yet just 30% previously accessed certified care. Post-operative edema management is gaining momentum as ERAS mandates universal compression, while DVT prophylaxis remains a hospital-centric niche, driven by hematology guidelines that recommend mechanical methods for anticoagulation-intolerant patients. Sports-injury and performance-recovery applications continue to move large unit volumes but at lower price points, tempering their revenue contribution to the compression bandages market.

By End-User: Home-Healthcare Settings Capture Value-Based Dollars

Hospitals held 47.22% of the end-user share in 2025, sustained by their role as the primary site for acute wound care and surgical procedures requiring immediate post-operative compression. However, their growth is decelerating as value-based contracts incentivize early discharge and shift follow-up care to lower-cost settings. Home healthcare settings are expanding at 9.69%, driven by Medicare Advantage plans that now cover 33 million Americans and prioritize home-based care to reduce hospital readmissions.

Owens & Minor's USD 1.36 billion acquisition of Rotech Healthcare in July 2024 created a vertically integrated model that bundles compression supplies with home medical equipment delivery, capturing both product margin and service fees. The shift to home care is also driven by patient preference; a 2024 JAMA study found that 78% of chronic-wound patients preferred home treatment when clinical outcomes were equivalent, citing reduced travel burden and greater scheduling flexibility. Telehealth platforms are enabling this transition by providing remote wound assessment and bandaging instruction, a capability that gained regulatory acceptance during the COVID-19 pandemic and has since been codified in permanent Medicare reimbursement codes.

Geography Analysis

North America captured 38.83% of global revenue in 2025, its leadership rooted in early reimbursement reform and dense wound-care ecosystems. The compression bandages market share in the region is stabilizing as treated chronic-wound prevalence leveled at 2.5% of the population in 2024, reflecting gains in diabetes control. Canada reimburses generic wraps universally but restricts premium multilayer systems, creating a two-tier market, while Mexico’s fragmented insurance and specialist shortages slow adoption outside major metros.

Asia-Pacific is the growth engine, set to deliver a 10.27% CAGR through 2031 as China, India, and South Korea fund chronic-disease infrastructure. China’s Healthy China 2030 allocation of CNY 16 trillion (USD 2.3 trillion) finances community clinics now dispensing compression supplies at scale. Volume-based procurement compels multinationals to localize or cede share to domestic leaders such as Winner Medical. India’s Ayushman Bharat insurance program added diabetic foot coverage, tripling provincial demand in 2024. Japan’s super-aging yet mature market grows slowly, while Australia’s benefit schedule still excludes lymphedema bandages, leaving an advocacy gap.

Europe must navigate the EU Medical Device Regulation, which raised clinical-evidence thresholds and squeezed smaller suppliers. Germany’s statutory insurance pays for compression without co-pays, sustaining volume, yet the UK’s NHS delays multilayer uptake despite NICE endorsement, citing budget constraints. The Middle East imports premium wraps for private hospitals, whereas sub-Saharan Africa relies on donated crepe bandages. Latin America’s demand clusters in Brazil and Argentina but is capped by low per-capita wound-care budgets.

Competitive Landscape

Five global incumbents, 3M, Smith & Nephew, Mölnlycke, ConvaTec, and Essity, command a significant share of the compression bandages market through brand depth and broad portfolios. 3M’s 2025 launch of Coban 2 Two-Layer Lite halved nurse application time, giving it traction in hospitals for discharge. Smith & Nephew’s patent covering laminate structures that hold pressure across limb circumferences signals further product differentiation. Mölnlycke invests in Flex-technology wraps, while ConvaTec leverages ostomy-care channels for cross-selling.

Mid-tier rivals pursue scale through acquisition: Lohmann & Rauscher bought Unisurge in April 2025 to secure Asian capacity and hospital access at a competitive cost. Owens & Minor’s USD 1.36 billion purchase of Rotech Healthcare in July 2024 integrated home-delivery logistics with compression supplies, creating a vertically integrated service model. Start-ups commercializing smart wraps with biosensors, such as the iSAFE platform described in a 2025 Nature Communications paper, threaten to disrupt premium niches once regulatory clearance arrives. Subscription e-commerce companies, including Compressa and BandageRx, court millennials with monthly refills that bypass legacy distribution, prompting incumbents to stand up their own direct-sales portals. Regulatory reclassification of multilayer wraps to Class I accelerates iteration cycles, raising the tempo of competitive launches and reinforcing a moderate-fragmentation structure.

Compression Bandages Industry Leaders

3M

Smith & Nephew

B. Braun Melsungen

Essity (BSN Medical)

Medline Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: An analysis of Israeli emergency kits explained how USD 1 tactical bandages popularized elastic compression for civilian preparedness.

- January 2026: Ayida (Xiamen) P&C Technology profiled its elastic and gauze-bandage portfolio as it pushes into export markets.

- June 2024: University of Southern California researchers unveiled “smart bandages” that embed electronics for chronic-wound monitoring.

Global Compression Bandages Market Report Scope

The Compression Bandages Market refers to the global industry encompassing the manufacturing, distribution, and sale of medical-grade compression bandages and related systems that apply controlled external pressure to limbs and other body areas. These devices are primarily used to improve venous return, reduce edema, manage chronic venous insufficiency, prevent and treat venous leg ulcers, control lymphedema, support post-operative swelling, prevent deep vein thrombosis (DVT), and aid in the management of sports injuries or sprains.

The Compression Bandages Market Report is Segmented by Product Type (Short-Stretch, Long-Stretch, Multilayer, Elastic Cohesive, Tubular), Application (Venous Leg Ulcers, Lymphedema, Post-operative Edema, DVT, Sports Injuries), End-user (Hospitals, ASCs, Home-Healthcare, Other), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Terms of Value (USD).

| Short-Stretch Bandages |

| Long-Stretch Bandages |

| Multilayer Compression Bandages |

| Elastic Cohesive Bandages |

| Tubular Compression Bandages |

| Venous Leg Ulcers |

| Lymphedema |

| Post-operative Edema |

| Deep-Vein Thrombosis (DVT) |

| Sports Injuries & Sprains |

| Hospitals |

| Ambulatory Surgical Centers |

| Home-Healthcare Settings |

| Other End Users (Specialty Clinics, Sports Medicine Centers, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Short-Stretch Bandages | |

| Long-Stretch Bandages | ||

| Multilayer Compression Bandages | ||

| Elastic Cohesive Bandages | ||

| Tubular Compression Bandages | ||

| By Application | Venous Leg Ulcers | |

| Lymphedema | ||

| Post-operative Edema | ||

| Deep-Vein Thrombosis (DVT) | ||

| Sports Injuries & Sprains | ||

| By End-user | Hospitals | |

| Ambulatory Surgical Centers | ||

| Home-Healthcare Settings | ||

| Other End Users (Specialty Clinics, Sports Medicine Centers, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the compression bandages market be by 2031?

Forecasts peg the value at USD 1.86 billion, up from USD 1.43 billion in 2026 at a 5.42% CAGR.

Which product category is expanding fastest?

Multilayer systems are projected to grow at a 7.09% CAGR on superior healing outcomes and discharge-kit adoption.

Why is Asia-Pacific attracting attention from manufacturers?

Public-health programs in China, India, and South Korea are funding chronic-disease infrastructure, driving a regional CAGR of 10.27% that surpasses all other geographies.

How are reimbursement changes influencing demand?

The Lymphedema Treatment Act and cascading private-insurance updates now cover more home-use wraps, shifting volume from hospitals to home-health settings growing at 9.69% annually.

What technological advances could reshape the sector?

Smart bandages with embedded sensors and compression-assisted drug-delivery patches promise real-time monitoring and pharmacologic integration within the next few years.

Page last updated on: