Community Wound Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

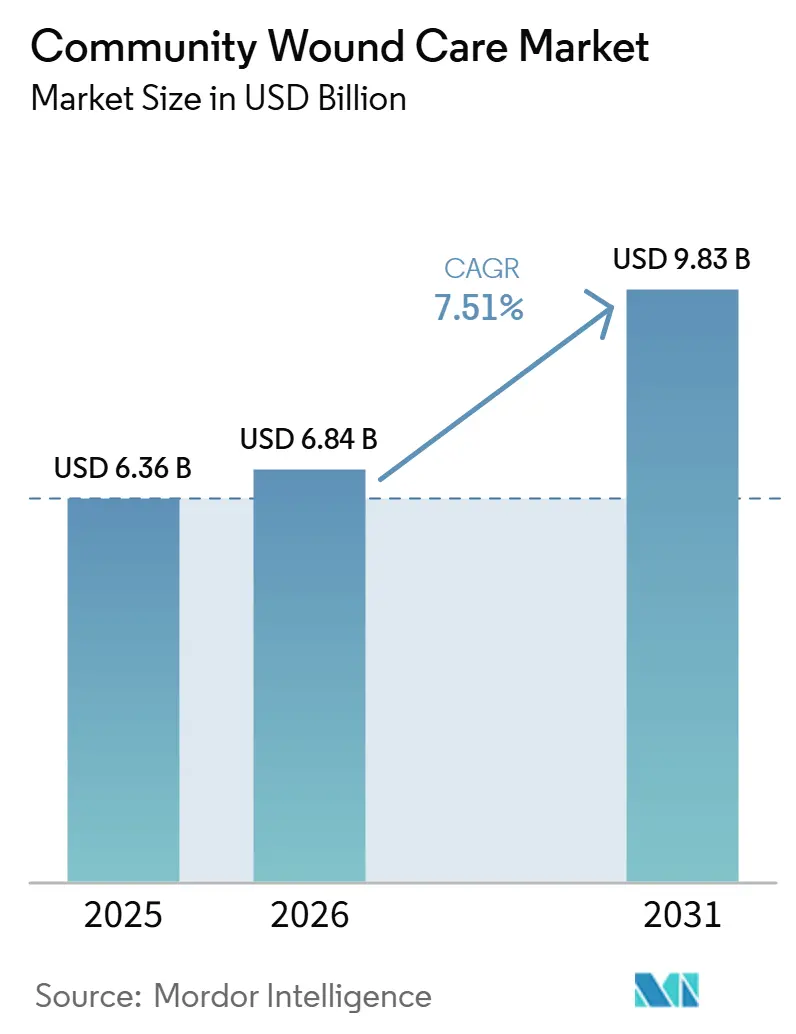

| Market Size (2026) | USD 6.84 Billion |

| Market Size (2031) | USD 9.83 Billion |

| Growth Rate (2026 - 2031) | 7.51% CAGR |

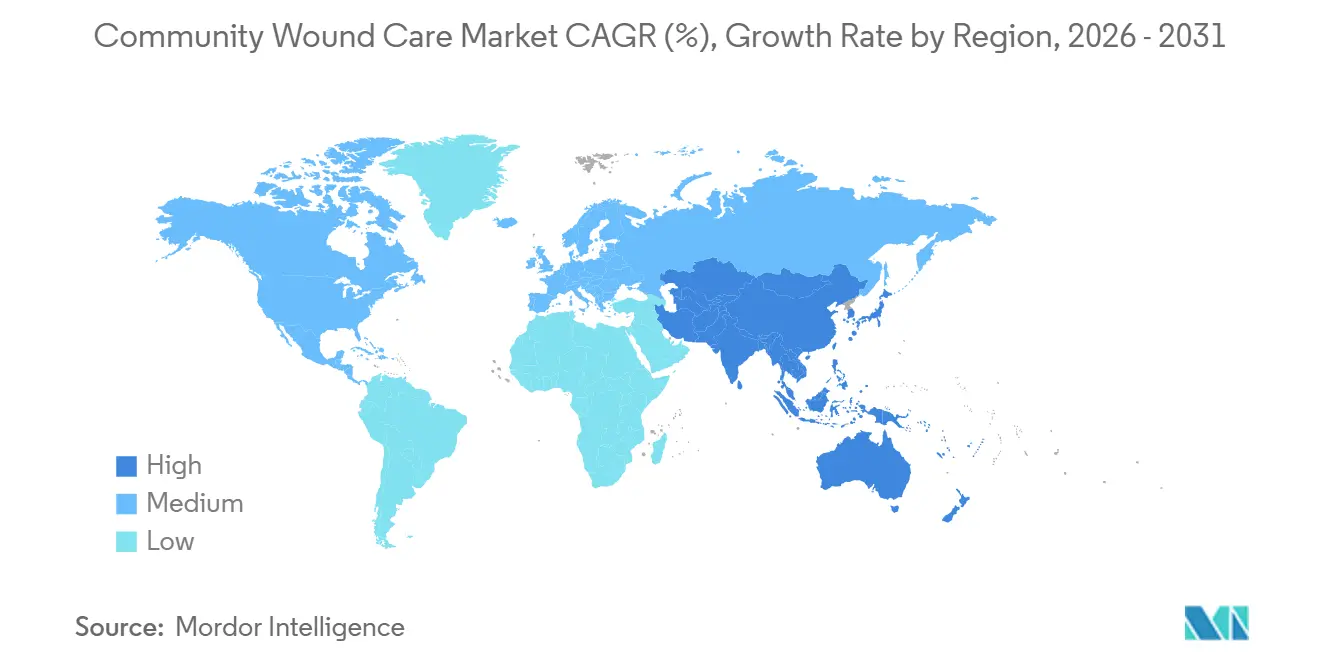

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

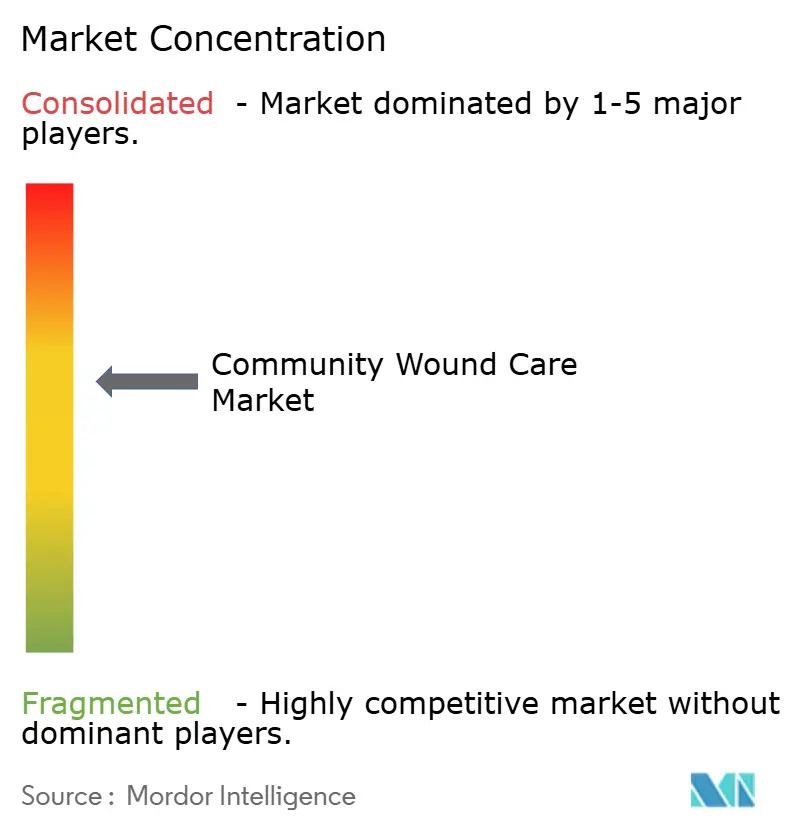

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Community Wound Care Market Analysis by Mordor Intelligence

The Community Wound Care Market size was valued at USD 6.36 billion in 2025 and is estimated to grow from USD 6.84 billion in 2026 to reach USD 9.83 billion by 2031, at a CAGR of 7.51% during the forecast period (2026-2031).

The expansion reflects a persistent chronic wound burden, with 1 in 6 Medicare beneficiaries, or 10.5 million people, living with chronic wounds in 2025, while Medicare wound care costs reached USD 22.50 billion, and 53.1 million Americans had diabetes. Portable negative pressure wound therapy and related advanced therapies are extending the range of wounds that can be treated outside inpatient settings, which is widening the role of the community wound care market across post-acute pathways. AI-enabled documentation and digitally supported wound programs are also helping agencies manage rising acuity with tighter staffing, which improves the operating case for the community wound care market. Reimbursement policy is becoming more decisive in product competition, especially as evidence-backed and covered products gain an advantage over categories that face tighter payment scrutiny in the community wound care market.

Key Report Takeaways

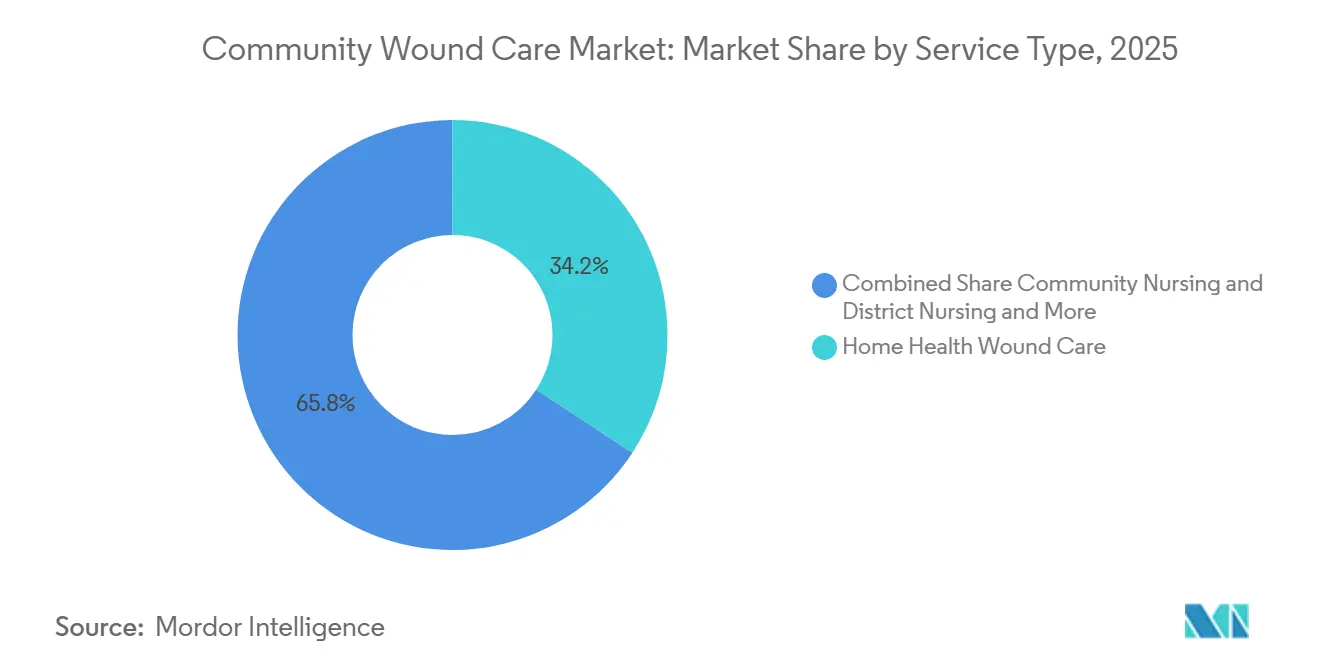

- By service type, Home Health Wound Care held 34.22% of revenue in 2025, while Community Nursing and District Nursing are projected to grow at 8.53% CAGR through 2031.

- By product type, Advanced Wound Dressings accounted for 52.19% of revenue in 2025, while Biologics and Skin Substitutes are projected to expand at 9.17% CAGR through 2031.

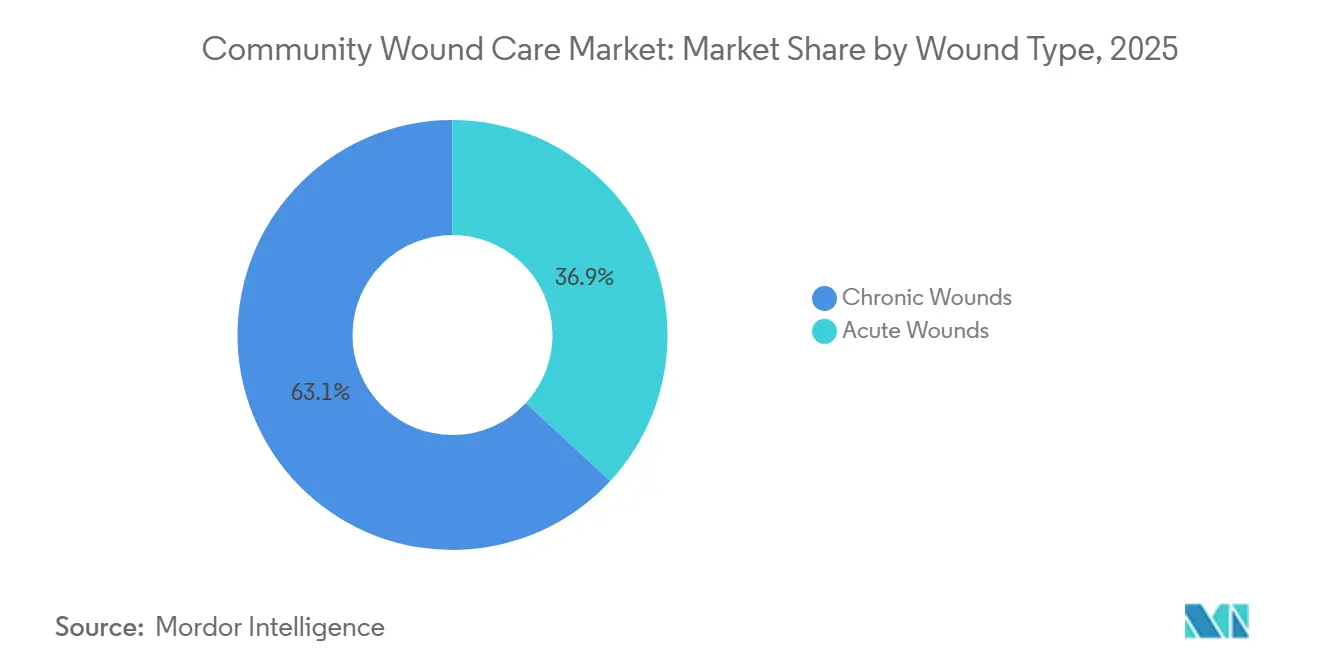

- By wound type, Chronic Wounds represented 63.11% of revenue in 2025, while Diabetic Foot Ulcers are projected to grow at 8.93% CAGR through 2031.

- By end user, Home Care Agencies held 35.21% of revenue in 2025, and the same segment is also projected to record the highest CAGR at 8.47% through 2031.

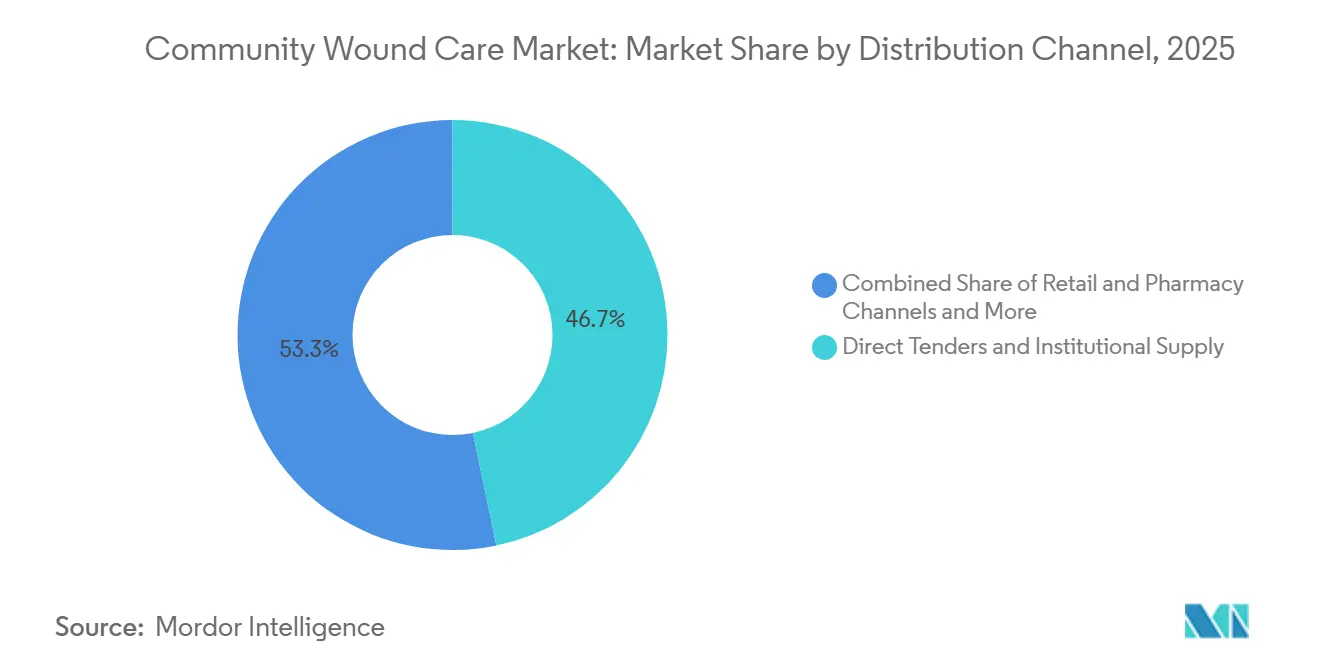

- By distribution channel, Direct Tenders and Institutional Supply captured 46.72% of revenue in 2025, while Online and eCommerce distribution is projected to grow at 11.71% CAGR through 2031.

- By geography, North America represented 35.50% share in 2025, while Asia-Pacific is expected to expand at 7.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Community Wound Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Chronic Wound Burden In Home And Post-Acute Settings | +1.50% | Global, with strongest pressure in North America, Western Europe, and aging Asia-Pacific markets | Long term (≥ 4 years) |

| Shift Of Wound Care Delivery From Hospitals To Community Sites | +1.80% | Global, especially the United States, the United Kingdom, Germany, and Australia | Medium term (2-4 years) |

| Greater Use Of Portable Advanced Wound Therapy In Home Care | +1.20% | North America and Europe, with emerging adoption in Asia-Pacific | Medium term (2-4 years) |

| Better Reimbursement Visibility For Outpatient And Home Health Wound Episodes | +1.40% | North America and selected European reimbursement systems | Short term (≤ 2 years) |

| AI-Assisted Wound Documentation Improving Nurse Productivity | +0.90% | North America, Northern Europe, and early urban Asia-Pacific adoption | Medium term (2-4 years) |

| Care Pathway Standardization In Community Nursing Networks | +0.70% | European Union, especially the United Kingdom, the Netherlands, and Nordic countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Chronic Wound Burden in Home and Post-Acute Settings

Diabetes and vascular disease are expanding the patient base that needs wound care outside hospital settings. In 2025, 53.1 million Americans had diabetes, and 15.00%-34.00% of people with diabetes develop a diabetic foot ulcer over their lifetime, which keeps a steady flow of patients moving into the community wound care market. Chronic wounds affect up to 2.50% of the population in developed countries, which supports recurring demand for dressings, professional visits, and telehealth-enabled monitoring in the community wound care market.

Pressure injuries affect 5.00% of patients receiving community nursing care, and that share rises in long-term care settings where repositioning resources are limited. Chronic wound demand is less exposed to short-term economic swings because healing often requires serial assessment, repeated consumable use, and extended follow-up. This leaves the community wound care market supported by disease patterns that remain embedded across aging and diabetic populations.

Shift of Wound Care Delivery from Hospitals to Community Sites

Payment reform and hospital capacity pressure are moving more wound care into home and community settings. CMS updated the Home Health Prospective Payment System for CY 2026, including changes to 30-day episode rates and case-mix weights that better reflect complex wound presentations managed at home. A 2026 study in the British Journal of Community Nursing reported that community nurses are handling a growing share of patients with multimorbidities whose wounds need interventions once associated with specialist outpatient settings. The shift is raising the clinical intensity of wound care episodes that sit within the community wound care market, which also raises the value of structured protocols and consistent assessment tools. Agencies that rely on unstructured clinical judgment alone are more exposed to variability in healing progression and workload. Agencies that standardize workflows are better placed to turn this care transfer into an advantage within the community wound care market.

Greater Use of Portable Advanced Wound Therapy in Home Care

Portable wound therapy devices are expanding the clinical range of wounds that can be managed outside acute care. Dynarex launched the Dürma+ negative pressure wound therapy pump in February 2026 as an 11.30 oz device with up to 72 hours of uninterrupted therapy, and the product was designed for continuity from hospital to home. Smith+Nephew also continued expanding the reach of its PICO disposable negative pressure wound therapy system into additional wound segments that fit community and home use. CMS set the CY 2026 disposable NPWT device payment at USD 282.10, which improves clarity for agencies using these systems in home health episodes. This helps the community wound care market because it supports earlier discharge without cutting therapy continuity for higher-risk wounds. It also gives providers a practical route to deliver more advanced wound management within the community wound care market.

AI-Assisted Wound Documentation Improving Nurse Productivity

Documentation remains one of the heaviest administrative burdens in home-based wound care. A 2025 review in the Journal of Multidisciplinary Healthcare found that ambient voice-enabled generative AI can reduce documentation time per encounter from 10 minutes to under 1 minute, which directly improves workflow efficiency in the community wound care market. A 2025 controlled intervention study also found that AI-based wound assessment applications are expected to reduce care time and task load once fully deployed. Related work in BMC Nursing noted that AI in home healthcare can support care quality, but implementation still depends on workflow design, staff training, and trust[1]Source: “Navigating Artificial Intelligence in Home Healthcare Challenges and Opportunities in Nursing Wound Care,” BMC Nursing, link.springer.com . The benefit goes beyond faster note entry because digitized wound progression records can also support benchmarking and payer dialogue. That makes AI tools a capacity lever as well as a data asset in the community wound care market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Per-Episode Cost Of Advanced Dressings And Biologics | -1.20% | Global, most acute in the United States following reimbursement reform, and also relevant across selected European private payors | Short term (≤ 2 years) |

| Uneven Coverage Rules Across Payers And Care Settings | -0.90% | North America, with additional variation across European systems | Medium term (2-4 years) |

| Community Workforce Shortages And Variable Wound Expertise | -0.80% | The United States, the United Kingdom, Australia, Germany, and France | Long term (≥ 4 years) |

| Documentation And Coding Burden For Home-Based Wound Claims | -0.60% | North America and the United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Per-Episode Cost of Advanced Dressings and Biologics

The cost of advanced dressings and biologics remains a practical limit on how far premium wound care can spread in community settings. Reimbursement pressure increased when only 18 skin substitute products were confirmed as covered under newly finalized Local Coverage Determinations effective January 1, 2026, which narrowed the commercially protected field around Medicare-supported products in the community wound care market. Coloplast later reported a DKK 3.00 billion (USD 0.45 billion) impairment loss, and linked a weaker recovery in U.S. outpatient wound care to the Medicare reimbursement overhaul affecting skin substitutes. These changes mean premium products need stronger economic justification when community providers operate inside tighter episode payments. Manufacturers can no longer depend on broad premium positioning if coverage is selective and provider margins are compressed. This creates near-term caution around category mix and product adoption in the community wound care market.

Community Workforce Shortages and Variable Wound Expertise

Workforce pressure remains one of the hardest constraints on scale in the community wound care market. A 2026 review in the British Journal of Community Nursing reported that the number of qualified district nurses able to manage hard-to-heal wounds is declining even as multimorbid caseloads are rising. PHI projected in 2025 that the U.S. home care sector will add more than 681,000 jobs over the next decade, yet specialist wound capability is still lagging behind overall home health demand growth. BMC Nursing and the Journal of Multidisciplinary Healthcare both show that digital tools can reduce workload, but they do not remove the need for training, adoption discipline, and clinical judgment[2]Source: Farooq F, Cooper H, Shipman A, Mitchell CD, “Artificial Intelligence Integration in Multidisciplinary Wound Management,” Journal of Multidisciplinary Healthcare, dovepress.com . When wound expertise is uneven, dressing selection, escalation timing, and healing consistency can vary across teams. That makes staffing depth and wound-specific capability a continuing restraint on the community wound care market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Home Health Dominates, District Nursing Accelerates

Home Health Wound Care held 34.22% of revenue in 2025, which made it the largest service segment in the community wound care market. That lead reflects the practical value of clinician-led in-home visits for patients who need repeated dressing changes and close wound follow-up. The service also fits the broader shift away from hospital-centered care, as more complex patients are discharged earlier into structured home episodes. CMS policy updates are reinforcing that direction by improving the payment visibility around home-based wound episodes. Outpatient Wound Clinics remain the next layer for patients whose wound complexity exceeds what one visit at home can safely support.

Community Nursing and District Nursing are projected to grow at 8.53% CAGR through 2031, which makes it the fastest-growing service category within the community wound care market. Germany strengthened this pathway in December 2025 when the G-BA amended the HKP-RL to prioritize chronic and hard-to-heal wound care in home settings using specialized providers. That change expands the addressable base for local nursing services and supports earlier referral away from hospital-led pathways. Long-Term Care and Skilled Nursing Facilities continue to serve older adults whose mobility limits and chronic wound exposure create recurring care demand. The community wound care industry is therefore moving toward more formalized local care pathways, especially where nursing infrastructure and reimbursement rules already support home-first delivery.

By Product Type: Dressing Dominance Faces a Biologics Inflection

Advanced Wound Dressings accounted for 52.19% of the community wound care market size in 2025, which kept them firmly in the lead among product categories. Their position reflects long clinical familiarity, broad payer acceptance, and easy integration into agency and distributor supply chains. Foam, hydrocolloid, and antimicrobial dressings remain core formulary items because they fit a wide range of chronic wound needs during routine community visits. Smith+Nephew reinforced this category in May 2026 with ALLEVYN COMPLETE CARE, a 5-layer foam dressing positioned for chronic wound use in home and community settings. Traditional Wound Care Products still serve lower-complexity acute wounds where cost and ease of use remain important buying factors.

Biologics and Skin Substitutes are projected to grow at 9.17% CAGR through 2031, which places them ahead of every other product segment in the community wound care market. The growth reflects a stronger clinical focus on placental allografts, fish-skin grafts, and related tissue-based options for difficult diabetic foot ulcers and other slow-healing wounds. Wound Therapy Devices also hold an important premium position, especially as portable negative pressure systems make complex wound management more practical at home. The January 2026 reimbursement reset means premium biologics now face more direct scrutiny around coverage and value. That leaves the community wound care market favoring suppliers that can pair strong healing outcomes with more defensible economic positioning.

By Wound Type: Chronic Wounds Define the Market, DFUs Lead Growth

Chronic Wounds represented 63.11% of revenue in 2025, which made them the core clinical demand base within the community wound care market. This group includes diabetic foot ulcers, venous leg ulcers, pressure injuries, and other non-healing wound types that often need repeated dressing changes and ongoing review. The European Wound Management Association reported that venous leg ulcers affect 1.00%-2.00% of the European population, which shows how broad the chronic wound base already is. Recurring wound care needs make these cases operationally important because they drive repeat consumable use, nursing visits, and follow-up across community pathways. Acute Wounds still contribute a meaningful share, but they are more often shorter-duration cases tied to surgery, trauma, or early post-procedural recovery.

Diabetic Foot Ulcers is projected to grow at 8.93% CAGR through 2031, which makes it the fastest-growing wound sub-segment within the community wound care market. Diabetic foot ulcers affect 12.90% of adults with diabetes globally, and the lifetime risk among people with diabetes ranges from 15.00% to 34.00%, which explains why this category draws so much clinical and product attention. MiMedx launched CHORIOFIX in March 2026 and enrolled it in the CAMPAIGN randomized trial, which shows how actively suppliers are targeting non-healing diabetic foot ulcer care. Agencies serving mainly chronic wound caseloads need broader formularies across dressings, biologics, and NPWT than agencies centered on shorter acute episodes. The community wound care industry therefore depends on procurement depth and clear escalation pathways when diabetic and other chronic wounds dominate local caseloads.

By End User: Home Care Agencies Lead and Grow Simultaneously

Home Care Agencies held 35.21% of the community wound care market share in 2025, and they are also projected to grow at 8.47% CAGR through 2031. That rare combination shows that the operational center of the community wound care market is moving deeper into structured home-based delivery. Hospitals and Clinics still act as clinical entry points, but they are more often transferring long-duration wound management into home and community pathways. Long-Term Care Facilities serve populations with high-pressure injury and diabetic foot ulcer exposure, yet per-diem payment structures can limit use of higher-cost advanced products. For suppliers, this means agency buyers increasingly shape product mix, service expectations, and digital workflow needs across the community wound care market.

Ambulatory and Specialized Wound Centers continue to provide the highest clinical density for vascular review, advanced applications, and escalation decisions. These centers are also becoming more important partners for home health teams that need shared oversight for higher-acuity cases between visits. A 2025 home health study found that digitally enabled wound care programs can improve clinical, operational, and economic outcomes, including reduced hospitalizations and visit optimization[3]Source: Mohammed HT et al., “Clinical, Operational, and Economic Benefits of a Digitally Enabled Wound Care Program in Home Health,” PubMed Central, pmc.ncbi.nlm.nih.gov. That finding supports demand for bundled offers that combine consumables with documentation, triage, and decision support in the community wound care market. Vendors that help agencies reduce visit burden without lowering healing quality should have a stronger route to adoption.

By Distribution Channel: Institutional Procurement Holds, eCommerce Disrupts

Direct Tenders and Institutional Supply captured 46.72% of revenue in 2025, which kept them as the largest route to market in the community wound care market. Large health systems, group purchasing organizations, and national home health chains support this position because they can negotiate volume pricing and standardize procurement across sites. MiMedx highlighted the value of this model in May 2026 when it secured Premier and Vizient agreements for G4Derm Plus to widen national access. Medical Supply Distributors still play an important role because many independent agencies depend on them for logistics support and dependable last-mile delivery. Retail and Pharmacy Channels remain relevant where patients manage acute wounds or less complex chronic wounds with simpler dressing needs.

Online and e-commerce distribution is projected to grow at 11.71% CAGR through 2031, which makes it the fastest-growing channel in the community wound care market. The shift reflects procurement digitization among agencies that need frequent replenishment and easier ordering across dispersed care teams. It also supports patient self-purchase when telehealth-linked monitoring points to quick replenishment of consumables. The channel shift is compressing part of the intermediary margin layer, which benefits manufacturers with direct fulfillment capability and puts pressure on slower channel partners in the community wound care market. As digital ordering becomes more routine, supplier responsiveness and inventory visibility are becoming more decisive in the community wound care market.

Geography Analysis

North America held 33.50% of the community wound care market share in 2025, which made it the largest regional base. The United States anchors that position because Medicare home health policy gives providers a defined payment structure for community wound episodes. The CY 2026 rate update set disposable NPWT payment at USD 282.10 per applicable device and updated home health episode rates by 2%, which improves visibility for agencies managing more complex wound caseloads. That clarity supports broader use of advanced wound management in the home and strengthens post-acute continuity within the community wound care market. The January 2026 Medicare skin substitute overhaul also changed competitive conditions by favoring categories and products with clearer reimbursement footing.

Europe remains a major pillar of the community wound care market because district nursing is already built into several health systems. Germany reinforced this model in December 2025 when the G-BA amended the HKP-RL to prioritize chronic and hard-to-heal wounds in home settings through specialized providers. That rule directly expands the reimbursable base for home wound visits under statutory health insurance and gives community providers a stronger position in the care pathway. The United Kingdom continues to face district nurse pressure, and recent nursing literature linked staffing levels and wound expertise directly to wound management consistency and outcomes. These conditions favor suppliers and care partners that can simplify protocols, standardize documentation, and reduce variability within the community wound care market.

Asia-Pacific is projected to grow at 7.21% CAGR through 2031, which makes it the fastest-growing regional part of the community wound care market size. China and India are the primary volume drivers because both combine large diabetic populations with wider community and primary care expansion. The region also benefits from policy direction that supports chronic disease management and community health capacity, which gives wound services a broader base for scale. Japan adds steady demand because its older population structure sustains long-term care and district nursing needs, especially for pressure injury management. The Middle East and Africa remain smaller in scale, but Gulf health systems are widening home health programs as part of broader care delivery diversification. South America is led by Brazil, where public community care structures support wound management, although product access and specialist training gaps still limit faster adoption of advanced wound care.

Competitive Landscape

The community wound care market is moderately concentrated at the product level, while service delivery remains spread across many local providers. Smith+Nephew, ConvaTec, Mölnlycke Health Care, and Solventum continue to anchor advanced dressings and NPWT through broad portfolios, established contracts, and clinical evidence. Biologics-focused challengers such as MiMedx, Organogenesis, and Kerecis add pressure in chronic wound categories where differentiated grafts and allografts can still command attention.

Competitive standing is now shaped more clearly by evidence, coverage status, and channel access, which gives the community wound care market a more selective growth pattern than before. This keeps the community wound care market active across mature dressing segments and faster-growing biologics niches.

Smith+Nephew showed one route in May 2026 when it launched ALLEVYN COMPLETE CARE and announced RENASYS EDGE for chronic wound use in community and home settings. ConvaTec followed an outcomes-led route, and its ConvaNiox dressing received EU and UK approval after a randomized trial showed 60% more diabetic foot ulcers healed and 3 times faster wound area reduction than standard care. MiMedx added distribution strength in May 2026 through Premier and Vizient agreements for G4Derm Plus, which improved national access across participating hospital and wound care networks. Kerecis also protected its position when MariGen and Shield were included among the 18 CMS-covered skin substitute products effective January 1, 2026. These moves show that product innovation, evidence generation, and route-to-market strength now sit at the center of competition in the community wound care market.

A large open space still lies in integrated care support because agencies need documentation tools, formulary guidance, and outcome tracking alongside products. Mid-tier companies can compete well here if they stay close to community nursing workflows and solve daily operating friction. That means the community wound care market rewards firms that lower administrative burden and fit tighter home care budgets, not only firms with the broadest catalogs. Competition should remain balanced rather than winner-take-all because dressings, devices, biologics, and service-linked support each reward different strengths in the community wound care market.

Community Wound Care Industry Leaders

Smith+Nephew

ConvaTec Group PLC

Mölnlycke Health Care AB

Coloplast A/S

Solventum

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Smith+Nephew launched ALLEVYN COMPLETE CARE, a 5-layer foam dressing with demonstrated clinical superiority, and announced the RENASYS EDGE tied NPWT system at the European Wound Management Association conference. Both products target chronic wound management in community and home care settings under Smith+Nephew's new RISE commercial strategy.

- February 2026: Dynarex Corporation launched the Dürma+ Negative Pressure Wound Therapy pump, an 11.30 oz portable device with 72-hour battery life and a full consumables ecosystem, specifically engineered for home care continuity wound management from inpatient through post-acute settings.

- April 2025: ConvaTec received EU and UK regulatory approval for ConvaNiox, a wound dressing combining advanced dressing technology with nitric oxide antimicrobial and antibiofilm action, achieving 60% more diabetic foot ulcers healed and 3 times faster wound area reduction versus standard care in an RCT. A limited European market release commenced, with U.S. regulatory clearance to be initiated in 2026.

Global Community Wound Care Market Report Scope

As per the scope of the report, community wound care refers to the assessment, treatment, management, and monitoring of acute and chronic wounds in non-acute healthcare settings, including patients' homes, community healthcare centers, outpatient clinics, long-term care facilities, and other community-based care environments. Community wound care aims to promote wound healing, prevent complications, reduce hospital admissions and readmissions, improve patient outcomes, and support cost-effective delivery of wound management services through coordinated care provided by healthcare professionals such as wound care specialists, community nurses, district nurses, and home healthcare providers.

The community wound care market is segmented by service type into home health wound care, community nursing and district nursing, outpatient wound clinics, long-term care and skilled nursing facilities, and other service types; by product type into advanced wound dressings, traditional wound care products, wound therapy devices, biologics and skin substitutes, and other product types; by wound type into chronic wounds and acute wounds, with chronic wounds further segmented into diabetic foot ulcers, venous leg ulcers, pressure injuries, and other chronic wounds, and acute wounds further segmented into surgical wounds, traumatic wounds, and other acute wounds; by end user into home care agencies, hospitals and clinics, long-term care facilities, ambulatory and specialized wound centers, and other end users; and by distribution channel into direct tenders and institutional supply, retail and pharmacy channels, online and eCommerce, medical supply distributors, and other distribution channels; and by geography into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Home Health Wound Care |

| Community Nursing and District Nursing |

| Outpatient Wound Clinics |

| Long-Term Care and Skilled Nursing Facilities |

| Others |

| Advanced Wound Dressings |

| Traditional Wound Care Products |

| Wound Therapy Devices |

| Biologics and Skin Substitutes |

| Others |

| Chronic Wounds | Diabetic Foot Ulcers |

| Venous Leg Ulcers | |

| Pressure Injuries | |

| Other Chronic Wounds | |

| Acute Wounds | Surgical Wounds |

| Traumatic Wounds | |

| Other Acute Wounds |

| Home Care Agencies |

| Hospitals and Clinics |

| Long-Term Care Facilities |

| Ambulatory and Specialized Wound Centers |

| Others |

| Direct Tenders and Institutional Supply |

| Retail and Pharmacy Channels |

| Online and eCommerce |

| Medical Supply Distributors |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Home Health Wound Care | |

| Community Nursing and District Nursing | ||

| Outpatient Wound Clinics | ||

| Long-Term Care and Skilled Nursing Facilities | ||

| Others | ||

| By Product Type | Advanced Wound Dressings | |

| Traditional Wound Care Products | ||

| Wound Therapy Devices | ||

| Biologics and Skin Substitutes | ||

| Others | ||

| By Wound Type | Chronic Wounds | Diabetic Foot Ulcers |

| Venous Leg Ulcers | ||

| Pressure Injuries | ||

| Other Chronic Wounds | ||

| Acute Wounds | Surgical Wounds | |

| Traumatic Wounds | ||

| Other Acute Wounds | ||

| By End User | Home Care Agencies | |

| Hospitals and Clinics | ||

| Long-Term Care Facilities | ||

| Ambulatory and Specialized Wound Centers | ||

| Others | ||

| By Distribution Channel | Direct Tenders and Institutional Supply | |

| Retail and Pharmacy Channels | ||

| Online and eCommerce | ||

| Medical Supply Distributors | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current and forecast size of community wound care?

The community wound care market size was USD 6.36 billion in 2025, reached USD 6.84 billion in 2026, and is forecast to reach USD 9.83 billion by 2031 at a 7.51% CAGR.

Which service setting leads wound care outside hospitals?

Home Health Wound Care led with 34.22% of revenue in 2025, which shows that clinician-led in-home visits remain the primary service model.

Which product category is growing the fastest?

Biologics and Skin Substitutes is the fastest-growing product category, with a projected 9.17% CAGR through 2031, although reimbursement scrutiny is stronger than before.

Why are diabetic foot ulcers so important in this field?

Diabetic Foot Ulcers are projected to grow at 8.93% CAGR, supported by a large diabetes burden and the long treatment cycles often required for non-healing cases.

Which distribution channel is expanding the quickest?

Online and eCommerce distribution is projected to grow at 11.71% CAGR through 2031 as agencies digitize procurement and patients increasingly self-purchase consumables.

Which region is growing the fastest?

Asia-Pacific is projected to grow at 7.21% CAGR through 2031, supported by large diabetic populations and wider community health capacity in major countries.

Page last updated on: