Foot And Ankle Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

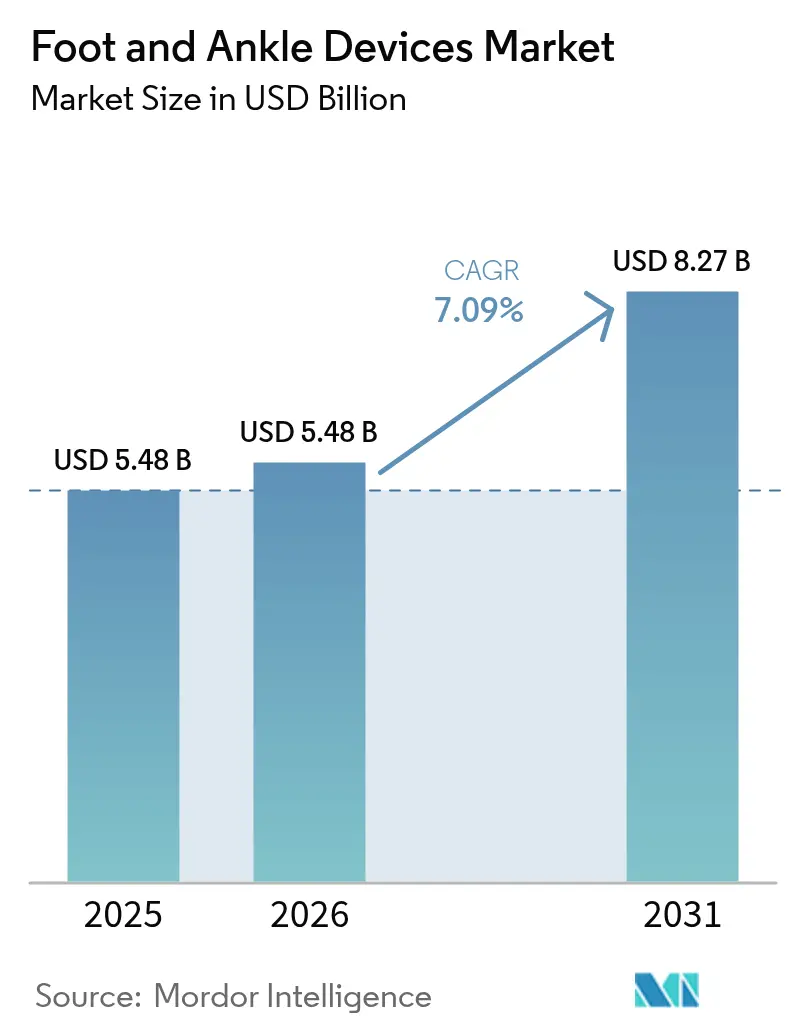

| Market Size (2026) | USD 5.48 Billion |

| Market Size (2031) | USD 8.27 Billion |

| Growth Rate (2026 - 2031) | 7.09% CAGR |

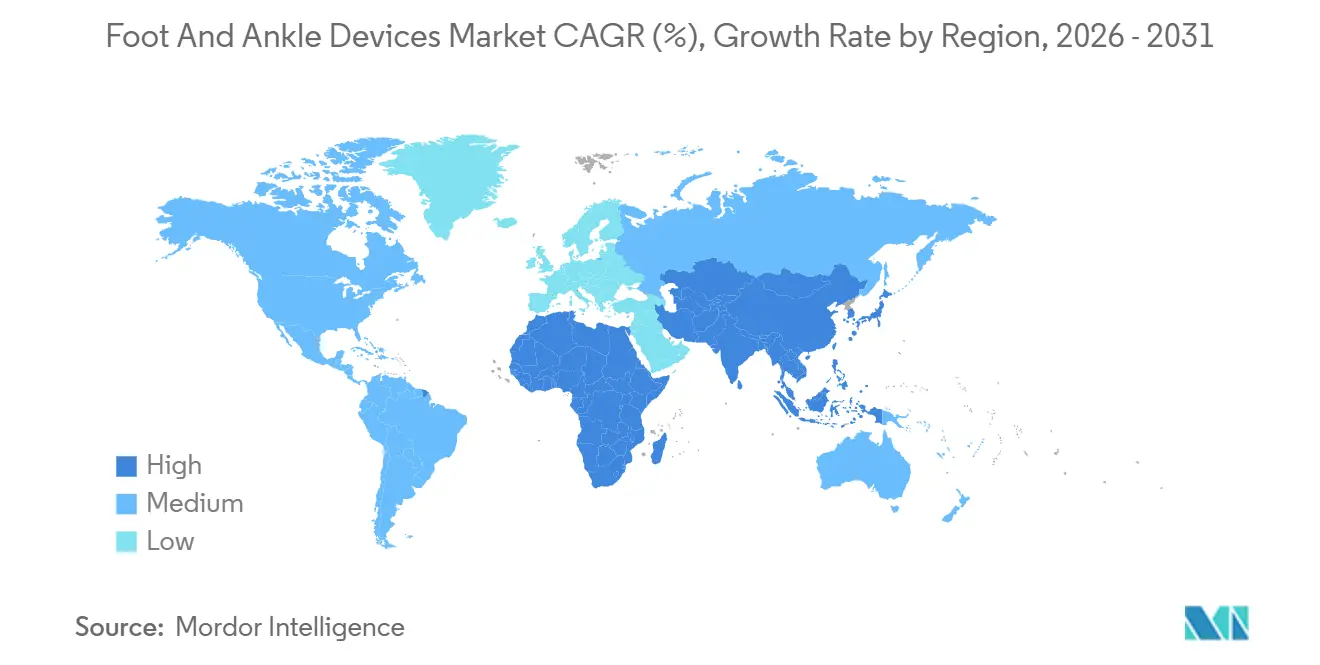

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

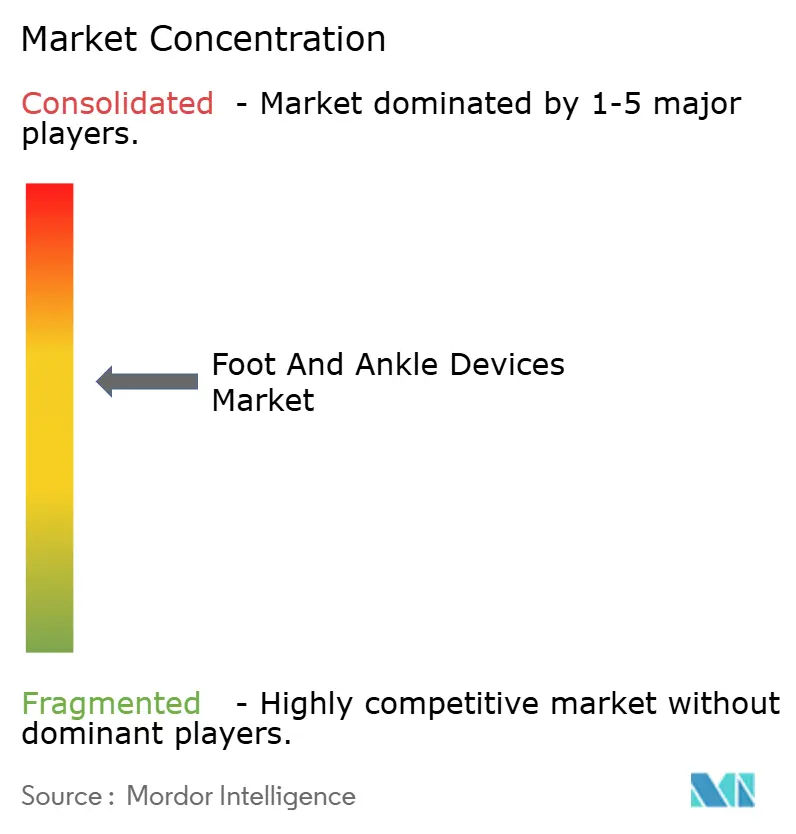

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Foot And Ankle Devices Market Analysis by Mordor Intelligence

The Foot And Ankle Devices Market size is expected to grow from USD 5.48 billion in 2025 to USD 5.48 billion in 2026 and is forecast to reach USD 8.27 billion by 2031 at 7.09% CAGR over 2026-2031.

Ambulatory surgery centers are absorbing elective reconstructions at scale, specialty clinics are adding in-house operating suites, and smart implants are entering routine use. Microprocessor-controlled prostheses, patient-matched fixation hardware, and porous 3D-printed fusion cages shorten operating time while raising procedural accuracy. Demographic aging in Asia-Pacific, the diabetes surge in every region, and an uptick in high-energy trauma among younger cohorts sustain double-digit growth in reconstructive and fracture care volumes. Competitive intensity is increasing as niche specialists convert focused R&D into quick FDA clearances, forcing diversified majors to accelerate additive manufacturing and digital-surgery programs.

Key Report Takeaways

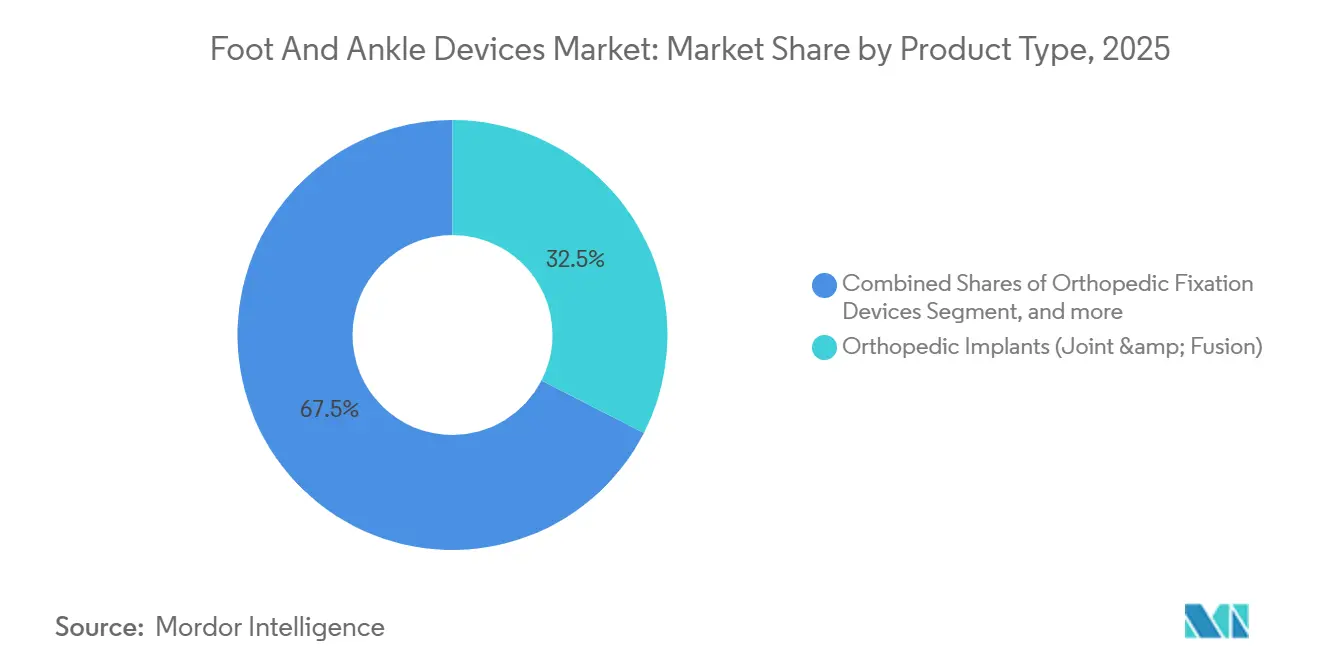

- By product type, prostheses commanded 32.8% of the foot and ankle devices market share in 2025 and are projected to lead growth at a 9.5% CAGR through 2031.

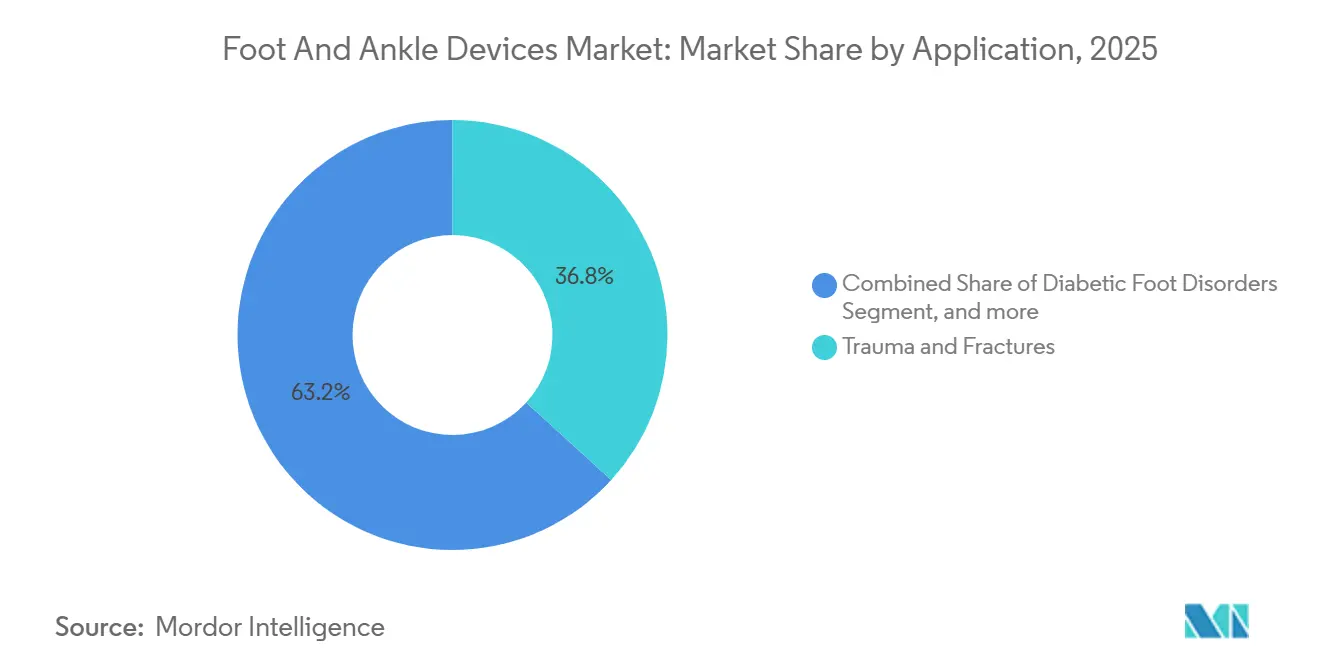

- By application, trauma and fractures accounted for 36.8% of the foot and ankle devices market in 2025, while diabetic foot disorders are forecast to grow at a 10.2% CAGR through 2031.

- By end user, specialty orthopedic and podiatric clinics captured the fastest expansion, advancing at a 10.4% CAGR over 2026-2031.

- By geography, North America held 43.21% of the ankle and foot devices market in 2025, whereas Asia is projected to grow the quickest with an 8.54% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Foot And Ankle Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Surgical Volume From Trauma And Degenerative Conditions | +1.8% | North America and Europe lead; global relevance | Medium term (2-4 years) |

| Technological Advancements In Implant Materials And Digital Surgery | +1.5% | North America and EU mature; APAC catching up | Long term (≥ 4 years) |

| Migration Of Procedures To Ambulatory Surgery Centers | +1.2% | North America dominant; Australia and UK early movers | Short term (≤ 2 years) |

| Rising Global Geriatric And Obese Population | +1.4% | Core APAC, global spill-over | Long term (≥ 4 years) |

| Emergence Of Bio-Scaffold And Regenerative Solutions | +0.9% | U.S., EU clinical hubs; early uptake in Japan | Medium term (2-4 years) |

| Integration Of Smart Implants And Remote Monitoring | +1.0% | U.S. and Canada first adopters; gradual EU rollout | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Surgical Volume from Trauma and Degenerative Conditions

Trauma and degenerative pathologies together drive more than half of all device demand, and fracture care alone represented 36.8% of 2025 applications. Vehicle collisions, sports injuries, and workplace accidents fuel high-energy ankle fractures in younger adults, while fragile bones amplify fracture rates in seniors living longer with osteoporosis. Surgeons increasingly favor minimally invasive fixation, locking plates, and revision-friendly nails that permit earlier weight bearing and faster rehabilitation. Registry data from 2025 confirmed that anatomic plating improved alignment and reduced nonunion rates compared with conventional constructs[1]British Orthopaedic Foot & Ankle Society, “Annual Registry Report 2025,” bofas.org.uk. Launches such as Zimmer Biomet’s Gorilla Pilon Fusion Plating System illustrate how companies refine hardware geometry for comminuted injuries and arthrodesis requirements. The steady rise of joint-preserving options delays end-stage arthrodesis, enlarging the long-term procedure pool.

Technological Advancements in Implant Materials and Digital Surgery

Regulatory clarity for patient-matched implants is accelerating adoption of 3D-printed titanium and cobalt-chromium constructs that mirror a patient’s bone contours[2]U.S. Food and Drug Administration, “Technical Considerations for Additively Manufactured Medical Devices 2024,” fda.gov. Porous lattices foster osseointegration, while single-use guides shave minutes off operative time. Clearance of Paragon 28’s APEX 3D Total Ankle System in 2024 validated the speed with which smaller firms can translate additive manufacturing into commercial products. Digital platforms overlay navigation cues in surgeons’ field of view; Johnson & Johnson’s VOLT mini plating system pairs with augmented-reality headsets to perfect screw trajectories. Sensor-enabled implants such as Canary Medical’s Canturio TE stream real-time load data to cloud dashboards, supporting tele-rehabilitation and early warning of loosening. Standardization bodies, notably ASTM F3001, now guide non-destructive testing routines that flag micro-porosity and prevent fatigue failure.

Migration of Procedures to Ambulatory Surgery Centers

Payer rule changes moved hip, knee, shoulder, and ankle procedures off inpatient-only lists, channeling cases to high-throughput ambulatory surgery centers. A 2025 Centers for Medicare & Medicaid Services review showed that outpatient joints accounted for more than 85% of total replacements in the United States, a pattern that also holds for elective hindfoot fusions. Lower overhead, tighter scheduling, and infection rates under 0.5% appeal to both surgeons and insurers. Device vendors respond with pre-sterilized implant sets and streamlined single-tray instrumentation that fit the ambulatory workflow. Specialty clinics, many physician-owned, reinvest procedural margins in on-site imaging and therapy, fueling a 10.4% CAGR through 2031 as they pull volume from hospitals.

Rising Global Geriatric and Obese Population

China expects 280 million citizens to be 60 years or older by 2025, and Japan already reports 28% of residents are above 65 years. The metabolic burden is rising in parallel: the International Diabetes Federation projects 783 million adults will live with diabetes by 2045, up from 578 million in 2025, and up to one-third risk chronic foot ulcers. Age and obesity degrade joint cartilage and elevate fracture risk, lifting surgical volumes for arthrodesis, arthroplasty, and complex fixation. Asia-Pacific hospitals investing in digital radiography and navigation under India’s 2025 Health Mission illustrate how emerging systems are scaling capacity. Device makers are tailoring portfolios, introducing lower-cost stainless constructions alongside premium titanium lines to address budget diversity without compromising outcomes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Treatment Cost And Limited Reimbursement In Emerging Markets | -0.9% | APAC, MEA, South America | Medium term (2-4 years) |

| Stringent Global Regulatory And Post-Market Surveillance Requirements | -0.7% | EU leads, worldwide convergence | Long term (≥ 4 years) |

| Clinical Concerns Over Implant Longevity And Revision Risk | -0.8% | North America, Europe registries; global watch | Short term (≤ 2 years) |

| Manufacturing Quality Challenges In Additive And Customized Implants | -0.6% | Global, with focus on U.S. and EU regulators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Treatment Cost and Limited Reimbursement in Emerging Markets

Self-payment remains dominant in much of South Asia, Africa, and parts of Latin America, where per capita health outlays are below USD 600. Implant packages for total ankle arthroplasty can exceed USD 8,000 before facility and surgeon fees, pushing procedures out of reach for most households. India’s Ayushman Bharat scheme reimburses catastrophic care but caps implant pricing, compelling many patients to downgrade to basic stainless-steel systems or forgo surgery. Private insurance penetration below 5% across several emerging economies slows the uptake of premium prostheses and digital instrumentation. Tiered product families help vendors address cost pressure, but fragmented pricing complicates forecasting and inventory management.

Stringent Global Regulatory and Post-Market Surveillance Requirements

The European Union’s Medical Device Regulation, fully enforced in 2024, now requires longitudinal clinical evidence and real-time vigilance reporting for Class III implants. Notified-body audits, predicate gaps, and expanded labeling raise compliance expenses, delaying market entry—especially for start-ups. The U.S. FDA is tightening oversight of additive manufacturing, requiring validation of powder reuse and XCT imaging datasets for every 510(k) submission. Registries, such as the British Orthopaedic Foot & Ankle Society’s 2025 report, flagged specific prosthesis models with elevated loosening rates, illustrating how surveillance can prompt recalls. China and Japan are echoing the EU's evidentiary demands, creating multilayered regulatory hurdles that lengthen product cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Prostheses Lead Innovation Velocity

Prostheses opened 2026 with 32.9% revenue and are projected to post a 9.5% CAGR to 2031, making them the strongest contributor to the foot and ankle devices market. High-end microprocessor ankles, such as Össur’s 2024 Proprio Foot, adjust joint angles in real time, lowering metabolic cost by up to 15% and enabling stair ambulation without compensatory hip swing. Orthopedic reconstruction implants secure a 32.5% share, yet their growth moderates as surgeons debate ten-year survivorship, which still trails hip and knee analogs by roughly 80%. Fixation hardware remains essential for complex fractures, with variable-angle plates and percutaneous nails facilitating soft-tissue-gentle techniques that quicken rehabilitation. The foot and ankle devices market size for fixation solutions is projected to reach USD 2.7 billion by 2031 at a 6.2% CAGR. Bracing, supports, and bio-scaffolds occupy smaller but rising niches as demand for ligament repair and cartilage preservation mounts.

A push toward patient-matched constructs is visible across all subcategories. Electron-beam melting and laser-powder bed fusion create porous geometries that are impossible to achieve with machining, enhancing osteointegration and distributing load more evenly across reconstructed joints. Regulatory acceptance is widening: the FDA cleared five patient-matched ankle constructs in 2025 alone, twice as many as in 2023. Vendors now ship single-use cutting guides with QR-coded sterilization logs, aligning with ambulatory center preferences for disposable instrumentation that curbs reprocessing overhead.

By Application: Diabetic Foot Disorders Surge Amid Metabolic Epidemic

Trauma and fractures kept their 36.8% lead in 2025, yet diabetic foot disorders are advancing at a 10.2% CAGR, poised to overtake sports-injury and arthritis segments before 2031. Roughly one in two adults with diabetes develops peripheral neuropathy, and up to 30% progress to ulceration without vigilant offloading. The foot and ankle devices market share attached to offloading orthoses, custom carbon insoles, and Charcot reconstruction implants is widening fastest in Asia-Pacific, where diabetes prevalence rose sharply in 2025. Limb-salvage algorithms that integrate multidirectional external frames with antibiotic-impregnated spacers preserve function and limit amputations. Sports and congenital categories maintain mid-single-digit growth, supported by bioresorbable suture anchors and interference screws that return athletes to play sooner.

Regenerative approaches are gaining mindshare in earlier-stage arthritis. Surgeons combine microfracture with particulated juvenile cartilage matrices, such as Arthrex’s BioCartilage, to delay definitive fusion or replacement. Real-world evidence presented at orthopedic congresses in 2025 indicated that biologic augmentation can prolong symptom-free intervals by two to three years for mid-foot chondral lesions. While payers remain cautious, procedure bundling that merges biologics with minimally invasive osteotomies is under evaluation in U.S. centers.

By End-User: Ambulatory Centers Accelerate Expansion

Hospitals still contributed 55.4% of 2025 revenue but ceded growth momentum to physician-owned specialty centers. Such clinics integrate imaging, therapy, and surgery under one roof, improving continuity and compressing overall care episodes. The foot and ankle devices market size in specialty settings is forecast to climb from USD 2.2 billion in 2026 to USD 3.6 billion by 2031. Ambulatory centers suit device kits optimized for single-tray logistics, reinforcing vendor efforts to simplify instrument lines. Hospitals, under payer pressure, negotiate volume rebates that favor established majors, whereas clinics often select premium, patient-specific systems to differentiate offerings.

Rehabilitation facilities form a smaller but strategic channel, absorbing advanced prosthetic fitting and force-plate gait training post-surgery. Collaborations between rehab networks and smart-implant makers generate outcome data that support value-based reimbursement. Device suppliers use these partnerships to refine sensor algorithms and to demonstrate reductions in readmission and revision, building the dossier payers demand for premium pricing.

Geography Analysis

North America accounted for 43.2% of 2025 sales, driven by Medicare-backed outpatient migration and the rapid adoption of patient-matched hardware. FDA guidance issued in 2024 clarified additive manufacturing file requirements, accelerating clearances for complex hindfoot cages that cut operative time by 20%. U.S. private insurers followed CMS's lead, expanding ambulatory surgery center coverage for ankle arthroplasty in their 2026 policies. Canadian provinces pooled procurement for standard trauma plates, slimming system costs, while Mexico’s private hospitals marketed premium reconstructions to inbound medical tourists from Central America.

Asia-Pacific is projected to record the fastest regional CAGR at 8.5% through 2031. China’s 14th Five-Year Plan prioritizes community trauma centers, and provincial tenders in 2026 favored vendors offering training packages with navigation units. India’s Health Mission funded digital radiography suites and navigation modules for 150 district hospitals in 2025, opening rural corridors previously underserved[3]. Japan’s super-aged demographic escalated ankle fracture admissions 11% year-on-year in 2025, prompting insurers to raise arthrodesis reimbursement. Australia’s robust private coverage underwrites early adoption of smart implants, while Korean surgeons pioneer mixed-reality navigation in hindfoot fusions supported by government innovation grants.

Europe and South America delivered mid-single-digit expansion. EU Medical Device Regulation compliance costs delayed several small-company launches but reinforced patient safety and opened consortium opportunities for real-world registries. Germany and France awarded multi-year bulk tenders in 2025 that bundled trauma and diabetic foot constructs, stabilizing prices but reducing vendor count. In the United Kingdom, National Health Service wait lists for complex reconstructions exceeded 12 months in late 2025, pushing some patients onto private pathways that offer quicker access to high-end implants. Brazil and Argentina led South American demand; fluctuating exchange rates added procurement risk, so hospitals negotiated installment contracts in USD to secure 2026 deliveries.

Competitive Landscape

The competitive field is moderately fragmented. Four diversified orthopedics majors—Stryker, Zimmer Biomet, Johnson & Johnson DePuy Synthes, and Smith & Nephew—collectively account for roughly 55% of worldwide revenue. Their strengths lie in multi-line portfolios, surgeon education programs, and global distribution. They defend share by investing in in-house 3D-printing hubs; Stryker’s Facility 8 in Arizona went live in mid-2025 with an annual capacity of 70,000 patient-matched trabecular implants. Meanwhile, agile specialists such as Paragon 28 and Extremity Medical focus on foot-and-ankle-only kits, accelerating iterations that address niche anatomical challenges. Paragon 28 logged 2025 revenue growth of more than 20% after its APEX 3D ankle debut.

Emerging disruptors marry digital and biologic capabilities. Canary Medical works with Zimmer Biomet to integrate load-sensing stems into legacy nails, enriching long-term surveillance datasets. Arthrex advances regenerative matrices that extend the time to replacement in younger, active patients. Manufacturers view post-market registries as competitive assets: companies that contribute validated real-world outcomes data gain faster tender acceptance and greater payer confidence. Quality management remains a litmus test under MDR and evolving FDA expectations; product lines passing radiographic defect analysis per ASTM F3001 gain a reputational advantage as additive manufacturing scales.

Foot And Ankle Devices Industry Leaders

Arthrex Inc.

Zimmer Biomet

Smith & Nephew PLC

Stryker Corporation

Johnson & Johnson (DePuy Synthes)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Zimmer Biomet unveiled the Gorilla Pilon Fusion Plating System and Phantom TTC Nail, broadening its trauma suite for comminuted fractures

- June 2025: Stryker secured FDA 510(k) clearance for the Incompass Total Ankle System, featuring a hydroxyapatite-coated tibial plate designed to curb aseptic loosening.

- October 2024: Johnson & Johnson MedTech introduced the VOLT mini plating set, compatible with augmented-reality navigation headsets, at AAOS Annual Meeting

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the foot and ankle devices market as the global sales value of surgical implants, replacement systems, fixation plates, screws, external fixators, biologics, and power tools that physicians deploy to repair, fuse, or replace bones and soft tissue structures from the mid-foot to the distal tibia.

Scope Exclusions: Everyday bracing, over-the-counter orthotics, and generic walking aids remain outside the defined scope to keep estimates anchored to implantable and OR-used hardware.

Segmentation Overview

- By Product Type

- Orthopedic Fixation Devices

- Orthopedic Implants (Joint & Fusion)

- Bracing & Support Devices

- Prostheses

- Soft-Tissue Orthopedic Devices

- By Application

- Trauma & Fractures

- Osteoarthritis & Rheumatoid Arthritis

- Diabetic Foot Disorders

- Neurological & Congenital Disorders

- Sports-Related Injuries & Others

- By End-User

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Specialty Orthopedic / Podiatric Clinics

- Rehabilitation Centers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed foot & ankle surgeons, ASC administrators, and procurement managers across North America, Europe, Asia-Pacific, and select Middle-East hubs. These discussions validated device mix shifts (for example, patient-matched 3-D printed talar implants) and confirmed regional ASP differentials as well as adoption hurdles that secondary sources could not capture.

Desk Research

We extracted baseline procedure counts and injury incidence from open data sets such as the World Health Organization hospitalization database, the United States CDC's National Hospital Discharge Survey, Eurostat surgical statistics, and Japan's MHLW patient survey, which outline how frequently ankle fractures or arthrodesis occur. Trade flow indicators from UN Comtrade helped us size import-dependent regions, while registries maintained by the American Academy of Orthopaedic Surgeons and the Australian Orthopaedic Association clarified device longevity and revision trends. To cross-check corporate revenue splits, we screened D&B Hoovers and Dow Jones Factiva filings, complemented by peer-reviewed papers in journals like Foot & Ankle International that report average selling prices. The sources named are illustrative; many additional references informed data checks and contextual understanding.

Market-Sizing & Forecasting

We begin with a top-down reconstruction that multiplies region-level procedure volumes by verified utilization rates and weighted ASPs, followed by a selective bottom-up roll-up of publicly reported revenues from leading suppliers to fine-tune totals. Key model variables include annual ankle fracture incidence, elective total ankle replacement penetration, outpatient surgery share, mean implant ASP progression, diabetes-linked ulcer prevalence, and regulatory approval cadence. Forecasts rely on a multivariate regression blended with scenario analysis; coefficients are stress-tested with expert consensus before locking the base case. Where supplier data are sparse, gap-fill factors draw on historical procurement ratios observed in comparable orthopedic segments.

Data Validation & Update Cycle

Outputs pass three internal reviews, variance flags trigger re-checks with interview contacts, and abnormal swings against sentinel metrics, such as procedure volumes, trade entries, or quarterly revenues, are resolved before sign-off. Reports refresh annually, and a mid-cycle update is issued if material events, such as major recalls or blockbuster approvals, shift market sentiment.

Why Mordor's Foot And Ankle Devices Baseline Stand Solid

Published estimates often diverge because firms choose dissimilar product mixes, convert currencies at different dates, or stretch projections beyond validated inputs.

Key gap drivers center on whether power tools are bundled with implants, how outpatient migration is modeled, and the refresh cadence each firm follows; Mordor's analysis reports current-year 2025 values and applies uniform 2024 average FX rates, which some publishers overlook.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.12 B (2025) | Mordor Intelligence | - |

| USD 4.75 B (2024) | Global Consultancy A | excludes power tools; older base year |

| USD 5.20 B (2024) | Industry Association B | bundles braces; assumes uniform ASP across regions |

In essence, our disciplined source hierarchy, clear product boundaries, and yearly refresh give decision-makers a balanced, reproducible baseline that withstands scrutiny while still being easy for new analysts and clients to follow.

Key Questions Answered in the Report

How fast is the foot and ankle devices market expected to grow through 2031?

Revenue is forecast to rise from USD 5.87 billion in 2026 to USD 8.27 billion by 2031, advancing at a 7.1% CAGR.

Which product category shows the strongest future momentum?

Prostheses are projected to expand at a 9.5% CAGR, fueled by microprocessor ankles and patient-matched total ankle systems.

Which application is emerging quickest?

Diabetic foot disorder interventions, including offloading orthoses and Charcot reconstruction hardware, are set to grow at a 10.2% CAGR.

Why are specialty clinics gaining share?

Payers reward lower-cost ambulatory settings, and physician-owned centers integrate imaging, therapy, and surgery, driving a 10.4% CAGR for this channel.

Which region will add the most new revenue?

Asia-Pacific is forecast to post the highest regional CAGR at 8.5% as China, India, and Japan expand orthopedic capacity and coverage.

What technology trends will shape competition?

Patient-matched 3D-printed implants, sensor-enabled hardware, and augmented-reality navigation will differentiate portfolios and support premium pricing.

Page last updated on: