Food Amino Acids Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

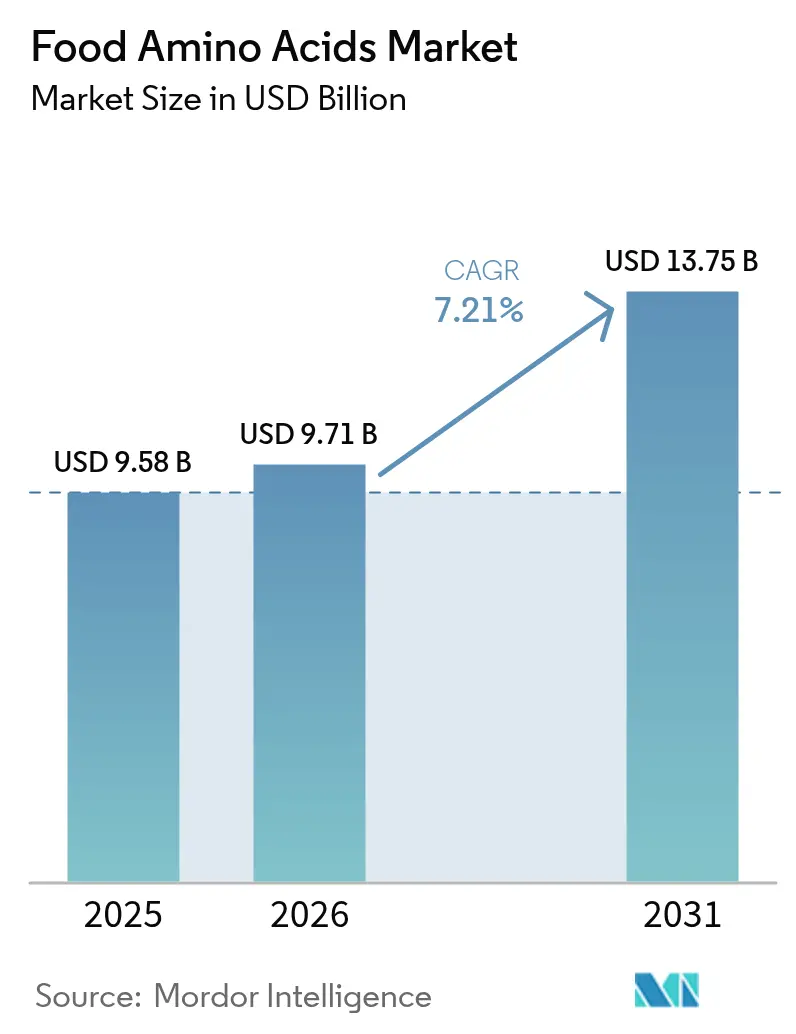

| Market Size (2026) | USD 9.71 Billion |

| Market Size (2031) | USD 13.75 Billion |

| Growth Rate (2026 - 2031) | 7.21% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Amino Acids Market Analysis by Mordor Intelligence

The Food Amino Acids market size is projected to grow from USD 9.58 billion in 2025 to USD 9.71 billion in 2026, reaching USD 13.75 billion by 2031, with a CAGR of 7.21% during the forecast period of 2026-2031. Key factors driving this growth include increasing fortification regulations for infant formula, expanding applications of amino acids in sports nutrition products, and a shift from animal-based protein to plant-based protein blends. The development of precision fermentation technology is enabling manufacturers to mitigate feedstock price fluctuations while reducing greenhouse gas emissions. Asia-Pacific holds the largest market share, primarily due to China's established lysine and methionine production clusters. Meanwhile, South America is emerging as a significant player, leveraging its abundant sugarcane and soy resources to attract foreign direct investment. Additionally, global consumers are increasingly demanding non-GMO, kosher, and halal certifications, prompting reformulations and the establishment of long-term offtake agreements with suppliers that can ensure traceability and regulatory compliance.

Key Report Takeaways

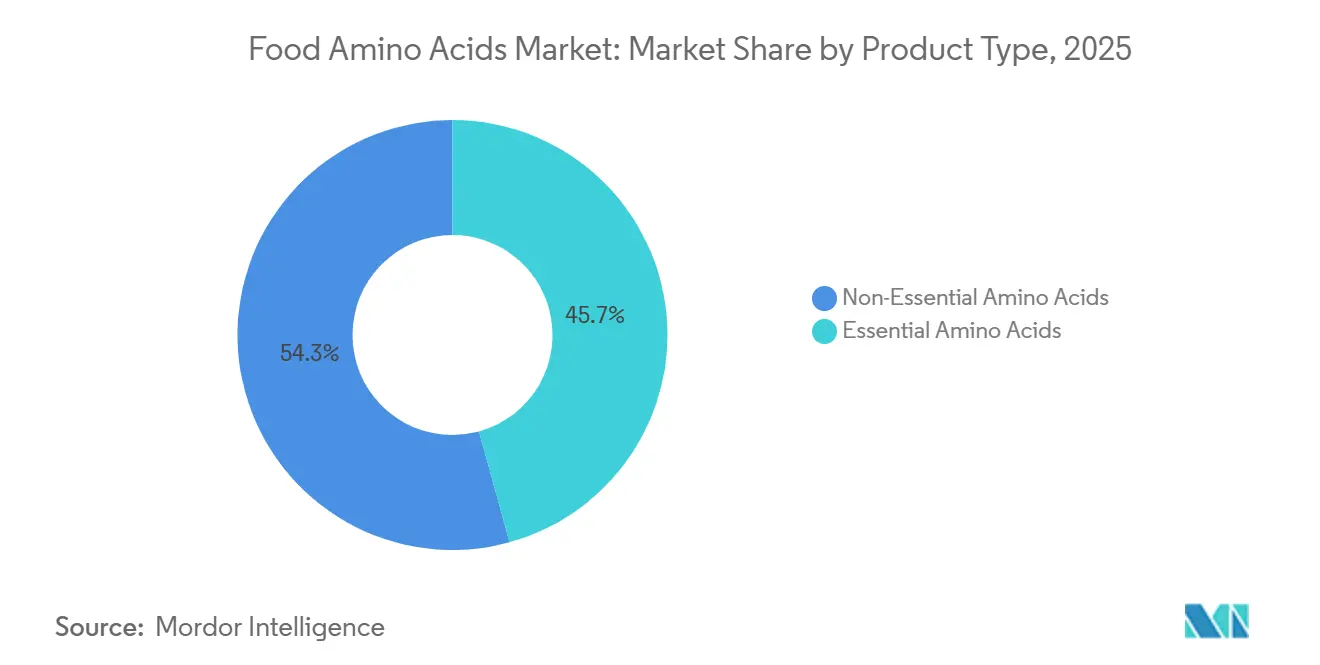

- By product type, non-essential amino acids held 54.27% of the 2025 food amino acids market share, while essential amino acids are forecast to post the fastest 8.88% CAGR through 2031.

- By source, plant-based fermentation accounted for 41.48% of 2025 supply; precision fermentation is projected to expand at a 9.36% CAGR to 2031, the highest among all sources.

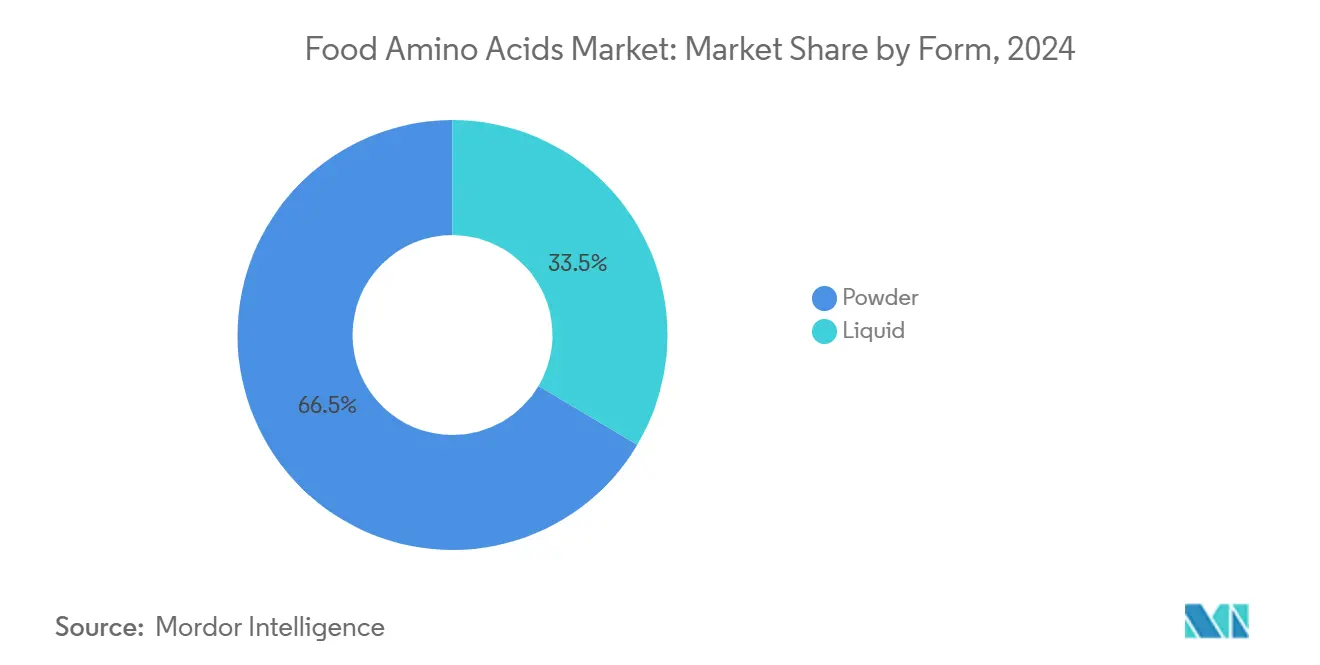

- By form, powders dominated with 66.47% share in 2025, whereas liquid concentrates are set to grow the quickest at 7.58% CAGR over 2026-2031.

- By application, dietary supplements commanded 40.18% of 2025 revenue, yet infant nutrition carries the top 7.45% CAGR through 203.

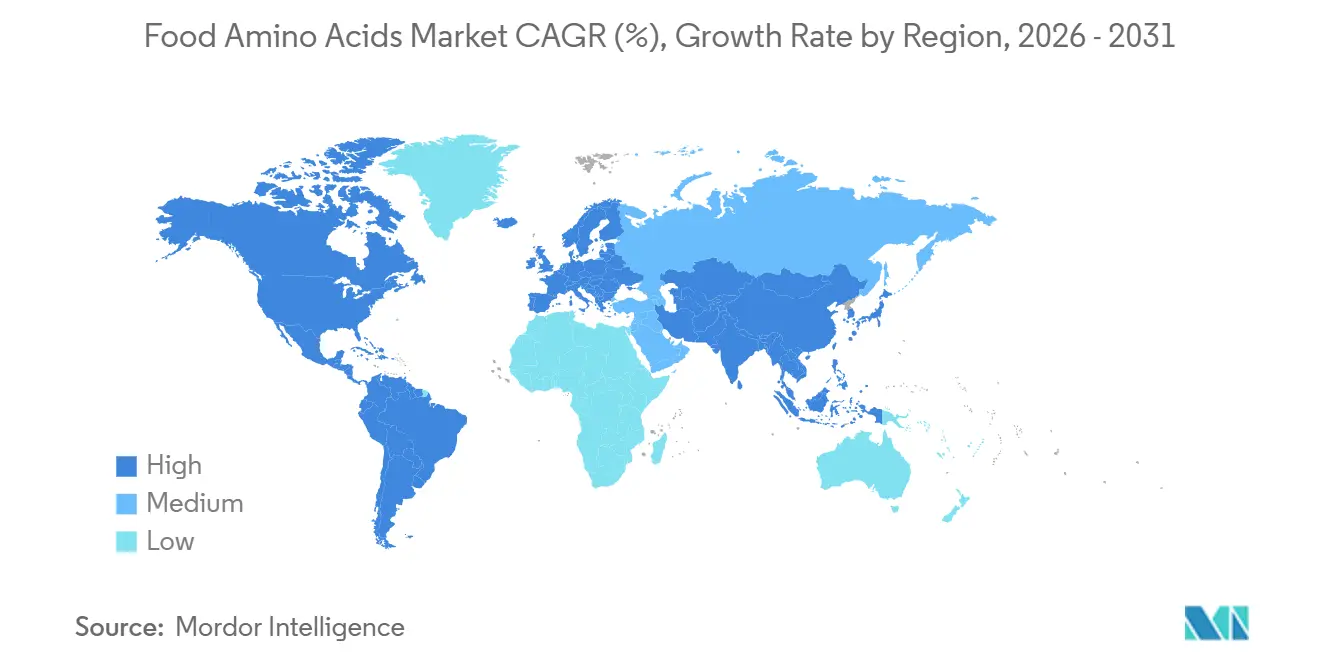

- By geography, Asia-Pacific led with 32.18% share in 2025; South America stands out with the strongest 8.15% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Food Amino Acids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for high-protein functional foods | +1.8% | Global, with strongest uptake in North America and Europe | Medium term (2-4 years) |

| Rising use in sports nutrition and dietary supplements | +1.5% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Growth of plant-based diets drives amino acid use for complete protein profiles | +1.2% | Global, led by North America and Western Europe | Medium term (2-4 years) |

| Increasing use of amino acids as food additives for flavor enhancement | +0.9% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Infant-formula fortification mandates | +1.1% | Global, with regulatory influence from FDA, EFSA, and China's SAMR | Short term (≤ 2 years) |

| Advancements in microbial fermentation and enzymatic production technologies | +1.4% | Global, concentrated in Asia-Pacific and North America production hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for high-protein functional foods

The increasing consumer emphasis on health, wellness, and nutrition is a key driver of the food amino acids market. Growing awareness of the advantages of high-protein diets, such as muscle maintenance, weight management, and overall well-being, has prompted food manufacturers to enhance products with amino acids to address the evolving nutritional preferences of health-conscious consumers. According to a 2025 International Food Information Council study, 70% of Americans aim to increase their protein intake, reflecting a nearly 20% rise over three years. Additionally, Cargill’s 2025 Protein Profile research revealed that 57% of consumers who read nutrition labels specifically seek information on protein content, underscoring the increasing significance of protein-rich foods and ingredients in daily diets [1]Source: International Food Information Council (IFIC), "Americans’ Perceptions of Protein", ific.org. This growing demand for protein is driving food and beverage manufacturers to integrate amino acids into a diverse range of products, including beverages, snacks, bakery items, and dairy alternatives. Amino acids enhance functional benefits, improve protein quality, and contribute to complete protein profiles, meeting consumer expectations for convenient and nutritionally optimized foods. As global trends toward health-conscious eating continue to expand, the demand for high-protein functional foods fortified with amino acids is anticipated to grow further, supporting the sustained expansion of the food amino acids market.

Rising use in sports nutrition and dietary supplements

The increasing emphasis on fitness, athletic performance, and overall wellness is driving significant demand for amino acids in sports nutrition and dietary supplements. Amino acids play a critical role as functional ingredients, aiding muscle recovery, endurance, and performance. They are widely used in protein powders, energy bars, ready-to-drink beverages, and specialized supplements designed for active adults. Between November 2023 and November 2024, 63.7% of adults in England adhered to the Chief Medical Officers’ guidelines of engaging in 150 minutes or more of moderate-intensity physical activity per week, representing approximately 30 million individuals [2]Source: Sport England Organization, "Record numbers playing sport and taking part in physical activity", sportengland.org. This high level of physical activity highlights a substantial, health-conscious population seeking nutritional products to optimize fitness outcomes, thereby driving the adoption of amino acid-enriched products. As consumers increasingly focus on functional nutrition to complement regular exercise, food manufacturers and supplement brands are incorporating amino acids into diverse product formats to meet this rising demand. This trend is anticipated to persist, establishing amino acids as a fundamental ingredient in the growing sports nutrition and dietary supplement market.

Growth of plant-based diets drives amino acid use for complete protein profiles

The increasing adoption of plant-based diets is a significant driver in the global food amino acids market. Manufacturers are utilizing amino acids to provide complete protein profiles in vegan and vegetarian products. Since plant-based proteins often lack certain essential amino acids, fortification with specific amino acids ensures these products achieve nutritional equivalence to animal-derived proteins. This approach is essential for product developers aiming to meet consumer expectations regarding health, functionality, and taste in plant-based alternatives. This trend is particularly evident in regions with growing plant-focused populations. For example, in the UK, the vegan population has reached 2.5 million, accounting for 4.7% of adults following a plant-based diet. This marks a notable increase of 1.1 million individuals between 2023 and 2024, highlighting the rapid shift toward plant-based lifestyles [3]Source: Vegconomist, "UK Vegan Population Estimated to Have Risen by 1.1 Million in Year", vegconomist.com. Such demographic growth directly drives demand for amino acids to improve protein quality in plant-based foods, including meat substitutes, dairy alternatives, and nutritional beverages.

Increasing use of amino acids as food additives for flavor enhancement

The increasing use of amino acids as food additives is a key factor driving the growth of the food amino acids market, particularly for improving taste and flavor profiles. Amino acids such as glutamate, glycine, and arginine are commonly used to enhance umami, sweetness, and overall flavor perception in various food products, including snacks, seasonings, sauces, and processed foods. These amino acids interact with taste receptors to amplify specific flavor notes, making them essential components in the formulation of savory and sweet products. With growing consumer demand for flavorful, clean-label, and naturally tasting products, food manufacturers are incorporating amino acids to achieve desired taste profiles without relying on artificial additives or high salt content. This approach not only facilitates product differentiation but also aligns with consumer preferences for healthier and more enjoyable eating experiences. Additionally, the use of amino acids supports the development of low-sodium and reduced-sugar products, catering to health-conscious consumers. As a result, the targeted use of amino acids for flavor enhancement continues to drive innovation and adoption within the food industry, enabling manufacturers to meet evolving consumer expectations while maintaining product quality and appeal.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile prices of key feedstocks | -0.8% | Global, with acute pressure in North America and South America | Short term (≤ 2 years) |

| Stringent purity and allergen regulations | -0.5% | Europe, North America, with emerging influence in Asia-Pacific | Medium term (2-4 years) |

| Supply-demand imbalance in specialty essential amino acids | -0.6% | Global, concentrated in tryptophan and threonine markets | Medium term (2-4 years) |

| Fermentation-plant environmental and odor compliance risk | -0.4% | Asia-Pacific core, with regulatory tightening in China and Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile prices of key feedstocks

The fluctuating prices of key feedstocks present a significant challenge to the market. Variations in the costs of raw materials, including soybeans, corn, and other agricultural products, directly affect the production costs of amino acids. These price fluctuations are influenced by factors such as unpredictable weather conditions, geopolitical tensions, and changes in trade policies. Such volatility in feedstock prices poses difficulties for manufacturers in maintaining stable profit margins and pricing strategies, thereby restraining market growth. Furthermore, the increasing demand for these feedstocks in other industries, such as biofuels and animal feed, heightens competition and exacerbates price instability. This competition often results in supply shortages, compelling manufacturers to pay higher prices, which can disrupt production schedules and elevate operational costs. The lack of price stability also complicates long-term planning and investment decisions for companies in the food amino acids market.

Stringent purity and allergen regulations

Regulatory complexity contributes to higher compliance costs and creates barriers to market entry, particularly for smaller manufacturers that lack robust quality assurance systems. The European Food Safety Authority (EFSA) has updated its guidance for novel food applications, mandating detailed documentation such as whole genome sequencing and antibiotic resistance assessments for production strains. These requirements have significantly increased both application costs and timelines. Similarly, the U.S. Food and Drug Administration (FDA) has enhanced oversight of dietary supplements, introducing mandatory adverse event reporting and updated manufacturing practices, which impose ongoing compliance obligations that disproportionately affect smaller manufacturers. Additionally, cross-border regulatory harmonization remains incomplete, compelling manufacturers to navigate multiple approval processes to access global markets. While the establishment of tolerable upper intake levels for amino acids provides regulatory clarity, it also introduces liability risks for manufacturers whose products exceed these safety thresholds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Essential Amino Acids Accelerate on Infant and Sports Demand

Non-essential amino acids accounted for 54.27% of the market share in 2025, while the essential amino acids are projected to grow at a compound annual growth rate (CAGR) of 8.88% during the period 2026-2031. This growth is driven by infant formula manufacturers adapting to updated Codex Alimentarius guidelines, which increased the minimum tryptophan concentration from 17 milligrams per 100 kilocalories to 22 milligrams per 100 kilocalories for formulas designed for preterm infants. Additionally, phenylalanine plays a key role in aspartame synthesis, while threonine is increasingly used in clinical nutrition formulas for patients with inflammatory bowel disease. Controlled trials have demonstrated that threonine supplementation can enhance intestinal barrier function by 35%.

Non-essential amino acids, particularly glutamic acid and aspartic acid, continue to dominate savory flavor applications and are integral to the Asian condiment industry. Glutamic acid's market share in 2025 highlights its widespread use in products such as soy sauce, oyster sauce, and instant noodle seasoning packets, where it provides umami flavor at one-tenth the cost of yeast extracts. Regulatory frameworks, including FDA 21 CFR Part 172 and the European Food Safety Authority's (EFSA) food additive database, allow unrestricted use of glutamic acid and aspartic acid in most food categories. This regulatory stability ensures a consistent demand base, even as essential amino acids experience incremental growth.

By Source: Precision Fermentation Disrupts Cost Curves

Plant-based fermentation, which accounted for 41.48% of the 2025 supply, relies on corn-glucose or cane-sugar feedstocks and remains the primary production method for lysine, threonine, and glutamic acid. This dominance is attributed to established economies of scale and regulatory approvals spanning over three decades. The process utilizes plant-based raw materials, such as corn, sugarcane, or other carbohydrate-rich sources, to produce amino acids through microbial processes. It is favored for its cost efficiency, scalability, and compatibility with existing production facilities, making it a preferred approach for large-scale amino acid manufacturing. Furthermore, plant-based fermentation aligns with growing consumer demand for natural and sustainable production methods, further supporting its adoption in the market.

In contrast, precision fermentation, supported by declining DNA synthesis costs and advancements in AI-driven strain engineering, is the fastest-growing segment in the market, with a CAGR of 9.36%. This method employs genetically engineered microorganisms to produce specific amino acids with high precision, purity, and efficiency. Precision fermentation is gaining momentum due to advancements in synthetic biology, which facilitate the development of optimized microbial strains tailored for amino acid production. Additionally, it offers the flexibility to produce rare or specialty amino acids that are difficult to obtain through traditional methods.

By Form: Liquid Formulations Gain Functional Advantage

Powder formats accounted for 66.47% of the total volume in 2025, while liquid amino acid concentrates are projected to grow at a CAGR of 7.58% during the period 2026-2031. This shift is driven by functional beverage brands prioritizing solubility, bioavailability, and manufacturing efficiency in ready-to-drink protein shakes and electrolyte solutions. Powder formats remain dominant in dietary supplements, bakery premixes, and infant formula blending due to their lower shipping costs, liquid concentrates weigh three to five times more per unit of active ingredient, and better shelf stability under ambient conditions.

However, liquid formats offer advantages such as eliminating the need for dissolution equipment and reducing clumping risks in high-humidity environments. These benefits make liquid concentrates appealing to co-packers producing single-serve beverage shots and clinical nutrition manufacturers developing enteral feeds that require precise amino acid ratios. The transition toward liquid concentrates is particularly notable in North America and Europe, where rapid beverage innovation cycles and co-packer requirements for reduced changeover times and simplified cleaning validation drive demand.

By Application: Infant Nutrition Leads Growth Amid Regulatory Upgrades

Dietary supplements accounted for 40.18% of applications in 2025, making them the largest end-use segment. This category is dominated by branched-chain amino acid powders, leucine capsules, and multi-amino-acid blends, which are marketed for purposes such as muscle recovery, weight management, and cognitive support. While sports and performance nutrition overlaps with dietary supplements, it is differentiated by higher amino acid content per serving, typically ranging from 10 grams to 15 grams compared to 3 grams to 5 grams, and by its distribution through specialty fitness retailers and direct-to-consumer channels. These channels often emphasize clinical validation and third-party testing for banned substances.

Infant nutrition is projected to grow at a CAGR of 7.45% through 2031. This growth is driven by FDA and EFSA regulations mandating minimum concentrations of lysine, methionine, tryptophan, phenylalanine, and threonine in formulas for full-term and preterm infants. Compliance deadlines are set for 2026 for existing products, with immediate effect for new launches. Functional beverages represent a rapidly growing niche, with amino-acid-fortified energy drinks, protein waters, and recovery shots gaining increased shelf space in North American and European convenience stores. The "Others" category, which includes food-grade amino acid consumption, is also expanding. Growth in this segment is supported by improving regulatory clarity and rising demand for human-grade ingredients in pet food due to premiumization trends.

Geography Analysis

In 2025, Asia-Pacific holds a significant 32.18% market share, reflecting its integrated supply chain capabilities and strong governmental support for biotechnology. However, this dominance faces challenges, including trade tensions and increased regulatory scrutiny, which create uncertainty for Chinese suppliers that dominate global production capacity. Key growth drivers in the region include rising health consciousness, urbanization, and a growing middle class with a preference for premium nutrition. While India's nutraceutical market is expanding and Japan is recognized for its advanced fermentation technologies, China's large-scale manufacturing capacity integrates these elements, creating a comprehensive ecosystem for amino acid production and consumption.

South America is projected to grow at a compound annual growth rate (CAGR) of 8.15% during 2026-2031, the highest among all regions. Brazil and Argentina are capitalizing on abundant soy and sugarcane feedstocks to attract foreign direct investment in fermentation capacity. Additionally, domestic demand for fortified foods is increasing alongside middle-class growth. Brazil's strong fermentation infrastructure, supported by its agricultural resources, positions the country for expanded amino acid production. In Argentina, the growing nutraceutical market is driving demand for specialized amino acid formulations.

North America and Europe continue to play important roles in the food amino acids market. North America benefits from advanced research and development capabilities, a well-established nutraceutical industry, and growing consumer interest in functional foods. Europe also contributes significantly, leveraging its mature market infrastructure and focus on innovation in food and nutrition. The Middle East and Africa, while smaller in absolute market size, are experiencing double-digit growth. Gulf Cooperation Council (GCC) countries are investing in food security initiatives, while Nigeria and Egypt are expanding domestic infant formula production to reduce reliance on imports. These developments are driving growth in the region's food amino acids market.

Competitive Landscape

The food amino acids market is moderately consolidated, with key players including Ajinomoto Co., Inc., Evonik Industries AG, Meihua Holdings Group Co., Ltd., CJ CheilJedang Corporation, and Daesang Holdings Co., Ltd. This market structure allows both established multinational corporations and emerging biotechnology firms to secure market share by utilizing differentiated production technologies and specialized application expertise. For instance, Ajinomoto has maintained a strong market presence through advanced chemical synthesis methods, while newer entrants are leveraging innovative approaches such as precision fermentation to gain a competitive advantage. This dynamic environment encourages collaboration and innovation across the value chain.

Strategic partnerships are significantly influencing the competitive landscape of the food amino acids market. For example, the collaboration between Danone and Ajinomoto focuses on developing amino acid feed supplements aimed at reducing CO2 emissions in dairy farming. These partnerships not only address sustainability challenges but also strengthen the market positioning of the participating companies. Additionally, precision fermentation startups are increasingly collaborating with traditional food companies to scale production and navigate regulatory requirements, further intensifying competition within the market.

Technology adoption in the food amino acids market reveals a distinct bifurcation. On one side, companies are investing heavily in precision fermentation technologies to produce amino acids more sustainably and efficiently. On the other side, firms optimizing traditional chemical synthesis methods continue to dominate segments where cost-effectiveness and established processes are critical. Regulatory approvals and cost structures remain pivotal factors influencing competitive positioning and strategic decisions. For instance, while precision fermentation technologies show significant promise, they often involve higher initial costs and face regulatory challenges, which can slow their adoption compared to traditional methods.

Food Amino Acids Industry Leaders

-

Ajinomoto Co., Inc.

-

Evonik Industries AG

-

Meihua Holdings Group Co., Ltd.

-

CJ CheilJedang Corporation

-

Daesang Holdings Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Daesang has announced its strategic entry into the pharmaceutical-grade amino acids market through the acquisition of AMINO GmbH, a German company specializing in high-purity amino acid production. The transaction, valued at approximately KRW 50.2 billion, is expected to be finalized by March 2026. This acquisition provides Daesang with access to AMINO’s advanced purification technologies, established manufacturing infrastructure, and regulatory networks within Europe. AMINO’s products are utilized in critical applications, including medical IV solutions, clinical nutrition, and biopharmaceuticals.

- September 2025: Yichang Sanxia Proudin Biopharmaceutical Co., Ltd. has introduced three new amino acid complex salts including, L-lysine-L-glutamate, L-lysine-L-aspartate, and L-arginine-L-aspartate. These products are now being supplied to international customers. The complex salts, formed through ionic bonding between two amino acid molecules, offer benefits over traditional supplements, such as reduced odor and enhanced utilization of the constituent amino acids. They are primarily designed for use as nutritional fortifiers and food additives, with additional functionality in improving food stability by minimizing stratification and precipitation.

- October 2024: Evonik has announced plans to restructure its Health Care business, focusing on key growth areas. As part of this strategy, the company is considering strategic options, including potential partnerships or divestments, for its keto and pharmaceutical amino acid production facilities in Ham and Wuming.

Global Food Amino Acids Market Report Scope

Amino acids together constitute the molecules that form protein. Food amino acids are ingredients that are used in the preparation of different protein-rich products across different industries. The global food amino acids market is segmented by type, application, and geography. Based on type, the market is segmented into glutamic acid, lysine, tryptophan, methionine, phenylalanine, and other types. Based on application, the market is further segmented into dietary supplements, fortified food and beverage, and infant nutrition. Moreover, the study provides an analysis of the food amino acids market in emerging and established markets across the globe, including in North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| Essential Amino Acids | Lysine |

| Methionine | |

| Tryptophan | |

| Phenylalanine | |

| Threonine | |

| Others | |

| Non-Essential Amino Acids | Glutamic Acid |

| Aspartic Acid | |

| Proline | |

| Others |

| Plant-based Fermentation |

| Synthetic Chemical Synthesis |

| Precision Fermentation |

| Powder |

| Liquid |

| Dietary Supplements |

| Sports and Performance Nutrition |

| Functional Beverages |

| Bakery and Confectionery |

| Infant Nutrition |

| Medical and Clinical Nutrition |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Singapore | |

| Thailand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Essential Amino Acids | Lysine |

| Methionine | ||

| Tryptophan | ||

| Phenylalanine | ||

| Threonine | ||

| Others | ||

| Non-Essential Amino Acids | Glutamic Acid | |

| Aspartic Acid | ||

| Proline | ||

| Others | ||

| By Source | Plant-based Fermentation | |

| Synthetic Chemical Synthesis | ||

| Precision Fermentation | ||

| By Form | Powder | |

| Liquid | ||

| By Application | Dietary Supplements | |

| Sports and Performance Nutrition | ||

| Functional Beverages | ||

| Bakery and Confectionery | ||

| Infant Nutrition | ||

| Medical and Clinical Nutrition | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Singapore | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big will the Food Amino Acids market be by 2031?

The Food Amino Acids market size is projected to reach USD 13.75 billion by 2031, reflecting a 7.21% CAGR from 2026 to 2031.

Which amino-acid type is growing fastest in food use?

Essential amino acids post the highest 8.88% CAGR, fueled by infant-formula updates and sports-nutrition reformulations.

Why is precision fermentation important for amino-acid supply?

It delivers higher yields, cuts carbon intensity by roughly 40%, and reduces exposure to corn-glucose price swings, making future supply more resilient.

Which region shows the strongest growth momentum?

South America leads with an 8.15% CAGR because investors exploit abundant soy and sugarcane feedstocks to build new capacity.

What is the market concentration level among key players?

The market is moderately fragmented with a concentration score of 4/10, allowing both multinationals and startups to compete effectively.

Page last updated on: