Market Overview

| Study Period | 2021 - 2031 |

|---|---|

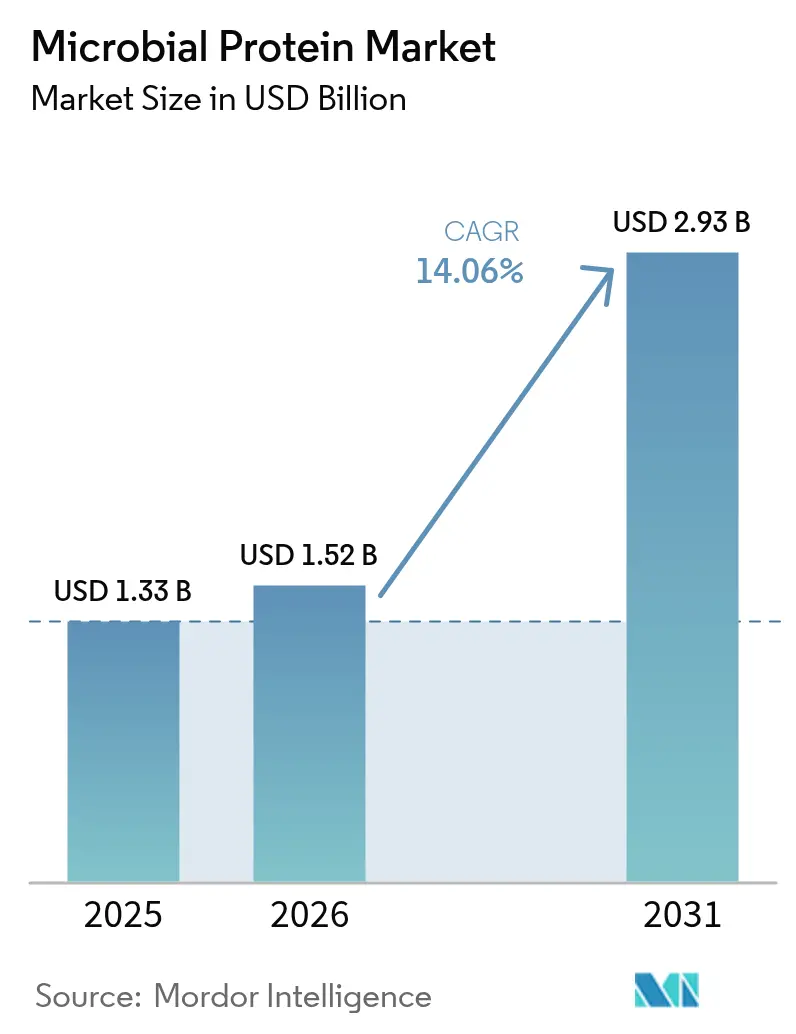

| Market Size (2026) | USD 1.52 Billion |

| Market Size (2031) | USD 2.93 Billion |

| Growth Rate (2026 - 2031) | 14.06% CAGR |

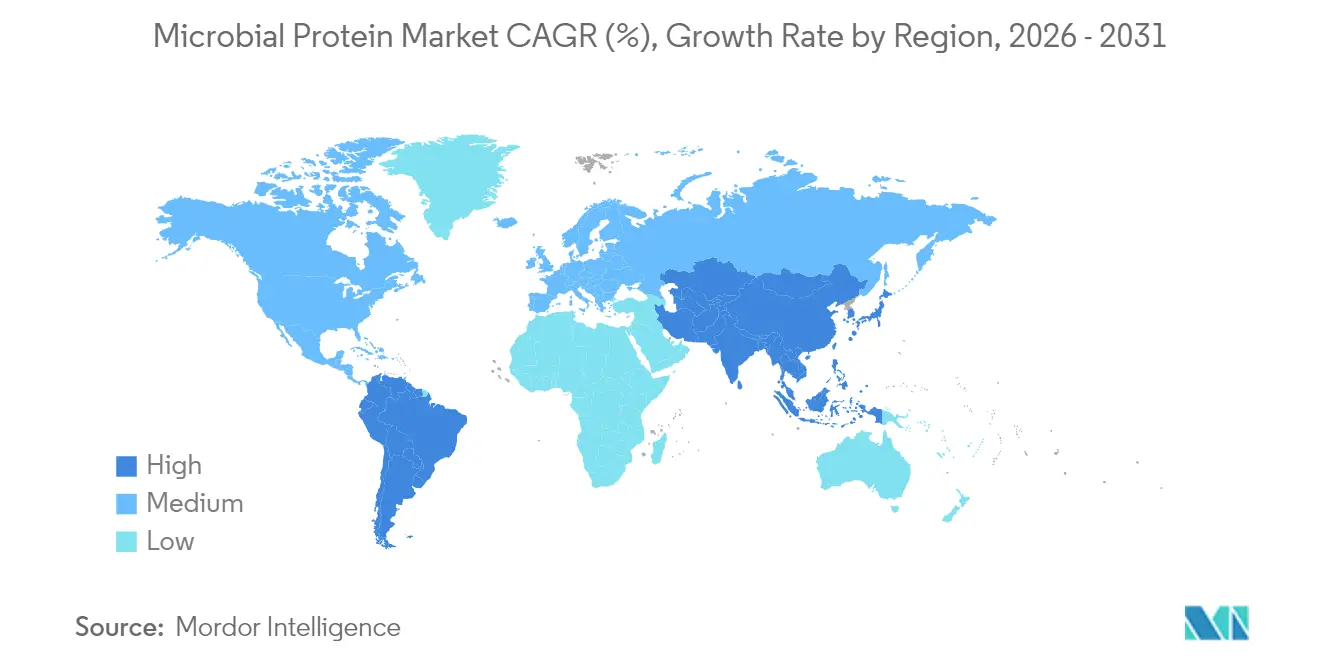

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Microbial Protein Market Analysis by Mordor Intelligence

The microbial protein market size in 2026 is estimated at USD 1.52 billion, growing from 2025 value of USD 1.33 billion with 2031 projections showing USD 2.93 billion, growing at 14.06% CAGR over 2026-2031. Rapid advances in precision fermentation, expanding regulatory acceptance, and corporate decarbonization targets are driving demand for low-impact protein ingredients. Europe's sustainability policies, Asia-Pacific's manufacturing investments, and North America's streamlined GRAS pathway create a diversified growth landscape for the microbial protein market. The FDA's GRAS status approvals for novel microbial proteins and EFSA's updated guidance for novel food applications enhance market penetration across key regions[1]European Food Safety Authority, "Navigating Novel Foods", www.efsa.europa.eu. While mycoprotein dominates current production volumes due to established infrastructure, bacterial protein technologies attract venture funding by offering reduced production costs and increased yields. The market continues to expand beyond meat alternatives and beverages into aquafeed, pet nutrition, and functional foods, establishing sustained growth potential.

Key Report Takeaways

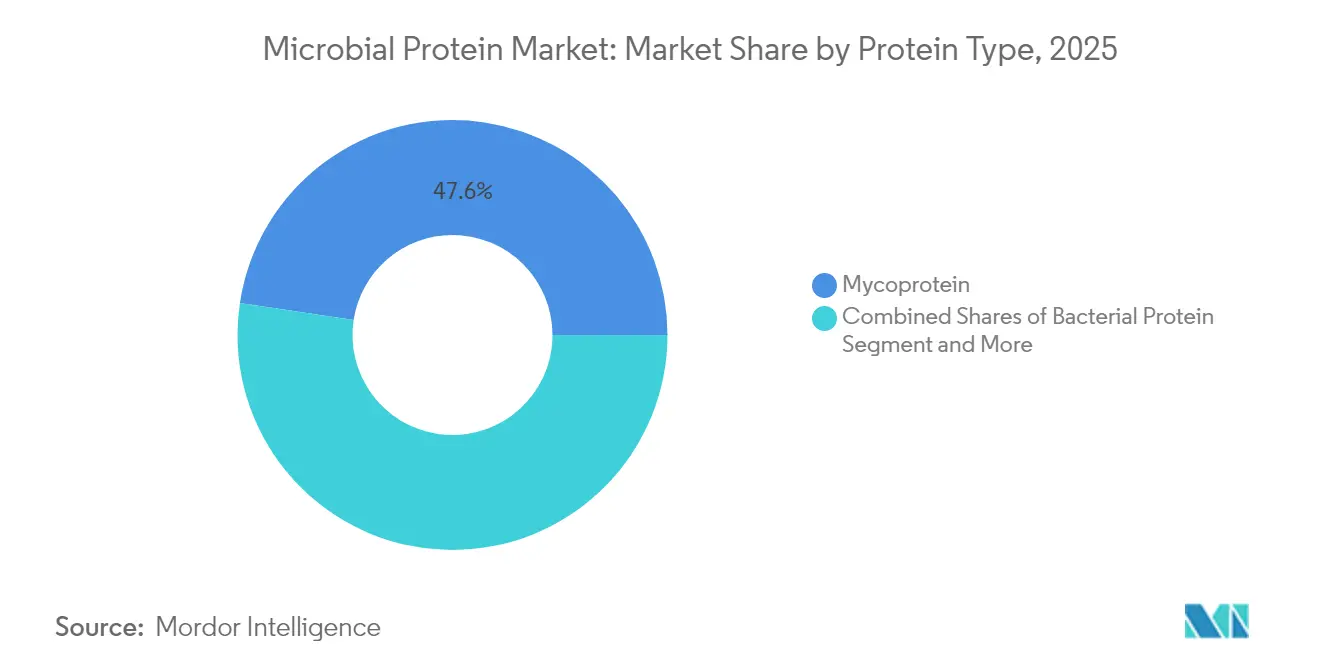

- By protein type, mycoprotein led with 47.62% revenue share in 2025; bacterial protein is forecast to scale at a 16.54% CAGR between 2026-2031.

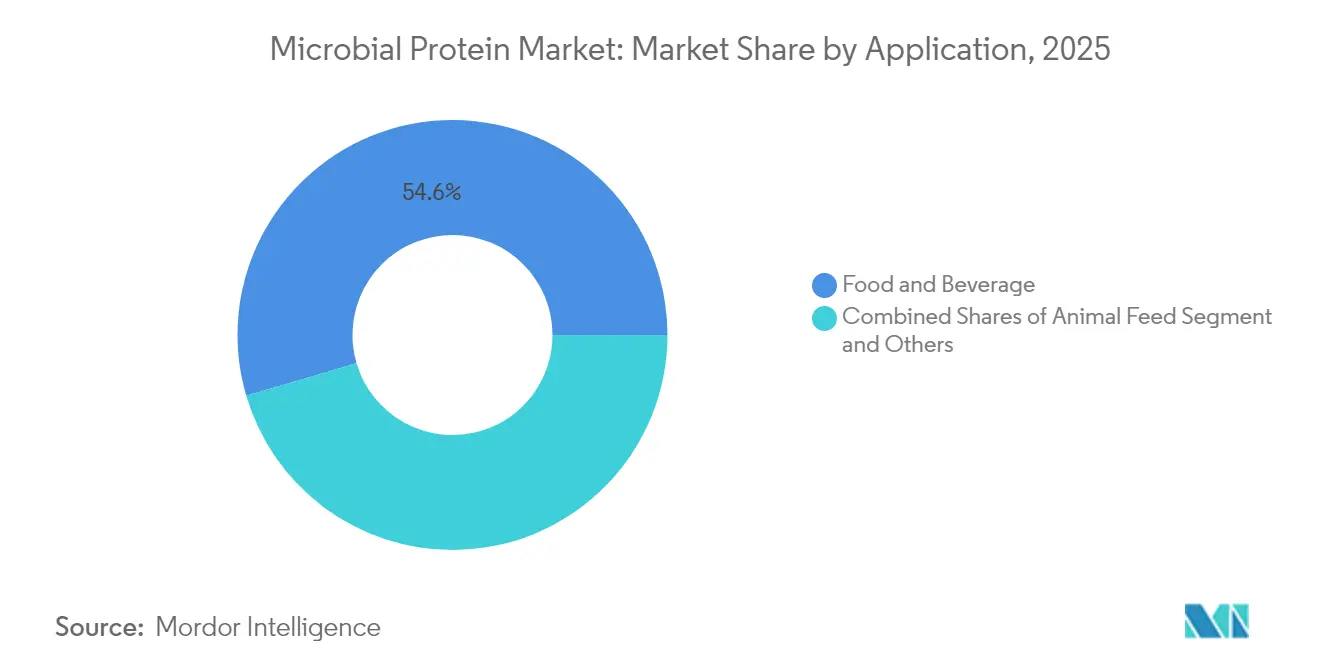

- By application, food and beverages held a 54.55% share of the microbial protein market size in 2025, whereas animal feed is advancing at a 19.02% CAGR to 2031.

- By geography, Europe captured 33.05% of the microbial protein market share in 2025, while Asia-Pacific is projected to register the fastest 18.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Microbial Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Sustainable Protein Sources | +3.2% | Global, with strongest impact in Europe & North America | Long term (≥ 4 years) |

| Technological Advancements in Fermentation and Bioprocessing | +2.8% | Global, concentrated in Netherlands, Finland, Germany | Medium term (2-4 years) |

| Increased Adoption in Pet and Aquafeed Sectors | +2.1% | Asia-Pacific core, spill-over to Europe & North America | Medium term (2-4 years) |

| Regulatory Support for Novel Food Ingredients | +1.9% | Europe & North America, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Expanding Applications in Functional Food and Beverages | +1.7% | North America & Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| High Protein Content and Rapid Biomass Generation | +1.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Sustainable Protein Sources

Consumer awareness of environmental impacts from conventional agriculture is driving unprecedented demand for microbial proteins as climate-conscious alternatives. This shift is particularly pronounced in Europe, where regulatory frameworks increasingly favor low-carbon protein sources, and among younger demographics who prioritize sustainability credentials. The protein transition is further accelerated by corporate sustainability commitments, with major food manufacturers seeking to reduce scope 3 emissions through alternative protein sourcing. The convergence of consumer demand, regulatory pressure, and corporate sustainability targets creates a self-reinforcing cycle that sustains long-term market growth beyond typical technology adoption curves. Market research indicates that microbial proteins require significantly less land and water compared to traditional animal proteins, making them an attractive option for sustainable food production. Additionally, technological advancements in fermentation processes have improved the scalability and cost-effectiveness of microbial protein production, further supporting market expansion.

Technological Advancements in Fermentation and Bioprocessing

Innovations in fermentation technology are reducing production costs and improving protein yields, making microbial proteins more cost-competitive with conventional alternatives. Recent advances include proprietary seed train technologies that accelerate production timelines and optimize fermentation parameters for enhanced biomass generation. The integration of artificial intelligence and machine learning in bioprocess optimization enables real-time adjustments that maximize protein content while minimizing resource consumption. The development of continuous cultivation methods and novel bioreactor designs enables industrial-scale production with lower capital expenditure requirements. These technological advancements have resulted in improved product quality and consistency, meeting stringent regulatory requirements for food-grade proteins. Additionally, the scalability of these processes has attracted significant investment from major food manufacturers, further accelerating market growth.

Increased Adoption in Pet and Aquafeed Sectors

The animal feed industry is driving significant growth in the microbial proteins market, particularly in aquaculture where sustainability concerns regarding fish meal sourcing are prominent. According to Nanyang Technological University, Singapore, microbial proteins can substitute up to 50% of fishmeal in aquaculture feed without affecting growth performance, addressing both economic and environmental challenges. The pet food segment is expanding through strategic collaborations, as evidenced by MicroHarvest and VEGDOG's introduction of microbial protein dog treats, which show higher palatability than conventional poultry-based products. The market benefits from simplified regulatory frameworks compared to human food applications, facilitating quicker market entry and concept validation. Market research indicates strong consumer acceptance, with 78.4% of dog owners in the UK and Germany expressing willingness to purchase microbial protein-containing products, indicating favorable conditions for market expansion.

Regulatory Support for Novel Food Ingredients

Regulatory frameworks are evolving to accommodate microbial proteins through streamlined approval processes and updated safety assessment guidelines. The FDA's updated GRAS pathway and EFSA's revised novel food guidance effective February 2025 are reducing approval timelines and providing clearer regulatory pathways for microbial protein applications. Recent approvals include String Bio's GRAS status for novel microbial protein and Calysta's MARA approval for aquaculture feeds, demonstrating regulatory acceptance across multiple jurisdictions. The European Commission's [2]European Commission, "Authorization of five novel foods", www.cirs-group.comauthorization of five novel foods in April 2024, including protein concentrates from Lemna species, signals expanding regulatory recognition of alternative protein sources. Government funding initiatives, including the Dutch National Growth Fund's EUR 60 million allocation for cellular agriculture and Business Finland's grants for fermentation technology, provide additional regulatory and financial support. This regulatory momentum creates predictable pathways for market entry and reduces investment risks for companies developing microbial protein technologies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Taste and sensory challenges in food formulations | -2.30% | Global, particularly acute in North America & Europe | Medium term (2-4 years) |

| Competition from Other Alternative Proteins | -2.00% | North America & Europe core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| High R&D and production setup costs | -1.80% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Limited consumer awareness and acceptance | -1.50% | Asia-Pacific & MEA core, moderate impact in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Taste and Sensory Challenges in Food Formulations

Consumer acceptance of microbial protein products faces constraints due to sensory limitations in taste, texture, and visual appeal. Microalgae incorporation in food products encounters challenges related to color and taste, with consumer studies indicating preferences for minimal inclusion levels to reduce sensory impact. These challenges are significant in direct consumption applications, where microbial proteins must match established taste profiles and meet consumer expectations. Companies are investing in flavor masking technologies and product formulation improvements, with some achieving success through enzymatic treatments and processing innovations to enhance palatability. This constraint has led to innovation in blended products, as demonstrated by Quorn's shift toward meat-mycoprotein blends that combine familiar tastes while gradually introducing alternative proteins. While industry partnerships with flavor houses and food technologists are developing solutions, addressing these challenges requires ongoing R&D investment and consumer education efforts.

High R&D and Production Setup Costs

Capital intensity requirements for microbial protein production facilities present significant barriers to market entry and scaling, particularly for smaller companies and emerging market participants. McKinsey estimates that over USD 250 billion in investment will be required by 2050 to achieve economies of scale in fermentation-based protein production. However, technological advances are driving cost reductions, with companies like MicroHarvest demonstrating scalable production models that achieve 10 tons daily output through optimized fermentation processes. Strategic partnerships and contract manufacturing arrangements are emerging as viable alternatives to full facility ownership, enabling companies to access production capacity without prohibitive capital investments. Government funding initiatives and sovereign wealth fund participation are providing alternative financing sources, though the capital intensity constraint continues to shape industry consolidation patterns and competitive dynamics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Protein Type: Bacterial Protein Drives Innovation

Mycoprotein holds the dominant market share at 47.62% in 2025, built on decades of commercial development by companies like Quorn Foods and established Fusarium venenatum cultivation methods. Bacterial protein is experiencing the highest growth rate with a 16.54% CAGR through 2031, supported by new production technologies that enable efficient scaling and high protein yields. Solar Foods demonstrates this potential with their Solein product, which produces protein from CO2 and hydrogen while using minimal land and water resources compared to conventional agriculture, as reported by European Biotechnology. Algae protein, including spirulina and chlorella variants, maintains steady growth through existing regulatory approvals and increased use in functional foods. Yeast protein advances through Saccharomyces cerevisiae engineering improvements that boost protein content and functionality.

The market segments show distinct development stages, with mycoprotein benefiting from existing production infrastructure while bacterial protein attracts venture capital for new production facilities. Cargill's investment in ENOUGH's mycoprotein production aims to produce over 1 million tons of ABUNDA mycoprotein by 2033 using zero-waste fermentation methods. Bacterial protein continues to grow through precision fermentation technology that produces animal-identical proteins without agricultural inputs. This segment is positioned for increased adoption as production costs decrease, and regulatory approvals expand globally.

By Application: Animal Feed Accelerates Adoption

Food and beverages represent the dominant application segment with a 54.55% market share in 2025, supported by increasing consumer demand for sustainable protein alternatives and favorable regulatory frameworks for novel food ingredients. The animal feed segment is experiencing rapid growth at a 19.02% CAGR through 2031, primarily due to increased adoption in aquaculture, where microbial proteins help address sustainability issues in fish meal production. The supplements segment capitalizes on high protein content and bioactive compounds for sports and medical nutrition, while industrial applications remain in early stages with potential for specialized protein ingredients.

The regulatory environment varies across application segments, with animal feed facing fewer approval requirements compared to human food applications. Industry collaborations strengthen the animal feed segment, as demonstrated by Nutreco's investment in BiomEdit for developing microbiome-based feed additives to improve animal health and productivity. In food and beverage applications, manufacturers continue to innovate through blended formulations, incorporating microbial proteins while maintaining familiar taste profiles to ensure consumer acceptance.

Geography Analysis

Europe holds 33.05% market share in 2025, supported by established fermentation infrastructure, favorable regulations, and government funding for alternative protein development. The region demonstrates significant commercial progress, with Solar Foods' Factory01 in Finland producing up to 160 tons of Solein annually and Cargill's partnership with ENOUGH targeting over 1 million tons of ABUNDA mycoprotein by 2033 according to Europan biotechnology. Germany has emerged as an innovation center, with MicroHarvest achieving 10 tons daily production capacity and Nosh.bio operating at thousands of tons annual capacity in Dresden. The updated EFSA novel food guidance, effective February 2025, simplifies approval processes and reduces market entry barriers. While the region's regulatory environment and consumer preferences support market growth, high production costs and regulatory complexity remain challenges for smaller companies.

Asia-Pacific exhibits the highest growth rate at 18.21% CAGR through 2031, supported by biomanufacturing investments, increasing protein demand, and food security initiatives. Singapore maintains its position as a regulatory gateway, with Solar Foods and Ajinomoto Group planning Solein distribution across Asia following regulatory approval. Regional research advances include Nanyang Technological University's development of single-cell proteins from food processing wastewater for aquaculture applications. Growth continues through increasing consumer awareness and government support for biotechnology innovation in food security.

North America maintains market growth through efficient GRAS regulatory pathways and venture capital support, despite smaller market share compared to Europe and Asia-Pacific. Recent FDA approvals include Superbrewed Food's postbiotic cultured protein and various microbial protein GRAS notifications. Industry developments include Fonterra's partnership with Superbrewed Food for postbiotic protein ingredients using lactose permeate, NovoNutrients' USD 18 million funding for CO2-to-aquafeed protein, and Liberation Labs' precision fermentation facility funding. South America and Middle East & Africa show growth potential, demonstrated by NEOM Investment Fund's support for Saudi Arabia's precision fermentation facility and Enifer's collaboration with Brazilian company FS for mycoprotein production using corn ethanol byproducts.

Note: Segment shares of all Individual segments will be available upon report purchase

Competitive Landscape

The microbial protein market shows moderate fragmentation with a concentration score of 4 out of 10. Some of the major players include Cargill, Incorporated., Corbion, DSM-Firmenich, among others. This creates opportunities for both established companies and new entrants to gain market share through technological innovation and strategic partnerships. Quorn Foods, a market leader, has expanded into blended meat-mycoprotein products to attract flexitarian consumers while maintaining its core mycoprotein production. The industry is experiencing strategic consolidation, as demonstrated by Cargill's investment in ENOUGH and their agreement to market ABUNDA mycoprotein, with production targets of over 1 million tons by 2033 using zero-waste fermentation.

Companies are competing primarily through technological advancement. MicroHarvest has achieved production scaling to 10 tons daily through its proprietary seed train technologies that reduce fermentation time. This advancement in production efficiency has enabled companies to meet growing market demand while maintaining product quality. The improved fermentation processes have also led to significant cost reductions in manufacturing operations.

New market entrants are developing innovative production methods to differentiate themselves. Solar Foods uses air-protein technology, while other companies utilize agricultural waste as feedstock to achieve cost and sustainability advantages. Regulatory compliance also shapes competition, as companies that obtain GRAS [3]Generally Recognized as Safe (GRAS), "novel food authorizations", https://www.knoell.com status and novel food authorizations gain advantages through faster market entry and lower regulatory risk.

Microbial Protein Industry Leaders

-

Cargill, Incorporated.

-

DSM-Firmenich

-

Sensient Technologies Corporation

-

Kerry Group plc.

-

Corbion N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Solar Foods announced investment plan for Europe's largest emission reduction moonshot project, significantly expanding their microbial protein production capabilities beyond the initial Factory01 facility in Finland.

- August 2024: Mycorena AB acquired by fellow mycoprotein producer Naplasol following Mycorena's bankruptcy filing due to insufficient financing for large-scale facility development, highlighting capital intensity challenges in the sector.

- April 2024: MicroHarvest and VEGDOG launched first microbial protein dog treat featuring hypoallergenic ingredients with 1.4kg CO2 equivalent per kilogram carbon footprint.

- March 2024: MicroHarvest became first biomass fermentation company to join Food Fermentation Europe, indicating industry recognition of microbial protein technologies.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the microbial protein market as the aggregate value of protein ingredients intentionally cultivated from microorganisms, yeasts, fungi, bacteria, or algae, using submerged or solid-state fermentation and sold for food, dietary supplement, and animal-feed applications. We leave out plant, insect, and cell-cultivated animal proteins, along with any biomass still at pilot scale.

Segmentation Overview

-

By Protein Type

-

Algae Protein

- Spirulina Protein

- Chlorella Protein

- Others

- Mycoprotein

- Bacterial Protein

- Yeast Protein

-

Algae Protein

-

By Application

-

Food and Beverages

- Meat/Poultry/Seafood and Meat Alternative Products

- Dairy and Dairy Alternatives

- Bakery

-

Supplements

- Sport/Performance Nutrition

- Elderly and Medical Nutrition

-

Animal Feed

- Aquafeed

- Poultry Feed

- Pet Food

- Industrial and Other Applications

-

Food and Beverages

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed fermentation technologists, food formulators, aquafeed nutritionists, and downstream brand managers across North America, Europe, and Asia-Pacific. Their insights helped us challenge desk-research yields, refine price-volume spreads, and validate utilization factors that a desk review alone rarely captures.

Desk Research

Mordor analysts began by mapping production capacities, trade flows, and regulatory filings from tier-1 agencies such as the FAO, USDA, EFSA, and China's MARA. We layered in shipment cues from Volza and tender logs from Tenders Info. Company 10-Ks, investor decks, and patent families gathered via Questel clarified cost curves and technology readiness. We also drew on peer-reviewed journals like Trends in Food Science & Technology, plus national algae and mycology associations for protein composition benchmarks. This list is illustrative; many additional open sources informed the baseline.

Market-Sizing & Forecasting

A top-down reconstruction of demand pools, built from human per-capita protein intake gaps, livestock compound-feed ratios, and regional adoption curves, sets the first estimate. Results are then stress-tested with selective bottom-up checks, sampled producer output multiplied by average selling price, before adjustments. Key drivers in our model include fermentation throughput per cubic meter, regulatory approvals issued, retail pricing of meat analogs, and venture funding inflows. Forecasts rely on multivariate regression that weights those variables and applies scenario analysis for feedstock pricing shocks; expert consensus steers final CAGR selection. Data gaps in supplier rolls were bridged by triangulating customs codes and peer conversion ratios.

Data Validation & Update Cycle

Outputs pass three rounds of variance checks and senior analyst review. Reports refresh annually, and interim updates trigger when large-scale capacity additions or material policy shifts occur.

Why Our Microbial Protein Baseline Commands Reliability

Published values often diverge because each firm chooses different scopes, baselines, and refresh cadences.

Key gap drivers include some publishers rolling microbial protein into broader 'alternative protein' pools, some assuming full-capacity commercialization from day one, and others limiting scope to animal feed. Mordor's disciplined segmentation and yearly refresh avoid those extremes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.33 billion (2025) | Mordor Intelligence | - |

| USD 5.24 billion (2024) | Global Consultancy A | Counts wider novel proteins and assumes rapid scale-up without discounting idle capacity |

| USD 4.10 billion (2023) | Research Firm B | Blends microbial with single-cell protein analogs and relies on revenue proxies with limited primary checks |

| USD 0.14 billion (2022) | Trade Journal C | Focuses only on animal-feed uses and omits food-grade demand |

Taken together, the comparison shows that Mordor Intelligence delivers a balanced, transparent baseline anchored to clear variables, repeatable steps, and live industry feedback, giving decision-makers a figure they can trust.

Key Questions Answered in the Report

What is driving the rapid growth of the microbial protein market?

Technological breakthroughs in precision fermentation, supportive regulations such as EFSA’s 2025 guidance, and corporate sustainability goals are propelling the microbial protein market at a 14.06% CAGR to 2031.

Which protein type is expanding fastest?

Bacterial protein is the quickest-growing segment, projected at a 16.54% CAGR thanks to low resource requirements and cost-competitive scaling.

Why is Asia-Pacific the growth engine for microbial protein?

Government biomanufacturing investments, rising protein demand, and facilities such as Malaysia’s upcoming microalgae biorefinery support an 18.21% CAGR for the region through 2031.

What are the key barriers to wider consumer adoption?

Sensory challenges around taste and color plus high capital costs for new plants currently restrain faster penetration, though ongoing R&D and new financing models are addressing these hurdles.

Which regulations most influence market entry?

The FDA’s GRAS process and EFSA’s novel food pathway, both recently updated, provide clear and faster approval routes that lower commercialization risk for new microbial protein products.

Page last updated on: