Fondant Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.29 Billion |

| Market Size (2031) | USD 4.13 Billion |

| Growth Rate (2026 - 2031) | 4.65% CAGR |

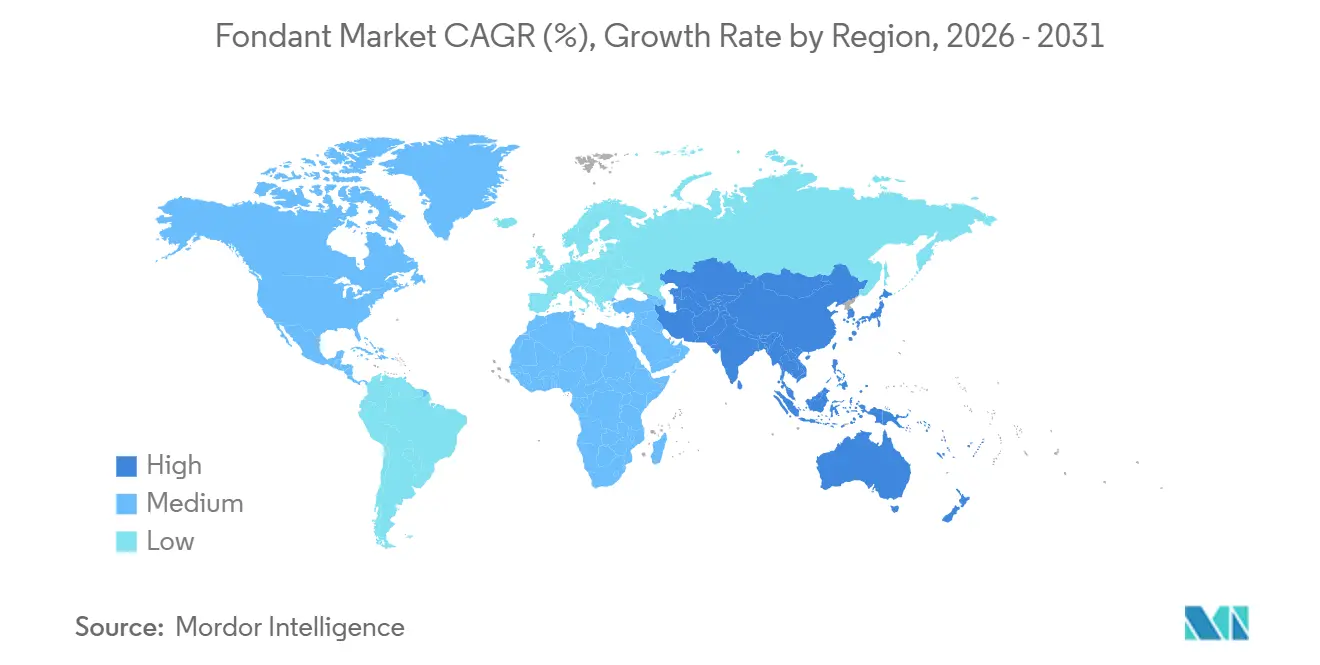

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fondant Market Analysis by Mordor Intelligence

The fondant market size is expected to increase from USD 3.15 billion in 2025 to USD 3.29 billion in 2026 and reach USD 4.13 billion by 2031, growing at a CAGR of 4.65% over 2026-2031. Premiumization, clean-label reformulation, and geographic diversification are emerging as key growth drivers for the global fondant market, replacing traditional volume expansion strategies. Rolled fondant formats remain prevalent in celebratory cakes across mature markets, while sculpting varieties are gaining traction due to the influence of social media aesthetics and the adoption of artisan techniques. The shift toward direct-to-consumer e-commerce channels is altering pricing dynamics, while demand in emerging markets is increasing as Western-style weddings and milestone celebrations become more culturally significant. Mergers such as the partnership between Puratos and Dawn Foods are consolidating research and development capabilities and global distribution networks, intensifying competitive pressure on mid-tier suppliers.

Key Report Takeaways

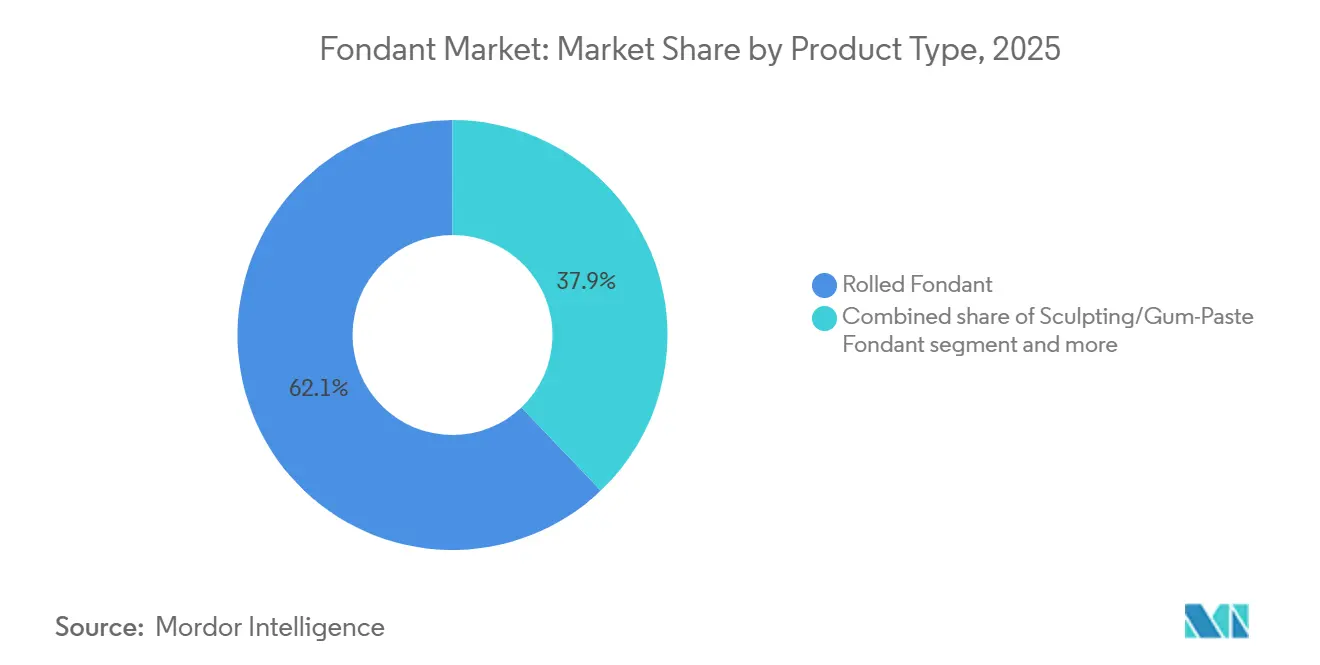

- By product type, rolled fondant led with 62.12% of fondant market share in 2025; sculpting and gum-paste fondant is projected to advance at a 5.65% CAGR through 2031.

- By form, ready-to-use packs captured 67.43% revenue in 2025, whereas powdered and instant mixes are forecast to grow at 5.81% annually through 2031.

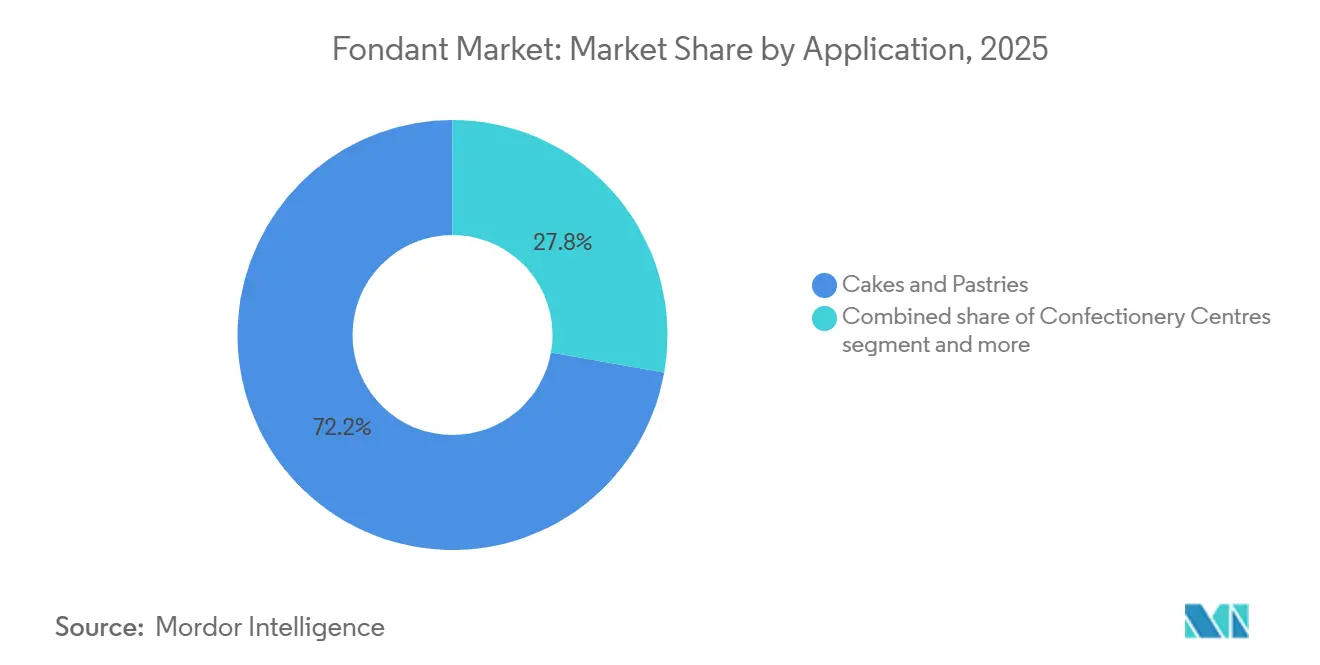

- By application, cakes and pastries absorbed 72.21% value in 2025; confectionery centers are set to expand at a 5.78% CAGR to 2031.

- By end-user, commercial bakeries and industrial producers held 54.28% of demand in 2025, but home bakers represent the fastest-growing cohort at 6.79% through 2031.

- By geography, Europe accounted for 36.24% of 2025 revenue, while Asia-Pacific is on track for a 5.92% CAGR between 2026-203

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fondant Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization in bakery and expansion of celebration culture | +1.2% | Global, with strongest impact in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Clean-label transition and natural color regulatory support | +0.9% | North America and Europe, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Commercial bakery capacity expansion and industrial scale-up | +0.8% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Home baking surge driven by social media and tutorial content | +1.1% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| E-commerce and direct-to-consumer retail channel growth | +0.7% | Global, early gains in North America and Western Europe | Medium term (2-4 years) |

| Wedding industry recovery and premium celebration-cake demand | +0.6% | Global, with emphasis on Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premiumization in bakery and expansion of celebration culture

As consumers in emerging markets increasingly embrace Western-style celebrations, fondant demand is witnessing a premiumization shift. These consumers are elevating tiered, decorated cakes from mere luxuries to essential centerpieces for weddings, birthdays, and corporate events. In a move underscoring this trend, General Mills, in February 2026, invested significantly in a second manufacturing facility in Nashik. This investment aims to bolster Pillsbury's baking-ingredient capacity in India, reflecting confidence in sustained double-digit growth for packaged bakery inputs, driven by rising disposable incomes and urbanization. Meanwhile, in China and Southeast Asia, there's a notable shift: urban millennials and Generation Z are moving away from traditional mooncakes and steamed desserts, gravitating instead towards multi-tier, fondant-covered celebration cakes. This shift not only mirrors a broader lifestyle alignment with Western norms but also highlights the status these elaborate cake decorations confer on social platforms. This demographic's willingness to splurge on custom designs, natural color palettes, and artisan finishes has birthed a bifurcated market. Here, mass-produced rolled fondant goes head-to-head with premium small-batch sculpting fondants, often priced significantly higher than their commodity-grade counterparts. The fondant trend isn't confined to retail alone. In the Middle East and Latin America, corporate gifting and event-catering sectors are increasingly opting for fondant-finished cakes, marking a shift in business-to-business procurement cycles. These cakes, once overshadowed by simpler buttercream or whipped-cream finishes, are now the go-to choice for product launches and executive gatherings.

Clean-label transition and natural color regulatory support

In the U.S., regulatory momentum is hastening the transition from petroleum-based synthetic colors to plant-derived alternatives. This shift is proving advantageous for fondant manufacturers who are now reformulating their products using natural pigments like beetroot red and spirulina extract. On February, 2026, the FDA, exercising its enforcement discretion, announced that products devoid of petroleum-based dyes could proudly claim "no artificial colors" on their labels [1]Source: U.S. Food & Drug Administration, “FDA Takes New Approach to "No Artificial Colors," Claims,” fda.gov. This holds true even if these products incorporate colors sourced from natural origins. This decision clarifies a long-standing labeling ambiguity, previously a deterrent for brands considering reformulation. The very next day, the FDA greenlit beetroot red as a new color additive. They also broadened the permitted applications for spirulina extract. With this, the current administration has now authorized a total of six new natural color options, offering fondant formulators credible alternatives to FD&C Red No. 3 and synthetic blues. This regulatory momentum is an extension of an April 2025 initiative by HHS and FDA, which advocated for a voluntary phase-out of petroleum-based synthetic colors. They even introduced a public tracker to monitor industry commitments, amplifying reputational pressure on those lagging behind. While the compliance costs are significant—natural colors typically necessitate higher dosages, show reduced stability under heat and pH variations, and require batch-certification protocols as per 21 CFR Parts 70 through 82—early adopters are reaping rewards. They're not only securing premium shelf space but also winning over health-conscious consumers in retail channels. The ramifications of these developments aren't confined to North America. Regulators in Europe and the Asia-Pacific are closely monitoring the FDA's moves. In response, multinational fondant suppliers are streamlining their formulations, aiming to prevent SKU proliferation and simplify their global supply chains.

Commercial bakery capacity expansion and industrial scale-up

As demand for decorated cakes surges in both foodservice and retail channels, large-scale bakery operators are ramping up investments in automation and capacity. This surge in demand is directly boosting fondant consumption, especially as ready-to-use formats help cut labor costs and enhance consistency. In a significant move, Puratos announced in March 2026 its intent to acquire Dawn Foods, a deal anticipated to finalize by year-end. This merger aims to blend Dawn's robust standardized manufacturing and distribution prowess in North America with Puratos' cutting-edge research and development ingredient technology and its expansive network spanning multiple countries. The union will bring together a substantial workforce and projected annual sales exceeding six billion United States dollars. Dawn's offerings, which include icings, glazes, and fillings closely tied to fondant, position the merged entity to fast-track product innovation, provide application-driven technical support, and deliver bundled ingredient solutions, potentially securing long-term contracts with bakeries. In a related development, British Bakels' move to integrate Renshaw, known for its annual production of significant volumes of fondant and marzipan at its British Retail Consortium-accredited facility in Liverpool, highlights the strategic advantages of vertical integration and in-house sugar milling, especially in navigating input-cost fluctuations.

Home baking surge driven by social media and tutorial content

Thanks to TikTok, Instagram, and YouTube, advanced cake-decorating techniques have become accessible to the masses. This shift has turned home bakers from occasional hobbyists into a lucrative customer base for fondant suppliers. Once exclusive to professional pastry chefs, skills like sculpted figurines, marbled finishes, and intricate floral work are now commonplace, thanks to tutorial videos. This newfound accessibility has led to a surge in purchases of specialty items like fondants, gum paste, and color gels. Satin Fine Foods, under the Satin Ice brand, boasts significant digital impressions monthly and a large television audience, underscoring the vast reach of content marketing in the home decorating realm. Annually, the company produces a substantial volume of icing and cake-decorating products from its expansive facility. With distribution spanning numerous countries and hundreds of customers, a notable portion of their products finds its way into craft and retail stores catering to home bakers. These home bakers are not just casual buyers; they show a pronounced willingness to invest in premium features. Attributes like Food Safety System Certification (FSSC) 22000, responsibly sourced ingredients, and vibrant natural-color palettes command a premium, allowing suppliers to maintain margins even as commodity-grade volumes wane. This trend feeds on itself: as home bakers showcase their creations online, the resulting viral attention draws newcomers to the hobby. This influx perpetuates a cycle of content creation, product experimentation, and brand allegiance. Yet, the same social platforms spotlight alternative techniques, like buttercream florals and Lambeth-style piping. Google Trends reveals these methods are capturing search interest, often at fondant's expense. This shift compels suppliers to broaden their offerings and spotlight fondant's distinct advantages, like its sculptability and smooth finish.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sugar and glucose price volatility driven by energy and feedstock risks | -0.8% | Global, acute in regions dependent on imported sugar and glucose | Short term (≤ 2 years) |

| Shelf-life and storage limitations constraining distribution reach | -0.5% | Global, most severe in tropical climates and underdeveloped cold chains | Medium term (2-4 years) |

| Competition from buttercream and alternative decorating methods | -0.9% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Health concerns over sugar content and clean-eating trends | -0.6% | Global, led by North America and Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sugar and glucose price volatility driven by energy and feedstock risks

Prices of sugar and liquid glucose, both crucial to fondant production, are subject to structural volatility influenced by energy markets, weather patterns, and geopolitical trade flows. In March 2026, sugar prices saw a significant increase month-on-month. This rise was driven by higher crude-oil prices, which led Brazilian mills to shift sugarcane towards ethanol production. This shift established a price floor for sugar, tethered to energy prices, as long as oil prices remain high. While the Food and Agriculture Organization projected a year-on-year increase in global sugar production for the 2025-2026 marketing season, forecasting it at millions of tonnes, and estimated ending stocks with a stocks-to-use ratio of over seventy percent, the ethanol arbitrage in Brazil's Center-South region poses a risk. It can significantly tighten the physical supply of sugar, regardless of harvests in the Northern Hemisphere [2]Source: Food and Agriculture Organization of the United Nations, “Sugar,” fao.org. Liquid glucose, essential for imparting plasticity and preventing crystallization in fondant, faces similar vulnerabilities. North America, holding a significant portion of the global glucose capacity, is at risk when U.S. corn prices surge due to droughts or when hurricanes on the Gulf Coast disrupt wet-milling operations. In 2025's third and fourth quarters, glucose prices in Asia fluctuated within a range. In early 2025, the U.S. saw prices reach higher levels, while early 2026 saw prices at a comparable level in Northwest Europe. These variations highlight regional supply-demand imbalances and logistical challenges, such as Red Sea diversions, which extended intercontinental shipments by several days. Fondant manufacturers, especially those with limited hedging options or reliant on single-source procurement, face margin pressures when input costs rise. Those catering to price-sensitive commercial bakeries struggle to pass on these cost increases, compelling them to either absorb the volatility or reformulate their products with lower-cost starches, risking texture and shelf life.

Shelf-life and storage limitations constraining distribution reach

Fondant faces challenges in gaining traction in regions with limited cold-chain infrastructure and tropical climates. These areas, characterized by high temperatures and humidity, accelerate the deterioration of fondant, which is vulnerable to moisture absorption, microbial spoilage, and texture degradation when not stored properly. While ready-to-use fondant has a relatively long shelf life in climate-controlled environments, exposure to heat and humidity can quickly lead to surface cracking, color bleeding, and a loss of pliability, making the product unsaleable. Innophos promotes LEVAIR Extended Shelf Life (ESL), an ingredient designed to extend the freshness of baked goods and reduce the carbon footprint per serving. However, its adoption is limited due to the added complexity and cost of formulation. Powdered and instant-mix fondants, with their longer shelf life and reduced freight costs due to lighter weight and volume, are expected to grow steadily. Yet, they present challenges as many small bakeries and home bakers lack the necessary skills and equipment for reconstitution. Distributing these products to rural areas, small-format retail, and emerging markets is further complicated by minimum-order quantities and high last-mile logistics costs, which make low-demand stock-keeping units (SKUs) uneconomical for distributors. As a result, there is a geographic focus on urban centers with reliable refrigeration, leaving significant demand unmet in regions with a strong celebration culture but inadequate infrastructure. Suppliers exploring solutions such as aseptic packaging, modified-atmosphere technologies, or localized production to streamline supply chains face significant barriers. The high capital requirements and regulatory approvals often favor established players with the necessary scale to overcome these challenges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sculpting Fondant Gains as Artisan Demand Rises

In 2025, rolled fondant accounted for 62.12% of the market share, driven by its widespread use in wedding cakes, tiered celebration cakes, and commercial bakery applications. Its ability to provide smooth, seamless finishes and maintain structural integrity makes it essential for event cakes that require durability during extended display and transport. The product's versatility enables decorators to cover large surfaces efficiently, accommodate airbrushing and edible printing, and support stacked tiers without sagging. This has solidified its position as the preferred choice for such applications.

Sculpting and gum-paste fondant, projected to grow at an annual rate of 5.65% through 2031, caters to artisan bakers and home decorators influenced by social media. These users prioritize moldable, detail-oriented materials for creating figurines, floral designs, and three-dimensional decorations. The segment benefits from the proliferation of tutorial content that promotes advanced techniques, encouraging non-professionals to adopt these skills. This trend drives repeat purchases of specialty formulations with higher gum-tragacanth or carboxymethyl cellulose (CMC) powder content, which enhance elasticity and reduce drying time. Manufacturers are also focusing on hybrid formulations that combine the workability of rolled fondant with the sculptability of gum paste. These products aim to meet the needs of professional decorators seeking single-stock keeping unit (SKU) solutions to simplify inventory management and optimize workflows.

By Form: Powdered Mix Expands on Cost and Logistics Advantages

Ready-to-use pack formats accounted for 67.43% of the market share in 2025, driven by their convenience, labor efficiency, and consistent quality. These features appeal to commercial bakeries, foodservice operators, and home bakers who aim to achieve professional results without requiring technical expertise. These formats remove the need for reconstitution equipment, reduce formulation errors, and provide immediate usability. This makes them a preferred option for high-volume operations and time-sensitive decorating tasks.

Powdered and instant-mix fondants, projected to grow at a rate of 5.81% through 2031, are becoming increasingly popular among cost-conscious commercial bakeries and export-oriented suppliers. This is due to their longer shelf life, lower freight costs resulting from reduced weight and volume, and the flexibility to adjust hydration levels for specific applications. The growth of this segment is primarily concentrated in emerging markets, where cold-chain infrastructure is underdeveloped, and local bakeries prefer to control water quality and mixing ratios to address variable ambient conditions.

By Application: Confectionery Centers Accelerate as Chocolate Premiumizes

In 2025, cakes and pastries accounted for 72.21% of fondant volume, highlighting their historical importance in wedding cakes, birthday cakes, and celebration pastries. These applications rely on fondant for smooth finishes, structural support, and decorative versatility. While the segment shows maturity in developed markets, growth is being driven by the Asia-Pacific and Middle East regions, where westernized celebration practices and increasing disposable incomes are fostering demand for multi-tier fondant-covered cakes for weddings, corporate events, and milestone birthdays.

Confectionery centers, projected to grow at a compound annual growth rate (CAGR) of 5.78% through 2031, are benefiting from the premiumization of chocolate assortments. Poured fondant plays a key role in creating liquid or semi-liquid centers in pralines, seasonal eggs, and gift boxes, which command higher price points compared to solid chocolates. Industrial chocolate manufacturers value poured fondant for its mouthfeel, flavor-release properties, and compatibility with enrobing lines. To align with clean-label trends in premium confectionery, these manufacturers are investing in natural-flavor and natural-color variants.

By End-User: Home Bakers Surge on Social Media and Tutorial Content

Commercial bakeries and industrial producers accounted for 54.28% of end-user demand in 2025, driven by their need for consistent quality, bulk purchasing, and technical support provided by large-scale suppliers through dedicated sales teams and application laboratories. These businesses focus on ready-to-use formats that help reduce labor costs, minimize waste, and ensure predictable results across multiple shifts and locations. They often establish long-term contracts to secure pricing and maintain a steady supply.

Home bakers, projected to grow at a rate of 6.79% through 2031, represent the fastest-growing end-user segment. This growth is supported by tutorial content on platforms such as TikTok, Instagram, and YouTube, which make advanced decorating techniques accessible and encourage the purchase of specialty ingredients among non-professionals. This segment shows a greater willingness to pay for premium features, including natural colors, Food Safety System Certification (FSSC) 22000, and responsibly sourced ingredients, creating opportunities for higher margins that compensate for volume declines in commodity-grade products. The expansion of the home-baker segment is self-reinforcing, as more individuals share images of finished cakes on social media, driving viral visibility that attracts new participants to the hobby. This cycle sustains content creation, product trials, and brand loyalty. For instance, Satin Fine Foods achieves 3.5 million digital impressions per month and reaches a combined television audience exceeding 25 million, demonstrating the impact of content marketing on this segment. However, these platforms also highlight alternative techniques, such as buttercream florals and Lambeth-style piping, which, according to Google Trends data, are gaining search interest at the expense of fondant. This shift is encouraging suppliers to diversify their product portfolios and emphasize fondant's unique qualities, such as its sculptability and smooth finish.

Geography Analysis

Europe is expected to maintain a 36.24% market share in 2025, driven by its rich traditions in British royal icing, French pâtisserie, and German marzipan artistry, which integrate fondant into cultural celebrations and professional training programs. The region benefits from a well-established bakery infrastructure, stringent food safety standards, and consumer preferences for artisan finishes, which support premium pricing and stable demand. However, per-capita consumption growth is limited due to increasing health-conscious trends and the adoption of alternative decorating methods. British Bakels' acquisition of Renshaw, a company producing approximately 20,000 tonnes of fondant and marzipan annually at its British Retail Consortium (BRC)-accredited Liverpool facility, highlights the strategic importance of vertical integration and on-site sugar milling to manage input-cost volatility. Eastern European markets, particularly Poland and Romania, are emerging as cost-effective production hubs for export-oriented suppliers aiming to meet Western European demand while addressing wage inflation. However, these operations face logistical challenges and concerns over quality perception. Regulatory changes, such as the European Union's evolving policies on synthetic food colors and front-of-pack nutrition labeling, are encouraging suppliers to adopt natural-color formulations and transparent ingredient declarations, aligning with Food and Drug Administration (FDA) standards and creating opportunities for globally harmonized stock-keeping units (SKUs) [3]Source: European Food Safety Authority, “Food Colours,” efsa.europa.eu.

The Asia-Pacific market is projected to grow at a compound annual growth rate (CAGR) of 5.92% through 2031, fueled by urbanization, rising disposable incomes, and the westernization of celebration rituals in China, India, Southeast Asia, and Oceania. General Mills' investment of INR 100 crore in a second Nashik plant in February 2026 to expand Pillsbury baking-ingredient capacity reflects confidence in sustained double-digit growth in Indian demand for packaged bakery inputs. This growth is supported by the increasing prevalence of nuclear families, dual-income households, and social media influence, which normalize home baking and celebration-cake purchases. In China, the expanding middle class and a shift from traditional mooncakes to multi-tier fondant-covered cakes for weddings and corporate events represent a structural demand driver. However, success requires localized flavors, color palettes, and portion sizes tailored to regional preferences. Southeast Asian markets, including Indonesia, Thailand, and the Philippines, exhibit strong celebration cultures and youthful demographics but face infrastructure challenges such as underdeveloped cold chains and fragmented retail networks, which limit the penetration of ready-to-use fondant and favor powdered formats with longer shelf life. Oceania, led by Australia and New Zealand, mirrors Western European consumption patterns with high per-capita cake spending and mature bakery sectors. However, geographic isolation and small population sizes constrain overall market potential.

North America, the Middle East and Africa, and South America collectively account for the remaining market share. North America demonstrates mature demand, moderate growth, and intense competition from buttercream and edible toppers. Puratos' pending acquisition of Dawn Foods, which operates extensive North American distribution and manufacturing networks, is expected to reshape competitive dynamics by combining scale, innovation, and technical support. This is particularly relevant in a region where commercial bakeries and foodservice operators prioritize supplier reliability and application expertise. The Middle East benefits from high per-capita celebration spending, especially in the Gulf Cooperation Council, where elaborate wedding cakes and corporate event desserts drive premium fondant demand. However, political instability and import dependencies pose supply-chain risks. Sub-Saharan Africa remains underpenetrated due to low disposable incomes, limited bakery infrastructure, and a preference for traditional desserts. Nonetheless, urban centers such as Lagos, Nairobi, and Johannesburg are witnessing emerging demand for celebration cakes among affluent consumers. In South America, led by Brazil and Argentina, strong celebration cultures and growing middle-class populations drive demand. However, economic volatility, currency fluctuations, and import tariffs hinder market development, favoring local or regional suppliers over global brands.

Competitive Landscape

The fondant market is moderately fragmented, characterized by the presence of multinational ingredient conglomerates, regional specialists, and artisan producers operating across overlapping yet distinct customer segments. Consolidation is gaining momentum as larger players focus on vertical integration, geographic expansion, and portfolio diversification to protect margins from raw material price volatility and competition from private-label products. For example, Puratos' agreement in March 2026 to acquire Dawn Foods, combining EUR 3.4 billion and USD 2.1 billion in respective annual sales, is set to create a major bakery-ingredient company with nearly 15,000 employees, operations in 87 countries, and integrated research and development (R&D), manufacturing, and distribution capabilities, offering a competitive edge over smaller players. Similarly, British Bakels' acquisition of Renshaw in December 2023, a Liverpool-based producer with an annual output of 20,000 tonnes, reflects a strategy of acquiring heritage brands with established customer bases, technical expertise, and on-site sugar-milling capabilities to mitigate input-cost fluctuations.

Opportunities for growth in the market include clean-label formulations, direct-to-consumer e-commerce, and localization in emerging markets. The Food and Drug Administration's (FDA) approval in February 2026 for expanded uses of beetroot red and spirulina extracts provides an advantage for suppliers that can quickly reformulate products and secure shelf space in health-focused retail channels. Conversely, companies that fail to adapt risk reputational damage and stock-keeping unit (SKU) reductions as retailers prioritize natural-color products. Additionally, niche disruptors are leveraging social media influencers, subscription models, and bundled kits to bypass traditional wholesale channels and build loyalty among home bakers. However, success in this area requires expertise in digital marketing and last-mile logistics, which many ingredient suppliers currently lack.

Technology adoption varies across the market. Leading companies are utilizing artificial intelligence (AI)-driven demand forecasting, blockchain for sugar traceability, and aseptic packaging to extend product shelf life and reduce waste. In contrast, smaller operators often rely on manual processes and outdated formulations, limiting their competitiveness. The market's future is likely to evolve into a bifurcated structure, with a few global platforms dominating the commercial and industrial segments through scale and innovation, while specialized artisan brands cater to premium and direct-to-consumer niches. Mid-tier players may face increasing margin pressures, potentially leading to strategic exits.

Fondant Industry Leaders

-

Oetker Group

-

Bakels Group

-

Satin Fine Foods Inc.

-

CSM Bakery Solutions

-

Dawn Food Products Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: General Mills India has opened a second manufacturing facility in Nashik, Maharashtra, with an investment of approximately INR 100 crore (USD 12 million) to enhance the production capacity of Pillsbury baking ingredients.

- May 2024: CakeSupplies was appointed as Renshaw's primary distributor for cake decorating products in Europe, overseeing all Renshaw customer accounts in the region. This partnership aligned with Renshaw's strategy to enhance product availability and customer service within the European market.

- April 2024: British Bakels unveiled a new brand identity for JF Renshaw following its acquisition from administration in December 2023. The producer of fondant icings, marzipan, and cake decorating ingredients now operates under the name Renshaw By Bakels. This rebranding highlights the combined 250-year heritage of the two companies. British Bakels also announced plans to launch a new website in summer 2024 and initiate marketing efforts, including public relations and digital campaigns.

Global Fondant Market Report Scope

The fondant market consists of edible sugar-based icing products used for covering, decorating, molding, and sculpting cakes, pastries, cupcakes, cookies, and other confectionery items. Fondant is typically made from sugar combined with water and other ingredients such as corn syrup, gelatin, glycerol, vegetable oil, or shortening, resulting in a smooth, pliable texture that can be rolled, poured, or shaped. The market is segmented by product type (rolled fondant, poured fondant, sculpting/gum-paste fondant, marshmallow fondant), by form (ready-to-use pack, powdered/instant mix, others), by application (cakes and pastries, cookies and biscuits, confectionery centers, ice cream and desserts), by end-user (commercial bakeries and industrial producers, retail/in-store bakeries, foodservice (HoReCa), home bakers), and by geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The market sizing has been done in value terms in USD and volume in Tons for all the abovementioned segments.

| Rolled Fondant |

| Poured Fondant |

| Sculpting/Gum-Paste Fondant |

| Marshmallow Fondant |

| Ready-to-Use Pack |

| Powdered/Instant Mix |

| Others |

| Cakes and Pastries |

| Cookies amd Biscuits |

| Confectionery Centres |

| Ice Cream and Desserts |

| Commercial Bakeries and Industrial Producers |

| Retail/In-store Bakeries |

| Foodservice (HoReCa) |

| Home Bakers |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Rolled Fondant | |

| Poured Fondant | ||

| Sculpting/Gum-Paste Fondant | ||

| Marshmallow Fondant | ||

| By Form | Ready-to-Use Pack | |

| Powdered/Instant Mix | ||

| Others | ||

| By Application | Cakes and Pastries | |

| Cookies amd Biscuits | ||

| Confectionery Centres | ||

| Ice Cream and Desserts | ||

| By End-User | Commercial Bakeries and Industrial Producers | |

| Retail/In-store Bakeries | ||

| Foodservice (HoReCa) | ||

| Home Bakers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is global demand for fondant expected to grow between 2026-2031?

The fondant market is projected to expand at a 4.65% CAGR from 2026 to 2031, reaching USD 4.13 billion by the end of the period.

Which fondant format is gaining the most popularity among cost-conscious bakeries?

Powdered and instant-mix fondant is forecast to grow 5.81% annually through 2031 because of its longer shelf life and lower freight weight.

Why are sculpting and gum-paste fondants outpacing rolled varieties?

Social-media tutorials and demand for intricate 3-D decorations are driving a 5.65% CAGR for sculpting grades, faster than any other product type.

What impact will FDA color-label changes have on suppliers?

The 2026 approval of beetroot red and spirulina extracts enables “no artificial colors” claims, rewarding early reformulators with shelf-space premiums.

Which region offers the strongest growth prospects?

Asia-Pacific leads, with a projected 5.92% CAGR, as Western-style celebration cakes gain traction across China, India, and Southeast Asia.

Page last updated on: