Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 33.01 Billion |

| Market Size (2031) | USD 43.46 Billion |

| Growth Rate (2026 - 2031) | 5.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

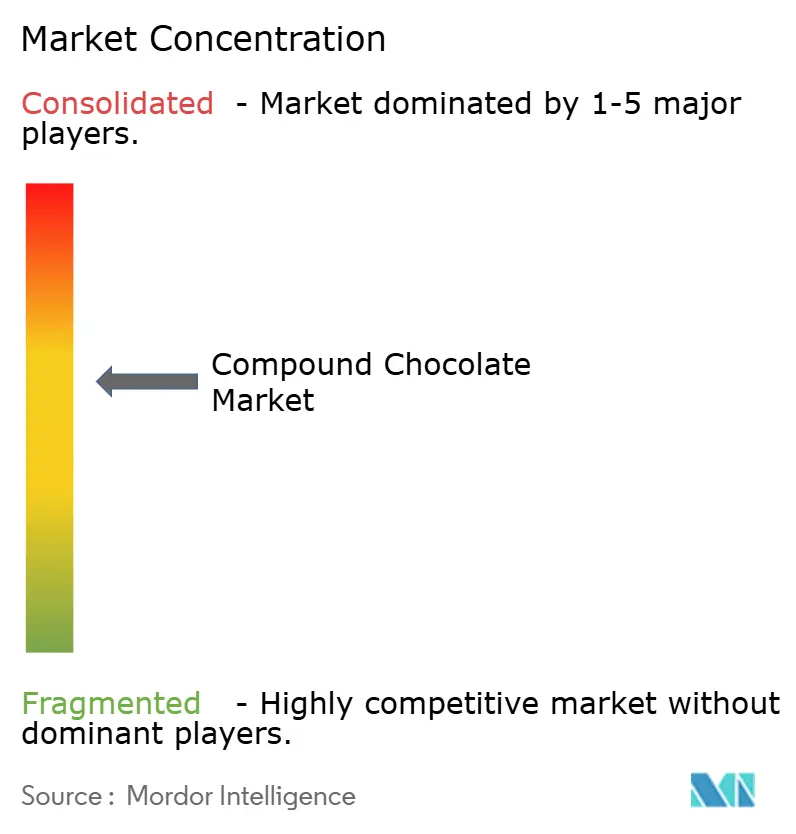

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Compound Chocolate Market Analysis by Mordor Intelligence

The compound chocolate market size is expected to grow from USD 31.24 billion in 2025 to USD 33.01 billion in 2026 and is forecast to reach USD 43.46 billion by 2031 at 5.65% CAGR over 2026-2031. The rising cost of cocoa beans has significantly influenced manufacturers to adopt compound chocolate, which uses vegetable fats instead of cocoa butter, thereby mitigating cost pressures. Additionally, the extended shelf life and simplified processing of compound chocolate offer manufacturers operational advantages, such as reduced labor and energy costs during large-scale production. This cost-effectiveness, coupled with its versatility, has positioned compound chocolate as a preferred ingredient in bakery, confectionery, and ice cream applications. Food processors are further enhancing their appeal by introducing innovative flavors and inclusions, catering to the evolving preferences of consumers. Meanwhile, regulatory developments are reshaping the market dynamics. The European Union’s Deforestation-Free Regulation, effective December 2025, is compelling global manufacturers to source certified fats and traceable cocoa equivalents. This move ensures compliance, maintains market access, and addresses sustainability concerns, all while managing associated costs effectively.

Key Report Takeaways

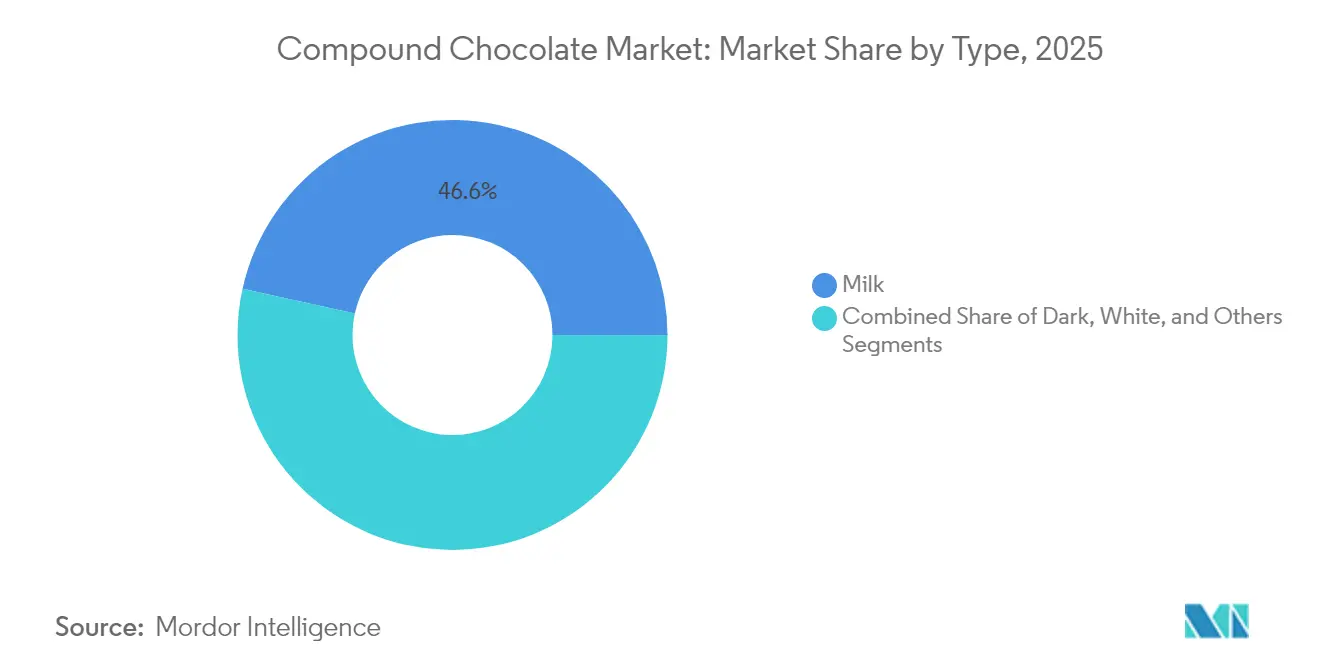

- By type, milk compound chocolate commanded 46.55% of the compound chocolate market share in 2025; dark compound chocolate is projected to grow at a 5.78% CAGR to 2031.

- By form, chips/drops/chunks accounted for 36.72% of the compound chocolate market size in 2025; fillings and spreads are set to expand at a 6.96% CAGR during 2026-2031.

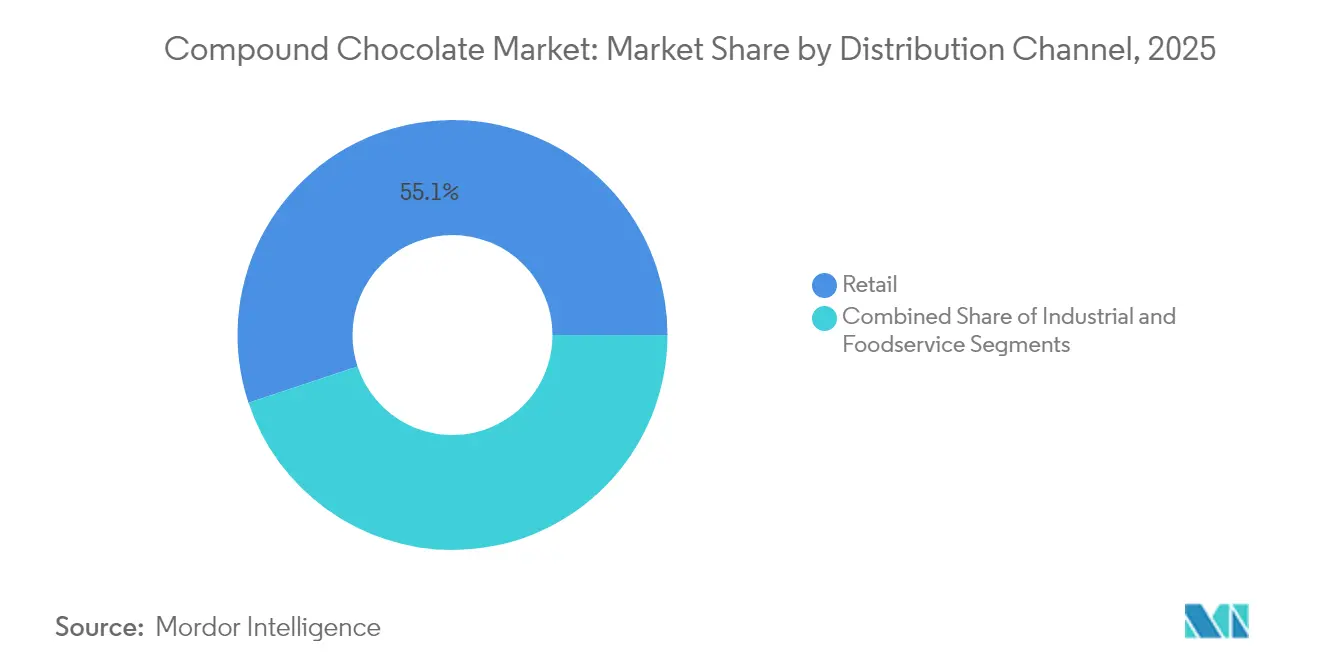

- By distribution channel, retail outlets held 55.10% revenue share in 2025; foodservice is forecast to climb at a 6.83% CAGR through 2031.

- By geography, Europe led with a 33.62% revenue share in 2025; Asia-Pacific is expected to post a 7.45% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Compound Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost effectiveness of compound chocolate as compared to real chocolates surges its demand | +1.7% | Global, with stronger impact in price-sensitive markets of Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Strong demand from the bakery, confectionery, and ice cream industries boosts market growth. | +1.3% | North America, Europe, and emerging Asia-Pacific markets | Medium term (2-4 years) |

| Growth in private label and budget chocolate brands drives demand for compound chocolate. | +0.9% | North America, Europe, with spillover to urban centers in Asia-Pacific | Medium term (2-4 years) |

| Innovations in flavors, textures, and inclusions broadens its consumer appeal. | +0.8% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Increasing adoption of vegan and plant-based diets encourages non-dairy compound variants. | +0.6% | Europe, North America, and urban centers in Asia-Pacific | Long term (≥ 4 years) |

| Longer shelf life than couverture chocolate makes it ideal for mass production and export. | +0.5% | Global, with higher impact in regions with challenging supply chain infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cost effectiveness of compound chocolate as compared to real chocolates surges its demand

The growing adoption of compound chocolate reflects a strategic response to intensifying cost pressures across the chocolate industry, as manufacturers seek ways to protect margins without sacrificing product appeal. Compound chocolate’s cost effectiveness, operational simplicity, and ability to bypass the tempering process make it an increasingly viable alternative to traditional chocolate, especially for large-scale commercial applications. In 2024, U.S. chocolate and cocoa product exports were valued at USD 2.36 billion, according to the U.S. Department of Agriculture, underscoring the persistent price pressures within the industry[1]United States Department of Agriculture, "U.S. Chocolate & Cocoa Products Exports in 2024", www.fas.usda.gov. The sharp and sustained rise in cocoa prices has widened the cost gap between real chocolate and compound chocolate, making the latter a more attractive option for manufacturers facing shrinking margins. Financial institutions expect elevated cocoa prices to persist in the medium term, reinforcing the urgency for structural adjustments like switching to compound chocolate, which enables manufacturers to manage input costs, safeguard profitability, and remain competitive in a volatile market landscape.

Strong demand from the bakery, confectionery, and ice cream industries boosts market growth.

The industrial applications of compound chocolate in the bakery, confectionery, and ice cream sectors are driving substantial volume growth, as manufacturers increasingly prioritize its functional benefits over cost advantages. Compound chocolate provides notable technical benefits, such as eliminating the need for tempering, offering stable melting properties, and ensuring compatibility with a wide range of ingredients. These attributes make it indispensable for large-scale production environments where efficiency and consistency are critical. The Institute of Food Technologists emphasizes the importance of applying scientific knowledge to enhance product quality and improve consumer satisfaction in the chocolate market[2]The Institute of Food Technologists, "Confection Content Collection", www.ift.org. They note that compound chocolate formulations can be customized to meet specific industrial needs, addressing challenges such as ingredient integration and production scalability. In response to this growing demand, companies are innovating by developing specialized compound chocolate products tailored for diverse industrial applications. With production capacities reaching tens of thousands of tons annually, these companies are well-positioned to supply food manufacturers across multiple regions, supporting the evolving needs of the global food industry.

Growth in private label and budget chocolate brands drives demand for compound chocolate.

Economic pressures in 2024-2025 have significantly accelerated the adoption of private label chocolate products, creating a structural advantage for compound chocolate formulations. This shift reflects broader changes in consumer behavior, where rising price sensitivity has pushed retailers to focus on delivering cost-effective solutions without sacrificing quality. Compound chocolate has become a pivotal component, enabling retailers to offer products that align with consumer expectations at competitive price points. The strategic relevance of this segment is further highlighted by the evolution of private label offerings, which now include premium-positioned products. These products utilize compound chocolate as a foundation while integrating innovative features such as distinctive flavors, diverse inclusions, and marketing narratives that emphasize attributes like sustainability, ethical sourcing, or health benefits. Government trade data indicates that this trend is particularly prominent in developed markets, where consumers increasingly prioritize value propositions while maintaining high-quality standards. This evolving dynamic is reshaping the competitive landscape, solidifying the role of compound chocolate in addressing the demands of an ever-changing market.

Innovations in flavors, textures, and inclusions broadens its consumer appeal.

Manufacturers are driving innovation in compound chocolate formulations, expanding market opportunities beyond traditional cost-driven applications. These advancements focus on delivering superior sensory experiences, positioning compound chocolate as a preferred ingredient rather than merely a cost-effective substitute. The market is experiencing significant progress in texture modification and flavor enhancement, with companies introducing specialized products designed to meet diverse and creative application needs. Industry associations underscore the importance of such innovations in improving product quality and addressing evolving consumer demands. Notably, compound chocolate is gaining traction in applications where it offers unique functional benefits, such as enhanced stability and versatility, which traditional chocolate cannot match.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over hydrogenated fats and additives used in some compound formulations. | -0.7% | North America, Europe, and urban centers in Asia-Pacific | Medium term (2-4 years) |

| Regulatory scrutiny on artificial ingredients and labeling standards could hinder growth. | -0.5% | Europe, North America, with gradual adoption in other regions | Medium term (2-4 years) |

| Fluctuating prices of vegetable fats and cocoa substitutes can affect cost stability. | -0.4% | Global, with particular impact on cost-sensitive applications | Short term (≤ 2 years) |

| Intense competition from real chocolate products in developed markets limits expansion. | -0.3% | North America, Europe, and premium segments in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health concerns over hydrogenated fats and additives used in some compound formulations.

Growing consumer awareness about the health risks associated with hydrogenated fats and artificial additives in compound chocolate is driving resistance in the market, particularly among health-conscious demographics. Regulatory developments further amplify these concerns. For example, the FDA enforces strict guidelines on chocolate production, specifying minimum cocoa content and restricting the use of certain additives. Similarly, the Singapore Food Agency has implemented a robust regulatory framework requiring safety assessments and permitting only specific additives, reflecting the increasing scrutiny on compound chocolate. These health-driven constraints significantly impact premium market segments, where consumers demand higher ingredient transparency and quality. Consequently, the market is experiencing a clear bifurcation: compound chocolate continues to expand its presence in value-oriented applications due to cost advantages, while its penetration in premium segments remains limited by concerns over its composition and regulatory compliance.

Regulatory scrutiny on artificial ingredients and labeling standards could hinder growth.

Compound chocolate manufacturers in developed markets are increasingly grappling with strategic challenges stemming from evolving regulatory frameworks on food labeling and ingredient transparency. For example, the Canadian government enforces detailed labeling requirements for confectionery and chocolate products in January 2025, underscoring the regulatory complexities manufacturers must address. These regulations are driving companies to prioritize cleaner formulations and adopt more transparent labeling practices to meet compliance standards. The situation becomes even more challenging in cross-border trade, where inconsistent standards across jurisdictions create additional compliance complexities and potential barriers to market entry. To navigate these challenges effectively, manufacturers are compelled to develop region-specific formulations and implement tailored labeling strategies that align with the regulatory requirements of each market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Milk Compound Chocolate Dominates Through Versatility

In 2025, the milk compound chocolate segment commands a dominant 46.55% market share, largely due to its favored status in bakery and confectionery applications. Its leadership is anchored in a balanced flavor profile and versatility, making it the go-to for manufacturers, whether for enrobing or molding. This segment's robustness is further highlighted by its ingredient compatibility and consistent performance in automated settings. Cargill's technical insights reveal that vegetable fat-based compound chocolates eliminate the need for tempering, enhancing their appeal for enrobing and molding. The milk variant's widespread popularity is attributed to its universally appealing taste and the functional advantages it offers to industrial users.

The dark compound chocolate segment is on the rise, with projections indicating an 5.78% CAGR from 2026 to 2031, outpacing the overall market. This surge is largely fueled by heightened consumer awareness of dark chocolate's health benefits, notably its antioxidant properties and potential heart advantages. Additionally, the segment aligns with the growing consumer trend of "mindful indulgence," where the focus is on balancing enjoyment with nutritional value. Industry experts emphasize the significance of market trends and consumer insights in crafting new chocolate offerings, especially as health-conscious choices gain traction. Moreover, the dark compound chocolate segment is reaping rewards from flavor innovations and the addition of functional ingredients that bolster its health appeal.

By Form: Chips/Drops/Chunks Lead Through Manufacturing Efficiency

In 2025, the chips/drops/chunks segment holds a leading 36.72% share of the compound chocolate market, driven by its adaptability across industrial baking, confectionery, and home cooking applications. This format's widespread adoption is due to its ease of handling, precise portion control, and reliable melting properties, which make it an ideal choice for large-scale manufacturing processes. Its compatibility with automated dispensing systems and ability to retain structural integrity during processing and storage further reinforce its dominance. According to Blommer Chocolate Company's technical documentation, compound chocolates in this format are highly user-friendly for various applications, provided they are handled correctly to avoid issues such as fat and sugar bloom. Moreover, the chips/drops/chunks format offers manufacturers significant flexibility in product development, enabling seamless integration into existing recipes and production workflows without requiring substantial equipment modifications. This adaptability makes it a preferred option for manufacturers aiming to optimize efficiency and maintain product quality.

The fillings and spreads segment is anticipated to grow at the fastest pace, with a projected 6.96% CAGR from 2026 to 2031, reflecting evolving consumer preferences for indulgent and ready-to-use products. This growth is fueled by advancements in texture and flavor, which enhance the appeal of compound chocolate-based fillings and spreads among both industrial users and end consumers. The segment benefits from the increasing demand for convenience products and the rising popularity of artisanal and premium bakery items that incorporate sophisticated fillings. Companies are focusing on developing specialized formulations that deliver improved stability, superior flavor release, and enhanced processing characteristics tailored for filling applications. Additionally, the expansion of the foodservice sector significantly contributes to this growth, as ready-to-use fillings and spreads offer operational efficiencies and consistent quality, which are highly valued by commercial kitchens. This combination of innovation and market demand positions the fillings and spreads segment as a key driver of growth in the compound chocolate market.

By Distribution Channel: Retail Dominance Reflects Consumer Access Patterns

In 2025, retail distribution channels dominate the market with a commanding 55.10% share. Supermarkets and hypermarkets stand out as the primary access points for consumers. This retail dominance underscores established purchasing patterns for chocolate products. Retail environments not only enhance visibility but also offer comparison shopping, pivotal in shaping consumer choices. Strengthening this retail channel is the rise of sophisticated private label programs. These programs leverage compound chocolate, ensuring competitive pricing without compromising on quality. Meanwhile, online retail is carving out a significant niche, boasting a broader product selection and unmatched convenience over traditional channels. Additionally, the retail sector capitalizes on seasonal demand and promotional activities, especially during holidays when chocolate sales surge.

From 2026 to 2031, the foodservice segment is set to outpace others, growing at a robust 6.83% CAGR. This growth is largely attributed to the hospitality sector's post-pandemic resurgence and the unique advantages of compound chocolate in commercial kitchens. Operators in the foodservice industry appreciate compound chocolate for its consistent performance, the convenience of not needing tempering, and its extended shelf life. These attributes lead to significant efficiencies in labor and inventory management. The segment's expansion is further fueled by the growth of quick-service restaurants, bakery chains, and institutional foodservices, all in search of reliable and cost-effective ingredients. Highlighting the foodservice segment's significance, Cargill has made strategic moves, expanding production capacities for coatings and fillings, particularly with facility expansions in Europe. Moreover, the foodservice sector is riding the wave of menu innovations, seamlessly integrating chocolate into both savory and sweet dishes.

Geography Analysis

In 2025, Europe commands the largest regional market share at 33.62%, capitalizing on its well-established chocolate manufacturing base and advanced retail networks. Europe's chocolate market thrives on a rich consumption tradition and is bolstered by major industry players pioneering innovations in compound chocolate. Sustainability is becoming a focal point in Europe, with initiatives like the EU's Deforestation-Free Regulation reshaping supply chains and imposing new compliance mandates on manufacturers. As European consumers increasingly prioritize sustainability in their purchasing choices, manufacturers are responding by crafting more transparent and eco-friendly compound chocolate formulations. While the market is mature, there's a vibrant push towards innovation, especially in premium and specialty segments.

Asia-Pacific is set to outpace others with a projected 7.45% CAGR from 2026 to 2031, fueled by urbanization, rising incomes, and the growth of modern retail. As lifestyles evolve and Western confectionery gains traction, new avenues for compound chocolate applications emerge. Major players are making strategic moves, establishing production units, and ramping up capacity to cater to local demands. Events like India's AAHAR fair, backed by government trade promotions, foster knowledge sharing and collaborations in food processing. Given the region's varied market dynamics, companies are customizing product development and distribution strategies to align with local tastes and regulations.

North America stands as a mature market, boasting a stronghold of leading chocolate manufacturers and a robust distribution network. The compound chocolate market here thrives on a vibrant foodservice sector and a surge in consumer interest in baking and home cooking. U.S. government data underscores the chocolate sector's significance, highlighting substantial export values for chocolate and cocoa products. With a regulatory focus on food safety and labeling clarity, North American manufacturers are held to high standards in both product development and marketing. Meanwhile, South America and the Middle East & Africa, though smaller in market share, are witnessing a surge in growth, spurred by a burgeoning middle class and modern retail developments enhancing product accessibility.

Regulatory Landscape

Regulation affecting compound chocolate covers food identity and labeling rules for chocolate and coatings, additive permissions, and traceability requirements for cocoa and vegetable fats. In Europe, Directive 2000/36/EC underpins national interpretations that distinguish chocolate from compound or flavored coatings through compositional thresholds, shaping how products can be named and marketed; the Food Safety Authority of Ireland also provides implementation guidance for cocoa and chocolate products. Separately, the EU Deforestation-Free Regulation, effective December 2025, has increased the compliance burden on global manufacturers selling into Europe by raising traceability and due-diligence expectations across cocoa equivalents and relevant fats.

Outside Europe, national and trade controls add further complexity. In the United Kingdom, The Food Additives and Novel Foods (Authorisations and Miscellaneous Amendments) Regulations 2024 updated additive permissions for cocoa and chocolate product categories, influencing formulation choices for compound coatings and fillings. In Brazil, Law No. 15.404 (enacted May 2026) set compositional standards for cocoa and chocolate products, tightening the definition and labeling boundary between standard chocolate and compound-style products. For cross-border flows, U.S. Customs and Border Protection published a 2026 tariff-rate quota for chocolate under Chapter 18, adding compliance and landed-cost considerations for importers managing product classification and quota utilization.

Competitive Landscape

The global compound chocolate market is dominated by players such as Cargill Incorporated, Barry Callebaut Group, and Fuji Oil Holdings Inc., among others, which hold a significant share. These companies benefit from well-established distribution networks, strong brand loyalty, and large-scale manufacturing capabilities, which create substantial barriers for new entrants. This market consolidation ensures consistent product quality, cost efficiency, and continuous innovation, particularly in meeting the needs of industrial and commercial bakery and confectionery clients.

Innovation plays a critical role in maintaining competitiveness, with companies heavily investing in research and development to create compound chocolates that closely replicate the taste and texture of real chocolate while remaining cost-effective. As regulatory requirements become stricter, vertical integration and effective supply chain management are becoming essential for maintaining a competitive edge.

Firms with strong sustainability practices and traceability systems are better positioned to meet increasing compliance demands, giving them a significant advantage. Additionally, manufacturers are focusing on balancing cost efficiency with quality improvements to expand the use of compound chocolates beyond traditional cost-sensitive markets into premium and specialty segments, driving further growth in the market.

Compound Chocolate Industry Leaders

-

Cargill Incorporated

-

Barry Callebaut Group

-

Fuji Oil Holdings Inc.

-

Puratos Group

-

The CAMPCO Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Diversification away from cocoa butter dependence is creating product and positioning space for compound chocolate, coatings, and chocolate alternatives that use different fat systems and ingredient bases. In Asia-Pacific, where shelf-life performance under heat and humidity is a practical constraint, manufacturers are emphasizing formulations designed for tropical distribution conditions; Barry Callebaut pointed to this need through compound capacity actions at its Suzhou, China site (February 2024). This supports demand for suppliers that can provide heat-stable chips, coatings, and ready-to-use fillings for industrial bakery, confectionery, and ice cream lines that prioritize processing simplicity (no tempering) and consistent performance.

New capacity and targeted investments by large players also suggest room in fast-growing production and application hubs, particularly India and North America. Barry Callebaut inaugurated a greenfield factory in Neemrana, India in July 2025 with production lines for chocolate and compound products, supporting localization for regional customers and private label programs. On the input side, investments tied to specialty fats reinforce compound chocolate competitiveness when cocoa volatility pushes manufacturers to reformulate; capability build-outs in specialty fats for confectionery and bakery applications give compound producers more levers for texture, melting behavior, and cost management while meeting region-specific labeling and additive constraints.

Recent Industry Developments

- May 2026: Cargill launched NextCoa, a cocoa-free chocolate alternative made by upcycling grape seeds. The launch expands the set of non-cocoa options available to confectionery and bakery customers facing cocoa price volatility and supply constraints. It also increases competitive pressure on compound and coating suppliers to differentiate on taste, functionality, and sustainability claims using alternative ingredient platforms.

- March 2026: Cargill announced an expansion of its Port Klang, Malaysia edible oil plant, adding a new specialty fats production line aimed at chocolate confectionery and bakery applications. The added specialty fats capability supports a broader range of compound chocolate and coating formulations that rely on vegetable fat systems. This strengthens regional supply for Asia-focused customers where heat stability and processing consistency are key product requirements.

- June 2024: Blommer Chocolate Company (Fuji Oil Holdings) launched Elevate chocolate coatings made with an ingredient positioned as an alternative to traditional cocoa butter. The product introduction broadened the coatings toolkit for manufacturers balancing performance, cost, and ingredient constraints. It also reinforced innovation activity around cocoa butter alternatives, a theme aligned with rising interest in compound solutions for large-scale production.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The compound chocolate market, for our sizing work, covers the revenue generated from compound chocolate products made using cocoa butter substitutes or equivalents, which are then sold for use in industrial and foodservice applications as well as retail formats.

Scope exclusions: We exclude traditional couverture and pure cocoa butter chocolate products, and we also exclude finished chocolate confectionery sales when compound chocolate is only one ingredient input.

Segmentation Overview

-

By Type

- Dark

- Milk

- White

- Others

-

By Form

- Chips/Drops/Chunks

- Slabs and Blocks

- Coatings

- Fillings & Spreads

- Others

-

By Distribution Channel

-

Retail

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

- Industrial

- Foodservice

-

Retail

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clear view of what compound chocolate is and how it is traded, priced, and regulated, since definitions can vary across countries and even across ingredient suppliers. We used public sources such as FAOSTAT for cocoa and vegetable oil context, UN Comtrade for relevant trade flows, national customs and statistical offices for food manufacturing indicators, and Codex Alimentarius and EU food labeling rules to interpret product inclusion.

After that, we pulled supporting signals from company annual reports and investor presentations, association websites for confectionery and bakery, and trusted press coverage on cocoa butter substitutes, palm kernel oil, and supply disruptions. Where needed, we also used paid subscriptions for company financials and intelligence, news and financials, patent databases, and shipment-level import or export checks to validate directionally the activity levels behind the model. These examples are indicative only, and many other sources were also consulted for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work was used to test what we found in desk research, especially around what suppliers count as compound, how pricing is quoted (contracted versus spot), and what typical end uses drive real demand. We spoke with a mix of ingredient suppliers, compound chocolate manufacturers, distributors, and industrial users across major regions, so assumptions on application mix, form preferences, and substitution behavior could be confirmed and adjusted.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | APAC: 50% |

| Mid tier: 50% | Functional/Unit leaders: 34% | EMEA: 30% |

| Smaller Players: 22% | Managers: 52% | Americas: 20% |

Market-Sizing & Forecasting

The model is built using both top-down and bottom-up logic. On the top-down side, we reconstructed the demand pool by linking chocolate and confectionery manufacturing activity to ingredient intensity, then adjusting for the share that is typically served by compounds rather than cocoa butter based chocolate. Once the market total was formed, it was cross-checked with selective bottom-up approximations such as sampled supplier revenue splits, channel checks for industrial and retail packs, and a volume times average selling price approach for common forms.

A few key inputs that shaped the totals were cocoa butter substitute and equivalent usage patterns, industrial bakery and confectionery output trends, form-level mix shifts (chips and drops, slabs and blocks, and coatings), application demand from ice cream and frozen desserts, and regional price movements for key vegetable fats. When data was not available for a smaller geography or niche application, gaps were handled by using proxy indicators like processed food output growth and import reliance, followed by expert confirmation.

For forecasting, scenario analysis was applied so we could reflect different paths for fat prices, cocoa-related constraints, and downstream demand from bakery and confectionery. The final trajectory was then checked against the direction and magnitude shared by industry respondents, which helped keep the forecast realistic and explainable.

Data Validation & Update Cycle

Outputs are checked in a few passes before they are finalized. We compare model results against independent signals such as trade movements, pricing direction, and changes in industrial production, and then we review any variances that look too large for a given region or application.

Before sign-off, the work is reviewed by another analyst, and follow-up calls are triggered when a key assumption changes or when new public information conflicts with earlier inputs. Reports are refreshed annually, and material events can be reflected through interim updates, followed by a last pre-delivery review so clients receive the latest view.

Mordor Intelligence's Compound Chocolate Market Size Measured Against Other Published Estimates

Different published market values can look far apart because firms do not always count the same products and channels, and they may also use different base years or currency timing. In compound chocolate, the biggest swing tends to come from what is treated as ingredient level revenue versus finished confectionery value, followed by how industrial consumption is translated into dollars.

Key gap drivers also include whether cocoa butter equivalents and substitutes are both included, how average selling prices are updated when vegetable fat costs move quickly, and how application shares are refreshed for coatings and bakery use versus retail packs. The main spread in the table is explained by the choice to count compound chocolate as a product market across forms and channels, a scope choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 33.01 B (2026) | |

| Trade Publisher A | USD 4.58 B (2025) | This estimate appears to sit on a narrower value capture, which can happen when only select product formats or a limited channel set is monetized, and when industrial ingredient demand is not fully reconciled with application-level consumption. |

| Industry Analyst Note B | USD 26.40 B (2023) | The value is anchored to an earlier year and may apply different price progression for vegetable fats and cocoa butter substitutes, which can understate later-year inflation effects and mix shifts toward higher-value coatings and specialty compounds. |

Overall, the spread is consistent with differences in year selection and what is being monetized, namely ingredient revenue versus downstream product value. By keeping scope rules explicit, using production and application signals as checks, and then validating pricing and mix assumptions through interviews, the final market size stays traceable to repeatable steps.

Key Questions Answered in the Report

What is the compound chocolate market size in 2026 and its growth outlook to 2031?

The market is valued at USD 33.01 billion in 2026 and is forecast to reach USD 43.46 billion by 2031 at a 5.65% CAGR.

Which region will record the fastest compound chocolate market growth?

Asia-Pacific is projected to register a 7.45% CAGR between 2026 and 2031, outpacing all other regions.

Which product type currently leads the compound chocolate market share?

Milk compound chocolate holds 46.55% of global revenue in 2025 due to its versatile flavor and processing reliability.

What factors are boosting compound chocolate demand in foodservice channels?

Consistent performance, long shelf life, and simplified handling support a 6.83% CAGR for foodservice use through 2031.

Page last updated on: