Fluorosilicone Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

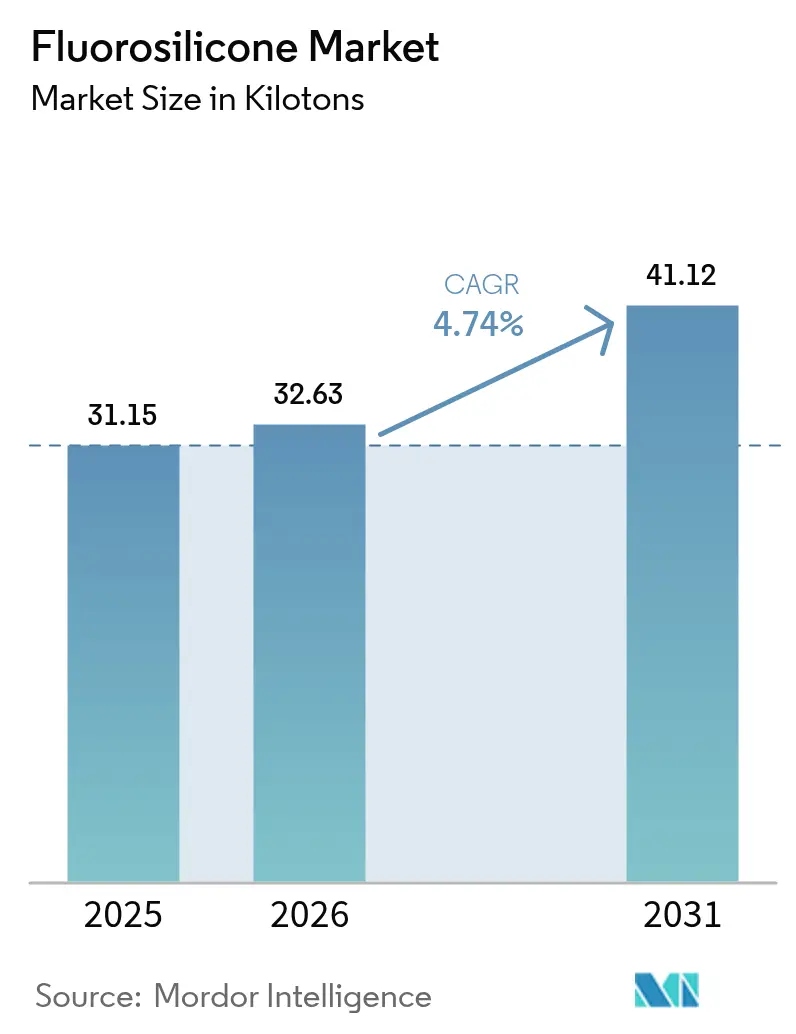

| Market Volume (2026) | 32.63 kilotons |

| Market Volume (2031) | 41.12 kilotons |

| Growth Rate (2026 - 2031) | 4.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

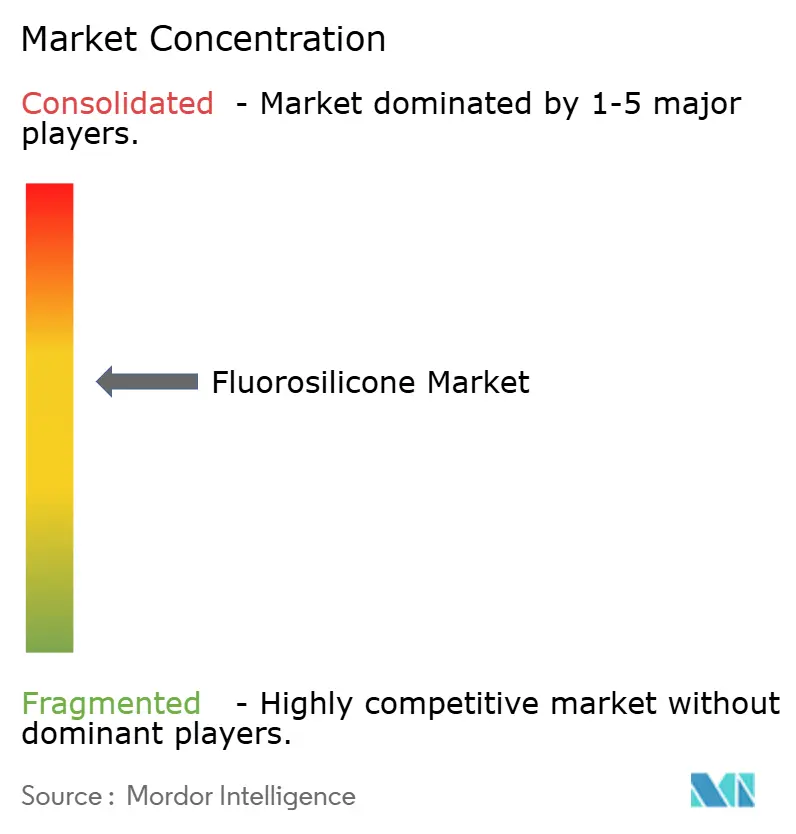

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fluorosilicone Market Analysis by Mordor Intelligence

The fluorosilicone market size is expected to grow from 31.15 kilotons in 2025 to 32.63 kilotons in 2026 and is forecast to reach 41.12 kilotons by 2031 at 4.74% CAGR over 2026-2031. Demand stays linked to applications where conventional elastomers cannot tolerate wide temperature swings, aggressive fuels, or rapid decompression. Growth is reinforced by greater use in aerospace fuel and hydraulic circuits, thermal management loops in battery-electric vehicles, and ultra-high-pressure oilfield tools. Simultaneously, global PFAS regulations dismantle parts of the fluoropolymer supply chain yet open substitution windows for fluorosilicone-based designs. Regional momentum centres on Asia-Pacific, where automotive and electronics plants convert to higher-value sealing and coating materials, while producers in North America and Europe target differentiated grades for defence and deep-sea energy assets.

Key Report Takeaways

- By product type, elastomers led with 46.55% of fluorosilicone market share in 2025; lubricants and other specialties are set to advance at a 7.55% CAGR through 2031.

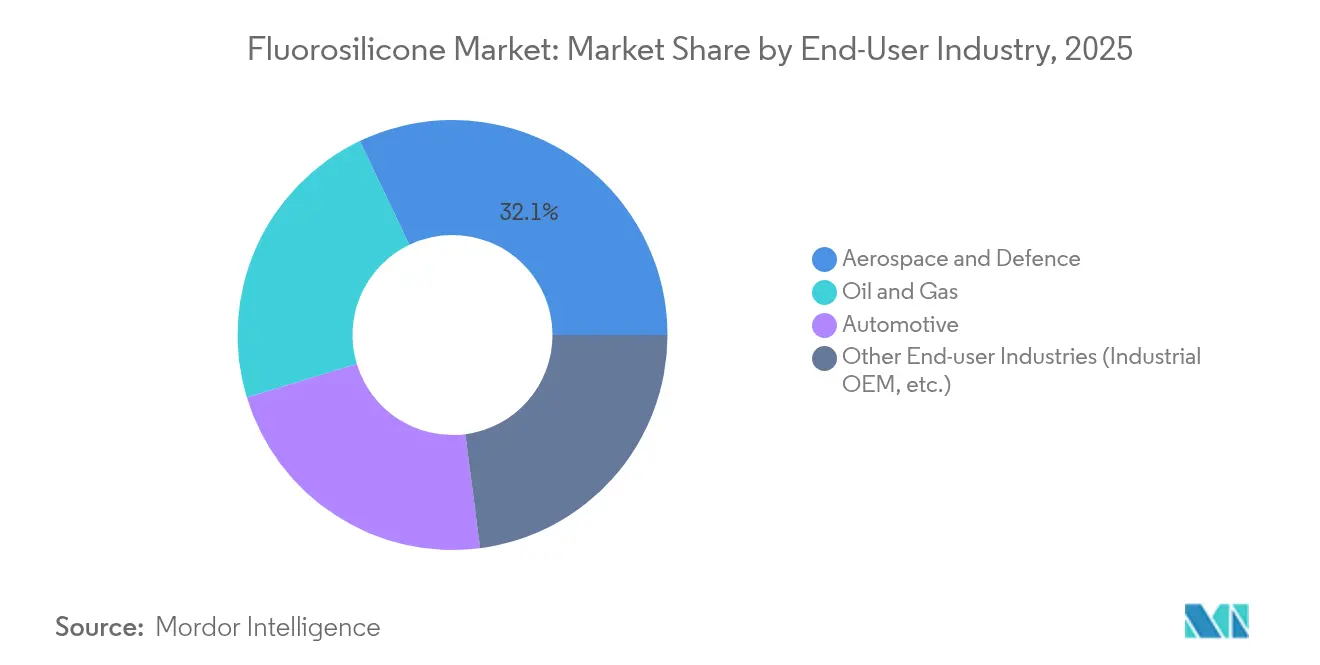

- By end-user industry, aerospace accounted for 32.10% of the fluorosilicone market size in 2025, whereas industrial OEM and other users are projected to record a 7.05% CAGR between 2026-2031.

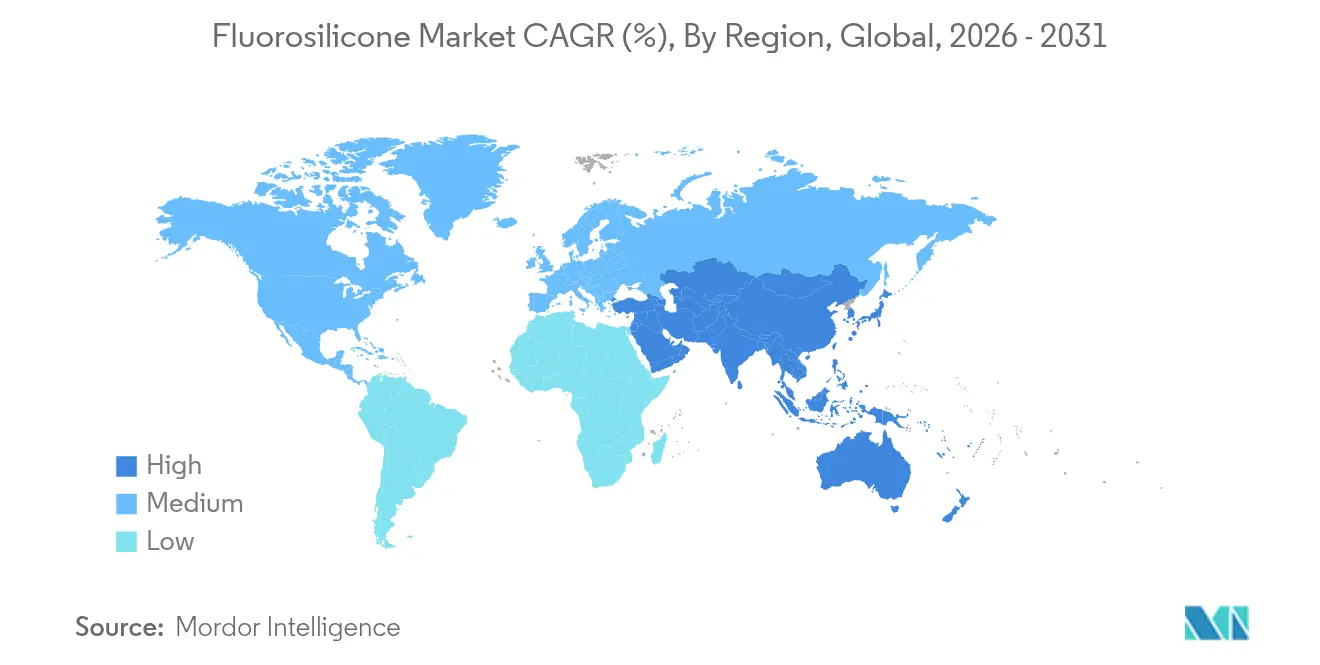

- By geography, Asia-Pacific held 38.55% of the fluorosilicone market share in 2025 and is forecast to register the fastest regional CAGR of 6.55% over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fluorosilicone Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from aerospace & defence fuel/hydraulic systems | +1.2% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Rising utilisation from the oil and gas industry | +0.9% | Global, with emphasis on offshore regions | Long term (≥ 4 years) |

| Adoption in high-temperature automotive turbo & bio-fuel lines | +0.8% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Emergence of flexible electronics and electric vehicle battery applications | +1.1% | APAC leading, expanding to North America & EU | Medium term (2-4 years) |

| Commercialisation of bio-sourced fluorinated siloxane monomer | +0.5% | EU & North America regulatory-driven adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from Aerospace & Defence Fuel/Hydraulic Systems

Modern aircraft fuel circuits run hotter than 177 °C and cycle between synthetic bio-jet blends, hydraulic fluids, and anti-icing additives. Standard silicones fracture or swell, but trifluoropropyl-substituted chains in fluorosilicone stay elastic down to -73 °C, avoiding brittle failure at altitude. Leading seal suppliers now qualify fluorosilicone O-rings under MIL-DTL-25988 to satisfy rapid pressure cycling without fatigue. Weight-saving trends intensify the switch because thinner seals rely on superior chemical tenacity to preserve lifetime reliability[1]ERIKS, “Fuel-Resistant Sealing Solutions for Aerospace,” eriks.com.

Rising Utilisation from Offshore Oil and Gas Fields

Ultra-deep wells exceed 22,000 psi and approach 450 °F. Completion strings and FPSO fluid swivels face sour gas, high brine salinity, and rapid gas decompression. Fluorosilicone keeps modulus and volume change within API-spec limits where HNBR and perfluoroelastomer grades either crack or lose strength. Longer mean time between intervention lowers lifting costs, so operators specify fluorosilicone on packers, blow-out preventer seals, and downhole sensors for harsh-gas reservoirs.

Adoption in High-Temperature Automotive Turbo & Bio-Fuel Lines

Smaller high-output engines expose hoses and gaskets to cyclical loads between -40 °C and 250 °C. Liquid fluorosilicone rubber processes in injection molds that produce complex geometries with minimal flash, trimming assembly waste. Resistance to ethanol-rich gasoline prevents 10-15% swelling seen with nitrile seals. Form-in-place fluorosilicone gaskets also combine electromagnetic shielding with thermal durability for electric vehicle power electronics[2]Dow, “SILASTIC Fluorosilicone Rubber for Turbocharger Hoses,” dow.com.

Emergence of Flexible Electronics and EV Battery Applications

Direct-immersion cooling for 800 V battery packs relies on dielectric fluids that neither conduct electricity nor degrade in hot spots. Fluorosilicone fluids offer low conductivity and remain stable above 200 °C, a range unreachable for hydrocarbon oils. In wearable devices, the polymer’s biocompatibility supports skin-contact sensors that survive perspiration and cleaning agents. Research prototypes use permeable fluorosilicone substrates to let vapor escape without compromising circuit function.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of cost-competitive alternatives | -0.7% | Global, particularly price-sensitive markets | Short term (≤ 2 years) |

| Fluoromonomer price volatility & supply bottlenecks | -0.8% | Global supply chain impact | Medium term (2-4 years) |

| Environmental concerns related to fluorine compounds | -0.6% | EU & North America regulatory focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of Cost-Competitive Alternatives

Advanced EPDM, HNBR, and VMQ compounds now reach fuel-resistance levels once exclusive to fluorosilicone, offering up to 70% material savings for moderate-temperature duties. The switch is fastest in mass-market automotive and appliance seals where total exposure temperatures seldom surpass 180 °C. However, in environments with simultaneous exposure to aggressive aromatics and large thermal swings, competing elastomers still fall short.

Fluoromonomer Price Volatility & Supply Bottlenecks

Only a handful of producers make trifluoropropyl vinyl silane, the critical monomer for fluorosilicone. Outages or regulatory delays tighten supply, sending spot prices higher and prompting some converters to ration capacity. Patent walls around advanced synthesis routes prolong the concentration. Car makers negotiating annual supply contracts often hedge with hybrid sealing stacks that blend fluorosilicone only in high-exposure sections[3]Daikin Chemicals, “Fluoromonomer Production and Supply,” daikinchemicals.com .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Elastomers Outperform on Versatility

Elastomers generated the largest slice of the fluorosilicone market in 2025, capturing 46.55% of volume. They dominate because high-consistency rubber and liquid silicone rubber formats suit press-molding, extrusion, and injection lines used by hose, gasket, and O-ring producers. Lubricants, greases, and dielectric fluids sit in a smaller but faster pool, expected to post a 7.55% CAGR through 2031 as battery-electric cooling circuits scale up. In mass production, liquid grades cut cycle times while holding tight tolerances, and two-part room-temperature-vulcanizing chemistries simplify on-line gasketing. Specialty coatings and antifoams stay niche yet profitable, sold to pharmaceutical and food processors that need chemically inert, non-tainting agents.

A wider formulation window allows suppliers to tailor hardness, resilience, and swelling limits to each customer specification. That flexibility preserves elastomer prominence even as volumes shift among industries. Meanwhile, the lubricant sub-segment rides the jump in direct-immersion battery cooling, where low electrical conductivity matters. Adoption also spreads in semiconductor vacuum pumps unable to tolerate hydrocarbon backstreaming. Across these uses the fluorosilicone market size for lubricants could move from lab scale to commercial tonnage by 2030.

By End-User Industry: Aerospace Remains the Premium Anchor

Aerospace represented 32.10% of the fluorosilicone market in 2025 as OEMs and airlines accept the higher price point in exchange for decades-long reliability. Each wide-body aircraft contains hundreds of fluorosilicone O-rings, diaphragms, and grommets that secure fuel, hydraulic, and bleed-air functions. The next growth pocket lies in industrial OEM segments such as semiconductor, chemical processing, and precision instrumentation, which together are forecast to expand at 7.05% CAGR through 2031. Electric vehicle powertrain makers follow, using seals and hoses that withstand high glycol mixes and rapid thermal cycles.

Military aviation and space launch systems specify fluorosilicone for exposure down to cryogenic temperatures, pressing the material beyond the reach of alternative polymers. Oilfield service companies also rank among the top buyers, reserving the compound for sour gas tools. As environmental scrutiny intensifies, chemical producers market low-VOC, bio-sourced grades to mirror sustainable sourcing rules imposed by aircraft and defence contractors. This interplay between performance and compliance keeps the fluorosilicone industry pivotal in mission-critical applications.

Geography Analysis

Asia-Pacific controlled 38.55% of global shipments in 2025 and is poised to record a 6.55% CAGR to 2031. China remains the central node, thanks to high-volume automotive turbocharger production, rapid expansion in 300 mm semiconductor fabs, and state programs that target domestic supply chains for specialty chemicals. Indigenous chemists are trialling fluorosilicone foams for oil-water separation, a step that underlines the region’s innovation depth. Japan leverages precision process know-how to turn out ultra-clean grades for space and defence instruments, while South Korea’s chaebol structure benefited after KCC Corporation absorbed Momentive, cementing in-house supply security.

North America maintains the second-largest consumption bloc, supported by its aviation, space, and defence sectors, plus shale and offshore operators that prefer premium materials. The fluorosilicone market size in the region is anchored by FAA and DoD certifications, which lock in long replacement cycles. Automotive demand is stable rather than stellar, hampered by cost-down targets, yet the shift to battery-electric trucks creates new thermal-interface and dielectric-fluid opportunities. Canadian oil sands push service temperatures high enough to justify fluorosilicone over FKM, extending regional demand into energy.

Europe faces the most intricate regulatory climate. Draft PFAS restrictions under REACH tighten reporting and substitution requirements, but carve-out exemptions exist for aerospace, medical, and critical energy infrastructure. German OEMs continue to fit fluorosilicone hoses on bio-fuel-capable engines, and French nuclear facilities keep using radiation-hard grades. Nordic countries explore recycled silicone loops that break down polymer chains into reusable monomers, a pathway for circularity that could stabilise long-term supply. Overall, European consumption grows slowly yet shifts toward sustainable, low-fluoro content designs, a niche that local producers are well placed to serve.

Competitive Landscape

The fluorosilicone market exhibits moderate concentration with established players leveraging technical expertise and manufacturing scale to maintain competitive positions, while regulatory pressures surrounding PFAS create opportunities for specialized formulations and sustainable alternatives. Wacker Chemie AG bolstered its "in-region-for-region" strategy by completing a specialty silicone facility in Zhangjiagang in 2025, enabling quicker turnarounds for Asian electronics and cosmetics clients. While Shin-Etsu Silicones carves out a robust presence in aerospace, DuPont zeroes in on ultra-high-purity perfluoroelastomer solutions, aiming to complement rather than duplicate fluorosilicone offerings.

Patent filings indicate a shift towards catalytic depolymerisation for recycling post-industrial scrap, hinting at preparations for take-back initiatives. Supply risks are concentrated on the trifluoropropyl monomer chain; in response, some converters are securing multi-year offtake agreements with Daikin and select smaller Chinese manufacturers.

Fluorosilicone Industry Leaders

Dow

Wacker Chemie AG

Momentive Performance Materials (KCC Corporation)

3M

Shin-Etsu Silicones of America, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Wacker Chemie AG commissioned a new state-of-the-art specialty silicone manufacturing facility in Zhangjiagang, China. This facility is designed to enhance the company's production capabilities for silicone fluids, emulsions, and elastomer gels, including fluorosilicones, as part of its broader strategy to strengthen its presence and meet growing regional demand in the Asia-Pacific market.

- July 2024: Momentive Performance Materials, now operating under the ownership of KCC, announced plans to expand its fluorosilicone production capacity in Europe. This initiative aims to address the increasing demand for fluorosilicones within the automotive industry, driven by advancements in automotive technologies and materials.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the fluorosilicone market as every commercial-grade material, elastomers, antifoams, specialty coatings, adhesives, sealants, and release fluids, whose backbone is a trifluoropropyl-substituted polysiloxane that offers combined fuel, oil, and high-temperature resistance. The assessment spans raw polymer through finished compounds and molded parts that reach end users in transportation, aerospace, oil and gas, electronics, and general industrial maintenance.

Scope exclusion: laboratory reagents, research-only oligomers, and short-lifecycle consumer cosmetics remain outside this sizing.

Segmentation Overview

- By Product Type

- Elastomer

- Adhesives and Sealants

- Antifoams

- Coating

- Other Product Types (Lubricants, etc.)

- By End-user Industry

- Oil and Gas

- Automotive

- Aerospace and Defence

- Other End-user Industries (Industrial OEM, etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Interviews were held with procurement managers at gasket molders, aviation MRO engineers, silicone formulators across Asia-Pacific, Europe, and North America, and distributors covering fuel-system parts. Their insights on average selling prices, spec-in lead times, and regional qualification cycles filled several data gaps and validated secondary assumptions.

Desk Research

Our analysts first mapped the supply pool with customs trade codes for fluorosilicone elastomers, U.S. ITC and Eurostat import data, and production disclosures posted by chemical makers in annual 10-K filings. Industry associations such as the International Rubber Study Group, the German Rubber Manufacturers Association, and ASTM material databases provided baseline demand clues. Government statistics on aircraft deliveries, light-vehicle turbocharger installations, and upstream oil-tool counts supplied end-use multipliers. Premium datasets from D&B Hoovers and Dow Jones Factiva supplemented company revenues and capacity plans. Many other public and proprietary touchpoints were tapped; the list above is illustrative, not exhaustive.

Market-Sizing & Forecasting

The model begins with a top-down reconstruction of global fluorosilicone output using production and trade tonnage, which is then layered with price bands reported by buyers and sellers. Results are cross-checked through selective bottom-up tallies such as sampled supplier revenues and channel checks. Key variables include commercial jet backlog, light-vehicle turbo penetration, average fluorosilicone price per kilogram, offshore drilling rig count, and semiconductor equipment shipments; each variable carries a weight reflecting its share in elastomer, fluid, or coating demand. Forecasts employ a multivariate regression that links those drivers to base-year tonnage before scenario testing low- and high-adoption cases. Where bottom-up evidence trails the headline figure, adjustment factors derived from primary interviews bridge the gap.

Data Validation & Update Cycle

Outputs pass anomaly checks against independent market signals, after which senior reviewers vet year-on-year shifts. Reports refresh every twelve months and are fast-tracked for interim events such as major capacity additions or regulation changes. A final analyst sweep just before delivery ensures you receive the latest calibrated view.

Why Mordor's Fluorosilicone Baseline Commands Reliability

Published figures often diverge because firms define the material slate differently, anchor prices to varying grade mixes, or refresh data on unequal cadences.

Key gap drivers include scope breadth (Mordor covers fluids and release coatings many publishers omit), our use of real-time average selling prices versus fixed historical averages, and an annual update cycle that absorbs currency swings and new PFAS rulings before others react.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.1 billion (2025) | Mordor Intelligence | - |

| USD 285 million (2025) | Global Consultancy A | Omits antifoam and release-coating segments, relies on 2023 price deck |

| USD 214 million (2024) | Trade Journal B | Uses conservative aerospace outlook and static currency conversion |

The comparison shows that when the full value chain is counted and live pricing is applied, the fluorosilicone market is materially larger than narrower estimates. That disciplined approach makes Mordor Intelligence a dependable baseline for tactical planning and long-term investment decisions.

Key Questions Answered in the Report

What is the current size of the fluorosilicone market?

The fluorosilicone market size stood at 32.63 kilotons in 2026 and is projected to reach 41.12 kilotons by 2031 at a 4.74% CAGR.

Which segment holds the largest share of the fluorosilicone market?

Elastomers commanded 46.55% fluorosilicone market share in 2025 due to their adaptability across aerospace, automotive, and oil-and-gas sealing duties.

Why is Asia-Pacific the fastest-growing region?

Asia-Pacific benefits from concentrated automotive, electronics, and chemical production capacity, translating into a regional CAGR of 6.55% through 2031 backed by supportive industrial policies.

How do PFAS regulations influence demand?

Tighter PFAS rules restrict some fluoropolymer uses but simultaneously steer designers toward fluorosilicone as a compliant substitute in fuel systems, EV cooling loops, and flexible electronics.

Page last updated on: