Africa Fluoropolymer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

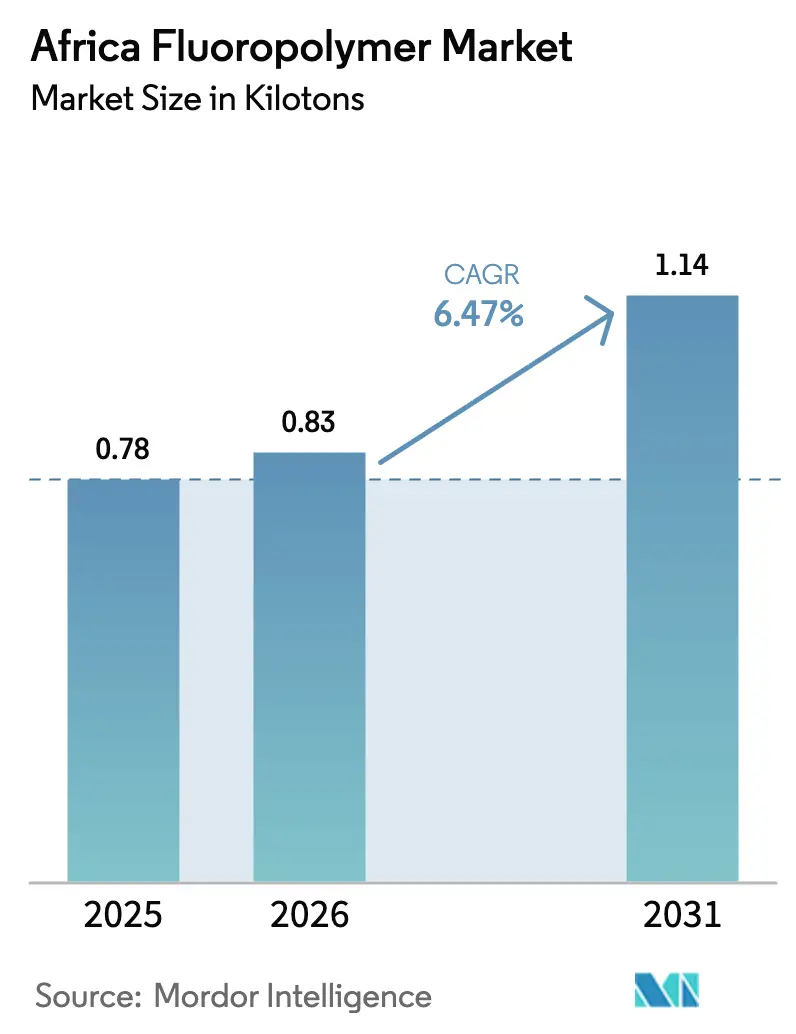

| Base Year Market Size (2025) | 0.78 kilotons |

| Market Volume (2026) | 0.83 kilotons |

| Market Volume (2031) | 1.14 kilotons |

| Growth Rate (2026 - 2031) | 6.47% CAGR |

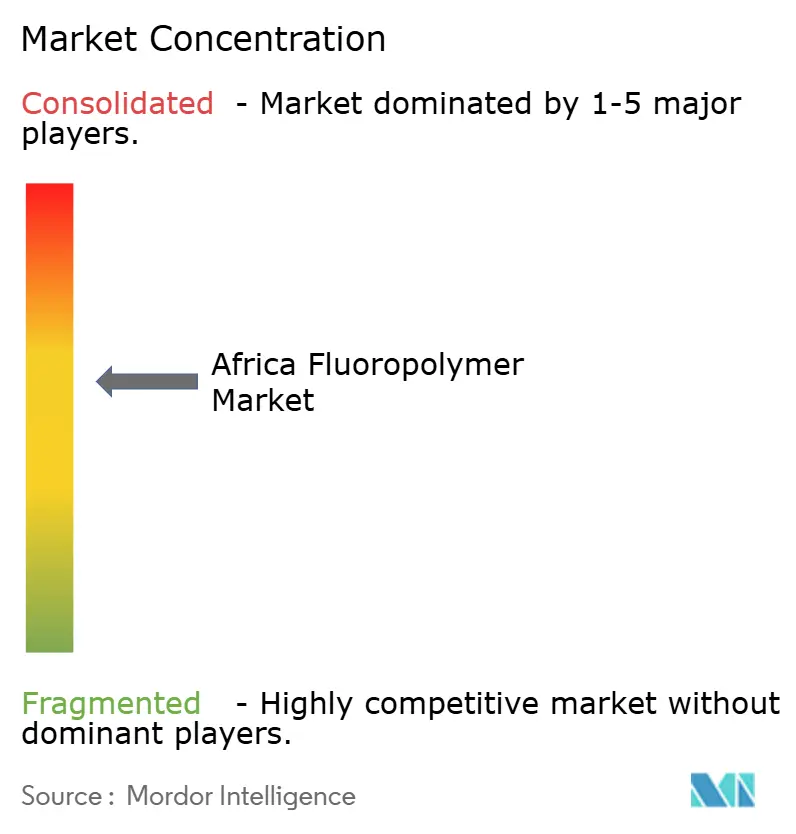

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Fluoropolymer Market Analysis by Mordor Intelligence

The Africa Fluoropolymer Market size was valued at 0.78 kilotons in 2025 and estimated to grow from 0.83 kilotons in 2026 to reach 1.14 kilotons by 2031, at a CAGR of 6.47% during the forecast period (2026-2031). Sustained infrastructure spending, accelerating electronics manufacturing, and renewed energy-sector investment are the pillars that keep the Africa fluoropolymers market on an expansionary path. South Africa remains the anchor geography, yet momentum spreads to West and East Africa as telecom carriers roll out 5G, solar developers broaden mini-grid footprints, and offshore operators advance gas megaprojects. Currency swings and import dependency temper near-term sentiment, but project pipelines, supportive trade policies, and gradual local processing upgrades continue to attract global suppliers into the Africa fluoropolymers market. Intensifying regulatory scrutiny around PFAS and EU F-gas rules simultaneously raises compliance costs and stimulates demand for advanced low-emission grades, steering future growth toward higher-margin specialty products across the Africa fluoropolymers market.

Key Report Takeaways

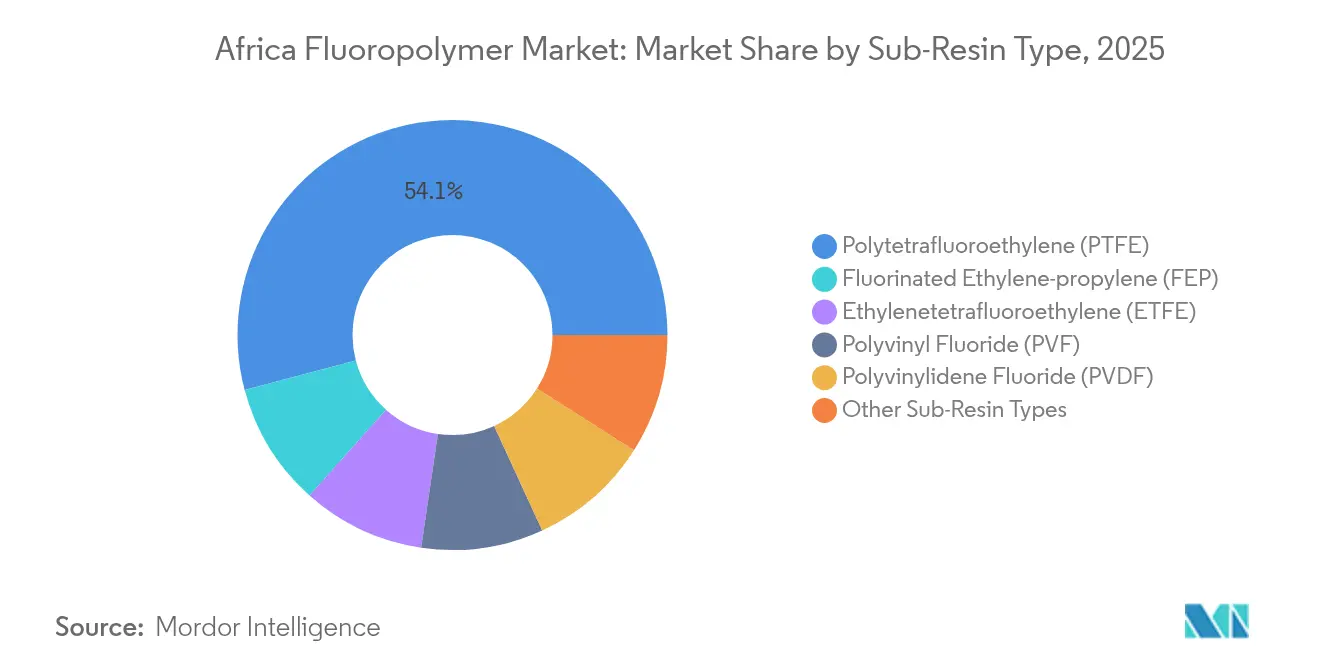

- By sub-resin type, Polytetrafluoroethylene (PTFE) captured 54.12% of Africa Fluoropolymers market share in 2025, whereas Fluorinated Ethylene-propylene (FEP) is projected to grow at a 7.65% CAGR through 2031.

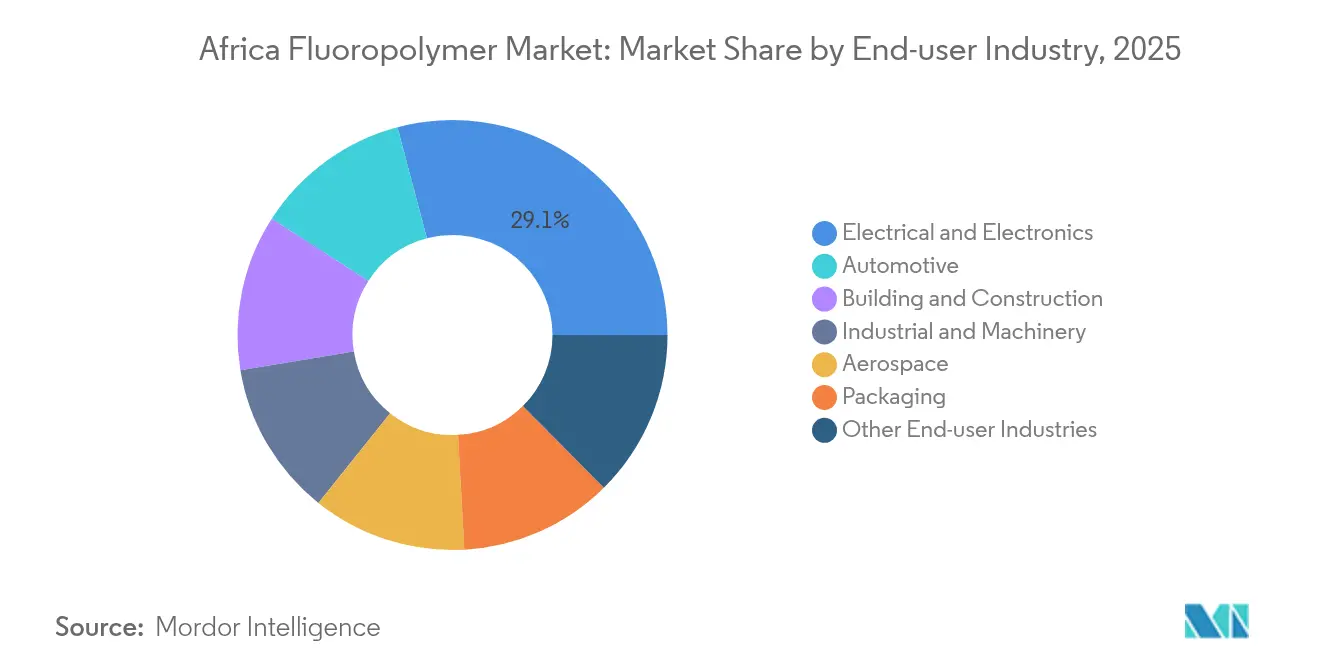

- By end-user industry, the electrical and electronics segment commanded 29.12% of the Africa Fluoropolymers market size in 2025, while the diverse “other industries” segment is projected to advance at a 7.41% CAGR to 2031.

- By geography, South Africa accounted for 56.78% of the Africa Fluoropolymers market size in 2025 and is progressing at a 6.62% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Fluoropolymer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid infrastructure build-out fuelling demand for weather-resistant coatings | +1.5% | South Africa, Nigeria, Ghana | Medium term (2-4 years) |

| Growing regional auto production boosting high-performance seal usage | +1.8% | South Africa, Morocco, Nigeria | Medium term (2-4 years) |

| 5G rollout increasing need for low-loss dielectric materials | +1.2% | South Africa, Nigeria, Kenya | Short term (≤ 2 years) |

| Offshore gas projects adopting PVDF/ETFE umbilicals | +0.9% | West Africa, Angola, Mozambique | Long term (≥ 4 years) |

| Mini-grid solar farms using fluoropolymer back-sheets | +0.7% | Global, with concentration in East Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Infrastructure Build-out Fuelling Demand for Weather-Resistant Coatings

Across Africa, multibillion-dollar petrochemical complexes, ports, highways, and smart-city precincts specify fluorinated coatings that withstand ultraviolet radiation, salt spray, and cyclic temperature extremes. Ghana’s USD 60 billion refinery-to-petrochemicals hub leads this wave, with architects and EPC contractors mandating PVDF or ETFE topcoats to guarantee 25-year façade performance[1]BASF Editorial Team, “Ultra-Durable Coatings for Harsh Climates,” basf.com. New power plants, onshore LNG terminals, and transcontinental railway corridors reflect this specification trend, securing continuous demand for high-durability fluoropolymers well beyond initial construction cycles. Rising insurance requirements further reinforce the preference, as project financiers increasingly insist on long-life materials to mitigate risks to their maintenance budgets. The multiplier effect extends to local fabricators of cladding panels, cable trays, and fasteners, all of whom source resin-rich powders and films, embedding additional volume into the Africa fluoropolymers market.

Growing Regional Auto Production Boosting High-Performance Seal Usage

Africa’s vehicle assembly volumes continue to rise, driven by preferential trade zones, new component clusters, and increasing middle-class car ownership. South African OEMs, which already export two-thirds of their output, have increased purchase orders for PTFE and FKM gaskets that withstand aggressive fuels and elevated under-hood temperatures. Moroccan plants focused on compact SUV exports follow suit, while Nigerian joint ventures leverage tariff incentives to localize fuel system subcomponents. As Euro 6-equivalent emission standards phase in, automakers deploy thinner yet more robust seals, raising per-vehicle fluoropolymer intensity. Early electric-vehicle pilot lines also select PVDF binders for lithium-ion battery electrodes, signaling a new layer of resin consumption that extends across charging infrastructure, where ETFE-insulated high-voltage cables are rapidly becoming the standard.

5G Rollout Increasing Need for Low-Loss Dielectric Materials

Telecom carriers in South Africa, Nigeria, and Kenya collectively earmarked more than USD 3 billion for 5G base-station equipment in 2024, accelerating the adoption of FEP and PFA for low-loss microwave cables. Millimeter-wave antennas operate at power-efficiency limits, prompting tower integrators to insist on dielectric materials with stable permittivity up to 35 GHz. Each macro site integrates hundreds of meters of fluoropolymer-jacketed coax, and densification strategies multiply node counts through thousands of small-cell deployments. Packet-core vendors report surging demand for PTFE circuit-board laminates that maintain signal integrity inside edge-compute servers, embedding incremental kilograms of resin in every data-center rack. The connectivity uplift subsequently stimulates fintech, e-health, and cloud-manufacturing services, each layering new fluoropolymer-reliant hardware into national networks.

Offshore Gas Projects Adopting PVDF/ETFE Umbilicals

TechnipFMC logged USD 829.6 million of subsea revenue from Angola alone in 2024, underscoring how deepwater E&P programs elevate demand for chemically inert umbilicals[2]TechnipFMC Investor Relations, “2024 Annual Report,” technipfmc.com. High-pressure PVDF liners, combined with abrasion-resistant ETFE outer sheaths, ensure integrity over 20-year design windows at depths exceeding 2,000 m. Mozambique’s Rovuma Basin and Senegal’s Sangomar field replicate these material profiles, embedding multiple tonnes of specialty fluoropolymers into every kilometer of composite conduit. Lifecycle service contracts further boost consumption as operators stock spare lengths and retrofit additional tie-backs that must match original material specifications. Importantly, successful field performance builds local confidence, prompting EPC contractors to extend the use of fluoropolymers into ancillary jumpers, downhole control lines, and topside chemical-injection tubing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency swings inflating import prices | -0.80% | Continental Africa, particularly import-dependent economies | Short term (≤ 2 years) |

| EU F-gas rules tightening export markets | -1.10% | Global, affecting African suppliers and importers | Medium term (2-4 years) |

| Weak recycling ecosystem triggering environmental push-back | -0.60% | South Africa, Nigeria, urban centers across Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Currency Swings Inflating Import Prices

Sharp exchange-rate fluctuations against the US dollar raise landed costs by double-digit percentages within weeks, forcing distributors to renegotiate contracts or absorb margin erosion. African Development Bank research shows that 56% of investors rank currency risk as their top hurdle, an assessment mirrored in capital expenditure delays for large-scale chemical projects. Smaller fabricators often lack hedge facilities, so they trim inventory, inadvertently elongating lead times for OEMs that need just-in-time fluoropolymer components. Financing costs, averaging 11.6% across the region, exacerbate stress because letters of credit price in additional risk premiums. Resultant purchase deferrals compress quarterly offtake, creating forecasting unpredictability that ripples back to exporters and marine shippers.

EU F-Gas Rules Tightening Export Markets

Regulation 2024/573 mandates progressive quota cuts on fluorinated substances, capping European imports of high-GWP products and compelling equipment makers to certify ultra-low residual PFAS levels. African converters that embed fluoropolymers into refrigeration lines or industrial hoses destined for EU customers now bear the burden of compliance audits, sampling charges, and documentary proof of traceability. Engineering change orders cascade through supply chains, extending design cycles and raising qualification costs. Some firms pivot toward domestic or Middle-East buyers, but economies of scale shrink, nudging unit prices upward and eroding competitiveness. Over the medium term, suppliers able to shift their portfolios toward melt-processable, low-emission grades stand to offset lost volumes, but transitional frictions weigh on the overall CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub-Resin Type: PTFE Dominance Faces Specialty Grade Pressure

PTFE supplied 54.12% of Africa Fluoropolymers market share in 2025, owing to its entrenched role in chemical-process gaskets, slurry pump liners, and conveyor belting. The Africa fluoropolymers market size linked to PTFE alone stood at 0.42 kilo tons that year. Price competition from East Asian producers has trimmed margins, yet users value global qualification certificates that minimize downtime in mining and refining operations. FEP, though starting from a smaller base, advances at a 7.65% CAGR, powered by telecom coax assemblies, aerospace wire harnesses, and inkjet printheads that require oxygen-plasma cleanability. PVDF volumes track offshore engineering schedules and solar rollouts, while PVF secures incremental wins in architectural films used to adorn stadium roofs and airport facades.

Commodity-grade PTFE faces substitution when tighter tolerances, lower permeability, or faster extrusion cycles are paramount. Hence, compounders pitch modified PTFE loaded with nano-fillers, whereas multinational suppliers promote ultra-pure PFA to semiconductor fabs in South Africa’s Western Cape. Fluoroelastomers, notably FKM and new-to-region FFKM, win share in acid-service valves and critical O-ring kits for diamond-processing autoclaves. Collectively, specialty streams lift average selling prices, partially hedging importers against foreign-exchange headwinds. Local recyclers, though nascent, explore melt-filtered PTFE regrind for non-critical sheet goods, hinting at future circular-economy tailwinds within the Africa fluoropolymers market.

By End-User Industry: Electronics Leadership Amid Diversifying Applications

The electrical and electronics sector absorbed 29.12% of Africa Fluoropolymers market size in 2025 as smartphone assembly, set-top box production, and fiber-optic cable plants expanded. In circuit boards, PTFE-glass laminates enable high-frequency RF front-ends, while FEP jackets dominate plenum-rated network cabling for hyperscale data centers. Semiconductor tool importers specify PFA spray tanks and PVDF pumps to handle ultra-pure chemicals, reinforcing steady offtake irrespective of consumer-device cycles.

Other industries, a catch-all category ranging from solar OEMs through specialty food-processing lines, post the fastest 7.41% CAGR. Photovoltaic back-sheet fabricators line up repeat orders for PVDF film, whereas mineral-processing plants opt for PTFE for cyclone liners that resist the hydrofluoric acid found in rare-earth ore leachates. Automotive brake-hose suppliers integrate FKM liners to meet new vapor-permeation norms, and desalination-plant EPC contractors adopt PVDF cartridges in ultrafiltration skids. The application map thus broadens every year, diffusing volume risk and strengthening the structural resilience of the Africa fluoropolymers market.

Geography Analysis

South Africa generated 56.78% of the Africa Fluoropolymers market size in 2025. Government-mandated PFOS/PFOA phase-outs, effective December 2021, led to swift substitution toward compliant grades, resulting in a 9% reduction in specialty resin imports. Meanwhile, domestic flake recycling trials target construction membranes, positioning local firms for future circular-procurement tenders.

Nigeria ranks second in volume and opportunity. Telecom operators accelerate 5G rollouts across Lagos, Abuja, and Port Harcourt, adding hundreds of small-cell sites that each integrate meters of fluoropolymer-insulated coax. On the downside, the naira's weakness frequently prompts mid-tier contractors to delay resin purchases, resulting in uneven quarterly demand. Yet offshore tie-backs at Bonga SW and Owowo drive PVDF umbilical call-offs, balancing the domestic consumption ledger.

The rest of Africa comprises a mosaic of niche yet rapidly scaling applications. Ghana’s megaproject pipeline alone could translate into tens of thousands of square meters of PVDF-coated structural steel once financial close is secured. East African mini-grids, spearheaded by rural electrification agencies, commission containerized solar and storage systems that embed fluoropolymers in both photovoltaic encapsulants and lithium-battery separators.

Competitive Landscape

The Africa Fluoropolymer Market is moderately concentrated. Global majors such as Arkema, Chemours, Daikin, and Solvay dominate the Africa fluoropolymers market through dedicated regional distributors rather than on-continent polymerization. Collaborative ventures with global suppliers could unlock downstream expansion, but they hinge on reliable power, skilled labor, and stable policy frameworks. Until these gaps close, the Africa Fluoropolymers market will continue to rely on well-capitalized foreign incumbents capable of absorbing currency fluctuations, navigating compliance audits, and stockpiling multi-grade inventories across several coastal free-trade zones.

Africa Fluoropolymer Industry Leaders

Arkema

Dongyue Group

Gujarat Fluorochemicals Limited (GFL)

Solvay

The Chemours Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Syensqo launched a new medical-grade Solef polyvinylidene fluoride (PVDF) designed for advanced healthcare and biopharmaceutical applications. This new grade is commercially available worldwide, including countries in Africa. This PVDF combines the properties requirements for reliable use in biopharmaceutical processing and medical applications.

- July 2025: AGC Inc., a supplier of fluoropolymers in Africa, unveiled its latest offerings in its AFLAS FFKM series of fluoroelastomers: the surfactant-free and fluorinated polymerization solvent-free "SF grades." These products are crafted entirely without surfactants or fluorinated polymerization solvents. They can address the rising market demand for eco-friendlier fluoroelastomers.

Africa Fluoropolymer Market Report Scope

Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery are covered as segments by End User Industry. Ethylenetetrafluoroethylene (ETFE), Fluorinated Ethylene-propylene (FEP), Polytetrafluoroethylene (PTFE), Polyvinylfluoride (PVF), Polyvinylidene Fluoride (PVDF) are covered as segments by Sub Resin Type. Nigeria, South Africa are covered as segments by Country.| Ethylenetetrafluoroethylene (ETFE) |

| Fluorinated Ethylene-propylene (FEP) |

| Polytetrafluoroethylene (PTFE) |

| Polyvinyl Fluoride (PVF) |

| Polyvinylidene Fluoride (PVDF) |

| Other Sub-Resin Types |

| Aerospace |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Packaging |

| Other End-user Industries |

| Nigeria |

| South Africa |

| Rest of Africa |

| By Sub-Resin Type | Ethylenetetrafluoroethylene (ETFE) |

| Fluorinated Ethylene-propylene (FEP) | |

| Polytetrafluoroethylene (PTFE) | |

| Polyvinyl Fluoride (PVF) | |

| Polyvinylidene Fluoride (PVDF) | |

| Other Sub-Resin Types | |

| By End-User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Packaging | |

| Other End-user Industries | |

| By Geography | Nigeria |

| South Africa | |

| Rest of Africa |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the fluoropolymers market.

- Resin - Under the scope of the study, virgin fluoropolymer resins like Polytetrafluoroethylene, Polyvinylidene Fluoride, Polyvinylfluoride, Fluorinated Ethylene-propylene, Ethylenetetrafluoroethylene, etc. in the primary forms are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms