Perfluoroalkoxy Alkane (PFA) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

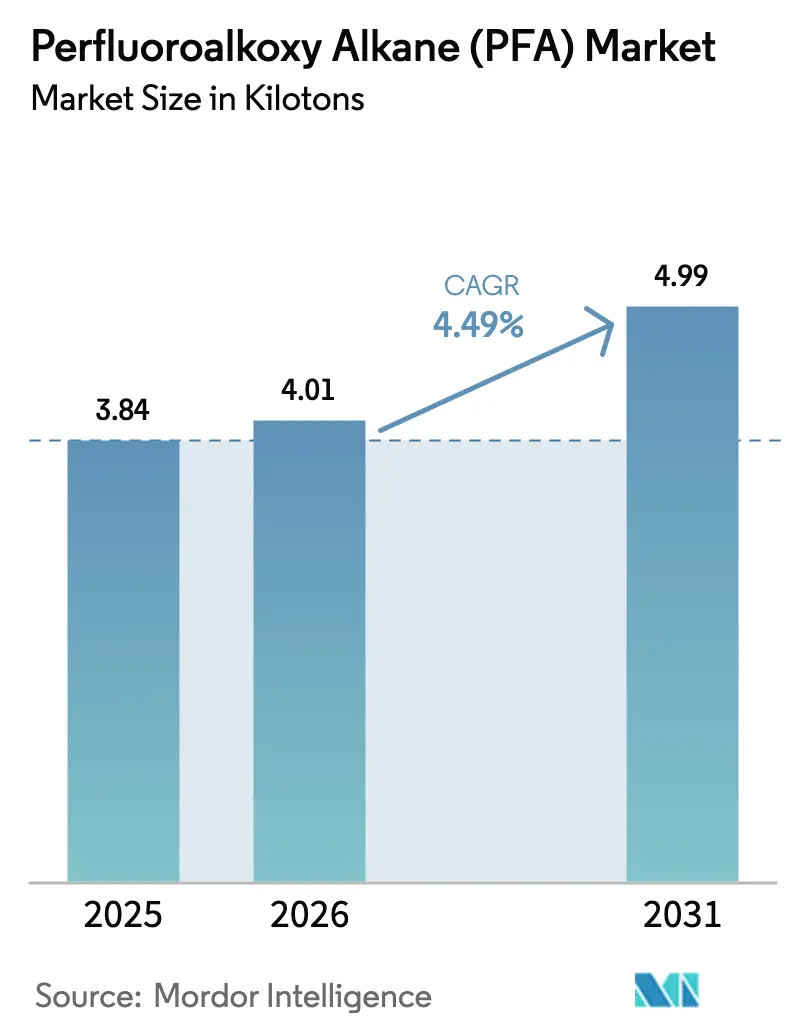

| Market Volume (2026) | 4.01 kilotons |

| Market Volume (2031) | 4.99 kilotons |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

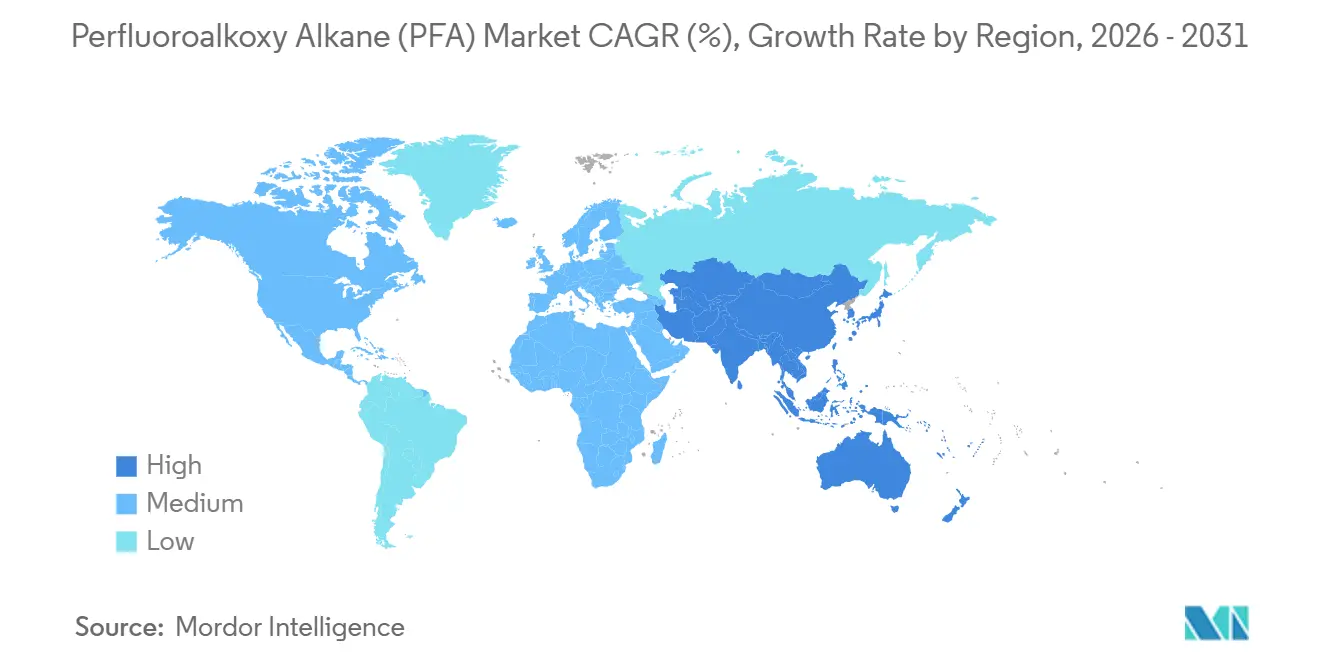

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

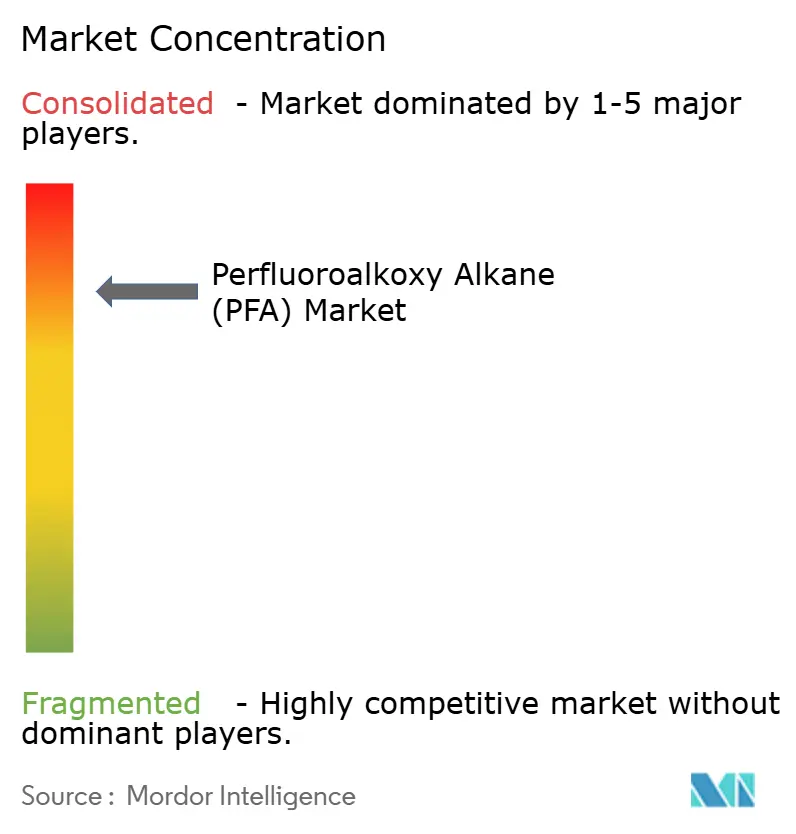

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Perfluoroalkoxy Alkane (PFA) Market Analysis by Mordor Intelligence

The Perfluoroalkoxy Alkane Market size is expected to increase from 3.84 kilotons in 2025 to 4.01 kilotons in 2026 and reach 4.99 kilotons by 2031, growing at a CAGR of 4.49% over 2026-2031. Demand resiliency is anchored in the polymer’s non-negotiable role within ultrapure fluid-handling loops inside sub-3-nanometer semiconductor fabs, specialty chemical reactors, and high-voltage electrical systems. Equipment makers continue to specify PFA-lined components because trace ionic contamination in advanced nodes can wipe out yields worth millions of U.S. dollars, even as regulators tighten per- and polyfluoroalkyl substances (PFAS) rules across North America and Europe. Capacity expansions by Chemours in West Virginia and Daikin in Japan temper supply risk, yet lead times for reactor-grade resin still stretch beyond 12 months when foundries launch simultaneous greenfield projects. Meanwhile, Asia-Pacific’s semiconductor build-out, North American petrochemical revamps, and European 5G densification collectively create multi-regional pull for the perfluoroalkoxy alkane market, balancing the drag from cookware bans and emerging non-fluorinated substitutes.

Key Report Takeaways

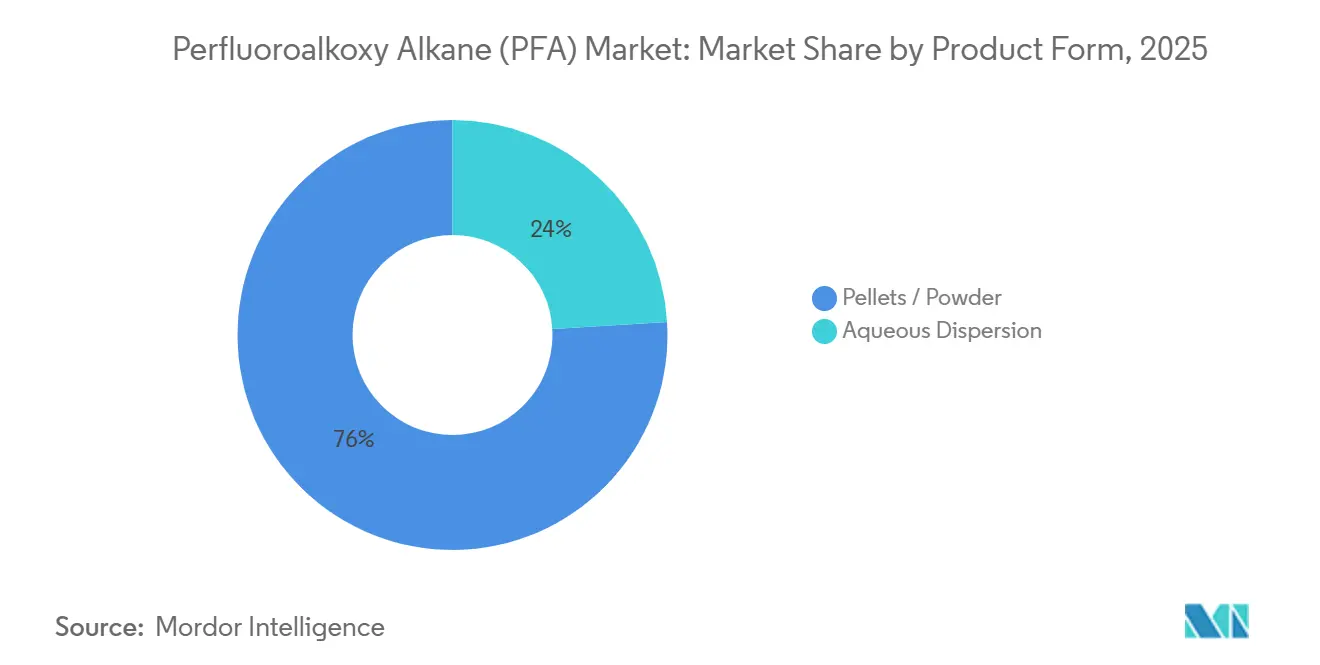

- By product form, pellets and powder led with 75.97% of the Perfluoroalkoxy Alkane market share in 2025, and the segment is forecast to expand at a 4.96% CAGR through 2031.

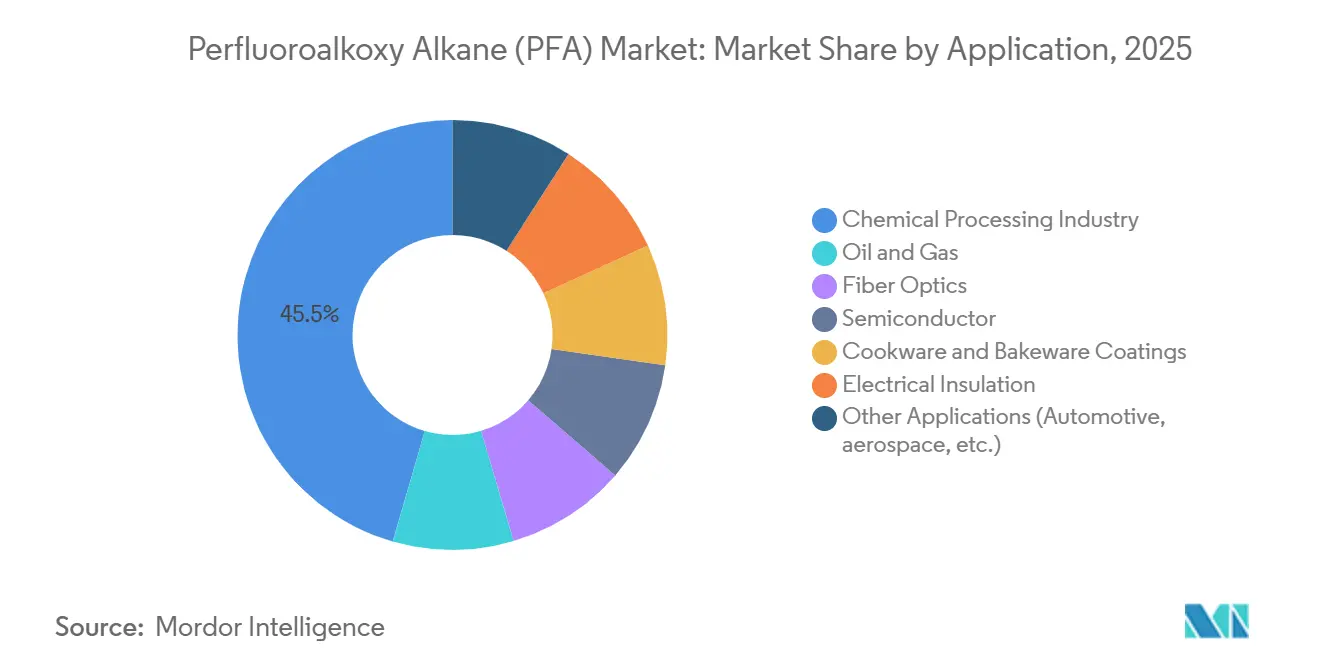

- By application, chemical processing accounted for 45.51% of the Perfluoroalkoxy Alkane market size in 2025, while electrical insulation is advancing at a 4.89% CAGR through 2031.

- By geography, Asia-Pacific held 40.02% revenue share in 2025 and is projected to grow at a 4.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Perfluoroalkoxy Alkane (PFA) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultrapure PFA tubing demand surge in advanced semiconductor fabs | +1.2% | Asia-Pacific core, spillover to North America and Europe | Medium term (2-4 years) |

| Corrosion-resistant linings for next-gen chemical processing plants | +1.0% | Global, with concentration in Asia-Pacific and North America | Long term (≥ 4 years) |

| Integrity-critical PFA tubing in deep-water and sour-service oil-and-gas | +0.8% | South America (Brazil pre-salt), North America (Gulf of Mexico), Middle East | Medium term (2-4 years) |

| Growing use of PFA in lithium-ion batteries | +0.7% | Asia-Pacific dominance, emerging in Europe and North America | Long term (≥ 4 years) |

| 5G-driven fiber-optic cable jacketing expansion | +0.6% | Global, with early gains in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ultrapure PFA Tubing Demand Surge in Advanced Semiconductor Fabs

Foundries running 3-nanometer and below processes consume roughly 0.5 kg of PFA tubing per square foot of cleanroom, translating to 300 metric tons for a single 600,000-square-foot mega-fab[1]National Institute of Standards and Technology, “Cleanroom Polymer Requirements for Next-Generation Fabs,” nist.gov. TSMC’s multibillion-dollar projects in Arizona and Kumamoto elevate immediate call-offs for semiconductor-grade PFA that withstands aggressive photoresist solvents without leaching ionic species. Japanese and Korean fabs reduce logistics risk by sourcing from regional producers such as Daikin and AGC, yet Chemours’ U.S. line secures domestic-content compliance under CHIPS Act rules. Extreme ultraviolet lithography ups purity thresholds, driving 12-month order backlogs during peak expansion cycles. These dynamics keep the Perfluoroalkoxy Alkane market tightly balanced despite regulatory headwinds.

Corrosion-Resistant Linings for Next-Gen Chemical Processing Plants

PFA linings operate reliably in concentrated sulfuric acid at 200 °C, chlorine trifluoride, and bromine pentafluoride, where stainless steel fails, eliminating the weld seams that trigger stress cracking. Melt-processability enables seamless liners, reducing downtime in pharmaceutical and fluorochemical reactors. Gujarat Fluorochemicals’ investment into higher-grade PFA for wet-etch systems signals vertical integration and rising Asian competition. Operators also specify PFA to curtail trace-metal contamination that can poison catalysts, elevating the polymer from commodity to critical process enabler. Long equipment lifecycles lock in demand for decades.

Integrity-Critical PFA Tubing in Deep-Water and Sour-Service Oil-and-Gas

Petrobras’ pre-salt output hit 2.2 million b/d in December 2024, and each new FPSO requires kilometers of PFA-lined tubing to survive hydrogen sulfide levels above 10,000 ppm. TechnipFMC subsea contracts across the Gulf of Mexico reinforce the material’s role where equipment retrieval costs exceed USD 10 million per intervention. PFA’s low friction eases hydraulic control over 3,000-meter water depths, allowing smaller topside pumps and cutting capex. As fields age and chemical injection intensifies, installed PFA umbilicals create captive replacement demand that underpins the Perfluoroalkoxy Alkane market.

Growing Use of PFA in Lithium-Ion Batteries

Syensqo’s USD 850 million PVDF complex and Gujarat Fluorochemicals’ battery-grade binder program illustrate fluoropolymer pivot toward energy storage. PFA’s niche lies in gaskets resisting LiPF6 electrolyte degradation at elevated temperatures; Daikin’s NEOFLON grades maintain compression set during 1000-hour soak tests. Dry-electrode coating reduces PVDF demand yet heightens seal integrity needs, magnifying PFA value. Battery gigafactories often co-locate with chip fabs, letting suppliers run shared high-purity resin lines and reinforcing regional volume for the Perfluoroalkoxy Alkane market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening global PFAS regulatory scrutiny | -0.9% | North America and EU primary, spillover to Asia-Pacific | Short term (≤ 2 years) |

| OEM migration toward non-fluorinated alternatives | -0.6% | Europe and North America lead, Asia-Pacific follows | Medium term (2-4 years) |

| End-of-life recycling gap hindering circular-economy targets | -0.4% | Global, with acute pressure in EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Global PFAS Regulatory Scrutiny

The U.S. EPA’s October 2024 test orders on 6:2 fluorotelomer acrylate copolymer and the delayed PFAS reporting rule to July 2025 inject compliance uncertainty for producers[2]U.S. Environmental Protection Agency, “PFAS Test Orders October 2024,” epa.gov. California’s AB 1200 cookware ban (January 2025) and Maine’s LD 1537 PFAS prohibition by 2030 fracture the North American market into state-specific grades. Europe’s PFHxA ban, effective April 2026, plus ECHA’s sweeping PFAS proposal, threaten to reclassify PFA outside the essential-use carve-out. Chemours’ USD 592 million water-system settlement exposes the financial risk even for incumbents. These developments temper investment appetite and trim near-term growth for the Perfluoroalkoxy Alkane market.

OEM Migration Toward Non-Fluorinated Alternatives

Consumer backlash fuels “PFAS-free” marketing despite performance compromises; brands such as Caraway and Great Jones shifted to non-fluorinated cookware coatings after U.S. media coverage. Semiconductor tools and chemical reactors have higher qualification hurdles, yet OEMs now test polyether ether ketone (PEEK) for sub-200 °C duties. Alternative polymers lag PFA on permeation resistance and dielectric strength, keeping substitution marginal through 2028. Nonetheless, procurement teams increasingly weigh regulatory simplicity over technical parity, moderating long-horizon demand within the Perfluoroalkoxy Alkane market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Pellets Dominate Melt-Processing Shift

Pellets and Powder captured 75.97% of 2025 volume, underscoring their central role in melt extrusion lines that produce semiconductor micro-tubing with ±0.05 mm inner-diameter tolerances. This dominant share of the Perfluoroalkoxy Alkane market stems from pellet-grade resin viscosity near 10^4 poise at 380 °C, enabling high-speed extrusion that slashes per-meter costs by up to 40% versus dispersion coating. Chemours’ USD 200 million expansion in West Virginia is adding pellet capacity integrated with TFE and PPVE monomer units, giving supply certainty to U.S. fabs.

Growth momentum stays with pellets through 2031, advancing at a 4.96% CAGR as chipmakers and battery plants scale kilometers of ultrapure tubing. Conversely, Aqueous Dispersion retains a foothold in spray-coated pump bodies and irregular reactor internals yet faces tightening PFAS surfactant rules that inflate formulation costs in Europe. Powder grades remain niche for rotational molding in offshore valve components where extreme corrosion undermines metals. The migration toward melt-processing, therefore, cements pellets at the center of the Perfluoroalkoxy Alkane market narrative.

By Application: Chemical Processing Anchors Demand, Electrical Insulation Accelerates

Chemical Processing commanded 45.51% of 2025 demand, reflecting entrenched use of PFA linings in reactors handling concentrated acids and halogenated solvents at up to 260 °C. High switching costs—downtime of up to six weeks and USD 300,000 for re-lining a 10,000-liter vessel—preserve incumbency and generate steady replacement cycles. The Perfluoroalkoxy Alkane market size for Chemical Processing is forecast to maintain mid-single-digit expansion as specialty chemical output localizes across Asia and the United States.

Electrical Insulation posts the fastest 4.89% CAGR to 2031 on the back of offshore wind arrays, 5G densification, and electric-vehicle harness upgrades. IEEE Standard 1829-2024 codifies UV-aging protocols that favor PFA over polyethylene for high-voltage outdoor insulators. Fiber-optic cables with 288 fibers rely on thin-wall PFA jacketing to cut wind loading, while EV platforms exploit the polymer’s 20 kV/mm dielectric strength in compact power electronics. These trends propel incremental high-margin volume that lifts the broader Perfluoroalkoxy Alkane market.

Geography Analysis

Asia-Pacific accounted for 40.02% of global volume in 2025 and is tracking a 4.67% CAGR to 2031, thanks to unabated semiconductor capex across Taiwan, Japan, and South Korea. China’s self-sufficiency program and India’s Gujarat Fluorochemicals push into semiconductor-grade PFA add regional production heft. Integrated supply reduces freight risk, giving local fabricators price and lead-time advantages over transoceanic shipments. Southeast Asian petrochemical expansions layer additional corrosion-lining demand, reinforcing the Perfluoroalkoxy Alkane market presence throughout the region.

North America benefits from Chemours’ sole domestic line and CHIPS Act content conditions that anchor regional sourcing for Arizona, Ohio, and Texas fabs. However, California’s AB 1200 cookware ban and the EPA’s data-call-ins fragment formulations and raise compliance costs. Canada and Mexico add moderate volumes via chemical plants and deepwater Gulf projects. The regulatory patchwork tempers the Perfluoroalkoxy Alkane market expansion despite firm semiconductor demand.

Europe’s growth is capped by the April 2026 PFHxA ban and ECHA’s wider PFAS proposal, though essential-use carve-outs for semiconductors safeguard niche high-purity consumption. TSMC’s planned EUR 10 billion Dresden fab provides a new node of demand, while Germany and France maintain chemical-processing baselines. United Kingdom rules diverge post-Brexit, adding supply-chain complexity. Overall, the region’s Perfluoroalkoxy Alkane market tracks low-single-digit growth offset by policy uncertainty.

South America hinges on Petrobras’ pre-salt program; six new FPSOs through 2029 require vast PFA umbilicals resilient to 10,000 ppm H2S. Brazil drives lumpy but sizeable call-offs, whereas Argentina and Colombia contribute smaller chemical-processing volumes. Middle East and Africa witness steady demand from Saudi petrochemical debottlenecks and United Arab Emirates refinery upgrades, yet infrastructure gaps limit broader uptake. Collectively, these regions offer opportunistic but volatile pockets within the global Perfluoroalkoxy Alkane market.

Regulatory Landscape

PFA sits inside the broader PFAS regulatory perimeter, and 2026 brought new inflection points across the EU and the United States. In Europe, ECHA committees (RAC and SEAC) moved the EU-wide PFAS restriction dossier forward in March 2026 via opinions that support restriction with targeted, time-limited derogations. This keeps fluoropolymers such as PFA under direct review rather than carved out by default. At the same time, the report scope continues to reflect application-level differentiation, with essential-use arguments central for semiconductor and critical industrial fluid-handling, while consumer-facing uses face tighter scrutiny.

In the United States, EPA actions are adding compliance uncertainty on top of existing TSCA oversight and state-level product restrictions. In May 2026, EPA proposed rescinding parts of the 2024 drinking water PFAS determinations and associated standards for specific PFAS, including PFHxS, PFNA, and HFPO-DA. It underscores that regulatory obligations can shift through administrative rulemaking even as PFAS remains a priority category. Taken together with prior EPA test orders (October 2024) and a patchwork of state measures already reflected in the market, these developments keep documentation, reporting readiness, and customer qualification files as ongoing requirements for PFA producers and downstream fabricators.

Value Chain Analysis

The PFA value chain is concentrated and qualification-driven, with a clear split between upstream fluoropolymer resin producers and downstream conversion into high-spec components. Upstream producers, including Chemours, Daikin, AGC, Solvay, and emerging Chinese capacity, polymerize TFE with perfluoroalkyl vinyl ether comonomers to make PFA resins. They also tightly control trace-metal and ionic contamination for semiconductor-grade lots. Midstream processors and fabricators, including Entegris, Saint-Gobain, Zeus, and other specialized fluoropolymer houses, convert resin into tubing, liners, valves, fittings, films, and coated components. OEMs and system integrators in semiconductor, chemical processing, and energy applications then qualify parts against purity, permeation, thermal cycling, and long-life corrosion requirements.

Bottlenecks run through monomer availability, reactor-time constraints for high-purity grades, and multi-quarter qualification cycles that limit rapid supplier switching, particularly for sub-3-nanometer semiconductor fluid-handling loops. Traceability and PFAS management requirements are increasingly built into procurement, pushing more closed-loop handling, emissions monitoring, and documentation across upstream and downstream sites. The market also shows a regionalization trend, with Asia-based resin capacity and local fabrication reducing logistics risk for fabs, while North America relies heavily on Chemours domestic production to support U.S. semiconductor build-outs with shorter lead times and domestic-content alignment.

Competitive Landscape

The Perfluoroalkoxy Alkane market remains highly consolidated, with the top five players accounting for a significant market share. Daikin and AGC leverage Japanese proximity to fab clusters to protect share against rising Chinese producers. Chinese players such as Hubei Everflon and Zhejiang Juhua add low-cost capacity, but qualification barriers slow penetration into advanced nodes. Mergers and acquisitions trends favor integration. Technology focus shifts to in-line melt-viscosity monitoring and trace-metal analytics that cut scrap and fast-track wafer-fab acceptance. The competitive playbook thus mixes backward integration, regional diversification, and process analytics to defend or capture Perfluoroalkoxy Alkane market positions.

Perfluoroalkoxy Alkane (PFA) Industry Leaders

The Chemours Company

Daikin Industries Ltd.

AGC Inc.

Solvay

Gujarat Fluorochemicals Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The largest white-space sits in ultra-high-purity PFA supply chains that can clear semiconductor qualification for advanced fabs while meeting tightening PFAS governance requirements. Demand signals remain linked to the non-negotiable role of PFA in ultrapure fluid-handling loops, and the market continues to face long lead times for reactor-grade resin during clustered fab build cycles. That combination creates room for capacity paired with validated contamination control, including ion and metal reduction processes, and for downstream fabricators that can deliver consistent, documented purity across tubing, liners, and wetted assemblies used in wet-etch and chemical delivery systems.

New Asian capacity also creates an opportunity around localized sourcing for regional semiconductor and specialty chemical expansions. Yonghe Group commissioned a special fluoropolymers project in Inner Mongolia in December 2025, with industrial-scale PFA intended for high-purity pipelines and reactor uses. Established players also reinforce supply through expansions cited in the report context, including Chemours in West Virginia and Daikin in Japan. On the demand side, opportunities extend beyond fabs into integrity-critical chemical processing linings and electrical insulation programs, where qualification is performance-led rather than marketing-led, supporting premium grades even as consumer-facing PFAS restrictions tighten.

Recent Industry Developments

- May 2026: Daikin Europe N.V. inaugurated Daikin Manufacturing Poland Sp. z o.o., a new production facility in the Lodz region backed by an investment of about EUR 300 million. While centered on heat pumps, the move reflects continued large-scale industrial investment by a leading fluorochemical and fluoropolymer group. It supports European operational footprint and customer proximity as PFAS policy evolves.

- February 2025: Chemours reported that volume growth in its Advanced Performance Materials segment was supported by a capacity expansion in Teflon PFA. This signaled incremental supply availability for high-spec applications such as semiconductor manufacturing, where qualification and lead-time constraints can translate into order backlogs quickly. It also reinforced throughput headroom for purity-sensitive programs.

- July 2024: Chemours announced receiving a permit to expand production for Teflon PFA used in semiconductor manufacturing. The approval helped de-risk a critical upstream step for adding PFA capacity. It also aligned with tightening purity requirements and rising demand for ultrapure fluid-handling components in advanced fabs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers demand and supply for perfluoroalkoxy alkane (PFA) resin and its typical commercial forms that are sold into industrial and specialty-use applications where chemical resistance and high purity performance are required.

Scope exclusions: the sizing excludes downstream finished equipment value and focuses only on PFA material volumes sold into end uses.

Segmentation Overview

- By Product Form

- Aqueous Dispersion

- Pellets / Powder

- By Application

- Oil and Gas

- Chemical Processing Industry

- Fiber Optics

- Semiconductor

- Cookware and Bakeware Coatings

- Electrical Insulation

- Other Applications (Automotive, aerospace, etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Thailand

- Vietnam

- Malaysia

- Indonesia

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordic Countries

- Russia

- Turkey

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- Egypt

- South Africa

- Nigeria

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market context and to make sure our assumptions are anchored to observable indicators. We referred to public sources such as the US International Trade Commission trade data, UN Comtrade trade statistics, Eurostat industrial indicators, the US Geological Survey chemicals and materials coverage, and patent databases to track material innovation signals and process routes.

On top of that, we used company filings and investor presentations to map capacity additions, plant utilization commentary, and product mix direction for fluoropolymer portfolios. Reputed press and association websites were also reviewed to capture PFAS regulatory direction and timing, since that can shift demand across end uses faster than macro data alone suggests. For company financials and news intelligence, we also used a paid subscription database for cross-checking and time-series tracking. The sources listed here are illustrative only, and many other public and internal references were consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with resin producers, distributors, compounders, and large end users that specify PFA in chemical processing, semiconductors, and electrical insulation. We covered demand patterns across APAC, EMEA, and the Americas so regional capacity moves, qualification cycles, and application substitution could be checked, and then the learnings were used to adjust conversion factors and timing assumptions that desk research cannot confirm on its own.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 15% | APAC: 40% |

| Mid tier: 58% | Functional/Unit leaders: 32% | EMEA: 37% |

| Smaller Players: 15% | Managers: 53% | Americas: 23% |

Market-Sizing & Forecasting

The core model is built using a top-down approach where production, trade, and end-use pull indicators are translated into PFA demand in kilotons, followed by regional splits that reflect where the material is processed and consumed. To keep the totals realistic, we then corroborate the result with selective bottom-up approximations, such as sampled supplier volume ranges by form factor and channel checks on application-level offtake.

Inputs used in the model include reported fluoropolymer capacity expansions, qualification and replacement cycles in high purity fluid handling, semiconductor fab build-out signals, chemical processing project activity, and the mix shift between pellets or powder and aqueous dispersion. Since PFA is often specified for corrosion and purity needs, regulatory timing around PFAS restrictions was also treated as a variable that can change adoption in coatings and consumer-adjacent uses.

For forecasting, we used scenario analysis supported by multivariate regression checks, where demand is linked to a small set of drivers that respondents consistently agreed on at the regional level. When bottom-up signals were incomplete for smaller channels, gaps were handled through conservative penetration and usage-rate assumptions that were re-tested during validation calls before finalizing the series.

Data Validation & Update Cycle

Outputs were validated through multiple checks so the final numbers do not rely on a single data stream. We compared the modeled volumes against independent signals like regional trade flow direction, announced capacity and ramp schedules, and application demand momentum, and then outliers were reviewed before sign-off.

If a material event occurs, such as a capacity outage, a major regulatory change, or a sharp shift in semiconductor investment plans, the team re-contacts sources and revisits key conversion assumptions. The report is refreshed annually, and before delivery a final review pass is completed so clients receive an updated view that reflects the latest data available.

Mordor Intelligence's Perfluoroalkoxy Alkane Pfa Market Size Compared With Other Published Estimates

It is common to see different market sizes for PFA because each publisher makes its own choices on units, what gets counted as the market, and which years are treated as the base. Differences also show up when pricing assumptions are used instead of physical volumes, since resin pricing can move for reasons that do not match real consumption.

Some published figures present PFA as a revenue market and may fold in broader value layers that are influenced by price swings and product-mix choices. Mordor Intelligence reports the PFA market in kilotons and keeps the scope at resin volumes by form and application, so the estimate stays tied to measurable demand and supply signals rather than blended pricing.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.84 M (2025) | |

| Global Research Publisher A | USD 469.10 M (2024) | This estimate is published in USD revenue terms, which can embed resin price assumptions and currency timing that are not visible, and it may treat product forms and end-use splits differently from a volume-first model. |

| Industry Research Publisher B | USD 1.44 B (2024) | The reported value is materially higher, which commonly happens when a wider revenue scope is used, such as including adjacent fluoropolymers or added downstream value beyond resin, and when aggressive growth scenarios are applied without clear reconciliation to capacity and trade signals. |

Looking at the spread, the biggest driver is not only the year used, but also whether the market is measured as physical resin demand or as revenue influenced by pricing and scope layering. By keeping the inputs traceable to capacity, trade flow direction, and application pull indicators, we can explain the market size in repeatable steps and reduce avoidable variance across updates.

Key Questions Answered in the Report

What is the projected demand for Perfluoroalkoxy Alkane in 2031?

Volume is expected to reach 4.99 kilotons by 2031, reflecting a 4.49% CAGR from 2026.

Which region leads consumption of Perfluoroalkoxy Alkane?

Asia-Pacific held 40.02% of global volume in 2025 and is on pace for the fastest regional growth to 2031.

Why are pellets the preferred product form for Perfluoroalkoxy Alkane?

Pellet grades enable high-speed melt extrusion that achieves ±0.05 mm tubing tolerances required in semiconductor fabs while cutting per-meter costs by up to 40%.

What drives fast growth in Electrical Insulation applications?

Offshore wind, 5G densification, and EV harness upgrades demand PFA’s flame resistance and >20 kV/mm dielectric strength, fueling a 4.89% CAGR through 2031.

How are regulations affecting Perfluoroalkoxy Alkane suppliers?

U.S. state bans, EU PFHxA restrictions, and EPA test orders raise compliance costs and prolong qualification cycles, consolidating demand among large incumbents with robust regulatory teams.

Page last updated on: