Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.85 Billion |

| Market Size (2031) | USD 2.48 Billion |

| Growth Rate (2026 - 2031) | 5.99% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

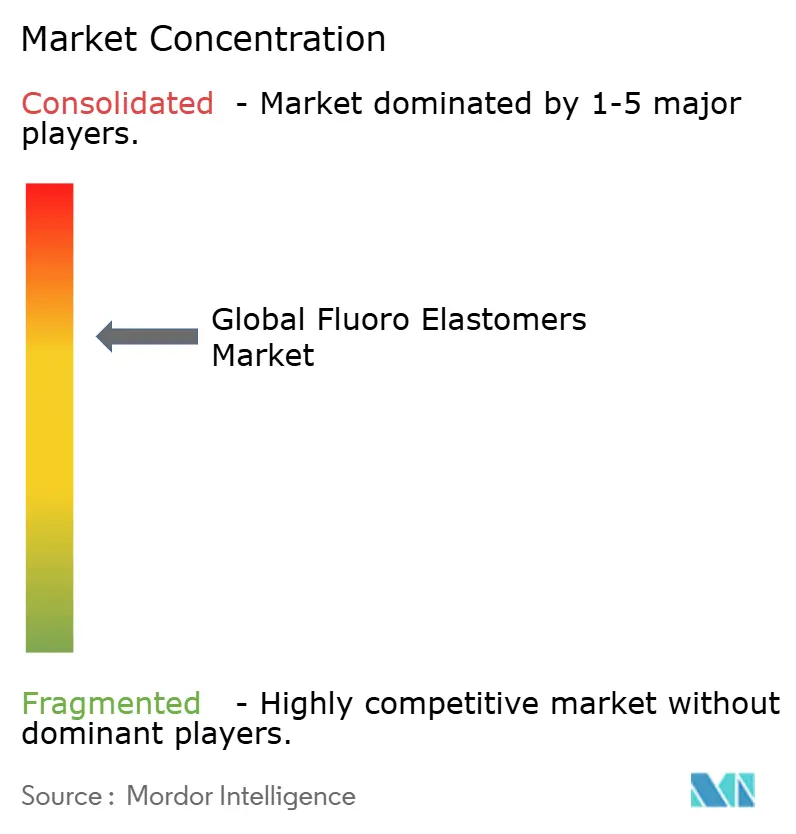

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fluoroelastomers Market Analysis by Mordor Intelligence

Fluoroelastomers Market size in 2026 is estimated at USD 1.85 billion, growing from 2025 value of USD 1.75 billion with 2031 projections showing USD 2.48 billion, growing at 5.99% CAGR over 2026-2031. A sustained shift toward battery-electric vehicles, the proliferation of small-satellite constellations, and relentless scaling in semiconductor fabrication keep demand for high-performance seals on an upward trajectory. Because carbon–fluorine bonds resist extreme temperatures, aggressive chemicals, and rapid thermal cycling, fluoroelastomers remain the default choice where failure is not an option. Automakers now specify Viton and Kalrez compounds in battery-coolant circuits to prevent dielectric fluid leakage, while chip manufacturers rely on low-outgassing perfluoroelastomers to protect 3 nm process nodes. At the same time, exploration of hotter, deeper oil reservoirs expands high-temperature sealing needs in energy operations. Proposed PFAS restrictions in Europe inject regulatory uncertainty, yet they also accelerate investment in non-fluorosurfactant production technologies that preserve performance advantages without legacy chemistries.

Key Report Takeaways

- By product type, Fluorocarbon elastomers led with 61.02% of the fluoroelastomers market share in 2025; perfluoroelastomers are projected to advance at a 6.98% CAGR through 2031.

- By application, O-rings and seals accounted for 44.02% of the fluoroelastomers market size in 2025, while the “other applications” category is poised for a 7.67% CAGR to 2031.

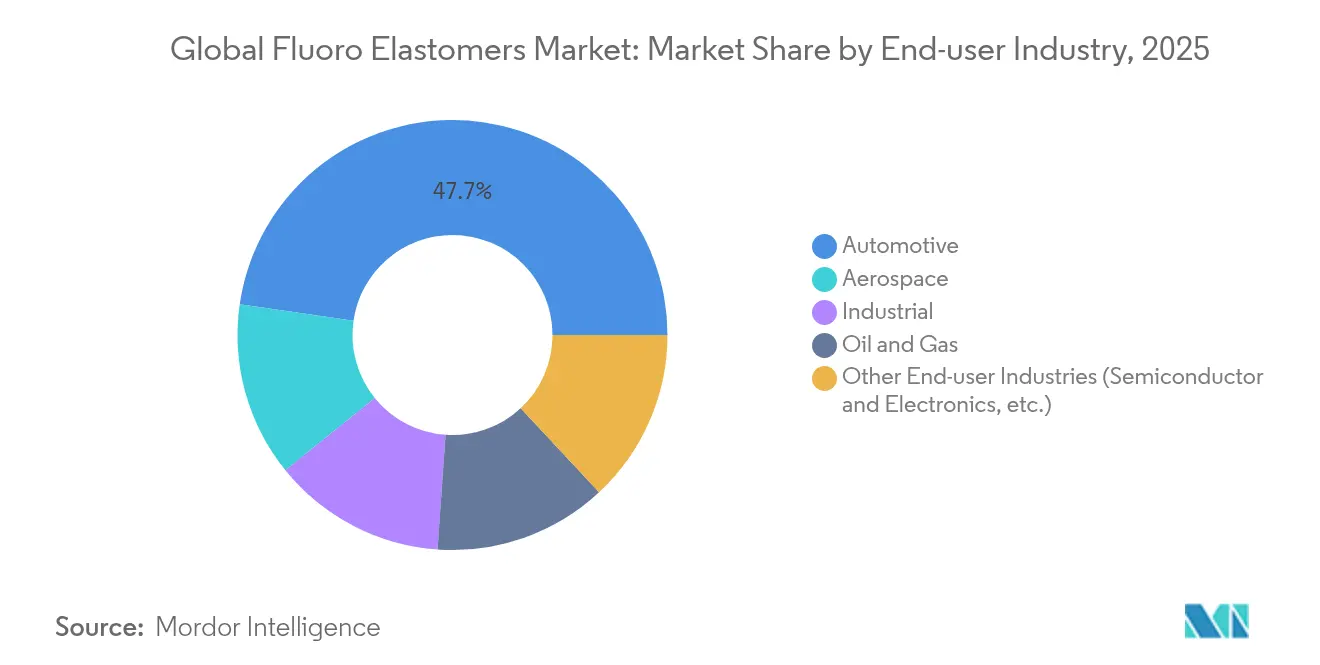

- By end-user industry, Automotive & transportation held 47.72% revenue share of the fluoroelastomers market in 2025; other end-user industries show the fastest growth at 7.42% CAGR.

- By geography, Asia-Pacific commanded 45.63% of the global fluoroelastomers market in 2025 and is expanding at a 7.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fluoroelastomers Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV thermal-management seal demand surge | +1.8% | Global, early gains in China, Europe, North America | Medium term (2-4 years) |

| Growing demand for aerospace & new space propulsion seals | +1.2% | North America & Europe core, spill-over to APAC | Long term (≥ 4 years) |

| Increasing requirement for semiconductor process seals | +1.5% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Growing utilization in the oil and gas industry | +0.8% | Global, focus in Middle East & North America | Medium term (2-4 years) |

| Expansion in renewable energy infrastructure | +0.7% | Global, with early gains in Europe, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV Thermal-Management Seal Demand Surge

Electric-vehicle battery packs rely on sophisticated liquid-cooling loops that circulate dielectric fluids able to dissipate heat without risking short circuits. Seals made from Viton and similar compounds limit swelling to less than 5% after 1 000 hours in polyalphaolefin-based coolants, outperforming silicone and EPDM alternatives. Prestone’s low-conductivity coolant formulated under China’s GB29743.2 standard illustrates how chemistry updates push sealing specifications to new thresholds, Automakers have extended battery warranties to 10 years, so perfluoroelastomers that maintain tensile strength below −30 °C and above 150 °C become essential. As global EV production climbs past 25 million units in 2025, OEM sourcing teams lock in multiyear supply contracts for high-purity perfluoroelastomer compounds, anchoring a key growth pillar for the fluoroelastomers market.

Growing Demand for Aerospace & New Space Propulsion Seals

Commercial launch providers, satellite manufacturers, and defense primes specify perfluoroelastomer seals that survive propellants such as hydrazine or liquid oxygen while cycling from −200 °C to +300 °C. DuPont’s Kalrez grades now guarantee chemical compatibility with more than 1 800 fluids, reducing mission-critical leak paths in spacecraft life-support lines and cryogenic feed systems [1]DuPont, “Kalrez High-Performance Perfluoroelastomers,” dupont.com. In aviation, lightweight turbochargers and sustainable-aviation-fuel delivery modules increasingly rely on Viton to curb maintenance frequency. Each reusable launch vehicle can contain over 1 200 individual O-rings, multiplying material demand as launch cadence accelerates. Consequently, aerospace programs amplify the long-run pull on the fluoroelastomers market.

Increasing Requirement for Semiconductor Process Seals

Sub-5 nm node production uses aggressive fluorine and chlorine plasma chemistries inside extreme-vacuum chambers. Even trace outgassing contaminates photoresist patterns, so fabs qualify Kalrez Spectrum 7375 parts for 300 °C continuous operation and <20 ppm total mass loss. Greene Tweed’s new South Korean plant shortens lead times for local fabs while diversifying away from single-region supply risk. As AI accelerators and advanced packaging lines proliferate, perfluoroelastomer seal demand scales with every added etch, deposition, or CMP step, reinforcing a steady growth channel for the fluoroelastomers market.

Growing Utilization in the Oil and Gas Industry

Extended-reach wells routinely exceed 200 °C downhole, subjecting elastomers to sour gas and supercritical brines. Field data show Kalrez perfluoroelastomers achieving zero seal failures across 50 000 V-ring deployments in high-pressure, high-temperature completions. James Walker’s compound formulations address rapid gas decompression by balancing cross-link density with fluorine content, mitigating blistering risk in 15 k psi service. As operators tap deeper reservoirs and employ enhanced-oil-recovery chemistries, the fluoroelastomers market gains a durable customer base in energy production.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High material & compounding cost | -0.9% | Global, acute in price-sensitive markets | Short term (≤ 2 years) |

| Feedstock supply volatility | -0.6% | Global, concentrated in APAC manufacturing | Medium term (2-4 years) |

| Circular economy recycling mandates | -0.4% | Europe core, expanding to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Material & Compounding Cost

Fluoroelastomer production relies on fluorinated monomers that trade at premiums standard petrochemical feedstocks. Tight process control and proprietary curing packages push conversion costs further, limiting uptake in low-margin components. Global natural rubber shortages extend price pressures across the wider elastomer landscape, reinforcing cost sensitivity even where performance benefits are clear-cut. To counterbalance, suppliers emphasize life-cycle savings: one gearbox seal rated for 10 000 operating hours often replaces two or three NBR equivalents. Halogen-free ethylene-acrylic alternatives such as Vamac creep into mid-temperature applications, compressing potential volume growth for the fluoroelastomers market.

Feedstock Supply Volatility

Production of hexafluoropropylene oxide dimer acid and related intermediates remains geographically concentrated. Any trade friction, force majeure, or pandemic-era shutdown cascades through inventories, sparking spot-price spikes of 20–30%. Regulatory scrutiny of PFAS processing aids intensifies sourcing risk, compelling firms like Greene Tweed to dual-qualify supply chains and build regional buffer stocks. Ongoing efforts to deploy non-fluorosurfactant polymerization platforms are promising but not yet at full capacity, leaving the fluoroelastomers market exposed to intermittent raw-material shocks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Perfluoroelastomers Drive Innovation

Fluorocarbon elastomers retained 61.02% of the fluoroelastomers market share in 2025, buoyed by entrenched use in automotive fuel-line connectors, refinery gaskets, and general industrial equipment. Their broad processing window helps component suppliers meet mass-production takt times without resorting to exotic tooling. Volume leadership, however, does not equate to highest growth. Perfluoroelastomers expand at a 6.98% CAGR through 2031, catalyzed by semiconductor cleanrooms and reusable launch vehicles that push sealing specifications past traditional fluorocarbon limits. This growth vector translates to a perfluoroelastomer segment contribution of roughly USD 613 million to the overall fluoroelastomers market size by the end of the decade.

Demand acceleration also stems from novel manufacturing methods. Solvay’s Tecnoflon NFS process eliminates PFAS surfactants yet delivers identical compression-set retention, addressing European policy uncertainty without sacrificing performance . As large fabs simulate chemical permeation down to parts-per-trillion thresholds, non-contaminating perfluoroelastomers gain value over lower-cost counterparts. Meanwhile, fluorosilicone elastomers hold a smaller niche but remain indispensable in aerospace environmental control systems where −60 °C flexibility meets jet-fuel resistance. Suppliers continue tailoring bisphenol-cure systems to enhance modulus at altitude pressures, protecting a steady revenue stream inside the broader fluoroelastomers market.

By Application: Specialized Components Gain Momentum

O-rings and standard profile seals accounted for 44.02% of the fluoroelastomers market size in 2025, making them the dominant application category. Tier-one molders achieve economies of scale by running multi-cavity tools that spawn millions of identical rings each month. Although unit prices are low, cumulative value remains high because critical operations—semiconductor vacuum doors, EV battery plates, refinery pump shafts—can require dozens of seals per assembly. Over the forecast horizon, standardized components will continue to underpin base demand for the fluoroelastomers market.

Yet the fastest momentum lies in the “other applications” bucket, which is tracking a 7.67% CAGR to 2031 as designers seek custom shapes for renewable-energy and advanced-manufacturing duties. Labyrinth seals in offshore wind gearboxes now combine PTFE inserts with perfluoroelastomer energizers, enabling 25-year maintenance intervals in saline atmospheres. In solar-thermal plants, fluoroelastomer bellows isolate molten-salt loops from control actuators while surviving daily thermal cycles exceeding 350 °C. The rapid prototyping of flow-battery gaskets—by blending glass micro-fibers into FKM matrices for improved compressive modulus—expands the addressable market beyond traditional fluid-sealing niches, keeping innovation churn high across the fluoroelastomers market.

By End-User Industry: Diversification Beyond Automotive

Automotive & transportation held 47.72% of the fluoroelastomers market revenue in 2025, anchored by legacy ICE fuel-system seals and rising EV coolant connectors. Although platform cost-control efforts are relentless, regulatory mandates for zero leakage drive persistent specification of premium compounds. Growth, however, is stronger elsewhere. “Other end-user industries” are climbing at a 7.42% CAGR, reflecting the spread of clean-room manufacturing, precision medical devices, and grid-scale storage solutions. Semiconductor fabs alone can consume more than 3 kg of perfluoroelastomer seals per 300 mm tool set, contributing meaningful incremental volume to the fluoroelastomers market.

Aerospace, while smaller in share, brings above-average unit margins. Energy infrastructure remains a durable customer set, from LNG liquefaction trains that need peroxide-cure fluorocarbon elastomer expansion joints to offshore production vessels where compound blends fight explosive decompression. Together, these verticals widen the revenue base and lower cyclical risk for the fluoroelastomers market.

Geography Analysis

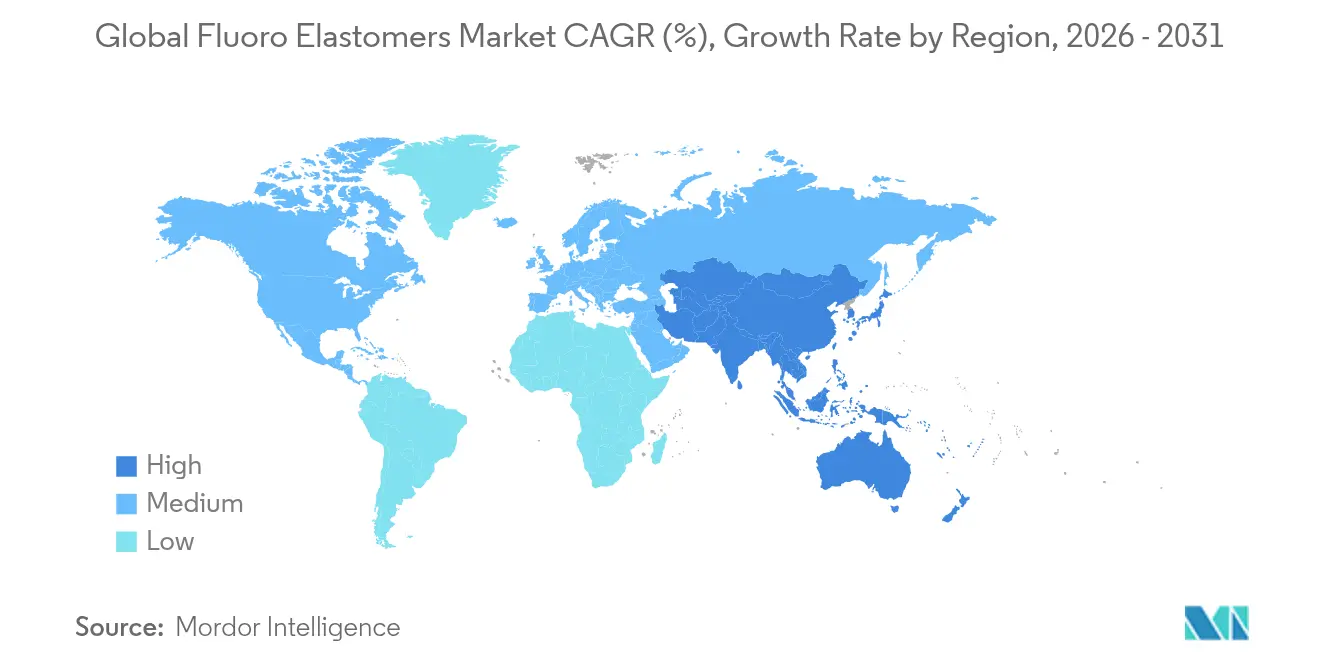

Asia-Pacific dominated the fluoroelastomers market in 2025 with 45.63% revenue share, and regional demand is projected to rise at a 7.02% CAGR through 2031. China’s push for semiconductor self-sufficiency drives sustained investment in 12-inch fabs, each requiring thousands of high-purity O-rings with single-digit ppm outgassing specifications. India’s automotive reforms, including PLI incentives for local battery manufacturing, encourage domestic production of EV-grade coolant seals. Gujarat Fluorochemicals has committed USD 6 billion over the next four years to expand battery-chemical capacity, signalling long-term regional integration of fluoropolymer supply chains.

North America ranks second, buoyed by mature aerospace programs, shale-oil activity, and onshoring of advanced logic foundries. The CHIPS and Science Act accelerates regional wafer capacity, translating into near-term spikes in perfluoroelastomer consumption. Additionally, US deepwater developments in the Gulf of Mexico reinforce demand for HPHT-rated sealing solutions. Europe’s share faces pressure from prospective PFAS bans that could restrict certain fluorinated intermediates. Manufacturers such as James Walker publicly advocate for application-based exemptions while simultaneously piloting PFAS-free compounds for moderate-duty services. Smaller regional clusters add incremental growth. South America’s pre-salt exploration programs necessitate high-performance fluoroelastomer isolation valves, whereas the Middle East targets hydrogen and ammonia export infrastructure that benefits from chemical-resistant sealing materials. Although these regions combined account for less than 10% of current fluoroelastomers market revenue, their multiyear capital-project pipelines suggest a notable contribution to volume upside by 2030.

Competitive Landscape

The fluoro elastomers market is moderately consolidated, with DuPont, Chemours, Daikin Industries, and 3M dominating through vertically integrated value chains and extensive patent portfolios exceeding 800 active families each. These leaders are shifting towards non-fluorosurfactant production in 2024–2025 to address regulatory risks, exemplified by Chemours’ partnership with Navin Fluorine to integrate Opteon dielectric fluids into India’s advanced manufacturing. Second-tier players like Solvay, LANXESS, and Gujarat Fluorochemicals leverage regional advantages and cost-efficient feedstocks, while niche firms such as Eagle Elastomer and Trp Polymer Solutions focus on custom pharmaceutical applications. The race for semiconductor qualification remains intense, offering multi-year revenue opportunities. Supply-chain resilience is a priority, with Greene Tweed expanding in South Korea and James Walker enhancing rapid prototyping capabilities. Companies increasingly use digital twins and finite-element modeling to optimize performance and reduce costs. Despite high entry barriers, Asia’s incremental capacity additions indicate growing geographical diversity in the market.

Fluoroelastomers Industry Leaders

3M

DAIKIN INDUSTRIES, Ltd.

AGC Chemicals Americas

The Chemours Company

Syensqo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: DuPont launched new Kalrez perfluoroelastomer components for semiconductor and electronics manufacturing, offering improved sealing performance, reduced leaks, and minimized waste under harsh conditions. The innovations align with DuPont’s sustainability goals and reinforce its commitment to delivering efficient, high-quality, and eco-friendly solutions globally.

- March 2025: Syensqo launched Tecnoflon FFKM NFS, a new range of high-performance perfluoroelastomers using proprietary non-fluorosurfactant (NFS) technology, addressing sustainability demands and expanding its perfluoroelastomer (FFKM) offerings for semiconductor manufacturing and other sectors.

Global Fluoroelastomers Market Report Scope

Fluoroelastomers are saturated rubbers that can't be cured with sulfur but need to be vulcanized with bisphenol. Because they can withstand heat and chemicals so well, they are often used in harsh environments. Market segments for fluoroelastomers include product type, applications, end-user industry, and geography. By product type, the market is segmented into fluorocarbon elastomers, fluorosilicone elastomers, and perfluorocarbon elastomers. By application, the market is segmented into diaphragms, valves, o-rings, seals and sealants, and other applications. By end-user industry, the market is segmented into automotive, aerospace, oil and gas, industrial, and other end-user industries. The report also covers the market size and forecasts for the fluoroelastomers market in 14 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (kilo tons).

By Product Type

| Fluorocarbon Elastomers |

| Fluorosilicone Elastomers |

| Perfluoroelastomers |

By Application

| O-Rings, Seals and Sealants |

| Diaphragms |

| Valves |

| Other Applications (Hoses and Tubes, etc.) |

By End-user Industry

| Automotive |

| Aerospace |

| Oil and Gas |

| Industrial |

| Other End-user Industries (Semiconductor and Electronics, etc.) |

By Geography

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | SaudI Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Fluorocarbon Elastomers | |

| Fluorosilicone Elastomers | ||

| Perfluoroelastomers | ||

| By Application | O-Rings, Seals and Sealants | |

| Diaphragms | ||

| Valves | ||

| Other Applications (Hoses and Tubes, etc.) | ||

| By End-user Industry | Automotive | |

| Aerospace | ||

| Oil and Gas | ||

| Industrial | ||

| Other End-user Industries (Semiconductor and Electronics, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | SaudI Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the fluoro elastomers market by 2031?

The fluoro elastomers market is forecast to reach USD 2.48 billion by 2031.

Which product type is growing fastest?

Perfluoroelastomers are expanding at a 6.98% CAGR through 2031 due to semiconductor and space-propulsion applications.

Why are fluoro elastomers critical for electric-vehicle batteries?

They withstand new dielectric coolants, maintain flexibility at sub-zero temperatures, and prevent leakage that could trigger thermal runaway.

How will European PFAS regulations affect the market?

Proposed restrictions could tighten supply of certain grades, accelerating development of non-fluorosurfactant manufacturing methods and alternative chemistries.

Which region leads current demand?

Asia-Pacific commands 45.63% of global revenue and is growing at a 7.02% CAGR, driven by semiconductor and EV investments.

Page last updated on: