Fluoropolymer Films Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

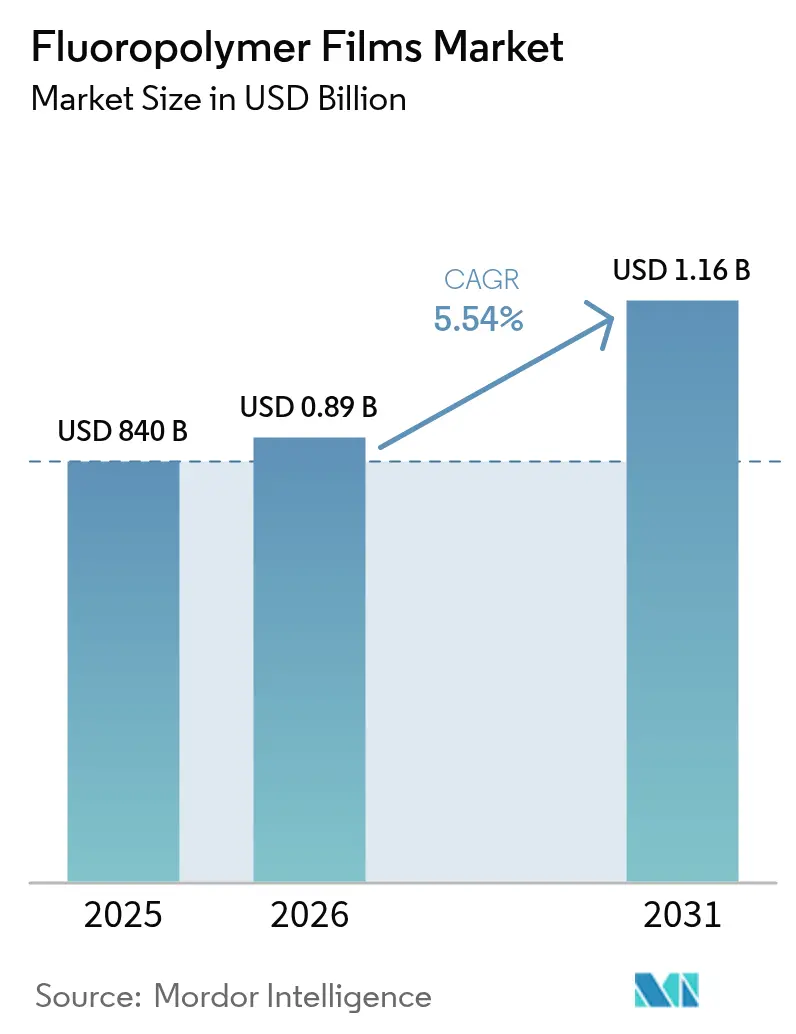

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 1.16 Billion |

| Growth Rate (2026 - 2031) | 5.54% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fluoropolymer Films Market Analysis by Mordor Intelligence

The Fluoropolymer Films market size is expected to grow from USD 840 million in 2025 to USD 886.5 million in 2026 and is forecast to reach USD 1.16 billion by 2031 at 5.54% CAGR over 2026-2031. This growth outlook underscores how irreplaceable performance attributes, notably chemical inertness, low surface energy, and wide-temperature stability, continue to outweigh mounting regulatory pressures on per- and polyfluoroalkyl substances (PFAS). Rapid photovoltaic (PV) build-out, electric-vehicle (EV) light-weighting, and semiconductor contamination control remain the three most influential demand engines. Incumbent producers are widening product portfolios for mission-critical applications rather than chasing volume alone, while downstream customers signal rising willingness to pay for durability and safety assurances. Asia Pacific retains structural cost advantages and end-use proximity, Northern American buyers prioritize high-purity and traceability, and European policy makers drive innovation in PFAS-compliant chemistries. Together, these forces point to a steady, rather than exponential, expansion path for the fluoropolymer films market over the next five years.

Key Report Takeaways

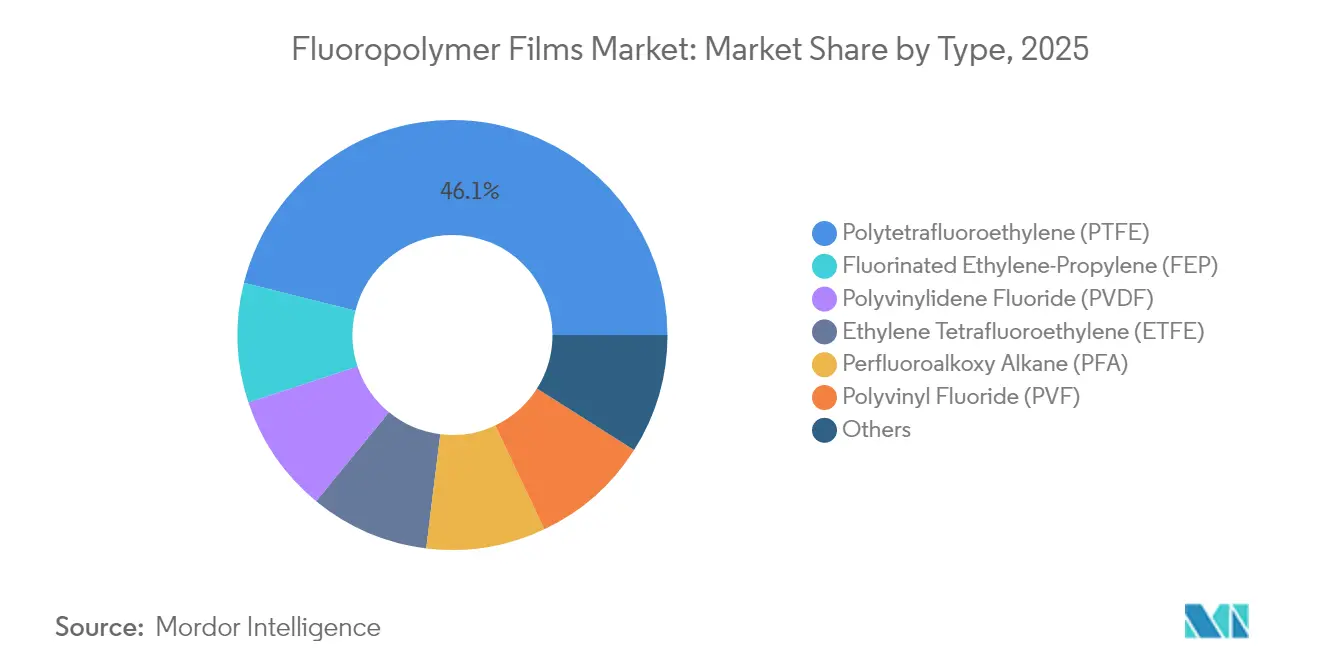

- By type, Polytetrafluoroethylene (PTFE) held 46.10% of the fluoropolymer films market share in 2025, while Fluorinated Ethylene-Propylene (FEP) is projected to expand at 5.93% CAGR through 2031.

- By application, barrier films led with 43.80% revenue share in 2025; microporous films recorded the fastest 6.05% CAGR to 2031.

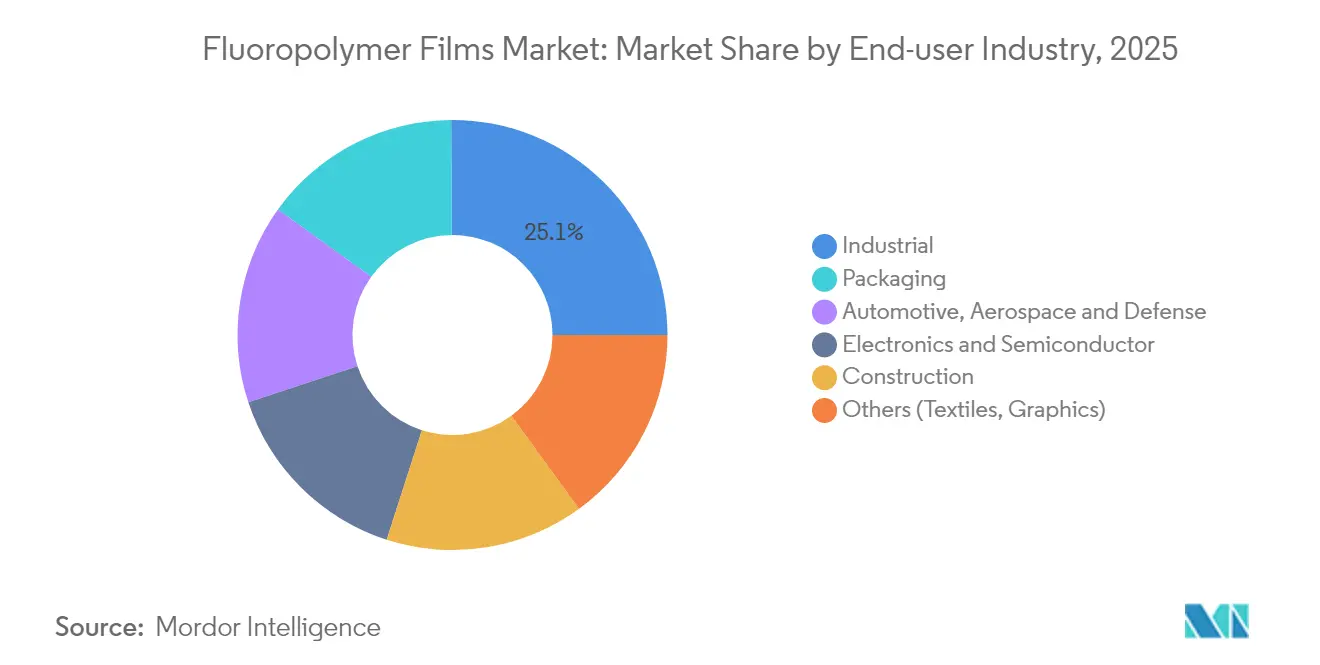

- By end-user industry, the industrial segment captured 25.10% share of the fluoropolymer films market size in 2025, whereas packaging shows the highest 6.42% CAGR through 2031.

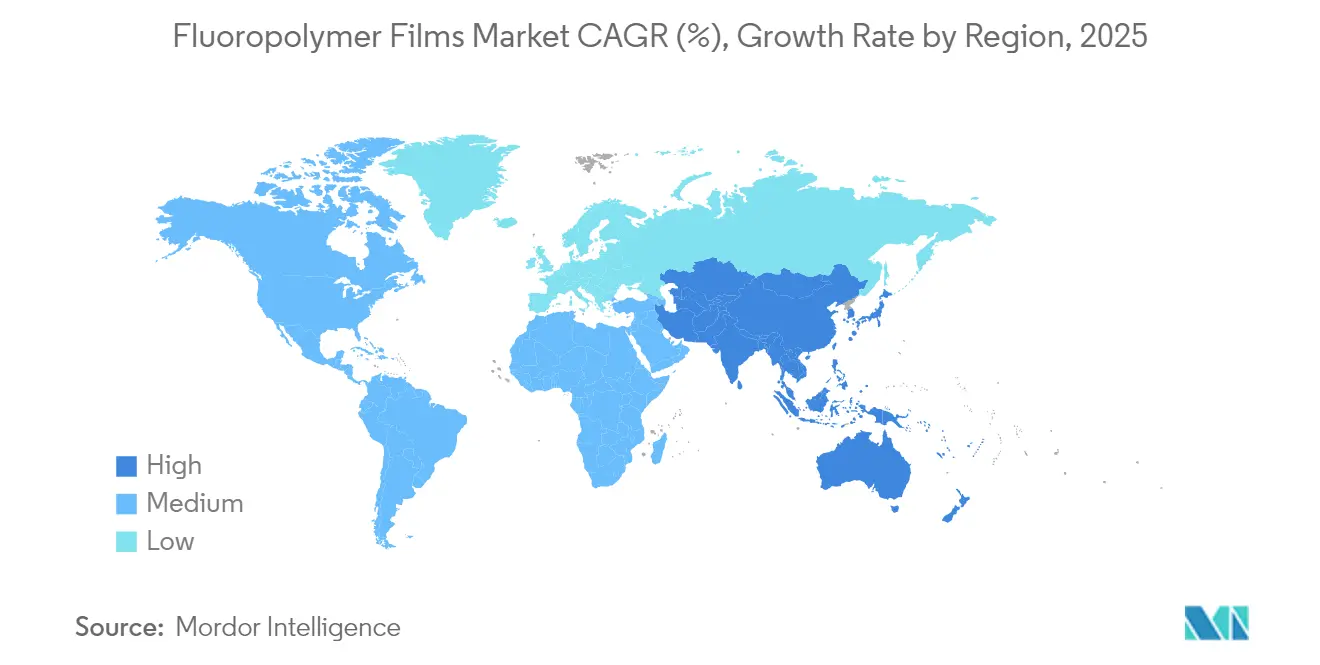

- By geography, Asia Pacific commanded 48.20% of 2025 revenue and is advancing at a 6.02% CAGR, the quickest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fluoropolymer Films Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating demand for PV solar front-sheet and back-sheet films | +1.8% | Global, strongest in China and the United States | Medium term (2-4 years) |

| Rising pharmaceutical and medical packaging adoption | +1.2% | North America and the European Union, expanding in the Asia Pacific | Long term (≥ 4 years) |

| EV-led uptake of release films for lightweight composites | +1.5% | China, the EU, and North America | Medium term (2-4 years) |

| Fluoropolymer proton-exchange membranes in green-hydrogen electrolysers | +0.9% | EU and the United States, early adoption in the Asia Pacific | Long term (≥ 4 years) |

| Microporous PTFE separators for solid-state e-aviation batteries | +0.7% | United States and EU, spill-over to Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Demand for PV Solar Front-Sheet and Back-Sheet Films

Flexible PV installations rely on transparent and weather-resistant fluoropolymer laminates to displace heavier glass. Lower water-vapor-transmission rates help perovskite modules retain 84% efficiency after 2,000 hours of damp-heat testing, extending module warranties to 25 years. Asia Pacific’s consumption share mirrors its photovoltaic assembly dominance, while U.S. community-solar policies reinforce demand peaks. Consequently, barrier films remain the largest application slice of the fluoropolymer films market.

Rising Pharmaceutical and Medical Packaging Adoption

Biologics and personalized therapies require stringent moisture and chemical barriers. Chemours confirms that PTFE and PVDF grades remain essential in pre-filled syringes and micro-catheters because of their low extractables and biocompatibility. U.S. FDA guidance on container-closure integrity pushes drug makers to specify high-purity fluoropolymer liners to protect sensitive actives. Matching trends in EU Annex 1 revisions strengthen demand for medical-grade films.

EV-Led Uptake of Release Films for Lightweight Composites

Automakers replace metal with carbon-fiber-reinforced plastics to improve range. Release films must endure more than 180 °C cure cycles without contaminating surfaces. Industry data show a 48% fuel-efficiency benefit across transportation when fluoropolymers enable weight reduction[1]Performance Fluoropolymer Partnership, “Mobility Gains from Fluoropolymers,” pffp.org. Syensqo’s Ajedium PEEK film finalist in the 2025 PACE Pilot Awards evidences continued material innovation for 800-V powertrains.

Fluoropolymer Proton-Exchange Membranes in Green-Hydrogen Electrolysers

The European Union targets 25 million tons annual green hydrogen production by 2030. Gore’s membrane technology lowers electrolyser stack resistance, trimming the levelized cost of hydrogen by improving efficiency and durability. While research into hydrocarbon alternatives advances, field trials show fluoropolymer PEMs still outperform on chemical stability, securing near-term demand growth.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global PFAS regulatory tightening | –1.4% | EU and North America, global follow-on | Short term (≤ 2 years) |

| Volatile feedstock costs | –0.8% | Worldwide, most acute in the Asia Pacific | Short term (≤ 2 years) |

| Rise of fluorine-free high-barrier multilayer films | –0.6% | North America and the EU, spreading to the Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Global PFAS Regulatory Tightening

The U.S. EPA has barred production of 329 PFAS without agency review and designated PFOA and PFOS as hazardous substances[2]U.S. Environmental Protection Agency, “PFAS Strategic Roadmap,” epa.gov. Minnesota and California ban PFAS in select consumer products from January 2025, while an EU REACH proposal seeks to restrict more than 10,000 substances above threshold concentrations. Compliance costs and potential substitution risks collectively shave 1.4 percentage points off the forecast CAGR for the fluoropolymer films market.

Volatile Feedstock Costs

Hydrofluoric-acid precursors depend on fluorspar price swings and regional production outages. Tight supply of polymer-grade propylene inflates intermediate costs, compressing margins for small extruders. Semiconductor customers enforce price-down clauses, limiting pass-through ability and placing a 0.8 percentage-point drag on growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Polytetrafluoroethylene Sustains Lead, While Fluorinated Ethylene-Propylene Accelerates

Polytetrafluoroethylene (PTFE) held a 46.10% share. High melt viscosity yet unmatched chemical inertness anchors its use in semiconductor fabrication chambers, gasket sheets, and high-frequency cables. Continued fab expansions in Taiwan and the United States support demand resilience. The material’s low friction coefficient also keeps PTFE relevant in surgical device liners despite looming regulatory review.

Fluorinated Ethylene-Propylene’s (FEP) 5.93% CAGR positions it as the fastest-growing polymer family through 2031. Lower melt temperature enables melt-extruded tubing, color-matchable sheets, and increasingly 3-D printed filaments for consumer electronics housings. Arkema’s FluorX filament release illustrates how FEP addresses processing constraints that limit PTFE uptake in additive manufacturing. Users value optical clarity combined with 200 °C continuous-use temperature, broadening adoption in flexible printed circuits.

By Application: Barrier Dominance, Microporous Momentum

Barrier films generated 43.80% of 2025 revenue as brands mandate 25-year solar panel warranties and strict moisture protection for biologics. The fluoropolymer films market share advantage stems from exceptionally low water vapour transmission and ultraviolet stability that extend product life.

Microporous separators, however, are racing ahead at 6.05% CAGR. Semiconductor fabs adopt similar structures as chemical filtration media to meet advanced node purity. This cross-industry convergence drives rising tonnage, albeit from a smaller base.

Release films remain indispensable in carbon-fiber composites, while security films serve banknote and ID authentication niches. Incremental innovation revolves around recycling scrap films into lower-grade sheets, supporting circularity targets without undermining primary-grade demand.

By End-User Industry: Industrial Core, Packaging Upswing

Industrial users accounted for 25.10% of 2025 revenue, a testament to long-standing reliance on fluoropolymer liners, tapes, and diaphragms in chemical reactors and clean-room consumables. Etch and deposition chambers in semiconductor fabs specify PTFE and PFA films to minimise particle generation, reinforcing a dependable baseline for the fluoropolymer films market.

Packaging records the strongest 6.42% CAGR. Pharmaceutical producers adopt laminated PVDF blisters that outperform aluminium-plastic combinations on puncture resistance and moisture barrier. Food processors position high-clarity ETFE wraps as premium alternatives to PVC, extending shelf life for ready-to-eat meals. Regulators accept fluoropolymer contact layers after stringent extractables testing, encouraging broader rollout.

Geography Analysis

Asia Pacific generated 48.20% of global sales in 2025, with the fluoropolymer films market size expanding at a region-leading 6.02% CAGR. China’s integrated PV supply chain consumes vast volumes of PVF backsheets and ETFE frontsheets, while government incentives accelerate rooftop-solar retrofits. India’s electronics manufacturing scheme promotes domestic sourcing of high-purity PTFE tapes, elevating baseline demand. Japan’s automotive platforms shift to 800-V architectures, favouring PEEK and PTFE dielectric films for improved thermal management.

North America benefits from strong semiconductor capital expenditure and medical-device innovation. Chip fabs under the U.S. CHIPS Act upgrade clean-room standards, driving PTFE and FEP consumables. EV platforms from Michigan to Georgia require composite release films for body-in-white panels.

Europe balances regulatory stringency with climate-policy pull. Green-hydrogen electrolyser pilots in Germany and Spain incorporate fluoropolymer PEMs. Automotive OEMs in Germany and France integrate ETFE roof skins for weight savings. Yet proposed EU-wide PFAS restrictions inject uncertainty, prompting producers to invest in closed-loop recovery and waste-gas abatement. Such measures sustain supply, albeit at higher compliance cost.

Regulatory Landscape

PFAS regulation is increasingly shaping near-term market decisions, with the EU REACH restriction process acting as the key inflection. In March 2026, ECHA's Risk Assessment Committee (RAC) adopted its final opinion supporting a broad PFAS restriction, and ECHA opened a 60-day public consultation on the draft Socio-Economic Analysis Committee (SEAC) opinion on 26 March 2026, which closed on 25 May 2026. For fluoropolymer films, the framework is moving toward use-specific, time-limited derogations for critical applications (notably medical and semiconductor uses) rather than a uniform allowance, which is raising documentation and compliance requirements across the lifecycle from production to disposal.

Outside the EU, policy alignment and industry advocacy are creating parallel pressure points for global suppliers and converters. The UK published a PFAS plan in February 2026, pointing to UK REACH reform by December 2028 to enable PFAS controls aligned with the EU approach, which increases the importance of EU regulatory outcomes for UK processors that rely on imported fluoropolymer inputs. Industry associations have also intensified engagement, including a January 2026 position statement from the Fluoropolymers Product Group calling for an exemption for fluoropolymers and advocating management through existing frameworks such as the Industrial Emissions Directive.

Value Chain Analysis

The value chain begins with fluorspar mining and conversion to hydrogen fluoride and downstream fluorinated intermediates, then moves into polymerization into fluoropolymers (PTFE, PVDF, FEP, ETFE, PFA, PVF) and compounding into grades suited for film processing. Film conversion uses specialized extrusion or casting, biaxial stretching, and high-control cooling and handling to meet tight tolerances for barrier, release, and microporous structures. These steps are capital- and know-how intensive, which makes film conversion a bottleneck for potential new entrants.

Downstream demand is met through direct supply to large OEMs and module makers (PV, electronics/semiconductor, industrial) as well as through converters and distributors for tapes, liners, and packaging laminations. Supply risk is concentrated upstream and in specific geographies, particularly for fluorspar and hydrogen fluoride capacity, which creates cost and availability exposure for film producers and converters. Europe remains structurally import-reliant for fluoropolymers (with a large share of supply sourced from outside the region), while processors face added friction from energy and compliance costs, increasing interest in alternative sourcing and regional production partnerships. Chemours provided a concrete example in August 2025, when it entered strategic agreements with SRF Limited in India to manufacture advanced fluoropolymers at SRF's Dahej facility via technology transfer, supporting essential applications and broadening supply options for film-grade resins and downstream processors.

Competitive Landscape

The fluoropolymer films market remains moderately fragmented. Medium-sized challengers focus on niche grades for optoelectronics or biomedical devices. Competitive intensity centres on regulatory preparedness rather than plant scale alone. Competitors are already courting their specialty tape and medical device customers. Looking forward, intellectual-property depth, life-cycle-assessment transparency, and captive monomer access stand out as primary competitive levers. Producers that balance environmental stewardship with application-focused innovation are best positioned to capture incremental share in the fluoropolymer films market.

Fluoropolymer Films Industry Leaders

3M

The Chemours Company

Saint-Gobain

Arkema

Daikin Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are most evident where fluoropolymer films address qualification-critical problems that substitutes struggle to match, especially in electronics and semiconductor contamination control, PV durability targets, and high-integrity medical and pharmaceutical packaging where extractables, barrier performance, and traceability influence purchasing decisions. PFAS tightening is also creating room for suppliers that can package application-specific compliance support (documentation, emissions controls, and closed-loop handling) for EU and UK customers working through the ECHA-driven REACH restriction process and the UK REACH reform timeline, rather than competing only on commodity film output.

Recent capacity and investment decisions reinforce a move toward higher-value fluoropolymer supply chains that feed film demand in batteries, electronics, and industrial applications. In June 2026, Arkema started up its Calvert City, Kentucky PVDF capacity expansion (15%, approximately USD 20 million), and in March 2026 it announced a further PVDF expansion plan at Changshu, China (20%, with a later startup), both aligning supply localization with major end-use manufacturing hubs. At the same time, China-based investments in high-end fluorine materials, including Yonghe Shares' large fluorine materials and pilot base project in July 2026, add to competitive intensity on specialty fluoropolymer supply, which increases the need for film producers to differentiate through purity, consistency, and end-use qualification support.

Recent Industry Developments

- June 2026: Arkema started up its 15% PVDF capacity expansion at Calvert City, Kentucky, backed by an investment of about USD 20 million. The added PVDF output supports downstream conversion into high-performance films and related components used across batteries, electronics, and industrial applications, strengthening regional supply resilience in North America.

- April 2026: Daikin Industries commenced construction of a new perfluoroelastomer (FFKM) production facility at its Kashima Plant in Japan, targeting semiconductor demand, with completion planned for August 2026. While centered on elastomers, the project reflects broader fluorine-materials capacity being built around semiconductor supply chains that also consume high-purity fluoropolymer films and consumables.

- October 2024: Honeywell announced plans to spin off its Advanced Materials business, including fluoropolymer films, into an independent company by early 2026. The planned separation has implications for product portfolio prioritization and capital allocation in fluoropolymer materials that serve film applications, potentially reshaping how the business competes and partners in specialty markets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues generated from fluoropolymer films sold as finished film materials for industrial and commercial use, whether supplied as rolls, sheets, or converted formats.

Scope exclusions: We exclude fluoropolymer resins sold in non-film forms (such as powders, pellets, dispersions, and coatings) unless they are explicitly sold as a film product.

Segmentation Overview

- By Type

- Polytetrafluoroethylene (PTFE)

- Polyvinylidene Fluoride (PVDF)

- Fluorinated Ethylene-Propylene (FEP)

- Ethylene Tetrafluoroethylene (ETFE)

- Perfluoroalkoxy Alkane (PFA)

- Polyvinyl Fluoride (PVF)

- Others

- By Application

- Barrier Films

- Release Films

- Microporous Films

- Security Films

- By End-User Industry

- Automotive, Aerospace and Defense

- Construction

- Packaging

- Industrial

- Electronics and Semiconductor

- Others (Textiles, Graphics)

- Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial model structure and to anchor the approach to real-world signals that move fluoropolymer film demand. We relied on public sources such as USGS mineral and materials statistics, UN Comtrade trade flows for fluoropolymer-related product groups, US International Trade Commission data, and regulatory or standards references from groups such as ASTM, which helped clarify common film specifications and the conditions under which films are used.

To keep assumptions grounded, we also reviewed annual reports and investor presentations from relevant producers and converters, along with technical papers in peer-reviewed polymer and materials journals that describe performance limits and typical end-use requirements. Where it helped fill gaps on company-level exposure and product mix, we referenced paid subscriptions for company financials and business intelligence, along with a patent database to understand which film chemistries and processing routes were being prioritized. The sources named here are illustrative, and other public and paid references were also used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary input was collected through expert interviews and structured surveys with film producers, converters, distributors, and downstream users serving electronics, industrial processing, construction, and packaging. In these discussions, we confirmed what is treated as a fluoropolymer film sale in practice, and then stress-tested pricing logic, substitution risk, and how regional demand changes show up in actual buying behavior before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | APAC: 38% |

| Mid tier: 52% | Functional/Unit leaders: 34% | EMEA: 37% |

| Smaller Players: 20% | Managers: 51% | Americas: 25% |

Market-Sizing & Forecasting

Sizing used a top-down approach where polymer film demand pools are reconstructed from end-use activity and adoption, then split by region using trade and production signals. To avoid overstating totals, we cross-checked outputs with selective bottom-up approximations, for example sampled price-per-kg or price-per-square-meter ranges multiplied by estimated shipment volumes for key film types, and then adjusted when implied values did not align with what interviewees see in contracts.

In the model, a few market fingerprints were treated as key inputs because they reflect purchase decisions in the field. These include the mix by fluoropolymer type (such as PTFE, PVDF, FEP, ETFE, PFA, and PVF), the application mix (barrier, release, microporous, and security uses), and end-user pull from electronics and semiconductor lines, industrial processing maintenance cycles, construction activity, and packaging demand. Pricing was handled as an average selling price progression that moves with feedstock-linked inflation and product-grade tightness, and this was validated through channel checks and supplier discussions.

Forecasting relied on scenario analysis anchored to expected changes in industrial output, electronics production, and construction activity, and then refined using primary feedback on the timing of capacity additions and the pace of substitution toward other high-performance films. Where bottom-up visibility was weaker, for example in niche converted formats, gaps were handled through proportionate allocations based on the most consistent triangulation signals, and then re-tested with respondents for plausibility.

Data Validation & Update Cycle

Validation was done through triangulation across the model, external indicators, and what respondents described as achievable volumes and prices. Outliers were flagged when regional splits, implied pricing, or growth rates drifted too far from independent signals such as trade movement, capacity commentary, or end-use activity, and then assumptions were reworked until the story and the math aligned.

Before sign-off, the full model is reviewed in steps so calculation logic, unit consistency, and currency handling are checked by another analyst. Reports are refreshed annually, and interim updates are made when material events occur, such as large capacity changes, regulation shifts, or sudden demand shocks. Right before delivery, we do a final pass to incorporate any newly available public data and the most recent interview guidance.

Mordor Intelligence's Fluoropolymer Films Market Size Versus Other Published Estimates

Published fluoropolymer film market sizes can appear far apart even when the end uses discussed are broadly similar, since each estimate makes different choices on product inclusion, the anchor year, and how pricing is projected.

The main gap comes from whether blended barrier films and adjacent high-performance non-fluoropolymer films are rolled into the total, where Mordor Intelligence counts only fluoropolymer film types (such as PTFE, PVDF, FEP, ETFE, PFA, and PVF) and keeps applications like barrier, release, microporous, and security within that definition. Differences also show up when one publisher uses a more aggressive price escalation path, or reports a 2024 base-year number that is not reconciled to later-year demand checks, while another centers sizing around the 2026 value and its implied run-rate.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.89 B (2026) | |

| Industry Publisher A | USD 1.87 B (2024) | Uses a 2024 base year and appears to include blended barrier film categories in type splits, which can widen scope versus counting only fluoropolymer film types. |

| Industry Publisher B | USD 1.99 B (2024) | Positions the total as a 2024 consumption value and may use a different application set (including photovoltaic), which can shift what is captured and how regional demand is summed. |

The spread in the table is largely explained by scope alignment and the choice of anchor year, and then amplified by different pricing and end-use mapping assumptions. When the same film-only definition is applied consistently and checked against end-use activity and pricing reality, the resulting market size becomes easier to trace and repeat from one update to the next.

Key Questions Answered in the Report

What is the current size of the fluoropolymer films market and how fast is it growing?

The market is valued at USD 886.5 million in 2026 and is projected to reach USD 1.16 billion by 2031, reflecting a 5.54% CAGR.

Which region leads global demand for fluoropolymer films?

Asia Pacific holds 48.20% revenue share in 2025 and is also the fastest-growing region with a 6.02% CAGR through 2031.

What type of fluoropolymer film accounts for the largest sales share?

PTFE films dominate with 46.10% of 2025 revenue, mainly due to widespread use in semiconductors, medical devices and industrial equipment.

Which application segment is expanding the quickest?

Microporous films used in solid-state battery separators and high-end filtration are advancing at a 6.05% CAGR, the fastest among all applications.

How are PFAS regulations influencing market dynamics?

Tighter U.S. and EU rules on PFAS trim about 1.4 percentage points from the forecast CAGR, prompting producers to invest in emission controls and alternative chemistries.

Page last updated on: