Polychlorotrifluoroethylene Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

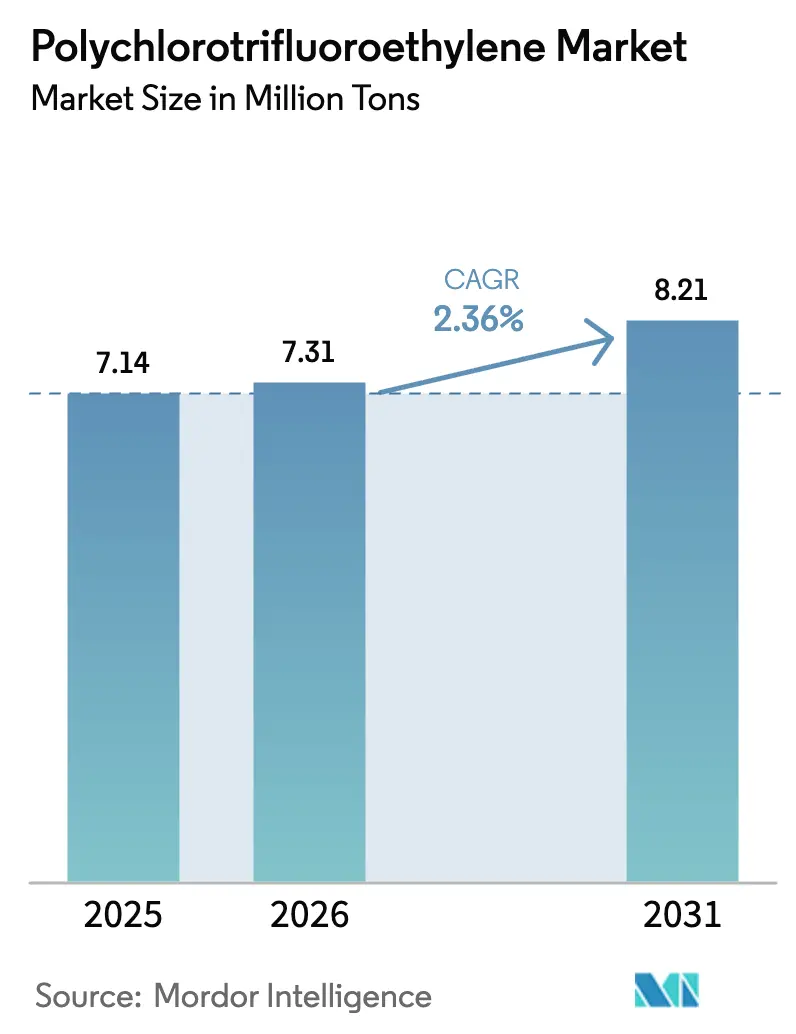

| Market Volume (2026) | 7.31 Million tons |

| Market Volume (2031) | 8.21 Million tons |

| Growth Rate (2026 - 2031) | 2.36% CAGR |

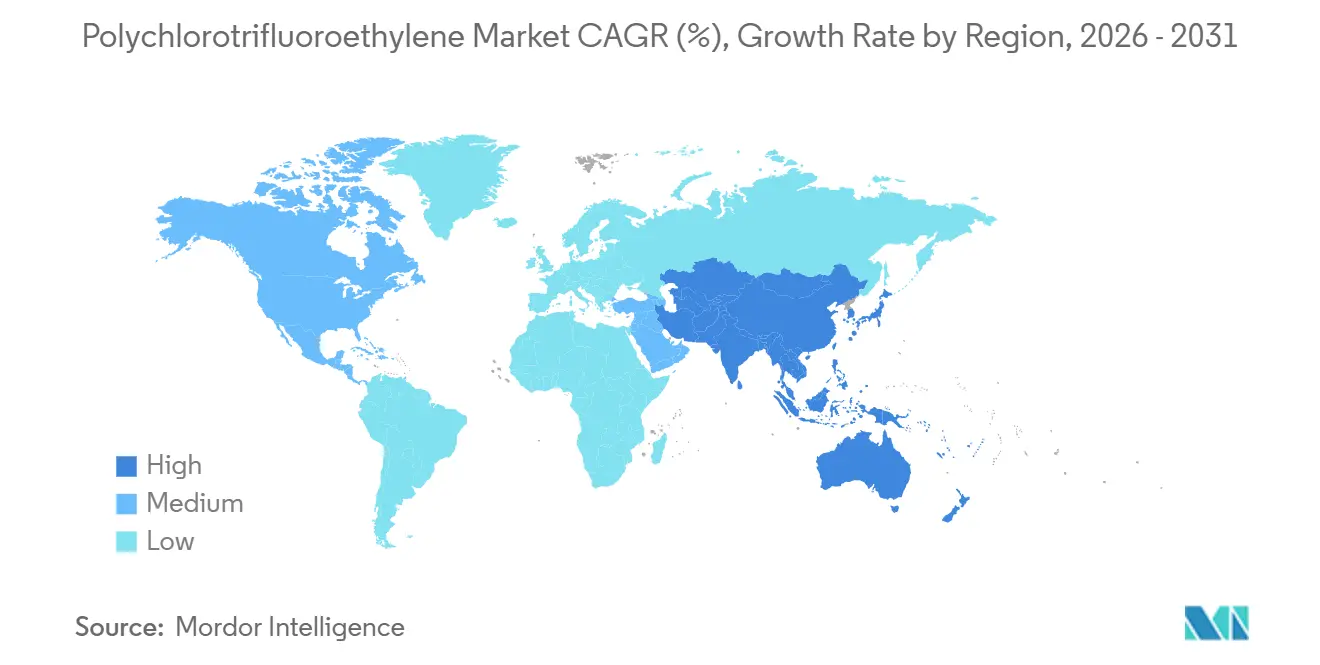

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

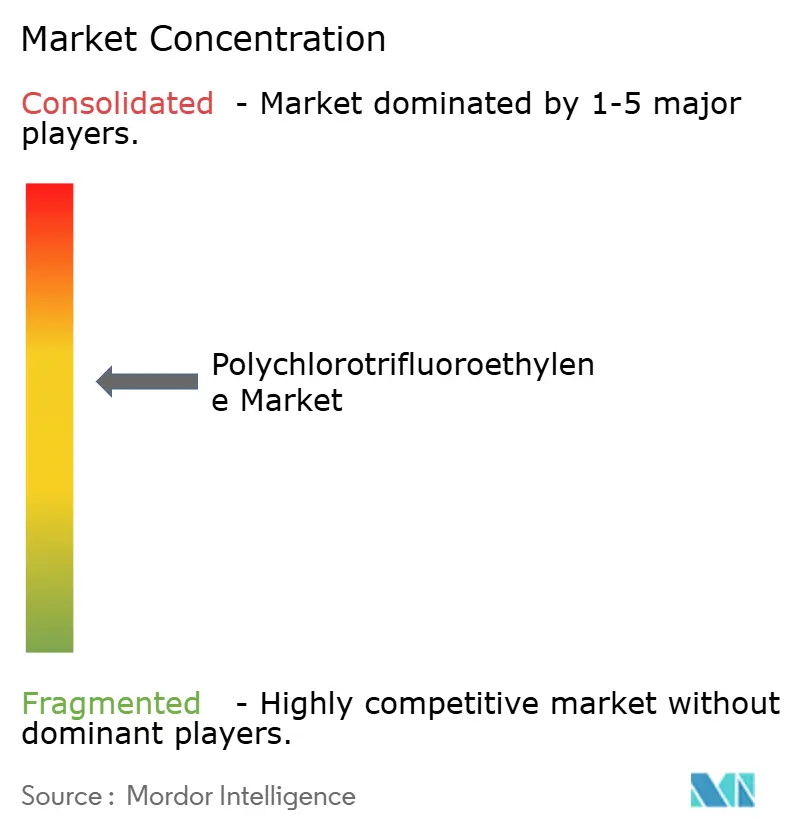

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polychlorotrifluoroethylene Market Analysis by Mordor Intelligence

The Polychlorotrifluoroethylene Market size was valued at 7.14 Million tons in 2025 and is estimated to grow from 7.31 Million tons in 2026 to reach 8.21 Million tons by 2031, at a CAGR of 2.36% during the forecast period (2026-2031). Strong demand from semiconductor, pharmaceutical, and aerospace supply chains offsets regulatory pressure on fluoropolymers and sustains steady volume growth. Growth pivots around Asia-Pacific fabs that need ultra-clean tubing, North American rocket programs that mandate cryogenic sealing reliability, and European blister-pack converters shifting to high-barrier laminates. Integrated producers invest in PFAS-capture technology and surfactant-free polymerization to maintain compliance while defending margins. New hydrogen infrastructure, helium-recovery projects, and flexible electronics create incremental opportunities that keep the Polychlorotrifluoroethylene market on an upward course despite competition from PTFE and PVDF.

Key Report Takeaways

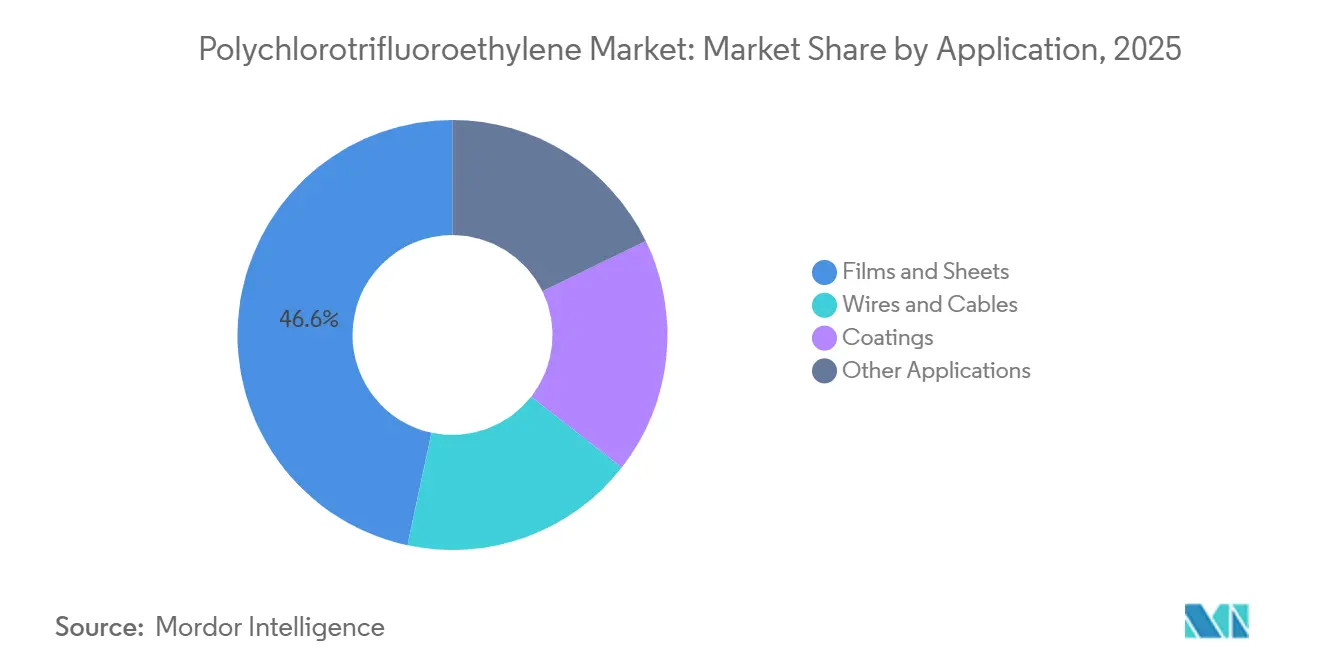

- By application, Films and Sheets captured 46.64% of the Polychlorotrifluoroethylene market share in 2025 and will expand at a 2.60% CAGR through 2031.

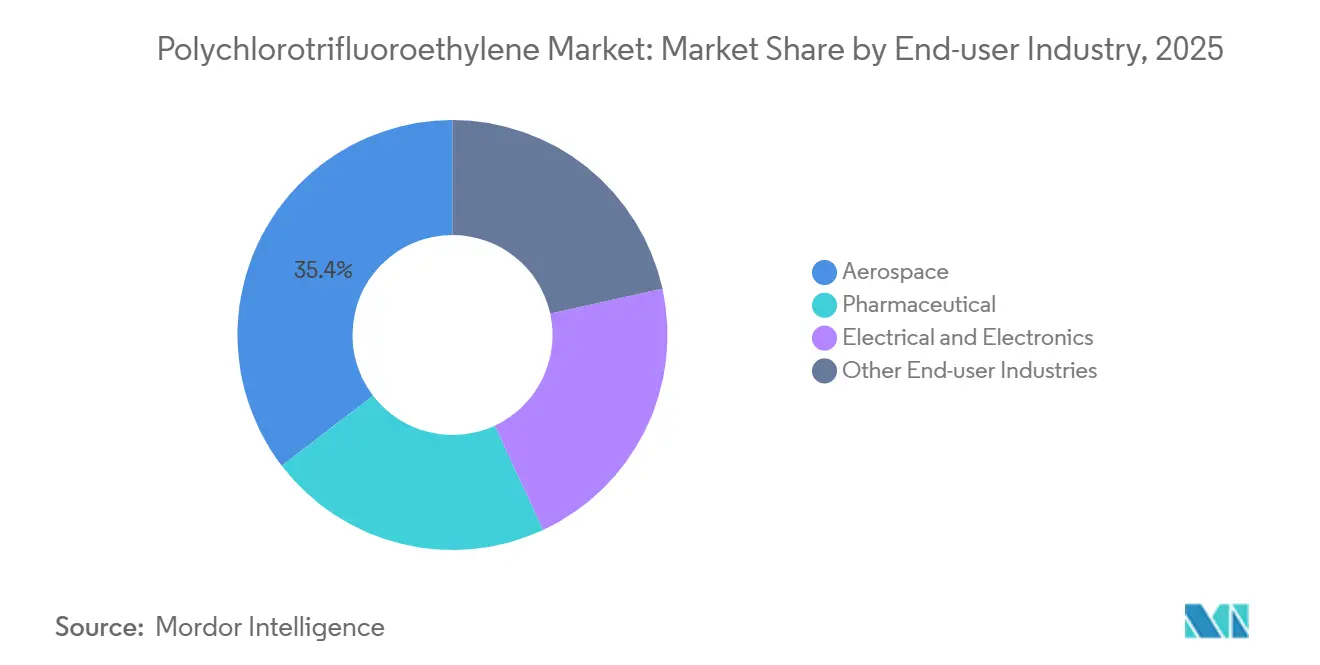

- By end-user industry, Aerospace held 35.40% of the Polychlorotrifluoroethylene market size in 2025, while Electrical and Electronics recorded the highest projected CAGR at 2.77% through 2031.

- By geography, Asia-Pacific accounted for 44.00% of the 2025 volume and is forecast to rise at a 2.82% CAGR to 2031, driven by semiconductor and pharmaceutical capacity additions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polychlorotrifluoroethylene Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pharma blister-pack demand surge | +0.6% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Aerospace cryogenic sealing growth | +0.5% | North America, Europe, APAC (China, India) | Long term (≥ 4 years) |

| Electronics low-k insulation uptake | +0.7% | APAC core (China, South Korea, Taiwan) | Short term (≤ 2 years) |

| Hydrogen fuel-cell sealing adoption | +0.3% | Europe, North America, Japan | Long term (≥ 4 years) |

| Helium-barrier membrane demand | +0.2% | Global, with early adoption in Middle East and Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pharma Blister-Pack Demand Surge

Cold-form blister lines are switching from aluminum-only laminates to PCTFE-aluminum structures because PCTFE delivers a water-vapor transmission rate below 0.05 g/m²/day, which safeguards biologics and high-potency generics during ambient transport. Aclar and PERLALUX films dominate premium grades, while Chinese converters underbid on generic packs to win share in cost-sensitive segments. Regulatory approvals from the FDA and the European Medicines Agency validate PCTFE for biosimilars and gene therapies, opening higher-value orders for converters that can supply pharmaceutical-grade traceability. Investment in high-speed thermoforming equipment narrows historical productivity gaps versus PVC, so converters no longer have to trade barrier performance for line speed. The result is an enduring pull on the Polychlorotrifluoroethylene market as global prescription volumes rise and cold-chain stress eases.

Aerospace Cryogenic Sealing Growth

Rocket engines, propellant transfer systems, and hydrogen refueling hardware require seals that keep elasticity at –253 °C. PCTFE stays ductile where PTFE turns brittle, thus rocket-grade valves, O-rings, and flange gaskets default to PCTFE across NASA Artemis and Ariane 6 platforms. Commercial launch providers add similar specifications, locking in multi-year tonnage with rigorous qualification barriers that protect incumbents. As spaceflight and green-hydrogen aviation scale, ground support equipment orders add continuous demand for high-purity machined shapes. Aerospace therefore preserves a stable core within the Polychlorotrifluoroethylene market even when macrocycles shift.

Electronics Low-k Insulation Uptake

Logic nodes below 5 nm require dielectrics with permittivity under 2.5. PCTFE’s dielectric constant of 2.3–2.6 meets that target while resisting aggressive etchants, so fabs adopt PCTFE tubing, pumps, and flexible circuit layers. Asia-Pacific’s USD 31 billion electronics greenfield FDI in 2024 underpins tool installations that specify fluoropolymer-wetted parts. As 450 mm wafer projects mature, each wet-bench cluster raises per-fab PCTFE demand, reinforcing upward volume momentum. The Polychlorotrifluoroethylene market thus aligns with semiconductor capital expenditure cycles rather than broader industrial activity, a dynamic that shields revenue when other sectors soften.

Hydrogen Fuel-Cell Sealing Adoption

Fuel-cell stacks face acidic membranes and humid temperatures near 100 °C, environments that degrade common elastomers. PCTFE gaskets resist acid, oxygen radicals, and hydrogen permeation, extending stack life beyond 5,000 hours and meeting commercial durability thresholds [1]Chemours, “Advanced Performance Materials Product Portfolio,” chemours.com . European electrolyzer projects and Japanese refueling stations list fluoropolymer parts certified to ISO 19880, embedding PCTFE in upcoming infrastructure. Although electric vehicles currently outpace fuel-cell rollouts, the stationary power and heavy transport segments create a dependable baseline that feeds incremental volume into the Polychlorotrifluoroethylene market through 2031.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Substitute fluoropolymers (PTFE, PVDF) | -0.4% | Global | Short term (≤ 2 years) |

| High processing complexity and cost | -0.3% | Global, acute in emerging markets | Medium term (2-4 years) |

| PFAS regulatory overhang | -0.5% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Substitute Fluoropolymers (PTFE, PVDF)

PTFE and PVDF deliver comparable chemical resistance at lower resin cost and simpler processing, so converters often down-spec assemblies where barrier or cryogenic extremes are not mission-critical. PVDF’s weldability and availability from new Kentucky capacity heighten price pressure on commodity PCTFE parts. As compounders tailor filled PTFE grades with improved wear resistance, overlap widens, forcing PCTFE suppliers to differentiate via ultra-high purity and custom formulations. This cost-performance squeeze tempers upside for the Polychlorotrifluoroethylene market until high-barrier or cryogenic requirements prevail.

PFAS Regulatory Overhang

The U.S. EPA classified PFOA and PFOS as hazardous under CERCLA in 2024, and the European Chemicals Agency advances a broad PFAS restriction proposal that may require authorization even for specialty fluoropolymers[2]U.S. Environmental Protection Agency, “Designation of PFOA and PFOS as CERCLA Hazardous Substances,” epa.gov. Public discourse rarely distinguishes between legacy surfactants and polymers like PCTFE, so brand owners apply blanket phase-out preferences that delay purchasing decisions. Producers invest in capture and destruction technology, yet compliance costs persist, and uncertainty deters downstream substitution of metals or engineering plastics. Regulatory drag, therefore, subtracts momentum from the Polychlorotrifluoroethylene market over the long term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Films Anchor Volume, Coatings Trail

Films and Sheets contributed 46.64% of 2025 volume, representing the largest slice of the Polychlorotrifluoroethylene market share, and will register a 2.60% CAGR through 2031. This dominance stems from cold-form blister demand and helium-barrier membranes that protect sensitive gases during storage. Pharmaceutical converters favor PCTFE because it halves moisture ingress compared with PVC-PVdC laminates, while gas processors value helium selectivity above 3,700 for low-concentration streams.

Wire and Cable holds a considerable share, powered by 5G rollouts and electric-vehicle charging systems that need low-loss RF performance. PCTFE’s dielectric constant near 2.4 and thermal stability to 200 °C enable thin-wall jacketing in high-frequency cables, though PVDF prices spur substitution where dielectric margins allow. Coatings remain niche due to limited solvent compatibility and adhesion hurdles, yet specialty reactors and valve bodies still specify PCTFE linings when permeation control overrides cost concerns. Advancements in melt-extrusion control aim to deliver sub-25 micron film gauges for flexible circuits, a move that could secure additional share if converters achieve uniformity without pinholes.

Films benefit from regulatory acceptance and rising biologics pipelines, creating volume resilience even during macro down-cycles. Wire and Cable growth links to data-center expansion and automotive electrification, but its trajectory is more cyclical and sensitive to infrastructure budgets. Coatings face sustained substitution risk from PVDF and FEP coatings that offer easier spray or dip processes. As converters leverage continuous-cast and blown-film technology upgrades, throughput gains keep unit costs stable, supporting segment profitability despite moderate resin inflation. Cumulatively, these trends fortify application-level diversity and insulate the Polychlorotrifluoroethylene market from single-sector shocks.

By End-User Industry: Aerospace Leads, Electronics Accelerates

Aerospace held 35.40% of 2025 volume, underscoring decades of entrenched design decisions that lock PCTFE into cryogenic feed systems for launch vehicles and satellite propulsion. Long qualification cycles and flight certification maintain supply-chain stability, sustaining margins even when resin input costs rise. Emerging demand from hydrogen aviation projects promises incremental tonnage that helps maintain segment weight in the global Polychlorotrifluoroethylene market.

Electrical and Electronics will clock a 2.77% CAGR through 2031, the fastest among end-user groups, driven by ultra-high-purity tubing, pump parts, and dielectrics in sub-5 nm wafer fabs. Asia-Pacific localization efforts and export control responses intensify regional pull for local fluoropolymer suppliers that can deliver SEMI-grade cleanliness and traceability. Pharmaceuticals and automotive fuel-cell stacks provide steady but smaller contributions, with growth limited by generic-drug cost pressures and the pace of hydrogen vehicle adoption. Collectively, end-user diversification reinforces market resilience and mitigates exposure to single-sector volatility.

Geography Analysis

Asia-Pacific dominates the Polychlorotrifluoroethylene market with 44.00% of 2025 volume and a 2.82% CAGR outlook through 2031. China anchors demand owing to semiconductor equipment localization and increased PCTFE uptake in domestic blister-pack lines. Regional producers gain share as 3M exits PFAS manufacturing, but quality-control requirements keep Western incumbents embedded at leading fabs. ASEAN electronics parks receive record foreign direct investment, bolstering cleanroom tubing and chemical delivery orders, while India adopts high-barrier films for export-oriented generics that meet FDA standards.

North America and Europe face a slower growth path. The U.S. CERCLA listing for long-chain PFAS elevates remediation liabilities and forces plants to install capture technology that raises operating expenses. European regulators pursue broad PFAS restrictions that create planning uncertainty for converters, even though PCTFE’s chemical profile differs from legacy surfactants. Aerospace programs such as NASA Artemis and Ariane 6 deliver predictable orders, but lack the explosive growth momentum of Asian semiconductor fabs. Competitive tension arises from Arkema’s PVDF expansion in Kentucky that targets battery and wafer wet-bench offerings.

South America, the Middle East, and Africa are witnessing rising demand for Polychlorotrifluoroethylene. Brazil scales blister-pack capacity for oncology and biologic therapies, though aluminum-PVC laminates still dominate mass-market prescriptions. Qatar and the United Arab Emirates explore PCTFE membranes for helium enrichment in new gas projects, adding specialized demand with high barrier requirements. South African chemical plants specify PCTFE linings for corrosive acids but remain niche buyers due to currency volatility and limited fabrication infrastructure. Regional adoption therefore trails global averages but provides a diversified demand floor that supports global supply-chain balance.

Competitive Landscape

Top Companies in Polychlorotrifluoroethylene (PCTFE) Market

The global polychlorotrifluoroethylene market is moderately consolidated, with key players driving innovation and operational efficiency. Companies are heavily investing in research and development to develop specialized grades for critical applications in aerospace, electronics, and pharmaceutical packaging. To enhance operational agility, firms are optimizing their manufacturing footprints and establishing strategic supply chain partnerships to secure consistent access to raw materials. Market leaders are expanding their distribution networks in emerging Asian markets while reinforcing their presence in established regions through the establishment of technical service centers. Vertical integration initiatives are being pursued to gain control over essential raw materials, alongside the development of application-specific product portfolios tailored to meet end-user requirements. Additionally, the industry is focusing on sustainable manufacturing processes and the introduction of eco-friendly product variants to comply with evolving regulatory standards and address changing customer preferences.

Polychlorotrifluoroethylene Industry Leaders

Honeywell International Inc.

Daikin Industries Ltd

Arkema

Solvay

HaloPolymer OJSC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: AGC Chemicals announced a surfactant-free fluoropolymer manufacturing process, targeting commercial scale by 2030.

- April 2024: Zhejiang Juhua filed Chinese patent CN 116731233 A for tuned-permeability fluorinated polymers applicable to PCTFE gas-separation membranes.

Global Polychlorotrifluoroethylene Market Report Scope

Polychlorotrifluoroethylene (PCTFE) is a type of fluoropolymer with outstanding dimensional stability, stiffness, and strength. The material has excellent flammability, radiation resistance, and chemical resistance properties.

The Polychlorotrifluoroethylene (PCTFE) market is segmented by application, end-user industry, and geography. By application, the market is segmented into films and sheets, wires and cables, coatings, and other applications. By end-user industry, the market is segmented into pharmaceutical, aerospace, electrical and electronics, and other end-user industries. The report also covers the market size and forecasts for the polychlorotrifluoroethylene market in 18 countries across major regions. The market sizing and forecasts for each segment have been done based on volume (Tons).

| Films and Sheets |

| Wires and Cables |

| Coatings |

| Other Applications |

| Pharmaceutical |

| Aerospace |

| Electrical and Electronics |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Turkey | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Films and Sheets | |

| Wires and Cables | ||

| Coatings | ||

| Other Applications | ||

| By End-user Industry | Pharmaceutical | |

| Aerospace | ||

| Electrical and Electronics | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Turkey | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected volume for the Polychlorotrifluoroethylene market in 2031?

The market is forecast to reach 8.21 million tons by 2031 at a 2.36% CAGR.

Which application segment leads current demand for Polychlorotrifluoroethylene?

Films and Sheets lead with 46.64% share in 2025, driven by pharmaceutical blister packaging.

Which region shows the fastest growth for Polychlorotrifluoroethylene demand?

Asia-Pacific grows the fastest with a 2.82% CAGR through 2031, supported by semiconductor and pharmaceutical investments.

Why is PCTFE preferred for cryogenic aerospace seals?

PCTFE keeps ductility and leak-tightness at –253 °C, unlike PTFE which becomes brittle in cryogenic service.

How do regulators influence the Polychlorotrifluoroethylene supply chain?

U.S. CERCLA designations and EU PFAS proposals raise compliance costs and encourage producers to adopt capture or destruction technologies for fluorinated emissions.

Which substitute materials pose the biggest threat to Polychlorotrifluoroethylene demand?

Lower-cost PTFE and PVDF compete on chemical resistance and easier processing, especially in commodity tubing and coatings.

Page last updated on: