Asia-Pacific Fluoropolymer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

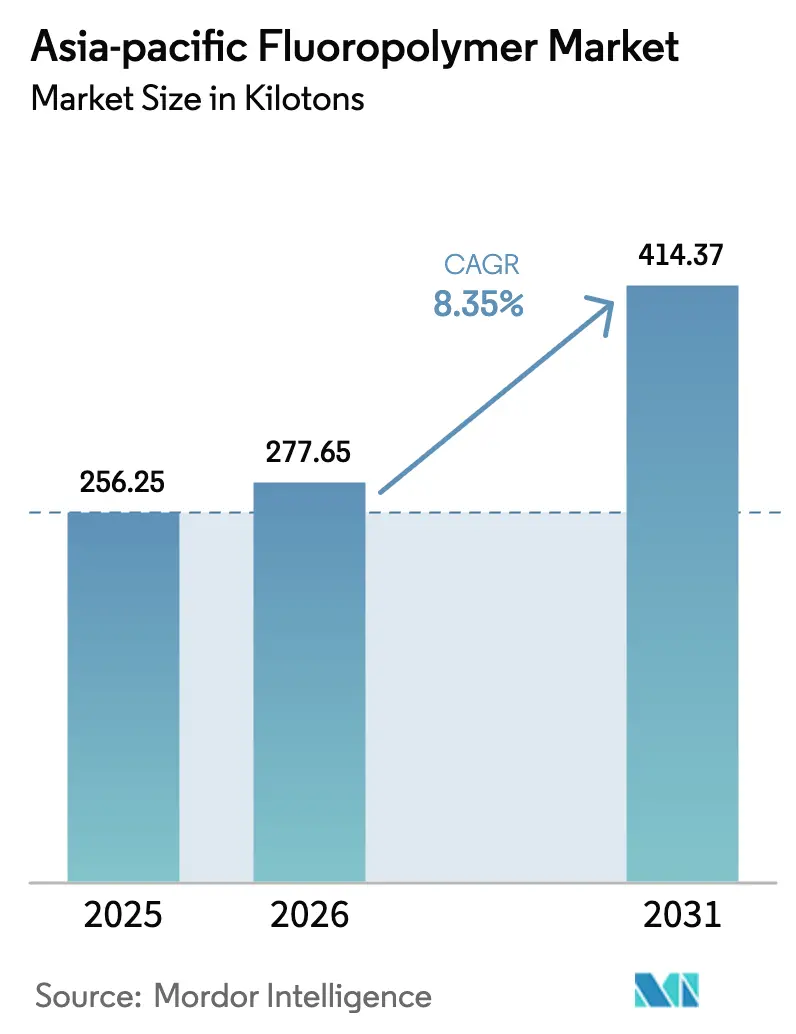

| Base Year Market Size (2025) | 256.25 kilotons |

| Market Volume (2026) | 277.65 kilotons |

| Market Volume (2031) | 414.37 kilotons |

| Growth Rate (2026 - 2031) | 8.35% CAGR |

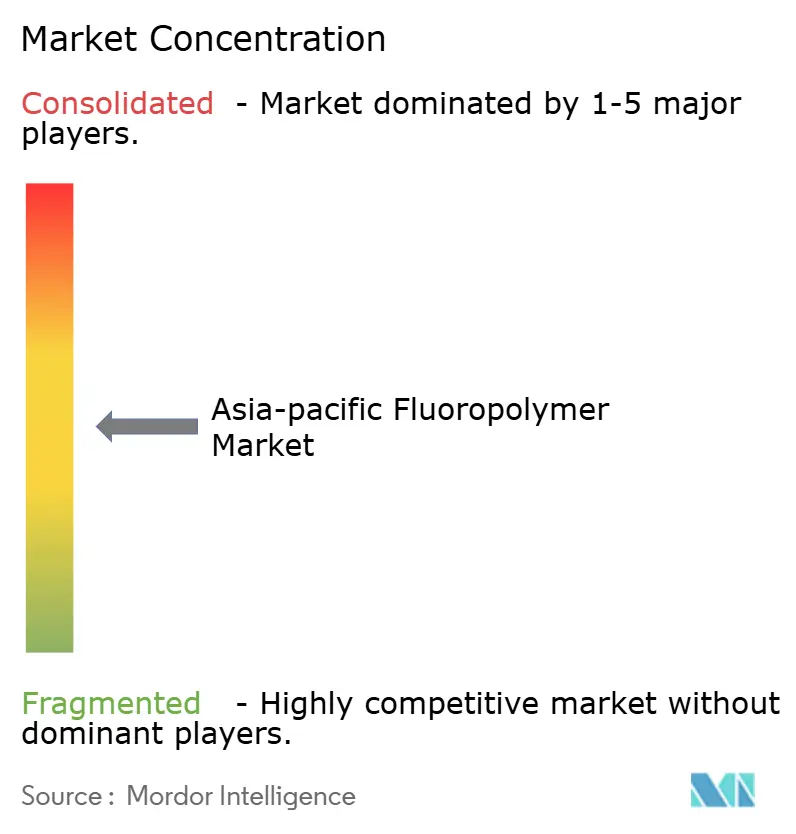

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Fluoropolymer Market Analysis by Mordor Intelligence

The Asia-Pacific Fluoropolymer Market size was valued at 256.25 kilotons in 2025 and estimated to grow from 277.65 kilotons in 2026 to reach 414.37 kilotons by 2031, at a CAGR of 8.35% during the forecast period (2026-2031). Momentum in electric-vehicle battery manufacturing, next-generation semiconductor fabrication, and advanced electronics assembly continues to drive the Asia-Pacific Fluoropolymer Market on a steady growth path. Widening uptake of high-purity grades in 3-nanometer nodes, sustained infrastructure investment, and the region’s cost-competitive production base further extend its global lead. Demand visibility has prompted both Western multinationals and fast-scaling Chinese suppliers to lock in multi-year offtake agreements, while downstream users intensify qualification programs for specialty grades that can meet tightening PFAS regulations. Raw-material volatility linked to R-142b and R-22 shortages remains a recurring challenge but is being mitigated through vertical integration and alternative synthesis routes.

Key Report Takeaways

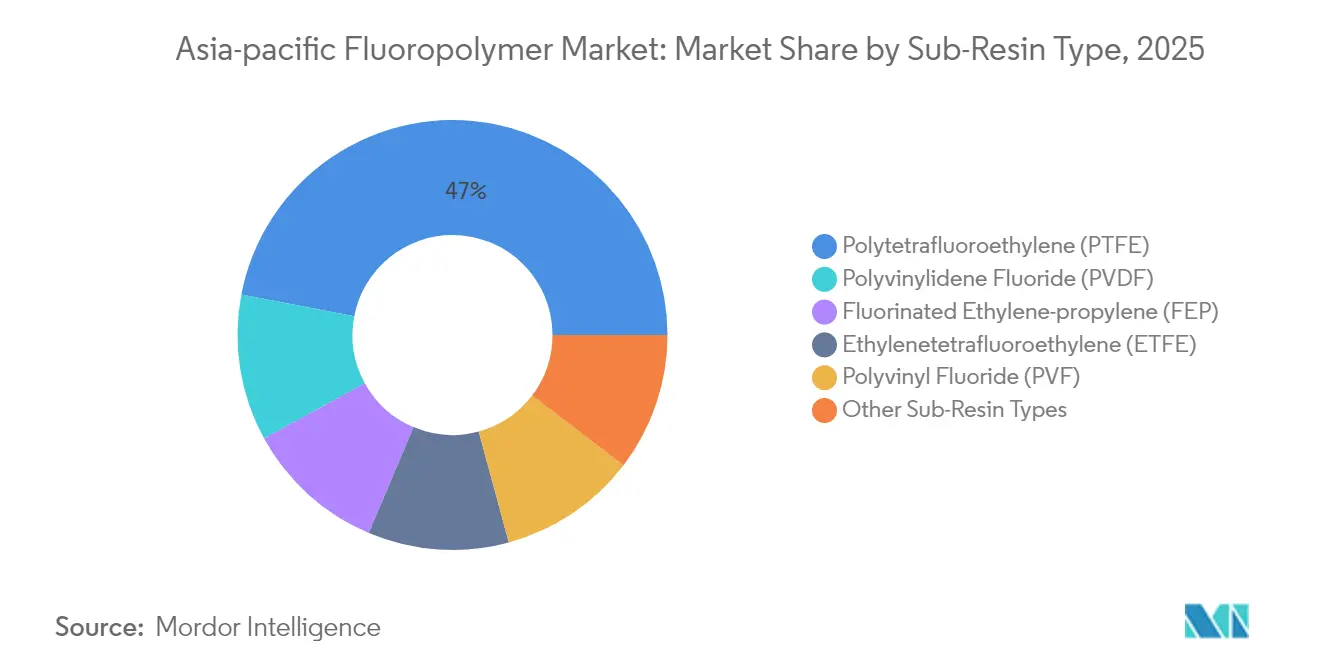

- By sub-resin type, polytetrafluoroethylene (PTFE) held 46.98% of the Asia-Pacific Fluoropolymer Market share in 2025. Polyvinylidene fluoride (PVDF) is forecast to advance at a 19.34% CAGR to 2031.

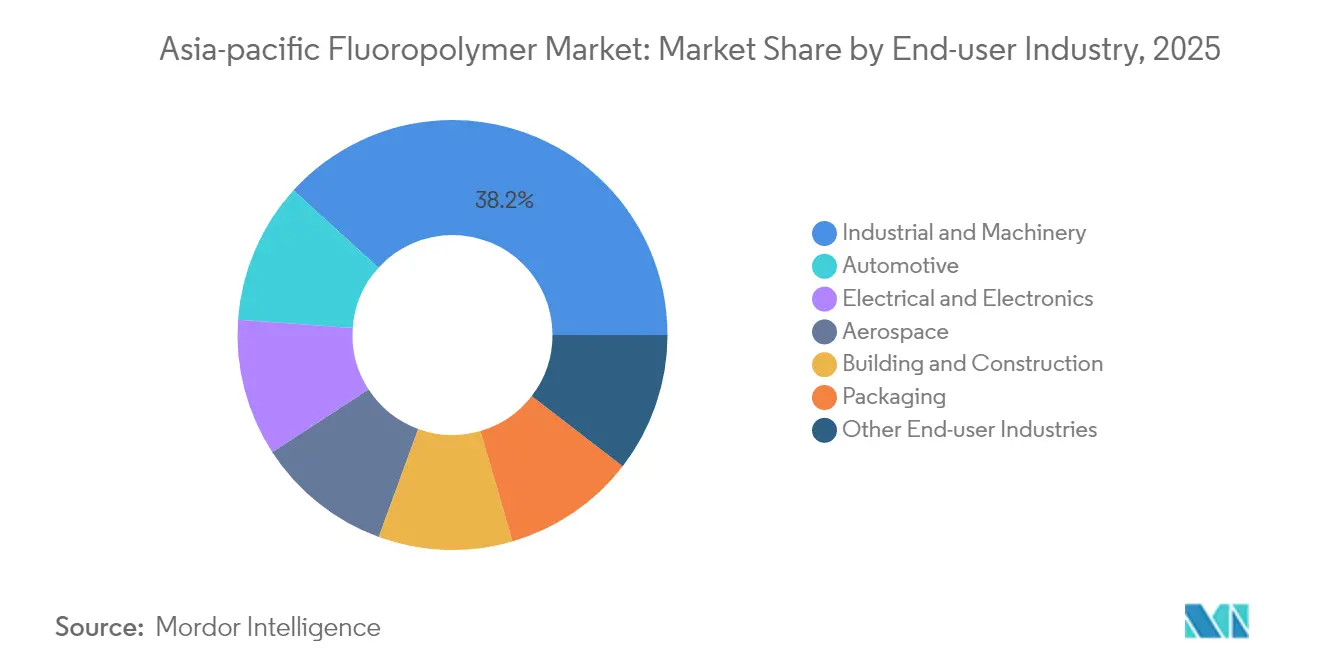

- By end-user industry, the industrial and machinery sector led with a 38.25% volume share in 2025. Automotive demand is projected to expand at a 15.95% CAGR through 2031.

- By geography, China captured a 61.25% share of the Asia-Pacific Fluoropolymer Market size in 2025 and is projected to grow at a 9.18% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Fluoropolymer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-grade PVDF demand surge from Asia’s battery supply-chain | +2.8% | China, South Korea, Japan, Southeast Asia | Medium term (2-4 years) |

| Electronics miniaturization driving high-purity PTFE & FEP | +1.9% | China, South Korea, Taiwan, Malaysia, Thailand | Long term (≥ 4 years) |

| Rapid build-out of semiconductor fabs in China & South Korea | +1.7% | China, South Korea, Japan | Medium term (2-4 years) |

| Construction shift to ETFE/PVF architectural membranes | +1.2% | China, Japan, Australia, India | Long term (≥ 4 years) |

| Sodium-ion battery separator pilots using modified PVDF | +0.9% | China, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV-Grade PVDF Demand Surge from Asia’s Battery Supply-Chain

Asia-Pacific’s lithium-ion battery capacity reached 1,200 GWh in 2024, and China alone accounted for 850 GWh[1]International Energy Agency, “Global Battery Supply-Chain Review 2025,” iea.org. This scale requires battery-grade PVDF for separators and binders that meet purity levels of under 500 ppm of metals, driving premiums of over 30% compared to industrial grades. CATL’s plan to add 500 GWh by 2027 signals a widening supply gap that spurs capacity additions by Solvay in Changshu and Arkema across the region. Chinese producers such as Dongyue Group have earmarked dedicated high-purity PVDF lines to secure domestic demand and eventually displace imports. The ongoing race to localize raw materials for electric vehicles anchors the Asia-Pacific Fluoropolymer Market to long-term structural volume growth.

Electronics Miniaturization Driving High-Purity PTFE & FEP

The shift to 3-nanometer logic, advanced packaging, and high-frequency 5G modules intensifies the need for purity requirements below 10 ppb for consumables and films. Foundry giants in Taiwan and South Korea set stringent benchmarks that only a handful of fluoropolymer grades can satisfy. Premium pricing and low tolerance for contamination have encouraged Chemours and Daikin to ring-fence dedicated semiconductor-grade output, essentially quarantining these lines from bulk industrial streams. Malaysia and Thailand’s contract manufacturers follow suit, adopting FEP films for flexible printed boards used in smartphones and automotive LiDAR. The Asia-Pacific Fluoropolymer Market, therefore, benefits from both top-end specification pull and volume ramp-up in the consumer electronics sector.

Rapid Build-Out of Semiconductor Fabs in China & South Korea

Beijing’s self-reliance agenda earmarks USD 150 billion in fab investments through 2027, with each advanced facility consuming 50-100 tons annually of PTFE, PFA, and related fluoropolymers. South Korea’s memory leaders add another 80 GWh worth of capacity, lengthening order books for semiconductor-grade materials and inflating lead times beyond 12 months. Suppliers respond by installing in-line particle analysis and dedicating reactors to avoid metal contamination, trends that consolidate high-purity supply under a handful of qualified plants. Long-term offtake agreements, in turn, stabilize cash flows for specialty producers, reinforcing vertical investment in the Asia-Pacific Fluoropolymer Market.

Construction Shift to ETFE/PVF Architectural Membranes

Large-span roofs and façades in China, Japan, and Australia increasingly specify 200-micron ETFE films or PVF-coated fabrics that last 30 years with minimal discoloration. Stadiums, airports, and retrofit solar canopies demonstrate a 65% weight savings compared to glass, resulting in lower structural steel requirements. Builders accept higher material costs in return for lifetime maintenance savings and daylighting benefits. Growing adoption in India’s commercial centers suggests a budding secondary demand base. As construction codes elevate energy-efficiency standards, ETFE membranes serve as both cladding and insulation, reinforcing the structural demand for the Asia-Pacific Fluoropolymer Market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile R-142b & R-22 feedstock availability | -1.8% | China, Japan, South Korea | Short term (≤ 2 years) |

| Escalating PFAS compliance costs in Japan & Australia | -1.2% | Japan, Australia, wider spillover | Medium term (2-4 years) |

| Unplanned outages at key HF plants in Shandong | -0.9% | China, whole Asia-Pacific supply chain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile R-142b & R-22 Feedstock Availability

Montreal Protocol enforcement cut Chinese R-142b output by 60% since 2023, spiking prices 40% and disrupting small- and mid-tier fluoropolymer plants[2]Chemical & Engineering News, “R-142b Feedstock Shortage,” cen.acs.org. Import dependence exposes producers to logistics shocks, while plant retrofits to non-ODS routes need 18-24 months. Integrated giants with captive HF units, including Chemours and Daikin, leverage backward integration to preserve margins, precipitating market consolidation. Short-term volatility affects order predictability and can delay downstream projects in the Asia-Pacific Fluoropolymer Market, particularly among electronics subcontractors that require just-in-time inventory management.

Escalating PFAS Compliance Costs in Japan & Australia

Japan’s essential-use regime, effective January 2025, obliges chemical makers to register every fluoropolymer application, adding USD 2-5 million yearly per site for monitoring and reporting. Australia’s parallel framework mandates environmental impact assessments, which can extend product approvals by up to 18 months. Companies shift R&D dollars toward low-bio-persistence chemistries, but commercial rollouts remain 5-7 years away. Interim compliance costs squeeze margins and can deter new entrants, yet they also catalyze innovation clusters that may eventually broaden the Asia-Pacific Fluoropolymer Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub-Resin Type: PTFE Dominance Meets PVDF Acceleration

Polytetrafluoroethylene (PTFE) claimed 46.98% of the Asia-Pacific Fluoropolymer Market share in 2025, driven by its applications in high-temperature seals, automotive gaskets, and chemical-processing linings. Mature end-uses ensure baseline growth aligned with industrial output across China, India, and Southeast Asia. Meanwhile, polyvinylidene fluoride is expected to register the fastest growth, with a 19.34% CAGR to 2031, driven by the demand for lithium-ion battery separators and binders, which account for 70% of the global cell capacity in the region. The Asia-Pacific Fluoropolymer Market size for PVDF is projected to increase alongside the growth of electric vehicle penetration and the expansion of stationary storage installations. Fluorinated ethylene-propylene (FEP) gains moderate momentum in wire-and-cable insulation for hyperscale data centers, whereas ETFE growth is tied to architectural membranes and chemical-tank linings, which require elevated chemical resistance.

Historical comparisons underline the shift: PVDF’s CAGR leapt from 12.8% during 2019-2024 to 19.34% through 2031. Polyvinyl fluoride strengthens via solar backsheets and façade films, while niche materials like perfluoroalkoxy and ECTFE carve a foothold in semiconductor wet benches and corrosion-prone pipelines. Regulatory pressure around PFAS persistence spurs R&D into modified PVDF architectures that degrade faster yet maintain electrochemical stability. Suppliers therefore allocate capital toward specialized grades with trace-metal thresholds under 100 ppb, positioning the Asia-Pacific Fluoropolymer Market for higher value capture per kilogram.

By End-User Industry: Industrial Backbone Supports Automotive Surge

Industrial and machinery customers accounted for 38.25% of volume in 2025, securing a stable demand for PTFE sheets, valve seats, and compressor components across petrochemical, pharmaceutical, and specialty chemical plants. The continuous expansion of refinery capacity in China and India underpins base demand, while process-safety codes increasingly favor fluoropolymer linings to mitigate corrosion and downtime. Automotive demand is projected to grow at a 15.95% CAGR through 2031, reflecting the shift to electric mobility. Battery modules integrate PVDF binders and coatings, high-voltage harnesses specify FEP, and fuel-cell stacks employ PTFE membranes. The Asia-Pacific Fluoropolymer Market size dedicated to automotive applications is forecast to surpass internal combustion components as OEMs increase their EV share to 50% by 2030.

Consumer electronics and semiconductor fabrication drive twin growth engines through the use of ultra-clean PTFE tubing, PFA wafer-process vessels, and FEP films for high-frequency circuits. Building and construction follows with ETFE stadium roofs, PVF wall cladding, and weather-resistant sealants. Aerospace remains a niche but high-margin market, utilizing PTFE-impregnated glass fabrics for wire harnesses and radome skins that can withstand temperatures of up to 200°C. Packaging grades of fluoropolymers serve pharmaceutical ampules and food pouches that require oxygen barriers, ensuring a balanced portfolio demand within the Asia-Pacific Fluoropolymer Market.

Geography Analysis

China’s 61.25% share in 2025, coupled with a 9.18% CAGR through 2031, affirms its dual status as volume leader and growth driver. Battery-grade PVDF consumption surpasses 40,000 tons annually, while semiconductor fabs import ultra-high-purity PTFE and FEP for 7-nanometer and finer nodes. Domestic conglomerates, such as Dongyue Group, integrate the production process from HF feedstock to finished fluoropolymers, thereby reducing logistics costs and enhancing export competitiveness.

Japan and South Korea anchor high-value niches that command premium prices. Japan’s semiconductor toolmakers adopt PTFE parts with ionic contamination below 50 ppb, while its automotive Tier-1 suppliers deploy PVDF in next-gen solid-state batteries. South Korea leverages leading memory manufacturers to source semiconductor-grade fluoropolymers and employs PVDF coatings in Hyundai’s EV packs. India, Australia, and Malaysia provide emerging vectors. India’s pharmaceutical output expansion and mega-refinery projects are fueling the uptake of PTFE and PVDF, aided by policy incentives under the Production-Linked Incentive scheme. Australia’s mining and chemical facilities require ETFE linings and PVF barriers to handle aggressive reagents under extreme UV exposure. Malaysia benefits from electronics manufacturing migration, as it consumes FEP and PTFE tubing in assembly plants. Collectively, these markets diversify demand sources and mitigate the Asia-Pacific Fluoropolymer Market's vulnerability to single-country shocks.

Competitive Landscape

The Asia-Pacific Fluoropolymer Market is moderately consolidated, with top multinationals competing against agile Chinese entrants. Chemours, Solvay, and Arkema protect IP-rich applications such as semiconductor-grade PFA and battery-grade PVDF that demand sub-10 ppb metal content. Over the medium term, compliance capability becomes a competitive moat, raising entry barriers and potentially consolidating the Asia-Pacific Fluoropolymer Market around players who can blend scale with regulatory expertise.

Asia-Pacific Fluoropolymer Industry Leaders

Daikin Industries, Ltd.

Dongyue Group

Gujarat Fluorochemicals Limited (GFL)

Arkema

Solvay

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: The Chemours Company (Chemours) announced the signing of strategic agreements with SRF Limited (SRF) in India. SRF is engaged in the manufacturing of industrial and specialty intermediates, including fluoropolymers. This collaboration strengthens Chemours’ global supply chain footprint, bolsters operational flexibility, and provides access to capacity for fluoropolymers.

- March 2024: Kureha Corporation has announced its decision to discontinue a capacity expansion project for polyvinylidene fluoride (PVDF) at its wholly owned subsidiary, Kureha Changshu Fluoropolymer Co., Ltd., in China.

Asia-Pacific Fluoropolymer Market Report Scope

Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging are covered as segments by End User Industry. Ethylenetetrafluoroethylene (ETFE), Fluorinated Ethylene-propylene (FEP), Polytetrafluoroethylene (PTFE), Polyvinylfluoride (PVF), Polyvinylidene Fluoride (PVDF) are covered as segments by Sub Resin Type. Australia, China, India, Japan, Malaysia, South Korea are covered as segments by Country.| Ethylenetetrafluoroethylene (ETFE) |

| Fluorinated Ethylene-propylene (FEP) |

| Polytetrafluoroethylene (PTFE) |

| Polyvinyl Fluoride (PVF) |

| Polyvinylidene Fluoride (PVDF) |

| Other Sub-Resin Types |

| Aerospace |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Packaging |

| Other End-user Industries |

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Malaysia |

| Rest of Asia-Pacific |

| By Sub-Resin Type | Ethylenetetrafluoroethylene (ETFE) |

| Fluorinated Ethylene-propylene (FEP) | |

| Polytetrafluoroethylene (PTFE) | |

| Polyvinyl Fluoride (PVF) | |

| Polyvinylidene Fluoride (PVDF) | |

| Other Sub-Resin Types | |

| By End-User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Packaging | |

| Other End-user Industries | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Malaysia | |

| Rest of Asia-Pacific |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the fluoropolymers market.

- Resin - Under the scope of the study, virgin fluoropolymer resins like Polytetrafluoroethylene, Polyvinylidene Fluoride, Polyvinylfluoride, Fluorinated Ethylene-propylene, Ethylenetetrafluoroethylene, etc. in the primary forms are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms