North America Fluoropolymer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

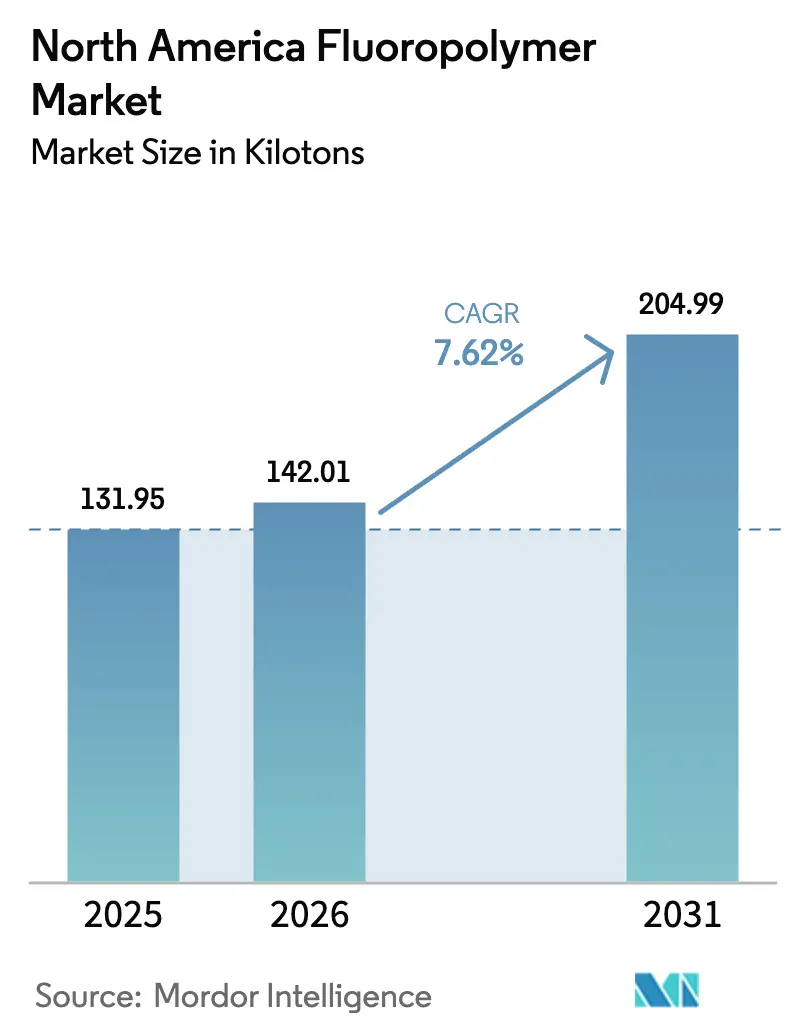

| Base Year Market Size (2025) | 131.95 kilotons |

| Market Volume (2026) | 142.01 kilotons |

| Market Volume (2031) | 204.99 kilotons |

| Growth Rate (2026 - 2031) | 7.62% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Fluoropolymer Market Analysis by Mordor Intelligence

North America Fluoropolymer Market size in 2026 is estimated at 142.01 kilotons, growing from 2025 value of 131.95 kilotons with 2031 projections showing 204.99 kilotons, growing at 7.62% CAGR over 2026-2031. Persistent demand from semiconductor fabrication, aerospace components, and corrosion-resistant chemical-processing equipment anchors volume expansion even as environmental regulations tighten across the region. Premium pricing power remains intact because each end user values performance attributes—chemical inertness, thermal stability, and dielectric strength—over raw-material cost fluctuations. In parallel, federal subsidies under the CHIPS and Science Act, sustained electric-vehicle (EV) investments, and gradual aerospace fleet renewal collectively reinforce the growth runway for the North America fluoropolymer market. Supply-side constraints rooted in PFAS compliance costs and fluorspar price volatility add complexity but have not derailed capital-spending programs among top converters.

Key Report Takeaways

- By sub-resin type, PTFE captured 49.12% of the North America fluoropolymer market share in 2025. PVDF is projected to expand at a 16.74% CAGR through 2031, making it the fastest-growing sub-resin segment.

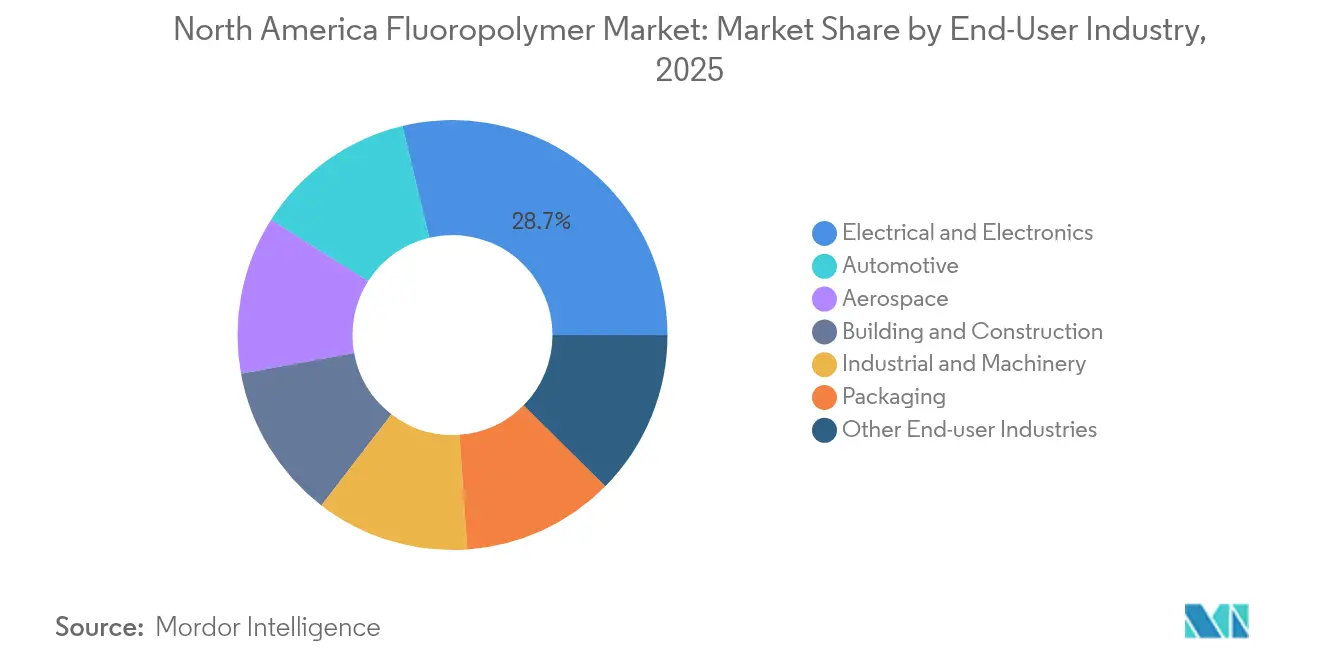

- By end-user industry, the electrical and electronics segment led with 28.74% revenue share in 2025. Automotive applications are forecast to climb at a 12.61% CAGR to 2031.

- By geography, the United States commanded 90.32% of the regional volume in 2025 and is advancing at an 7.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Fluoropolymer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding electronics & electrical demand | +2.10% | United States core, Canada spillover | Medium term (2-4 years) |

| Automotive & aerospace lightweighting | +1.80% | North America wide, Mexico manufacturing focus | Long term (≥ 4 years) |

| Growth in chemical-processing corrosion-resistant assets | +1.40% | United States Gulf Coast, Alberta oil sands | Medium term (2-4 years) |

| U.S. semiconductor-fab build-out (CHIPS Act) | +1.90% | United States concentrated | Short term (≤ 2 years) |

| Data-center wire-&-cable boom | +0.90% | North America wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Electronics & Electrical Demand

Semiconductor fabrication equipment is the single highest-value application within the North America fluoropolymer market, and ultra-pure PTFE and PFA components routinely trade above USD 50 per kg because contamination thresholds sit below 10 ppb[1]Semiconductor Industry Association, “CHIPS Act Implementation Progress Report 2024,” sia.org . The CHIPS Act’s USD 39 billion incentive pool is underwriting 23 new fabs across Arizona, Texas and Ohio, each of which incorporates 200–300 tons of clean-room-grade fluoropolymers for fluid handling and wafer-processing modules. Taiwan Semiconductor Manufacturing Company’s Arizona complex alone will consume approximately 450 tons of ETFE and PFA tubing annually once both production lines reach nameplate capacity, reinforcing a localized supply chain loop that favors regional converters with ISO 14644-certified facilities. Parallel data-center buildouts by Microsoft and Amazon Web Services add a secondary pull for ETFE-jacketed cables that meet stringent smoke-toxicity limits in closed server halls. Consequently, electronics customers continue to underwrite long-term supply agreements even amid raw-material price swings, preserving margin stability for qualified fluoropolymer producers.

Automotive & Aerospace Lightweighting

Rapid electrification drives PVDF adoption in lithium-ion battery separators and binders, with each Tesla Model S containing about 12 kg of battery-grade PVDF. General Motors has earmarked USD 35 billion through 2025 to localize EV supply chains and has signed multi-year sourcing accords that prioritize North American fluoropolymer suppliers for binder, separator and wire-coating formulations. In aerospace, PTFE and PFA seals continue to displace legacy elastomers because they tolerate −100 °C to +260 °C flight-cycle extremes, and Boeing’s 737 MAX production ramp combined with Airbus A321XLR certification sustains 4–5% annual volume growth for these materials. The twin upswings in mobility end markets lengthen order visibility for PVDF and high-performance PTFE grades, reinforcing capacity-expansion logic for established resin producers.

Growth in Chemical-Processing Corrosion-Resistant Assets

Petrochemical operators on the U.S. Gulf Coast and Alberta oil sands have accelerated fluoropolymer retrofits to curb unplanned downtime. ExxonMobil’s USD 2 billion Baytown refinery upgrade integrates PTFE-lined reactors and ETFE-coated heat exchangers that extend service life by up to 12 years versus stainless-steel alternatives. Suncor Energy reports a 40% drop in pipeline-replacement frequency after switching to PVDF-lined flowlines in bitumen dilution units. These case studies validate the total-cost-of-ownership narrative that underpins steady procurement even when spot resin prices spike.

U.S. Semiconductor-Fab Build-Out (CHIPS Act)

The CHIPS Act has set off a construction wave whose near-term material call-off is already visible in purchase orders for semiconductor-grade PTFE, ETFE and PFA tubing. Intel’s USD 20 billion Ohio project has pre-qualified three domestic suppliers for 125 tons of PTFE wet-etch tubing and 80 tons of PFA fittings for Phase 1 alone. Early-stage demand is so concentrated that qualified inventories routinely clear within days, allowing suppliers to command 300–400% premiums over industrial-grade equivalents. The locational clustering of new fabs within a 500-mile radius of Phoenix further raises transportation barriers for Asian exporters whose door-to-door transits exceed 45 days.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PFAS regulatory tightening | -1.70% | United States federal, state variations | Medium term (2-4 years) |

| Fluorspar/raw-material price volatility | -1.20% | North America wide | Short term (≤ 2 years) |

| Community litigation & permitting hurdles | -0.80% | United States concentrated | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PFAS Regulatory Tightening

The Environmental Protection Agency has classified PFOA and PFOS as hazardous substances under CERCLA, obliging producers to fund remediation and install advanced abatement systems that can cost USD 50 million per site[2]Environmental Protection Agency, “National Drinking Water Standard to Protect Communities from PFAS Pollution,” epa.gov . Chemours has booked USD 1.2 billion in cumulative liabilities for legacy PFAS discharges at Fayetteville Works and now levies environmental surcharges of 8–12% on every fluoropolymer invoice, pushing downstream customers to re-price finished goods. While no immediate production shutdowns have occurred, project proponents routinely add 6–9 months to permitting timelines as state regulators demand groundwater-impact modeling. Smaller processors lacking balance-sheet flexibility are therefore scaling back capacity-expansion plans, trimming effective supply in the North America fluoropolymer market.

Fluorspar/Raw-Material Price Volatility

China controls the majority of global fluorspar exports, and its 2024 quota reductions drove a 35% surge in average landed cost for North American buyers within four months. Arkema reported USD 45 million in third-quarter margin compression because feedstock spikes could not be passed through existing contracts fast enough. Mexican mining expansions may relieve pressure by 2026, yet lead times of 18–24 months mean converters must navigate recurrent raw-material swings in the interim. Hedging strategies remain limited because forward markets are illiquid, leaving cost-plus models as the primary buffer against volatility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub-Resin Type: PTFE Dominance Faces PVDF Innovation Challenge

PTFE retained 49.12% of the North America fluoropolymer market share in 2025, buoyed by deep entrenchment in semiconductor wet-etch systems and chemical-processing reactors that expose materials to acids above 200 °C. The North America fluoropolymer market size attributed to PTFE applications is projected to reach 96.1 kilo tons by 2031 as every new fab deploys 150–200 tons of PTFE across tubing, fittings and valve bodies. PTFE’s ultra-low dielectric constant also supports high-frequency radar arrays, safeguarding incremental demand from defense electronics over the forecast window. While PTFE’s incumbency gives it price stability, the regulatory spotlight on legacy emulsion-polymerization surfactants compels manufacturers to accelerate non-PFAS processing routes. Capacity debottlenecking therefore focuses on melt-granule grades that bypass aqueous surfactants and ease wastewater treatment loads.

PVDF is tracking a 16.74% CAGR through 2031, the quickest pace within the North America fluoropolymer market, because battery-grade formulations unlock 300 Wh/kg cell energy densities in next-generation EV platforms. The North America fluoropolymer market size for PVDF is forecast to top 36.9 kilo tons by 2031 as Tesla, Ford and General Motors collectively target 6 million annual EV assemblies. Beyond mobility, PVDF architectural coatings offer 30-year weathering warranties, expanding pull from commercial-roof retrofit projects across hurricane-exposed Gulf states. Specialty grades such as copolymeric PVDF-HFP (hexafluoropropylene) further widen solvent windows for solid-electrolyte interface stabilization in all-solid-state batteries, ensuring that PVDF’s innovation pipeline remains robust even if separator densities fall. Collectively, these vectors chip away at PTFE’s volumetric dominance while fostering a more diversified resin mix.

By End-User Industry: Electronics Leadership Challenged by Automotive Acceleration

Electronics and electrical applications held 28.74% of 2025 volume, placing them at the top of the North America fluoropolymer market hierarchy. Every advanced lithography step now specifies fluoropolymer delivery lines to prevent metal-ion contamination, and hyperscale data-center builds adopt ETFE-jacketed Category 6a cables to satisfy smoke-toxicity codes. Growth rates do normalize in the outer years once the current fab-construction cycle peaks, but refurbishment schedules and process-node migrations should sustain recurrent pull.

Automotive demand is rising at a 12.61% CAGR—fastest among tracked verticals—because EV battery separators, binder systems and high-temperature wire harnesses rely on PVDF and ETFE to meet thermal-runaway criteria. Each mid-size SUV battery pack embeds 8–12 kg of fluoropolymer content, and lightweight ETFE insulation trims up to 20% harness mass compared with PVC, directly extending driving range. As U.S., Canadian and Mexican plants localize cell and module output under USMCA rules of origin, resin producers gain logistical advantages over Asian suppliers facing 8-week sea-freight cycles. The North America fluoropolymer industry’s automotive pipeline therefore supports double-digit growth until at least 2031, even if internal-combustion vehicle volumes plateau.

Geography Analysis

The United States accounted for 90.32% of regional consumption in 2025, reflecting its dense cluster of semiconductor fabs, specialty-chemical complexes, and aerospace assembly lines. Federal incentives totaling USD 52.7 billion under the CHIPS Act have already unlocked USD 200 billion in private wafer-fabrication outlays, each demanding ultra-pure fluoropolymer fluid-handling systems that few offshore suppliers can qualify within procurement windows. PFAS-compliance costs are highest in states such as North Carolina and West Virginia, yet plant closures are limited because tier-one customers foot environmental-surcharge bills. The North America fluoropolymer market therefore retains a U.S. core that logs an 7.77% CAGR through 2031, supported by domestic content rules and proximity advantages.

Canada contributes a measured but resilient share anchored in oil-sands upstream operations and a niche aerospace supply chain. Suncor’s shift to PVDF-lined pipelines in Alberta substantiates a 40% reduction in maintenance outlays, reinforcing the cost-benefit proposition despite smaller volume baselines. Bombardier’s regional-jet program maintains demand for FEP and PFA wire bundles that endure high-altitude thermal swings. Although volumes trail U.S. levels, Canadian buyers often pay 10–15% premiums to secure just-in-time deliveries during winter months when transport corridors face weather disruptions, thereby supporting healthy margins for regional distributors.

Mexico’s growth vector stems from EV assembly localization under the USMCA. General Motors’ USD 1 billion Ramos Arizpe retooling allocates procurement budgets for PVDF separators and ETFE harnesses sourced from within North America to capture tariff exemptions. Domestic resin-polymerization know-how remains limited, channeling demand toward U.S. plants that extrude semi-finished forms before shipping them south for component fabrication. As new battery-cell joint ventures come online, Mexican fluoropolymer consumption could outpace Canada, yet its share remains constrained by lower semiconductor exposure.

Competitive Landscape

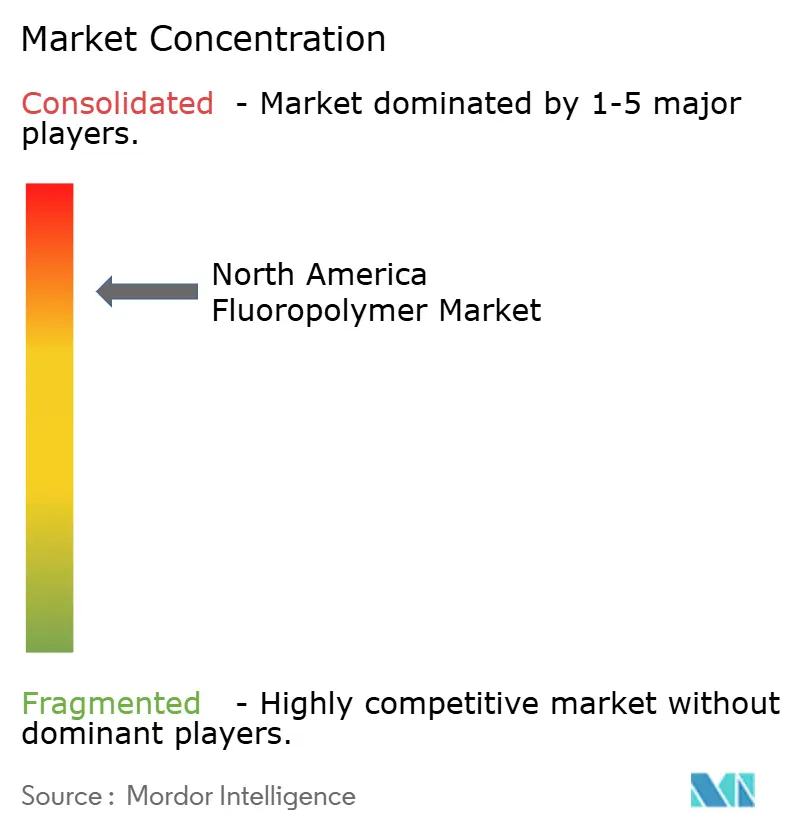

The North America fluoropolymer market exhibits highly consolidated concentration. Chemours safeguards PTFE leadership through captive fluorspar derivatives and a broad Teflon portfolio, enabling prioritized allocation to semiconductor OEMs even during feedstock shortages. Arkema controls the largest regional PVDF footprint and is investing USD 20 million to boost Calvert City output by 15%, specifically targeting battery-grade Kynar HSV 900 that omits fluorosurfactants without sacrificing electrochemical stability. Daikin leverages Japanese process discipline to court aerospace and defense primes that stipulate long certification cycles, thereby locking in multi-year supply contracts.

Strategic playbooks increasingly emphasize sustainability credentials. Chemours, 3M and Daikin each devote USD 100–200 million to PFAS-abatement R&D, aiming to replace long-chain surfactants with short-chain or polymeric alternatives that attenuate bioaccumulation risk. Syensqo’s recent acquisition of Solvay’s specialty-polymer assets accelerates end-market diversification into medical devices and 3D-printing powders, hedging against cyclical downturns in any single vertical. Price mechanisms trend toward quarterly indexing tied to fluorspar benchmarks, while semiconductor-grade products keep value-based premiums intact due to rigorous validation hurdles.

M&A prospects favor bolt-on deals that deliver application expertise or geographic adjacency rather than pure-play capacity. Private equity interest remains muted after elevated compliance liabilities surfaced in 2024 under CERCLA amendments, yet infrastructure funds are assessing greenfield PVDF projects linked to battery corridors in the U.S. Midwest. Intellectual-property barriers stay formidable: resin formulation recipes, sintering profiles and clean-room extrusion protocols carry proprietary status that restricts fast follower entry. The competitive equation thus hinges on balancing environmental stewardship against end-user qualification lead times that can exceed two years.

North America Fluoropolymer Industry Leaders

3M

AGC Inc.

Arkema

Daikin Industries Ltd.

The Chemours Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Arkema announced that its scientists and engineers have received an award from the American Chemical Society (ACS) for their innovative development of Kynar HSV 900 PVDF, a fluorosurfactant-free solution for battery applications. This award reflects Arkema's commitment to innovation and sustainability in the e-mobility sector.

- February 2025: Arkema has announced plans to expand its PVDF production capacity by 15% at its Calvert City, Kentucky, facility in the United States, supported by an investment of approximately USD 20 million. This initiative aligns with the Group's strategy to strengthen its global PVDF footprint in response to market growth.

North America Fluoropolymer Market Report Scope

Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging are covered as segments by End User Industry. Ethylenetetrafluoroethylene (ETFE), Fluorinated Ethylene-propylene (FEP), Polytetrafluoroethylene (PTFE), Polyvinylfluoride (PVF), Polyvinylidene Fluoride (PVDF) are covered as segments by Sub Resin Type. Canada, Mexico, United States are covered as segments by Country.| Ethylenetetrafluoroethylene (ETFE) |

| Fluorinated Ethylene-propylene (FEP) |

| Polytetrafluoroethylene (PTFE) |

| Polyvinyl Fluoride (PVF) |

| Polyvinylidene Fluoride (PVDF) |

| Other Sub-Resin Types |

| Aerospace |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Packaging |

| Other End-user Industries |

| United States |

| Canada |

| Mexico |

| By Sub-Resin Type | Ethylenetetrafluoroethylene (ETFE) |

| Fluorinated Ethylene-propylene (FEP) | |

| Polytetrafluoroethylene (PTFE) | |

| Polyvinyl Fluoride (PVF) | |

| Polyvinylidene Fluoride (PVDF) | |

| Other Sub-Resin Types | |

| By End-User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Packaging | |

| Other End-user Industries | |

| By Geography | United States |

| Canada | |

| Mexico |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the fluoropolymers market.

- Resin - Under the scope of the study, virgin fluoropolymer resins like Polytetrafluoroethylene, Polyvinylidene Fluoride, Polyvinylfluoride, Fluorinated Ethylene-propylene, Ethylenetetrafluoroethylene, etc. in the primary forms are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms