Fluorinated Polyimide Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.28 Billion |

| Market Size (2031) | USD 1.65 Billion |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fluorinated Polyimide Market Analysis by Mordor Intelligence

The Fluorinated Polyimide Market size is estimated at USD 1.28 billion in 2026, and is expected to reach USD 1.65 billion by 2031, at a CAGR of 5.21% during the forecast period (2026-2031). A measured headline number masks a strategic shift from rigid substrates toward ultra-thin, heat-stable films that underpin foldable displays, millimeter-wave antennas, and radiation-tolerant solar arrays. Unit growth in smartphones is leveling off, yet display makers are widening the design envelope to rollable televisions, foldable laptops, and curved automotive dashboards, all of which sustain substrate demand. Semiconductor packaging houses have moved to finer line-and-space architectures, pulling through low-dielectric-constant fluorinated grades that survive 400 °C reflow processes. Meanwhile, commercial satellite constellations and Saudi-led solar megaprojects amplify demand for radiation-hardened and UV-resistant films, offsetting slower momentum in Europe and North America, where PFAS regulations inflate compliance costs.

Key Report Takeaways

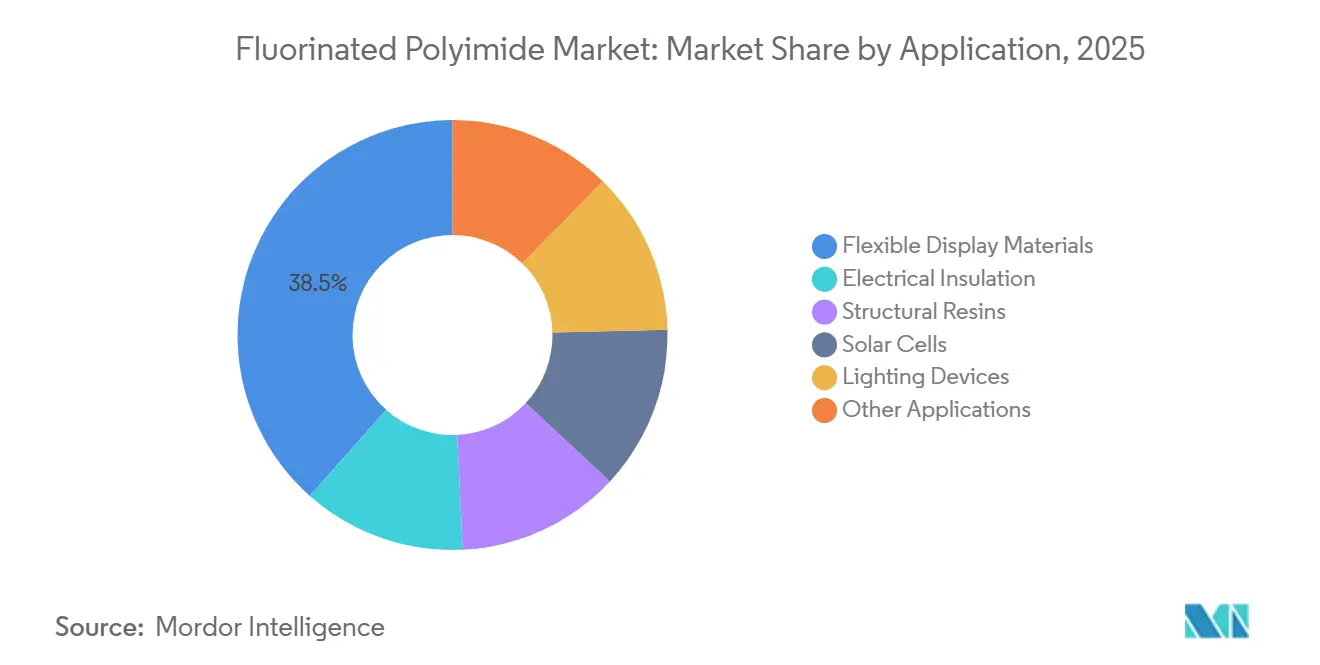

- By application, flexible display materials led with a 38.46% revenue share of the fluorinated polyimide market in 2025, while solar cells are advancing at a 6.34% CAGR through 2031.

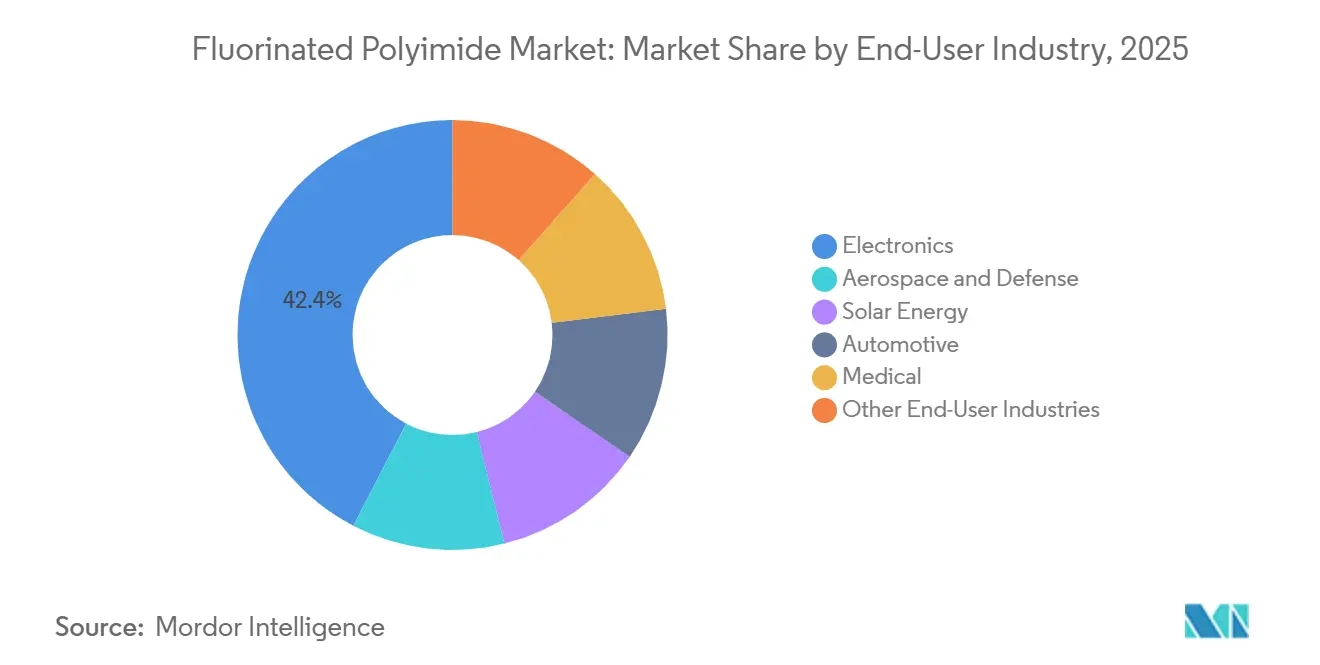

- By end-user industry, electronics accounted for 42.37% of the fluorinated polyimide market share in 2025, whereas solar energy is projected to expand at a 6.41% CAGR to 2031.

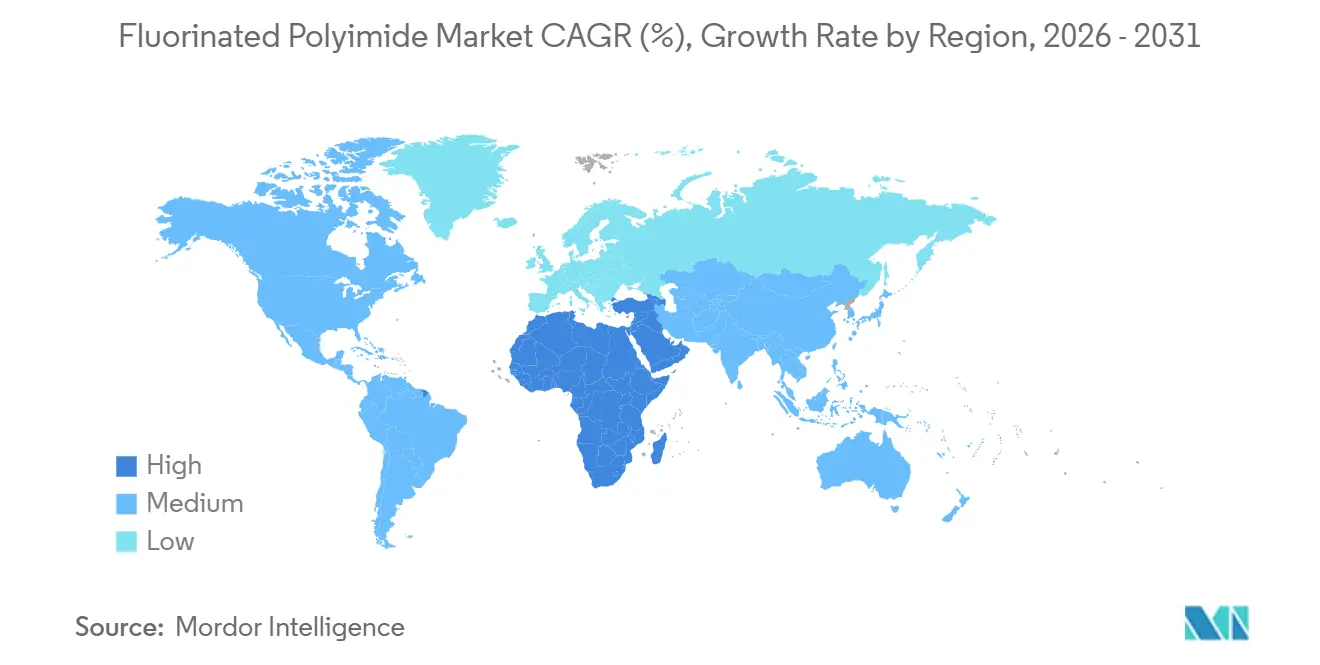

- By geography, Asia-Pacific contributed 49.28% of the 2025 value, and the Middle East and Africa region is forecast to post a 5.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fluorinated Polyimide Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in consumer demand for flexible display devices | +1.3% | APAC core (South Korea, China), spill-over to North America | Short term (≤ 2 years) |

| Ramp-up of 5G/high-frequency infrastructure necessitating low-Dk films | +1.2% | Global, with early concentration in APAC and North America | Medium term (2-4 years) |

| Electronics miniaturization demanding ultra-thin, heat-resistant substrates | +0.9% | Global, led by APAC electronics hubs | Medium term (2-4 years) |

| Space-grade solar-array substrates requiring radiation-hardened FPIs | +0.7% | North America, Europe (satellite programs), emerging in Middle East | Long term (≥ 4 years) |

| Additive manufacturing unlocks on-site custom aerospace components | +0.6% | North America, Europe (aerospace clusters) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Consumer Demand for Flexible Display Devices

Foldable smartphones have shifted from concept to mainstream, and the installed base of flexible OLED lines now exceeds 15 plants in South Korea and China. Each line consumes colorless fluorinated polyimide films thinner than 50 µm that must survive 200,000-fold cycles without cracking. Fluorination lowers the refractive index and curbs yellowing, helping devices maintain color gamut across their service life. Samsung’s Galaxy Z series shipped several million units in 2025; by extending foldable form factors to mid-tier price points, panel makers expect to double substrate throughput by 2028. Hybrid stacks combining ultra-thin glass and fluorinated polyimide balance scratch resistance with flexibility, a trend likely to spread to automotive clusters and wearable screens.

Ramp-up of 5G/High-Frequency Infrastructure Necessitating Low-Dk Films

Millimeter-wave antennas operating beyond 24 GHz demand low dielectric constants and dissipation factors. Fluorinated polyimides maintain a high glass-transition temperature, allowing for seamless integration into antenna-in-package modules without the risk of warpage. In 2025, base station deployments surged, and the trend of densifying with small cells further amplified the demand for low-loss flex circuits. IEEE laminate guidelines have shortened qualification cycles, permitting material suppliers to convert pilot-plant output to commercial scale faster than in prior wireless generations.

Electronics Miniaturization Demanding Ultra-Thin, Heat-Resistant Substrates

System-in-package designs are now stacking multiple dies within footprints with high power density. Redistribution layers and die-attach films, made from fluorinated polyimide tapes, can withstand high solder reflow temperatures without outgassing. Fan-out wafer-level packaging, a method embraced by foundries in Taiwan and South Korea, completely does away with rigid substrates. Instead, it utilizes polymer layers for signal routing, significantly increasing the demand for polymers in each package. As chipmakers shift towards chiplet architectures for 2.5-D integration, the anticipated rise in interconnect layers is set to further amplify this demand.

Space-Grade Solar-Array Substrates Requiring Radiation-Hardened FPIs

Fluorinated polyimides have become essential for solar arrays destined for space, thanks to their resilience against proton and electron flux degradation and atomic oxygen attacks. These materials maintain their mechanical strength even after exposure to high-energy electron radiation, surpassing the performance of their non-fluorinated counterparts. Weighing significantly less than rigid panels, the film enables satellite designers to fit larger arrays within fixed payload envelopes. With commercial broadband constellations planning to deploy thousands of satellites by 2030, each designed to carry flexible cells, the demand for radiation-hardened films is poised to grow significantly.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs and raw-material volatility | -0.8% | Global, acute in regions with limited monomer supply | Short term (≤ 2 years) |

| Stringent PFAS-related environmental regulations | -0.7% | North America, Europe; potential spill-over to APAC | Medium term (2-4 years) |

| OLED image-sticking failures linked to fluoride-ion migration | -0.6% | APAC core (South Korea, China), North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Production Costs and Raw-Material Volatility

Hexafluoroisopropylidene-based dianhydrides command multiples of conventional aromatics, reflecting multi-step syntheses and specialized containment. An unplanned outage at a single supplier can spike spot prices within weeks, and currency swings magnify volatility because many contracts are denominated in euros or yen. Integrated players such as DuPont and Daikin can buffer disruptions by back-integrating into monomers, but smaller converters lack this hedge and face allocation risk during tight markets.

Stringent PFAS-Related Environmental Regulations

In 2023, the European Chemicals Agency proposed sweeping restrictions on around 10,000 PFAS compounds under REACH[1]European Chemicals Agency, “Annex XV Restriction Report: Per- and Polyfluoroalkyl Substances (PFASs),” ECHA.EUROPA.EU. This move includes high-molecular-weight fluorinated polyimides, compelling companies to demonstrate the absence of safer alternatives for every specific use. Meanwhile, in April 2024, the U.S. EPA classified PFOA and PFOS as hazardous substances under CERCLA. This designation brings about cradle-to-grave liability and necessitates expensive upgrades to wastewater systems. As a result, compliance could increase production costs and postpone the introduction of new grades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Displays Dominate Volume, Solar Cells Accelerate

Flexible display materials captured 38.46% of 2025 revenue, mirroring the proliferation of foldable and rollable OLED products. This slice of the fluorinated polyimide market is sustained by South Korean and Chinese fabs expanding Gen-6 lines and by automotive OEMs piloting curved dashboards. Electrical insulation—wire coatings, motor slot liners, transformer tapes—delivers stable volume because utilities favor proven dielectrics over cheaper substitutes.

Solar cells are projected to log a 6.34% CAGR, the highest among applications, as mega-constellations and Middle East concentrator farms demand radiation-hardened and UV-stable backsheets. Lighting devices such as OLED luminaires adopt thin, transparent films for architectural and automotive ambient lighting, a modest but rising outlet. Niche uses—from medical catheters to high-frequency connectors—round out the application mix, underscoring material versatility.

By End-User Industry: Electronics Leads, Solar Energy Surges

Electronics held 42.37% of 2025 demand, anchored in smartphones, tablets, and laptops. Growth now depends on emerging form factors—foldable laptops, flexible monitors, augmented-reality glasses—rather than incremental handset volume. Aerospace and defense capitalize on flame resistance and dimensional stability; fluorinated grades meet FAA flammability norms without halogens, simplifying end-of-life handling. Additive manufacturing of custom brackets adds an incremental pull as qualified printers spread across maintenance depots.

Solar energy is forecast to post a 6.41% CAGR, the fastest among end users, fueled by orbital power systems and desert-based concentrator farms that require backsheets resilient to UV and particle bombardment. Automotive demand stretches beyond instrument clusters to heating elements, heads-up displays, and battery busbars. Medical applications—catheter liners, implantable electrode carriers—leverage reduced protein adsorption to extend device life, while oil-and-gas sensors and industrial automation labels furnish steady niche consumption.

Geography Analysis

Asia-Pacific held 49.28% of the 2025 value on the back of South Korea’s flexible OLED dominance and China’s 5G rollout. Samsung Display, LG Display, and BOE collectively control most of the world’s foldable-panel throughput, consuming large volumes of colorless films. Japan retains expertise in monomer synthesis; suppliers like Kaneka and Ube provide high-purity feedstocks, sustaining a regional ecosystem unbeatable on cost and quality. India is ramping up electronics assembly, though substrates remain largely imported.

Growth in North America is propelled by aerospace and satellite projects. DuPont’s Circleville, Ohio, expansion added Kapton and Pyralux capacity, targeting EV battery interconnects and 5G antenna modules. Regulatory drag in the United States—where CERCLA liability applies to PFAS—pressures margins and encourages some converters to shift secondary processing offshore.

In Europe, the market is divided between Germany’s in-car electronics, France and the UK’s aerospace composites, and specialized industrial niches. The broad PFAS restriction proposal lengthens approval cycles and deters greenfield investment. Airbus and satellite primes continue to specify fluorinated films, but consumer-electronics manufacturing remains minimal compared with Asia. South America and the Middle East and Africa together account for small revenue; the latter will expand at 5.92% as Saudi Arabia and the UAE roll out gigawatt-scale solar farms that mandate heat-stable, low-outgassing backsheets.

Competitive Landscape

The fluorinated polyimide market is moderately consolidated in nature. Integrated players command monomer synthesis, film calendaring, and downstream coating, ensuring end-to-end quality control. Capital intensity is high; DuPont invested USD 220-250 million between 2019 and 2022 to boost Kapton capacity at Circleville, underscoring barriers to entry[2]DuPont, “DuPont Announces Major Investment in Kapton Polyimide Capacity,” DUPONT.COM . Niche converters in South Korea and Taiwan have carved competitive space in ultra-thin, colorless films tailored to specific hinge radii and scratch-resistant overlays. Many operate in close collaboration with panel makers, co-locating pilot coaters inside clean rooms to accelerate iterative design. Emerging opportunities include additive manufacturing feedstocks and bio-based fluorinated polyimides. Aerospace primes seek pellet-fed extruders that avoid nozzle clogging while printing high-temperature parts on demand. Regulatory scrutiny of PFAS is steering research and development toward partially fluorinated or renewable dianhydrides, though current bio-routes still trail incumbents on thermal stability. Chinese newcomers, buoyed by state subsidies, are racing to localize monomer production, potentially eroding incumbent pricing power in commodity display grades.

Fluorinated Polyimide Industry Leaders

DuPont

Kaneka Corporation

Kolon Industries

Sumitomo Chemical Co. Ltd.

Daikin Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Arkema and its affiliate PI Advanced Materials introduced the Zenimid brand for high-performance polyimide films, broadening penetration into aerospace, automotive, and electronics sectors.

- July 2023: French chemicals group Arkema has acquired a 54% stake in South Korea's PI Advanced Materials (PIAM), enhancing its foothold in consumer electronics and electric mobility. Arkema secured the shares from Glenwood Private Equity, a Seoul-based investor. PIAM specializes in polyimide films, known for their high heat resistance and electrical insulation properties. These films are pivotal in printed circuit boards, especially for smartphones and various other applications.

Global Fluorinated Polyimide Market Report Scope

Fluorinated polyimides belong to the class of high-performance plastics designed by using fluorine-containing diamines or dianhydrides as monomers. Fluorinated polyimides are ingrained with dielectric properties and resistance to heat, temperature, and chemicals. The high-end properties of fluorinated polyimides have caused them to capture the market of electronics and the optoelectronics segment with applications in photovoltaics, display devices, flexible printed circuit boards, etc. In comparison to conventional polyimides, fluorinated polyimides offer superior solubility properties, low dielectric constant, and high optical transparency, which have made them extremely popular in display devices used in consumer electronics, healthcare, aerospace, etc.

The fluorinated polyimide market is segmented by application, end-user industry, and geography. By application, the market is segmented into flexible display materials, electrical insulation, structural resins, solar cells, light devices, and other applications. By end-user industry, the market is segmented into electronics, aerospace and defense, solar energy, automotive, medical, and other end-user industries. The report also covers the market size and forecasts for the fluorinated polyimide market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done based on value (USD).

| Flexible Display Materials |

| Electrical Insulation |

| Structural Resins |

| Solar Cells |

| Lighting Devices |

| Other Applications |

| Electronics |

| Aerospace and Defense |

| Solar Energy |

| Automotive |

| Medical |

| Other End-User Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Flexible Display Materials | |

| Electrical Insulation | ||

| Structural Resins | ||

| Solar Cells | ||

| Lighting Devices | ||

| Other Applications | ||

| By End-User Industry | Electronics | |

| Aerospace and Defense | ||

| Solar Energy | ||

| Automotive | ||

| Medical | ||

| Other End-User Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the fluorinated polyimide market in 2026, and what growth rate is expected?

The fluorinated polyimide market size reached USD 1.28 billion in 2026 and is projected to rise to USD 1.65 billion by 2031 at a 5.21% CAGR.

Which application segment leads revenue?

Flexible display materials led with a 38.46% share in 2025, reflecting heavy use in foldable and rollable OLED products.

Which end-user industry is expanding the fastest?

Solar energy shows the highest growth, forecast to post a 6.41% CAGR through 2031 as orbital and desert solar projects multiply.

Why is Asia-Pacific dominant in fluorinated polyimide demand?

Co-location of OLED panel facilities, semiconductor packaging hubs, and 5G network rollouts gives Asia-Pacific 49.28% of the 2025 value and a continuing scale advantage.

How are PFAS regulations affecting producers?

U.S. CERCLA designations and the EU’s broad PFAS restriction proposal add compliance costs, extend product-approval timelines, and may prompt reformulation or relocation of capacity.

Page last updated on: