Flexible Film Packaging Machines Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

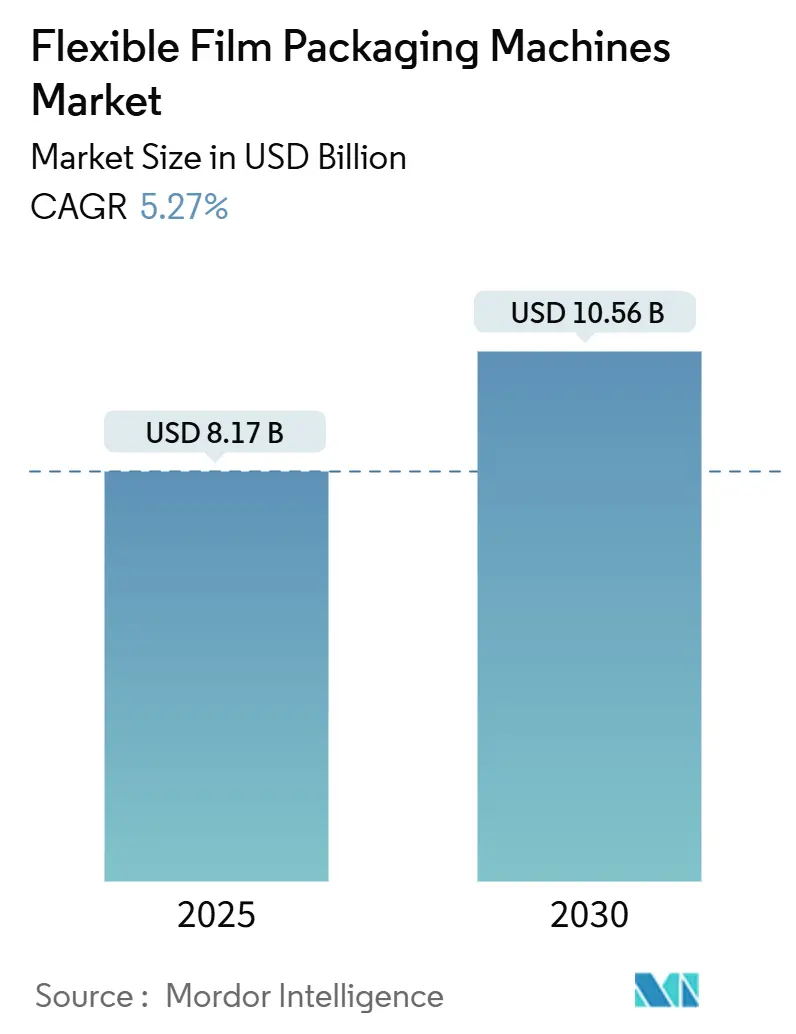

| Market Size (2025) | USD 8.17 Billion |

| Market Size (2030) | USD 10.56 Billion |

| Growth Rate (2025 - 2030) | 5.27% CAGR |

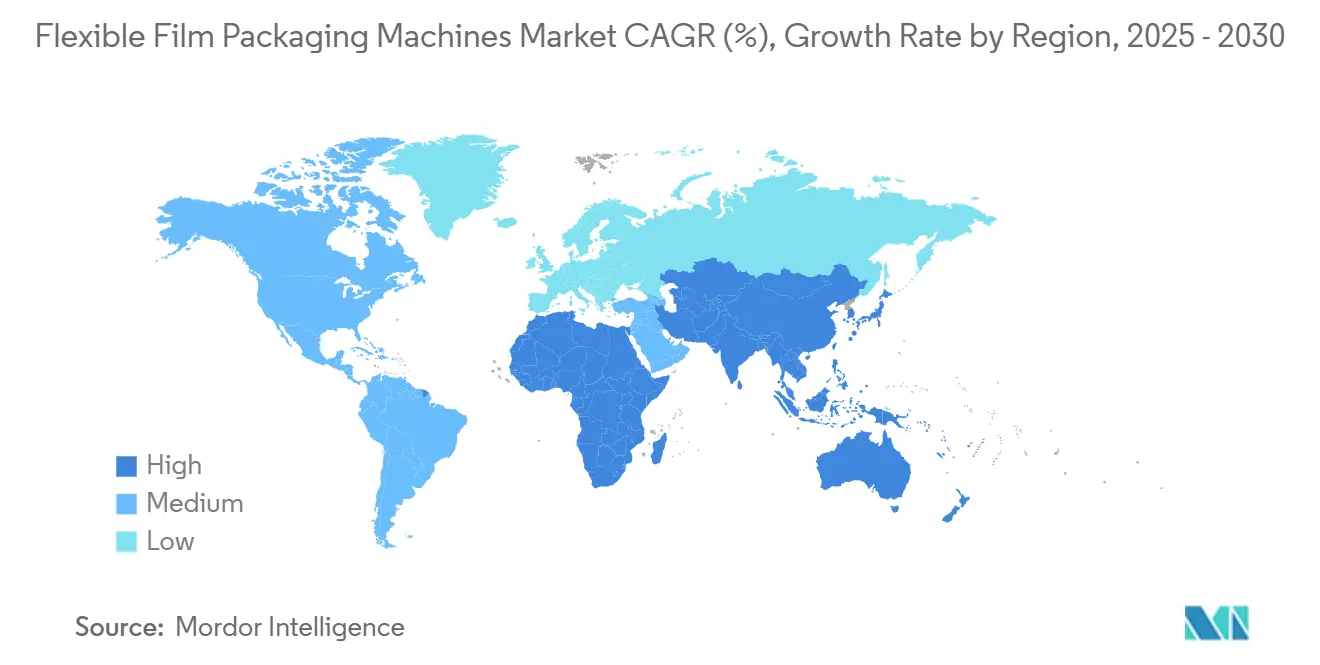

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flexible Film Packaging Machines Market Analysis by Mordor Intelligence

The flexible film packaging machines market size reached USD 8.17 billion in 2025 and is projected to increase to USD 10.56 billion by 2030, registering a 5.27% CAGR during the forecast period. Several forces shape this trajectory, including e-commerce growth that drives demand for protective yet lightweight packs, rising consumer preference for single-serve portions that reduce production runs, and increasing regulatory pressure for recyclable materials. Technology convergence is equally important: suppliers routinely embed Industry 4.0 sensors, AI-enabled vision, and predictive maintenance into classic form-fill-seal lines, cutting downtime and material waste. Automation now offsets labor shortages, with 77% of manufacturers reporting hiring challenges; meanwhile, precision controls help processors meet corporate sustainability pledges without compromising throughput. The flexible film packaging machines market benefits from government subsidies in the Asia-Pacific region, the expansion of contract packaging organizations (CPOs) in North America, and capital recycling among European converters as they upgrade to mono-material capability.[1]Asia Pacific Foundation of Canada, “India's 2024 Budget Prioritizes Foreign Investment, Manufacturing,” asiapacific.ca

Key Report Takeaways

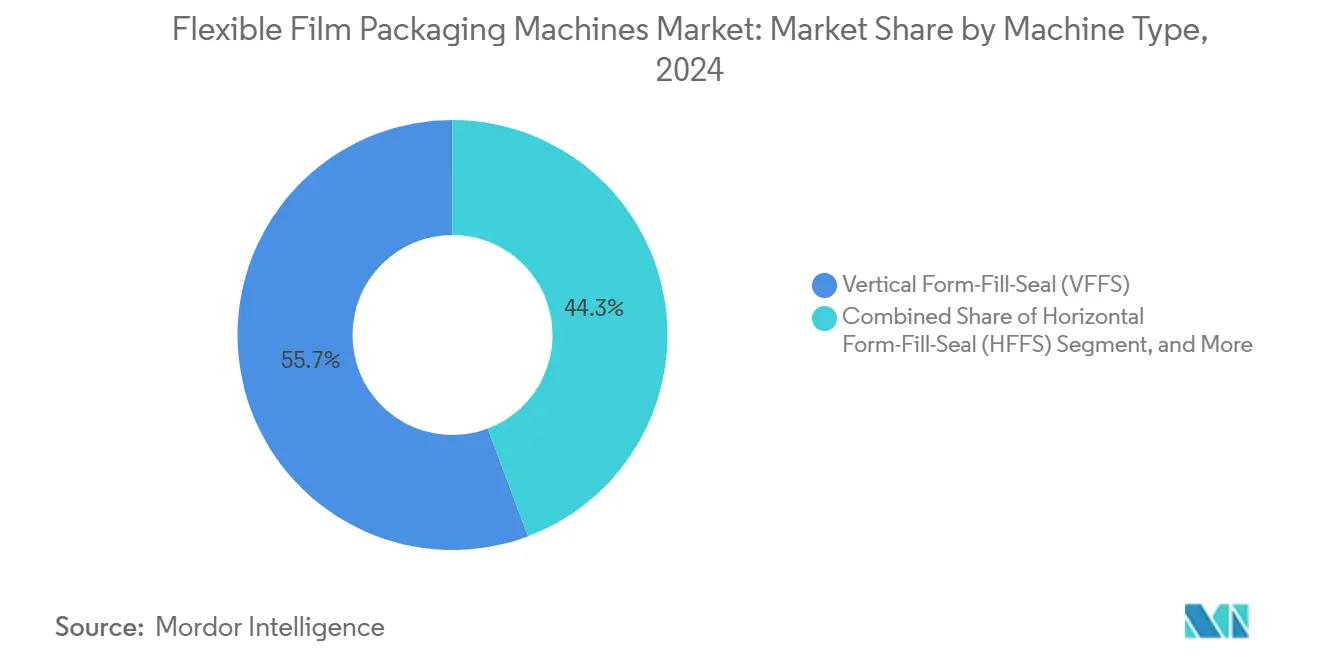

- By machine type, the Vertical Form-Fill-Seal equipment segment captured 55.74% of the flexible film packaging machines market share in 2024.

- By automation level, the flexible film packaging machines market size for Fully Automatic systems is projected to grow at a 6.28% CAGR between 2025–2030.

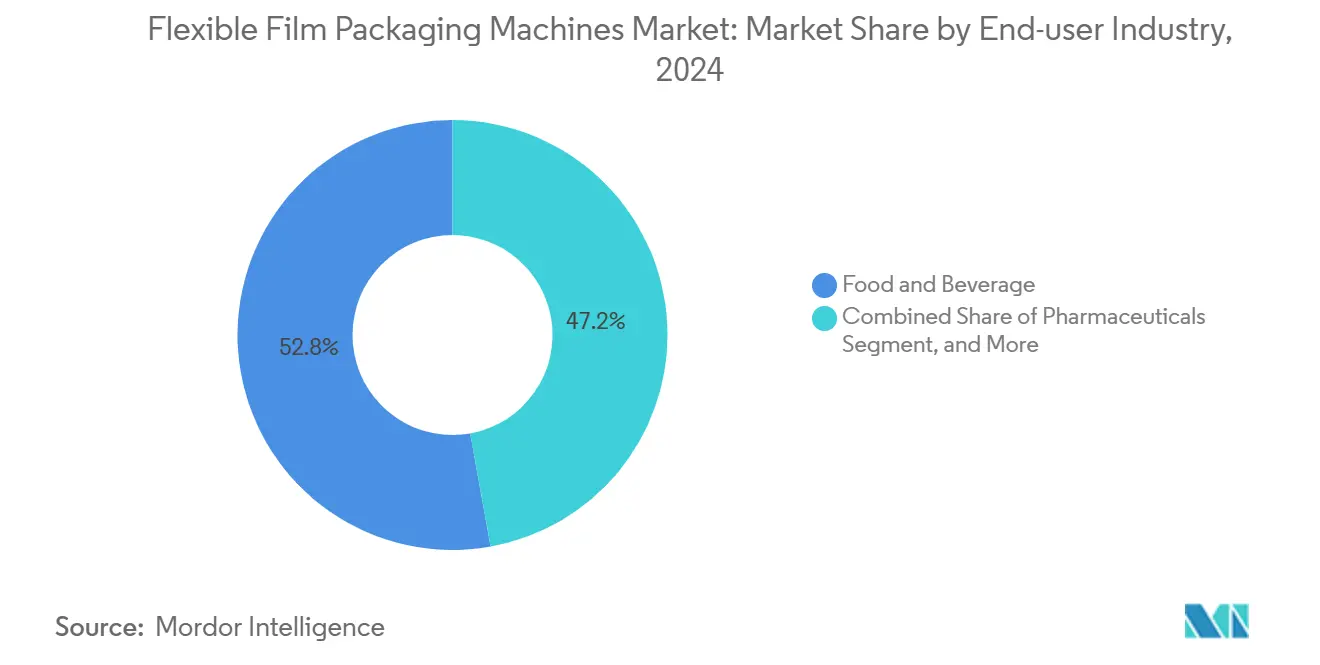

- By end-user industry, the food and beverage segment captured 52.83% of the flexible film packaging machines market share in 2024.

- By geography, the flexible film packaging machines market size in South America is projected to grow at a 6.79% CAGR between 2025-2030.

Global Flexible Film Packaging Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Single-serve convenience boom | +1.2% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Industry 4.0 and automation surge | +1.5% | APAC core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Sustainability-driven machine upgrades | +0.8% | Europe and North America, expanding to APAC | Long term (≥ 4 years) |

| Explosive growth in e-commerce | +1.1% | Global, led by APAC and North America | Short term (≤ 2 years) |

| Rise of contract packaging organisations (CPOs) | +0.6% | North America and Europe, emerging in APAC | Medium term (2-4 years) |

| Asia-Pacific subsidies for domestic OEMs | +0.5% | APAC core, particularly China and India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Industry 4.0 and automation surge

Artificial intelligence, Internet of Things connectivity, and predictive maintenance are redefining modern flexible film packaging lines. AI vision flags foreign particles in milliseconds, while machine-learning algorithms automatically tune sealing parameters to ambient humidity, reducing film waste and energy consumption. Such autonomy eases the talent crunch that leaves 77% of manufacturers short of skilled operators. Syntegon’s SVX series exemplifies this shift by pairing high-output form-fill-seal modules with condition monitoring dashboards that enhance overall equipment effectiveness to nearly 99%. The flexible film packaging machines market now sees entire production cells orchestrated by single-line control platforms that synchronize mixing, weighing, filling, and palletizing, creating data loops that drive continuous improvement.

Single-serve convenience boom

Smaller household sizes, on-the-go lifestyles, and portion-control diets boost demand for packs that weigh only a few grams yet run at elevated cycle speeds. E-commerce compounds the trend: individual sachets cushion products during parcel handling and permit right-sized shipping cartons. PMMI forecasts indicate that filling and dosing systems, core to single-serve formats, will capture more than 20% of total global packaging machinery sales by 2027. Rapid-changeover features enable producers to juggle multiple SKUs without incurring costly downtime, a priority as brands rush to launch limited-time flavors and health-oriented variations. These dynamics reinforce volume growth for the flexible film packaging machines market across snacks, baby foods, nutraceuticals, and personal-care wipes.

Sustainability-driven machine upgrades

Regulators and brand pledges raise the bar on recyclability, driving capital toward equipment that forms packs from mono-material polyethylene, paper-polymer laminates, or bio-based films. The EU Machinery Regulation 2023/1230 introduced new safety and eco-design obligations for all packaging assets. Unilever aims to reduce 100,000 tonnes of virgin plastic, a goal that requires converters to deploy machines like Syntegon’s PMX, which can seal recyclable films while consuming up to 30% less energy. The Fraunhofer IVV Pack4Sense project unveiled thermoforming processes for detachable cardboard-plastic composites, demonstrating how R&D can reduce polymer content without compromising barrier life. The resulting demand lifts the flexible film packaging machines market as converters swap their legacy assets for new, sustainable models.

Explosive growth in e-commerce

Global online retail sales surge prompts shippers and brand owners to prioritize tamper-evident packaging, compact dimensions, and customer-friendly unboxing. Contract packagers report that 67% of brand owners plan to maintain or increase outsourcing for e-commerce tasks, thereby reinforcing order pipelines for high-speed pouch, mailer, and sachet lines. Flexible formats help minimize dimensional weight fees while ensuring product integrity through multi-layer barrier films and zip reclosures. Machine builders consequently integrate downstream case packers and robotic palletizers, which are tuned for automated fulfillment centers. This ecosystem effect amplifies the revenue potential for the flexible film packaging machines market across both developed and emerging economies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for SMEs | -0.7% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| Skilled-labour shortage | -0.9% | North America and Europe, spreading to APAC | Medium term (2-4 years) |

| Chip-set supply-chain bottlenecks | -0.4% | Global, most severe in high-tech automation segments | Short term (≤ 2 years) |

| Paper-based packaging substitution trend | -0.3% | Europe and North America, limited APAC impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for SMEs

Fully automatic lines with embedded analytics often exceed USD 2 million, a hurdle beyond many small processors. Even compact thermoformers, tailored for modest output, still require a significant upfront investment in auxiliary chilling, air, and tooling. Financing is tighter in emerging economies, while currency swings inflate import prices. Some vendors respond with modular pay-as-you-grow configurations, yet adoption remains slow. SMEs that delay upgrades risk missing sustainability compliance and losing private-label contracts, which limits addressable volume for the flexible film packaging machines market.[2]GEA, “New Thermoforming Packaging Machine at FachPack,” gea.com

Skilled-labour shortage

Modern lines mix mechanics, electronics, pneumatics, and software. Finding technicians fluent in all four is difficult, especially in rural production hubs. Downtime rises when scarce experts rotate among multiple plants, driving managers to favor self-diagnosing machines and remote support dashboards. Vendors build user interfaces with guided wizards and mixed-reality headsets for troubleshooting, but these aids cannot fully replace the expertise of qualified personnel. Persistent vacancies constrain commissioning schedules and slow project payback, moderating expansion of the flexible film packaging machines market in high-wage regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: VFFS dominance faces pouch challenge

Vertical Form-Fill-Seal equipment accounted for 55.74% of the flexible film packaging machines market share in 2024, underscoring its suitability for high-volume snack and cereal lines that prioritize speed and low unit cost. Pre-made Pouch Fillers, despite having a smaller base, are growing at a 6.53% CAGR due to the demand for premium coffee, pet treats, and nutraceuticals, which require intricate graphics and consumer-friendly closures. The flexible film packaging machines market continues to favor VFFS for commodity rice and sugar packs; however, brand owners are shifting their investment to pouch fillers, where differentiation commands higher retail margins. The rising adoption of recyclable mono-material pouches adds another catalyst, as precise temperature control is easier to achieve with pre-made pouch units.

VFFS suppliers defend their market share by incorporating quick-change forming sets and servo-based tension control, which reduces film scrap. In parallel, pouch system vendors shorten cycle times by utilizing dual-lane infeed and integrating ultrasonic sealing that handles paper-based laminates. Horizontal Form-Fill-Seal machines serve the bar confectionery industry, where precise orientation is crucial, while stretch wrappers are gaining popularity in industrial bulk packaging. Thermoformers gain traction for shelf-ready meat and cheese trays processed from thinner films. Bag-making machines, though niche, remain popular in Africa and parts of South Asia where labor cost advantages keep semi-automated models attractive. This diverse mix ensures that the flexible film packaging machines market remains healthy, with healthy competition and momentum for innovation.

By Automation Level: Labor shortages accelerate full automation

Fully automatic lines captured 52.12% of the flexible film packaging machines market size in 2024 and are projected to post a 6.28% CAGR through 2030. Acute staffing gaps in mature economies make autonomy essential rather than optional, pushing processors to favor machines that self-adjust seal pressure, log downtime reasons, and order spare parts proactively. Predictive algorithms that flag motor bearing wear before failure minimize unplanned halts, strengthening the business case. Semi-automatic units maintain presence among small coffee roasters and regional bakery plants where batch flexibility outweighs volume pressure.

Manual stations remain prevalent in micro-enterprise settings, but they are losing ground as governments offer tax credits for automation. The flexible film packaging machines industry also witnesses cost reductions for servo drives and vision sensors, lowering entry barriers for mid-tier buyers. Pharmaceutical packagers are adopting robotic pouch loaders that keep operators outside ISO-class enclosures, aligning with stringent contamination control rules. Over the next five years, cloud analytics and subscription software will turn machinery into service platforms, pushing overall adoption curves and further entrenching full automation within the flexible film packaging machines market.

By End-user Industry: Pharma growth challenges food dominance

Food and beverage users accounted for 52.83% of the flexible film packaging machines market share in 2024, benefiting from steady demand for snacks, dairy products, and frozen meals. However, pharmaceuticals exhibit the fastest 6.63% CAGR, reflecting aging populations and stricter dosing protocols that favor unit-dose sachets and stick packs. Serialization mandates in many countries compel drug makers to invest in inline printers and vision inspectors, bundled with high-precision form-fill-seal modules. Cosmetics and personal care lines adopt refill pouch concepts, while industrial and household chemicals prioritize multilayer barrier films that withstand corrosive contents.

The flexible film packaging machines market experiences cross-sector learning as food processors borrow pharma-grade hygiene designs, and drug firms emulate snack quick-change ideas to manage SKU proliferation. Syntegon’s Telstar acquisition enhances its fill-finish and isolator offerings, enabling turnkey sterile lines that cater to vaccine and biologics producers. Meanwhile, CPOs absorb demand spikes by installing multi-purpose pouch and stick pack equipment, providing smaller drug brands with access to advanced packaging without requiring them to own assets. These dynamics diversify revenue streams and accelerate the transfer of technology across various user industries.

Geography Analysis

Asia-Pacific’s 37.42% stake in 2024 reflects policy-backed industrialization and deep supply chain linkages that keep component sourcing local and costs competitive. Chinese OEMs benefit from tax credits on smart manufacturing equipment, enabling them to undercut imports while improving quality. India’s 2024 federal budget earmarked USD 574 billion for infrastructure and manufacturing, driving new plant builds that specify automated pouch and sachet units. Japan’s Supply Chain Diversification Program allocates USD 2 billion for regional relocation, directing machinery orders to line integrators with experience in rapid validation protocols.[3]ERIA, “Harnessing India–Japan Economic Partnership for Supply Chain Resilience,” eria.org

North America and Europe represent mature yet lucrative replacement markets. PMMI indicates that United States shipments reached USD 10.9 billion in 2023 and are expected to continue rising, driven by single-serve demand and the adoption of robotics. European buyers prioritize energy-efficient servo systems and recyclable film compatibility to comply with Green Deal tenets. Canada imported CAD 791.6 million worth of machinery in 2024, primarily from Germany and Italy, underscoring the enduring transatlantic flow of technology.

South American growth outpaces averages as processed food exports climb and consumer goods multinationals localize production. Brazil leverages agribusiness surpluses to build modern filling plants, while Chile applies flexible film to protect copper concentrate shipments against moisture. The flexible film packaging machines market further gains traction in the Middle East and Africa, where diversified economies prefer light, space-saving packs for desert logistics. Saudi Arabia’s SAR 1 billion packaging complex investment will feature advanced pouch and thermoform lines, underscoring how fiscal stimuli can broaden geographic demand.

Competitive Landscape

The flexible film packaging machines market remains moderately fragmented. Syntegon, Ishida, and Coesia anchor the premium tier by bundling engineering expertise with global service. Barry-Wehmiller moves up the value chain through 2025 acquisitions of Systec Conveyors and Automatan, a strategy that stitches material handling and robotics into turnkey lines. ProMach expands its regional reach by adding HMC Products, offering mid-market buyers integrated pouch, label, and cartoning solutions.

Technology rivalry centers on software. Krones introduces AI-enabled process control that optimizes blower pressure on stretch blow molders, hinting at similar future features for pouch inflation. MULTIVAC launches all-electric thermoformers for small plants, attacking the SME affordability gap with modular layouts. Start-ups position cloud dashboards that normalize machine data across mixed fleets, giving processors predictive insights without vendor lock-in.

Regulation shapes barriers to entry. Vendors with ISO-class buildrooms and FDA-validated suites secure pharmaceutical orders ahead of competitors lacking comparable documentation depth. Patent filings climb in sealing tool geometry, paper-film lamination techniques, and remote diagnostics, cementing intellectual moats. Regional players survive by focusing on after-sales and spare parts availability, vital in Latin America where customs delays can idle a line.

Flexible Film Packaging Machines Industry Leaders

Duravant LLC

Ishida Co., Ltd.

Syntegon Technology GmbH

IMA Industria Macchine Automatiche S.p.A.

ProMach, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Barry-Wehmiller completed acquisitions of Systec Conveyors and Automatan, broadening its packaging automation scope.

- November 2024: Syntegon finalized the Telstar acquisition, integrating isolator and freeze-dryer solutions into its pharma line portfolio.

- October 2024: ProMach bought HMC Products, boosting its capabilities in pouch and bag forming equipment.

- August 2024: GEA debuted a compact thermoforming machine for SMEs at FachPack 2024, targeting cost-sensitive food processors.

Global Flexible Film Packaging Machines Market Report Scope

| Horizontal Form-Fill-Seal (HFFS) |

| Vertical Form-Fill-Seal (VFFS) |

| Pre-made Pouch Fillers |

| Stretch Wrappers |

| Bag-Making Machines |

| Thermoformers |

| Other Machine Types |

| Manual |

| Semi Automatic |

| Fully Automatic |

| Food and Beverage |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| Industrial and Household Chemicals |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Machine Type | Horizontal Form-Fill-Seal (HFFS) | ||

| Vertical Form-Fill-Seal (VFFS) | |||

| Pre-made Pouch Fillers | |||

| Stretch Wrappers | |||

| Bag-Making Machines | |||

| Thermoformers | |||

| Other Machine Types | |||

| By Automation Level | Manual | ||

| Semi Automatic | |||

| Fully Automatic | |||

| By End-user Industry | Food and Beverage | ||

| Pharmaceuticals | |||

| Cosmetics and Personal Care | |||

| Industrial and Household Chemicals | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the flexible film packaging machines market?

It stands at USD 8.17 billion in 2025 with a projected rise to USD 10.56 billion by 2030.

Which region leads global demand for flexible film packaging machines?

The Asia-Pacific region commands 37.42% of 2024 revenue, thanks to its manufacturing scale and policy incentives.

Which machine type holds the largest market share?

Vertical Form-Fill-Seal equipment leads with 55.74% share in 2024.

Why are fully automatic systems gaining popularity?

Labor shortages and the need for consistent output are driving processors toward fully automatic lines that incorporate predictive maintenance and remote monitoring.

Which end-user segment is growing the fastest?

Pharmaceuticals, supported by unit-dose packaging and strict regulatory compliance, is advancing at a 6.63% CAGR through 2030.

What is a key restraint affecting small and medium enterprises?

High capital expenditure remains a barrier, as advanced lines often require investments exceeding USD 2 million.

Page last updated on: