Packaging Film Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

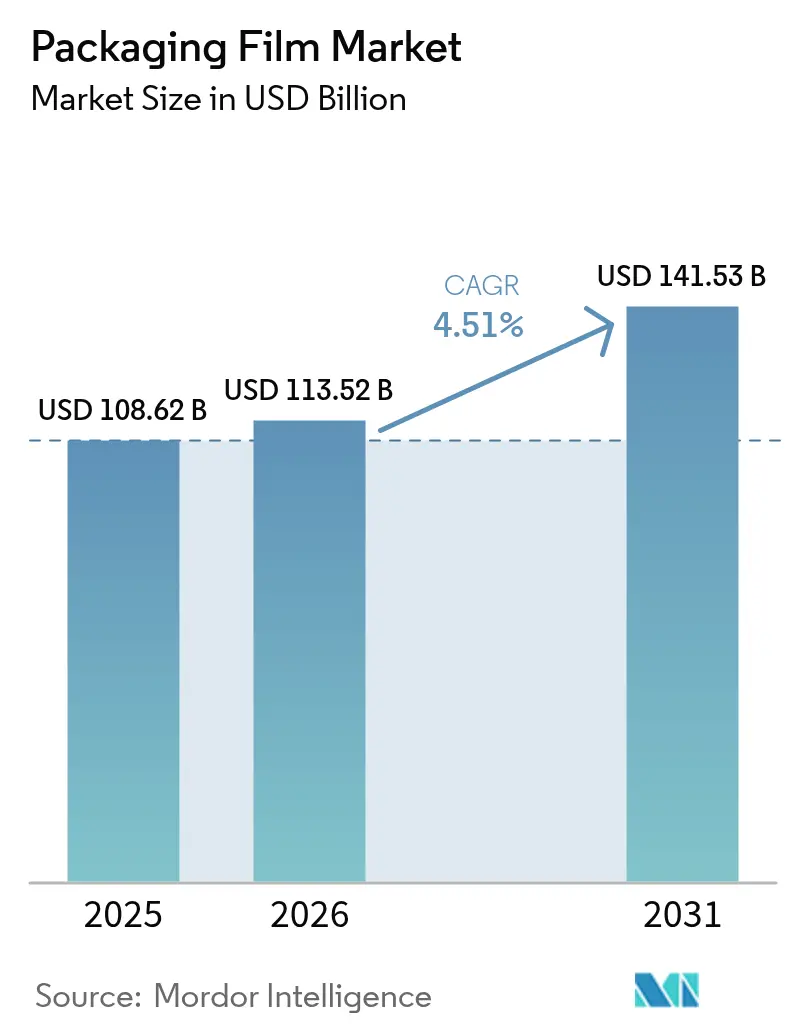

| Market Size (2026) | USD 113.52 Billion |

| Market Size (2031) | USD 141.53 Billion |

| Growth Rate (2026 - 2031) | 4.51% CAGR |

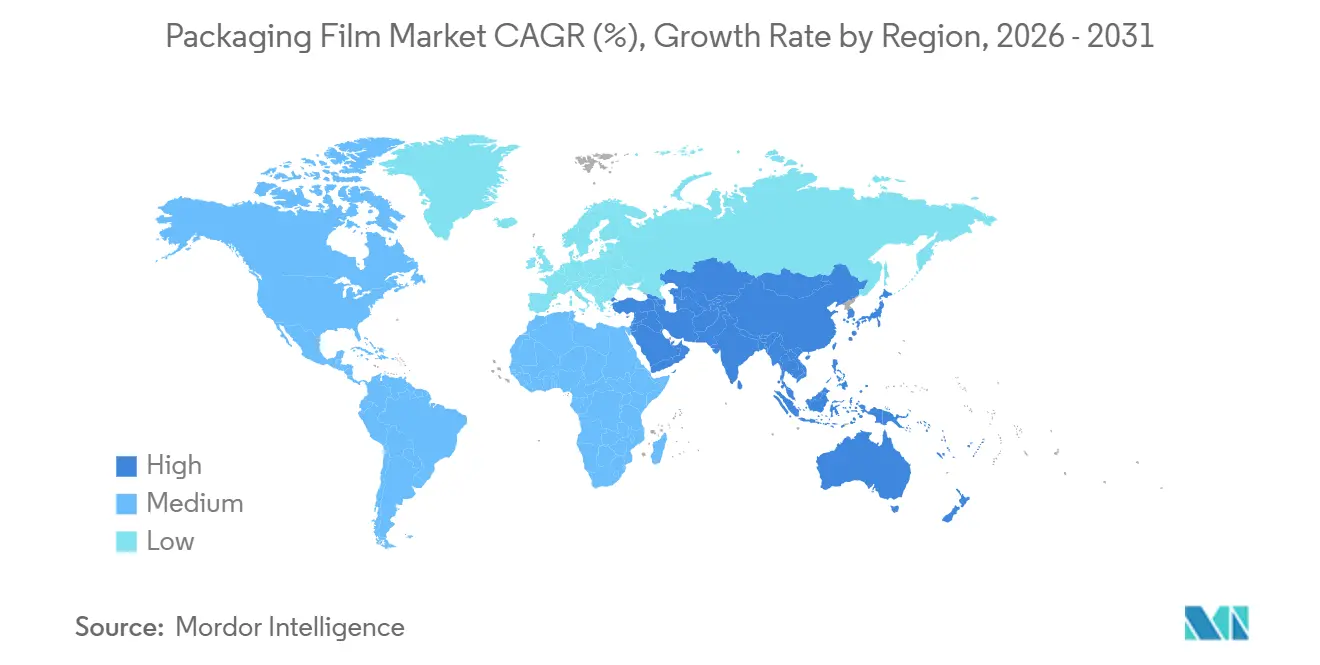

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Packaging Film Market Analysis by Mordor Intelligence

The packaging film market size is projected to expand from USD 108.62 billion in 2025 and USD 113.52 billion in 2026 to USD 141.53 billion by 2031, registering a 4.51% CAGR between 2026-2031. Strong policy pressure for fully recyclable mono-material packs in the European Union, rising direct-to-consumer freight volumes that favor lightweight polyethylene mailers, and rapid cold-chain build-outs in emerging Asia drive the near-term outlook. Brand owners are also specifying thinner gauges that still resist puncture, a shift enabled by high-performance metallocene LLDPE grades. At the same time, chemical-recycling contracts for food-grade recycled polyethylene safeguard supply continuity as plastic-tax regimes tighten. Finally, merger activity among global converters is set to unlock procurement synergies and reinforce bargaining power on post-consumer resin supply.

Key Report Takeaways

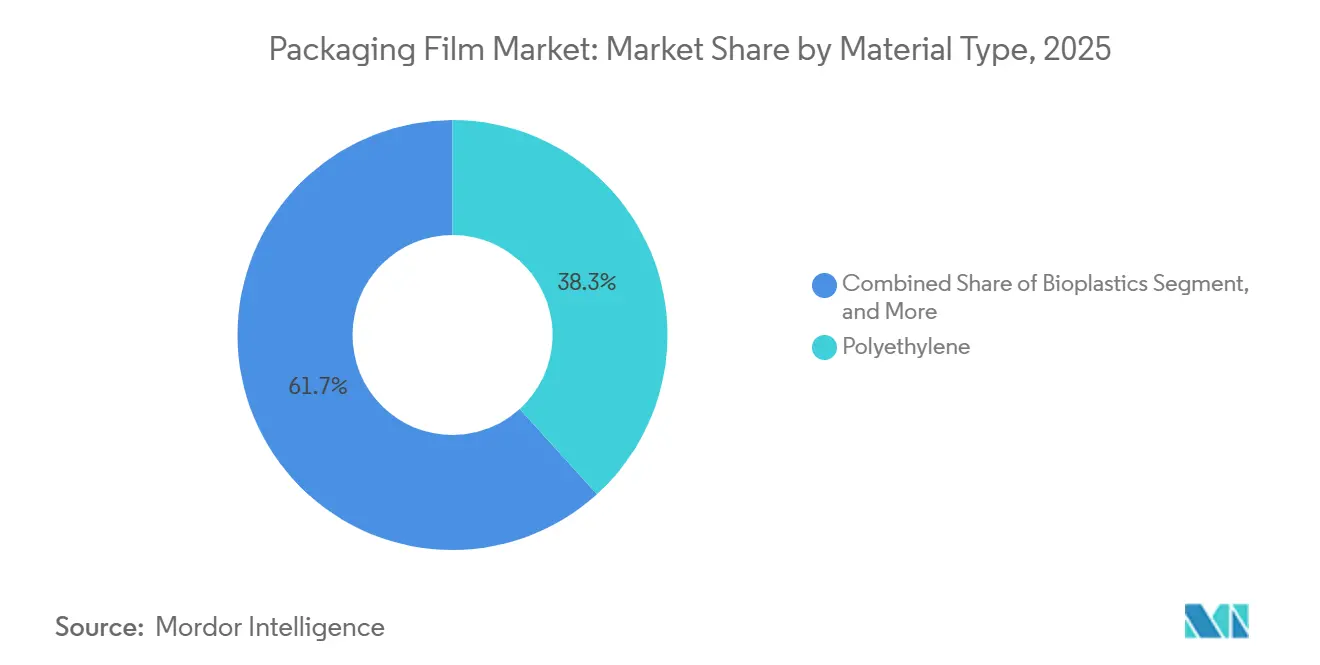

- By material type, polyethylene led with 38.27% revenue share in 2025, while bioplastics are forecast to advance at a 5.53% CAGR through 2031.

- By film structure, multilayer constructions accounted for 47.36% of the packaging film market share in 2025, whereas barrier multilayer formats are set to grow at a 5.19% CAGR through 2031.

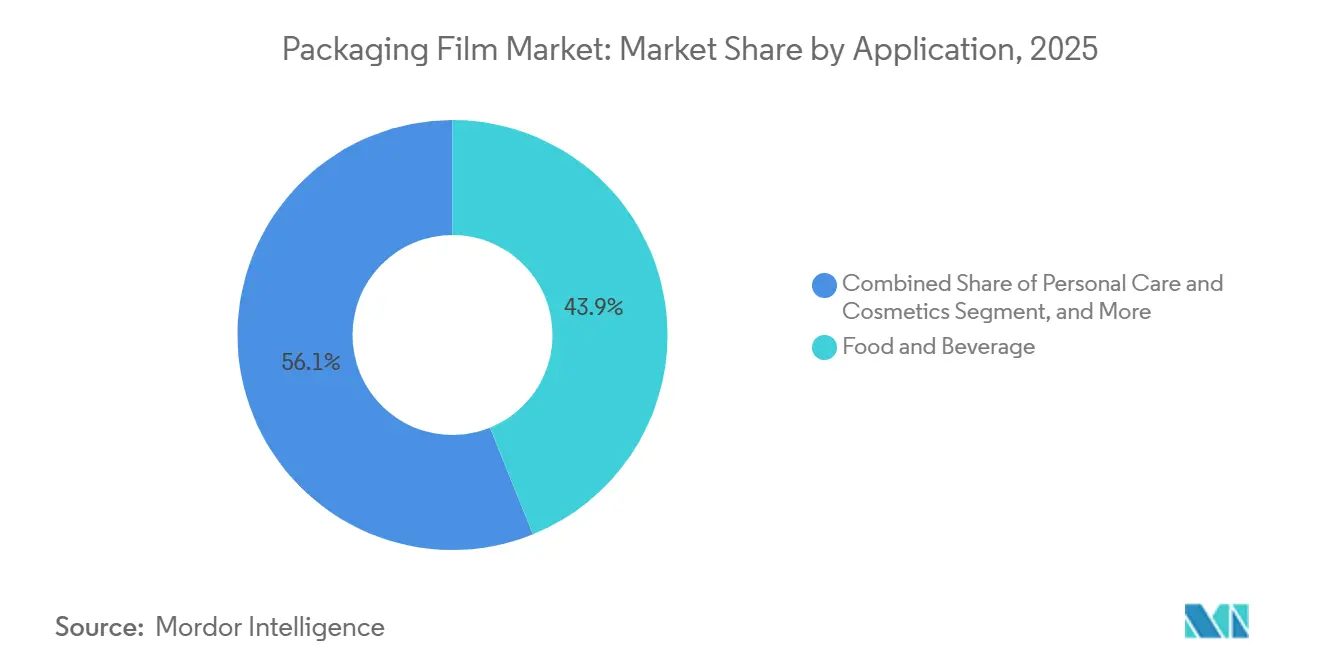

- By application, food and beverage captured 43.89% of the market share in 2025; personal care and cosmetics are projected to grow at a 5.93% CAGR during 2026-2031.

- By end-use format, bags and pouches commanded 38.42% of the packaging film market share in 2025, while labels and sleeves are forecast to grow at a 5.57% CAGR through 2031.

- By geography, Asia-Pacific accounted for 36.89% of global turnover in 2025, as the Middle East is expected to record a 5.61% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Packaging Film Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom driving demand for lightweight shipping films | +1.2% | Global, concentrated in North America, Europe, Asia-Pacific urban corridors | Short term (≤ 2 years) |

| EU push for mono-material recyclable films | +1.0% | Europe core, spillover to United Kingdom and export-oriented Asia-Pacific plants | Medium term (2-4 years) |

| Cold-chain packaged-food growth in emerging Asia-Pacific | +0.9% | China, India, Southeast Asia, with Middle East follow-on | Medium term (2-4 years) |

| Digital printing enabling short-run personalized packs | +0.7% | Early adoption in North America and Western Europe | Short term (≤ 2 years) |

| Antimicrobial additive masterbatches for meat films | +0.5% | Global, regulatory uptake differs by country | Long term (≥ 4 years) |

| Chemical-recycling feedstock agreements for food-grade rPE | +0.6% | North America and Europe pilots, select Asia-Pacific trials | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Boom Driving Demand for Lightweight Shipping Films

Parcel networks charge by dimensional weight, so every micron trimmed from a mailer cuts freight costs and emissions. By 2025, major online retailers validated 30% resin savings after switching to right-sized polyethylene mailers, accelerating converter uptake of metallocene LLDPE that delivers equivalent dart-drop impact at 20% lower thickness. Films now incorporate tailored slip-additive packages to maintain stable friction coefficients on high-speed sorters, minimizing downtime. As fulfillment centers automate, consistent film gauge and tack are mission-critical, prompting investments in real-time inline gauging. The e-commerce surge, therefore, channels sustained volume into the packaging film market and rewards converters that master ultra-thin but rugged constructions.[1]Amazon, “Amazon Packaging Innovations 2025,” aboutamazon.com

EU Push for Mono-Material Recyclable Films

The Packaging and Packaging Waste Regulation, adopted in 2024, bans non-detachable multi-material laminates in Europe from 2030. Converters now redesign coffee, snack, and pet-food pouches with all-polyethylene or all-polypropylene substrates that still achieve oxygen transmission rates below 5 cm³/m²·day·atm using metallized or silicon-oxide-coated layers. Leading suppliers rolled out high-density polyethylene films coextruded with ethylene-vinyl alcohol that meet 12-month shelf-life targets while passing polyolefin recycling sortation. Fluorine-free grease-resistant coatings based on bio-wax or polyvinyl alcohol also replace PFAS ahead of the January 2026 prohibition. This legislative thrust effectively locks in demand for recyclable substrates within the packaging film market.[2]European Parliament, “Parliament Adopts New Rules to Boost Packaging Sustainability,” europarl.europa.eu

Cold-Chain Packaged-Food Growth in Emerging Asia-Pacific

Rising disposable incomes expand frozen and chilled food consumption, but distribution climates in tropical regions swing widely. Brand owners now demand multilayer films with moisture vapor transmission below 2 g/m²·day to curb freezer burn. Regional regulators, such as China’s SAMR, enforce strict limits on extractable additives, adding compliance steps but improving quality. Meanwhile, India mandates that converters print storage temperatures in local languages, a directive ideally suited to digital presses that run variable-data jobs without plates. These requirements together elevate barrier multilayer share and propel the packaging film market in Asia-Pacific.[3]State Administration for Market Regulation, “Food Contact Materials Standards,” samr.gov.cn

Digital Printing Enabling Short-Run Personalized Packs

Digital presses slash makeready waste from hundreds to under 50 meters, enabling profitable runs in the low thousands. Personal care brands capitalize on the model by releasing influencer collaborations that live on the shelf for only a few weeks. Converters armed with HP Indigo 25K units can swap designs same-day, turning artwork around in 48 hours rather than the eight-week cycles typical of gravure. Black polyethylene films now incorporate IR-detectable pigments that enable optical sortation, aligning personalization with recyclability. Short-run capability thus dovetails with sustainable design, expanding premium niches in the packaging film market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic bans and taxes in North America and Europe | -0.8% | National and sub-national programs in Canada, United States, European Union | Short term (≤ 2 years) |

| Volatile virgin-resin prices | -0.6% | Global, petrochemical supply swings | Short term (≤ 2 years) |

| Barrier limits of bio-based films | -0.3% | Global, food-safety approval paths differ | Medium term (2-4 years) |

| Converter downtime from ultra-thin gauges | -0.2% | High-speed blown-film and cast-film lines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Plastic Bans and Taxes in North America and Europe

Canada’s nationwide single-use plastics prohibition removed checkout bags, cutlery, and stir sticks from the market, triggering costly line conversions and material substitutions. In parallel, the European Union imposes a USD 0.90-per-kilogram levy on unrecycled plastic packaging waste, incentivizing lightweight designs and higher recycled content. Retail take-back schemes achieve only a 42% polyethylene-film recycling rate in Germany because of contamination from adhesives and multilayer labels, highlighting infrastructure gaps. Such policy headwinds shave growth from the packaging film market even as they spawn recycling investment.

Volatile Virgin-Resin Prices

High-density polyethylene traded between USD 1,100 and USD 1,400 per metric ton in 2025 after hurricane-related shutdowns on the U.S. Gulf Coast, while European polypropylene swung USD 1,180-1,460 under refinery rationalizations. Polyester film makers paid more for purified terephthalic acid as Asian paraxylene supply tightened until new capacity came online late-2025. Price swings compress converter margins and can defer capital expenditure on high-barrier coextrusion lines that would otherwise sharpen competitive positioning in the packaging film market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polyethylene Commands Volume While Bioplastics Outperform on Growth

Polyethylene accounted for 38.27% of the packaging film market share in 2025, led by LLDPE stretch wrap and HDPE shipping sacks. The material’s cost-performance edge allows 15-20 micron down-gauging without losing pallet-load stability, keeping freight costs low. HDPE’s stiffness supports stand-up pouch formats, whereas LDPE remains the mainstay seal layer for snack and bakery wraps. Polypropylene services biaxially oriented niches that require high gloss and dead-fold, and polyester is indispensable in lidding where thermal stability matters.

Bioplastics are forecast to expand at a 5.53% CAGR, faster than the overall packaging film market, yet account for a modest value base today. Polylactic acid earns compostability logos that resonate with premium personal-care buyers, but its water-vapor barrier is 5-10 times worse than that of oriented polypropylene, necessitating metallized or oxide coatings for moisture-sensitive goods. A 40-60% price premium over polyethylene confines demand to brands willing to pay for environmental positioning. Even so, pilot lines blending polyhydroxyalkanoate into PLA improve toughness and broaden applications in producing films and capsule lidding.

By Film Structure: Multilayer Dominates but Barrier Multilayer Gains Momentum

Multilayer films accounted for 47.36% of the 2025 value as converters leverage three- and five-layer coextrusion to balance economics and functionality. Modified-atmosphere packaging is utilized to significantly extend the shelf life of oxygen-sensitive products such as cheese and meat, increasing it from one week to three weeks. In contrast, monolayer films continue to be widely used in commodity produce bags, where cost considerations take precedence over the effectiveness of barrier properties.

Barrier multilayer webs, however, are projected to outpace the packaging film industry average at 5.19% CAGR. Ethylene-vinyl alcohol cores achieve oxygen transmission below 1 cm³/m²·day·atm, though humidity control is vital because absorbed moisture doubles permeation. New nine-layer lines permit thinner tie layers, cutting total film weight while preserving adhesion. Where heat-seal temperature windows are tight, polyvinylidene chloride coatings lower sealing energy and speed form-fill-seal lines, bolstering converter margins.

By Application: Food Retains Size Lead, Personal Care Accelerates

Food and beverage accounted for 43.89% of 2025 revenue, as everyday grocery items require sealing, printability, and moderate barrier properties at the lowest unit cost. In the packaging film market, retort pouches, formable meat webs, and snack wraps collectively account for a significant share in terms of volume. Additionally, digital inkjet coders have increasingly been utilized to apply traceability data inline, which is an essential requirement mandated by global food-safety regulations.

Personal care and cosmetics, in contrast, are expected to register the fastest CAGR of 5.93%. Stand-up pouches with corner fitments displace rigid bottles, trimming pack weight by 60-70% and improving e-commerce parcel density. Limited-edition influencer collaborations exploit digital printing to cycle artwork every few weeks. Brand mandates for 25% recycled content by 2027 further trigger investments in FDA-approved decontamination for recycled polyethylene streams.

By End-Use Format: Bags and Pouches Lead, Labels and Sleeves Scale Quickly

In 2025, bags and pouches, including flat-bottom coffee bags, zipper-closure pet-food pouches, and side-gusseted snack packs, accounted for 38.42% of the global market value. Advancements in sealant chemistry have facilitated the development of 100% polyethylene structures that successfully meet drop-test requirements after the filling process. These innovations enable processors to participate in store drop-off recycling programs, thereby contributing to sustainability efforts.

Labels and sleeves are forecast to expand at a 5.57% CAGR as pressure-sensitive converters integrate inline digital presses that handle variable data for pharmaceutical serialization mandates. Polyolefin-based shrink sleeves with wash-off inks now comply with Association of Plastic Recyclers guidelines, lifting yields in bottle-to-bottle recycling. As brands intensify customization, converters see steady revenue gains from these label formats within the broader packaging film market.

Geography Analysis

Asia-Pacific generated 36.89% of global turnover in 2025, reflecting dense manufacturing clusters and fast-growing packaged-food penetration. China enforces strict migration limits for additives, compelling third-party testing that lengthens qualification times yet raises consumer trust. India mandates multilingual storage instructions, driving digital printing adoption, while Japan now permits chemically recycled PET in food contact under stringent decontamination protocols. These policy environments collectively underpin predictable, if compliance-heavy, expansion for the packaging film market in the region.

The Middle East is on track for the fastest 5.61% CAGR through 2031. Saudi Arabia’s Vision 2030 megaprojects and the United Arab Emirates’ cold-storage build-outs are attracting investment in high-barrier film lines tailored for pharmaceuticals and perishable foods. Greenhouse projects in NEOM demand UV-blocking yet photosynthesis-friendly films incorporating titanium dioxide and hindered-amine stabilizers, opening a specialty niche. Egypt’s plastic-bag levy is shifting retail toward woven-polypropylene totes, pulling some volume from commodity HDPE bags while creating upscale branding opportunities.

Europe remains the regulatory bellwether, compelling converters worldwide to develop mono-material films that can be mechanically recycled. North America shows mature per-capita use, yet e-commerce shipping inflates demand for durable mailers. South America’s growth clusters in Brazil as packaged-food consumption rises inland, offset by Argentina’s capital-control constraints. Africa offers long-range promise once cold-chain logistics and harmonized standards take hold, potentially unlocking incremental volume for the global packaging film market share in the coming years.

Competitive Landscape

The packaging film industry shows moderate concentration, with the ten largest producers capturing about 35-40% of global revenue, while a long tail of regional converters fills local demand niches. Market leaders retain bargaining power on resin procurement and recycling feedstock, yet no single firm controls enough share to dictate pricing unilaterally. Competitive intensity, therefore, hinges on scale-driven cost advantages, access to post-consumer resin, and the ability to meet tightening recyclability mandates.

A wave of mergers and private-equity deals is redrawing the supplier map. Amcor’s pending all-stock merger with Berry Global, valued at USD 8.43 billion, will create a network of more than 400 manufacturing plants and unlock an estimated USD 650 million in annual procurement and footprint. Sealed Air agreed in November 2025 to a USD 10.3 billion take-private by CD&R, a move that promises expanded automation investment across its protective-packaging lines once the transaction closes in 2026. Mondi diversified upstream in September 2025 by purchasing a 25% stake in a German polyethylene recycler that supplies 60,000 t per year of EFSA-compliant PCR, securing a captive supply to support its 30% recycled-content pledge.

Technology adoption is becoming a decisive differentiator for mid-tier converters seeking to gain market share. More than 200 flexible-packaging plants had installed HP Indigo 25K digital presses by late 2025, enabling profitable runs of fewer than 2,000 units and shortening artwork changeovers to hours rather than weeks. Patent filings for fluorine-free grease-resistant coatings climbed 40% between 2024 and 2025 as suppliers race to replace PFAS ahead of the January 2026 European ban. Converters that pair secure PCR supply with rapid digital print capability are best positioned to meet brand-owner demands for sustainable, short-run packaging while defending margins against raw-material volatility.

Packaging Film Industry Leaders

Amcor plc

Sealed Air Corporation

Mondi plc

Cosmo Films Ltd

Huhtamaki Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Cosmo Films received International Sustainability and Carbon Certification for bio-attributed BOPP produced in Aurangabad, India, enabling Scope 3 emission reductions without supply-chain retooling.

- November 2025: Sealed Air agreed to a USD 10.3 billion acquisition by CD&R, with closing targeted for mid-2026 pending antitrust clearances.

- September 2025: Mondi bought a 25% stake in a German polyethylene recycler with 60,000 t annual capacity to secure food-grade PCR supply.

- June 2025: Huhtamaki completed a USD 45 million expansion of its Pune, India, plant, adding a nine-layer line that serves pharmaceutical and high-barrier food pouches.

Global Packaging Film Market Report Scope

The Packaging Film Market Report is Segmented by Material Type (Polyethylene, Polypropylene, Polyester, Bioplastics, Other Material Types), Film Structure (Monolayer, Multilayer, Barrier Multilayer), Application (Food and Beverage, Pharmaceutical and Medical, Personal Care and Cosmetics, Consumer Durables and Electronics, Industrial and Institutional, Agriculture and Horticulture, Other Applications), End-Use Format (Bags and Pouches, Wraps and Lidding Films, Labels and Sleeves, Blister and Sachets, Shrink and Stretch Wrap), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Polyethylene | High-Density Polyethylene (HDPE) |

| Low-Density Polyethylene (LDPE) | |

| Linear Low-Density Polyethylene (LLDPE) | |

| Polypropylene | |

| Polyester | |

| Bioplastics | |

| Other Material Types |

| Monolayer |

| Multilayer |

| Barrier Multilayer |

| Food and Beverage |

| Pharmaceutical and Medical |

| Personal Care and Cosmetics |

| Consumer Durables and Electronics |

| Industrial and Institutional |

| Agriculture and Horticulture |

| Other Applications |

| Bags and Pouches |

| Wraps and Lidding Films |

| Labels and Sleeves |

| Blister and Sachets |

| Shrink and Stretch Wrap |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Material Type | Polyethylene | High-Density Polyethylene (HDPE) | |

| Low-Density Polyethylene (LDPE) | |||

| Linear Low-Density Polyethylene (LLDPE) | |||

| Polypropylene | |||

| Polyester | |||

| Bioplastics | |||

| Other Material Types | |||

| By Film Structure | Monolayer | ||

| Multilayer | |||

| Barrier Multilayer | |||

| By Application | Food and Beverage | ||

| Pharmaceutical and Medical | |||

| Personal Care and Cosmetics | |||

| Consumer Durables and Electronics | |||

| Industrial and Institutional | |||

| Agriculture and Horticulture | |||

| Other Applications | |||

| By End-Use Format | Bags and Pouches | ||

| Wraps and Lidding Films | |||

| Labels and Sleeves | |||

| Blister and Sachets | |||

| Shrink and Stretch Wrap | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the packaging film market today and where is it headed by 2031?

It stood at USD 108.62 billion in 2025 and is forecast to reach USD 141.53 billion by 2031 on a 4.51% CAGR.

Which material has the highest share in flexible films?

Polyethylene led with 38.27% of 2025 value thanks to its cost-performance balance across stretch wrap and shipping sacks.

What segment will grow the fastest to 2031?

Personal care and cosmetics packaging is projected to post the quickest 5.93% CAGR as brands pivot to lightweight pouches and short-run digital designs.

Why are barrier multilayer films gaining traction?

Pharmaceutical, meat, and dairy packs need oxygen transmission below 1 cm³/m²·day·atm, an objective met more reliably by seven- to nine-layer structures.

Which region offers the highest growth runway?

The Middle East is expected to expand at a 5.61% CAGR through infrastructure and cold-storage investments supporting high-barrier applications.

How will the Amcor-Berry merger affect supply dynamics?

The combined entity will operate over 400 plants, improving leverage in recycled-resin procurement and accelerating standardization on mono-material designs.

Page last updated on: