Fish Feed Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

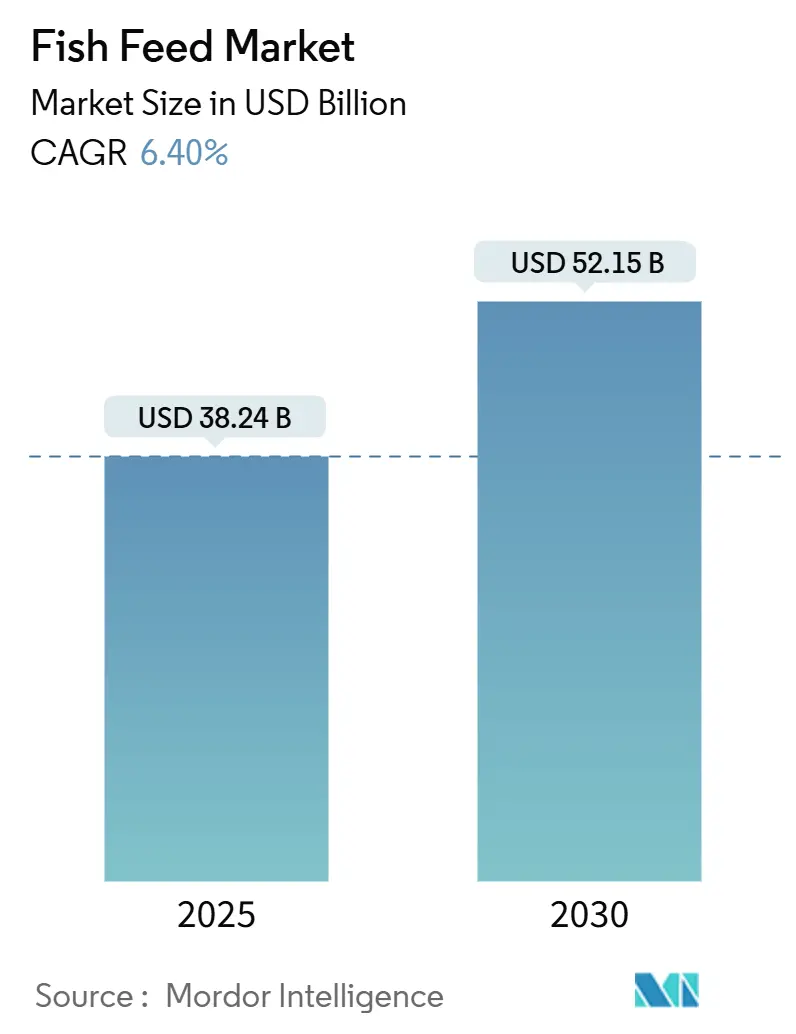

| Market Size (2025) | USD 38.24 Billion |

| Market Size (2030) | USD 52.15 Billion |

| Growth Rate (2025 - 2030) | 6.40% CAGR |

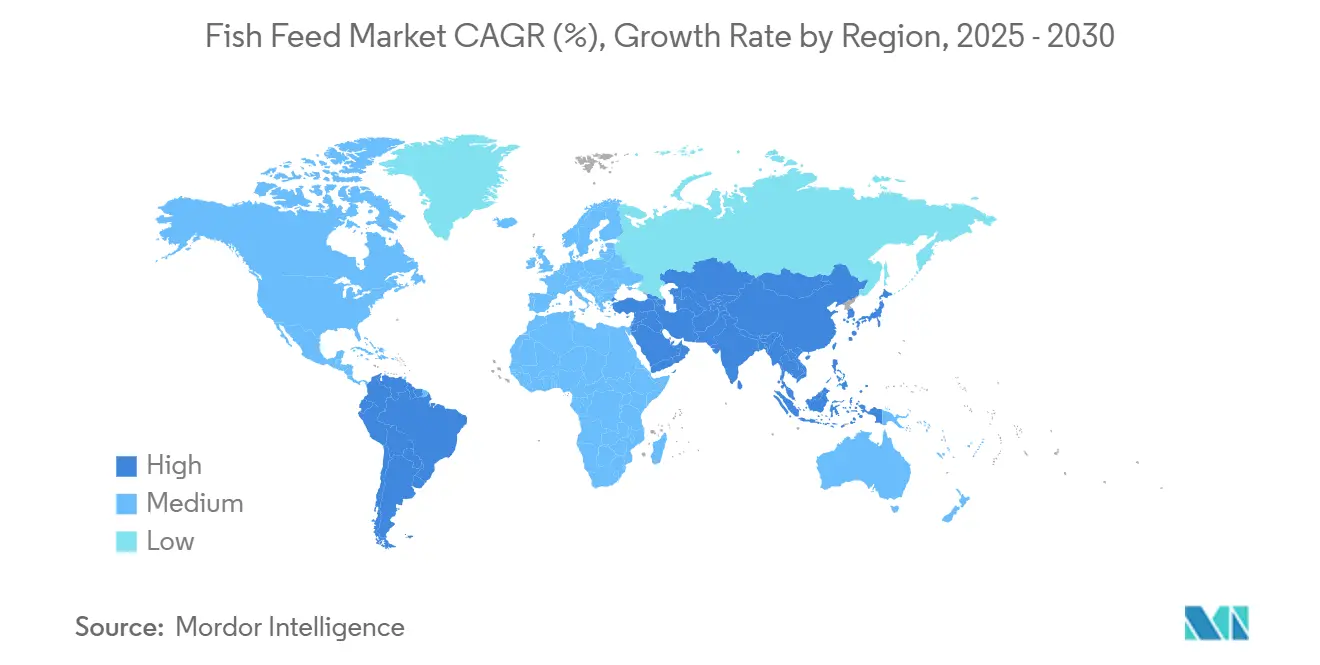

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fish Feed Market Analysis by Mordor Intelligence

The fish feed market size reached USD 38.24 billion in 2025 and is forecast to climb to USD 52.15 billion by 2030, advancing at a 6.4% CAGR. Robust demand for farmed seafood, policy-backed shifts toward precision nutrition, and scaling of novel protein sources collectively reinforce a steady expansion path for the fish feed market. Asia-Pacific anchors the growth through high-volume carp and tilapia production, while functional feed innovation in Europe and North America accelerates value creation. Ingredient diversification away from marine proteins toward plant, insect, and algal options reduces cost volatility and strengthens supply security. Competitive intensity remains moderate, with leading firms leveraging research investments, digital feeding platforms, and certified supply chains to consolidate positions across premium segments of the fish feed market.

Key Report Takeaways

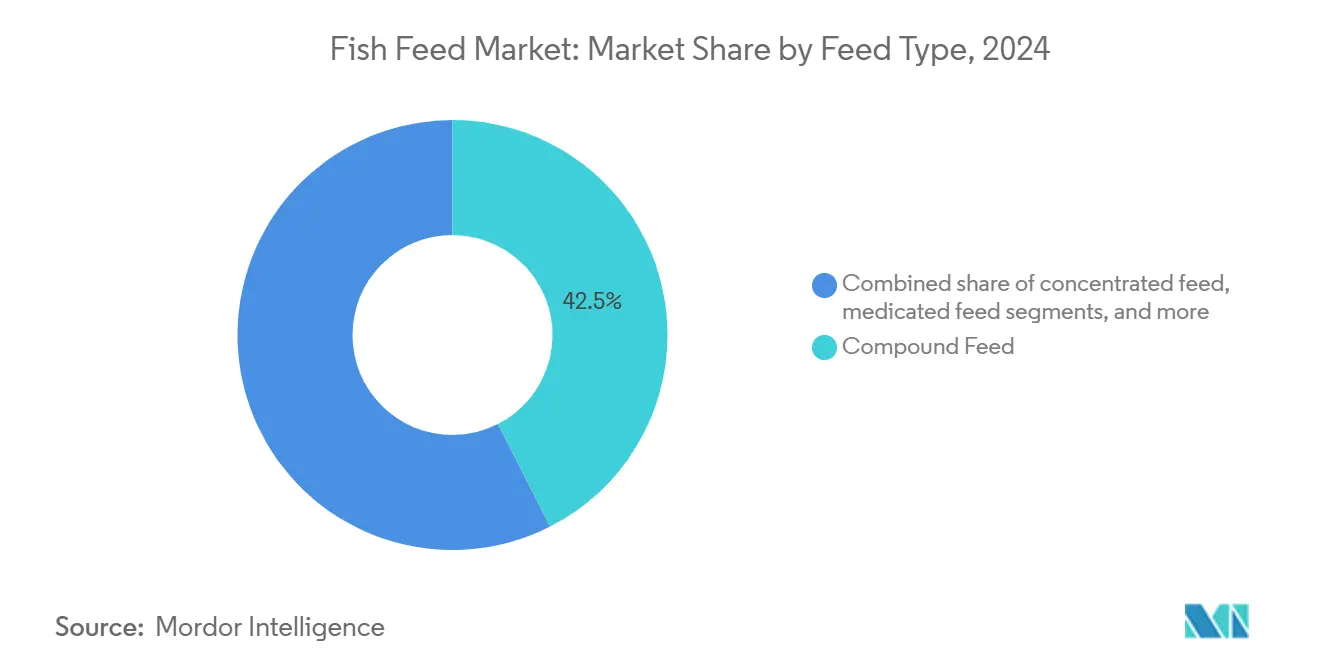

- By feed type, the compound feed held 42.5% of the fish feed market share in 2024, while functional feed is projected to expand at a 9.1% CAGR through 2030.

- By ingredient type, plant-based proteins accounted for a 37.0% share of the fish feed market size in 2024, and insect meal is set to rise at a 13.4% CAGR to 2030.

- By form, pellets led with a 55.1% share in 2024, whereas extruded feeds are projected to advance at an 8.9% CAGR to 2030.

- By species, carp feed captured 33.0% of the fish feed market share in 2024, and salmonid feed shows the fastest growth at 7.8% CAGR to 2030.

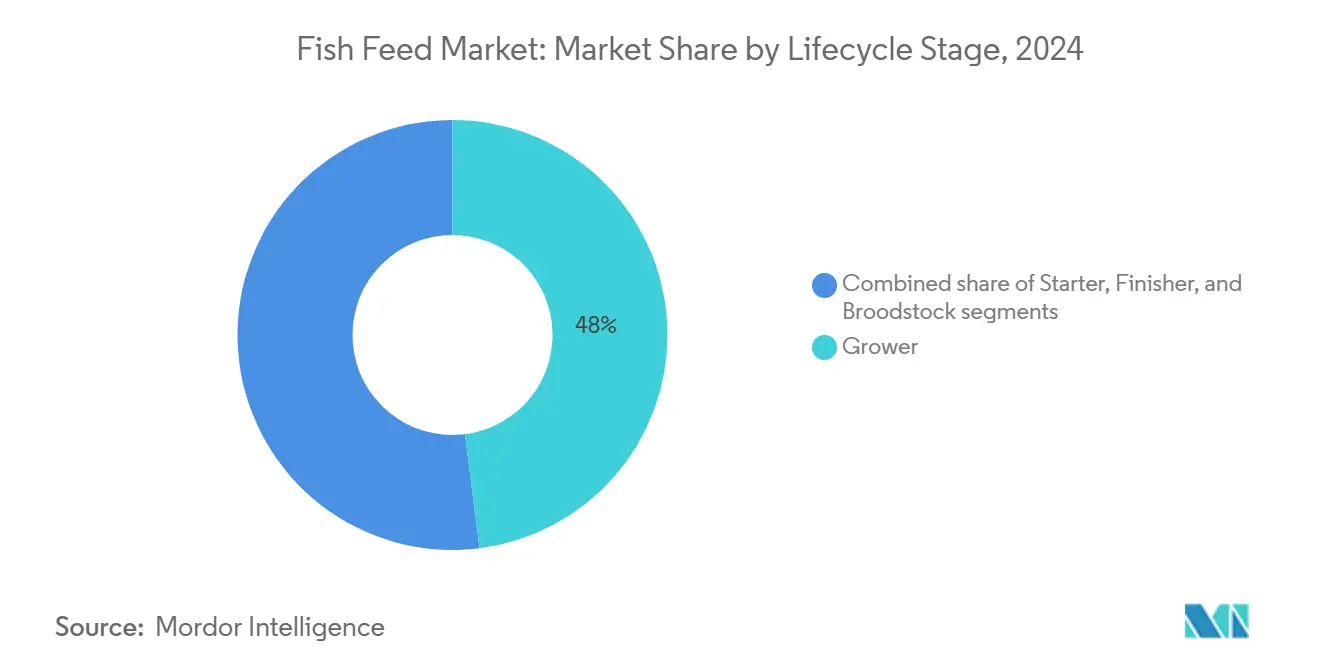

- By lifecycle stage, grower feed led with a 48.0% share in the fish feed market, while starters are growing with a 9.4% CAGR in the fish feed market through 2030.

- By geography, Asia-Pacific commanded 48.0% revenue share in 2024, while registering 7.1% CAGR in the fish feed market through 2030.

- Nutreco N.V., Cargill Incorporated, BioMar Group, Charoen Pokphand Foods Public Company Limited, and Mowi ASA collectively held a majority share of the market, underscoring a moderately concentrated competitive field.

Market Trends and Insights

Drivers Impact Analysis of Fish Feed Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating shift toward high-protein aquatic diets in Asia-Pacific mass aquaculture | +1.8% | Asia-Pacific core, global spill-over | Medium term (2-4 years) |

| Industry adoption of functional feeds to reduce antibiotic usage | +1.2% | Global, early gains in Europe and North America | Short term (≤ 2 years) |

| Expansion of recirculating aquaculture systems demanding specialized feeds | +0.9% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Rising demand for sustainable and certified marine ingredients | +0.8% | Global, strongest in Europe and North America | Medium term (2-4 years) |

| Scaling of insect meal production lowering cost parity by 2027 | +0.6% | Europe and North America initially, expanding globally | Long term (≥ 4 years) |

| AI-driven precision feeding platforms boosting feed-conversion efficiency | +0.5% | Technology-advanced markets, gradual global adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Shift Toward High-Protein Aquatic Diets in Asia-Pacific Mass Aquaculture

Rising urban incomes across Asia-Pacific move farmers toward protein-dense rations that shorten grow-out cycles and lift profitability. China recorded 60.8 million metric tons of aquaculture fish output in 2024[1]Source: Ministry of Agriculture and Rural Affairs of China, “China Fishery Statistical Yearbook 2024,” moa.gov.cn, and commercial ponds increasingly apply feeds with 32–38% crude protein instead of legacy 28–30% blends. Vietnam’s shrimp sector trims production time from 120 to 90 days by choosing high-protein diets, while India’s intensifying carp systems replicate similar gains. Expanding cold-chain infrastructure further validates investment in nutritional upgrades by assuring producers that premium seafood reaches metropolitan buyers without spoilage. The shift also prompts government extension programs to deliver feed-use guidelines, effectively closing knowledge gaps among smallholder farmers and boosting overall diet consistency across the fish feed market.

Industry Adoption of Functional Feeds to Reduce Antibiotic Usage

Stricter residue rules and consumer mistrust of prophylactic antibiotics propel rapid uptake of probiotic-rich, immunostimulant formulas[2]Source: European Food Safety Authority, “Scientific Opinion on the Safety and Efficacy of Feed Additives 2024,” efsa.europa.eu. The European Union ban triggered a USD 2.1 billion opportunity for functional additives, and Norwegian salmon farms dropped antibiotic application after switching diets. BioMar Group documented higher sales growth of such feeds during 2024, buoying profitability in the fish feed market. Asia’s shrimp exporters increasingly adopt the same solutions to retain United States market access, showing policy diffusion outside Europe. Suppliers, in turn, expand technical-service teams to prove health benefits via on-farm trials, further broadening functional feed adoption curves across diverse climatic zones.

Expansion of Recirculating Aquaculture Systems Demanding Specialized Feeds

Land-based RAS grew 25% worldwide in 2024, led by projects in the United States, Norway, and Singapore[3]Source: Global Aquaculture Alliance, “RAS Technology Adoption Survey 2024,” aquaculturealliance.org. Closed-loop tanks require digestibility above 90% to control waste, spurring feed makers to refine protein-to-lipid ratios and add yeast extracts that enhance gut health. Atlantic Sapphire’s Florida salmon facility exemplifies these needs, using tailor-made rations that protect water quality while maximizing biomass gain. Investor prospectuses increasingly rank feed partnerships alongside biosecurity and energy costs when evaluating new RAS sites, embedding suppliers earlier in project feasibility studies. This deep collaboration accelerates innovation cycles and locks in multi-year contracts that stabilize revenue visibility for the fish feed market.

Rising Demand for Sustainable and Certified Marine Ingredients

Retail and food-service pledges for fully traceable seafood amplify calls for Marine Stewardship Council (MSC) and Aquaculture Stewardship Council (ASC) approved inputs. Certified fishmeal and fish oil sell at 20–30% price premiums, yet major players such as Mowi ASA target 100% certified inclusion by 2025, forcing suppliers to adapt. Cargill Incorporated’s EWOS business met 95% certified sourcing in 2024, securing long-term contracts at higher average selling prices. Government-backed eco-labeling incentives in South America and Southeast Asia strengthen the commercial logic for certification adoption by raising retail visibility of responsibly produced seafood. As blockchain traceability pilots mature, certified ingredient data flows align with environmental, social, and governance (ESG) reporting metrics demanded by institutional investors, adding fresh momentum to the fish feed market.

Restraints Impact Analysis of Fish Feed Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in fishmeal and fish-oil prices | −1.4% | Global, strongest in premium segments | Short term (≤ 2 years) |

| Stringent environmental regulations on feed discharge | −0.8% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Disease outbreaks impacting feed-demand cycles | −0.6% | Global, regional clusters | Short term (≤ 2 years) |

| Limited availability of high-quality algal biomass for commercial feed use | −0.4% | Global, premium and specialty segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Fishmeal and Fish-Oil Prices

Fishmeal averaged USD 1,400–2,100 per metric ton in 2024 as El Niño cut anchovy landings off Peru and Chile, squeezing gross margins for high-end formulations. A 10% raw-material spike raises salmon feed cost 3–4%, according to Norwegian suppliers, diminishing profitability when retail prices lag. Limited forward-contract options and a concentrated supplier base make hedging difficult, prompting feed makers to stockpile or blend cheaper substitutes. Expansion of fisheries management quotas remains uncertain, layering geopolitical risk into sourcing. In response, firms allocate more research spending to plant and insect proteins to damp volatility’s impact on the fish feed market.

Stringent Environmental Regulations on Feed Discharge

The European Union Water Framework Directive caps nutrient output, forcing feeds with reduced phosphorus and nitrogen. Chile mandates phosphorus below 9 kg per metric ton of salmon harvested, adding 5–10% to formulation cost. Such specifications require finer grinding, selective amino acids, and low-ash ingredients, driving up operating expenses. Compliance audits now inspect entire ingredient supply chains, complicating vendor qualification processes and lengthening time to market for new formulas. As regulators introduce carbon accounting to licensing criteria, even low-impact feeds may need evidence of renewable energy use during extrusion, adding new cost layers to the fish feed market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Fish Feed Market Segment Analysis

By Feed Type:

Compound Feeds Drive Market MaturationCompound feeds accounted for 42.5% of the fish feed market size in 2024 on the strength of turnkey formulas that streamline farm management. Producers embrace them to secure predictable growth outcomes regardless of seasonal ingredient swings. Demand rises alongside intensive ponds and cages where labor savings and biosecurity justify a price premium. Functional diets outpace the broader fish feed market at a 9.1% CAGR as regulators restrict prophylactic antibiotics and buyers pay for elevated survival. Widening insurance discounts for farms using probiotic-enhanced feeds adds a fresh financial incentive, reinforcing the upward trajectory for functional products in premium export markets.

Concentrated feeds face slower expansion as farmers prefer fully balanced rations. Medicated lines remain niche yet sustain relevance in developing regions where veterinary infrastructure lags. Ongoing research by Skretting, the aquaculture brand of Nutreco N.V., into micro-pellet technology stands to elevate starter feed performance and keep innovation circulating within established categories. Continued mergers between compound and premix specialists may consolidate formulation expertise, raising capital barriers for new entrants but leveraging economies of scale for certified raw-material sourcing.

By Ingredient:

Plant-Based Proteins Reshape Traditional FormulationsPlant-Based Proteins captured 37.0% of expenditure in 2024, signaling a maturing quest to cut marine dependency without compromising amino acid balance[4]Source: Food and Agriculture Organization, “The State of World Fisheries and Aquaculture 2024,” fao.org. Soy, wheat gluten, and pea concentrates set the benchmark for cost efficiency, especially across carp and tilapia diets. Fishmeal still represents a substantial consumption for larval stages and premium salmonid feeds, but inclusion rates trend lower yearly. New enzyme blends allow higher soybean inclusion without lowering palatability, moving diets closer to complete fishmeal replacement for certain life stages.

Insect meal growing at 13.4% is the fastest-growing ingredient within the fish feed market, due to supportive policy frameworks and expanded factory outputs. Algae oils and biomass enter at premium price points yet attract sustainability-minded buyers. Additive demand also grows as formulators seek enzymes and immune boosters that allow higher plant or insect substitution without sacrificing performance. Vertical integration by feed companies into soybean crushing and insect farming locks in input security and supports margin protection against commodity swings.

By Form:

Pellets Maintain Dominance Through VersatilityPelletized products made up 55.1% by form, proving adaptable across species and easy to transport and store. Uniform sinking rates and minimal fines support feeding control in both static ponds and cages. Extruded feeds recorded an 8.9% CAGR as their porous structure enhances water stability and nutrient digestibility, pivotal for Recirculating Aquaculture System (RAS) and high-density farms. Extrusion also enables vacuum lipid coating that boosts energy density, helping producers reach harvest weight faster.

Powder and liquid formats remain specialized. Powders feed hatcheries and command premium margins, while liquid micro-capsules aid broodstock conditioning. Innovation in extrusion, such as twin-screw technology, reduces shear stress on heat-sensitive vitamins and probiotics, broadening functional options and protecting nutrient integrity. These advances keep form differentiation an active competitive battleground within the fish feed market.

By Lifecycle Stage:

Starter Feeds Command Premium PricingStarter diets face skewed profitability upward since survival hinges on micro-particulate quality and palatability, growing at a CAGR of 9.4% through 2030. Grower formulas dominate tonnage at 48.0%, fostering the bulk of biomass gain and revenue stability for suppliers. Finisher feeds focus on flesh attributes like color and fat profile that drive consumer preference, especially for export-grade salmon and shrimp. Emerging regulatory interest in humane harvesting practices has sparked product development of sedative-infused finisher diets aimed at reducing handling stress.

Broodstock rations require refined nutrient density to maximize fecundity and larval vigor, remaining strategically important despite modest sales volumes. Suppliers now introduce customized breeder diets with adjusted essential fatty acid ratios for specific spawning seasons, anchoring long-term contracts and enhancing genetic program outcomes across hatcheries worldwide.

By Species:

Carp Farming Drives Volume GrowthCarp diets generated 33.0% of the revenue by species in 2024, primarily due to the mass production models in the Asia-Pacific region. Their affordability bolsters domestic protein intake and positions carp as a stable pillar of demand. Growth opportunities now emerge in genetically improved strains that convert feed more efficiently, spurring interest in high-energy formulas tailored to those lines. Salmonid rations, although smaller in tonnage, yield outsized value due to high inclusion of fish oil, astaxanthin, and functional additives. Salmonid feeds' growth of 7.8% CAGR underscores the expansion of land-based Atlantic salmon projects and rising consumer acceptance in emerging economies.

Tilapia feed remains crucial, particularly in Africa and South America, where the species’ resilience suits a variety of freshwater bodies. Shrimp and other marine species round out diversified demand, enabling mills to balance freshwater and saltwater production cycles, thus stabilizing plant utilization within the fish feed market. The diets of sea bass and sea bream in the Mediterranean also require specific lipid profiles, creating a profitable niche for specialists focused on warm-water marine carnivores.

Geography Analysis

APAC Fish Feed Market

Asia-Pacific possessed 48.0% of regional consumption in 2024 and is projected to advance at a 7.1% CAGR through 2030. Intensifying freshwater pond culture in China, shrimp expansion in Vietnam, and India’s protein demand fuel consistent volume gains. Urban density and land scarcity accelerate conversion to manufactured feeds that unlock higher output per hectare. Regional governments prioritize aquaculture self-sufficiency in national food-security plans, offering subsidized credit for feed mills that embrace precision nutrition. Rising electricity costs motivate the adoption of high-energy formulations that shorten production cycles and lower fixed costs per kilogram harvested, broadening budget space for feed improvements.

Europe Fish Feed Market

Europe's sustainability leadership shapes premium product niches. Norway’s sophisticated salmon sector pioneers functional and certified feeds that later diffuse to other regions. Growth constraints tied to environmental permitting drive innovation into RAS and offshore cages, feeding demand for highly digestible, low-emission formulas. The European Commission’s Farm-to-Fork strategy also mandates lower carbon footprints for animal protein supply chains, promoting alternative ingredients such as insect proteins and fermentation-based amino acids. Peripheral producers, including Poland and Turkey, pivot toward value-added trout and sea bass exports to leverage upgraded feed programs and capture rising gourmet demand across Central Europe.

The Americas and MEA Fish Feed Market

North America's aquaculture growth stems from U.S. land-based salmon production, Canadian marine cage operations, and Mexican tilapia and shrimp farming. Labor shortages drive automation and precision feeding adoption, while environmental policies supporting low-carbon protein production attract recirculating aquaculture system (RAS) projects in the Great Lakes region. This increases the demand for algae oil and probiotic-enriched feeds. In South America, Chilean salmon farming and Brazilian tilapia production lead the expansion. The integration of local soy protein and feed mill consolidation reduces costs in Brazil, while Argentina develops land-based trout farming. In the Middle East and Africa, tilapia farming in Egypt's Nile Delta dominates consumption, while Kenya and Uganda increase cage farming operations in Lake Victoria. Gulf states' offshore submersible system trials create specialized markets for stable feed formulations.

Competitive Landscape

The market exhibits moderate concentration, with Nutreco N.V. leading, followed by Cargill Incorporated, BioMar Group, Charoen Pokphand Foods Public Company Limited, and Mowi ASA. These companies collectively hold a major market share. Market concentration varies significantly by region and species. European salmon feed markets exhibit higher consolidation, whereas Asian freshwater feed markets remain fragmented, with local mills serving specific farming systems and species requirements. Competition has intensified as the industry shifts from volume-based competition to value-added solutions that focus on feed conversion efficiency, sustainability, and digital integration.

Multinational leaders like Nutreco N.V. and Cargill Incorporated utilize global scale and research capabilities to serve premium market segments. These companies invest 2-3% of revenue in research and development, focusing on functional feeds, precision nutrition systems, and alternative protein sources that enable premium pricing. Regional companies, such as Charoen Pokphand Foods Public Company Limited and Tongwei Co., focus on cost leadership through vertical integration and local market expertise, managing supply chains from raw material sourcing to aquaculture production. This integration enables margin capture across value chain segments while ensuring supply chain stability during fluctuations in raw material prices.

Technology adoption has become a crucial competitive factor. Companies are investing in artificial intelligence platforms, precision feeding systems, and digital customer engagement tools to improve feed conversion efficiency and reduce environmental impact. Cargill Incorporated's partnership with ViAqua shows how established companies acquire external technology capabilities, while BioMar Group's investment in computer vision systems for feeding optimization demonstrates an internal innovation focus. Patent filings in aquaculture nutrition increased 35% during 2024, with functional feed additives and precision feeding algorithms showing the highest growth, indicating increased competition in technology-driven segments.

Fish Feed Industry Leaders

Nutreco N.V

Biomar Group

Cargill, Incorporated

Charoen Pokphand Foods Public Company Limited

Mowi ASA

- *Disclaimer: Major Players sorted in no particular order

Fish Feed Market Companies Covered in this Report

- Nutreco N.V

- Cargill, Incorporated

- Biomar Group

- Mowi ASA

- Charoen Pokphand Foods Public Company Limited

- Ridley Corporation

- Aller Aqua

- Tongwei Co.

- Guangdong Haid Group

- De Heus Animal Nutrition B.V.

- New Hope Group

- Avanti Feeds

- Adisseo France S.A.S

- PT Central Proteina Prima

- BioMar-Tongwei JV

- Beneo Animal Nutrition

- Growel Feeds Private Limited

- Dibaq Aquaculture

- Archer Daniels Midland Company

- Inve Aquaculture

Recent Industry Developments in Fish Feed Market

- September 2025: BioMar Group, Innovafeed, and Auchan formed a partnership to integrate insect protein into commercial shrimp feed production in Ecuador. This collaboration demonstrates the viability of insect protein in sustainable shrimp farming. Auchan, a major European retailer, will incorporate shrimp fed with this insect-based feed into its supply chain and product range by 2026.

- June 2025: Canada's Ocean Supercluster launched five ocean innovation projects worth over USD 18 million, including the USD 7.2 million Microbial Protein for Sustainable Aquaculture Project. Led by DeNova, a Nova Scotia-based biotech company, the project develops sustainable microbial proteins as alternatives to fishmeal and soy, partnering with The Verschuren Centre, Neptune Properties, Onda, and Cooke Aquaculture to reduce aquaculture’s environmental footprint.

- February 2025: Insectika Biotech, an Indo-Israeli technology firm specializing in insect farming, has introduced a new insect protein-based fish feed in Odisha, India. The product is formulated specifically for Asian sea bass and aquarium species. The feed, developed in partnership with the Central Institute of Brackishwater Aquaculture (CIBA), was presented at the Shrimp Farmers' Conclave 2025. The launch event was attended by over 500 advanced farmers and hatchery owners.

Global Fish Feed Market Report Scope

The Fish Feed Market Report is Segmented by Feed Type (Compound Feed, Concentrated Feed, and More), by Ingredient (Fishmeal, Fish Oil, Plant-Based Proteins, and More), by Form (Pellets, Extruded, and More), Species (Salmonids, Carp, Tilapia, Catfish, and More), by Lifecycle Stage (Starter, Grower, and More), and by Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Segmentation Overview

| Compound Feed |

| Concentrated Feed |

| Medicated Feed |

| Functional Feed |

| Fishmeal |

| Fish Oil |

| Plant-Based Proteins |

| Insect Meal |

| Algae Ingredients |

| Additives |

| Pellets |

| Extruded |

| Powders |

| Liquid |

| Salmonids |

| Carp |

| Tilapia |

| Catfish |

| Trout |

| Marine Species |

| Shrimp |

| Others |

| Starter |

| Grower |

| Finisher |

| Broodstock |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | France |

| Germany | |

| Norway | |

| Spain | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Indonesia | |

| Vietnam | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Iran | |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | Egypt |

| Nigeria | |

| South Africa | |

| Rest of Africa |

| By Feed Type | Compound Feed | |

| Concentrated Feed | ||

| Medicated Feed | ||

| Functional Feed | ||

| By Ingredient | Fishmeal | |

| Fish Oil | ||

| Plant-Based Proteins | ||

| Insect Meal | ||

| Algae Ingredients | ||

| Additives | ||

| By Form | Pellets | |

| Extruded | ||

| Powders | ||

| Liquid | ||

| By Species | Salmonids | |

| Carp | ||

| Tilapia | ||

| Catfish | ||

| Trout | ||

| Marine Species | ||

| Shrimp | ||

| Others | ||

| By Lifecycle Stage | Starter | |

| Grower | ||

| Finisher | ||

| Broodstock | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | France | |

| Germany | ||

| Norway | ||

| Spain | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Indonesia | ||

| Vietnam | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Iran | ||

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | Egypt | |

| Nigeria | ||

| South Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the fish feed market in 2025 and what is its growth outlook?

The fish feed market size stands at USD 38.24 billion in 2025 and is projected to reach USD 52.15 billion by 2030, growing at a 6.4% CAGR.

Which feed type currently generates the highest revenue?

Compound feed leads with 42.5% share, driven by turnkey formulations that simplify farm operations and improve feed efficiency.

What ingredient category is expanding the fastest?

Insect meal shows the steepest ascent, rising at a 13.4% CAGR and approaching price parity with fishmeal by 2027.

Why are functional feeds attracting more buyers?

Functional formulas help cut antibiotic use, strengthen immunity, and often secure premium price points that offset their higher ingredient cost.

Which region dominates commercial fish feed consumption?

Asia-Pacific commands 48.0% of global demand, buoyed by extensive carp, tilapia, and shrimp farming industries.

What technology trend promises meaningful feed cost savings?

AI-enabled precision feeding platforms can reduce ration waste by up to 15% and enhance feed conversion ratios, lifting farm profitability.

Page last updated on: