Salmon Market Size and Share

Salmon Market Analysis by Mordor Intelligence

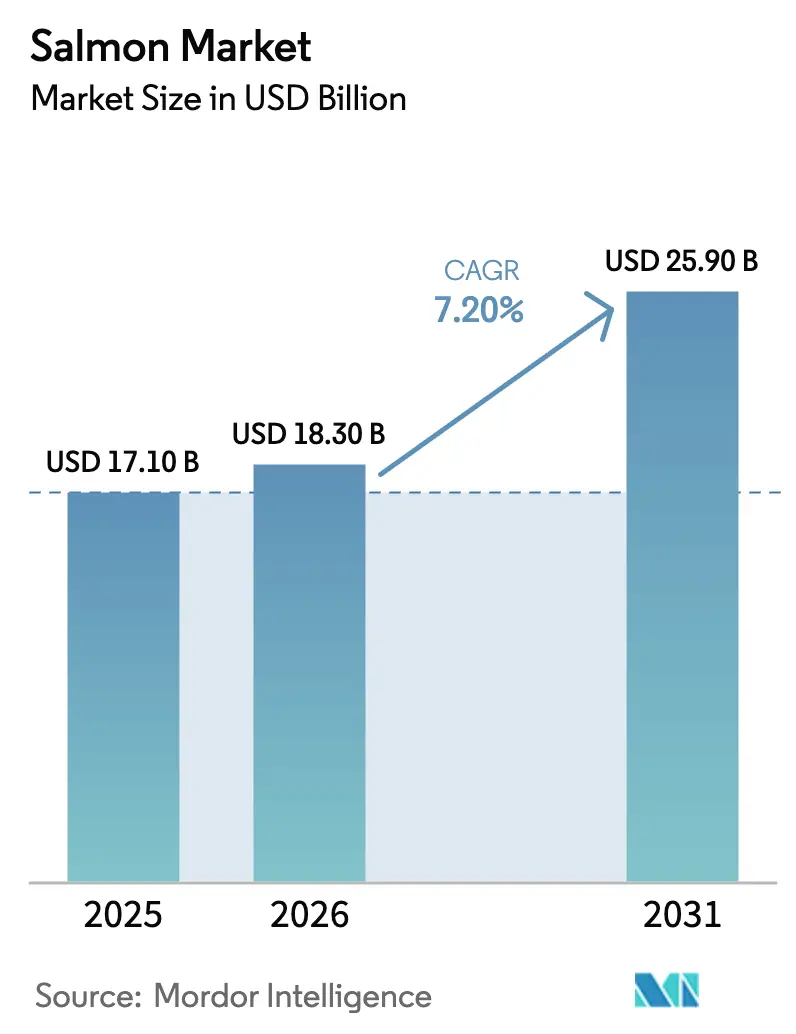

The salmon market size is projected to expand from USD 17.1 billion in 2025 and USD 18.3 billion in 2026 to USD 25.9 billion by 2031, registering a CAGR of 7.2% between 2026 to 2031. This growth rate reflects the rapid build-out of land-based recirculating aquaculture systems that slash freight and disease‐management costs, placing output within a day’s drive of major retail hubs. Norway remained the benchmark producer in 2025, equivalent to 1.4 million metric tons and a significant share of global value, but rising capacity in Saudi Arabia, the United Arab Emirates, and China is steadily rebalancing regional weightings. Feed innovations that cut feed conversion ratios by 10% are cushioning producers against fishmeal price swings exceeding 25% year-over-year. At the same time, regulatory biomass caps in Norway, Scotland, and Canada steer investment toward offshore licenses and closed-containment modules, underpinning a more diversified global supply base.

Key Report Takeaways

- By geography, Europe led the salmon market size in 2025, accounting for 56.0%, and the Middle East is anticipated to grow at a 9.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Salmon Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding cold-chain infrastructure in emerging economies | +1.4% | Asia-Pacific, Middle East, Africa | Medium term (2–4 years) |

| Growing consumer preference for healthy animal protein | +1.8% | Global, highest in North America and Asia-Pacific | Long term (≥ 4 years) |

| Technological advances in recirculating aquaculture systems | +1.5% | North America, Middle East, Asia-Pacific | Medium term (2–4 years) |

| Sustainability certifications influencing buyer decisions | +1.4% | North America, Europe, Asia-Pacific spillover | Long term (≥ 4 years) |

| Development of functional-feed additives that cut FCR by ≥ 10% | +1.1% | Global, early adoption in Norway, Chile, Canada | Medium term (2–4 years) |

| Real-time IoT-based biomass monitoring reducing mortality | +0.8% | North America, Europe, advanced Asia-Pacific farms | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Cold-Chain Infrastructure in Emerging Economies

Multi-temperature logistics hubs commissioned across Southeast Asia and East Africa after 2024 increased the fresh-salmon shipping window from 48 hours to 72 hours, allowing direct-to-retail distribution that earns a 15% to 20% premium over frozen product[1]. Kenya’s 12,000-pallet Mombasa site and the Philippines' National Cold Chain Roadmap, which allocates PHP 8 billion (approximately USD 143 million), have unlocked underserved tier-2 cities. Saudi Arabia’s Public Investment Fund co-financed last-mile fleets, which keep spoilage below 2%, thereby reinforcing the Kingdom’s 19% production CAGR goal. Rising incomes, especially in secondary Asian cities, are shifting consumption toward portion-controlled fresh packs, prompting producers to place land-based farms within 500 kilometers of supermarkets.

Growing Consumer Preference for Healthy Animal Protein

Farmed Atlantic salmon contains 2.0–2.5 grams of omega-3 per 100 grams, aligning with American Heart Association guidance and supporting a 12% rise in United States per-capita intake to 2.55 pounds in 2025. Japanese imports reached 312,000 metric tons as fresh Atlantic salmon displaced local species in sushi and sashimi due to year-round supply and consistent marbling in 2025. Urban Chinese shoppers increased e-commerce purchases by 18% annually, repositioning salmon as a regular protein source rather than a holiday treat. Retailers in North America and Europe now require labels from the Aquaculture Stewardship Council or Global Good Agricultural Practices (GlobalG.A.P.), embedding sustainability in the health narrative and widening price premiums for certified fish.

Technological Advances in Recirculating Aquaculture Systems

Land-based units commissioned since 2024 report survival rates above 95%, compared to 88% to 92% in sea cages, by eliminating sea lice exposure and stabilizing water quality. Pure Salmon’s Jeddah facility was established in 2023, following an agreement with the Kingdom of Saudi Arabia, and was built for SAR 1.9 billion (USD 507 million). The facility recycles 99% of its process water and achieves a feed conversion ratio of 1.05, significantly below the 1.20 sea-cage benchmark. The energy demand of 12–18 kilowatt-hours per kilogram makes co-location with renewable assets an emerging site-selection criterion.

Sustainability Certifications Influencing Buyer Decisions

The Aquaculture Stewardship Council certification covered 45% of the global volume in 2025, and major North American retailers have refused non-certified supplies. Mowi achieved 100% certification in Norway and Scotland, securing multi-year contracts with premiums ranging from 8% to 12%. Global Good Agricultural Practices (GlobalG.A.P.) version 6 tightened biomass limits and antibiotic reporting, prompting investment in cleaner fish and hydrogen peroxide treatments across Chilean farms. German, Dutch, and UK shopper surveys show that 62% actively seek sustainability labels, reinforcing certification as a price-defense tool.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating prevalence of sea-lice and related treatment costs | -1.7% | Norway, Scotland, Chile, Canada | Short term (≤ 2 years) |

| Volatility in fish-meal and fish-oil prices | -1.3% | Global, highest in Chile and Norway | Medium term (2–4 years) |

| Increasing regulatory caps on biomass densities | -1.1% | Norway, Scotland, Canada, Chile | Long term (≥ 4 years) |

| Cyber-physical risks to automated feeding and net-cleaning systems | -0.6% | North America, Europe, advanced Asia-Pacific farms | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Escalating Prevalence of Sea-Lice and Related Treatment Costs

Sea-lice infestation in Norway averaged 0.45 adult females per fish in 2025, more than double the regulatory trigger, adding USD 0.30 to USD 0.50 per kilogram in delousing cost. Thermal barges cost USD 3 to USD 5 million and add USD 0.15 per kilogram in operating expense, while cleaner-fish programs face winter mortality above 20%. Heightened environmental scrutiny of azamethiphos reduces chemical options, nudging capital toward closed-containment and offshore cages that demand 50% to 80% higher capital outlays.

Volatility in Fish-Meal and Fish-Oil Prices

Peruvian anchovy landings fell from 3.2 million metric tons in 2024 to a projected 2.8 million metric tons in 2026, pushing fishmeal from USD 1,850 to USD 2,400 per metric ton over 2024-2026 [2]Source: DP World, “Annual Report 2024,” dpworld.com. Each USD 500 rise lifts feed cost roughly USD 0.25 per kilogram of harvested fish, compressing margins by up to 300 basis points[3]Source: BioMar, “Sustainability Report 2025,” biomar.com. Producers are fast-tracking soy concentrate, insect meal, and single-cell proteins, but regulatory approvals delay full substitution until after 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Europe accounted for 56.0% of the salmon market value in 2025, with Norway contributing the largest share due to sustained export demand and premium pricing driven by tight global supply. The region's dominance is further supported by strong consumer preference for salmon as a healthy protein source. Additionally, advancements in aquaculture technology have increased production efficiency, bolstering Norway's market position.

South America, led by Chile as the dominant producer and exporter, faces environmental challenges such as harmful algal blooms and stricter sanitary-distance regulations enforced by Servicio Nacional de Pesca y Acuicultura. Despite these challenges, the region's growth is supported by producer investments in offshore concessions and recirculating hatcheries aimed at mitigating disease risks and improving survival rates. Brazil's increasing consumption of Chilean salmon underpins stable export demand, as urban households incorporate salmon into regular meal plans. North America's market share in 2025 expanded due to land-based recirculating-system projects that bypass traditional net-pen constraints. However, Canadian producers face mandated transitions to closed-containment systems, which may temporarily disrupt production capacity.

The Middle East is projected to achieve the fastest growth among all regions, with a CAGR of 9.4% through 2031. This growth is driven by sovereign wealth co-investments in large-scale land-based facilities that utilize desalination brine as feedwater to meet stringent environmental regulations. Greenfield recirculating aquaculture projects in Saudi Arabia and the United Arab Emirates are transitioning from pilot to commercial scale, positioning the region as an emerging production hub with near-market delivery advantages. Asia-Pacific is the second-fastest-growing region globally, driven by China's licensing of coastal recirculating facilities that bypass import tariffs and reduce cold-chain lead times. In Japan, omega-3 dietary guidelines sustain retail demand for fresh Atlantic salmon, particularly for premium sushi applications. Africa's contribution to the salmon market remains modest, supported by investments in cold-chain infrastructure that enhance distribution efficiency. However, domestic production is negligible, and the region relies predominantly on imports to meet urban demand.

Competitive Landscape

The salmon market is characterized by significant investments and strategic acquisitions. Mowi's acquisition of Nova Sea for NOK 6.1 billion (USD 570 million) in 2025 and SalMar's purchase of Arnarlax for NOK 9.4 billion (USD 880 million) reflect a vertical integration approach focused on securing low-risk licenses. Investments in capital-intensive technologies, including IoT sensors, automated feeders, and thermal delousing barges, support cost leadership for leading players, further widening the performance gap with mid-tier farms.

Companies like Atlantic Sapphire, Nordic Aqua Partners, and Ocean Harvest utilize modular tank systems and renewable energy co-location to achieve feed conversion ratios below 1.10 while avoiding costs associated with sea lice. However, operational challenges, such as temperature-control failures, have extended payback periods. Despite these setbacks, investor interest remains strong as retailers prioritize certified supply sources located near markets.

Intellectual property filings for enzyme-enhanced and microalgae-based feeds increased significantly after 2024. DSM and BioMar obtained patents that reduced feed conversion ratios by 10% to 12%, highlighting nutrition as a growing area of competition. Certification continues to be essential, as non-certified producers face potential exclusion from mainstream channels in North America and Europe, necessitating operational upgrades or acceptance of price discounts.

Recent Industry Developments

- May 2025: Salmon Evolution reported a 45% quarter-on-quarter increase in biomass and progressed with Phase 2 of its Indre Harøy facility, supporting growth and supply stability in the salmon market.

- March 2025: Kelly Cove Salmon acquired a former AquaBounty facility in Prince Edward Island to increase smolt production capacity and add a new Recirculating Aquaculture System (RAS) unit. This development supports the salmon market by enhancing production efficiency and meeting growing demand.

- March 2025: SalMar acquired full ownership of its offshore subsidiary by purchasing Aker's 15% stake. This move is to strengthen SalMar's position in the salmon market by enhancing its operational control and expanding its offshore farming capabilities.

- January 2025: South Korea has begun operations at its first land-based salmon farm utilizing AKVA technology. This development is to support the salmon market by enhancing local production capabilities, reducing reliance on imports, and ensuring a stable supply of high-quality salmon.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global salmon market as the revenue earned when farmed or wild-caught salmon sold whole, filleted, frozen, smoked, canned, or fresh leaves a processor or an importer at its first commercial sale.

Scope exclusions include fishmeal, collagen, oil, leather, and any other by-products from salmon off-cuts that sit outside this review.

Segmentation Overview

- By Geography

- North America

- United States

- Production Analysis (Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Canada

- Production Analysis (Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- United States

- Europe

- Norway

- Production Analysis (Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- United Kingdom

- Production Analysis (Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Russia

- Production Analysis (Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- France

- Production Analysis (Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Spain

- Production Analysis (Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Italy

- Production Analysis (Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Netherlands

- Production Analysis (Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Greece

- Production Analysis (Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Norway

- Asia-Pacific

- China

- Production Analysis (Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Japan

- Production Analysis (Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Australia

- Production Analysis (Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- China

- South America

- Brazil

- Production Analysis (Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Chile

- Production Analysis (Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Brazil

- Middle East

- Saudi Arabia

- Production Analysis (Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- United Arab Emirates

- Production Analysis (Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Saudi Arabia

- Africa

- Egypt

- Production Analysis (Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- South Africa

- Production Analysis (Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Egypt

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed RAS engineers, feed makers, import distributors, and chilled seafood buyers across Europe, Asia-Pacific, and North America. These conversations tightened biomass ceilings, realistic ex-farm prices, and regional consumption elasticities before we locked the figures.

Desk Research

We began with FAO FishStat harvest series, Norway Directorate of Fisheries export dashboards, UN Comtrade codes, and USDA GATS price lists that map volume-price flows worldwide. Trade bodies such as the Norwegian Seafood Council and SalmonChile then highlighted licensing shifts, disease events, and feed norms that sway biomass. Company filings gathered through D&B Hoovers and news preserved in Dow Jones Factiva revealed capacity moves, while peer-reviewed journals clarified omega-3 demand and RAS efficiency. These sources are illustrative; many other public and paid references guided data checks and clarification.

Market-Sizing & Forecasting

A single top-down pass multiplies each producing country's harvest and wild catch by sampled first-sale prices to set the 2024 base. It then cross-checks this with selective bottom-up producer roll-ups. Five fingerprints, harvest volume, average export price, feed-cost index, new RAS capacity, and per-capita seafood intake feed a multivariate regression that extends the series to 2030; elasticities plug unavoidable gaps.

Data Validation & Update Cycle

Model outputs face variance thresholds; any swing above seven percent versus trend triggers anomaly reviews, extra calls, and model edits. We refresh every study yearly and issue interim flashes whenever disease, trade, or currency shocks materially move the baseline.

Why Mordor's Salmon Baseline Earn Dependable Trust

Published estimates often diverge because firms slice product mix, price point, and geography differently and refresh on uneven calendars.

Key gap drivers we observe are the exclusion of processed formats, reliance on retail receipts, dated baselines, and blanket growth rates that miss the North American RAS build-out.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 23.70 bn (2025) | Mordor Intelligence | - |

| USD 19.10 bn (2024) | Global Consultancy A | Omits smoked & canned, five regions, biennial updates |

| USD 30.59 bn (2025) | Regional Consultancy B | Uses retail values and single 6.7 percent CAGR, lacks supply checks |

| USD 15.96 bn (2022) | Trade Journal C | Old base year, constant 2021 prices, ignores new farms |

Together, the comparison shows that Mordor Intelligence's disciplined scope, variable selection, and annual review give decision-makers a transparent baseline traceable to real harvest data and repeatable steps.

Key Questions Answered in the Report

What is the projected growth rate for the salmon market through 2031?

The salmon market is to grow at a 7.2% CAGR, rising from USD 18.3 billion in 2026 to USD 25.9 billion by 2031.

Which region will expand fastest in value terms?

The Middle East is projected to grow at a 9.4% CAGR through 2031, supported by over USD 500 million in sovereign-linked equity investments.

How do land-based farms influence supply reliability?

They eliminate sea-lice exposure and cut freight by up to USD 2 per kilogram, helping stabilize year-round fresh supply near major retail centers.

Why are sustainability certifications crucial for market access?

North American and European retailers require Aquaculture Stewardship Council or GlobalG.A.P. labels, allowing certified producers to secure contracts at 8%–12% premiums.

What cost risk concerns producers most?

Fish-meal and fish-oil price volatility can lift feed expense by roughly USD 0.25 per kilogram, pressuring margins and accelerating adoption of alternative protein ingredients.

Page last updated on: