Fishing Net Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

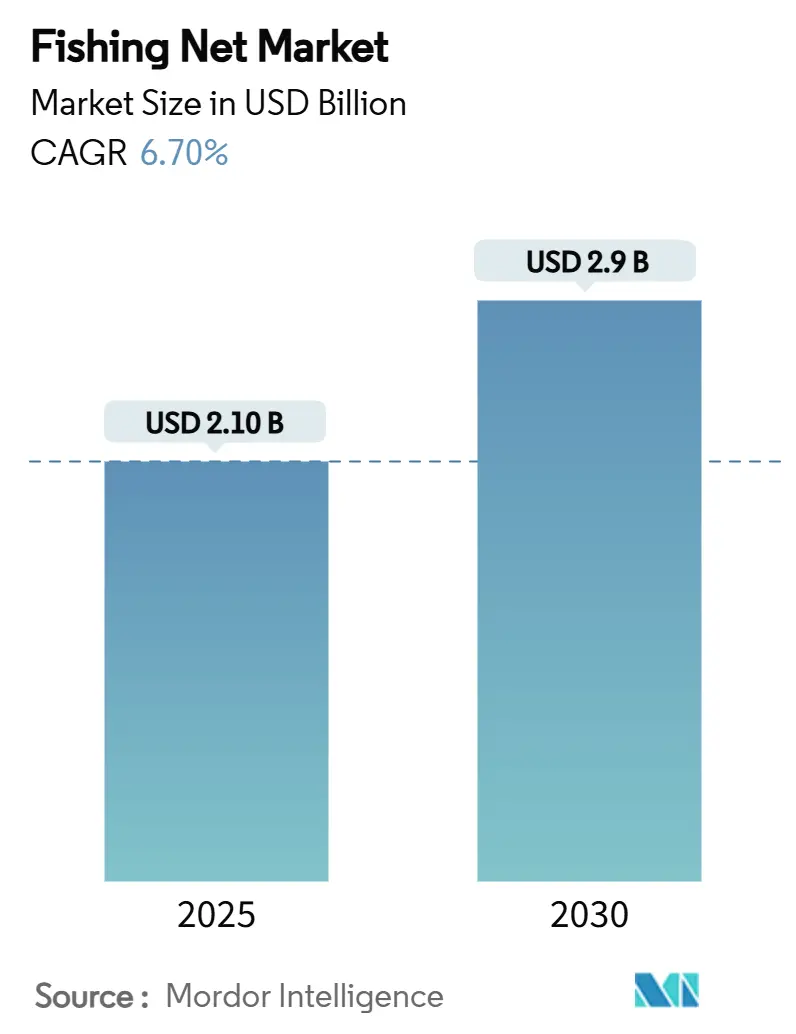

| Market Size (2025) | USD 2.10 Billion |

| Market Size (2030) | USD 2.9 Billion |

| Growth Rate (2025 - 2030) | 6.70% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fishing Net Market Analysis by Mordor Intelligence

The fishing net market size is USD 2.1 billion in 2025 and is forecast to reach USD 2.9 billion by 2030, reflecting a 6.7% CAGR for the review period. Rapid aquaculture build-outs in the Asia-Pacific, steady growth in seafood demand, and ongoing fleet modernization subsidies combine to keep the fishing net market on a sustained expansion path. Breakthroughs in biodegradable polymers, smart sensor integration, and high-strength synthetic fibers are broadening performance expectations and reshaping purchasing criteria[1]Source: FAO Fisheries Division, “The State of World Fisheries and Aquaculture 2024,” fao.org. At the same time, precision aquaculture and shifting gear regulations are steering some buyers toward alternative solutions, forcing suppliers to innovate and recalibrate product portfolios. Competitive intensity is moderate but rising, with the top five suppliers holding a majority share and using technological differentiation as a primary defense against margin pressure.

Key Report Takeaways

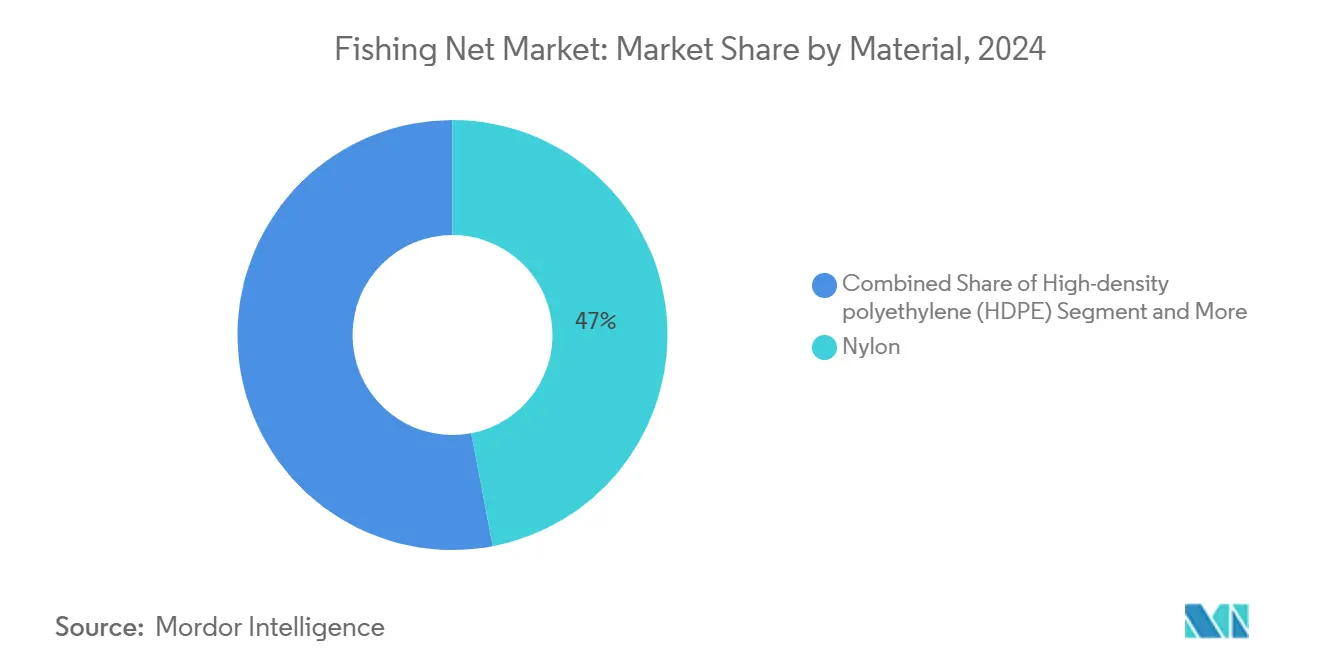

- By material, nylon held 47% of the fishing net market share in 2024, while biodegradable polymers posted the fastest 11.8% CAGR to 2030.

- By net type, gill nets led with a 32% revenue share in 2024, while drift nets are projected to expand at an 8.7% CAGR through 2030.

- By end user, commercial fishing accounted for 54% of the fishing net market size in 2024, whereas aquaculture cages are projected to advance at a 9.1% CAGR.

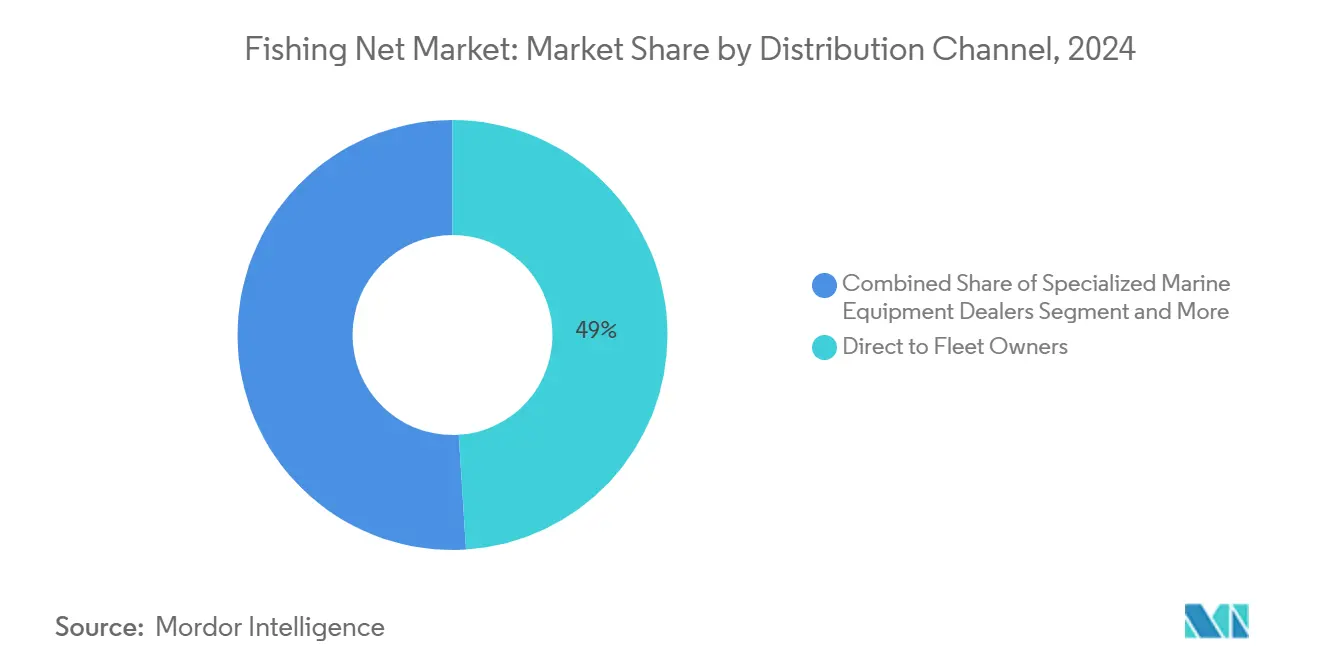

- By distribution channel, direct-to-fleet sales accounted for a 49% share in 2024, while online B2B platforms are projected to rise at a 12.6% CAGR through 2030.

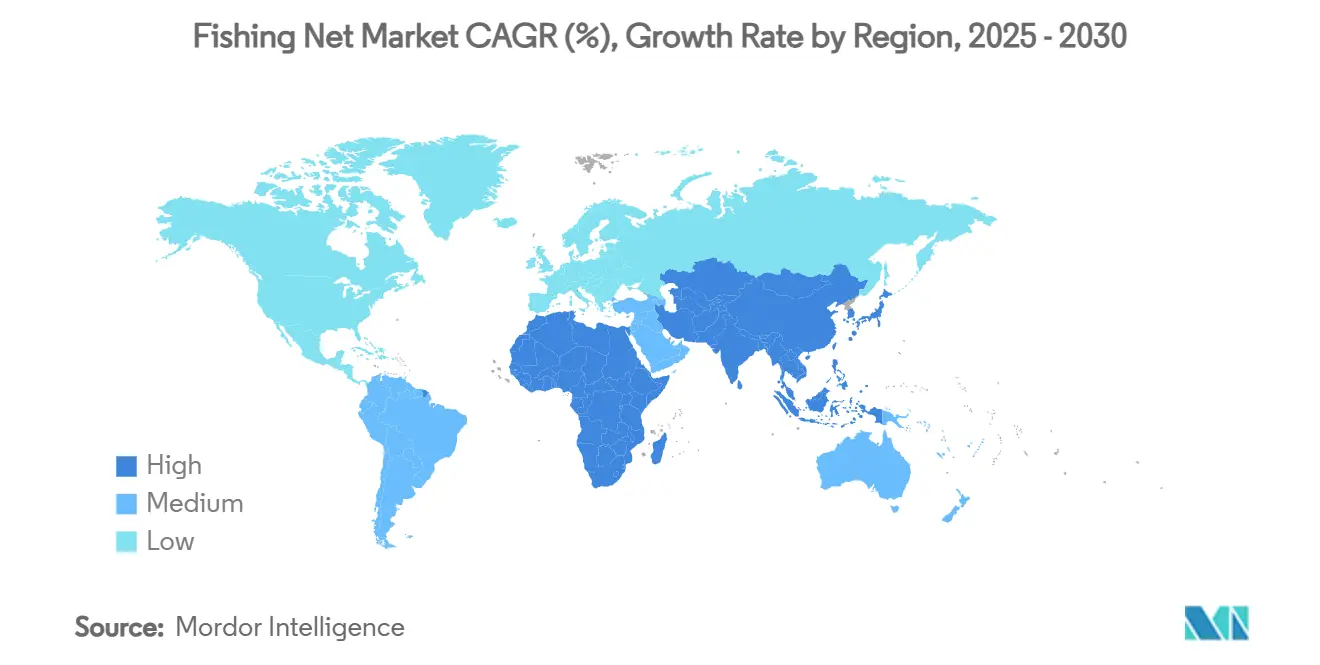

- By geography, Asia-Pacific dominated with a 43% share in 2024, and Africa is forecast to register a 9.2% CAGR through 2030.

- Garware Technical Fibres, Diopas, FISA, AKVA group, and Nitto Seimo collectively controlled majority share of the global market share.

Global Fishing Net Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global seafood consumption | +1.2% | Global, highest in Asia-Pacific, and Africa | Medium term (2-4 years) |

| Accelerating aquaculture capacity additions | +1.8% | Asia-Pacific core, spill-over to Africa and South America | Short term (≤ 2 years) |

| Advances in high-strength synthetic fibers | +0.9% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Government modernization subsidies for fishing fleets | +1.1% | Asia-Pacific and Europe, selective impact in Africa | Medium term (2-4 years) |

| Commercialization of biodegradable net polymers | +0.7% | Europe and North America are leading | Long term (≥ 4 years) |

| Integration of smart sensors in nets for precision catch | +0.5% | Japan, Norway, and other advanced fishing nations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Seafood Consumption

Per-capita fish intake is projected to climb to 21.5 kg by 2030, stretching capture-fish supplies and prompting gear upgrades that boost catch efficiency. Africa’s per-capita consumption is set to slip to 9.8 kg, creating a protein gap that drives public and private aquaculture investment, which in turn lifts demand for specialized nets. Aquaculture overtook capture fisheries in global output during 2024 and should reach 54% of world production by 2032, steering net specifications toward cage-ready formats[2]Source: Jason Holland, “FAO projects a decade of increased fish consumption, but Africa poses concerns,” seafoodsource.com. Operators are prioritizing durability, anti-fouling coatings, and sensor compatibility so they can maximize harvest volumes while complying with evolving sustainability metrics. The sustained consumption trend underpins long replacement cycles and reduces revenue volatility for leading manufacturers.

Accelerating Aquaculture Capacity Additions

Global aquaculture has experienced massive growth in recent years. This surge fuels robust demand for cage nets engineered to handle higher stocking densities and mitigate biofouling. Garware’s patented V2 coating exemplifies supplier responses that claim prolonged net life and lower cleaning frequency. Across Africa, annual aquaculture growth of 11% is doubling the number of net orders for deep-lake cages, designed to handle greater water currents while improving fish welfare. Offshore submersible systems are gaining acceptance, reducing maintenance by 10% and increasing income potential by 44%, placing further emphasis on high-tensile, lightweight designs that can withstand the stresses of open oceans.

Advances in High-Strength Synthetic Fibers

Ultra-high-molecular-weight polyethylene (UHMWPE) blends have markedly extended service life and reduced weight, helping fleets cut fuel use even as workloads climb. Korean polyester-amide polymers deliver 92% decomposition in seawater after 12 months but match nylon for tensile strength, signaling a future pivot toward products that combine performance with end-of-life environmental compliance. European trials with bioplastic netting expose stiffness and strength deficits yet underscore policy commitment to greener alternatives that could mature quickly under incoming gear-disposal directives. Suppliers are thus hedging with dual-track research and development programs, and one focused on maximizing fiber robustness, the other on accelerating eco-friendly degradation while preserving in-use durability.

Government Modernization Subsidies for Fishing Fleets

Global fisheries subsidies total USD 35.4 billion per year, and roughly USD 22 billion is classified as harmful, yet they continue to stimulate near-term equipment spending spikes[3]Source: Pew Charitable Trusts, “A Global Deal to End Harmful Fisheries Subsidies,” pewtrusts.org. China’s CNY 20 billion (USD 3.2 billion) fuel-linked stimulus in 2024 fast-tracked large orders for replacement nets and gear upgrades. A new OECD framework calls for better linkage between subsidies and stock-assessment data, likely redirecting funds toward fleets that adopt verified sustainable gear. Norway’s 40% resource-rent tax adds uncertainty but keeps modernization incentives in place, preserving order flow for premium aquaculture nets designed to meet strict fish-welfare rules. Manufacturers able to certify environmental compliance stand to capture a larger share of subsidy-driven procurements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening regulations on by-catch and ghost-gear disposal | -0.8% | Global, strictest in North America and Europe | Short term (≤ 2 years) |

| Volatile nylon and HDPE feedstock prices | -1.1% | Global, deepest effect in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Shift toward alternative gear (longline, traps) | -0.6% | North America and Europe first, and gradual elsewhere | Medium term (2-4 years) |

| Precision aquaculture curbing capture-fish net demand | -0.9% | Europe and North America are leading | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Regulations on by-Catch and Ghost-Gear Disposal

Regulators are ramping up mandates such as Turtle Excluder Devices and Marine Mammal Take Reduction Plans that require costly net modifications[4]Source: National Oceanic and Atmospheric Administration, “Fishing Gear and Risks to Protected Species,” fisheries.noaa.gov. European Union proposals on abandoned gear encourage fleets to shift toward biodegradable materials, although early trials indicate diminished catch rates that complicate the economics of adoption. Certification agencies impose weighted lines and tori lines, creating a compliance premium for gear that incorporates preinstalled mitigation devices. Small-scale operators face liquidity pressures, but high-value fisheries accept retrofits to maintain eco-labels and market access, which sustains a baseline replacement cadence even under stricter rules.

Volatile Nylon and HDPE Feedstock Prices

Prices for polyethylene and polypropylene climbed in late 2024 due to hurricane-driven prebuying and competitive pricing dynamics, squeezing manufacturer margins. Subsidies worth USD 30 billion to primary plastic producers in China and Saudi Arabia skew cost curves and amplify volatility. Dependence on caprolactam for nylon 6 and ethylene for HDPE creates bottlenecks that quickly transmit to net-makers. In response, suppliers are trialing recycled blends and multi-layer constructions that extend service life, allowing fleets to offset higher upfront costs through longer usage cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Nylon Retains the Lead as Biodegradable Growth Accelerates

Nylon nets held a 47% market share of the fishing net market in 2024, owing to their long-established supply chains, strong abrasion resistance, and broad application versatility. The segment continues to benefit from fleet expansions in the Asia-Pacific region, where operators value predictable performance and straightforward maintenance. At the same time, biodegradable polymers are projected to grow at an 11.8% CAGR, driven by stringent gear-disposal regulations in Europe and performance gains, such as the Korean polyester-amide formula that decomposes 92% within a year while matching the strength of nylon. Feedstock cost volatility for polyethylene and polypropylene spurs a pivot toward recycled content and bio-based inputs, positioning hybrid constructions as a bridge between durability and eco-compliance.

Market differentiation now hinges on advanced coatings that slow biofouling and embedded Radio-Frequency Identification (RFID) tags that track asset life. Nylon suppliers have responded with UV-stable finishes and antimicrobial additives, while biodegradable entrants emphasize life-cycle certification. Buyers weigh the total cost of ownership, factoring in maintenance, end-of-life fees, and evolving subsidy structures that often reimburse eco-compliant purchases. As incentive frameworks mature, biodegradable suppliers could erode nylon’s volume lead, but a wholesale switchover is unlikely before price parity narrows further.

By Net Type: Gill Nets Dominate, Drift Nets Scale Up Through Technology

Gill nets commanded 32% of 2024 revenue due to their ease of deployment and suitability across numerous species. Design upgrades like thinner monofilaments and knot-free panels help minimize bycatch and maintain target species selectivity. Drift nets, while controversial, are projected to post an 8.7% CAGR through 2030, supported by smart-sensor modules that alert crews to saturation points and catch composition. These add-ons elevate net cost but deliver faster haul decisions that increase profitability.

Trawl nets retain a solid installed base in industrial fleets but face mounting regulatory scrutiny over benthic impacts. Manufacturers respond with lighter, higher-opening designs that reduce seabed contact and fuel burn. Seine and cast nets occupy niche segments serving purse-seine operations and small-scale coastal fisheries, respectively. Ongoing research and development aim to build modular frames that allow rapid switching between net formats, creating flexibility for multi-species licenses and supporting vessel utilization gains.

By End User: Commercial Capture Remains Core as Aquaculture Surges

Commercial capture fleets represented 54% of the fishing net market size in 2024 and continue to anchor baseline demand. Subsidy frameworks, notably in China and Norway, funnel recurring capital toward replacement nets that comply with new bycatch and ghost-gear standards. Aquaculture cages, however, are the fastest-growing end-user group at 9.1% CAGR as governments push inland and offshore farming to secure protein supplies. Africa’s 11% annual aquaculture growth and Indonesia’s production leap illustrate the scale of incremental cage-net requirements.

Precision aquaculture modifies this trajectory. Land-based RAS reduces open-water cage demand but increases orders for fine-mesh filters and tank screens. Recreational and artisanal segments stay stable, although gear-type shifts and sustainability labeling slowly shape buyer preferences. Suppliers balance product portfolios by bundling capture and aquaculture lines, offering service contracts that integrate inspection, cleaning, and remote monitoring to build residual revenue streams.

By Distribution Channel: Direct Relationships Prevail, E-Commerce Gains Speed

Direct to Fleet Owners held 49% of the market revenue in 2024, reflecting the technical advisory role suppliers play in tailoring mesh size, knot configuration, and coating choice to vessel-specific requirements. Large fleet owners negotiate multi-year supply agreements that lock in pricing formulas pegged to commodity indices, shielding procurement budgets from feedstock volatility. Online B2B platforms are advancing at a 12.6% CAGR as digital procurement tools grow more sophisticated, integrated inventory systems, and predictive maintenance alerts turn the ordering interface into a value-added service.

Regional dealers persist where fleets are fragmented or require immediate field support. However, some distributors evolve into hybrid models that combine localized stock with cloud-based ordering portals, thereby preserving relevance while reducing overhead. Blockchain pilots test end-to-end traceability, ensuring authenticity and environmental-impact data accompany every net. As more fleets integrate enterprise resource planning modules, seamless API links with supplier catalogs will hard-wire e-commerce into routine refit schedules.

Geography Analysis

Asia-Pacific accounted for 43% of global sales in 2024, with China’s CNY 20 billion (USD 3.2 billion) fleet-modernization grant and Indonesia’s meteoric aquaculture rise underpinning large-volume orders. Japanese research and developement on wide-area tracking and smart-sensor nets amplifies regional technology spillovers, while Indian champion Garware exports to 75 countries and reports 31.4% revenue growth, underscoring the region’s manufacturing heft. Still, precision aquaculture’s spread in advanced economies tempers cage-net growth, prompting suppliers to push higher-value sensor-ready products as a hedge.

Africa is the fastest-growing region, projected at 9.2% CAGR to 2030. The continent’s 11% annual aquaculture expansion outpaces global averages yet still leaves a USD 12 billion infrastructure gap that international lenders and private equity are eager to close[5]Source: Essam Yassin Mohammed, “Accelerating Aquaculture to Combat Africa’s Fish Deficit,” worldfishcenter.org. Benin’s USD 36.4 million modernization project illustrates state-backed momentum, though disease outbreaks and financing constraints persist. Demand tilts toward anti-fouling, predator-resistant cage nets suited to large lakes, with suppliers offering extended credit terms to capture footholds.

Europe and North America form mature markets where regulatory rigor shapes product evolution. Norway’s NOK 175.4 billion (USD 16.4 billion) seafood export windfall supports steady replacement spending, even as a 40% resource-rent tax chills new net-pen projects. Recirculating systems are proliferating in Denmark and the Netherlands, reducing cage volumes but increasing orders for internal screening meshes. Environmental Product Declarations, such as AKVA’s 25 metric tons CO₂ benchmark, encourage suppliers to reduce lifecycle emissions, influencing tender specifications. South America offers a moderate upside, with production volatility tied to disease, and regulatory red tape keeps investment cautious. However, niche, high-value species farming sustains specialized net demand.

Competitive Landscape

Competition is moderately fragmented, yet tilting toward consolidation, as leading firms invest in research and development and expand their global distribution footprints. The top five companies, Garware Technical Fibres, Diopas, FISA, AKVA group, and Nitto Seimo, command a majority share of revenue, but regional specialists still thrive by tailoring products to unique fisheries. Garware leverages its status as the world’s largest salmon aqua-net supplier to introduce the Sapphire CFR predator net and X12 non-pharmacological shield, differentiating on durability and fish-health claims. Diopas expanded its Greek research and development center to accelerate prototype cycles, and FISA’s SUPRA HDPE line targets high-energy offshore cages.

Strategic moves center on vertical integration and sustainability proofs. AKVA’s environmental declaration demonstrates how carbon accounting is becoming a sales tool in Europe, while Nitto Seimo pilots RFID-embedded tags for gear tracking. Biodegradable polymer innovators form a disruptive flank. Korean research labs partner with domestic fiber companies to leapfrog into commercial supply within two years. Established suppliers hedge their investments by signing co-development agreements, ensuring early access to new material platforms.

Market entry barriers rise with each regulatory turn. Gear must pass mandatory tear strength and biodegradation tests in the EU, favoring firms with in-house labs and certification budgets. Scale economies help absorb resin price swings, giving larger players pricing flexibility that squeezes smaller rivals. Still, regional customization, rapid servicing, and consultative selling keep niches open for agile mid-sized competitors, especially in underserved African and South American fisheries.

Fishing Net Industry Leaders

Garware Technical Fibres Limited

Nitto Seimo Co., Ltd.

King Chou Marine Technology Co., Ltd.

AKVA group ASA (Egersund Net)

Miller Net Company, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Kawasaki Heavy Industries unveiled the MINATOMAÉ sustainable aquaculture system, testing trout salmon farming near Kobe to cut logistics costs and improve density management. The pilot validates large scale, land-adjacent aquaculture that can shorten supply chains and improve biosecurity. Wider adoption of this model will raise demand for durable, predator-resistant cage nets, lifting high-end sales in the fishing net market.

- July 2024: Benin, working with the African Development Bank, launched a USD 36.4 million aquaculture hub that targets annual output of 65 million fingerlings and aims to upgrade smallholder production practices. The added capacity will lift regional demand for cage nets and related accessories, reinforcing Africa’s position as the fastest-growing slice of the global fishing net market

- May 2024: Korean scientists created a marine-biodegradable polymer that breaks down by 92% within a year yet matches nylon for strength, setting the stage for commercialization by 2027. Successful scaling of this material could accelerate the shift toward eco-friendly net options and alter long-term material shares across the fishing net market

Global Fishing Net Market Report Scope

| Nylon |

| High-density polyethylene (HDPE) |

| Polypropylene |

| Polyester |

| Biodegradable polymers (PLA, PHA) |

| Gill Nets |

| Trawl Nets |

| Cast Nets |

| Seine Nets |

| Drift Nets |

| Commercial Capture Fishing |

| Aquaculture Cages |

| Recreational/Artisanal Fishing |

| Direct to Fleet Owners |

| Specialized Marine Equipment Dealers |

| Online B2B Platforms |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Chile | |

| Rest of South America | |

| Europe | Norway |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | Nigeria |

| South Africa | |

| Rest of Africa |

| By Material | Nylon | |

| High-density polyethylene (HDPE) | ||

| Polypropylene | ||

| Polyester | ||

| Biodegradable polymers (PLA, PHA) | ||

| By Net Type | Gill Nets | |

| Trawl Nets | ||

| Cast Nets | ||

| Seine Nets | ||

| Drift Nets | ||

| By End User | Commercial Capture Fishing | |

| Aquaculture Cages | ||

| Recreational/Artisanal Fishing | ||

| By Distribution Channel | Direct to Fleet Owners | |

| Specialized Marine Equipment Dealers | ||

| Online B2B Platforms | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Chile | ||

| Rest of South America | ||

| Europe | Norway | |

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | Nigeria | |

| South Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the fishing net market and what is the market projected to reach by 2030?

The fishing net market size stands at USD 2.1 billion in 2025 and is projected to reach USD 2.9 billion by 2030.

Which region leads the fishing net market?

Asia-Pacific holds the largest share at 43% of global revenue, supported by sizable modernization subsidies and rapid aquaculture expansion.

Which material is gaining traction as an eco-friendly alternative to nylon nets?

Biodegradable polyester-amide polymers that decompose 92% in seawater within a year are emerging as the fastest-growing alternative, advancing at an 11.8% CAGR.

How are smart sensors changing fishing net performance?

Embedded sensors provide real-time data on catch load and net geometry, helping fleets optimize hauling schedules, cut fuel use, and reduce bycatch.

What impact do precision aquaculture systems have on net demand?

Recirculating aquaculture systems reduce reliance on large cage nets by recycling up to 99% of water, thereby shifting demand toward fine-mesh tank screens and filtration nets.

Page last updated on: