GCC Fisheries And Aquaculture Market Analysis by Mordor Intelligence

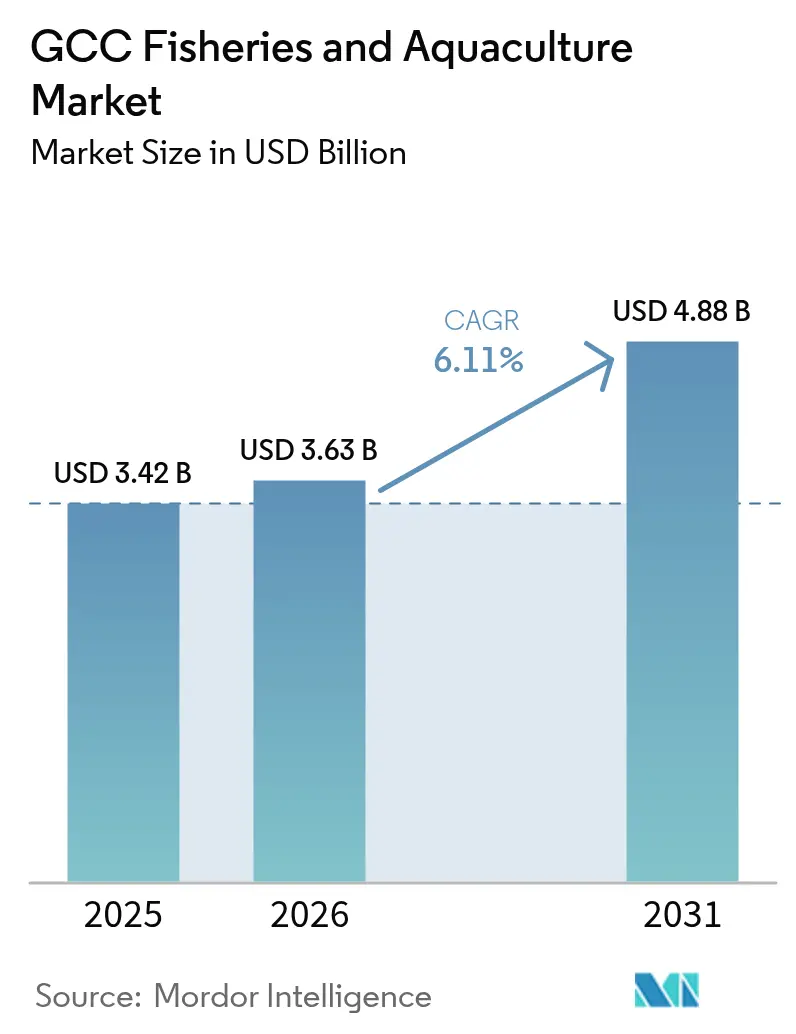

The GCC fisheries and aquaculture market size was valued at USD 3.42 billion in 2025 and estimated to grow from USD 3.63 billion in 2026 to reach USD 4.88 billion by 2031, at a CAGR of 6.11% during the forecast period (2026-2031). This growth is primarily driven by sovereign investments in land-based recirculating aquaculture systems, expedited licensing processes for desert fish farms, and a demographic shift toward younger consumers willing to pay premiums for locally sourced, traceable seafood. Protein self-sufficiency goals in Saudi Arabia and the United Arab Emirates (UAE) provide a stable demand base, attracting investors focused on scaling modern infrastructure. Government support, including zero-interest loans, reduced water lease fees, and duty-free broodstock imports, lowers capital costs by up to 30%. Additionally, investments in green-hydrogen cold chains and blockchain-based traceability enhance export competitiveness. The market is also witnessing a shift toward specialty species, such as farmed salmon, reflecting a growing interest in technology-driven ventures despite higher energy costs.

Key Report Takeaways

- By type, Crustaceans and Mollusks captured 18.45% of the GCC fisheries and aquaculture market size in 2025, while Specialty fish is projected to advance at a 14.80% CAGR through 2031.

- By geography, Saudi Arabia held a 36.05% share of the GCC fisheries and aquaculture market size in 2025, and the United Arab Emirates shows the fastest 11.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Fisheries And Aquaculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing production initiatives | +1.2% | Saudi Arabia, United Arab Emirates (UAE), Oman, and Qatar | Medium term (2-4 years) |

| Rising government support | +1.4% | Saudi Arabia, United Arab Emirates (UAE), Oman, Qatar, Bahrain, and Kuwait | Short term (≤ 2 years) |

| Greater focus on food security | +1.1% | Saudi Arabia, United Arab Emirates (UAE), Oman, Qatar, Bahrain, and Kuwait | Long term (≥ 4 years) |

| Rapid build-out of Recirculating Aquaculture Systems (RAS) in desert zones | +0.9% | United Arab Emirates (UAE), Saudi Arabia, and Qatar | Medium term (2-4 years) |

| Green-hydrogen powered chill-chain pilots | +0.4% | United Arab Emirates (UAE), Saudi Arabia, and Oman | Long term (≥ 4 years) |

| Traceability blockchains mandated by United Arab Emirates retailers | +0.3% | United Arab Emirates (UAE), spillover to Saudi Arabia, and Qatar | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Production Initiatives

National food security programs are channeling capital into offshore cage arrays and hatchery expansions at a pace that outstrips private-sector investment cycles. Saudi Arabia's National Fisheries Development Program allocated USD 320 million in 2024 to co-finance shrimp and tilapia projects, with disbursements tied to production milestones rather than upfront capital expenditures [1]Source: Saudi Ministry of Environment, Water and Agriculture, “National Fisheries Development Program,” MEWA.GOV.SA. This performance-based funding model reduces speculative project launches and concentrates resources on operators with proven hatchery survival rates of 75% or higher. The UAE's Ministry of Climate Change and Environment expedited the issuance of 14 aquaculture licenses in 2024, representing a 40% increase over 2023, with a focus on prioritizing applications that incorporate renewable energy or closed-loop water systems. These initiatives are rebalancing the market away from import reliance, yet they also introduce supply volatility as new farms ramp production in staggered waves rather than smooth increments.

Rising Government Support

Zero-interest loans, reduced water lease fees, and duty-free imports of post-larval shrimp and tilapia fry are lowering the effective cost of capital for aquaculture ventures by an estimated 25% to 30% relative to unsubsidized financing. Saudi Arabia's Public Investment Fund acquired a 35% stake in National Aquaculture Group in 2024, injecting USD 150 million to expand shrimp hatchery capacity from 1.2 billion to 2.0 billion post-larvae annually. Bahrain's National Initiative for Agricultural Development extended duty-free status to imported broodstock and feed additives, reducing input costs for Delmon Aquaculture's seabream operations by 12%. These interventions compress payback periods and enable operators to price output below import parity, yet they also create dependency risks if subsidy frameworks shift in response to fiscal pressures.

Greater Focus on Food Security

Vision 2030 mandates across Saudi Arabia and the United Arab Emirates treat seafood self-sufficiency as a strategic buffer against supply chain disruptions, a calculus reinforced by pandemic-era import bottlenecks and geopolitical tensions affecting Red Sea shipping lanes. Saudi Arabia's target of 55% domestic seafood production by 2030 requires adding 180,000 metric tons of annual output, equivalent to building 12 to 15 industrial-scale shrimp farms or 25 to 30 mid-sized tilapia operations. The United Arab Emirates National Food Security Strategy 2051 prioritizes aquaculture as one of five protein pillars, with interim checkpoints in 2025 and 2028 to assess progress toward 40% self-sufficiency in fish and crustaceans. These policy frameworks are pulling forward investment decisions that might otherwise wait for clearer demand signals, yet they also risk oversupply if multiple countries simultaneously ramp production without coordinating export strategies.

Rapid Build-Out of Recirculating Aquaculture Systems (RAS) in Desert Zones

Closed-loop recirculating systems are gaining regulatory approvals in 6 to 9 months in the United Arab Emirates, compared to 18 to 24 months in jurisdictions with established aquaculture sectors, because Gulf environmental agencies treat Recirculating Aquaculture Systems (RAS) as a low-impact technology that minimizes coastal zone conflicts. Fish Farm LLC's 1,200 metric tons Atlantic salmon facility in Abu Dhabi operates on a 95% water recirculation system, discharging less than 5% of the water daily as treated effluent that meets municipal wastewater standards. The technology's appeal extends beyond speed of permitting as it also insulates production from harmful algal blooms and jellyfish swarms that periodically disrupt open-water cage farms in the Arabian Gulf. The economics of Recirculating Aquaculture Systems (RAS) remain sensitive to energy costs, with electricity representing 25% to 35% of operating expenses. This vulnerability is being mitigated by operators through on-site solar arrays and power purchase agreements tied to renewable tariffs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import dependency for high-value species | -0.8% | United Arab Emirates (UAE), Saudi Arabia, Qatar, Kuwait, Bahrain, and Oman | Medium term (2-4 years) |

| Premium price points for selective species | -0.5% | Saudi Arabia, United Arab Emirates (UAE), Qatar, Bahrain, Kuwait, and Oman | Short term (≤ 2 years) |

| Disease-management skills gap in shrimp hatcheries | -0.6% | Saudi Arabia, Oman, United Arab Emirates (UAE), Qatar, and Bahrain | Medium term (2-4 years) |

| Salinity spikes from desalination brine returns | -0.4% | United Arab Emirates (UAE), Saudi Arabia, Bahrain, Kuwait, Qatar, and Oman | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Import Dependency for High-Value Species

Premium species such as salmon, cod, and sea bass remain 70% import-dependent across the GCC, a structural constraint that limits the market's ability to capture full value-chain margins and exposes operators to currency fluctuations and freight cost volatility. Norway and Scotland supply over 80% of GCC salmon imports, with landed costs in Dubai averaging USD 12 to USD 14 per kilogram in 2024. This price point poses a challenge for domestic Recirculating Aquaculture Systems (RAS) producers, who struggle to undercut it due to high electricity and feed expenses. The United Arab Emirates imported 42,000 metric tons of salmon in 2024, a volume that exceeds the combined output of all planned Recirculating Aquaculture Systems (RAS) projects through 2028, underscoring the scale gap between aspiration and execution [2]Source: UAE Ministry of Climate Change and Environment, “National Food Security Strategy 2051,” MOCCAE.GOV.AE. This import exposure incentivizes domestic production investments, yet the capital intensity of establishing hatcheries and grow-out facilities for cold-water species means that dependency will persist through the forecast period.

Premium Price Points for Selective Species

Domestically farmed species in the GCC often trade 15% to 20% above global benchmarks, a premium that reflects higher input costs for energy, feed, and labor but also constrains volume growth by limiting addressable customer segments to upper-income households and premium dining establishments. Shrimp from National Aquaculture Group's farms retails at USD 23 to USD 25 per kilogram. In Saudi supermarkets, the price ranges from USD 19 to USD 20 per kilogram for imported shrimp from India or Ecuador. Operators are exploring cost reduction through feed localization and solar energy integration, yet structural factors such as high cooling expenses in desert climates will sustain price premiums relative to tropical or temperate producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Species: Crustaceans Lead Volume While Specialty Segments Command Growth

Crustaceans and Mollusks captured 18.45% of the GCC fisheries and aquaculture market size in 2025. This includes crustaceans and mollusks beyond shrimp, such as lobster, harvested primarily in Oman's Dhofar region for export to European markets, and oysters, where Dibba Bay Oysters has carved a premium niche, supplying Michelin-starred restaurants in Dubai and Abu Dhabi. Shrimp holds the largest share in 2024, anchored by National Aquaculture Group's industrial operations in Saudi Arabia's Eastern Province, which produce 35,000 metric tons annually, and emerging projects in Oman's Batinah coast targeting export markets in Asia and the Middle East. Pelagic fish such as sardines, mackerel, and barracuda remain the backbone of Oman's capture sector, with 2024 landings exceeding 150,000 metric tons, yet aging vessel fleets and limited cold storage capacity at landing sites constrain growth.

Specialty fish is projected to advance at a 14.80% CAGR through 2031, a trajectory that reflects capital-intensive bets on import substitution for a species that currently accounts for over 30% of GCC's high-value seafood imports. Specialty segments, such as caviar and salmon, represent less than 5% combined share in 2024 yet attract disproportionate investment due to ultra-high margins. For instance, Emirates AquaTech produces 2 metric tons of sturgeon caviar annually in Abu Dhabi's desert climate using Recirculating Aquaculture Systems (RAS) technology. The segment's diversity creates opportunities for operators to specialize in underserved niches, yet it also fragments marketing efforts and complicates supply chain coordination across species with vastly different handling and storage requirements.

Geography Analysis

Saudi Arabia's 36.05% share in 2025 reflects its dual advantages, extensive Red Sea and Arabian Gulf coastlines totaling over 2,600 kilometers, and the region's most comprehensive aquaculture subsidy framework, which includes zero-interest loans, reduced water lease fees, and co-financing for hatchery expansions. The Kingdom's National Fisheries Development Program disbursed USD 320 million in 2024 to support shrimp and tilapia projects, with performance-based milestones that concentrate resources on operators demonstrating hatchery survival rates above 75%. The National Aquaculture Group's 35,000 metric tons of annual shrimp output positions it as the Gulf's largest single producer, while the Saudi Fisheries Company operates a vertically integrated model spanning capture, processing, and cold storage.

The United Arab Emirates is the fastest-growing geography, 11.45% CAGR through 2031, driven by regulatory frameworks that approve Recirculating Aquaculture Systems (RAS) projects in 6 to 9 months compared to 18 to 24 months in neighboring states and Abu Dhabi's integration of aquaculture into its broader agri-tech cluster strategy. Fish Farm LLC's operational 1,200 metric tons RAS salmon facility exemplifies the Emirates' willingness to back capital-intensive ventures that bypass traditional marine spatial planning constraints, while Asmak's vertically integrated operations spanning 40-plus vessels, processing plants, and retail distribution position it as the region's most diversified seafood player.

Oman holds a significant share in 2025, anchored by pelagic capture fisheries that landed 220,000 metric tons of sardines, tuna, and mackerel, with over 60% exported to Japan, Thailand, and East African markets under Marine Stewardship Council and other sustainability certifications. Qatar, Bahrain, and Kuwait collectively represent smaller shares but are witnessing niche expansions, with Qatar's Al Sulaiteen Farm pioneering shrimp aquaculture in the northern Al Khor zone, Bahrain's Delmon Aquaculture operating the country's only commercial finfish hatchery for seabream and seabass, and Kuwait exploring tilapia aquaponics to overcome land and water constraints.

Regulatory Landscape

Aquaculture and capture-fisheries governance across the GCC is handled by national ministries that combine licensing, environmental oversight, and biosecurity enforcement. In Saudi Arabia, the Ministry of Environment, Water and Agriculture (MEWA) regulates fishing and aquaculture activity and supports sector development through programs such as the National Fisheries Development Program (referenced in this report with USD 320 million allocated in 2024). Regulatory compliance commonly requires project-level technical and economic feasibility submissions, environmental impact assessments, and facility biosecurity plans before licenses are granted, with approvals aligned to national food-security objectives.

In the United Arab Emirates, the Ministry of Climate Change and Environment (MOCCAE) administers aquaculture licensing and biosecurity protocols, supported by Federal Law No. 23 of 1999 governing exploitation and protection of living aquatic resources and subsequent executive regulations. The UAE also applies permit controls for import and export of aquatic organisms, with species-specific restrictions where applicable, and uses service-based permitting (for example, export permits for locally produced fish). Across the GCC, these frameworks elevate traceability, water-quality management, and disease-risk controls as operating conditions for both land-based Recirculating Aquaculture Systems (RAS) and coastal production models.

Value Chain Analysis

The GCC fisheries and aquaculture value chain covers broodstock and fry/post-larvae supply, feed and farm-input procurement, grow-out (coastal cages, ponds, and land-based RAS), harvesting and primary handling, processing (filleting, freezing, value-added), cold-chain logistics, and distribution through wholesale, modern retail, and foodservice. Saudi Arabia and the UAE are seeing increasing vertical integration, where larger operators combine hatchery capacity, grow-out, processing, and branded distribution. At the same time, niche premium producers such as Dibba Bay Oysters and Emirates AquaTech emphasize controlled production, high-grade handling, and direct routes into premium hospitality and retail channels.

Key bottlenecks and upgrade priorities cluster around (i) reliable hatchery output and disease-management capability, (ii) feed economics and localized formulation, and (iii) cold-chain resilience for domestic distribution and exports. Recent ecosystem-building efforts point to this direction, including Saudi Aramco launching the Regional Center for Sustainable Development of Fisheries (RCSDF) on Abu Ali Island, Jubail (June 2025) to support sector capability building, and NEOM with Tabuk Fisheries Company launching Topian Aquaculture (April 2025) to develop marine-pen production at scale. The value chain is also being shaped by faster permitting for desert RAS projects in the UAE (6 to 9 months cited in this report), which increases demand for water treatment, automation, and energy integration from technology and infrastructure providers.

Market Opportunities and Future Outlook

Import substitution remains a clear opportunity in premium seafood, based on the report context that premium species such as salmon, cod, and sea bass are about 70% import-dependent across the GCC, and the UAE imported 42,000 metric tons of salmon in 2024. That gap is pulling investment toward land-based RAS and controlled-environment production, where biosecurity and year-round output are central. In January 2025, ADQ and Finnforel signed a joint venture for a planned 5,000 metric tons RAS salmon facility in Abu Dhabi, with commissioning targeted for Q4 2026, and separate 2026 initiatives broaden the pipeline for land-based and closed-containment projects.

Opportunities are also tied to upstream enabling capacity, including hatcheries, genetics, and health services, and to species diversification supported by purpose-built infrastructure. In Saudi Arabia, National Aquaculture Group and MAT-KULING moved a barramundi hatchery project into construction (reported March 2026) with a stated capacity of up to 40 million fry annually, addressing a constraint for scaling marine and coastal grow-out. In Oman, Fisheries Development Oman started construction on an OMR 23.5 million (USD 61 million) vannamei shrimp farming project in Shinas, North Batinah (reported February 2026), creating a concrete route to expand farmed shrimp supply and related processing and cold-chain throughput. Across the GCC, retailer-led traceability requirements and licensing emphasis on environmental controls also support demand for digital traceability platforms, QA/QC services, and energy-efficient cold-chain solutions aligned with the food-security mandates cited in this report (Vision 2030 in Saudi Arabia and the National Food Security Strategy 2051 in the UAE).

Recent Industry Developments

- May 2026: Oman's Ministry of Agriculture, Fisheries and Water Resources announced the signing of aquaculture investment agreements worth over RO 50 million. The package targets more than 15,000 tonnes of additional annual production capacity, supporting faster scale-up of farm output and associated demand for hatchery supply, feed, and cold-chain infrastructure.

- April 2026: Sara National Trading Company completed the acquisition of a 51% stake in Al-Haridah Aquaculture Company from Saudi Fisheries Company. The transaction reshapes asset control within Saudi Arabia's seafood value chain and can influence how production, processing, and domestic distribution capacity are prioritized across portfolio operations.

- September 2024: Saudi Arabia's Ministry of Environment, Water and Agriculture approved four new Recirculating Aquaculture Systems (RAS) project licenses for grouper, seabass, and barramundi with a combined capacity of 3,500 metric tons. These licenses expand the pipeline for premium finfish production using controlled systems, reinforcing the Kingdom's shift toward technology-intensive aquaculture models.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of fisheries (wild catch) and aquaculture (farmed aquatic output) across GCC countries, measured at the first point of sale and tracked in USD for historical and forecast years.

Scope exclusions: We exclude downstream seafood processing, retail and foodservice margins, and non-seafood inputs such as feed equipment unless they are priced into the first sale value of fish and shellfish.

Segmentation Overview

- By Species Type (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis)

- Pelagic Fish

- Sardine

- Mackerel

- Tuna

- Barracuda

- Demersal Fish

- Grouper

- Trevally

- Emperor

- Pomfret

- Freshwater Fish

- Tilapia

- Crustaceans and Mollusks

- Scallop

- Lobster

- Shrimp

- Specialty Fish

- Caviar

- Salmon

- Pelagic Fish

- By Geography

- Saudi Arabia

- United Arab Emirates

- Oman

- Qatar

- Bahrain

- Kuwait

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the fact base on how much is produced, traded, and consumed across the GCC, and to map the price direction that converts volumes into value. We relied on public datasets such as FAO FishStat, UN Comtrade and national customs portals, World Bank indicators, and official statistics and releases from GCC ministries responsible for environment, agriculture, and fisheries.

To cross-check patterns that are not always visible in one dataset, we also reviewed association websites, port authority updates, and company annual reports and investor presentations for capacity additions and operating changes. Select paid subscriptions for company financials and intelligence, patent databases, and shipment-level import-export data were used to confirm timelines, product mix shifts, and pricing signals. This list is illustrative only, and many other sources were also consulted for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with producers, importers and distributors, large buyers, and sector specialists, so assumptions on prices, product mix, and route to market could be tested in plain language. Coverage was balanced across the GCC, and discussions were used to validate secondary signals, fill gaps where reporting lags exist, and then align the final model with what participants see on the ground.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | |

| Mid tier: 49% | Functional/Unit leaders: 42% | |

| Smaller Players: 14% | Managers: 44% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where production, import, and export series were reconstructed by country, and then translated into market value using observed price trends for key fish and shellfish categories. To keep totals realistic, we also used selective bottom-up checks, such as rolling up a sample of supplier revenues, validating typical farm gate and landing prices through channel checks, and sanity checking value by applying average price per ton to a controlled volume basket.

Inputs that mattered most included capture landings and aquaculture harvest volumes, import and export volumes by product type, price trend movements (including seasonal effects), share of chilled versus frozen in trade flows, and the split between local consumption and re-exports. When a data point was missing for a smaller country or a niche category, the gap was handled through proxy ratios from similar GCC markets and then adjusted using interview feedback. For forecasting, scenario analysis was used around production expansion, policy support, and feed cost driven price pressure, and then the chosen path was aligned to what industry participants expect for supply additions and demand absorption.

Data Validation & Update Cycle

Outputs were triangulated across independent signals, so value totals reconcile with trade balances, production growth, and realistic price ranges. Any large variance triggers a deeper review of the underlying assumption, followed by a second pass where the calculation trail is rechecked and, where needed, respondents are re-contacted to clarify what changed.

The report is refreshed annually, and interim updates are made when material events occur, such as policy shifts, sudden trade disruptions, or major capacity additions. Before delivery, an analyst performs a fresh review so the final numbers reflect the most recent public releases and the latest validation conversations.

Mordor Intelligence's Gcc Fisheries and Aquaculture Sector Analysis Market Size Versus Other Published Estimates

Published market sizes for GCC fisheries and aquaculture do not always match because the scope boundary and the conversion from tons to USD are handled differently across sources. Differences also show up when one estimate blends wild catch and farmed output into one number while another focuses on a narrower supply definition.

The table shows a visible spread that is mainly explained by what is counted as market value and which activities are left outside the number, followed by how price assumptions are carried through the forecast. The table also reflects timing differences, where some publishers anchor the market to an earlier base year and then apply a higher growth curve without re-checking it against production and trade signals each year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.42 B (2025) | |

| Regional Consultancy A | USD 3.04 B (2024) | Uses an earlier anchor year and appears to apply a higher growth curve, with limited visibility on how first sale pricing is derived from GCC price trend signals and whether re-exports are netted out. |

| Industry Publisher B | USD 2.21 B (2025) | Covers aquaculture only, so wild-catch fisheries value is excluded, which lowers the total when compared with a combined fisheries plus aquaculture view. |

The table points to scope as the main driver, and in Mordor Intelligence's model the value includes both capture fisheries and aquaculture at the first point of sale, with volumes and price trends checked against GCC production and trade balances. With these clear steps, the estimate stays traceable to measurable indicators and can be repeated when new statistics or price signals are released.

Key Questions Answered in the Report

How large is the GCC fisheries and aquaculture market in 2026?

It is valued at USD 3.63 billion and is projected to hit USD 4.88 billion by 2031 at a 6.11% CAGR.

Which species segment is growing fastest in Gulf aquaculture?

Specialty fish is expanding at a 14.80% CAGR through 2031, as investors target import substitution for premium cold-water fish.

Why is Saudi Arabia the largest contributor in Gulf seafood?

A dual-coastline exceeding 2,600 kilometers and generous subsidies give Saudi Arabia 36.05% of 2025 value.

What are the main restraints on GCC seafood growth?

Import dependence for high-value species, price premiums on local product, disease skills gaps in shrimp hatcheries, and salinity spikes from desalination brine.

Page last updated on: