Fibrinogen Concentrate Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.43 Billion |

| Market Size (2031) | USD 1.95 Billion |

| Growth Rate (2026 - 2031) | 6.46% CAGR |

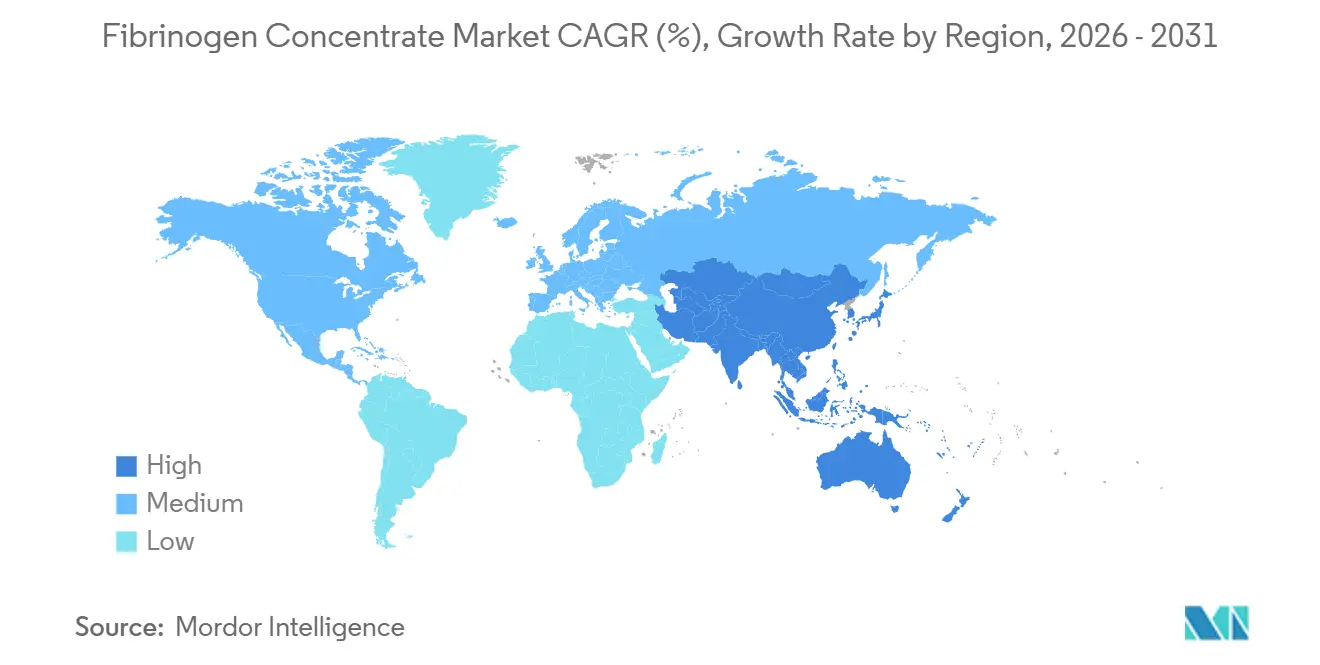

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

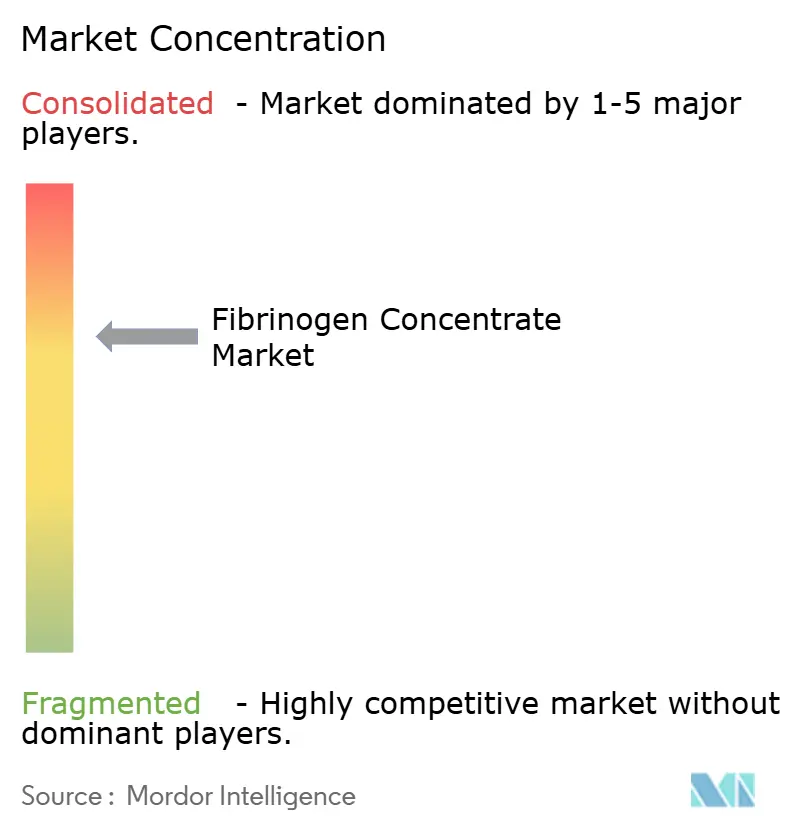

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fibrinogen Concentrate Market Analysis by Mordor Intelligence

The fibrinogen concentrate market size is expected to increase from USD 1.34 billion in 2025 to USD 1.43 billion in 2026 and reach USD 1.95 billion by 2031, growing at a CAGR of 6.46% over 2026-2031. Advances in goal-directed coagulation algorithms, rising adoption of viscoelastic point-of-care testing, and recent U.S. regulatory approvals that validate pathogen-reduced concentrates over cryoprecipitate are expanding clinical use. Payers in North America and Western Europe now factor the operational simplicity of lyophilized vials into coverage decisions, even as pharmacovigilance programs address thrombotic risk signals. Plasma-fractionation capacity additions in China, India, and the United States aim to secure raw material supply, while venture capital targets recombinant platforms that promise long-term resilience against plasma shortages. Defense and aerospace agencies accelerate demand for shelf-stable heat-tolerant formats that fit battlefield and spaceflight medical kits.

Key Report Takeaways

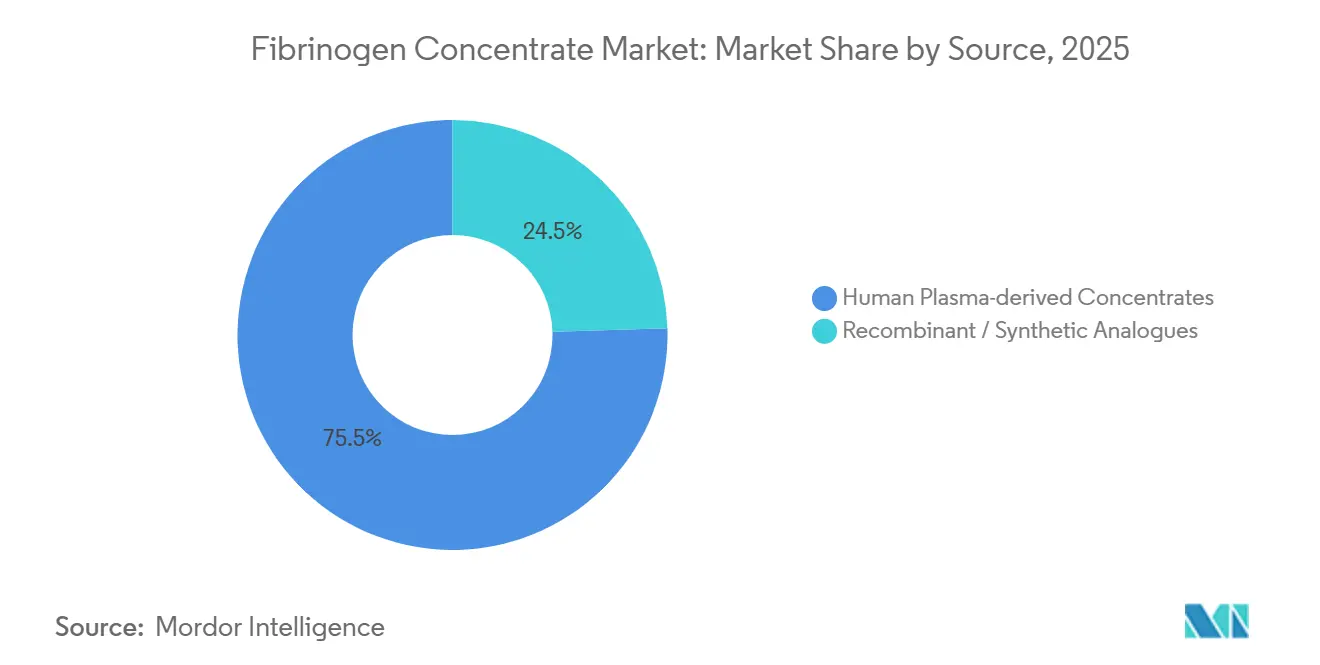

- By source, plasma-derived products commanded 75.54% of the fibrinogen concentrate market share in 2025, while recombinant and synthetic analogues are forecast to expand at a 12.25% CAGR through 2031.

- By application, trauma and surgery led with 46.54% revenue share in 2025; obstetric and gynecological bleeding is projected to advance at a 12.65% CAGR to 2031.

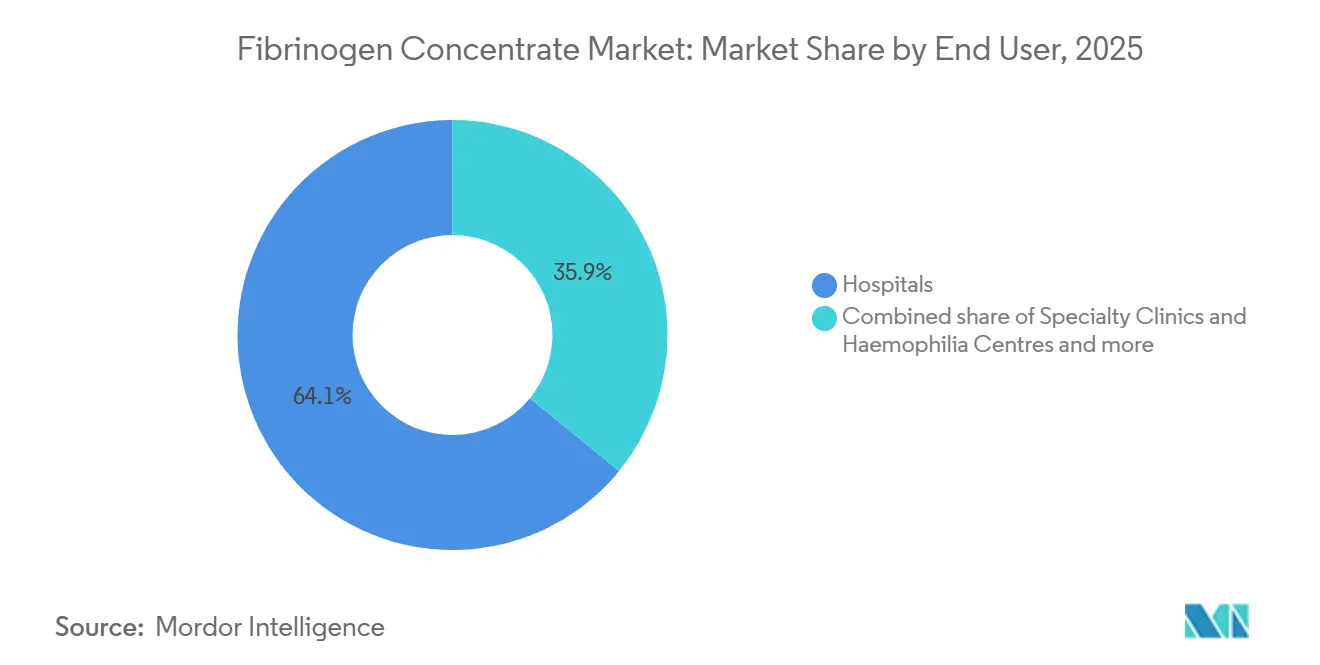

- By end user, hospitals held 64.15% of the fibrinogen concentrate market size in 2025, whereas military and emergency medical services record the fastest projected CAGR at 12.82% through 2031.

- By form, lyophilized powder vials captured 68.23% share of the fibrinogen concentrate market size in 2025 and ready-to-use liquids are gaining at an 11.42% CAGR between 2026-2031.

- By geography, North America led with 37.53% revenue share in 2025, while Asia-Pacific is forecast to accelerate at a 10.1% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fibrinogen Concentrate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing diagnosis of congenital & acquired bleeding disorders | +0.8% | Global; early gains in North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Regulatory shift from cryoprecipitate to virally-inactivated concentrates | +1.2% | North America, Western Europe, Australia | Short term (≤2 years) |

| Capacity expansion of plasma-fractionators in emerging markets | +1.0% | China, India, Brazil, South Korea | Medium term (2-4 years) |

| Shelf-stable heat-tolerant formulations for battlefield & aerospace kits | +0.5% | United States, NATO states, GCC | Long term (≥4 years) |

| Recombinant & plant-based fibrinogen platforms attracting venture capital | +0.4% | North America, Western Europe R&D hubs | Long term (≥4 years) |

| Lab-on-chip viscoelastic point-of-care testing enabling protocolized concentrate use | +0.9% | Global; early adoption in North America, Western Europe, Australia | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Growing Diagnosis of Congenital & Acquired Bleeding Disorders

Rare-bleeding-disorder registries and next-generation sequencing panels make FGA, FGB, and FGG variant detection routine, shrinking the diagnostic gap for fewer than two patients per million affected by congenital fibrinogen loss. Consumption coagulopathy in trauma, obstetrics, and liver disease drives acquired deficiency episodes, prompting Ontario’s March 2025 Major Hemorrhage Protocol to replace cryoprecipitate with a 4-gram fibrinogen bolus. Australia followed in September 2025 with guideline revisions that set a 2 g/L threshold for concentrate use. Collectively, these moves institutionalize fibrinogen concentrate within goal-directed transfusion bundles, reduce product thaw time, and standardize dosing. Improved diagnosis expands the potential treated population, reinforcing market momentum.

Regulatory Shift from Cryoprecipitate to Virally-Inactivated Concentrates

FDA clearance of Octapharma’s Fibryga for acquired deficiency in September 2024, anchored by the 735-patient FIBRES trial, signaled U.S. endorsement of standardized concentrates over variable cryoprecipitate. Ireland, the United Kingdom, and Canada quickly embedded concentrates into national transfusion protocols, with the United Kingdom awarding a GBP 1.168 billion tender in February 2024 that ring-fenced Lot 18 exclusively for fibrinogen concentrate. These policy shifts shorten thaw-to-administration times, lower pathogen-transmission risk, and create predictable demand that encourages capacity expansion by fractionators.

Capacity Expansion of Plasma-Fractionators in Emerging Markets

Grifols’ June 2024 sale of a 20% stake in Shanghai RAAS to Haier and extension of the albumin pact through 2034 exemplify strategic positioning in a nation collecting only 7 of its 12 million-liter theoretical plasma capacity. Bharat Serums and Intas in India and Hemobrás in Brazil add localized throughput that trims import reliance. The World Health Organization’s January 2025 call for domestic fractionation partnerships provides political tailwind and technology-transfer blueprints[1]World Health Organization, “Recommendations for the Prevention and Treatment of Postpartum Haemorrhage,” who.int . Incremental liters of fractionated plasma translate directly into higher output of fibrinogen concentrate, supporting regional supply security and price stability.

Shelf-Stable Heat-Tolerant Formulations for Battlefield & Aerospace Kits

In August 2024 the FDA issued an Emergency Use Authorization for OctaplasLG powder, a freeze-dried plasma containing fibrinogen and other factors, specifically for combat hemorrhage. The U.S. Department of Defense followed with FY 2025 funding lines for dried-plasma technologies, and the Defense Health Agency’s January 2026 communique highlighted logistical gains in austere theaters. Gulf states replicate this procurement pattern for desert deployment. Shelf-stable vials bypass cold-chain constraints, extending product reach to far-forward medics and aerospace missions, a niche that commands premium pricing yet expands total addressable volume.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy cost & uneven reimbursement | -1.1% | Global; acute barriers in Latin America, Middle East, Africa, rural Asia-Pacific | Short term (≤2 years) |

| Thrombotic-event pharmacovigilance burden | -0.6% | Global; heightened scrutiny in North America and Europe | Medium term (2-4 years) |

| Plasma-supply export restrictions after geopolitical shocks | -0.8% | Europe, import-reliant Asia-Pacific | Medium term (2-4 years) |

| Competition from next-gen synthetic fibrin sealant patches | -0.5% | North America, Western Europe, Japan | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Therapy Cost & Uneven Reimbursement

A standard 4-gram dose costs USD 2,000–4,000, a hurdle for hospitals in lower-income regions. Cost-effectiveness analysis from the Canadian FIBRES trial showed median 7-day all-blood-product costs of USD 1,697 for concentrate versus USD 2,063 for cryoprecipitate, yet payer coverage still varies. Anthem’s March 2025 policy added Fibryga under HCPCS J7177, but some Medicaid plans label concentrate investigational for dysfibrinogenemia, limiting access. Static CMS furnishing fees fail to offset hospital acquisition inflation, particularly in safety-net facilities. The reimbursement mosaic slows uptake outside premium health systems.

Thrombotic-Event Pharmacovigilance Burden

FDA review of Fesilty logged a 9% rate of serious thrombotic events in a 45-patient pivotal study, while RiaSTAP labeling warns of arterial and venous thrombosis. Hospitals must implement enhanced monitoring and informed-consent protocols, adding administrative load. Although incidence remains low relative to underlying bleeding risk, clinicians may hesitate in marginal cases, restraining volume growth until long-term safety datasets mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Plasma Dominance Yields to Recombinant Pipeline

Human plasma-derived products captured 75.54% of 2025 revenue, anchoring the fibrinogen concentrate market share with well-entrenched brands such as RiaSTAP, Fibryga, and Fesilty. Takeda’s USD 230 million Los Angeles upgrade underscores ongoing investment to secure plasma inputs. The fibrinogen concentrate market size for plasma products is projected to grow steadily as new collection centers open, yet its CAGR lags the 12.25% pace forecast for recombinant entrants.

Recombinant and synthetic formats, although nascent, promise supply independence and zero pathogen risk. The RECOFIB consortium’s 1 g/L milestone advances commercial viability, and venture funding accelerates bioprocess optimization[2]European Commission, “RECOFIB – Recombinant Fibrinogen Production,” cordis.europa.eu . Cost parity and regulatory equivalence remain hurdles; however, once achieved they can erode plasma dominance. Over the forecast horizon, incremental penetration by recombinant platforms will diversify sourcing and mitigate supply shocks, reshaping competitive dynamics within the fibrinogen concentrate market.

By Application: Trauma Protocols Drive Volume, Obstetrics Accelerates

Trauma and surgical hemorrhage commanded 46.54% of the fibrinogen concentrate market size in 2025 as massive-transfusion bundles mandate immediate fibrinogen replacement. Viscoelastic testing ensures dose precision, curbing wastage and reinforcing hospital adoption. Obstetric bleeding is set to lead growth at a 12.65% CAGR, lifted by WHO 2025 guidance that endorses concentrate over cryoprecipitate for postpartum hemorrhage.

The fibrinogen concentrate market share linked to congenital deficiency remains niche but sustained by new FDA-approved indications that provide prophylactic paradigms. Off-label cardiac and hepatic surgery usage rounds out the application mix, and emerging evidence from ongoing real-world registries is likely to broaden labeled claims, supporting further incremental adoption across specialties.

By End User: Hospitals Anchor Demand, Military Procurement Surges

Hospitals accounted for 64.15% of the 2025 fibrinogen concentrate market share, reflecting entrenched use in trauma bays, operating rooms, and obstetric theaters. Automated EMR prompts linked to TEG or ROTEM shorten decision-to-infusion intervals, increasing throughput.

Military and emergency medical services, though smaller in absolute volume, will expand fastest at 12.82% annually as the U.S. Department of Defense and NATO allies stock heat-tolerant vials to manage battlefield bleeding. Specialty clinics treating congenital deficiencies represent a stable tail segment, relying on predictable prophylactic dosing schedules that support recurring revenue.

By Form: Lyophilized Vials Dominate, Liquids Gain Traction

Lyophilized powder vials held 68.23% of 2025 form-based revenue, underscoring their portability and multi-year shelf life. Kedrion’s Melville and Bolognana expansions dedicate capacity mainly to lyophilized stock, reinforcing supply security.

Ready-to-use liquids grow at an 11.42% CAGR as trauma centers prize the seconds saved by eliminating reconstitution. Cold-chain dependence and shorter expiry constrain rural uptake, but metropolitan Level 1 trauma centers justify premium pricing for time-critical scenarios. As fill-finish technologies improve stability, liquid formats will chip away at lyophilized share, particularly in high-acuity settings within the fibrinogen concentrate market.

Geography Analysis

North America led with 37.53% of 2025 revenue thanks to early regulatory approvals, payer coverage under HCPCS J7177, and widespread viscoelastic testing infrastructure. The United States alone accounts for more than 70% of regional demand as new indications widen the addressable pool, while Canada’s national blood strategy cements concentrate use in major trauma. Mexico remains entirely import-reliant, but formulary inclusion discussions are underway.

Asia-Pacific posts the fastest forecast CAGR at 10.1%, propelled by China’s plasma-fractionation modernization and India’s capacity scale-up[3]Grifols S.A., “Q2 2024 Results,” grifols.com. Japan and South Korea maintain self-sufficient fractionation ecosystems that prioritize high-purity products, whereas Southeast Asian markets still depend on multilateral procurement donors for supply continuity. Upward revisions to postpartum hemorrhage protocols in Australia further stimulate regional uptake.

Europe’s fragmented reimbursement keeps growth moderate. Northern and Western states adopt concentrates rapidly via centralized tenders, but Southern and Eastern regions face budget constraints. LFB’s EUR 500 million capacity build aims to cut U.S. plasma dependence and could smooth future supply. The Middle East and Africa rely on imports, with Gulf Cooperation Council militaries driving niche demand for shelf-stable formats. Latin America lags as reimbursement hurdles and cold-chain limits slow substitution of cryoprecipitate.

Regulatory Landscape

Fibrinogen concentrate is regulated primarily as a plasma-derived biologic, with market access shaped by indication-specific approvals and ongoing post-market pharmacovigilance for thrombotic risk. In the United States, FDA/CBER actions have reinforced the shift from cryoprecipitate to standardized concentrates, including the September 2024 FDA clearance of Octapharma's Fibryga for acquired fibrinogen deficiency and the December 2025 FDA approval of Grifols' FESILTY for acute bleeding episodes in congenital fibrinogen deficiency across pediatric and adult patients.

In Europe, national competent authorities and decentralized procedures continue to determine the pace of access, with Germany's Paul-Ehrlich-Institut granting marketing authorization in November 2025 for Biotest (Grifols Group) Prufibry for congenital and acquired fibrinogen deficiency. Across major markets, regulatory scrutiny emphasizes validated pathogen-reduction steps (such as solvent/detergent treatment and nanofiltration), GMP controls for plasma-derived medicines, and labeling that distinguishes congenital versus acquired deficiency use-cases, which in turn affects hospital protocols and tender eligibility.

Competitive Landscape

The fibrinogen concentrate market features vertically integrated multinationals—CSL Behring, Octapharma, and LFB—that collectively control raw plasma collection, fractionation, and global distribution. Grifols’ Biotest acquisition delivered a 3.5-million-liter German plant, boosting European share. Octapharma’s EUR 200 million Vienna expansion doubled vial capacity to serve Scandinavian and Eastern European tenders. Takeda’s Los Angeles upgrade ensures supply resilience amid geopolitical plasma export scrutiny.

Regional challengers such as Kedrion, Bharat Serums, GC Pharma, and Shanghai RAAS compete on domestic tenders leveraging cost advantages and government relations. White-space disruptors pursue recombinant and plant-based platforms that bypass plasma-collection risk. Synthetic topical patches represent adjacent competition siphoning elective-surgery volume but rarely overlap systemic replacement indications. Entry barriers remain high due to Good Manufacturing Practice compliance, validated viral inactivation, and intensive pharmacovigilance commitments.

Fibrinogen Concentrate Industry Leaders

LFB

Octapharma AG

CSL Behring

Hualan Biological Engineering Inc

Shanghai RAAS Blood Products

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Expanding use beyond congenital deficiency into acquired fibrinogen deficiency and trauma-related settings creates whitespace linked to protocolized care pathways and trial-supported substitution of cryoprecipitate. Randomized evidence and real-world protocol changes are shifting purchasing behavior toward concentrates that align with goal-directed coagulation algorithms and viscoelastic point-of-care testing, with milestones such as the June 2025 publication of the AdFIirst Phase 3 results showing non-inferiority of human fibrinogen concentrate to standard of care in acquired fibrinogen deficiency.

On the supply side, capacity programs and lifecycle-management actions point to where manufacturers are directing capital to meet tender and hospital demand for lyophilized, fast-to-administer products. Grifols' July 2025 EUR 160 million plan for a new site in Llica de Vall, Spain to double plasma fractionation capacity in Europe, and Kedrion's May 2026 EUR 150 million investment at Bolognana, Italy to triple processing capacity to 3.3 million liters per year, target availability in import-reliant systems. At the product level, convenience and dosing precision are being addressed through format extensions such as the FDA-approved 2-gram Fibryga presentation (January 2026), while late-stage programs, including CSL Behring's Phase 3 CSL511 registry update in March 2026, keep momentum in high-bleed surgical settings.

Recent Industry Developments

- June 2026: Grifols launched FESILTY (fibrinogen, human-chmt) in the United States for treatment of acute bleeding episodes in pediatric and adult patients with congenital fibrinogen deficiency. The commercial rollout converts the December 2025 FDA approval into hospital ordering and formulary activity, strengthening Grifols presence in rare bleeding disorders and acute care accounts.

- January 2026: Octapharma USA received FDA approval for a new 2-gram presentation of Fibryga for fibrinogen supplementation in bleeding patients with acquired fibrinogen deficiency. The additional dose format supports dosing flexibility and operational efficiency in time-critical settings such as trauma and surgery, aligning with protocol-driven use supported by viscoelastic testing.

- September 2024: The FDA approved an additional indication for Octapharma's Fibryga for use in acquired fibrinogen deficiency, expanding U.S. labeled use beyond congenital deficiency. This regulatory step validated broader clinical positioning against cryoprecipitate in acquired bleeding scenarios and accelerated protocol and payer discussions around concentrate-based fibrinogen replacement.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues from fibrinogen concentrate used to prevent or treat bleeding where fibrinogen replacement is clinically required. It includes plasma-derived and recombinant concentrates supplied as lyophilized powder or ready-to-use liquid, used across hospital and specialist care settings.

Scope exclusions: Products that are not fibrinogen concentrate, such as fibrin sealants, topical hemostats, and other coagulation factor concentrates, are excluded.

Segmentation Overview

- By Source

- Human Plasma-derived Concentrates

- Recombinant / Synthetic Analogues

- By Application

- Congenital Fibrinogen Deficiency

- Trauma & Surgery-related Haemorrhage

- Obstetric & Gynaecological Bleeding

- Others (Intracranial, Cardiac, etc.)

- By End User

- Hospitals

- Specialty Clinics & Haemophilia Centres

- Military & EMS

- By Form

- Lyophilised Powder Vials

- Ready-to-use Liquid Formulations

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the clinical and supply context, then to build clean assumptions that can be checked against public signals. We mainly refer to sources such as the US FDA and EMA for approvals and label scope, the World Health Organization for blood and plasma system indicators, and the US CDC for procedure and safety related context where relevant.

To support sizing inputs, we also review sources such as peer-reviewed hematology and transfusion medicine journals, national health statistics portals, and customs or trade statistics for plasma fractionation related flows when they are reported. Company annual reports, investor decks, and press releases help align product availability, manufacturing footprints, and geographic focus. A paid subscription for company financials and patent databases is used selectively to cross-check narratives. These sources are not exhaustive, and many other public references were used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work focused on validating the demand pool and real-world use of fibrinogen replacement in acute bleeding and inherited deficiency care. We spoke with a mix of manufacturers and distributors, clinicians involved in trauma, surgery, and obstetrics care pathways, and procurement or pharmacy leaders, with coverage spread across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 20% | APAC: 40% |

| Mid tier: 55% | Functional/Unit leaders: 30% | EMEA: 37% |

| Smaller Players: 20% | Managers: 50% | Americas: 23% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where procedure volumes and bleeding management pathways are used to reconstruct an addressable treatment pool. That pool is then translated into fibrinogen replacement demand using usage rates and dosing patterns. The model is corroborated with selective bottom-up approximations, such as supplier revenue roll-ups in key countries and sampled ASP times volume checks, before totals are adjusted.

Inputs are kept practical and market-specific. The model uses indicators such as trauma and major surgery volumes, obstetric hemorrhage incidence signals, diagnosed congenital fibrinogen deficiency prevalence and treated share, plasma fractionation capacity and supply tightness, and average dosing per episode tied to published clinical practice and expert inputs. Where bottom-up information is incomplete, gaps are handled by applying region-level uptake ratios anchored to hospital access and reimbursement maturity, and then rechecking implied per-capita consumption against clinician feedback.

For forecasting, we mainly use scenario analysis supported by trend lines on the above drivers. Adoption can change stepwise after guideline updates, supply expansions, or new indications. Assumptions are finalized only after pressure-testing with interview feedback on pricing direction, access constraints, and expected changes in care protocols over the forecast window.

Data Validation & Update Cycle

Validation is done through repeated cross-checks between the modeled totals and independent signals, such as implied use per major procedure, supply capacity developments, and regional access patterns. Outliers are flagged early, and then reviewed with an analyst-led variance log so each revision is traceable back to one assumption or input series.

Before sign-off, the work goes through multi-step internal review, and follow-up calls are triggered when an input shift changes the year-by-year trend beyond an acceptable band. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory changes, manufacturing disruptions, or meaningful shifts in clinical practice. Right before delivery, the latest public data and news are rechecked so clients receive an up-to-date view.

Mordor Intelligence's Fibrinogen Concentrate Market Size Compared Against Other Published Estimates

Published market values for fibrinogen concentrate can differ even when the product is described with similar wording, since groups use different definitions for what counts as a sale and how demand is mapped to treatment settings. The largest gaps are typically driven by product scope, the starting year used in the build, pricing assumptions, and the speed of updates after supply or guideline changes.

Fibrin sealants and topical hemostats sit outside Mordor Intelligence's scope, which can lead to lower totals versus estimates that bundle broader surgical hemostasis products alongside fibrinogen replacement. Differences also come from how inherited deficiency versus acute bleeding use is weighted, whether dosing per episode is kept constant or allowed to shift with care protocols, and how currency conversion timing is handled for multi-country totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.34 B (2025) | |

| Global Consultancy A | USD 0.85 B (2025) | Uses a narrower definition focused on human fibrinogen concentrates with more conservative treated-patient assumptions, which can undercount acute bleeding usage tied to trauma, surgery, and obstetrics pathways. |

| Industry Publisher B | USD 1.33 B (2025) | Often reports a similar headline year but can differ in what is counted through channels, how list prices are converted to net pricing, and whether short-term supply constraints are modeled as temporary or persistent. |

The spread in the table mainly comes from what adjacent products are excluded, how the treated pool is constructed, and how pricing is carried forward year to year. By keeping the demand build tied to observable procedure and bleeding indicators, then checking it with practical supplier and pricing signals, we keep the estimate transparent and repeatable for decision-making.

Key Questions Answered in the Report

How large will global demand for fibrinogen concentrate be by 2031?

The fibrinogen concentrate market size is projected to reach USD 1.95 billion by 2031, reflecting a CAGR of 6.46% from 2026 to 2031.

Which therapeutic area will add the most new volume?

Obstetric and gynecological bleeding shows the fastest growth, advancing at a 12.65% CAGR as postpartum hemorrhage protocols adopt concentrate over cryoprecipitate.

Why are recombinant products drawing investment?

They remove dependence on donor plasma, eliminate pathogen-transmission risk, and achieved pilot-scale titers above 1 g/L in 2025, signaling commercial feasibility.

What limits wider uptake in low-income regions?

High per-dose cost and uneven reimbursement policies restrict hospital adoption, despite evidence of clinical and economic value.

How are militaries influencing product design?

Defense buyers demand shelf-stable, heat-tolerant formulations such as freeze-dried plasma, driving manufacturers to prioritize lyophilized formats that do not require cold chains.

Page last updated on: