Electroceuticals/Bioelectric Medicine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

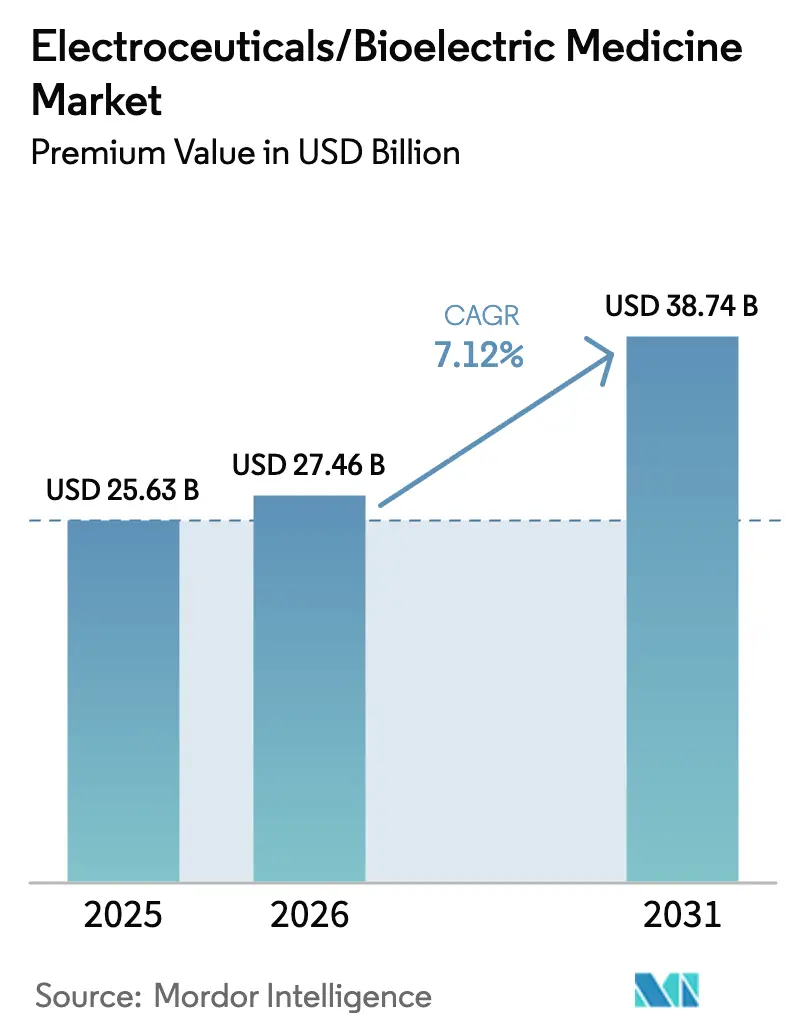

| Market Size (2026) | USD 27.46 Billion |

| Market Size (2031) | USD 38.74 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

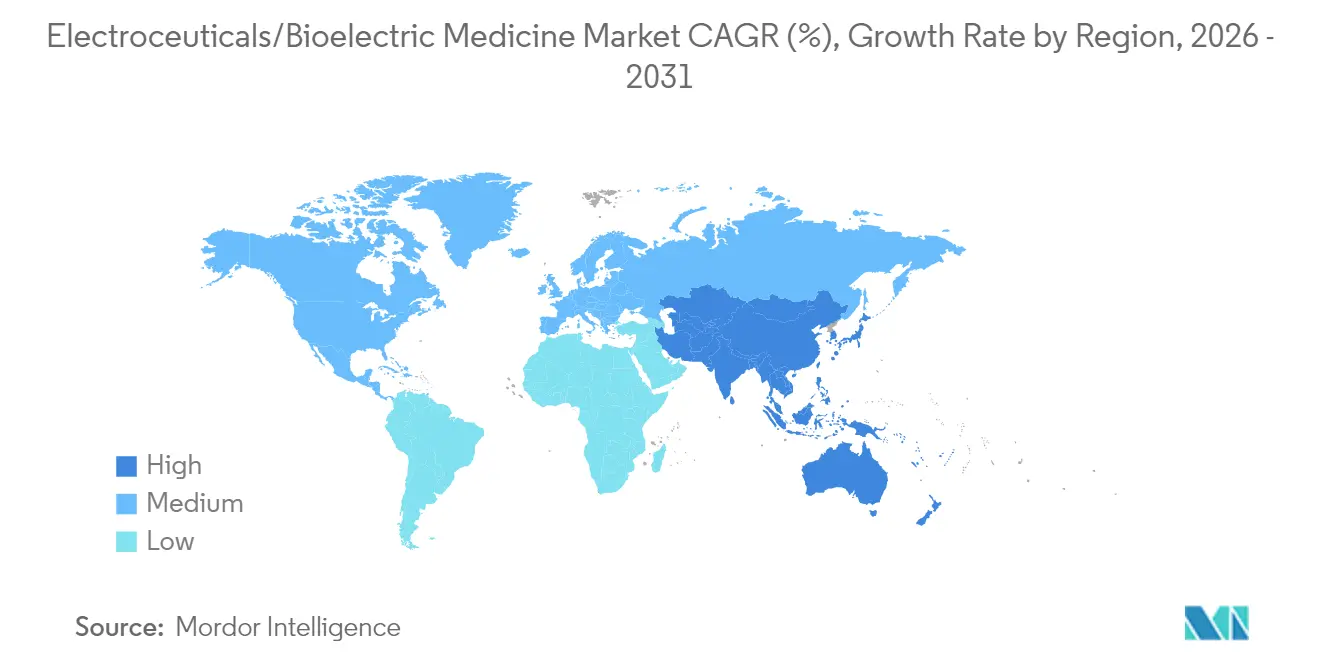

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

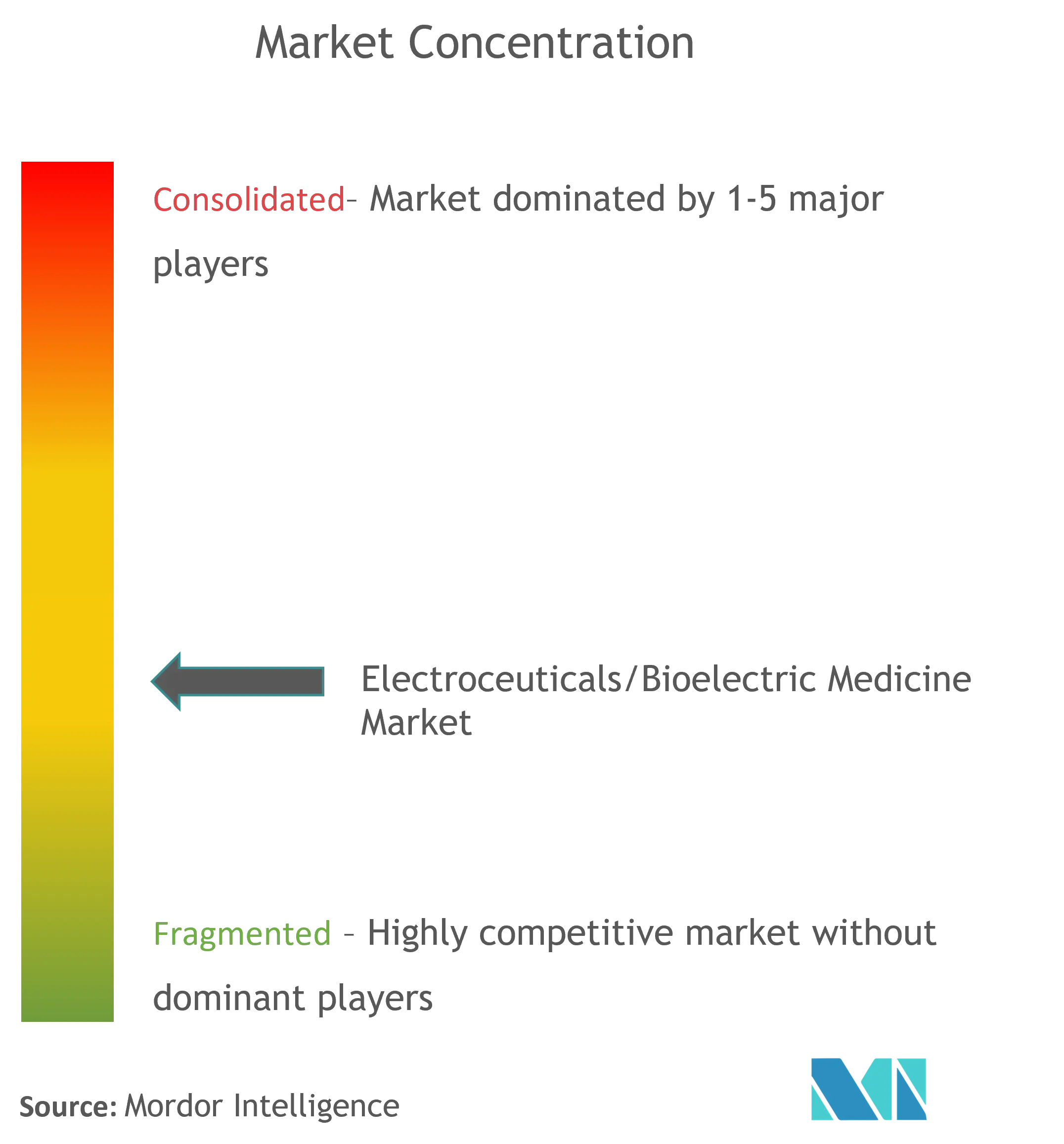

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electroceuticals/Bioelectric Medicine Market Analysis by Mordor Intelligence

The electroceuticals/bioelectric medicine market size was valued at USD 25.63 billion in 2025 and estimated to grow from USD 27.46 billion in 2026 to reach USD 38.74 billion by 2031, at a CAGR of 7.12% during the forecast period (2026-2031). Closed-loop sensing, miniaturized hardware and on-board artificial intelligence now let devices fine-tune stimulation dozens of times per second, opening the door to precision therapy for complex neurological and cardiovascular disorders. Competitive positioning depends less on production scale and more on technological differentiation; firms able to combine adaptive algorithms with reliable power management are taking share. Regulatory agencies in the United States, the European Union and Japan continue to streamline breakthrough-device pathways, accelerating time-to-market for novel platforms while keeping safety thresholds high. Meanwhile, payers are shifting toward value-based reimbursement, favoring device therapies that can document real-world outcome improvements and lower lifetime treatment costs compared with chronic drug regimens.

Key Report Takeaways

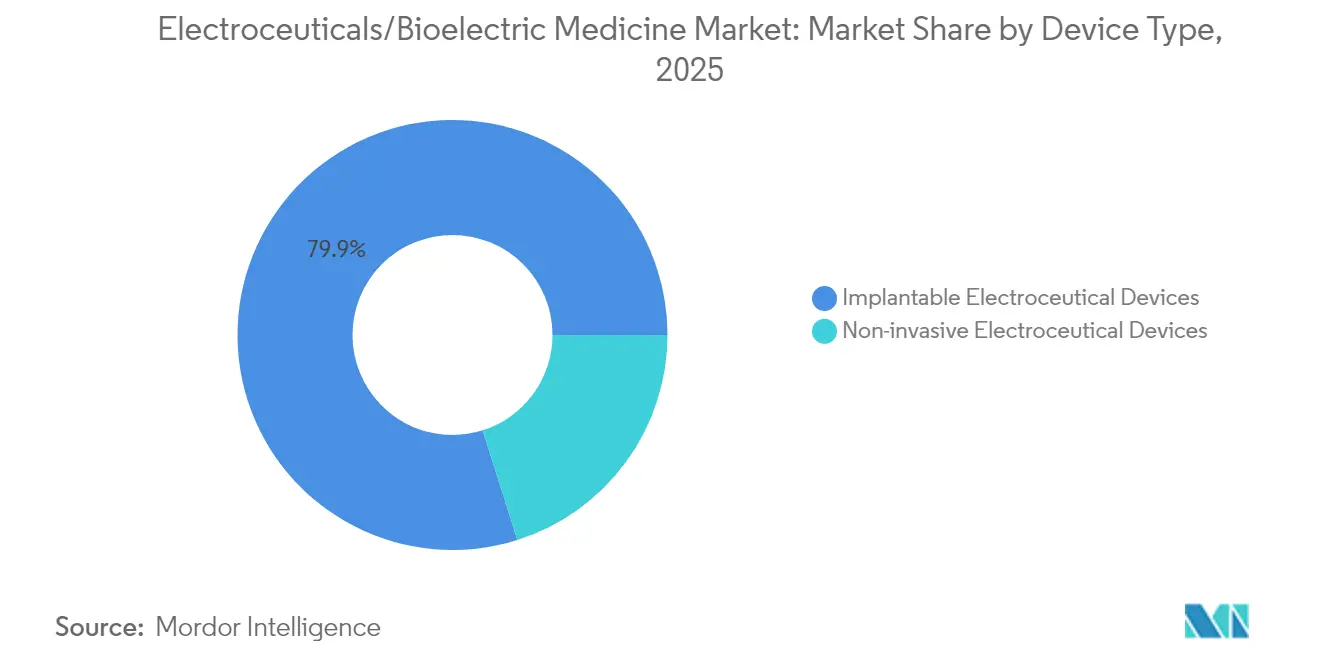

- By device type, implantable systems held 79.88% of electroceuticals/bioelectric medicine market share in 2025, whereas non-invasive devices are forecast to expand at a 9.32% CAGR through 2031.

- By product, pacemakers led with 34.10% revenue share in 2025; vagus nerve stimulators record the fastest projected CAGR at 9.46% to 2031.

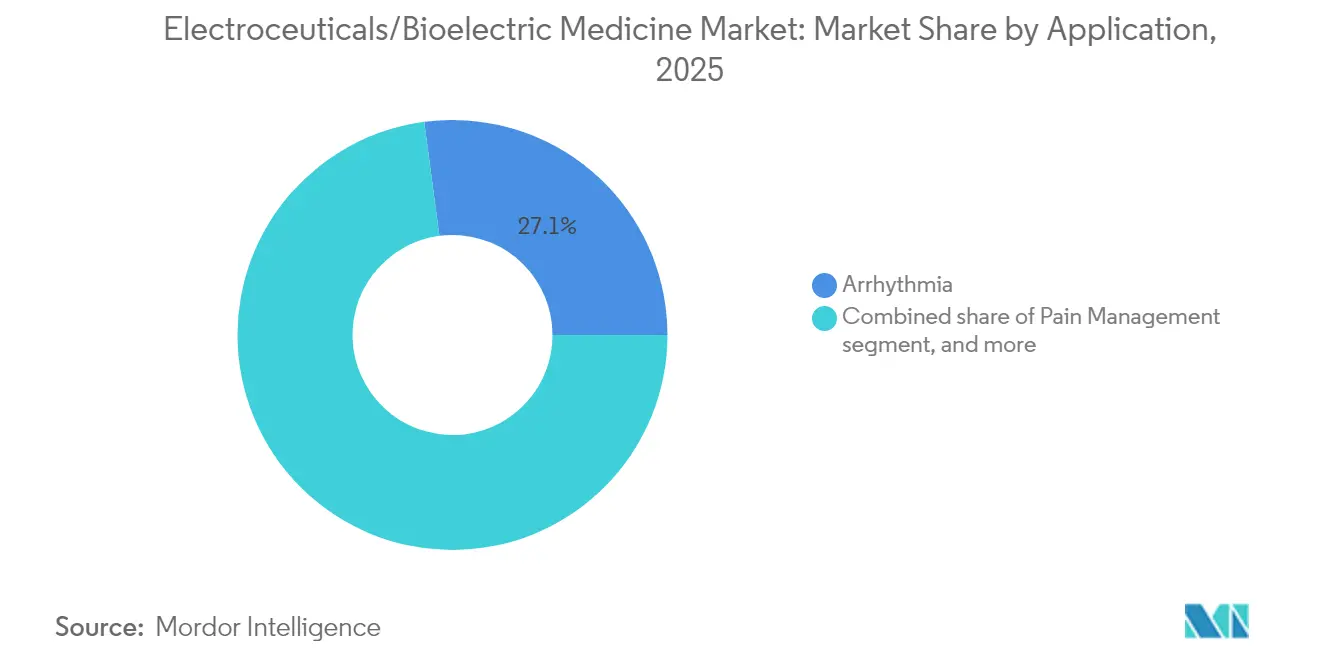

- By application, arrhythmia treatments accounted for 27.10% of the electroceuticals/bioelectric medicine market size in 2025, while depression applications are advancing at a 9.98% CAGR.

- By end user, hospitals retained 61.85% share in 2025, yet home-care settings are growing at 10.05% CAGR as remote monitoring gains traction.

- By geography, North America captured 42.10% market share in 2025; Asia-Pacific represents the fastest-growing region with an 8.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electroceuticals/Bioelectric Medicine Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of chronic neurological & cardiovascular diseases | +1.8% | North America, Europe, global spill-over | Long term (≥ 4 years) |

| Continuous technological innovations in implantable & non-invasive devices | +1.5% | North America, EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Expansion of clinical indications across multiple therapeutic areas | +1.2% | Global | Medium term (2-4 years) |

| Increasing preference for device-based therapies over pharmaceuticals | +1.0% | North America, EU, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Rising healthcare expenditure & favorable government initiatives | +0.8% | Asia-Pacific core, spill-over to Middle East & Africa | Short term (≤ 2 years) |

| Advancements in miniaturization & battery technologies | +0.9% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Chronic Neurological and Cardiovascular Diseases

Worsening prevalence of refractory epilepsy, Parkinson’s disease and heart rhythm disorders is pushing clinicians toward bioelectric interventions able to bypass pharmacological limitations. Real-world evidence shows vagus-nerve stimulation delivered meaningful symptom relief to 71% of treatment-resistant depression patients and cut hospital days significantly[1]Frontiers in Psychiatry, “Vagus Nerve Stimulation for Treatment-Resistant Depression,” frontiersin.org. Closed-loop spinal cord stimulation achieved 93% pain-reduction success in chronic cases, outperforming conventional approaches. As developed-market populations age, multi-morbid patients seek therapies with lower systemic side-effect profiles, reinforcing demand across hospital and outpatient settings.

Continuous Technological Innovations in Implantable and Non-Invasive Devices

The latest generation of stimulators can adjust output 50 times per second, turning therapy from reactive to proactive care. Medtronic’s Inceptiv closed-loop spinal cord stimulator won FDA clearance in April 2024 and has already demonstrated superior outcomes via automatic dose optimization. Miniaturization breakthroughs have yielded pacing modules smaller than a grain of rice; Northwestern University’s light-activated pacemaker eliminates lead-related complications while maintaining efficacy. Focused-ultrasound and transcutaneous platforms now offer near-implant precision without surgery, broadening eligibility to patients previously unable or unwilling to undergo invasive procedures.

Expansion of Clinical Indications Across Multiple Therapeutic Areas

Evidence continues to accumulate for oncology, metabolic and autoimmune uses. Tumor Treating Fields improved overall survival in glioblastoma by 70% when paired with immunotherapy, underscoring the potential of electrical fields to disrupt cancer cell division. In gastroenterology, targeted vagal modulation is alleviating inflammatory bowel diseases, while electric dressings cut wound-healing times by 30%. Psychiatric care is a fast-emerging frontier, with transcutaneous auricular stimulation easing borderline personality disorder symptoms in early trials. This diversification shields manufacturers from reimbursement headwinds in any single indication.

Increasing Preference for Device-Based Therapies Over Pharmaceuticals

Long-term medication often brings cumulative toxicity and escalating cost, prompting stakeholders to explore durable implant- or patch-based alternatives. Spinal cord stimulators have delivered better pain control at lower lifetime expenditure and sharply cut opioid reliance. Patient surveys report 88% preference for adaptive neurostimulators that demand fewer clinic visits and provide individualized dosing. Value-based care contracts amplify this shift, rewarding interventions with documented quality-of-life gains and reduced downstream spending.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & procedural costs of electroceutical therapies | −1.2% | Global, especially acute in developing regions | Short term (≤ 2 years) |

| Complex & stringent regulatory approval processes | −0.8% | Worldwide with regional variability | Medium term (2-4 years) |

| Limited reimbursement coverage in developing regions | −0.6% | Asia-Pacific, Latin America, parts of Africa | Short term (≤ 2 years) |

| Data security & patient privacy concerns in connected devices | −0.5% | North America, Europe, spreading to other connected-health markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Procedural Costs of Electroceutical Therapies

Initial expenditure ranges from USD 310 for clinic-based transcutaneous sessions to nearly USD 60,000 for complex implantable pulse generators, straining budgets in cost-sensitive systems. CMS reimbursement caps still confine auricular vagus stimulation to restricted indications, forcing providers to absorb part of the expense. Alongside the device, hospitals shoulder additional outlays for imaging, programming consoles and specialized staff, while patients may face follow-up revision surgeries if leads migrate or batteries deplete. These front-loaded costs, though often offset by long-term drug-savings, slow uptake in markets with constrained capital cycles.

Complex and Stringent Regulatory Approval Processes

Fragmented global rules add years and millions to development timelines. Japan’s well-documented “device lag” persists despite its USD 40 billion market and a 5.5% forecast CAGR[2]U.S. Department of Commerce, “Japan Medical Device Market,” trade.gov. China’s 2024 revision of its device law tightens safety reviews yet promises longer dossiers, raising hurdles for smaller innovators. Divergent risk-classification and post-market surveillance frameworks oblige firms to run overlapping trials, duplicate audits and adapt labeling for every jurisdiction. Although groups such as the International Medical Device Regulators Forum promote harmonization, meaningful convergence remains a mid-decade prospect.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Implantables Hold Sway as Non-Invasive Platforms Accelerate

Implantable systems commanded 79.88% share of the electroceuticals/bioelectric medicine market in 2025, reflecting their unmatched ability to deliver continuous, high-precision stimulation deep within neural or cardiac tissue. Leadless pacemakers, injectable electrodes and micro-battery advances have trimmed incision sizes and reduced infection risk, keeping implants attractive for high-acuity cases. Epiminder’s Minder, the first implantable continuous EEG monitor cleared by the FDA in April 2025, illustrates how sensing and therapy now coexist inside a single platform.

Non-invasive devices are progressing at a 9.32% CAGR to 2031, buoyed by payer enthusiasm for outpatient-friendly solutions and patient demand for needle-free care. Focused ultrasound, transcutaneous magnetic stimulation and next-generation wearables have tightened the efficacy gap with implants for several mental-health and pain indications. Over the forecast horizon, R&D pipelines suggest a convergence: implants will become less traumatic, while surface devices will gain targeting depth through adaptive waveform modeling, crowding the mid-invasiveness continuum.

By Product: Pacemakers Retain Leadership while Vagus Nerve Stimulators Surge

Pacemakers held 34.10% product revenue in 2025, an anchor position built on decades of clinical evidence and clear reimbursement coding. The electroceuticals/bioelectric medicine market size for pacemakers grows steadily as dual-chamber leadless models such as Abbott’s AVEIR DR secure 97% atrio-ventricular synchrony and simplify implant workflows. At the same time, vagus nerve stimulators are expanding at 9.46% CAGR, propelled by new protocols for depression, rheumatoid arthritis and even obesity.

Defibrillators and deep-brain stimulators keep advancing through smarter arrhythmia detection and adaptive frequency delivery, yet vagus platforms presently set the innovation pace. Studies showing 71% responder rates in drug-resistant depression are driving fresh clinical guideline endorsements. As software-defined therapy grows, manufacturers differentiate less on hardware and more on algorithm accuracy, cloud analytics and machine-learning-guided titration.

By Application: Arrhythmia Dominance Gives Way to Mental-Health Momentum

Arrhythmia therapies led the electroceuticals/bioelectric medicine market with 27.10% share in 2025, supported by well-established cardiology care pathways and public screening initiatives. Growth, however, is moderating as penetration nears saturation in high-income nations. In contrast, depression applications are scaling at 9.98% CAGR, catalyzed by rising mental-health awareness and inconsistent efficacy of pharmacological antidepressants.

Pain management remains a large installed base where closed-loop spinal cord systems have shown 93% functional improvement rates. Parkinson’s disease care took a step forward in February 2025 when the FDA cleared the first adaptive deep-brain stimulation platform that adjusts current based on real-time neural signals. Oncology use cases, particularly Tumor Treating Fields, hint at a future where bioelectric modulation works alongside immunotherapy to slow tumor proliferation.

By End User: Hospitals Command Volume as Home-Care Uptake Quickens

Hospitals controlled 61.85% of 2025 system placements, a function of surgical complexity and the need for multidisciplinary intraoperative teams. Teaching centers also dominate early adoption of investigational protocols, reinforcing institutional share. Yet home-care channels are on track for a 10.05% CAGR as wireless telemetry, smartphone-based dashboards and auto-titration software simplify patient self-management.

Ambulatory centers bridge these models, handling day-case leadless pacemaker implants and generator exchanges that once demanded overnight stays. The electroceuticals/bioelectric medicine market size flowing through non-hospital sites will rise steadily as reimbursement codes for remote programming and virtual follow-up mature. The COVID-19 era normalized telehealth consults, giving payers and regulators a blueprint for remote neuro-stimulation supervision.

Geography Analysis

North America retained 42.10% market share in 2025 on the back of an innovation-friendly regulatory regime, high disposable income and payer openness to device-based disease management. The FDA’s April 2025 authorization of Epiminder’s Minder illustrates how breakthrough pathways bring sensor-rich implants to clinics faster than in most regions. Provider familiarity with neuromodulation keeps pacemaker and spinal-cord-stimulator volumes rising, while veterans’ health programs accelerate uptake of closed-loop pain solutions.

Europe remains a cornerstone for evidence-driven adoption. Harmonized CE-Mark protocols create a single entry point, yet the Medical Device Regulation has tightened clinical-data expectations, lengthening dossiers but bolstering patient confidence. Boston Scientific’s FARAPULSE won Japanese clearance in September 2024 after European roll-out, demonstrating Europe’s role as a proving ground for pulsed-field ablation.

Asia-Pacific is the growth engine with an 8.38% CAGR outlook. Japan’s USD 40 billion device market continues to liberalize reimbursement for neuromodulation despite persistent approval lag. China’s revised device law, enacted October 2024, integrates risk-based review but increases documentation depth, prompting local-international joint ventures to navigate submission complexities. Rising chronic-disease prevalence and rapidly expanding private insurance pools in India and Southeast Asia further enlarge the prospective user base.

Middle East & Africa and South America hold smaller revenue but sizable runway. Gulf Cooperation Council states finance specialized cardiac-rhythm programs, stressing implant success metrics to guide tender awards. In Brazil, tele-stimulation pilots for chronic pain are under evaluation at federal teaching hospitals, which may seed broader adoption once efficacy and cost-benefit are demonstrated locally.

Competitive Landscape

Market concentration sits at a moderate level: the top five manufacturers collectively hold well over half of revenue, yet niche start-ups continue to attract funding for unaddressed indications. Boston Scientific booked 13.6% organic revenue growth and USD 1.208 billion profit in 2024, crediting pulsed-field ablation for part of the gain[3]University of Nebraska, “Boston Scientific 2024 Financial Report,” unl.edu. The February 2025 acquisition of pain-stim specialist Nevro by Globus Medical for USD 250 million underscores the premium placed on closed-loop neuromodulation know-how. Medtronic, Abbott and Boston Scientific remain the scale leaders, leveraging integrated manufacturing, global service networks and extensive clinical-trial portfolios.

Challengers carve out beachheads in mental health, metabolic regulation and wound care, often partnering with university labs for proof-of-concept studies before courting strategic investors. Venture capital continues to back early-stage neuro-tech, although rising capital-efficiency demands tilt funding toward platforms with scalable software and remote-upgrade capability. Competitive focus has shifted from hardware miniaturization alone to data-driven outcome analytics, cybersecurity safeguards and cloud-based over-the-air firmware updates. As payer models migrate toward longitudinal bundled payments, suppliers that can document durable efficacy over multi-year horizons are poised to win formulary preference.

The intellectual-property landscape remains active, with hundreds of patents filed annually around bio-signal detection, adaptive waveform libraries and energy-harvesting power modules. Litigation risk is climbing in markets where device classes converge, prompting firms to seek cross-licensing deals that secure freedom-to-operate while keeping R&D on schedule.

Electroceuticals/Bioelectric Medicine Industry Leaders

Boston Scientific Corporation

Medtronic

Biotronik SE & Co. KG

Koninklijke Philips N.V.

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Epiminder secured FDA authorization for Minder, the first implantable continuous EEG monitor approved under the De Novo pathway.

- February 2025: Globus Medical completed a USD 250 million acquisition of Nevro Corp, broadening its neuromodulation portfolio for chronic pain.

- February 2025: Medtronic gained FDA clearance for the BrainSense Adaptive DBS system, the first deep-brain stimulator that adjusts therapy using real-time neural feedback.

- November 2024: The FDA approved the VARIPULSE catheter-ablation platform for paroxysmal atrial fibrillation; 74.4% of patients remained arrhythmia-free at 12 months.

- August 2024: FDA green-lit the Altius direct electrical nerve-stimulation system for phantom-limb pain, documenting ≥ 50% relief in pivotal trials.

Global Electroceuticals/Bioelectric Medicine Market Report Scope

As per the scope of this report, bioelectronic medicine focuses on electrical signaling in the nervous system. Bioelectronic medicine is a new approach to treating and diagnosing disease. It represents a convergence of molecular medicine, neuroscience, and bioengineering. It uses a medical device (electrical pulses) and the body's natural mechanisms as an adjunct or alternative to drugs and medical procedures. The Electroceuticals/Bioelectric Medicine Market is Segmented by Device Type (Implantable Electroceutical Devices, Non-invasive Electroceutical Devices), by Product Type (Defibrillators, Pacemakers, Stimulator, and Others), by Application (Arrhythmia, Pain Management, Parkinson's Disease, Depression, Others), End-user (Hospitals, Clinics, Others) and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD million) for the above segments.

| Implantable Electroceutical Devices |

| Non-invasive Electroceutical Devices |

| Defibrillators |

| Pacemakers |

| Stimulators |

| Cochlear Implants |

| Others |

| Arrhythmia |

| Pain Management |

| Parkinson's Disease |

| Depression |

| Other Applications |

| Hospitals |

| Ambulatory Surgical Centers |

| Home Care Settings |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Implantable Electroceutical Devices | |

| Non-invasive Electroceutical Devices | ||

| By Product | Defibrillators | |

| Pacemakers | ||

| Stimulators | ||

| Cochlear Implants | ||

| Others | ||

| By Application | Arrhythmia | |

| Pain Management | ||

| Parkinson's Disease | ||

| Depression | ||

| Other Applications | ||

| End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Home Care Settings | ||

| Other End Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the electroceuticals medicine market?

The electroceuticals medicine market size reached USD 27.46 billion in 2026 and is forecast to hit USD 38.74 billion by 2031 at a 7.12% CAGR.

Which device category dominates the market?

Implantable electroceutical systems hold 79.88% share, reflecting clinician confidence in their precision and durability.

What is the fastest-growing product segment?

Vagus nerve stimulators are advancing at a 9.46% CAGR as clinical protocols expand from epilepsy to mental-health and inflammatory disorders.

How quickly are home-care electroceutical therapies growing?

Home-care adoption is rising at 10.05% CAGR thanks to wireless monitoring and simplified user interfaces that support self-management.

Which region offers the highest growth potential?

Asia-Pacific leads in growth, expected to post an 8.38% CAGR through 2031, driven by aging populations and improving reimbursement.

What major trend will shape competition over the next five years?

Integration of real-time sensing with AI-driven adaptive algorithms is set to become the primary differentiator, shifting competition from hardware specs to data-enabled outcomes.

Page last updated on: