Cryotherapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

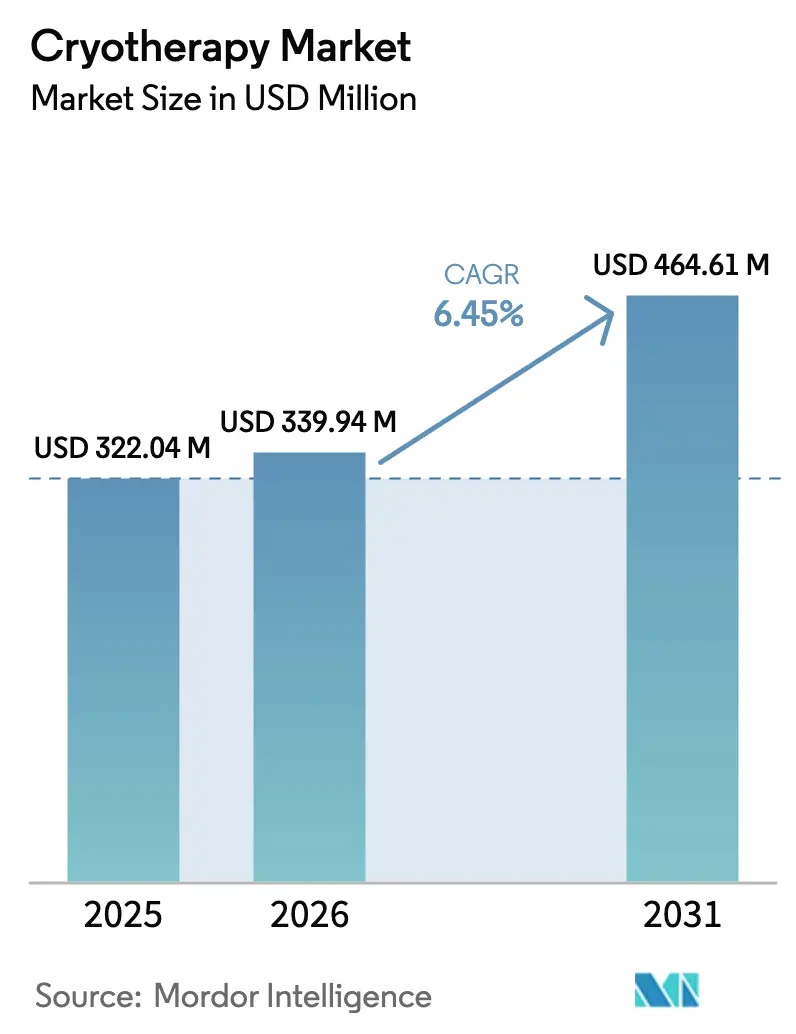

| Market Size (2026) | USD 339.94 Million |

| Market Size (2031) | USD 464.61 Million |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

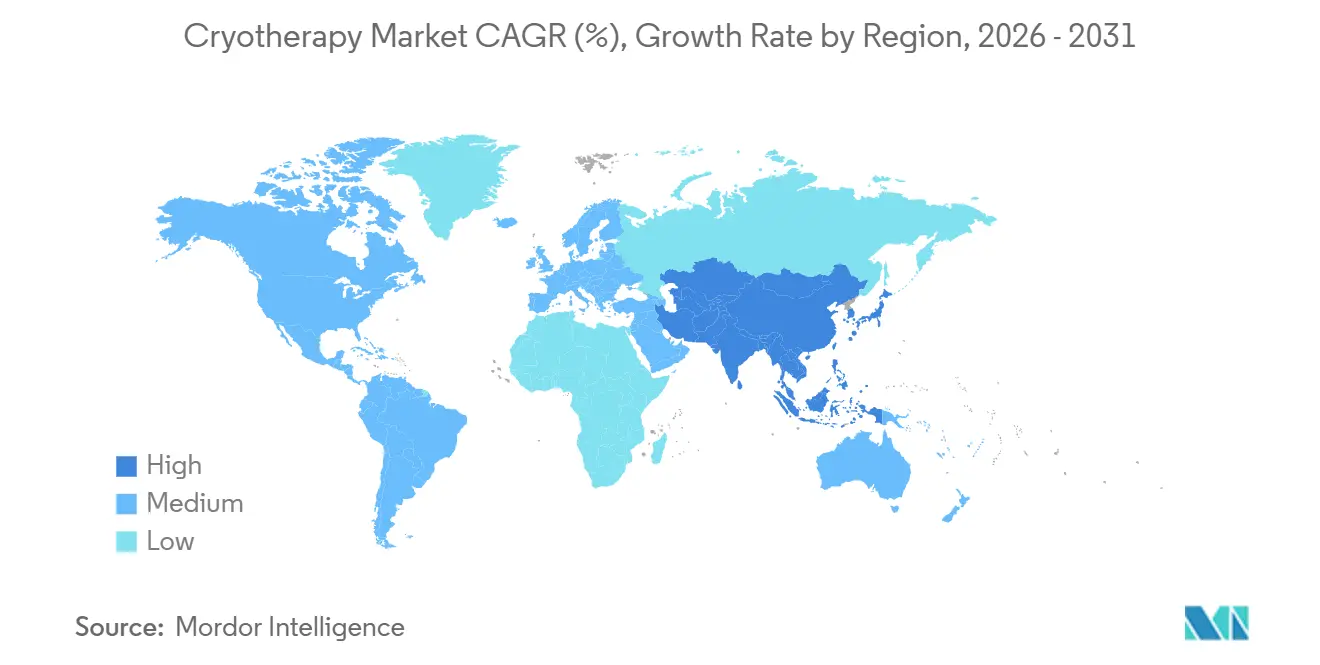

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cryotherapy Market Analysis by Mordor Intelligence

The Cryotherapy Market size is expected to increase from USD 322.04 million in 2025 to USD 339.94 million in 2026 and reach USD 464.61 million by 2031, growing at a CAGR of 6.45% over 2026-2031.

Accelerated replacement of liquid-nitrogen chambers with fully electric systems has started to re-shape cost structures, because clinics shed recurring gas deliveries and ventilation retrofits.[1]CryoBuilt Team, “Polaris Electric Chamber Cuts Five-Year Cost 60%,” CryoBuilt, cryobuilt.com Fitness-club installations, mobile rental fleets, and home devices are widening access beyond sports-medicine clinics, creating fresh demand for consumable-light hardware and software subscriptions. Oncology and pain-management reimbursements in North America provide a medical pathway for localized cryoablation, while aesthetics-oriented spot-cooling devices flourish in cash-pay channels.[2]American Medical Association, “CPT 64624 for Cryoneurolysis,” AMA, ama-assn.org Competitive dynamics emphasize AI-enabled temperature control and throughput optimization rather than ever-lower chamber temperatures, signaling a pivot toward data-rich user experiences.

Key Report Takeaways

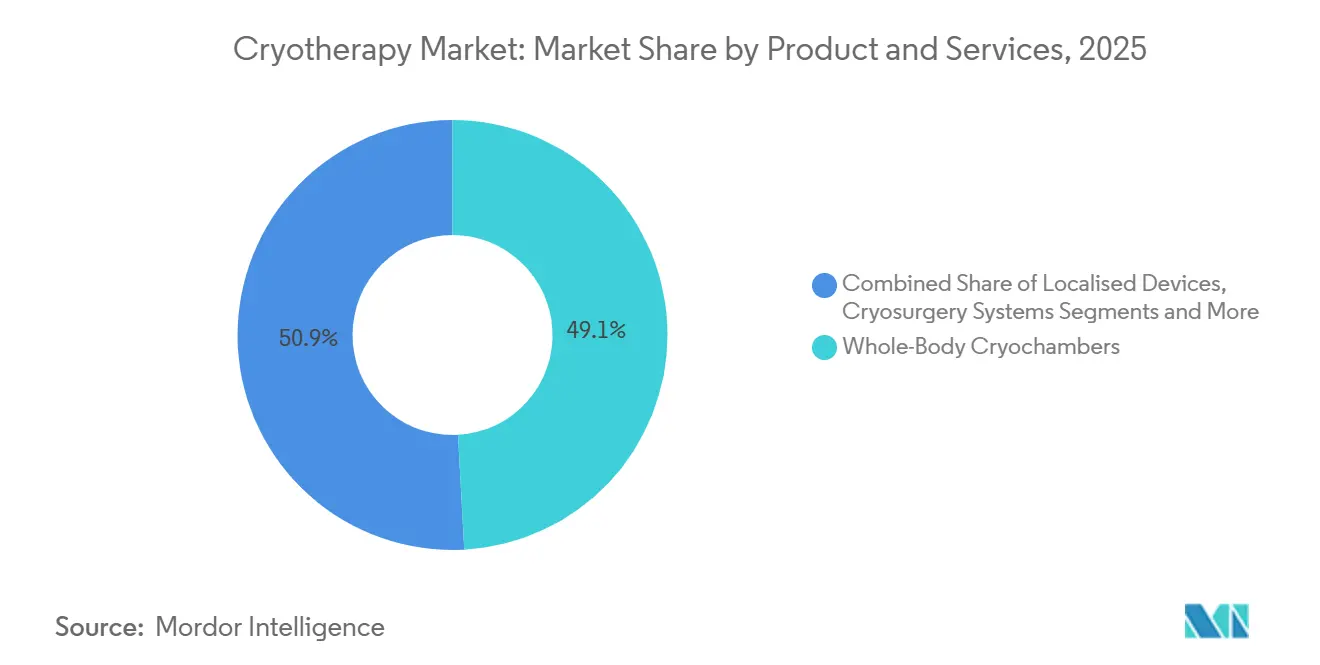

- By product and services, whole-body cryochambers led with 49.13% revenue share in 2025; hybrid and mobile units are projected to post the fastest 10.63% CAGR to 2031.

- By application, sports recovery accounted for 33.45% share in 2025, while dermatology and aesthetics is forecast to expand at a 9.24% CAGR through 2031.

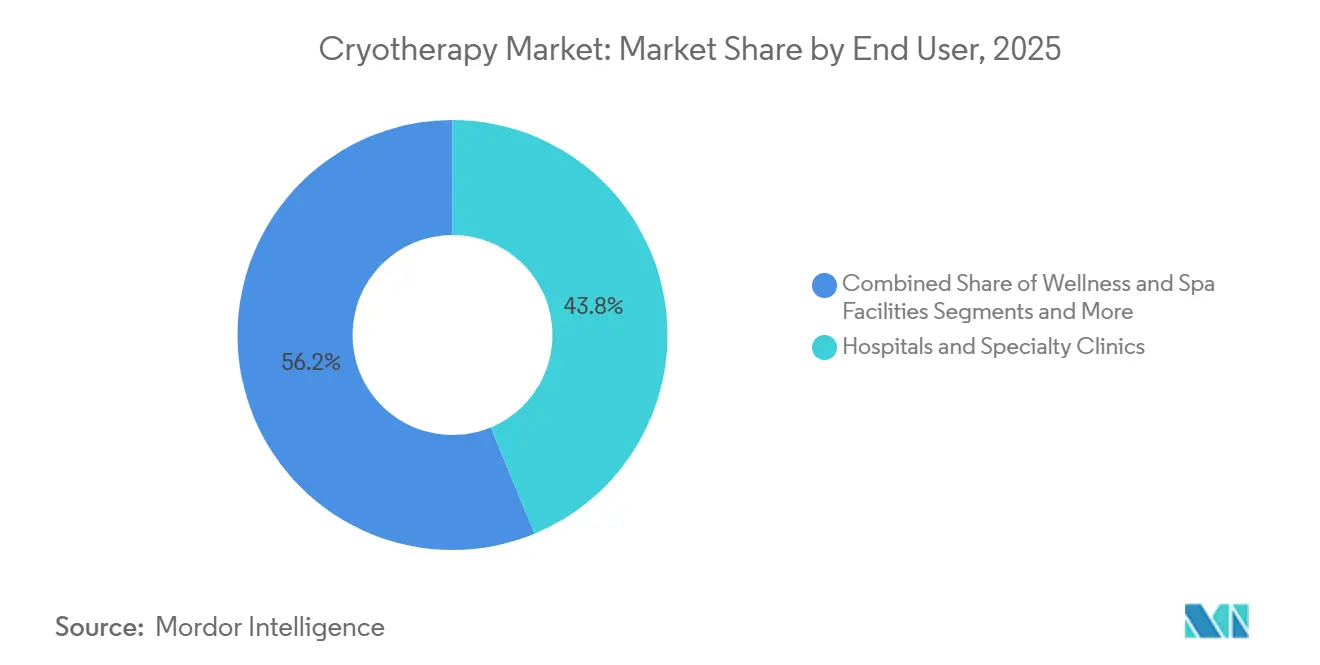

- By end user, hospitals and specialty clinics held 43.76% spending share in 2025; home-use and direct-to-consumer devices are expected to grow at a 10.53% CAGR over 2026-2031.

- By technology, liquid-nitrogen systems commanded 56.84% revenue share in 2025, whereas fully electric platforms are poised for the highest 8.23% CAGR to 2031.

- By geography, North America dominated with 37.83% revenue share in 2025; Asia-Pacific is anticipated to register the quickest 7.74% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Cryotherapy Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Shift from Liquid Nitrogen to Fully-Electric Cryo-Systems Cut Costs | 1.2% | Global, with early adoption in EU and North America | Medium term (2-4 years) |

| Reimbursement Expansion in Key Regions | 0.9% | North America, select EU markets | Long term (≥ 4 years) |

| Increased Cryo Access in Fitness Clubs | 0.8% | North America, Asia-Pacific urban centers | Short term (≤ 2 years) |

| AI-Driven Chambers Enhance Throughput | 0.6% | Global, concentrated in premium clinics | Medium term (2-4 years) |

| Rental Market Growth with Mobile Cryo-Vans | 0.7% | North America, Western Europe | Short term (≤ 2 years) |

| Fat-Reduction Demand Spurs Cryo Adoption | 1.0% | Global, strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift From Liquid-Nitrogen to Fully-Electric Cryo-Systems Cut Costs

Clinics switching to electric chambers remove weekly dewar deliveries, lower insurance premiums linked to pressurized-gas storage, and meet net-zero mandates in the European Union and California. CryoBuilt’s Polaris electric chamber demonstrated a 60% reduction in five-year operating cost compared with nitrogen models. The transition accelerates in regions with unstable gas logistics, enabling new operators in Southeast Asia and Latin America to enter the cryotherapy market without specialized supply chains. Facility managers also favor electric units because they bypass OSHA oxygen-monitor requirements. Collectively, these shifts add 1.2 percentage points to forecast CAGR by broadening the serviceable venue base and raising replacement demand.

Reimbursement Expansion in Key Regions

The American Medical Association introduced CPT 64624 in 2024, legitimizing cryoneurolysis billing and prompting capital purchases in pain clinics. Germany’s insurers began reimbursing whole-body cryotherapy for rheumatoid arthritis under pilot programs in 2025, signaling a European precedent. Although the U.S. Centers for Medicare & Medicaid Services still classifies whole-body cryo as investigational,[3]Centers for Medicare & Medicaid Services, “Coverage Determination for Whole-Body Cryotherapy (E0218),” CMS, cms.gov partial reimbursement steers investment toward localized medical devices that enjoy procedural fees. Over the long term, consistent payer recognition could inject nearly 1 percentage point into the global CAGR, especially if more Payors align on chronic-pain indications.

Increased Cryo Access in Fitness Clubs

Premium gym chains add three-minute cryo sessions to memberships to lock in higher monthly fees and drive secondary spending on recovery services. Equinox installed cryochambers in 12 U.S. clubs during 2025, bundling unlimited sessions into USD 300 packages that reach wellness-oriented consumers who previously avoided stand-alone clinics. Similar rollouts in Seoul and Tokyo expand exposure among office workers. The club route normalizes cryotherapy as routine recovery rather than specialized therapy, lifting session volumes and supporting a +0.8% impact on CAGR through new user acquisition.

AI-Driven Chambers Enhance Throughput

MECOTEC’s CryoStar system senses skin temperature and dynamically modulates cooling intensity, reducing cycle variance by 40% while doubling hourly client capacity. Automated logs ease ISO 9001 audits, strengthening hospital adoption. Although AI chambers carry premium price tags now, component costs fall as edge-AI chips commoditize. Higher throughput boosts revenue per square foot, incentivizing chain operators to upgrade and nudging CAGR upward by 0.6%.

Restraints Impact Analysis of Cryotherapy Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Gas Prices Increase Risks | -0.8% | Europe, Asia-Pacific regions dependent on LNG imports | Short term (≤ 2 years) |

| Insurer Pushback Due to Lack of Standards Benchmarking Study | -0.6% | North America, select EU markets | Long term (≥ 4 years) |

| Tariffs Impact Mobile Chamber Costs | -0.5% | North America, import-dependent markets | Medium term (2-4 years) |

| High Costs Limit Adoption in Small Clinics | -0.7% | Global, most acute in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Gas Prices Increase Risks

European nitrogen spot prices spiked above EUR 50 per MWh in late 2025, eroding margins at high-volume sports clinics and prompting deferred purchases of nitrogen-fed systems. Operators recalculated break-even analyses, delaying replacement cycles until electric alternatives become affordable. Similar volatility in Asia-Pacific LNG markets compresses budgets in Japan and South Korea. These conditions shave 0.8 percentage points off short-term growth.

Insurer Pushback Due to Lack of Standards Benchmarking Study

The American Academy of Physical Medicine and Rehabilitation highlighted wide variation in session protocols, complicating insurer evaluation. Absent consensus guidelines, Payors label whole-body cryotherapy experimental. The uncertainty forces clinics into cash-pay models, limiting volume in price-sensitive populations and dragging CAGR by 0.6 points over the long run.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Cryotherapy Market Segment Analysis

By Product and Services:

Hybrid Units Gain as Rental Fleets ExpandWhole-body cryochambers generated almost half of 2025 revenue, yet hybrid and mobile units will outpace at a 10.63% CAGR as rental operators send trailer-mounted systems to events and corporate campuses. The shift diversifies the cryotherapy market because customers with no capital budget can still provision sessions on demand.

Consumables revenue shrinks as the sector turns electric, but software subscriptions grow when operators use cloud dashboards to schedule sessions, track utilization, and document safety compliance. Localized devices hold roughly 18% share, driven by dermatology uptake for aesthetic spot treatments. Cryosurgery systems, vested mainly in oncology, maintain steady adoption inside interventional radiology suites. Accessories, including nitrogen dewars and thermal gloves, taper in lock-step with the electric transition, so vendors hedge by bundling maintenance contracts and analytics platforms. The evolving mix means chamber form-factors, not temperatures, define competitive advantage, intensifying a platform race across the cryotherapy market.

By Application:

Aesthetics Outpace Traditional RecoverySports recovery retained 33.45% of the cryotherapy market size in 2025 thanks to elite teams and collegiate programs. Dermatology and aesthetics, however, add sessions faster, climbing 9.24% annually through 2031 on social-media visibility and financing plans.

Pain-management clinics deploy cryoneurolysis probes under CPT 64624, but reimbursement gaps cap statewide rollouts. Oncology usage broadens as imaging-guided cryoablation lowers collateral tissue damage, supporting steady unit placements inside tertiary hospitals. Wellness and weight-management kiosks remain fragmented yet visible in luxury resorts that position cryo as a metabolism booster. The application landscape shows recovery saturation in professional sports, so operators court amateur athletes, beauty seekers, and chronic-pain patients to enlarge the cryotherapy market.

By End User:

Home Devices Disrupt Clinic ModelsHospitals and specialty clinics controlled 43.76% of 2025 spending, underpinned by reimbursable cryoneurolysis and oncology cases. Home-use devices, positioned below USD 5,000, clock a double-digit CAGR as affluent consumers bypass per-visit fees.

Sports and fitness centers fold cryo into premium memberships, softening churn in saturated metropolitan gyms. Destination wellness resorts curate multi-day detox packages featuring cold exposure, mindfulness, and IV therapy. The democratization of hardware forces clinics to differentiate through guided protocols, biometric dashboards, and integration with electronic health records, adding data resonance to the cryotherapy market share calculus.

By Technology:

Electric Systems Erode Nitrogen’s LeadLiquid-nitrogen systems preserved 56.84% revenue share in 2025 but face attrition as electric chambers mature. Electric units save USD 800-1,200 monthly in gas and skip OSHA ventilation mandates, raising the cryotherapy market size addressable to urban boutique studios.

Practitioners preferring sub-140 °C levels will cling to nitrogen systems in research and elite performance labs. CO₂ spot devices stay niche yet vital in dermatology because they require minimal room prep and cost only USD 2,000-5,000. Regulatory nudges like Germany’s Blue Angel eco-label and California’s Title 24 energy code incentivize electric adoption, plotting a measured but inexorable shift inside the cryotherapy market.

Geography Analysis

North America Cryotherapy Market

North America generated 37.83% of global revenue in 2025, with the United States comprising 85% of that figure on the back of pro-sports demand and early medical reimbursement. Canada and Mexico remain smaller but stable, supporting cash-pay models in Toronto, Vancouver, Monterrey, and Mexico City. FDA clearance of IceCure’s ProSense system for benign breast tumors signals regulatory momentum for minimally invasive cryoablation.

APAC Cryotherapy Market

Asia-Pacific will expand the cryotherapy market at 7.74% through 2031 as China’s domestic builders undercut European imports by 30-40%. Japan rides aging-population demand for non-pharmacological pain relief despite absent reimbursement. India’s cricket academies and private hospitals in Mumbai and Bangalore buy chambers to serve professional and affluent amateur athletes. South Korea gravitates toward aesthetics in Seoul’s Gangnam district, while Australia focuses on sports recovery in Sydney and Melbourne. Fragmented rules and cultural preferences for traditional remedies slow uptake, but growing middle-class income and sports participation widen the user base.

EMEA and South America Cryotherapy Market

In Europe, Germany led, aided by statutory insurers piloting cryo coverage for rheumatoid arthritis. France’s thalassotherapy spas and the United Kingdom’s Premier League clinics maintain robust demand. Italy and Spain add aesthetic and sports-rehab users respectively. Middle East and Africa collectively held about 6% share, dominated by UAE and Saudi Arabia luxury wellness centers. South America’s 5% share is concentrated in Brazil and Argentina, where private hospitals equip orthopedic wards. Together, these regional profiles underline differing adoption curves yet a converging preference for electric, data-rich hardware across the cryotherapy market.

Regulatory Landscape

Regulation continues to split between medical-grade cryosurgery/cryoablation and wellness-oriented whole-body systems, with claims and intended use shaping classification and evidence expectations. In the United States, cryosurgical units are regulated as Class II devices under 21 CFR 878.4350 and commonly use the FDA 510(k) pathway. Late-2025 clearances such as K250742 (focused cryotherapy system) and K253000 (OTC CryoFreeze wart and skin tag remover) reinforce ongoing labeling, safety, and substantial-equivalence requirements for both professional and consumer-facing devices.

In Europe, cryotherapy devices marketed for medical purposes fall under EU MDR 2017/745, often classified as Class IIa or IIb depending on risk and intended use. This framework requires conformity with Annex I GSPR and structured technical documentation. Canada remains comparatively restrictive for higher-risk applications, with Health Canada generally treating cryotherapy instruments as Class III devices that require a medical device license for sale or import. Across regions, quality and risk frameworks (ISO 13485 and ISO 14971), along with industrial gas safety guidance from bodies such as EIGA for cryogen-based systems, influence compliance workflows and operator training expectations.

Value Chain Analysis

The value chain runs from component suppliers (cryogen handling hardware, precision valves, sensors, compressors, and control electronics) to OEM manufacturing and system integration (whole-body chambers, localized devices, and cryosurgery platforms), followed by regulatory clearance and quality compliance and then multi-channel distribution. Hospitals and specialty clinics typically buy through capital-equipment procurement and GPO-style channels, while wellness and aesthetics offerings expand via specialty distributors, franchise networks, and direct-to-consumer routes that bundle software, maintenance, and operator training.

Recent moves point to a more channel-controlled go-to-market approach. CryoBuilt's July 2025 equity investment in ChillyBox and its exclusive distribution rights for at-home cryotherapy technology indicate tighter control of downstream residential routes. BENEV's March 2026 partnership with LaserAway to launch XTherma (RF plus cryogen combination therapy) also reflects modality-stacking in aesthetics and reliance on large clinic networks for scale. On the clinical side, FDA marketing authorization functions as a gating step for expansion, as shown by IceCure Medical reporting increased U.S. commercial installations for its ProSense platform following its October 2025 authorization. The accompanying 2026 sales momentum disclosures further emphasize how service coverage, consumables/probes, and installed-base support underpin recurring revenue capture.

Competitive Landscape

The cryotherapy market is moderately concentrated. Market leaders pursue vertical integration, as Boston Scientific absorbs probe suppliers for oncology ablation. Medtronic’s cryoablation line added USD 180 million to FY 2025 sales, leveraging hospital relationships and procedure-based billing.

Challengers focus on electric systems that eliminate nitrogen logistics. CryoBuilt and JUKA emphasize sustainability messaging to court eco-certified facilities. Patent trends steer toward AI-controlled temperature algorithms and modular chambers that switch between whole-body and localized modes. Home-use devices below USD 5,000 remain a white-space where incumbents have limited presence. Mobile fleet operators cultivate niche revenue at sporting events and corporate wellness activations, reinforcing a service-led layer within the cryotherapy industry.

Technology differentiation now centers on user-experience features—biometric tracking, smartphone connectivity, and EHR export—rather than ever-colder temperatures. Hospitals demand ISO-compliant logs, whereas consumer segments want gamified recovery metrics. Regulatory divergence sustains two strategic tracks: medical-grade devices chase FDA or CE approval, and wellness brands exploit cash-pay channels aided by influencer marketing. Consolidation pressure likely rises in the medical segment as compliance burdens escalate, but low barriers keep the wellness side fragmented, preserving competitive diversity inside the cryotherapy market.

Cryotherapy Industry Leaders

Zimmer MedizinSysteme GmbH

MECOTEC GmbH

Cryomed s.r.o

Impact Cryotherapy Inc.

CRYO Science

- *Disclaimer: Major Players sorted in no particular order

Cryotherapy Market Companies Covered in this Report

- Art of Cryo

- Boston Scientific

- Brymill Cryogenic Systems

- The Cooper Companies

- Cryo Innovations

- CRYO Science

- CryoAction

- CryoBuilt Inc.

- Cryomed s.r.o.

- CRYONiQ

- Grand Cryo

- IceCure Medical

- Impact Cryotherapy Inc.

- JUKA

- KRION

- MECOTEC GmbH

- Medtronic plc (Cryoablation)

- Metrum CryoFlex

- Vacuactivus

- Zimmer MedizinSysteme

Market Opportunities and Future Outlook

White-space is widening across regulated clinical indications and in consumer-grade, consumable-light devices where safety monitoring and defensible claims help differentiate offerings. A 2026 cadence of device clearances and certifications creates more visible expansion pathways: FDA 510(k) activity around cryoablation and cryotherapy applicators, including K260377 for IceCure's XSense cryoablation system and K251928 for Medinice's CoolCryo cryoapplicator, supports broader adoption of minimally invasive cryo workflows. In Europe, CE marking under EU MDR for Erbe Elektromedizin's ERBOKRYO 2 (April 2026) reinforces an expanding addressable installed base for medical cryosurgical platforms.

Opportunities also cluster around integrated platforms that combine hardware with data capture, standardized protocols, and multi-modality treatment. MECOTEC's Cryo Arctic 4.0 (April 2025) signals demand for biometric monitoring features that align with safety expectations, and the shift from liquid nitrogen toward fully electric chambers aligns with operator efforts to reduce gas logistics, ventilation retrofits, and liability exposure. In breast and other focal oncology applications, clinical adoption has shown commercial signals, such as IceCure reporting growth in its active U.S. commercial install base after FDA authorization. This supports a pathway for vendors that pair procedural evidence generation with scalable service and training networks.

Recent Industry Developments in Cryotherapy Market

- June 2026: IceCure Medical reported a 70% increase in its active U.S. commercial install base for the ProSense system following its FDA marketing authorization. The update underscores how regulatory clearance translates into faster site activation and service footprint expansion in hospital and clinic channels.

- November 2025: CryoTherapeutics partnered with SpectraWAVE and the Cardiovascular Research Foundation on the ICECAP clinical study for coronary plaque treatment. The collaboration strengthens clinical-evidence generation around intravascular cryotherapy concepts, supporting longer-cycle adoption in cardiology settings.

- September 2024: MECOTEC GmbH completed the acquisition of Polish cryo-chamber manufacturer Zimno Tech Sp. z o.o. from Restore Hyper Wellness and established an exclusive partnership connected to Restore's U.S. network. The deal expanded MECOTEC's manufacturing and service capacity and tightened access to a large wellness chain deployment channel for electric whole-body chambers.

Cryotherapy Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers revenue generated from cryotherapy solutions used to expose the body or a targeted area to very low temperatures for therapy, recovery, wellness, and clinical procedures. It includes equipment, related consumables, and service income where it is part of the delivered cryotherapy offering.

Scope exclusions: We exclude general cold packs and basic ice therapy that do not rely on purpose-built cryotherapy devices or controlled cryogenic systems.

Segments Covered in This Report

- By Product and Services

- Whole-Body Cryochambers

- Localised Devices

- Cryosurgery Systems

- Hybrid / Mobile Units

- Accessories and Conusmables

- Software and Services

- By Application

- Sports Recovery

- Pain Management

- Oncology (Cryo-ablation)

- Dermatology & Aesthetics

- Wellness & Weight-Management

- By End User

- Hospitals & Specialty Clinics

- Sports & Fitness Centers

- Wellness & Spa Facilities

- Home-Use / Direct-to-Consumer

- By Technology

- Liquid-Nitrogen Systems

- Fully-Electric Systems

- CO₂ Spot-Therapy Devices

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping where demand shows up, then tying it back to measurable signals. We typically use public health and regulatory references such as the US FDA database and clinical guidance portals, followed by peer reviewed medical journals to track adoption patterns across pain management, dermatology, and oncology use cases.

To ground the market in real activity, supporting data is pulled from sources such as the US Bureau of Labor Statistics for service footprint signals, UN Comtrade style customs statistics for equipment trade direction, and association or conference publications that describe practice trends and safety notes. Company filings, investor presentations, and trusted press coverage are used to understand product launches and channel expansion, and then a paid subscription for company financials plus a patent database is used selectively to validate scale and innovation intensity. These desk research sources are illustrative, and many other public references were also reviewed for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary inputs come from interviews and structured surveys across device suppliers, cryotherapy center operators, hospital and specialty clinic users, and distributors. We also speak with sports recovery and wellness decision-makers across key regions so pricing, utilization, and technology mix (liquid nitrogen versus electric systems) can be checked, and gaps from desk findings can be closed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 18% | APAC: 40% |

| Mid tier: 57% | Functional/Unit leaders: 27% | EMEA: 36% |

| Smaller Players: 18% | Managers: 55% | Americas: 24% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where procedure and service adoption is reconstructed by region using a practical demand pool, then converted into revenue using observed pricing and utilization ranges. Since cryotherapy is delivered through clinics, hospitals, and wellness centers, the model uses facility counts, estimated utilization per unit, and typical session pricing as core building blocks, with adjustments for technology mix and replacement cycles.

The totals are then corroborated using selective bottom-up approximations, such as sampling installed base indicators, checking supplier shipment direction where available, and validating average selling prices for major device classes and consumables. Key inputs that were used as model drivers include the mix of whole-body cryochambers versus localized devices, session volume per site, the share of clinical procedures versus wellness sessions, liquid nitrogen versus electric system uptake, and regional price bands in USD.

Forecasting is done using scenario analysis supported by light multivariate regression, where drivers like facility expansion rates, utilization normalization, and clinical adoption trends are varied within bounds experts considered plausible. Where bottom-up visibility is weaker (for example, smaller independent centers), assumptions are controlled through conservative utilization caps and rechecked with operator feedback before finalizing the run.

Data Validation & Update Cycle

Outputs are checked using multiple validation steps so the final number does not rely on a single assumption. We compare modeled revenue against independent signals such as estimated installed base direction, typical site throughput, and observed pricing ranges, then investigate variances when a country or application trend looks out of pattern.

Before sign-off, the work goes through an internal review where inputs, formulas, and country splits are re-tested, followed by targeted re-contact with interviewees if a key parameter shifts. Reports are refreshed annually, and interim updates are done when material events occur, such as a major regulatory change or a sharp shift in system pricing. Right before delivery, the analyst completes a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Cryotherapy Market Size Versus Other Published Estimates

Published cryotherapy market numbers often vary even when the topic is framed the same, and the table makes that spread easy to see. Differences usually come from what is counted as cryotherapy revenue, which year is treated as the base, and how fast pricing and utilization are assumed to move.

In this market, the biggest gap drivers are typically whether clinical cryosurgery systems and related service income are included alongside wellness-focused chambers, and whether home-use devices are treated as a meaningful revenue stream. Currency timing, treatment of consumables, and how utilization ramps are modeled also matter, especially when newer sites are assumed to run at mature occupancy too quickly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 339.94 M (2026) | |

| Global Consultancy A | USD 207.50 M (2024) | Uses an earlier base year and tends to center the scope on cryochambers and cryosaunas tied to wellness and spa settings, which can undercount clinical cryosurgery-related revenue and attached consumables. |

| Industry Publisher B | USD 376.80 M (2025) | Uses a different base year and a broader product framing that can lift totals if more consumables and system categories are counted without tightening utilization and pricing checks by end user. |

The table highlights year alignment and scope boundaries as the main reasons for the spread, and in Mordor Intelligence's model, cryotherapy is counted only when it is delivered through defined device-based systems across clinical and wellness settings, with utilization and price bands rechecked by region. With that structure, the final total stays traceable to facility footprint, technology mix, and realistic throughput assumptions, which makes it easier to reproduce and update.

Key Questions Answered in the Report

How fast will global cryotherapy revenues grow through 2031?

The cryotherapy market is forecast to expand at a 6.45% CAGR from 2026 to 2031, reaching USD 464.61 million.

Which technology is replacing liquid-nitrogen chambers?

Fully electric systems are growing at an 8.23% CAGR because they eliminate gas costs and meet sustainability mandates.

What segment holds the largest cryotherapy market share today?

Whole-body cryochambers led with 49.13% share in 2025.

Where is regional growth strongest after North America?

Asia-Pacific is projected to post a 7.74% CAGR through 2031, buoyed by lower-cost domestic manufacturers in China.

Are home cryotherapy devices economically viable for consumers?

Yes, devices priced below USD 5,000 can break even after 30-50 sessions compared with clinic fees.

What is the key reimbursement milestone for cryoneurolysis?

AMA CPT 64624, introduced in 2024, allows U.S. providers to bill Medicare and private insurers for peripheral-nerve cryoablation.

Page last updated on: