Adaptogens Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

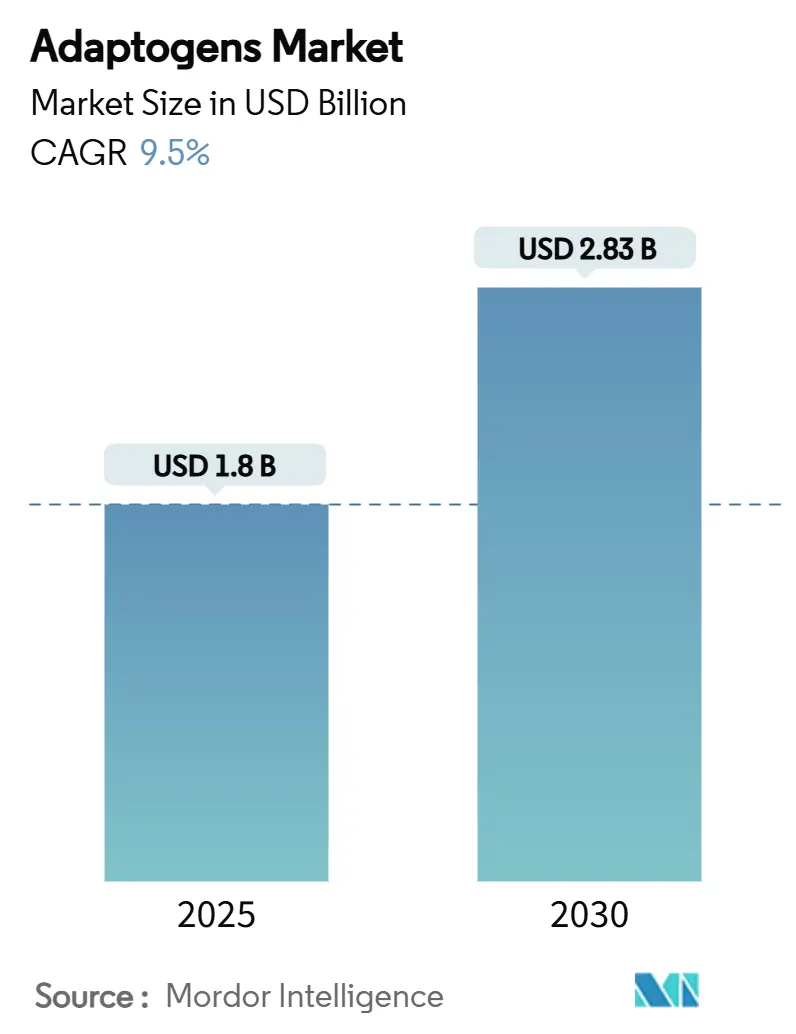

| Market Size (2025) | USD 1.8 Billion |

| Market Size (2030) | USD 2.83 Billion |

| Growth Rate (2025 - 2030) | 9.50% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Adaptogens Market Analysis by Mordor Intelligence

The adaptogens market size is currently valued at USD 1.80 billion and is projected to reach USD 2.83 billion by 2030, expanding at a 9.50% CAGR. This strong trajectory underscores how producers are pivoting toward natural stress-mitigation strategies as climate volatility, heat stress, and antibiotic restrictions collide. Regulatory curbs on antibiotic growth promoters alone have opened a USD 1.03 billion replacement gap, and the adaptogens market for animal nutrition is filling it by providing dual stress-reduction and immune-support benefits. Demand acceleration is most visible in Asia-Pacific aquaculture, Middle Eastern heat-management programs, and North American precision-nutrition platforms that verify feed-additive ROI through real-time biomarkers. Industry players are capitalizing on shifting consumer preferences, sustainable-production mandates, and cost-optimization pressures that position adaptogenic herbs and mushrooms as economically viable multifunctional additives.

Key Report Takeaways

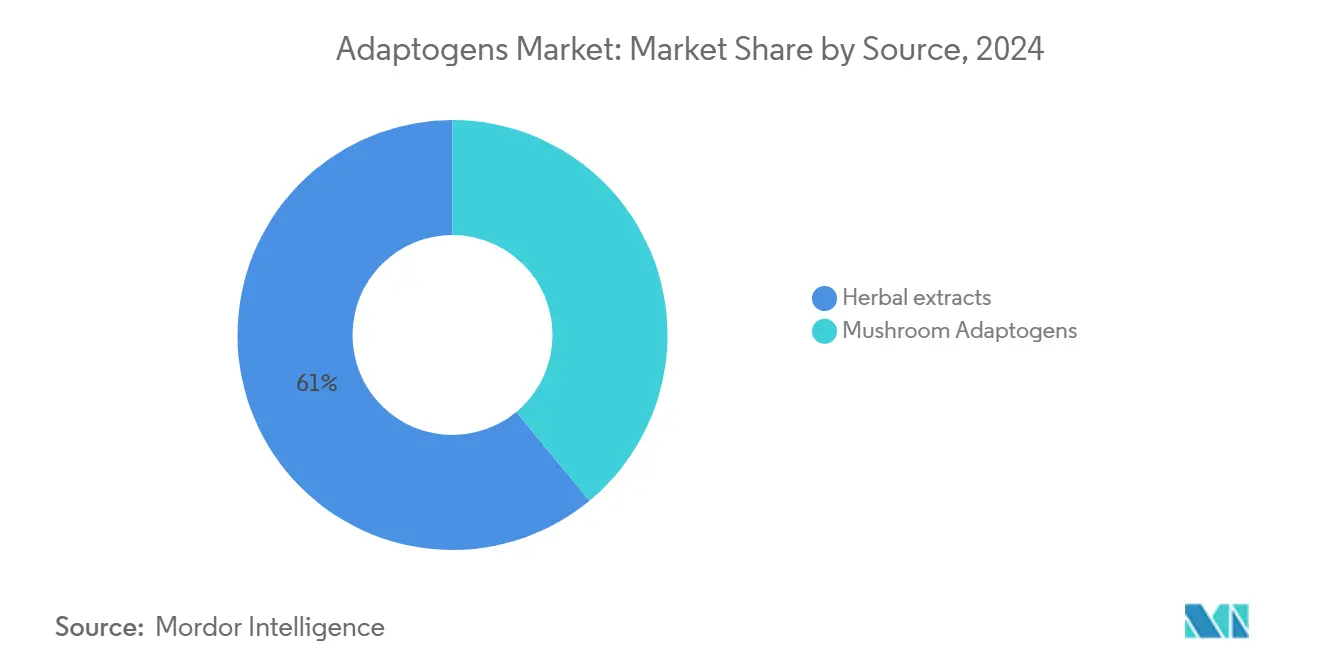

- By source, herbal adaptogens led with 61.0% revenue share in 2024, while mushroom extracts are advancing at an 11.8% CAGR through 2030.

- By livestock species, poultry accounted for 34.8% of the adaptogens market share in 2024, and aquaculture is forecast to expand at a 14.2% CAGR to 2030.

- By form, powders dominated with a 52.3% share of the adaptogens market size in 2024, yet liquids are set to grow at a 12.5% CAGR.

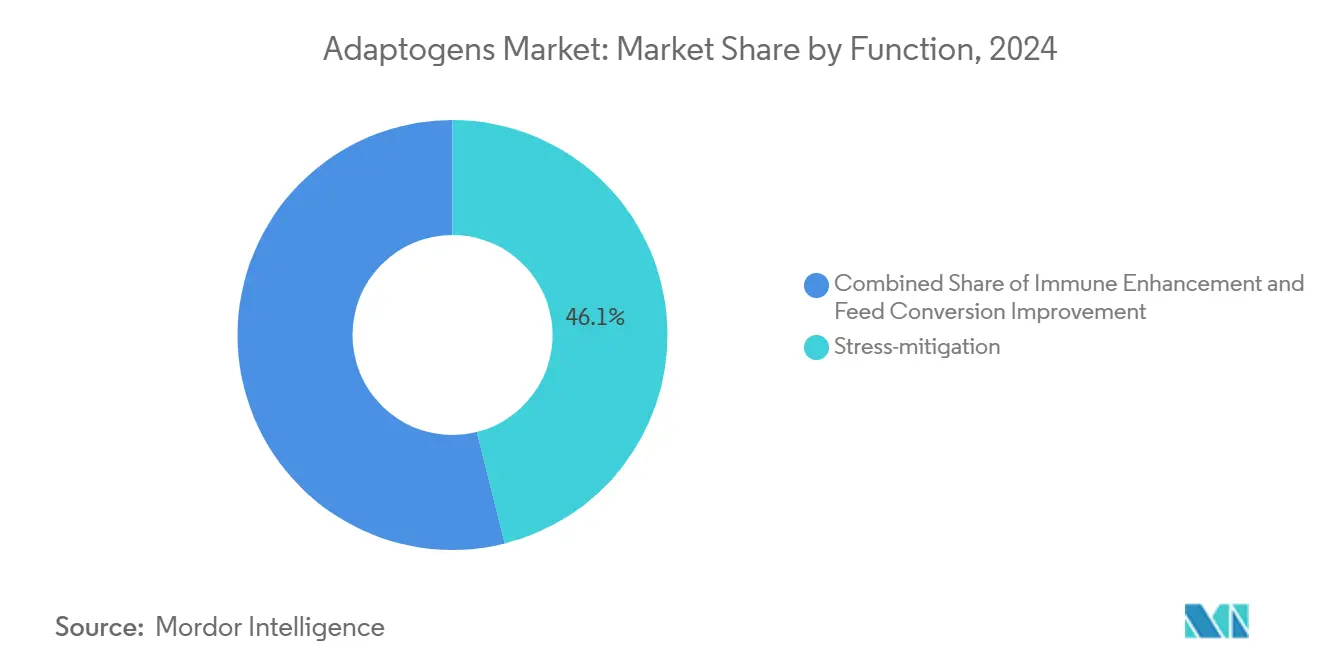

- By function, stress-mitigation additives held 46.1% of the adaptogens market size in 2024, and immune-enhancement applications will rise at a 13.6% CAGR.

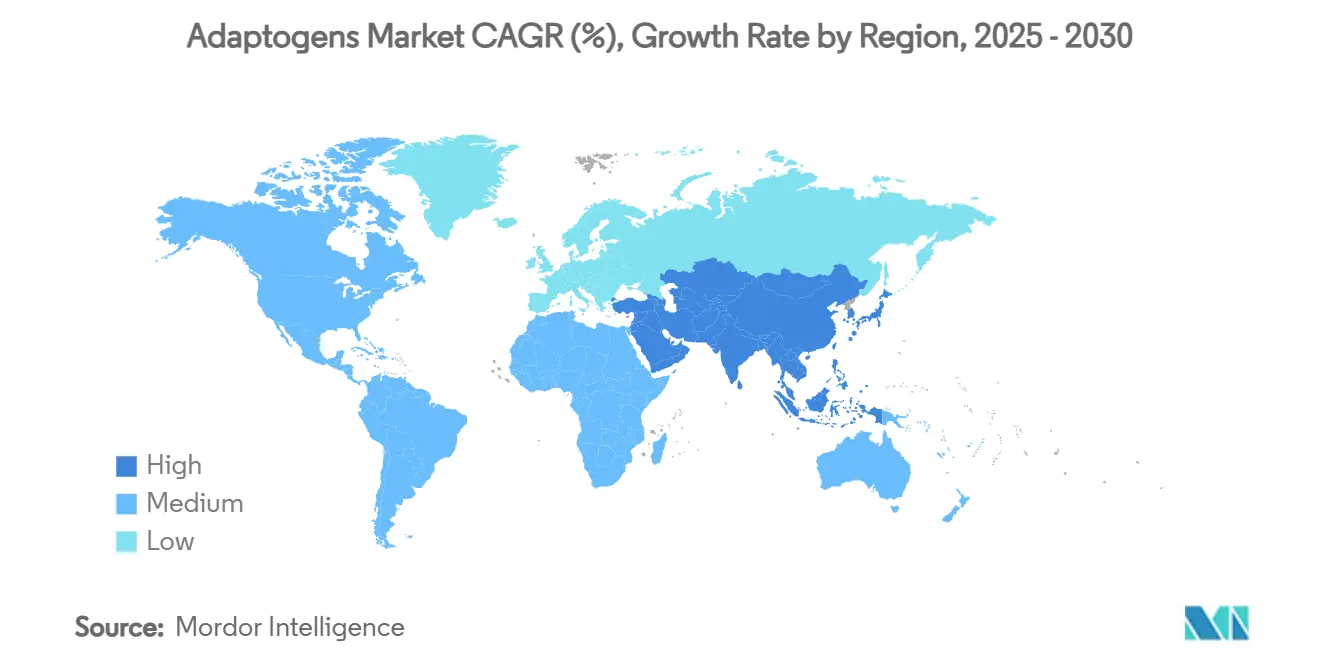

- By geography, Asia-Pacific was the largest contributor with 35.4% in 2024, whereas the Middle East will register the fastest 10.9% CAGR through 2030.

- DSM-Firmenich, Cargill, Delacon, Anpario, and Novus International together commanded 45.0% market share in 2024.

Global Adaptogens Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising ban on antibiotic growth promoters in feed | +2.1% | Europe and North America | Medium term (2 – 4 years) |

| Mainstream demand for natural stress-mitigation additives | +1.8% | Asia-Pacific and North America | Short term (≤ 2 years) |

| Inflation-triggered feed-cost optimization using adaptogenic herbs | +1.2% | Emerging markets | Short term (≤ 2 years) |

| Integration of adaptogenic mycobiotics in aquafeed | +1.0% | Asia-Pacific and South America | Medium term (2 – 4 years) |

| Heat-stress episodes linked to climate change | +1.6% | Middle East and North Africa | Long term (≥ 4 years) |

| Emergence of precision-nutrition platforms validating adaptogen ROI | +0.8% | North America and the EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Ban on Antibiotic Growth Promoters in Feed

The European Union’s full phase-out of antibiotic growth promoters by 2024 and stricter FDA Veterinary Feed Directive rules in the United States have compelled producers to find botanical alternatives that offer equivalent performance without pharmacological oversight[1]Source: U.S. Food and Drug Administration, “Guidance for Industry 302,” fda.gov. Adaptogens help regulate stress hormones and improve metabolic efficiency, giving the adaptogens market for animal nutrition a premium credential as the principal beneficiary of the USD 15 billion antibiotic-replacement segment. Asian regulators are mirroring these policies, turning adaptogens into a default feed formulation option.

Mainstream Demand for Natural Stress-Mitigation Additives

Feed integrators are shifting from symptomatic relief to root-cause stress management because heat, handling, and transport losses cost livestock producers USD 3.5 billion each year. Trials show 8 – 12% feed-conversion gains when Scutellaria-based blends are added, validating the adaptogens market for animal nutrition as a proactive welfare tool. Precision-feeding systems now auto-adjust botanical dosing to real-time stress indicators, raising both adoption and confidence levels.

Inflation-Triggered Feed-Cost Optimization Using Adaptogenic Herbs

Commodity inflation of 15 – 20% has spurred feed formulators to adopt multifunctional botanicals that can replace several single-purpose additives. Ashwagandha and ginseng extracts deliver stress control, immune support, and feed-conversion benefits within one inclusion, lowering overall formulation costs by up to 30% versus synthetic blends. This economic edge is magnified in emerging markets where currency devaluation makes imported additives more expensive, enhancing the relevance of the adaptogens market for animal nutrition.

Heat-Stress Episodes Linked to Climate Change

Heat events now occur 40% more often, and livestock housed above their thermal comfort zone lose output worth USD 2.4 billion a year. Dietary betaine and similar adaptogens adjust lipid metabolism and insulin signaling, enabling animals to sustain productivity during extreme temperatures. The Middle East’s 10.9% CAGR confirms that the adaptogens market for animal nutrition is becoming a core climate-resilience measure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory ambiguity on botanical claims | -1.4% | Europe and North America | Medium term (2 – 4 years) |

| Volatile sourcing of wild-crafted herbs | -1.1% | Asia-Pacific and emerging markets | Short term (≤ 2 years) |

| Limited species-specific efficacy data | -0.8% | Developed markets | Long term (≥ 4 years) |

| Risk of mycotoxin co-contamination in mushroom adaptogens | -0.6% | Asia-Pacific | Medium term (2 – 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Ambiguity on Botanical Claims

The absence of harmonized definitions for botanical feed additives forces companies to submit separate safety dossiers, residue studies, and label texts in every major market, driving registration costs above USD 2 million per stock keeping unit[2]Source: EFSA Panel on Feed Additives, “Guidance on the Assessment of Botanicals,” EFSA Journal, efsa.europa.eu. European Food Safety Authority (EFSA) assessments routinely exceed 24 months, while the United States Food and Drug Administration requires a full Food Additive Petition that adds comparable delays and toxicology requirements. These duplicated demands deter smaller innovators, slow product launches, and redirect R&D toward regions with lighter oversight.

Limited Species-Specific Efficacy Data

Roughly 70% of peer-reviewed adaptogen trials still focus on broilers and grow-finish pigs, leaving major gaps for dairy cattle, shrimp, and carp segments where adoption potential is highest. Without robust dose-response curves, interaction studies, or withdrawal data, regulators classify many botanicals as non-functional “flavoring compounds,” limiting on-label efficacy claims and discouraging veterinarians from recommending widespread use[3]Source: United States Department of Agriculture, “Feed Additive Efficacy Claim Guidelines 2024,” USDA, usda.gov. This evidence vacuum slows uptake even though preliminary field trials point to promising immune-modulation gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Herbal Dominance Faces Mushroom Innovation

Herbal extracts retained a 61.0% share of the adaptogens market for animal nutrition in 2024, led by ashwagandha and ginseng. Mushroom extracts are advancing at an 11.8% CAGR through 2030, as aquaculture proves their pathogen-resistance value. Mushrooms’ beta-glucans and cordycepin deliver unique immune benefits that herbs cannot match, helping this niche outgrow the broader adaptogens market for animal nutrition.

Technological gains in spawn cultivation and solvent-free extraction are driving down costs and improving consistency. Survival rates in tilapia improved 16% when mushroom beta-glucan mixes were dosed at 0.2% feed inclusion. Such performance lifts justify premium pricing and are widening the customer base.

By Form: Liquid Innovation Drives Processing Evolution

Powders dominated at 52.3% in 2024 because they fit current mash and pellet workflows within the adaptogens market for animal nutrition. Liquids, however, are rising at a 12.5% CAGR because they offer two- to three-fold higher bioavailability and integrate with automated dosing pumps.

Advanced stabilization extends shelf life beyond 18 months, helping liquids penetrate aquaculture via in-water delivery systems. Encapsulated beadlets cater to pelleting temperatures above 80 °C by releasing actives post-pelletization, preserving efficacy.

By Livestock Species: Aquaculture Emerges as Growth Engine

Poultry commanded a 34.8% share in 2024 as producers fight heat stress and subclinical diseases. Aquaculture is scaling at a 14.2% CAGR, making it the fastest-growing slice of the adaptogens market for animal nutrition.

Ruminants hold a significant share as dairy herds use botanicals for metabolic stress, followed by swine with solid uptake through precision-feeding systems. Companion-animal formulations have a limited share, however, are expanding at a higher CAGR as premium pet-food brands leverage adaptogens to address stress-related issues.

By Function: Immune Enhancement Accelerates Beyond Stress Management

Stress-mitigation still leads at 46.1% of the adaptogens market for animal nutrition. Yet, immune-enhancement roles are gaining at a 13.6% CAGR because mushroom beta-glucans elevate lysozyme and complement activity, improving pathogen defense.

Feed-conversion improvement applications cover the majority share, fueled by margin pressure. Precision-nutrition dashboards now let producers monitor immune biomarkers and adjust inclusion rates, providing granularity that speeds the shift from generic stress relief to targeted immune modulation.

Geography Analysis

The Asia-Pacific region held the largest share of the adaptogens market for animal nutrition in 2024, accounting for 35.4% of the market. China’s policy backing for botanical feed additives and India’s dairy and poultry expansion keep regional demand high. Government-funded programs incorporate mushroom beta-glucans into carp and shrimp diets to reduce antibiotic dependence.

North America’s market is growing at an significant CAGR, driven by precision nutrition platforms and increasing consumer demand for antibiotic-free meat. DSM-Firmenich’s Verax system quantifies stress biomarkers in commercial broilers, verifying adaptive-herb ROI and driving adoption. The United States, in particular, values adaptogens for mitigating heat stress in southern agricultural production areas.

Europe advances as EFSA’s stringent vetting raises costs but also builds consumer trust in botanical safety, encouraging premium pricing. Germany’s on-farm trials use automated feeding stations to adjust ashwagandha dosing based on environmental temperature shifts. Eastern Europe is catching up as integrators modernize barns and feed mills. The Middle East, however, is the stand-out growth region at 10.9% CAGR, driven by year-round heat burdens on poultry and dairy herds that make adaptogens indispensable to animal welfare programs.

Competitive Landscape

The adaptogens market for animal nutrition is moderately consolidated. The top five players hold 45.0% of the market share, with companies including DSM-Firmenich AG leading through its Delacon Biostrong Protect line and Verax biomarker analytics. Cargill Incorporated follows with Proviox StressGuard formulations integrated into its global premix network.

Strategically, players pursue vertical integration to lock in botanical supply and de-risk quality. Novus International’s USD 15 million microbiome partnership with Resilient Biotics aims to create precision swine products, while Cargill’s tie-up with ENOUGH scales zero-waste mycoprotein that can complement adaptogenic feed programs. Patent race activity centers on mushroom-extraction processes and fermentation-derived adaptogens.

Niche innovators such as Anpario and Hubbard Feeds compete by local botanical sourcing and species-specific blends. Regional premix blenders in India, Brazil, and Vietnam fragment share further because they combine indigenous herbs with localized technical support, eroding the dominance of multinationals.

Adaptogens Industry Leaders

DSM-Firmenich AG

Archer Daniels Midland

Adisseo

Alltech Inc

Cargill Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Cargill and ENOUGH expanded ABUNDA mycoprotein production via zero-waste fermentation to enhance sustainable feed solutions. The project scales a fermentation platform capable of turning low-value substrates into high-protein biomass enriched with functional polysaccharides. These polysaccharides can be co-formulated with adaptogens, providing Cargill with a vertically integrated source that mitigates mushroom-supply volatility in the adaptogen market for animal nutrition.

- January 2025: Novus International invested USD 15 million in Resilient Biotics for precision swine health platforms using microbiome analytics. The partnership links real-time gut-microbiome data to tailored dosing recommendations for botanical and microbial additives. Such data-driven validation helps overcome limited species-specific efficacy evidence, a key restraint on the adaptogens market for animal nutrition.

- December 2024: Cargill acquired two United States feed mills from Compana Pet Brands to increase its adaptogenic product output. The acquisition adds 275,000 metric tons of annual capacity and modern mixing lines designed for heat-sensitive phytogenics. Additional throughput and controlled-temperature processing enable Cargill to meet the rising demand for adaptogen-infused formulations from customers across North America.

- September 2024: Anpario has completed the acquisition of Bio-Vet, adding direct-fed microbials to its range of natural additives. Bio-Vet’s probiotic strains complement Anpario’s existing herbal portfolio, enabling the development of synbiotic products that address gut health on multiple fronts. These hybrid offerings position Anpario to compete in the adaptogens market for animal nutrition with multifunctional solutions that command premium pricing.

Global Adaptogens Market Report Scope

| Herbal Adaptogens |

| Mushroom Adaptogens |

| Powder |

| Liquid |

| Encapsulated/Beadlet |

| Poultry |

| Swine |

| Ruminants |

| Aquaculture |

| Pets |

| Stress Mitigation |

| Immune Enhancement |

| Feed Conversion Improvement |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Source | Herbal Adaptogens | |

| Mushroom Adaptogens | ||

| By Form | Powder | |

| Liquid | ||

| Encapsulated/Beadlet | ||

| By Livestock Species | Poultry | |

| Swine | ||

| Ruminants | ||

| Aquaculture | ||

| Pets | ||

| By Function | Stress Mitigation | |

| Immune Enhancement | ||

| Feed Conversion Improvement | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the adaptogens market for animal nutrition?

The adaptogens market size for animal nutrition stands at USD 1.80 billion in 2025 and is forecast to hit USD 2.83 billion by 2030.

Which region leads the adaptogens market for animal nutrition?

Asia-Pacific leads due to intensive aquaculture in China and expanding livestock production in India.

Why are mushroom adaptogens growing faster than herbal ones?

Mushrooms such as cordyceps and reishi provide beta-glucans that deliver measurable immune improvements, driving an 11.8% CAGR through 2030.

How are precision-nutrition platforms influencing adoption?

Tools like DSM-Firmenich’s Verax use blood biomarkers to quantify stress reduction and performance gains, offering proof of ROI that accelerates uptake.

What are the biggest restraints for the adaptogens market for animal nutrition?

Regulatory ambiguity, volatile wild-crafted herb sourcing, limited species-specific data, and mycotoxin risks in mushroom extracts present the main challenges.

Which livestock segment is projected to grow the fastest?

Aquaculture will expand at a 14.2% CAGR because adaptogenic mycobiotics effectively reduce mortalities in high-density aquatic systems.

Page last updated on: