Market Overview

| Study Period | 2021 - 2031 |

|---|---|

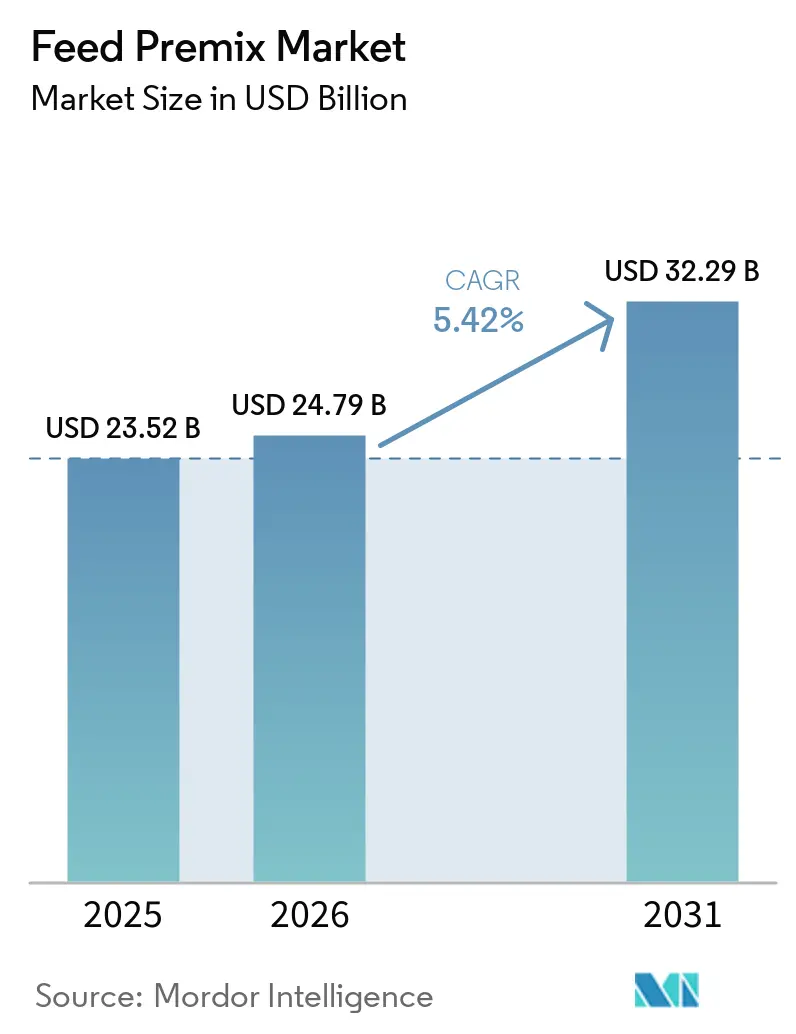

| Market Size (2026) | USD 24.79 Billion |

| Market Size (2031) | USD 32.29 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

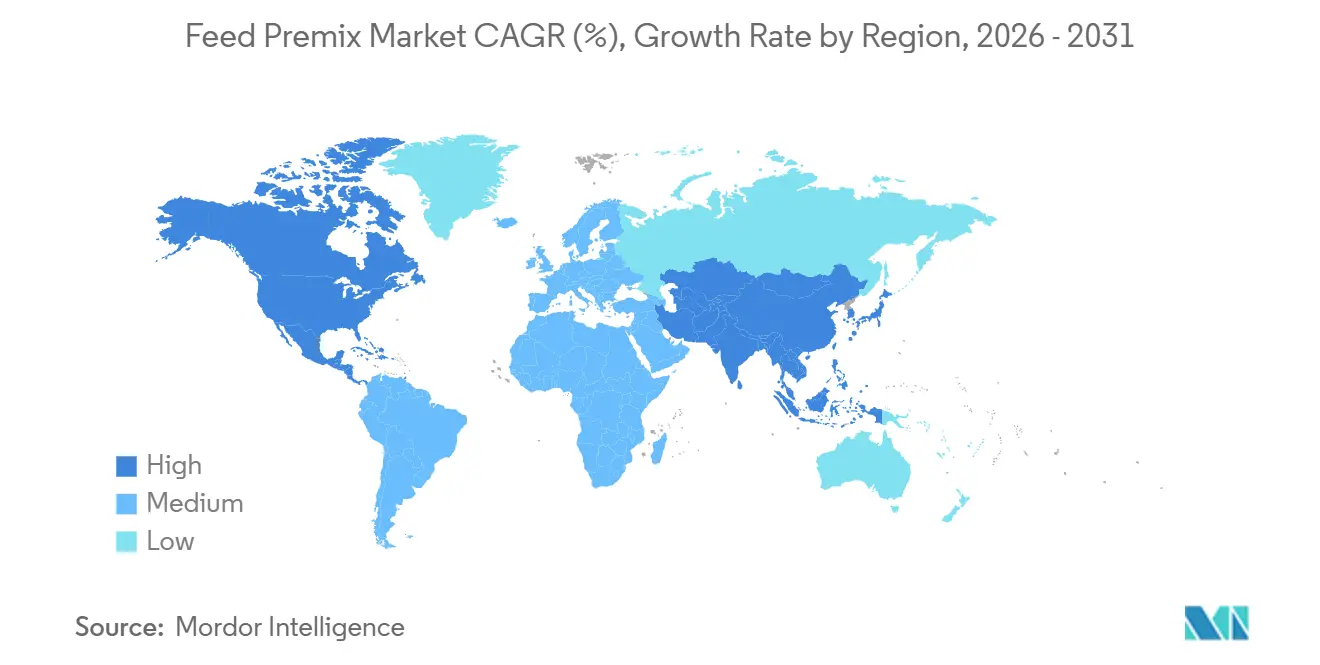

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Feed Premix Market Analysis by Mordor Intelligence

The feed premix market size is projected to grow from USD 23.52 billion in 2025 and USD 24.79 billion in 2026 to USD 32.29 billion by 2031, registering a CAGR of 5.42% between 2026 and 2031. The move from on-farm mixing to industrial compound feed systems across Asia, Africa, and South America continues to support the feed premix market, as formal feed production requires more consistent micronutrient inclusion and traceable sourcing. According to the Alltech Agri-Food Outlook 2026, global feed production reached 1.44 billion metric tons in 2025, with aquaculture feed up 4.7% and broiler feed up 3.7%, which kept demand in the feed premix market elevated across species rather than tying growth to a single livestock cycle[1]Source: Alltech, "Alltech Agri-Food Outlook 2026", April, 2026, alltech.com. North America held the leading position in 2025, while Asia-Pacific is set to post the fastest expansion, reflecting the difference between mature compliance-led demand and newer commercial feed industrialization in the feed premix market. The market is also being reshaped by antibiotic reduction policies, greater use of alternative ingredients such as insect protein, algae meal, distillers dried grains, fermented plant proteins, and tighter mineral balancing, which are raising the value of more complex premix formulations across multiple animal systems. Competition remains moderate because the top 5 companies held a significant share of the market in 2025, leaving a large portion of the feed premix market open to regional specialists, custom blenders, and species-focused formulators.

Key Report Takeaways

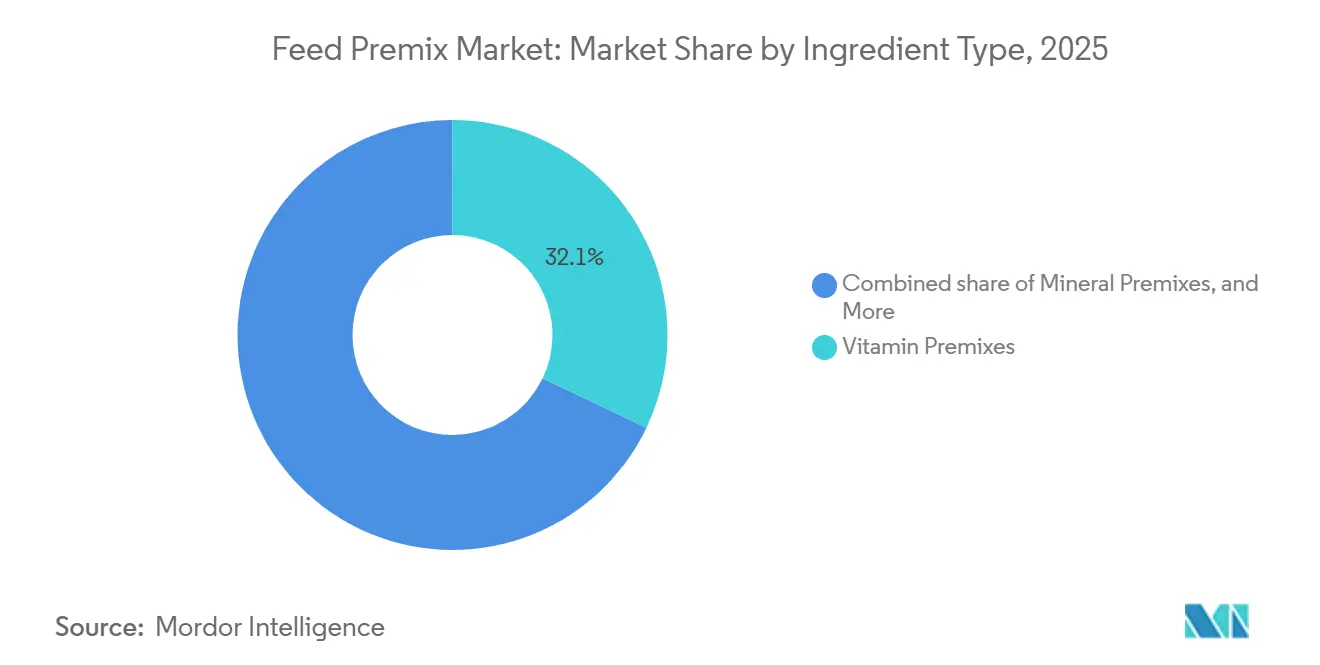

- By ingredient type, vitamin premixes held 32.1% of the feed premix market share in 2025, while mineral premixes estimated to grow at a CAGR of 7.6% from 2026 to 2031.

- By form, powder premix accounted for 67.5% of the feed premix market size in 2025, while liquid premix estimated to grow at a CAGR of 7.6% from 2026 to 2031.

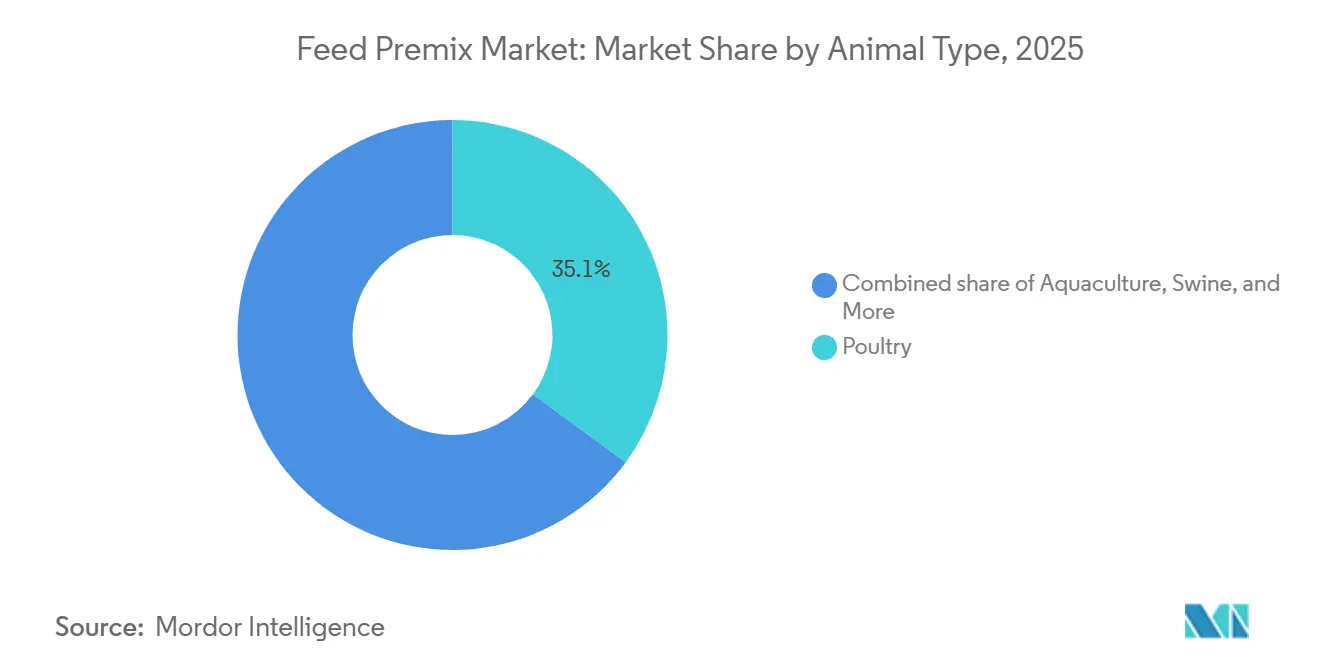

- By animal type, poultry captured 35.1% of the feed premix market size in 2025, while aquaculture is projected to expand at a 6.5% CAGR from 2026 to 2031.

- By geography, North America held 34.3% of the feed premix market share in 2025, while Asia-Pacific projected to grow at the highest CAGR of 7.9% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Feed Premix Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising poultry and egg feed intensity | +1.2% | Global, strongest in China, India, Brazil, United States, and Mexico | Short term (≤ 2 years) |

| Commercial compound feed penetration in Asia and Africa | +1.1% | Asia-Pacific core, with spillover to the Middle East and Africa, especially China, India, Vietnam, Nigeria, and Egypt | Medium term (2-4 years) |

| Antibiotic reduction nutrition programs | +0.8% | Global, concentrated in the European Union and China, with early gains in Germany, France, Spain, and Thailand | Medium term (2-4 years) |

| Precision nutrition and digital formulation adoption | +0.6% | North America and Europe, spreading to China and Brazil | Long term (≥ 4 years) |

| Increasing feed fortification in dairy production systems | +0.5% | Strongest in the United States, the European Union, India, New Zealand, and China | Medium term (2–4 years) |

| Alternative ingredients requiring micronutrient formulation adjustment | +0.4% | Global, concentrated in China, Norway, Brazil, and Vietnam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Poultry and Egg Feed Intensity

Broiler feed production rose 3.7% to 400.4 million metric tons in 2025 compared to 2024, which reinforced poultry as the largest consumption base for premix demand in the feed premix market, according to Alltech Agri-Food Outlook. Demand is not coming only from flock growth, because producers are also moving toward denser housing, faster cycles, and tighter feed conversion targets in large poultry systems. That operating model raises the need for dependable vitamin and trace mineral inclusion per ton of finished feed. Layer feed also increased by 3.2% to 180.1 million metric tons between 2024 and 2025, supported by steady egg consumption in Asia and Africa amid higher red meat prices, according to the Alltech Agri-Food Outlook 2026. Poultry, therefore, provides the feed premix market with a broad, recurring demand base that is renewed through frequent production cycles rather than seasonal buying. The large share of broiler and layer feed in global compound feed output also limits producers' ability to move away from certified premix suppliers without compromising quality consistency. This makes poultry a stabilizing force for the feed premix market even when disease events disrupt individual regions.

Commercial Compound Feed Penetration in Asia and Africa

Africa recorded 11.5% growth in commercial feed production between 2024 and 2025, the fastest regional growth rate reported in the draft, with gains across poultry, dairy, and ruminant systems in markets such as Nigeria, Egypt, Kenya, and Ethiopia, according to Alltech Agri-Food Outlook. The larger significance is that this shift reflects a move away from informal grain blending toward industrial compound feed channels. Once feed output moves into formal mill systems, certified premix becomes a standard input rather than an optional add-on. That change tends to raise premix demand faster than animal numbers alone would suggest. In Southeast Asia, Cargill Incorporated’s Giang Dien premix plant in Vietnam, established in 2024, features an annual capacity of 40,000 metric tons and over 95% automation, showing how local production is being built around traceability and export-grade quality requirements[2]Source: Aquafeed, “Cargill Opens State-of-the-Art Premix Plant in Vietnam,” aquafeed.com. Indonesia’s halal certification requirements for animal nutrition inputs are also pushing mills toward documented and verified premix procurement. As a result, commercial feed formalization remains one of the clearest structural growth supports for the feed premix market in developing regions.

Antibiotic-Reduction Nutrition Programs

The European Medicines Agency reported a 17.4% year-on-year decline in medicated premix sales across European Union member states in 2024, showing that legacy medicated formats are losing ground in regulated livestock systems[3]Source: European Medicines Agency, “European Sales and Use of Antimicrobials for Veterinary Medicine”, ema.europa.eu. This does not reduce nutritional complexity in the feed premix market instead, it shifts demand toward more functional, multi-component blends. Producers replacing antibiotic growth promoters often rely on mixes that combine vitamins, minerals, enzymes, probiotics, organic acids, and phytogenics. A 2026 scoping review in Agriculture found that probiotics, phytogenics, and organic acids were the most studied alternatives to antibiotic growth promoters in livestock diets. That pattern supports a stronger demand for higher-value formulations rather than simpler legacy blends. Kemin Industries, Inc. also secured European Union authorization for Clostat across all pig categories in January 2025, demonstrating how regulatory approval can turn clinical evidence into a long-term commercial opportunity. With the European Union still targeting a 50% reduction in veterinary antimicrobial use by 2030 relative to 2018 levels, this driver is likely to remain important across the feed premix market for several years.

Precision Nutrition and Digital Formulation Adoption

Trouw Nutrition’s NutriOpt platform processes desktop near-infrared reflectance scans across a broad network of feed mills, enabling real-time feed analysis, formulation optimization, and nutrient consistency management within commercial feed production systems, which shows that digital formulation is already operating at a commercial scale across the feed premix market. The main change is that mills can now revise recipes more frequently as commodity prices and raw material composition shift. That shortens the specification cycle for premix suppliers and favors companies that can deliver more customized blends with faster response times. The same platform logic also makes formulation less dependent on fixed quarterly assumptions and more tied to daily nutrient measurement. Cargill’s digital formulation analysis noted that poor control of raw material variability can result in substantial feed-efficiency losses for medium-sized broiler integrators, strengthening the economic case for precision nutrition tools. Research on real-time formulation also showed that tighter nutrient control can reduce lysine use while sustaining target performance, supporting more phase-specific and value-added premix demand. Over time, this is estimated to increase the role of data-linked customization within the feed premix market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Farmer margin pressure and cost volatility | -0.6% | Global, most acute in Brazil, Argentina, Mexico, and India | Short term (≤ 2 years) |

| Regulatory fragmentation for feed premixes | -0.4% | Global, concentrated in the United States, Germany, China, and Brazil | Medium term (2-4 years) |

| Trace-mineral supply chain disruptions | -0.3% | Global, concentrated in China, with sourcing pressure in Europe and North America | Medium term (2-4 years) |

| Consumer pushback on over-fortified animal products | -0.2% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Farmer Margin Pressure and Cost Volatility

Cost pressure remains a clear restraint for the feed premix market because feed buyers often adjust formulation quality when grain and additive costs rise quickly. Corn procurement costs increased sharply in early 2026, while soybean meal prices also moved higher over the same period, squeezing margins for poultry and swine producers. When these pressures intensify, some buyers shift toward lower-specification blends or cheaper mineral sources rather than maintaining premium premix formulas unchanged. Similar cost stress affected vitamins, amino acids, minerals, and organic acids during the 2025–2026 Gulf supply disruption, with vitamin E and methionine among the inputs facing notable price increases. This pressure tends to weigh more heavily on specialty functional products because those purchases are more flexible than minimum nutritional requirements. Buyers are therefore relying increasingly on forward contracting, options, and dual sourcing strategies to protect supply plans. Even so, margin pressure can still slow value growth in the feed premix market when producers prioritize cost control over premium formulation depth.

Regulatory Fragmentation for Feed Premixes

Regulatory fragmentation continues to slow the feed premix market because additive approvals, medicated feed rules, import standards, and traceability requirements vary widely across major regions. The European Commission’s Implementing Regulation (EU) 2025/2575, adopted in December 2025, ordered the withdrawal of several feed additives from the market, which forces product reformulation and registration work under tight timelines[4]Source: European Commission, Official Journal of the European Union, “Commission Implementing Regulation (EU) 2025/2575 of 18 December 2025 Withdrawing From the Market Certain Feed Additives,” eur-lex.europa.eu. That creates a heavier burden for smaller regional manufacturers that do not have the same regulatory resources as multinational suppliers. The draft also points to non-tariff barriers in markets such as Indonesia and India, where import and certification requirements reduce the usefulness of standardized global formulations. In this environment, pre-registered portfolios become strategic assets rather than back-office tools. Phibro Animal Health Corporation’s 2024 acquisition of Zoetis’ medicated feed additive portfolio reflected the value of owning licensed product lines across many countries and manufacturing sites. The result is a feed premix market where compliance depth can be as important as scale in securing long-term customer relationships.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Vitamins Anchor Demand While Minerals Accelerate

Vitamin premixes led this segment with a 32.1% share in 2025, supported by their central role in immunity, reproduction, and carcass quality across species. Within the feed premix industry, this category remained the broadest demand base because commercial diets rarely remove vitamins even during periods of cost pressure. Their widespread inclusion across poultry, swine, ruminant, aquaculture, and pet nutrition applications continues to support stable, long-term global demand.

Mineral premixes are projected to grow at the fastest pace, at a 7.6% CAGR from 2026 to 2031, as tighter control of bioavailability and excretion becomes more important in the feed premix market. Amino acid blends also benefit from lower crude protein strategies, while enzyme premixes gain from reformulated diets that use more variable alternative ingredients. Probiotic and prebiotic blends are gaining momentum in antibiotic-restricted production systems, and antioxidant, acidifier, and specialty functional blends are increasingly sold as part of multi-functional packages rather than stand-alone additives. Precision nutrition programs and sustainability-focused livestock production systems are further accelerating the adoption of advanced mineral and functional premix solutions globally.

By Form: Powder Holds Structural Lead While Liquid Expands Faster

Powder premix accounted for 67.5% of the market in 2025, reflecting its fit with dry-mixing systems, longer shelf life, and wide regulatory acceptance. Across the feed premix market, powder remained the standard commercial format because most mills were already built around dry-handling and batch-consistency requirements. Its compatibility with automated feed manufacturing systems and lower transportation complexity also continues to support large-scale commercial adoption globally.

Liquid premix is projected to record the fastest growth, at a 7.6% CAGR from 2026 to 2031, especially in aquaculture and other applications where post-pelleting delivery improves additive survival in the feed premix market. Powder will still hold the structural lead because new dry-premix investments continue to support export-quality and traceable production. Liquid systems, however, are gaining from precision feeding setups that blend multiple nutrient streams and can reduce manufacturing, storage, handling, and shipping costs by 2-3% in controlled trials. Adoption of intensive livestock systems is also increasing as producers seek better nutrient uniformity, flexibility, and dosing accuracy across production stages.

By Animal Type: Poultry Leads While Aquaculture Delivers the Fastest Growth

Poultry held 35.1% of the global market in 2025, supported by broiler, layer, and turkey operations across all major livestock regions. In the feed premix industry, poultry remained the most stable reorder cycle because flock turnover is frequent, and quality standards in integrated systems keep premix use relatively consistent. Rising demand for high-protein poultry products and increasing commercial feed penetration continue to reinforce long-term global poultry premix consumption.

Aquaculture is anticipated to expand at the fastest pace, at a 6.5% CAGR, from 2026 to 2031, in the feed premix market. Ruminants continue to benefit from dairy modernization in countries such as India and China, while swine is recovering as restocking continues in parts of Asia. Pet feed is still smaller in scale, but it is improving on premiumization and higher companion animal ownership, which adds another adjacent demand stream for more specialized micronutrient formulations. Sustainability-focused aquafeed formulations and improving feed conversion targets are also accelerating demand for precision premix solutions in aquaculture.

Geography Analysis

North America held a 34.3% share of the feed premix market in 2025, underpinned by high-throughput feed mills, rigorous oversight, and an enduring focus on cost-of-gain optimization within cattle, poultry, and swine supply chains. The region’s producers use sophisticated NIR analytics and cloud-linked formulation software to adjust premix inclusion in real time, reducing nutrient waste and ensuring label compliance. Ongoing regulatory clarity, such as the Food and Drug Administration's (FDA’s) October 2024 update to animal feed ingredient approval and feed labeling compliance requirements, has strengthened traceability and formulation standardization across the feed industry, enabling premix manufacturers to expand regional production capacity and technical support operations with greater regulatory certainty.

The Asia-Pacific region exhibits the fastest trajectory, with an 7.9% CAGR from 2026 to 2031, driven by rapid livestock population growth and a growing dominance of commercial feeds over farm-mixed rations. China’s premix manufacturers capitalize on the Ministry of Agriculture and Rural Affairs' (MARA) 2024 additive approvals, accelerating time-to-market for novel blends that appeal to integrators seeking performance lifts. India’s dairy modernization, Indonesia’s shrimp expansion, and Thailand’s broiler exports further enlarge addressable volumes. Digital feed platforms, once the domain of Western markets, are proliferating in Southeast Asia through cloud-based mobile tools that enable field technicians to adjust nutrient density on-site.

Europe remains a mature but reformulation-heavy region for the feed premix market because antibiotic restrictions and additive withdrawals are reshaping product design. South America continues to offer poultry and beef growth potential, although farmer margin volatility can lead to temporary downgrades in formulation depth. Africa posted the fastest feed production growth rate in 2025, and that is important because compound feed is replacing on-farm mixing in poultry and dairy systems. Middle East demand remains centered on food security-driven livestock investment, which supports incremental premix imports from both European and Asian suppliers.

Competitive Landscape

The feed premix market remains moderately concentrated, with the top 5 companies holding a significant share in 2025. Cargill, Incorporated. led the market, followed by DSM-Firmenich AG, BASF SE, Archer Daniels Midland Company, and Nutreco N.V. (SHV Holdings N.V.). This leaves a meaningful portion of the feed premix market open to regional blenders, local specialists, and species-focused suppliers. The competitive balance, therefore, favors large global platforms in standard and high-compliance categories, while still leaving room for local flexibility in tailored formulations.

A major change in February 2026 was DSM-Firmenich AG’s agreement to divest its Animal Nutrition and Health division to CVC Capital Partners for EUR 2.2 billion (USD 2.38 billion), with the business being split into a Solutions Company and an Essential Products Company. The division generated EUR 3.5 billion (USD 3.78 billion) in net sales in 2025, so this transaction separates premix services from a long-standing integrated vitamins supply structure. DSM-Firmenich AG had already sold its Feed Enzyme Alliance stake to Novonesis for USD 1.62 billion in June 2025, which further reduced vertical integration across the portfolio. In North America, Archer Daniels Midland Company and Alltech launched Akralos in February 2026, following a 2025 signing of the definitive agreement, combining 44 manufacturing facilities across the United States and Canada and changing regional buying dynamics for feed and premix distribution. These moves show that ownership structure, channel control, and regional manufacturing presence are becoming more important within the feed premix market.

Competitive strategy now centers on 3 themes, digital formulation integration, geographic expansion into higher-growth regions, and stronger positioning in functional premix categories. Trouw Nutrition’s NutriOpt platform shows how digital tools are being tied directly to formulation decisions and mill-level purchasing in the feed premix market. Evonik Industries AG is using a lower carbon footprint profile in MetAMINO to strengthen its position as sustainability requirements tighten across animal nutrition supply chains. Kemin Industries, Inc. has built regulatory positioning through Clostat authorization and product launches, while Phibro Animal Health Corporation expanded its licensed product reach through the Zoetis portfolio acquisition. White space remains more visible in precision aquaculture premix and in localized Sub-Saharan African production, where certification capability and supply proximity still create barriers that are hard to match with import-led models.

Feed Premix Industry Leaders

-

Cargill, Incorporated

-

DSM-Firmenich AG

-

BASF SE

-

Nutreco N.V. (SHV Holdings N.V.)

-

Archer-Daniels-Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DSM-Firmenich AG reached a formal agreement to divest its Animal Nutrition and Health division to CVC Capital Partners for USD 2.38 billion, plus an earnout of up to USD 0.54 billion, retaining a 20% equity stake. The business will split into a Solutions Company covering premix, performance solutions, and precision services, and an Essential Products Company covering vitamins, carotenoids, and aroma ingredients.

- February 2025: Novonesis completed the acquisition of DSM-Firmenich’s stake in the Feed Enzyme Alliance for USD 1.55 billion, adding 3% to group revenue and integrating distribution into its biosolutions platform.

- September 2024: DSM-Firmenich has expanded its premix and additives manufacturing plant in Egypt. The new facility spans 10,000 square meters and features modern infrastructure and advanced technology from Buhler Technologies. It incorporates an integrated plant control system with bar coding and serves customers in Egypt, the Middle East, Southern Europe, and Africa.

Global Feed Premix Market Report Scope

A premix is a value-added solution to livestock feed consisting of a mixture of requisite vitamins, minerals, diluents, and other nutrients. The feed premix market is segmented by Ingredient Type (Vitamins, Minerals, Amino Acids, Antioxidants, Enzymes, Probiotics and Prebiotics, Acidifiers, and Other Specialty Functional Premixes), by Form (Powder and Liquid), by Animal Type (Poultry, Ruminants, Swine, Aquaculture, Pets, and Other Animals), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The report offers market size and forecasts in terms of value (USD) for all the above segments.

By Ingredient Type

| Vitamins |

| Minerals |

| Amino Acids |

| Antioxidants |

| Enzymes |

| Probiotics and Prebiotics |

| Acidifiers |

| Other Specialty Functional Premixes |

By Form

| Powder |

| Liquid |

By Animal Type

| Poultry |

| Ruminants |

| Swine |

| Aquaculture |

| Pets |

| Other Animals |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Poland | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Thailand | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Ingredient Type | Vitamins | |

| Minerals | ||

| Amino Acids | ||

| Antioxidants | ||

| Enzymes | ||

| Probiotics and Prebiotics | ||

| Acidifiers | ||

| Other Specialty Functional Premixes | ||

| By Form | Powder | |

| Liquid | ||

| By Animal Type | Poultry | |

| Ruminants | ||

| Swine | ||

| Aquaculture | ||

| Pets | ||

| Other Animals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Poland | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Thailand | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of the feed premix market in 2031?

The sector is projected to reach USD 32.29 billion by 2031.

Which region grows fastest in feed premixes through 2031?

Asia-Pacific posts the quickest expansion with an 7.9% CAGR through 2031, fueled by livestock and aquaculture growth.

Which ingredient segment records the highest CAGR?

Mineral premixes register the steepest climb at 7.6% CAGR as producers favor chelated trace elements for better bioavailability.

How dominant are powder formulations within feed premixes?

Powder premix accounted for 67.5% of the feed premix market size in 2025, though liquids are steadily gaining share.

Page last updated on: