Expression Vectors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

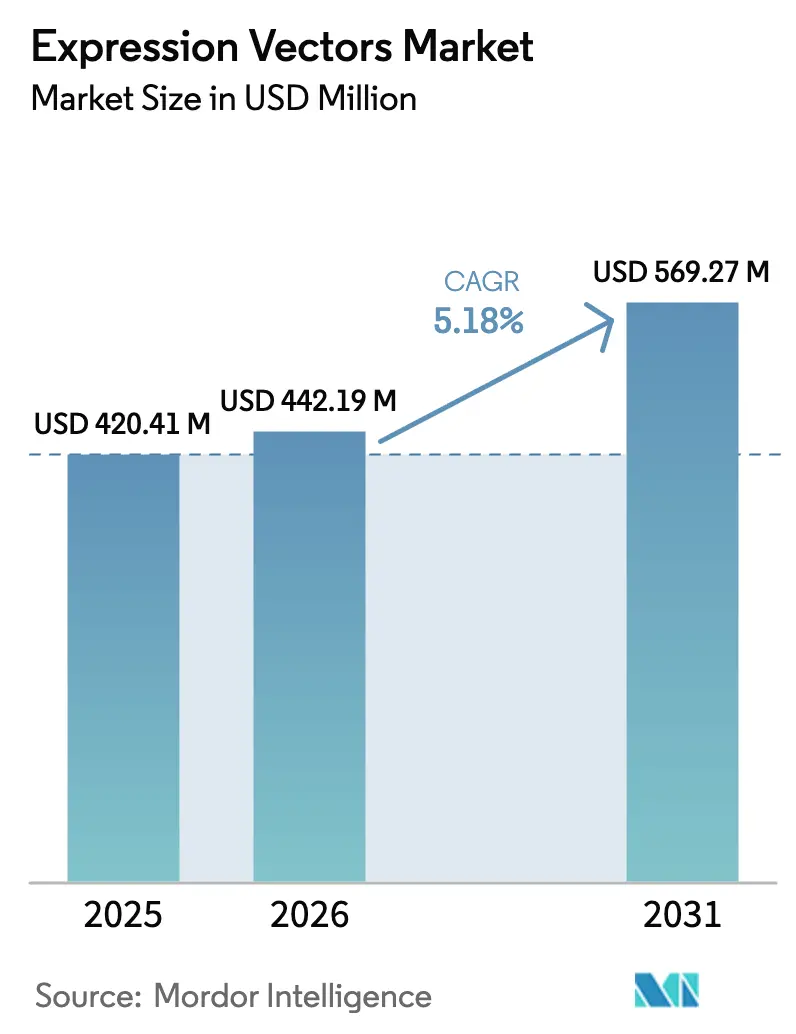

| Market Size (2026) | USD 442.19 Million |

| Market Size (2031) | USD 569.27 Million |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Expression Vectors Market Analysis by Mordor Intelligence

Expression vectors market size in 2026 is estimated at USD 442.19 million, growing from 2025 value of USD 420.41 million with 2031 projections showing USD 569.27 million, growing at 5.18% CAGR over 2026-2031. Rapid adoption of vectors in clinical-grade biologics, rising investments in artificial-intelligence-enabled vector optimization, and expanding contract manufacturing capacity are accelerating demand. Bacterial systems remain cost-efficient for simple proteins, while insect and mammalian hosts gain traction for complex therapeutics that require native-like folding [1]U.S. Food and Drug Administration, “Approved Cellular and Gene Therapy Products,” fda.gov . Contract development and manufacturing organizations (CDMOs) use scale and specialization to lower per-unit costs, yet escalating raw-material prices and tighter viral-safety standards lift compliance overheads. Competitive intensity rises as suppliers integrate AI-driven design with good-manufacturing-practice (GMP) production to secure long-term supply agreements.

Key Report Takeaways

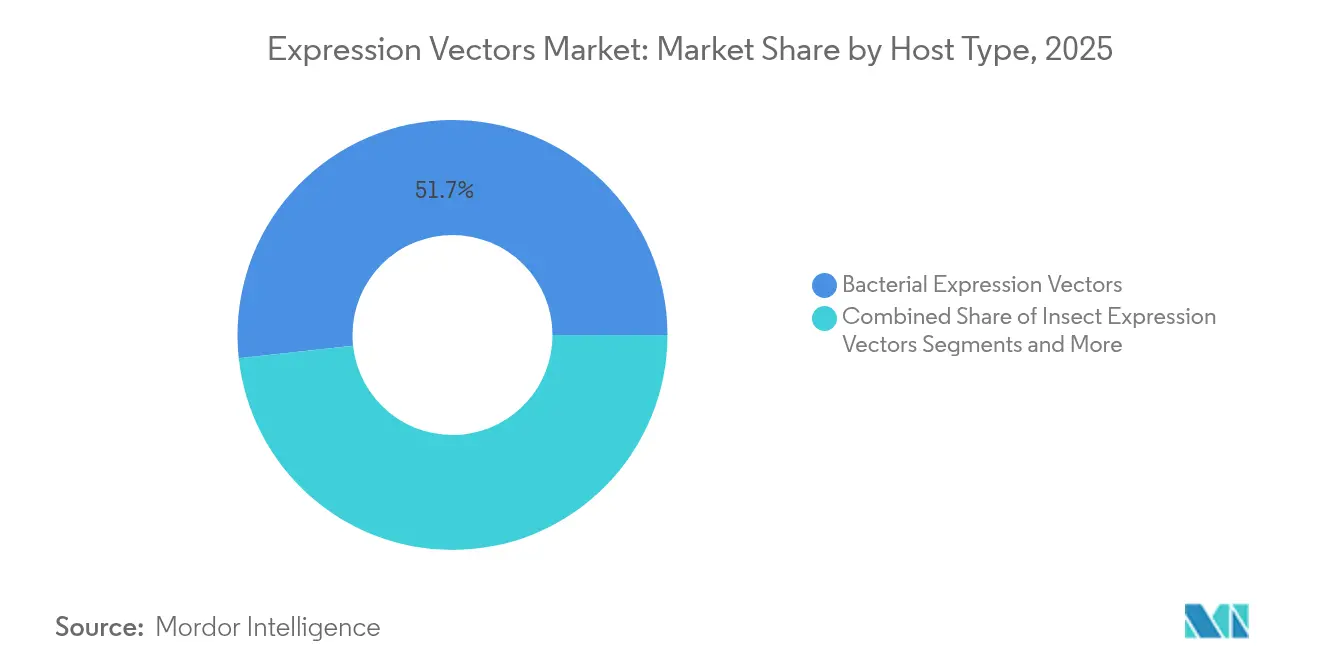

- Bacterial expression vectors held 51.72% of the Expression vectors market share in 2025. Insect expression vectors are projected to grow at a 5.97% CAGR through 2031.

- Therapeutic applications commanded 49.35% of the Expression vectors market size in 2025, while research applications are advancing at a 6.01% CAGR to 2031.

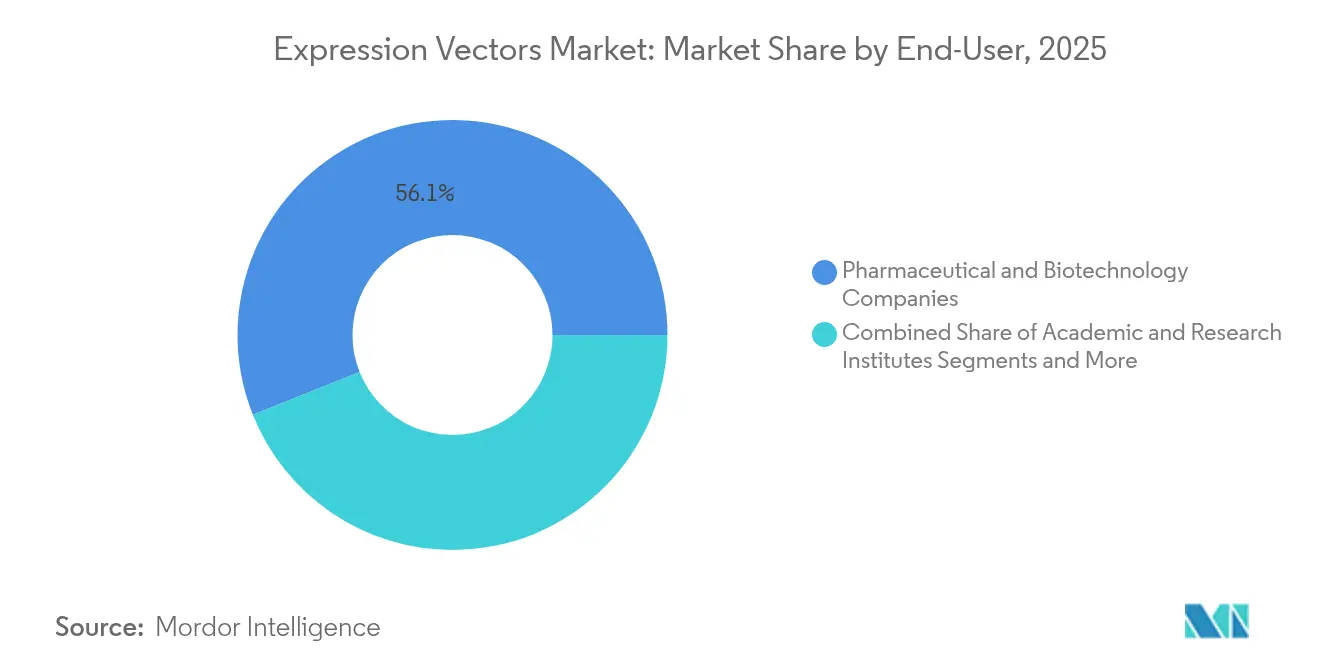

- Pharmaceutical and biotechnology companies captured 56.05% revenue share in 2025; academic and research institutes post the fastest growth at a 6.08% CAGR through 2031.

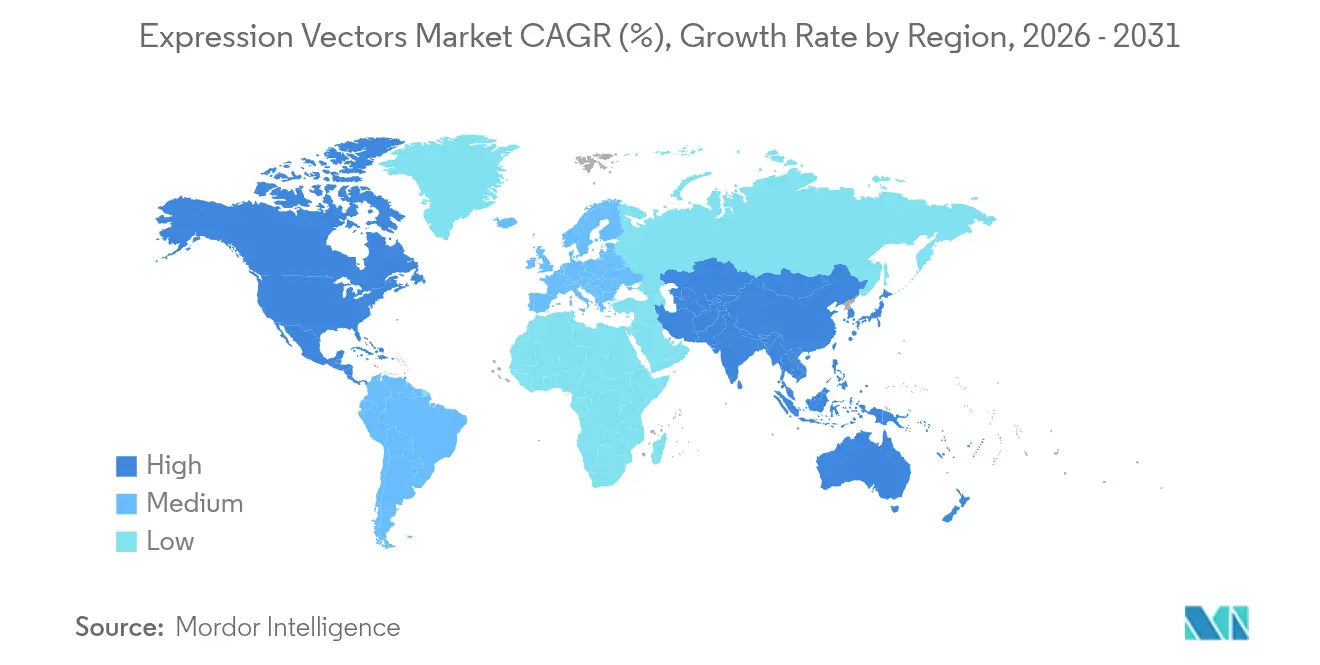

- North America accounted for 42.05% of 2025 revenue, whereas Asia-Pacific is forecast to expand at a 6.15% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Expression Vectors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in demand for advanced biologics & cell-/gene-therapies | +1.2% | Global, with North America & EU leading | Medium term (2-4 years) |

| Growing adoption of mammalian & insect hosts for complex proteins | +0.9% | Global, concentrated in APAC manufacturing hubs | Long term (≥ 4 years) |

| Expansion of contract vector manufacturing capacity | +0.8% | North America & EU core, spill-over to APAC | Short term (≤ 2 years) |

| AI-driven codon optimisation & de-novo vector design | +0.7% | Global, early adoption in US & Germany | Medium term (2-4 years) |

| Open-source vector repositories accelerating translation | +0.6% | Global, concentrated in academic research centers | Medium term (2-4 years) |

| mRNA-vaccine spill-over boosting plasmid-vector demand | +0.5% | North America & EU primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Demand for Advanced Biologics & Cell-/Gene-Therapies

Gene-therapy approvals climbed from 8 in 2023 to 15 in 2024, each requiring customized, high-purity vectors. Clinical programs now specify vector designs compatible with perfusion bioreactors and single-use systems, tightening supplier selection. Autologous CAR-T pipelines intensify batch-specific vector demand, prompting companies such as Bluebird Bio and Oxford BioMedica to restructure in-house production schedules. CDMOs with redundant suites absorb overflow, but their capacity utilization peaks during regulatory surges. Developers perceive secure vector supply as a strategic differentiator and often lock multi-year contracts, reinforcing long-term revenue visibility across the Expression vectors market.

Growing Adoption of Mammalian & Insect Hosts for Complex Proteins

Biopharma firms pivot toward baculovirus expression vector systems (BEVS) for membrane proteins and glycoproteins that need authentic post-translational modifications [2]Nature Biotechnology, “Advances in Baculovirus Expression Vector Systems for Complex Protein Production,” nature.com . Regulatory guidance now evaluates glycosylation consistency alongside sequence identity, favoring eukaryotic hosts. Although mammalian cell production costs remain higher, demand for distinctive safety and efficacy profiles justifies premiums, particularly for first-in-class therapies. Suppliers respond by widening transfection-media portfolios and offering ready-to-transfect kits optimized for Chinese hamster ovary and Spodoptera frugiperda cells. The trend reallocates R&D spending from bacterial optimization toward scalable eukaryotic platforms, broadening revenue channels across the Expression vectors market.

Expansion of Contract Vector Manufacturing Capacity

AGC Biologics, Polyplus, and other CDMOs invested more than USD 400 million in specialized vector plants during 2024. Expanded GMP suites lower per-gram costs by up to 35%, enticing small biotech firms that lack internal infrastructure. Outsourcing streamlines timelines, yet it also centralizes production in fewer hubs, raising systemic risk from capacity disruptions. CDMOs try to mitigate concentration risk through multi-site networks across the United States, Denmark, and Singapore. This outsourcing boom democratizes access to therapeutic-grade vectors, accelerating pipeline progression and fueling incremental demand within the Expression vectors market.

AI-Driven Codon Optimization & De-Novo Vector Design

The CodonTransformer algorithm improves average protein yield by 15-20% versus classical approaches, trimming development cycles from months to weeks [3]Nature Machine Intelligence, “CodonTransformer: AI-Driven Codon Optimization,” nature.com . Machine-learning pipelines now match promoters, enhancers, and codon biases to host-specific translational kinetics, raising predictability. Early adopters integrate AI into quality-by-design frameworks, translating improved expression into smaller bioreactor footprints and lower cost-of-goods. Open-source AI toolkits broaden experimentation in academic settings, intensifying competitive pressures but also accelerating innovation across the Expression vectors market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost & complexity of GMP-grade vector production | -0.8% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Stringent viral-vector safety regulations | -0.6% | North America & EU primarily | Medium term (2-4 years) |

| Patent thickets around promoters/regulatory elements | -0.4% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Supply-chain fragility for critical raw materials | -0.3% | Global, acute in APAC manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost & Complexity of GMP-Grade Vector Production

Clinical-grade plasmid DNA costs range between USD 50-200 per gram, four to ten times research-grade pricing. Capital expenses for ISO-classified cleanrooms, quality-management systems, and sterility testing inflate operating budgets. Small biotech firms often delay trials due to procurement bottlenecks, while academic centers rarely absorb full compliance costs. Although CDMOs mitigate scale constraints, tighter capacity during peak demand inflates spot prices and lengthens lead times. These dynamics dampen adoption rates in emerging markets and moderate overall expansion of the Expression vectors market.

Stringent Viral-Vector Safety Regulations

The FDA’s Q5A(R2) revision mandates broader adventitious-agent testing, extending development timelines by up to 12 months and adding USD 0.5-2 million per program. Similar European Medicines Agency guidance layers regional specificity onto global compliance frameworks, creating documentation redundancies. Small developers may struggle to finance incremental assays, limiting the pace of novel vector launches. Although the regulations raise safety standards and improve patient outcomes, they constrain near-term growth across the Expression vectors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Host Type: Bacterial Dominance Faces Insect System Challenge

Bacterial systems captured 51.72% of the Expression vectors market share in 2025, supported by cost-efficient fermentation and well-understood genetic toolkits. In contrast, Insect vectors record a robust 5.97% CAGR to 2031 as BEVS technology resolves folding and glycosylation constraints.

The Expression vectors market continues to migrate toward eukaryotic hosts, with mammalian platforms commanding premium pricing due to regulatory emphasis on protein quality. Yeast systems maintain relevance for certain enzymes, while plant and algal vectors explore non-pharma niches. As therapeutic pipelines tilt toward multi-subunit biologics, host-selection frameworks prioritize fidelity over cost, accelerating demand for sophisticated insect and mammalian solutions.

By Application: Research Applications Accelerate Beyond Therapeutics

Therapeutic programs accounted for 49.35% of the Expression vectors market size in 2025, yet research uses are growing faster at a 6.01% CAGR through 2031. Open repositories lower entry barriers, and NIH funding for vector-based discovery climbed 18% in 2024.

Academic labs exploit rapid prototyping to interrogate gene functions, fuel synthetic-biology constructs, and validate drug targets, creating consistent baseline demand. Improved translation frameworks shorten the bench-to-clinic timeline, enabling discoveries to progress into regulated pipelines within five years. These dynamics extend revenue opportunities throughout the Expression vectors market life cycle.

By End-User: Academic Institutes Drive Innovation Pipeline

Pharmaceutical and biotech firms represented 56.05% of 2025 revenue, relying on long-term supply agreements to de-risk clinical milestones. Academic and research institutes, however, exhibit the fastest 6.08% CAGR to 2031 as universities scale vector core facilities and bolster translational funding.

Shared infrastructure reduces per-experiment costs and promotes standardized quality. Cross-sector collaborations pair academic discovery with industrial scale-up, enhancing commercialization prospects. CDMOs serve both cohorts, positioning themselves as connective tissue across the Expression vectors market.

Geography Analysis

North America’s 42.05% share reflects entrenched venture investment, streamlined FDA pathways, and integrated supply chains connecting discovery through commercialization. Canada’s CAD 2.2 billion Advanced Biomanufacturing initiative furthers domestic vector capacity, and Mexico’s near-shoring trend adds process-development demand.

Asia-Pacific is the fast-growing region at 6.15% CAGR. China authorised its first home-grown CAR-T therapy in 2024, spurring domestic CDMOs to boost vector output. Singapore’s tax-incentive clusters attract global majors, and South Korea’s K-Bio Belt builds dedicated biomanufacturing corridors. Japan reduces review timelines by 30%, enhancing deployment speeds for regenerative products.

Europe maintains a consolidated but innovative market, with Germany’s EUR 500 million BioRegion program enhancing infrastructure. The United Kingdom speeds approvals post-Brexit, while France’s Genopole adds vector suites. Southern European nations grow gradually, yet shared EMA guidelines permit seamless product movement, reinforcing pan-regional demand within the Expression vectors market.

Competitive Landscape

The Expression vectors market shows moderate fragmentation as no single vendor exceeds one-third revenue, yielding space for niche innovators. Thermo Fisher Scientific and Merck KGaA anchor portfolios spanning cloning kits, transfection reagents, and GMP production. GenScript and New England Biolabs gain share through tailored services and rapid turnaround.

AI-enabled sequence design, proprietary promoters, and integrated regulatory consulting emerge as differentiators. Patent filings on vector technologies rose 34% in 2024, highlighting intensifying innovation. CDMOs like AGC Biologics and Lonza leverage scale to negotiate bulk raw-material prices, creating price pressure on smaller labs. Yet, high compliance barriers limit new entrants, preserving margins for established actors.

Industry participants increasingly adopt platform approaches. Agreements such as the Lonza–Oxford BioMedica partnership integrate lentiviral expertise with global manufacturing footprints. Suppliers bundle AI-guided design, plasmid topology selection, and cGMP output, giving customers single-source convenience. These strategies fuel healthy competition while sustaining innovation velocity across the Expression vectors market.

Expression Vectors Industry Leaders

Thermo Fisher Scientific, Inc.

Promega Corporation

Merck KGaA

Agilent Technologies

Bio-Rad Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Thermo Fisher Scientific announced a USD 350 million viral-vector capacity expansion in California and the Netherlands, adding advanced AAV suites.

- September 2024: Thermo Fisher Scientific announced a USD 350 million viral-vector capacity expansion in California and the Netherlands, adding advanced AAV suites.

- August 2024: AGC Biologics secured USD 200 million from Asahi Kasei to scale viral-vector manufacturing in Seattle and Copenhagen.

- July 2024: GenScript opened a 150,000-sq-ft cGMP plasmid and viral-vector plant in New Jersey.

Global Expression Vectors Market Report Scope

As per the scope of the report, expression vector, also known as an expression construct, are plasmid or virus that is specially designed for expressing genes in a cell. It is a vector widely used for protein production. The expression vectors market is segmented by Host Type (Bacterial Expression Vectors, Mammalian Expression Vectors, Insect Expression Vectors, Yeast Expression Vectors and Other Expression Vectors), Application (Therapeutic Applications, Research Applications and Industrial Applications), End-User (Pharmaceutical and Biotechnology Companies, Contract Research Organizations (CROs) and Contract Manufacturing Organizations (CMOs), and Academic Research Institutes), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Bacterial Expression Vectors |

| Mammalian Expression Vectors |

| Insect Expression Vectors |

| Yeast Expression Vectors |

| Others |

| Therapeutic Applications |

| Research Applications |

| Enzyme Manufacturing |

| Pharmaceutical and Biotechnology Companies |

| CDMOs / CROs / CMOs |

| Academic & Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Host Type | Bacterial Expression Vectors | |

| Mammalian Expression Vectors | ||

| Insect Expression Vectors | ||

| Yeast Expression Vectors | ||

| Others | ||

| By Application | Therapeutic Applications | |

| Research Applications | ||

| Enzyme Manufacturing | ||

| By End-User | Pharmaceutical and Biotechnology Companies | |

| CDMOs / CROs / CMOs | ||

| Academic & Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Expression vectors market?

The Expression vectors market size is USD 442.19 million in 2026.

How fast is demand expected to grow over the next five years?

Revenue is projected to reach USD 569.27 million by 2031, reflecting a 5.18% CAGR.

Which host system is gaining the most market traction?

Insect expression vectors show the fastest growth, advancing at a 5.97% CAGR through 2031.

What region offers the highest growth opportunity?

Asia-Pacific leads with a projected 6.15% CAGR due to large-scale investments in gene-therapy manufacturing.

Who are the leading suppliers in this space?

Thermo Fisher Scientific, Merck KGaA, GenScript, and New England Biolabs command significant share with comprehensive vector portfolios and GMP capacity.

Page last updated on: