Europe Wood Decorative Wall Panel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

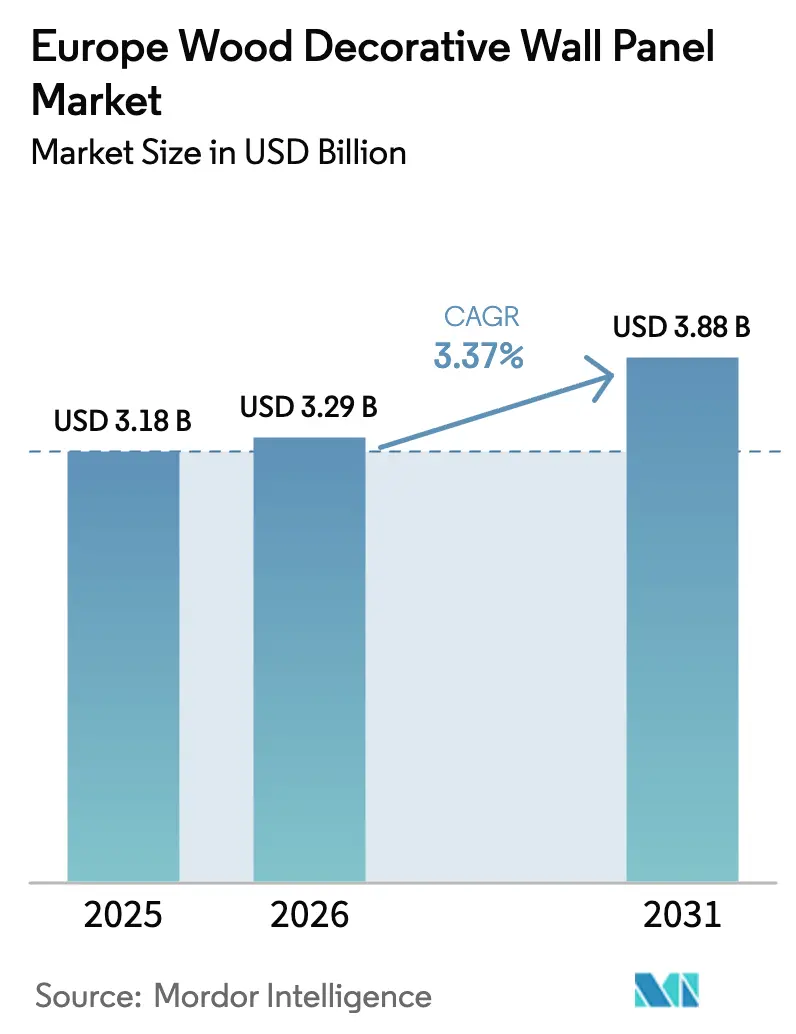

| Base Year Market Size (2025) | USD 3.18 Billion |

| Market Size (2026) | USD 3.29 Billion |

| Market Size (2031) | USD 3.88 Billion |

| Growth Rate (2026 - 2031) | 3.37% CAGR |

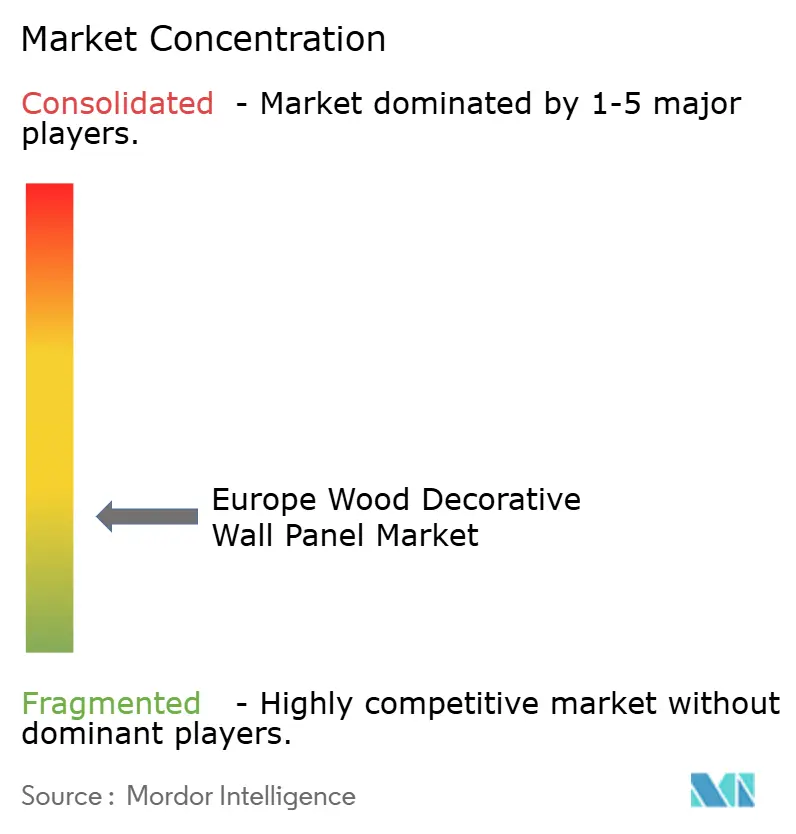

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Wood Decorative Wall Panel Market Analysis by Mordor Intelligence

The Europe wood decorative wall panel market size is expected to increase from USD 3.18 billion in 2025 to USD 3.29 billion in 2026 and reach USD 3.88 billion by 2031, growing at a CAGR of 3.37% over 2026-2031. The forward outlook signals a shift to steadier growth after the 2019–2025 whipsaw of pandemic-era supply shocks and post-2021 retrofit surges, keeping the European wood decorative wall panel market on a more predictable path. Elevated financing costs and a soft construction backdrop in key economies temper new-build momentum, yet renovation, acoustic retrofits, and sustainability-led procurement sustain baseline demand. Regulatory change is a durable driver, with the revised Construction Products Regulation introducing environmental declarations and Digital Product Passports while the EU Deforestation Regulation hardens traceability, a combination that supports integrated producers with strong certification frameworks. Circular-economy initiatives and the push toward low-emission engineered wood reinforce mid-cycle growth pockets across residential and commercial fit-outs, supporting the Europe wood decorative wall panel market through the forecast window.

Key Report Takeaways

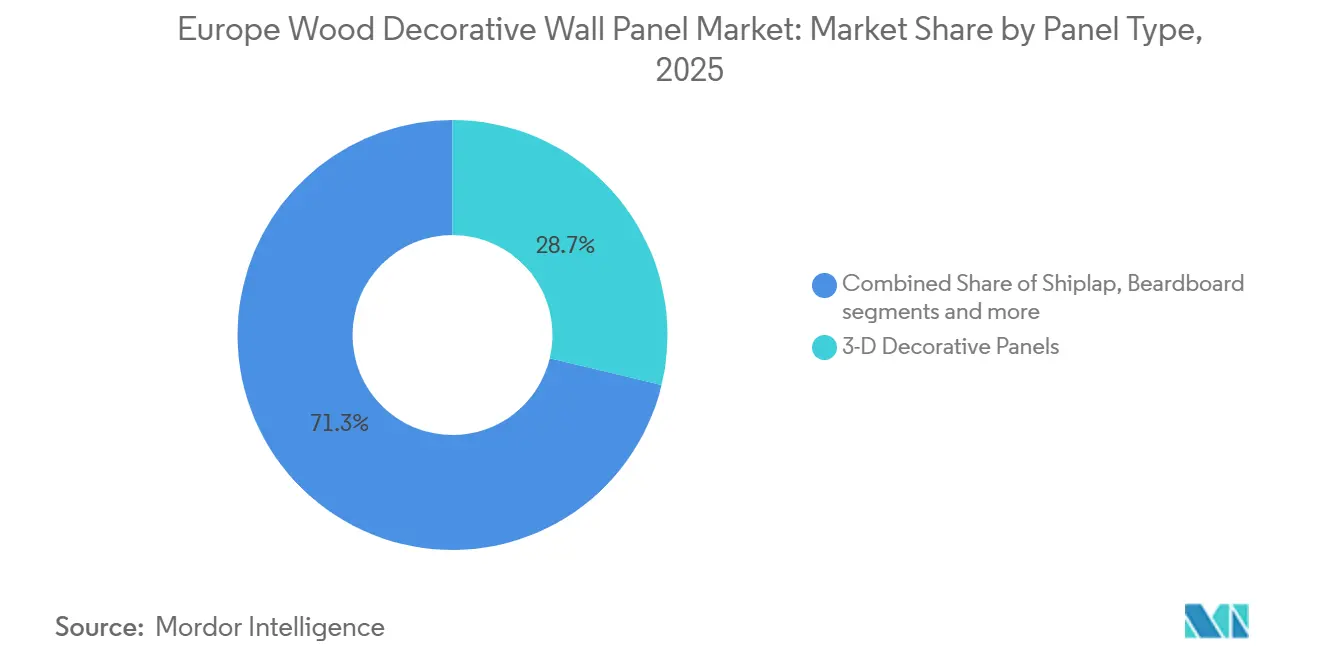

- By wood type, engineered wood held 47.21% of the Europe wood decorative wall panel market share in 2025. Within wood types, engineered wood is forecast to grow at a 3.98% CAGR through 2031.

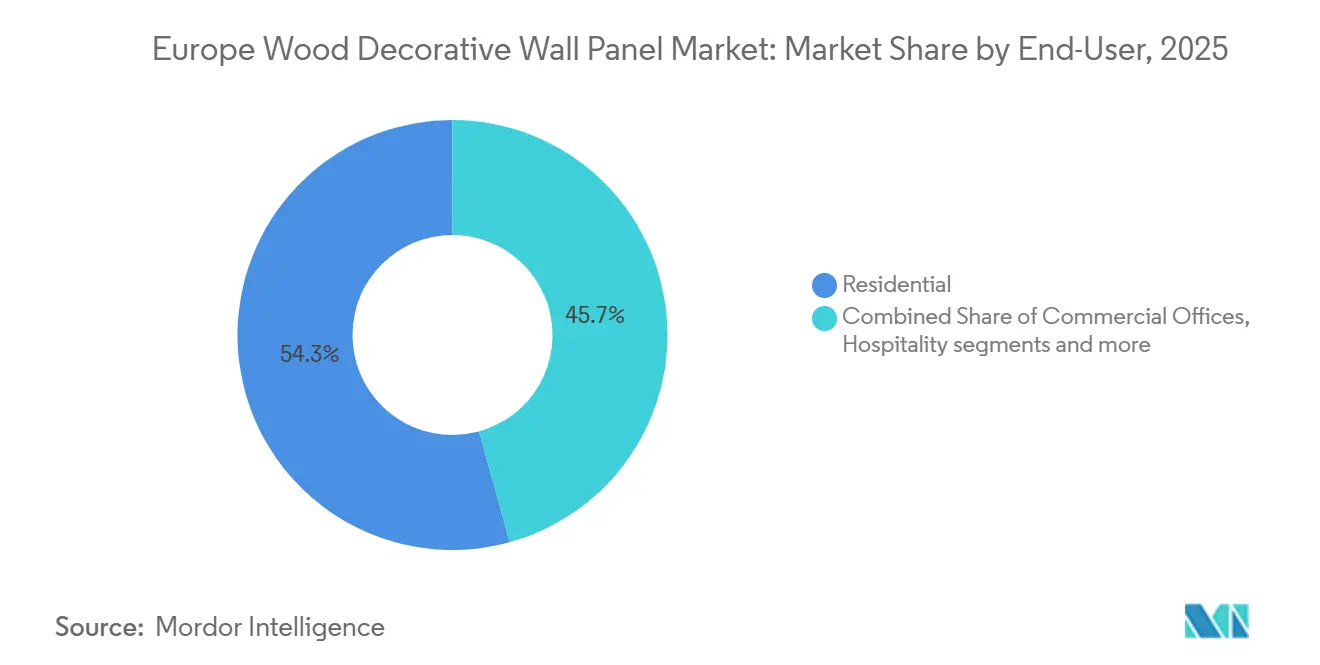

- By end-user, residential accounted for 54.14% of the Europe wood decorative wall panel market share in 2025. Within end-users, hospitality and leisure is expected to grow at a 4.24% CAGR to 2031.

- By distribution channel, specialty interior stores retained 41.92% of the Europe wood decorative wall panel market share in 2025. Within channels, online platforms are projected to record a 4.73% CAGR through 2031.

- By geography, Germany held 23.81% of the Europe wood decorative wall panel market share in 2025. Within country markets, Spain is projected to grow at a 4.61% CAGR over 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Wood Decorative Wall Panel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Renovation & Remodeling Activities | +1.2% | Strongest in Germany, France, the Nordics, and Spain, showing the fastest residential recovery. | Medium term (2-4 years) |

| Eco-Friendly & Sustainable Material Demand | +0.9% | Early gains in Germany, Netherlands, Nordics | Long term (≥ 4 years) |

| Aesthetic Customization Trend | +0.5% | Concentrated in the United Kingdom, Italy, and Spain, for hospitality and retail | Short term (≤ 2 years) |

| Remote/Hybrid Work Driving Acoustic Panels | +0.6% | Peak demand in the United Kingdom, Germany, and Benelux office hubs | Medium term (2-4 years) |

| QSR Biophilic Design Rollouts | +0.3% | Western Europe, led by France, Germany, the United Kingdom, and Spain | Short term (≤ 2 years) |

| Circular-Economy Mandates Boosting Recycled Wood Panels | +0.7% | EU-wide enforcement beginning 2025–2026; strongest in the Netherlands, Germany, and France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Renovation & Remodeling Activities

Residential renovation momentum improved in 2024–2025, although the recovery varied by country. In France, renovation material costs for maintenance and improvement posted modest gains through 2025, with the relevant index indicating positive activity levels tied to household upgrades that draw decorative finishes into scope. Germany’s interior repair and finishing costs firmed into late 2025 as new-build conditions weakened, which redirected spending to maintenance and energy-related upgrades that frequently include wall panel refreshes. In the United Kingdom, construction output slipped in late 2025 on a three-month basis, mainly due to weaker private housing repair and maintenance, yet order books earlier in the year showed signs of release as inflation receded and financing conditions stabilized. Spain bucked broader softness as new-dwelling permits rose at a double-digit pace in 2024 and renovation-linked applications increased, underpinned by European recovery funds that encouraged residential upgrades. These shifts reinforce a renovation-led pathway for the Europe wood decorative wall panel market, with project mix favoring energy efficiency, acoustic comfort, and biophilic finishes in both homes and high-traffic spaces.

Eco-Friendly & Sustainable Material Demand

Producers increase recycled wood integration and reduce emissions as customers and regulators coalesce around circularity and climate metrics. Sonae Arauco reported 33% recycled wood integration in 2024 and expanded recycling infrastructure, while signaling a path to higher recycled content in core European markets. Pfleiderer reached 53.5% recycled content in 2024 and broadened its certified portfolio, positioning engineered panels to satisfy project specifications that now frequently prioritize low embodied carbon and verified sourcing [1]Source: Pfleiderer, “Sustainability Report 2024,” Pfleiderer, pfleiderer.com. At the policy level, the EU’s product and circularity framework pushes recyclability, material passports, and robust disclosure practices, which amplify the appeal of traceable engineered wood systems. EU-driven research programs target adhesive reformulation and improved recyclability at scale, aiming to address fiber contamination and recovery quality constraints in MDF and HDF. Together, these advances encourage design teams to shift toward engineered solutions in public and private projects, supporting the Europe wood decorative wall panel market across the forecast window.

Remote/Hybrid Work Driving Acoustic Panels

A return to offices on hybrid schedules reconfigures interior layouts and increases demand for sound absorption, privacy zones, and flexible partitions. Building owners and tenants upgrade finishes during refresh cycles, and acoustic wall systems are part of comprehensive approaches that complement ceilings, flooring, and furnishings in a single spec. Suppliers expand acoustic product portfolios that integrate sustainability credentials with performance, making recycled or bio-based acoustic wall treatments more visible in commercial RFPs. In this setting, branded product lines and architectural specialties designed for classrooms, healthcare, and offices gain traction by addressing both noise mitigation and design coherence. These patterns directly support acoustic subsegments across the European wood decorative wall panel market as project scopes balance cost, comfort, and compliance in multi-tenant assets.

Circular-Economy Mandates Boosting Recycled Wood Panels

EU circularity policies increase pressure to use certified and recycled inputs, accelerate the adoption of Digital Product Passports, and improve end-of-life recovery pathways. The European Panel Federation highlights production recovery in 2024 and emphasizes the regulatory push toward higher environmental ambition, which sets a clear direction for panel assortments and supply chains. Companies respond by scaling recycling lines and piloting reversible adhesives and coatings designed for future material separation and reuse. EUDR requirements harden upstream diligence and favor operations with robust chain-of-custody systems and forest-asset visibility, reducing risk for buyers that now screen for compliance as a condition of award. These developments align with specifier preferences and municipal procurement guidelines, reinforcing the structural pull toward traceable, low-emission panels in the European wood decorative wall panel market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Installation Complexity and Higher Skilled-Labor Dependence | -0.4% | Acute in Germany, United Kingdom, Nordics | Medium term (2-4 years) |

| Timber Price & Supply Volatility | -0.6% | Northern Europe exposure cascades to Central Europe mills | Short term (≤ 2 years) |

| Competition from Alternative Wall Coverings | -0.3% | Spain, Italy, and France, where ceramic tile and stone veneers retain preference | Long term (≥ 4 years) |

| Stricter Urban Fire-Safety Codes | -0.2% | United Kingdom, Germany, France public-building standards | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Installation Complexity and Higher Skilled-Labor Dependence

Decorative panel installation, especially for 3-D profiles and acoustic systems, often requires substrate preparation, precision joinery, and specialized adhesives, which raises reliance on skilled trades. Tight labor markets in key countries and contractor preference for higher-margin scopes can extend lead times and elevate installed costs for residential retrofit projects. These conditions steer some customers toward simpler alternatives or supplier-developed modular systems that reduce install time but still carry premium pricing when specifications require higher fire-safety or acoustic performance. Evolving fire-safety rules increase the technical bar for treated wood panels, with EN 13501-1 classifications and associated tests now the norm for public facilities and high-occupancy interiors. Fire-retardant treatments and full testing protocols add costs and procedural steps that are harder for small fabricators to absorb, which consolidates demand with certified suppliers in the wood decorative wall panel market.

Timber Price & Supply Volatility

Wood raw-material markets remain sensitive to supply shifts, pest damage, and geopolitical trade flows, which together can swing sawlog availability and pricing across the region. European industry reporting shows that sawmilling and panel producers contended with price spikes and margin pressure through 2024 before conditions began to stabilize. Producers with less vertical integration find it harder to pass through costs when end-demand is weak, while large integrated firms hedge with forest leases or asset ownership. Company disclosures indicate significant EBITDA sensitivity to wood input costs, underscoring the operational importance of raw-material management during periods of volatility. These realities shape near-term planning and purchasing strategies and can delay discretionary upgrades, moderating momentum in the Europe wood decorative wall panel market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Panel Type: Acoustic Panels Propel Retrofit Demand as Hybrid-Work Reorders Office Acoustics

3-D decorative panels secured a 28.73% share in 2025, reflecting strong placement in hospitality feature walls, retail brand environments, and premium residential accents, although their pace tracks below segment highs. Acoustic wood panels, while smaller in absolute volume, lead growth at 4.12% CAGR through 2031 as occupiers and developers address distraction and privacy needs in modern open-plan and hybrid layouts. Rising expectations around wellness and comfort steer specifications toward acoustic finishes that pair sound absorption with natural textures and low-emission materials. Manufacturers now position acoustic product lines as part of integrated solutions, linking panels with ceilings and partitions to meet performance and design briefs in offices, schools, and healthcare. This momentum broadens adoption across the market as owners upgrade interiors to support new patterns of use.

The acoustic category’s advance extends into hospitality and public venues, where visual identity and noise control are both important. Design-led acoustic collections that incorporate recycled content or wood-wool compositions gain traction as teams seek to balance sustainability with sound control. Supplier innovations that improve fire performance without harmful treatments further expand use cases in public buildings where Class B or higher classifications are often required. Portfolio breadth from established brands reduces specification risk, smoothing adoption for general contractors and installers. These factors reinforce the Europe wood decorative wall panel market as acoustic panels steadily increase share within retrofit budgets across mixed-use and commercial assets.

By Wood Type: Engineered Wood Dominates on Cost-Performance While Solid Hardwood Retreats to Luxury Tiers

Engineered wood captured 47.21% in 2025 and leads growth at 3.98% CAGR through 2031, supported by scalable manufacturing, consistent density for digital machining, and compatibility with low-formaldehyde resin systems that improve indoor-air profiles. Producers step up to tighter emission norms, and leading facilities commit to lower emission classes across MDF and HDF lines to meet specifier and regulatory expectations. Engineered solutions expand into thinner 3-D profiles and textured finishes that replicate the look of solid wood while staying within budget and performance parameters. In contrast, solid hardwood and softwood panels are concentrated in high-end homes and heritage renovations where provenance and tactile qualities command a premium. These dynamics keep engineered substrates central to the wall panel market across both residential and commercial interiors.

Pfleiderer's OrganicBoard Pure (100% organic binder, 100% recycled fiber) and Swiss Krono's planned 2025 recycling center (30t/hour, replacing 100,000 m³ of virgin logs) position MDF/HDF as circular-economy flagships [2]Pfleiderer Sustainability Report 2024, Swiss Krono Sustainability Report https://www.pfleiderer.com/fileadmin/content/Images/Sustainability_Report_2025/Pfleiderer_Sustainability_Report_2024_EN.pdf. . However, technical barriers remain: cross-linked formaldehyde adhesives in post-consumer MDF hinder fiber reintegration, with current recycling yielding degraded particles suitable only for particleboard, not virgin-grade MDF. Horizon Europe's CIRCULAR-C project (2025-2029) targets this gap via reversible-bond resins, but commercial deployment lags 2027-plus [3]Source: VITO, “CIRCULAR-C Develops Novel Biobased Formulations for Circular Construction Materials,” VITO, vito.be.

By End-User: Residential Volumes Lead but Hospitality/Leisure Posts Steepest Gains via Biophilic Mandates

Residential accounted for 54.14% in 2025, reflecting the region’s aging housing stock and interior upgrades that emphasize comfort, style, and healthier indoor environments. Growth within residential tracks the broader construction cycle and financing conditions, with owners and landlords scheduling improvements to coincide with planned maintenance or energy-efficiency works. Hospitality and leisure advance faster at 4.24% CAGR through 2031 as restaurants and hotels refresh interiors to strengthen brand identity and improve acoustic comfort. Commercial offices stabilize as hybrid schedules push fit-outs toward zoned collaboration areas and quiet spaces in refurbishments. These factors together lift the specification of performance-oriented panels across the Europe wood decorative wall panel market’s end-use mix.

Institutional segments contribute through programs that address classroom acoustics, patient well-being, and community facility upgrades. Education and healthcare tend to prioritize durable, easy-clean, low-emission surfaces, which support certain coated or laminated engineered products in areas where hygiene and maintenance matter. Retail fit-outs bifurcate, with luxury and flagship concepts investing in customized finishes while value-oriented chains concentrate on modular systems to control costs. Corporate sustainability commitments nudge specifications toward certified, recycled, and low-emission options in each of these segments. These application patterns reinforce sustained demand pathways for the Europe wood decorative wall panel market across 2026–2031.

By Distribution Channel: Specialty Stores Hold Ground Yet Online Platforms Surge on Digital-Native Builders

Specialty interior stores held 41.92% in 2025, sustaining share through showroom experiences, design advisory, and relationships with architects and contractors. Channel strength in consultative selling supports complex or bespoke projects where specifiers and installers value tactile evaluation and technical support. Online platforms post the fastest growth at 4.73% CAGR through 2031 as trade customers expand digital ordering and suppliers invest in product data, configurators, and logistics. Direct-to-contractor models remain important for large projects where coordinated delivery and technical field support are critical, especially in acoustic or fire-rated applications. The result is a hybrid channel environment that blends in-store advisory with digital convenience for the Europe wood decorative wall panel market.

As e-commerce tools improve visualization and documentation, standard and mid-range products move online faster than bespoke or solid-wood lines that still benefit from in-person selection. Packaging and last-mile practices continue to evolve because panel shipments require careful handling to avoid damage and returns. Product information management and BIM-ready content also matter, since trade buyers increasingly expect downloadable data for project coordination. Suppliers that align channel strategy with product complexity and logistics realities are best positioned to capture full value. These dynamics enable steady share gains for digital channels while preserving the role of showrooms in the Europe wood decorative wall panel market.

Geography Analysis

Germany held 23.81% in 2025 for the European wood decorative wall panel market, but construction output weakened, and completed dwellings fell to 161,682 in 2024 as building permits dropped again from 2023 levels [4]Source: German Federal Statistical Office, “Construction Price Indices for Civil Engineering and Maintenance,” Destatis, destasis.de. Renovation and interior repair costs, however, firmed in 2025, suggesting a pivot to maintenance, energy-related improvements, and interior refreshes. These conditions favor panel demand in repair and refurbishment as new-home volumes undershoot policy targets. National programs that raise environmental ambition maintain the focus on certified and low-emission materials, supporting engineered panels with strong documentation. As log markets stay tight, domestic producers face input cost pressure, reinforcing the advantage of integrated supply and strategic sourcing.

The United Kingdom’s late-2025 construction output softened modestly on a rolling basis, but earlier 2025 order trends pointed to stabilization alongside falling inflation. Trade statistics show wood and panel-related imports remain a significant component in the construction materials basket, with the EU still dominant in supply lines for thick sawn wood and allied products. The NISTA framework (National Infrastructure and Service Transformation Authority), established in 2025, aims to streamline infrastructure delivery, potentially catalyzing non-residential panel demand in public projects post-2026 [5]Source: Bain & Company, "Europe’s construction industry is turning a corner as early signs of recovery point to strengthening medium-term prospects", https://www.bain.com/about/media-center/press-releases/20252/europes-construction-industry-is-turning-a-corner-as-early-signs-of-recovery-point-to-strengthening-medium-term-prospects--bain--company. Supplier reporting indicates capacity and shipments guidance that aligns with a cautious recovery scenario in European wood panel demand. As financing conditions ease, multi-year refurbishment plans and public programs underpin steady fit-out activity tied to the market.

France faced ongoing new-build weakness in 2024, but maintenance and improvement activity signaled better momentum late in 2025, supported by incentives that favored residential rehabilitation. Renovation material costs ticked up quarter-over-quarter in Q3 2025, while the business climate for building construction improved slightly in December 2025. Timber-building turnover edged higher in 2024 despite unit declines, indicating resilience within wood-based systems even as broader housing activity fell. These conditions keep France on a moderate-growth track, with interior upgrades and public-sector renovation sustaining decorative panel demand.

Spain is projected to grow at a 4.61% CAGR in 2026–2031 trajectories, led by a sharp rise in new-dwelling permits in 2024 and broader recovery-fund support for residential improvements. Construction contributed materially to the economy in 2024 by both value added and investment metrics, and input price indices stabilized, improving the outlook for fit-out materials. Tourism tailwinds lift hotel and hospitality construction, which supports feature walls and acoustic systems in guest-facing spaces. Municipal incentives that reward energy-efficiency retrofits reinforce demand for low-emission, certified panels in renovations. Spain’s balanced mix of residential and commercial drivers makes it a growth leader within the Europe wood decorative wall panel market.

Competitive Landscape

The Europe wood decorative wall panel market features a clear top tier and a long tail of regional specialists. EGGER, Kronospan, and Swiss Krono together account for roughly 38% of value, leveraging integration in resins, panel lines, and distribution. EGGER’s decorative products performance in fiscal 2025/26 and its targeted investments in press capacity underscore a strategy aligned with textured, design-forward panels. Kronospan’s acquisition of a chemical producer deepens resin self-sufficiency, reinforcing cost control and supply stability across MDF, particleboard, and OSB lines. These moves secure upstream resilience and product breadth that support specification wins in both residential and commercial interiors across the market..

Beyond the leaders, specialty brands and mid-cap producers differentiate on circular content, fire performance, and acoustic engineering. BAUX expands its recyclable, fire-rated acoustic collections for commercial retrofits with strong sustainability credentials. Pfleiderer reinforces its positioning on recycled content and certifications while addressing liquidity and capital structure to stabilize operations and maintain product development. International suppliers focused on ceilings and architectural specialties are expanding their portfolio into wall applications for education, healthcare, and workplace projects. This mix of innovation and channel specialization keeps competition active across product tiers within the market.

Input cost management and regulatory compliance remain defining strategic capabilities. Company disclosures quantify material cost sensitivity, highlighting the earnings impact of wood price swings and supporting vertical-integration rationales. EUDR geolocation mandates and stricter fire-safety testing requirements are pushing smaller fabricators to partner with certified suppliers or exit high-specification segments. Central and Eastern Europe continue to draw capacity commitments in select lines as large groups scale near customer bases and strengthen logistics. The result is an industry that rewards traceability, documentation, and technical support as much as price, reinforcing disciplined growth pathways in the European wood decorative wall panel market.

Europe Wood Decorative Wall Panel Industry Leaders

-

Egger Group

-

Kronospan

-

Swiss Krono Group

-

Finsa

-

Sonae Arauco Deutschland GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: West Fraser announced permanent closures of two North American sawmills by end-2025 and provided a 2026 operational outlook that includes stable resin and chemical inputs and steady European and UK OSB shipment ranges, reflecting broader timber-supply constraints that shape pricing conditions linked to European markets.

- November 2025: EGGER commissioned a new short-cycle press in Gütersloh to expand coated board capacity for textured 3-D decorative applications, while Pfleiderer presented its 2026 decor collection with new wood, stone, and textile designs and synchronized-pore technologies.

- October 2025: Stora Enso completed the divestment of a significant portion of Swedish forest assets to strengthen its balance sheet and continued to refine its wood products strategy as disclosed in regulatory filings.

Europe Wood Decorative Wall Panel Market Report Scope

| Shiplap |

| Beadboard |

| Board & Batten |

| Raised Panels |

| 3-D Decorative Panels |

| Acoustic Wood Panels |

| Solid Hardwood |

| Softwood |

| Engineered Wood (MDF, HDF, Plywood) |

| Residential |

| Commercial Offices |

| Hospitality & Leisure |

| Retail |

| Educational & Institutional |

| Healthcare Facilities |

| Specialty Interior Stores |

| Large DIY / Home-Improvement Stores |

| Direct-to-Contractor Sales |

| Online Platforms |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Panel Type | Shiplap |

| Beadboard | |

| Board & Batten | |

| Raised Panels | |

| 3-D Decorative Panels | |

| Acoustic Wood Panels | |

| By Wood Type | Solid Hardwood |

| Softwood | |

| Engineered Wood (MDF, HDF, Plywood) | |

| By End-User | Residential |

| Commercial Offices | |

| Hospitality & Leisure | |

| Retail | |

| Educational & Institutional | |

| Healthcare Facilities | |

| By Distribution Channel | Specialty Interior Stores |

| Large DIY / Home-Improvement Stores | |

| Direct-to-Contractor Sales | |

| Online Platforms | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

What is the Europe wood decorative wall panel market size and expected growth to 2031?

The Europe wood decorative wall panel market size is estimated USD 3.29 billion in 2026 and is projected to reach USD 3.88 billion by 2031 at a 3.37% CAGR.

Which panel types lead demand in the Europe wood decorative wall panel market?

3-D decorative panels lead by share in 2025, while acoustic wood panels post the fastest growth through 2031 as hybrid work and hospitality retrofits expand.

Which materials are gaining traction in the Europe wood decorative wall panel market?

Engineered wood leads by share and growth due to scalable production, low-emission resin systems, and circularity programs that raise recycled content.

Which end-use segments support growth in the Europe wood decorative wall panel market?

Residential leads by volume, while hospitality and leisure grow fastest through 2031 as brands invest in acoustic comfort and biophilic finishes.

How are regulations affecting the Europe wood decorative wall panel market?

Rules on product declarations and deforestation-free sourcing elevate traceability and favor certified, low-emission, and recycled-content panels with proven testing.

Which countries are most influential in the Europe wood decorative wall panel market?

Germany leads by share, Spain leads by growth, and the UK, France, and Italy contribute through renovation programs and sector-specific refurbishment cycles.

Page last updated on: