Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

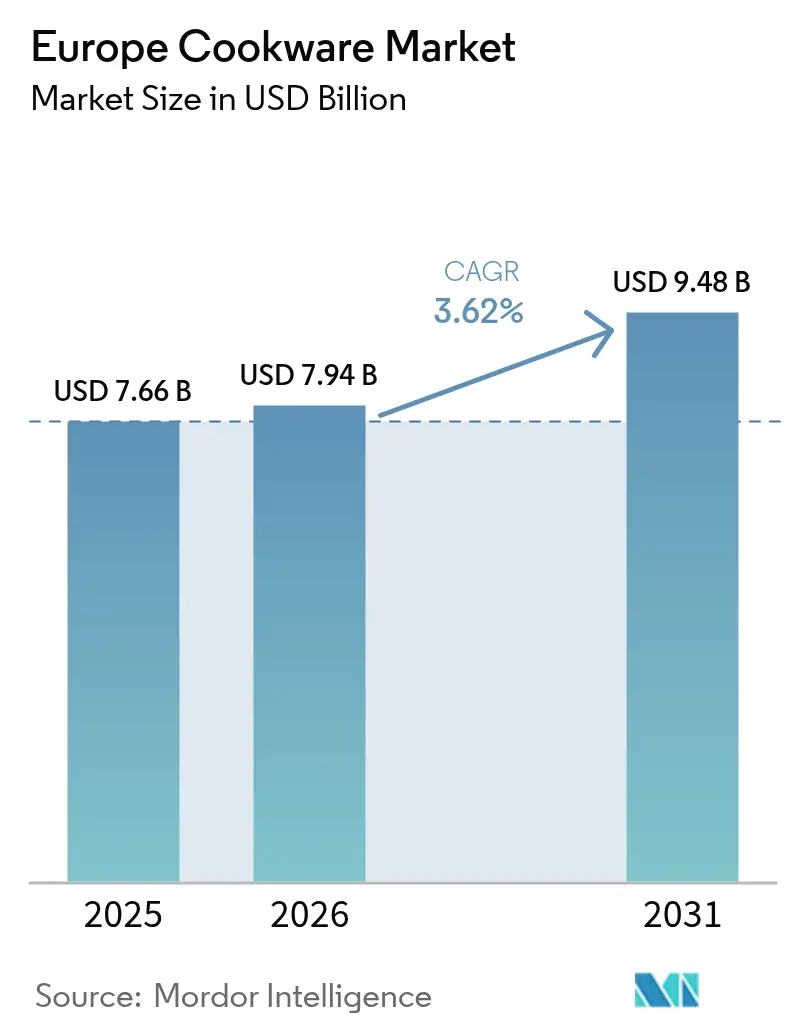

| Base Year Market Size (2025) | USD 7.66 Billion |

| Market Size (2026) | USD 7.94 Billion |

| Market Size (2031) | USD 9.48 Billion |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Cookware Market Analysis by Mordor Intelligence

The European cookware market size is expected to grow from USD 7.66 billion in 2025 to USD 7.94 billion in 2026 and is forecast to reach USD 9.48 billion by 2031 at 3.62% CAGR over 2026-2031. Sustained home-cooking engagement that began during pandemic lockdowns, accelerating premium purchases in Western Europe, and policy-driven demand for eco-designed, induction-ready products together keep revenue expanding even as unit volumes mature. Price-sensitive households still stretch replacement cycles yet rising disposable incomes in Central and Eastern Europe enable first-time buyers to trade up rather than trade down. Rapid e-commerce adoption, especially where augmented-reality tools let shoppers “feel” weight and finish online, lowers entry barriers for niche brands while preserving premium price bands in stores. Raw-material volatility clouds margins but simultaneously pushes manufacturers toward recycled inputs that satisfy both cost-control and sustainability mandates.

Key Report Takeaways

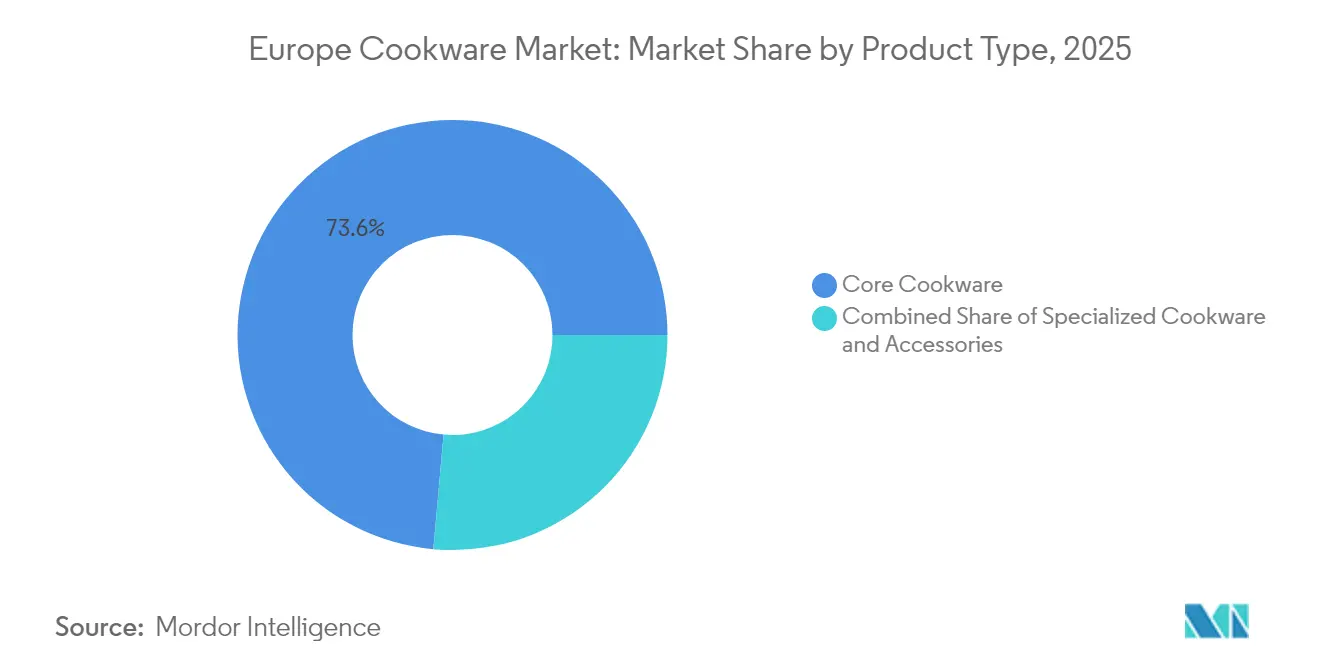

- By product type, core cookware held 73.58% of the European cookware market share in 2025, whereas specialized pieces are forecast to log a 4.85% CAGR through 2031.

- By material, stainless-steel products commanded 34.92% share of the European cookware market size in 2025; ceramic and glass are projected to rise at a 3.68% CAGR to 2031.

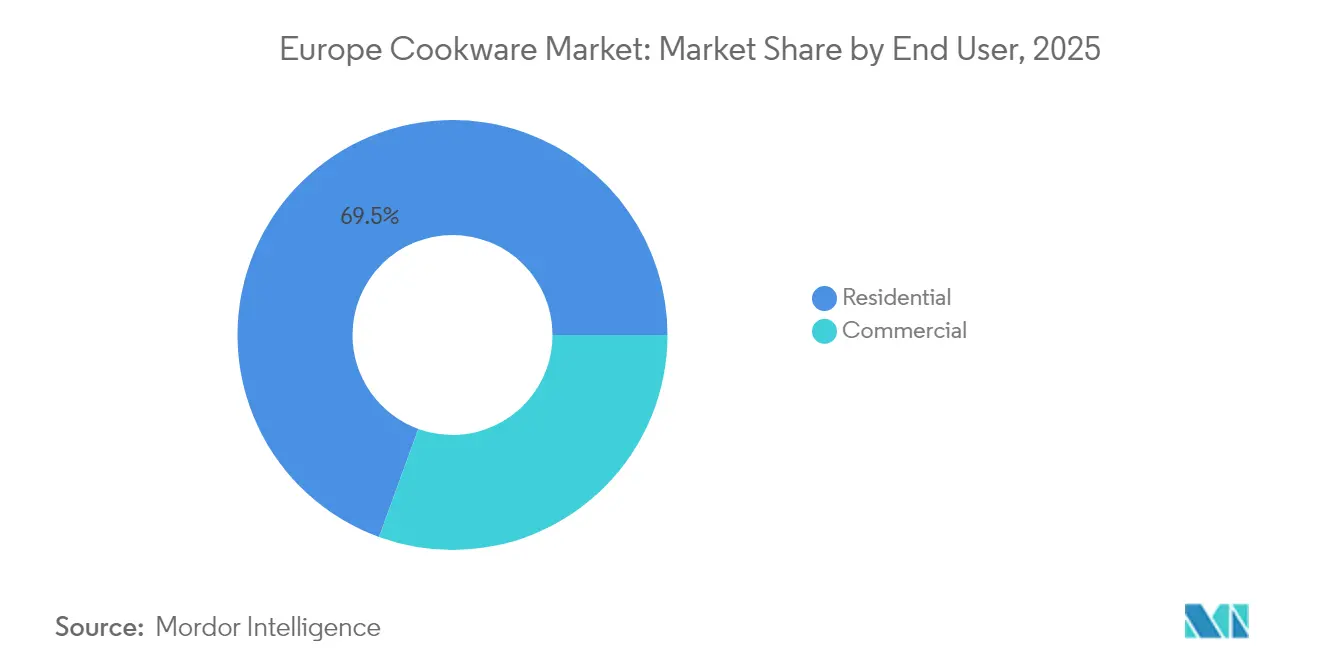

- By end user, residential demand accounted for 69.45% of 2025 revenue, while the commercial segment is expected to post the fastest 4.11% CAGR during 2026-2031.

- By distribution, offline retail captured 66.58% of sales in 2025 even as online channels are set to expand at a 4.46% CAGR.

- By geography, Germany led with 22.84% revenue share in 2025; Poland is on track for the quickest 5.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Cookware Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising popularity of ceramic & PTFE-free non-stick cookware | +0.8% | EU-wide, strongest in Germany, France, Nordics | Medium term (2-4 years) |

| Home-cooking boom sustained post-COVID | +0.6% | Global, particularly strong in Western Europe | Short term (≤ 2 years) |

| Expansion of e-commerce kitchenware retail | +0.5% | EU-wide, accelerated in BENELUX, UK | Medium term (2-4 years) |

| Premiumisation fuelled by rising disposable incomes | +0.4% | Western Europe, emerging in CEE markets | Long term (≥ 4 years) |

| EU eco-design push for induction-ready cookware | +0.3% | EU-wide, strongest compliance in Germany, Netherlands | Long term (≥ 4 years) |

| Residential electrification programmes boosting all-electric cookware sets | +0.2% | Nordic countries, Germany, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising popularity of ceramic & PTFE-free non-stick cookware

Manufacturers race to bring fluorine-free coatings to market as the European Chemicals Agency evaluates a potential PFAS phase-out that could reach cookware in the next regulatory wave[1]Source: European Chemicals Agency, “Universal PFAS Restriction Proposal,” echa.europa.eu. Fraunhofer IFAM’s PLASLON® process shows that cold-plasma ceramic layers can replicate PTFE slipperiness while surviving dishwashers, giving brand owners a ready alternative. Groupe SEB already commercializes the RENEW line featuring 100% recycled aluminum bodies and bio-sourced Inoceram® surfaces to capture health-conscious households willing to pay pricing premiums. Consumer confusion persists after France opted to exempt cookware from its own PFAS ban, yet that carve-out merely delays rather than removes demand for safer chemistries. As a result, premium suppliers gain margin headroom, whereas low-cost importers scramble to validate coating safety claims under stricter “green-claim” rules.

Home-cooking boom sustained post-COVID

Hybrid work models keep Europeans in their kitchens for lunch and early-evening meals even after restaurants fully reopened in 2024. McKinsey reports that food inflation slowed to 2.4% in 2024, freeing household budgets for durable upgrades rather than emergency pantry stocking. Specialized pieces such as Dutch ovens or fermentation crocks therefore outsell expectations because social-media tutorials nudge amateur chefs toward category-specific gear that promises professional results. Brands bundle multi-piece starter sets to catch these upgrade cycles without forcing shoppers into ultra-premium price tiers. Nevertheless, bifurcation remains: high-income consumers embrace €500 cast-iron sets, but price-sensitive segments stretch legacy aluminum pans until performance visibly dips.

Expansion of e-commerce kitchenware retail

Digital penetration is forecast to top 60% of European household-appliance purchases by 2027, and cookware is tracking ahead of that curve. High-definition spin images and augmented-reality apps let shoppers test pan diameters on their actual stovetops, mitigating one of the last tactile barriers to online conversion. Direct-to-consumer webshops permit mid-sized European labels to reach Polish or Spanish cooks without paying department-store slotting fees, compressing the go-to-market timeline from seasons to weeks. However, logistics expenses for a 3 kg cast-iron braiser remain steep; “click-and-collect” models therefore flourish, blending digital browsing with brick-and-mortar pickup. Cross-border price arbitrage also forces brands to harmonize EU-wide MSRP lists, narrowing gray-import gaps exploited by third-party resellers.

Premiumisation fuelled by rising disposable incomes

Poland’s EUR 25.3 billion allocation from the EU Recovery and Resilience Plan funds energy upgrades and urban redevelopment that lift consumer confidence and discretionary spend. Rising salaries motivate middle-class households to migrate from single-wall aluminum skillets to tri-ply stainless steel lines that promise even heating and longer life. Premium storytelling around European heritage—such as Solingen steel craftsmanship—justifies retail tags that exceed EUR 150 per frying pan. Le Creuset’s continued success with USD 650 Dutch ovens demonstrates ceiling-less willingness to pay when the product symbolizes lifestyle aspiration. Yet authenticity is critical; digital natives rigorously fact-check sustainability claims before committing to high-ticket cookware.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in aluminium & stainless-steel prices | -0.7% | EU-wide, particularly affecting Germany, Italy production | Short term (≤ 2 years) |

| Mature replacement market limiting unit growth | -0.5% | Western Europe, particularly Germany, France, UK | Long term (≥ 4 years) |

| Price pressure from Asian private-label imports | -0.4% | EU-wide, strongest impact in price-sensitive segments | Medium term (2-4 years) |

| Stricter EU "green-claims" rules on PFAS coatings | -0.2% | EU-wide, immediate compliance requirements | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in aluminium & stainless-steel prices

Euro-area aluminum producer-price indices slid from 140.2 in May 2022 to 114.4 in April 2024 but still swing quarter-to-quarter, complicating margin forecasting for pot manufacturers that lock tooling schedules six months ahead[2]Source: Trading Economics, “Euro Area Aluminum Producer Prices,” tradingeconomics.com. Stainless markets add a geopolitical overlay: Scandinavian demand firms while Central European auto slowdowns crimp mill orderbooks, whipsawing surcharge formulas. Energy cost spikes—electricity futures rose 38% in Italy during 2024—further inflate smelter overheads and roll through to billet pricing. The 2026 Carbon Border Adjustment Mechanism will assign CO₂ costs to imported metals, raising landed prices for Asian inputs and potentially favoring intra-EU sourcing. Firms hedge exposure via long-term supply contracts and sharpen product-mix toward high-margin specialty lines where raw-material cost share is lower.

Mature replacement market limiting unit growth

In Western Europe, nearly every household already owns multiple pans, meaning growth relies on replacement or upgrading rather than first-time adoption. Durable stainless and enameled cast-iron lines last decades; owners report sentimental reluctance to discard well-seasoned pieces even when cosmetics fade. Ecodesign durability rules tighten further in 2025, mandating repair-friendly construction that could lengthen lifecycles beyond current 6-8-year replacement norms, capping unit demand. Brands therefore prioritize service subscriptions, accessory parts, and modular handles to monetize installed bases without accelerating waste streams. Simultaneously, marketing pivots toward efficiency benefits—faster induction boil, lower energy bills—to motivate voluntary turnover rooted in function rather than planned obsolescence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Specialized pieces elevate cooking ambitions

Specialized items accounted for only 26.42% of 2025 sales but will add USD 668 million by 2031 as home chefs seek tools that mirror restaurant technique. The European cookware market recognizes that a Japanese carbon-steel wok or a French madeleine tin solves a distinct culinary challenge unmet by generic pots, so manufacturers fill shelves with purpose-built forms in multiple diameters. Social-media creators broadcast sourdough timelines and tataki searing tips, each post quietly prescribing new hardware and raising category awareness. Retailers curate seasonal “theme corners”-Nordic baking in December, Mediterranean grilling in June-to cross-sell spice mixes and small electrics alongside niche pans. As a result, specialized lines grow volume 1.3 times faster than core sets, cushioning overall revenue when base-level replacements flatten.

Core cookware still posts the lion’s share, yet differentiation shifts from count of pieces to ergonomic refinements such as rivetless interiors that simplify cleanup or stay-cool composite handles rated for 250 °C oven use. Tri-ply stainless variants suppress hot spots on induction tops, justifying price points 40% above mono-material rivals. Stackable set designs reduce cabinet footprint, answering the urban-living pain point common in Paris or Amsterdam apartments. Energy labeling gains relevance: hangtags now display time-to-boil metrics validated under EU test protocol EN 12983, guiding eco-minded shoppers. Together, these features preserve pricing power even as base volumes mature, ensuring the European cookware market continues monetizing core lines.

By Material: Ceramic innovation challenges stainless dominance

Stainless products hold 34.92% revenue share due to scratch resistance, dishwasher safety, and aesthetic fit with modern appliances. Multi-layer clad builds marry stainless durability with aluminum heat diffusion, appealing to cooks upgrading from thin-gauge entry pieces. The European cookware market size for ceramic-coated aluminum, however, is forecast to grow 3.68% annually, spotlighting health-first shoppers and regulators targeting fluoropolymer risk. Technology convergence helps: sol-gel ceramic top-coats now achieve 50,000 abrasion cycles, extending lifespan closer to PTFE norms. Manufacturers combine recycled post-consumer beverage-can alloy with these coatings, checking both sustainability and safety boxes.

Cast iron enjoys a renaissance among hobby bakers chasing perfect crust or steakhouse-style sear. Enamel layers remove seasoning effort, making the category friendlier for first-time buyers. Carbon steel travels the opposite direction-lighter than cast iron yet still pan-to-oven capable-winning favor in professional kitchens and spilling into prosumer channels. Glass roaster sales rise where consumers trust visibility to manage browning without lid lifts, a small but growing niche. Meanwhile, copper settles into ultra-premium status, buoyed by television chefs but limited by maintenance and price; a 28 cm tin-lined pan can top USD 400, confining demand to enthusiasts.

By End User: Foodservice rebound lifts commercial lines

The commercial channel’s 4.11% CAGR reflects restaurants re-opening and refurbishing after pandemic-era cash preservation. European cookware market suppliers equip cloud-kitchen networks scaling across urban nodes that favor induction due to ventilation savings. Chain operators standardize supplier lists, guaranteeing repeat orders for compliant SKUs across 50-plus outlets, smoothing revenue profiles for manufacturers. Catering tender documents increasingly require proof of PFAS-free coatings and dishwasher endurance beyond 1,000 cycles, ratcheting specification complexity that favors established players. Institutional users like hospitals and schools prioritize stainless stockpots sized for 100-portion batches, a volume niche unserved by consumer brands yet lucrative for firms with deep-draw presses.

Residential demand remains the bedrock, delivering 69.45% of sales alongside emotional branding opportunities unavailable in the utilitarian B2B arena. Gift registries and holiday-season promotions anchor volume spikes, while influencer tie-ins foster year-round engagement. “Kitchen hack” viral clips reveal how a single sauté pan can function as grill-press or pizza steel, stretching perceived value and reinforcing manufacturer claims of versatility. Post-pandemic nesting translates into weekend recipe experimentation that often triggers mid-tier upgrades rather than luxury splurges, keeping the middle of the price pyramid well-populated. Finally, repair-oriented programs such as lifetime handle replacement maintain brand loyalty and extend revenue per unit beyond initial sale.

By Distribution Channel: Omnichannel maturity defines sales paths

Offline retail controlled 66.58% of 2025 sales because buyers still lift pans to judge heft before swiping a card. Department stores dedicate demonstration corners where chefs cook lunch-hour samples, linking aroma with purchase intent. Yet online baskets grow bigger: European cookware market shoppers who start on a brand’s website convert at 3.4% rates when 360-degree photos accompany technical specs, double the rate of static listings. Live-stream events mimic in-store demos, with chat-led Q&A that overcomes last-mile hesitation. Freight innovations such as lightweight nested packaging shave 18% off parcel weight, narrowing cost gaps to apparel shipping.

Marketplace giants remain price battlegrounds, prompting brands to open direct-to-consumer portals that offer color exclusives or engraving services unavailable through third parties. Click-and-collect hubs inside hypermarkets address return anxiety while boosting impulse add-on sales in adjacent aisles. B2B portals streamline specification purchase; a hotel group can reorder 120 identical sauté pans in three clicks, feeding ERP systems without phone calls. Omnichannel loyalty programs stitch data: scanning a receipt in-store credits points in the same wallet used online, reinforcing brand echo across touchpoints. Europe’s Digital Services Act intensifies policing of counterfeit listings, offering legitimate manufacturers cleaner marketplace real estate.

Geography Analysis

Germany’s 22.84% revenue share springs from entrenched manufacturing clusters in Baden-Württemberg and Bavaria that export engineering credibility onto shop floors nationwide. Domestic brands such as WMF and Fissler hold household recognition topping 90%, allowing them to command premium shelf space even during consumer-confidence dips. Induction adoption tops 60% of new residential builds, shortening replacement cycles as incompatible pans retire early. Federal climate incentives co-fund kitchen electrification, further propelling high-spec tri-ply sets. Supply-chain near-shoring under the Carbon Border Adjustment Mechanism could enhance home-grown cost advantages once CO₂ tariffs apply to Asian metal inputs in 2026.

Poland’s 5.12% forecast CAGR outpaces the European cookware market average as EU resilience funds increase household disposable income by EUR 640 per capita between 2023 and 2025. Retail modernization substitutes Soviet-era bazaars with hypermarkets and e-commerce lockers that showcase branded cookware previously inaccessible outside Warsaw. Foodservice expansion follows tourism rebounds-2024 visitor numbers climbed 12% year on year-boosting commercial stock-pot and bakeware orders for hotel kitchens. Local aluminum foundries in Podkarpackie province begin contract casting for Western European labels, anchoring value-chain jobs regionally. Government apprenticeship programs fortify metalworking skills pipelines, lowering production costs that feed back into competitive retail prices.

France, Spain, Italy, BENELUX, and the Nordics together form a mature yet premium-oriented bloc where upgrades hinge on style, sustainability, and kitchen fashion cycles. France’s decision to exclude cookware from its 2024 PFAS restriction offers a regulatory breather, yet leading suppliers still advance ceramic lines to pre-empt future scope expansion. Spain’s energy-efficiency tax rebates cover induction cooktop purchases and implicitly stimulate compatible pan replacements, while Italy’s artisan cast-iron workshops differentiate via localized enameling hues tied to regional cuisine narratives. BENELUX households, characterized by compact kitchens, gravitate toward space-saving stackables that command margins rivaling full-size sets elsewhere. Nordic consumers display the highest willingness to pay for recycled-content claims, making the region a test bed for circular-economy pilots such as lifetime trade-in vouchers.

Competitive Landscape

Market concentration sits in a moderate band where the top five brands control major market share in 2024, leaving space for challenging labels to flourish in niches like specialty bakeware or carbon-steel woks. Groupe SEB couple’s broad portfolio depth—Tefal, WMF, All-Clad—with pan-European distribution agreements, allowing simultaneous positioning from entry-level aluminum to high-end copper. Meyer Group leverages Asian manufacturing scale yet fronts European design centers in Belgium to reassure retailers on quality stewardship. Fissler and Zwilling stress Solingen heritage and lifetime-repair guarantees, winning loyalty among eco-minded consumers wary of disposability culture.

Strategic consolidation continued in 2025, notably Kartesia’s acquisition of International Cookware Group, guardian of the Pyrex brand, which extends the buyer’s reach into heat-resistant glass and unlocks cross-category bundling with metal lids. Ardian’s pursuit of Robot-Coupe and Magimix aligns small-appliance platforms with cookware ecosystems, enabling countertop-to-cooktop upsell flows[4]Source: Drax Executive Search, “Ardian Acquires Robot-Coupe and Magimix,” drax.com. On the innovation front, Tefal’s 2025 “pan-take-back” program promises to recycle 20 million units by 2027, a headline that establishes sustainability credentials while feeding secondary aluminum supply loops. Fiskars, after splitting tableware from cutting tools, dedicates new capital to smart-sensor-embedded pans that relay exact surface temperature to mobile apps, bridging cookware with IoT kitchens.

Asian challengers exploit private-label contracts, shipping container loads of low-cost pans that European hypermarkets badge under house names. Their share inches upward yet faces headwinds from forthcoming CO₂ levies on imported metal and EU enforcement of supply-chain due-diligence rules. European mid-caps retaliate by localizing limited-edition colorways and seasonal shapes that mass OEMs cannot emulate quickly. Start-ups tackle single-pain-point innovation—detachable walnut handles, graphene composite cores—securing crowdfunding millions before scaling via contract production. Overall, sustained brand investment in manufacturing transparency, coating safety, and circular logistics defines the durable moat in a market where cost pressure alone no longer decides.

Europe Cookware Industry Leaders

Groupe SEB

Meyer Group Ltd.

Fiskars Group

Zwilling J.A. Henckels AG

Le Creuset Group AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Tefal launched the world’s first large-scale pan recycling program with French retailers, targeting 20 million utensil collections by 2027.

- June 2025: Tefal and Paul Bocuse introduced a premium cookware collection featuring French-made stainless steel and aluminum pieces set for September 2025 release.

- April 2025: Fiskars Group finalized the separation of business areas, unlocking EUR 12 million annual savings and sharpening its focus on cooking categories.

- July 2024: Ardian opened exclusive talks to acquire a majority stake in Robot-Coupe and Magimix, consolidating professional and consumer appliance leadership.

Europe Cookware Market Report Scope

Cookware refers to a variety of cooking vessels, such as pots, pans, and baking dishes, used to prepare food. These items are essential in both residential and commercial kitchens, playing a crucial role in meal preparation. The European cookware market is segmented by product, materials, distribution channels, and country. By product, the market is segmented into pots and pans, cooking racks, cooking tools, microwave cookware, and pressure cookers. By materials, the market is segmented into stainless steel, aluminum, glass, and other materials (ceramic). By distribution channels, the market is segmented into hypermarkets and supermarkets, specialty stores, online, and other distribution channels (local dealers). By country, the market is segmented into Germany, the United Kingdom, France, Poland, Italy, and the Rest of Europe. The report offers market size and forecasts for the European cookware market in value (USD) for all the above segments.

By Product Type (Value)

| Core Cookware | Pans (Fry/Saute, Grill, Wok/Kadhai, Crepe) |

| Pots (Sauce, Stock, Dutch Oven) | |

| Pressure Cookers & Steamers | |

| Cookware Sets | |

| Specialized Cookware | Dutch Ovens & Casseroles |

| Specialty Cookware (Idli, Appam, BBQ Grill Pan, etc.) | |

| Bakeware (Ovenware, Muffin trays, Cake tins, etc.) | |

| Accessories (Lids, Handles) |

By Material (Value)

| Stainless Steel |

| Aluminium |

| Cast Iron |

| Carbon Steel |

| Copper |

| Ceramic/Glass |

| Silicone |

| Other Coated Substrates |

By End User (Value)

| Residential |

| Commercial (HoReCa, Institutional, Catering) |

By Distribution Channel (Value)

| Offline Retail | Super/Hypermarkets |

| Department Stores | |

| Specialty Stores | |

| Online | E-commerce Marketplaces |

| Brand Webshops | |

| B2B / Direct Sales |

By Country

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Product Type (Value) | Core Cookware | Pans (Fry/Saute, Grill, Wok/Kadhai, Crepe) |

| Pots (Sauce, Stock, Dutch Oven) | ||

| Pressure Cookers & Steamers | ||

| Cookware Sets | ||

| Specialized Cookware | Dutch Ovens & Casseroles | |

| Specialty Cookware (Idli, Appam, BBQ Grill Pan, etc.) | ||

| Bakeware (Ovenware, Muffin trays, Cake tins, etc.) | ||

| Accessories (Lids, Handles) | ||

| By Material (Value) | Stainless Steel | |

| Aluminium | ||

| Cast Iron | ||

| Carbon Steel | ||

| Copper | ||

| Ceramic/Glass | ||

| Silicone | ||

| Other Coated Substrates | ||

| By End User (Value) | Residential | |

| Commercial (HoReCa, Institutional, Catering) | ||

| By Distribution Channel (Value) | Offline Retail | Super/Hypermarkets |

| Department Stores | ||

| Specialty Stores | ||

| Online | E-commerce Marketplaces | |

| Brand Webshops | ||

| B2B / Direct Sales | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the European cookware market?

The market is valued at USD 7.94 billion in 2026 and is forecast to reach USD 9.48 billion by 2031.

Which country leads cookware sales in Europe?

Germany tops revenue with 22.84% share owing to manufacturing heritage and high induction-cooktop adoption.

Which segment is growing fastest?

Specialized cookware pieces such as Dutch ovens and niche bakeware are projected to expand at a 4.85% CAGR through 2031.

How quickly are online cookware sales rising?

E-commerce is set to grow at a 4.46% CAGR, benefiting from augmented-reality visualization and direct-to-consumer strategies.

What regulatory trend will affect future material choices?

EU initiatives targeting PFAS and mandating eco-design durability are steering manufacturers toward ceramic and recycled-metal solutions.

Page last updated on: