Europe Immersive Entertainment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

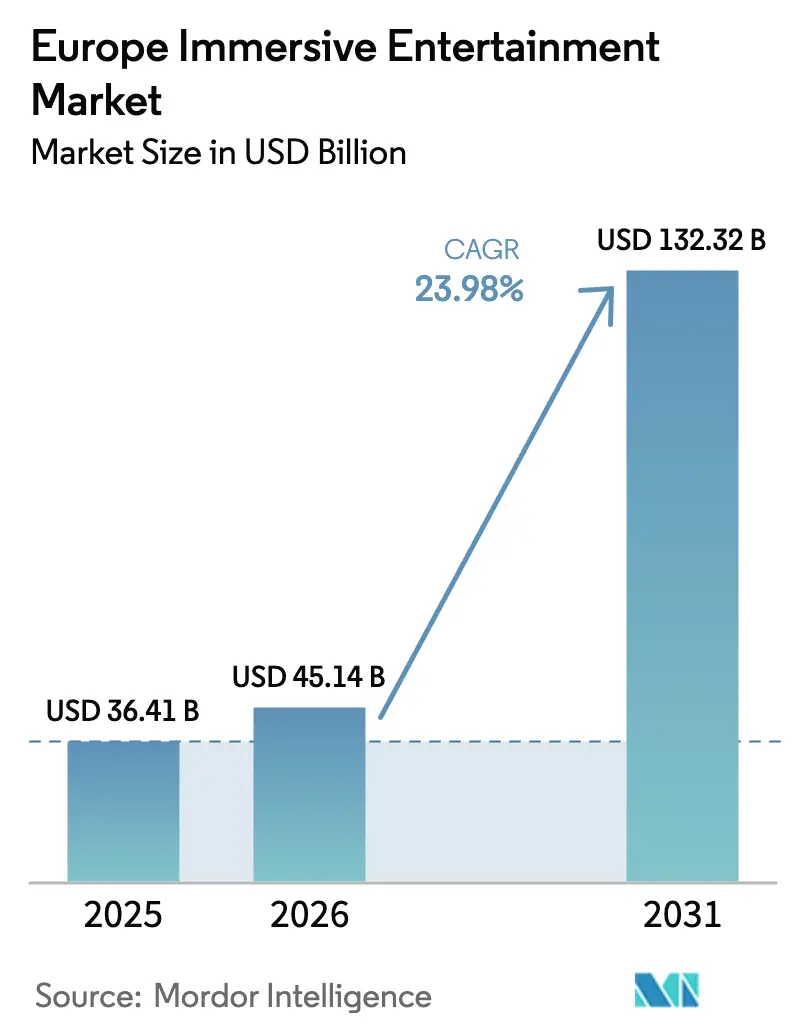

| Base Year Market Size (2025) | USD 36.41 Billion |

| Market Size (2026) | USD 45.14 Billion |

| Market Size (2031) | USD 132.32 Billion |

| Growth Rate (2026 - 2031) | 23.98% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Immersive Entertainment Market Analysis by Mordor Intelligence

The Europe immersive entertainment market size was valued at USD 36.41 billion in 2025 and estimated to grow from USD 45.14 billion in 2026 to reach USD 132.32 billion by 2031, at a CAGR of 23.98% during the forecast period (2026-2031). Rapid roll-out of 5G in Western Europe, surging investments in location-based virtual-reality attractions, and renewed museum footfall after pandemic-era lows are expanding both consumer reach and frequency of visits. Government cultural-innovation funds in France, Germany, and the Nordics continue to channel grants toward multi-sensor installations that blend art, storytelling, and spatial computing. Brands in automotive, luxury fashion, and beverages are sponsoring pop-up mixed-reality showrooms, widening revenue beyond ticket sales. At the same time, content studios are shifting to real-time engines to deliver episodic experiences that increase repeat traffic and subscription uptake, reinforcing the growth path of the Europe immersive entertainment market.

Key Report Takeaways

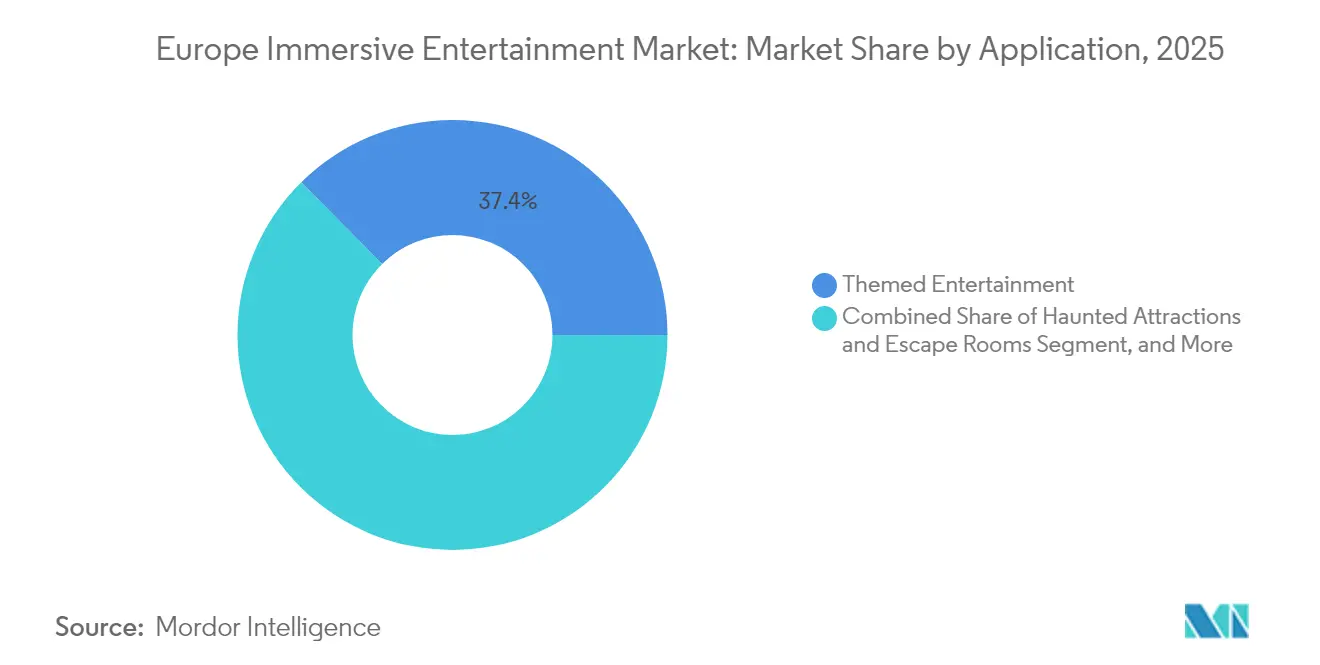

- By application, themed entertainment commanded 37.42% of the Europe immersive entertainment market share in 2025, whereas experiential art museums are projected to expand at a 27.15% CAGR through 2031.

- By technology, virtual reality held 54.20% revenue share in 2025, while mixed reality is forecast to advance at a 30.05% CAGR to 2031.

- By offering, hardware generated 62.35% of 2025 revenue; services are set to post a 28.1% CAGR between 2026-2031.

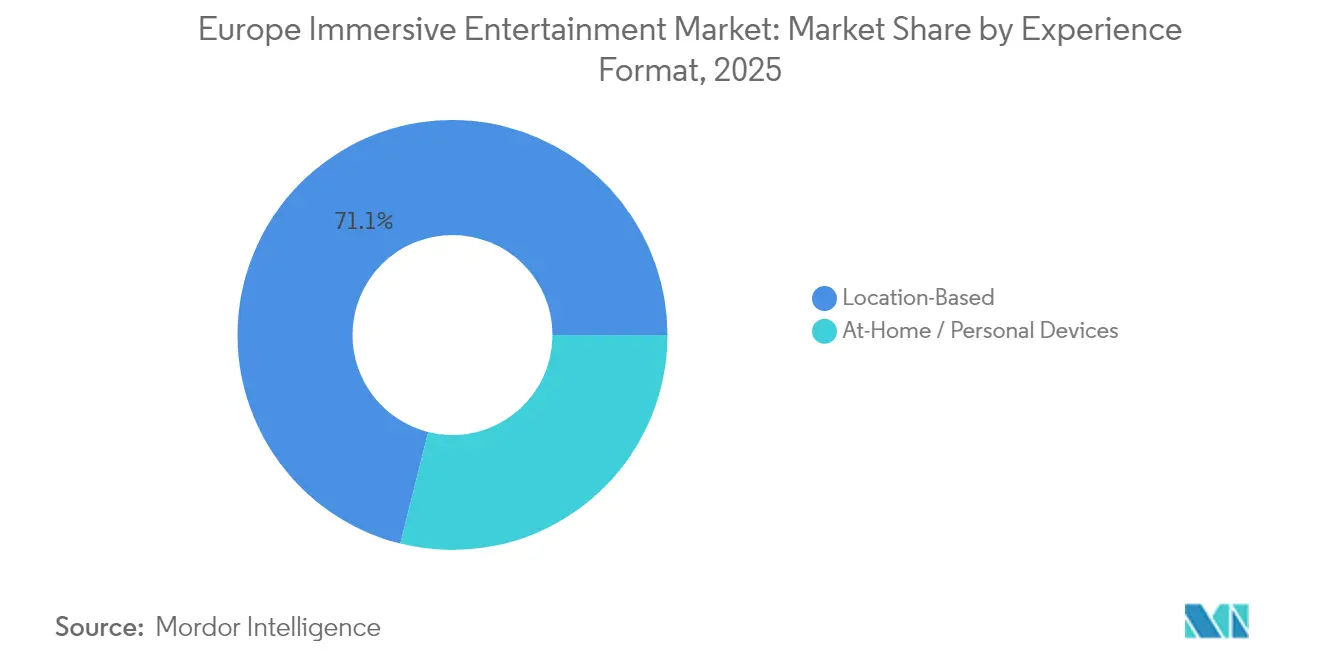

- By experience format, location-based venues captured 71.10% of 2025 spending; at-home/personal devices are poised for a 29.45% CAGR.

- By revenue model, ticket sales delivered 66.25% of 2025 inflows; subscriptions and memberships are likely to climb at a 31.85% CAGR.

- By geography, the United Kingdom contributed 21.60% of 2025 revenue, but Spain is expected to grow at a 26.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global valuation is built by aggregating outputs from multiple regions, with Europe forming one of the important contributors. Mordor Intelligence's global immersive entertainment market size report represents that cumulative total.

Europe Immersive Entertainment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising location-based VR installations across major EU capitals | +5.80% | United Kingdom, France, Germany, Spain, Italy | Medium term (2-4 years) |

| 5G roll-out enabling untethered XR experiences in Western Europe | +4.20% | Germany, United Kingdom, France, Spain, Italy | Long term (≥ 4 years) |

| Government-backed digital-culture funds | +3.70% | France, Germany, Nordics, Spain | Medium term (2-4 years) |

| Corporate sponsorship of immersive brand activations | +2.90% | Germany, United Kingdom, France, Italy | Short term (≤ 2 years) |

| Growing museum attendance recovery post-COVID | +2.10% | United Kingdom, France, Italy, Spain | Short term (≤ 2 years) |

| EU Horizon-Europe grants driving immersive technology R&D | +1.80% | Pan-European; focus on Germany, France, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising location-based VR installations across major EU capitals

Flagship arenas in London, Paris, Berlin and Madrid combine free-roam tracking, haptic vests and projection-mapped scenery, lifting dwell time and F&B spend. Operators such as Sandbox VR and Zero Latency publish satisfaction scores above 90%, drawing new audiences and validating revenue splits that anchor the Europe immersive entertainment market. Repeat traffic flows from IP-licensed titles like Star Trek, with venues franchised into Tier-2 cities to broaden reach.

5G roll-out enabling untethered XR experiences in Western Europe

Mid-band 5G now covers 81% of EU urban corridors, letting headsets offload compute to edge clouds and eliminating heavy backpacks. Latency improvements enable synchronous multiplayer quests and real-time photogrammetry overlays, strengthening premium pricing power inside the Europe immersive entertainment market. [1]GSMA, “5G Adoption in Europe 2024,” gsma.com

Government-backed digital-culture funds

France’s Fonds d’Expériences Immersives awards up to EUR 3 million (USD 3.51 million) per project, underwriting projection-mapped heritage walks and training programs for real-time artists. Comparable schemes in Germany and the Nordics prolong funding visibility, steering both public and private capital toward the Europe immersive entertainment market. [2]Ministère de la Culture, “Fonds d’Expériences Immersives—2025 Awards,” culture.gouv.fr

EU Horizon-Europe grants driving immersive technology R&D

Horizon-Europe allocates EUR 95.5 billion (USD 111.68 billion) for 2025-2027, earmarking XR for cultural inclusion and industrial training. University-spin-off prototypes flow into commercial pilots, deepening the technology pipeline that sustains the Europe immersive entertainment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented safety and building codes for mixed-reality attractions | –2.3% | Historic city centers | Medium term (2-4 years) |

| High up-front CAPEX for multi-sensor installations in historic venues | –1.9% | Italy, France, Spain, United Kingdom | Short term (≤ 2 years) |

| Limited consumer awareness outside Tier-1 cities | –1.4% | Eastern Europe, rural regions | Short term (≤ 2 years) |

| Talent shortage in real-time 3-D content creation | –1.2% | Pan-European creative hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented safety and building codes for mixed-reality attractions

Municipal disparities on laser limits, headset hygiene and evacuation paths extend permitting cycles by up to nine months, increasing sunk costs and slowing roll-outs that would otherwise accelerate the Europe immersive entertainment market.

High up-front CAPEX for multi-sensor installations in historic venues

Structural preservation mandates non-invasive rigs and climate controls, lifting capital needs above EUR 4 million (USD 4.68 million) per site. Only chains backed by institutional capital can absorb such risk, leaving regional white space inside the Europe immersive entertainment market. [3] ICOMOS, “Guidelines for Heritage-Site XR Installations 2025,” icomos.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Themed attractions anchor demand while museums accelerate engagement

Themed entertainment parks, escape rooms and haunted mazes generated 37.42% of 2025 revenue, confirming their status as the largest slice of the Europe immersive entertainment market. Operators retrofit dark rides with head-tracked surfaces and scent emitters, lifting per-capita spend by 17%. Significantly, this cohort’s 2025 revenue equals USD 13.62 billion, underscoring its hold on the Europe immersive entertainment market size. Cross-IP seasons—from streaming dramas to game franchises—encourage return visits every quarter.

Experiential art museums will expand at a 27.15% CAGR to 2031, the fastest within applications. Over 350 sites were operational by end-2024, and projects such as “Horizon of Khufu” recorded 2 million visitors in 14 months, a validation that augments the Europe immersive entertainment market. These venues use 270-degree walls, ambisonic sonics and gesture-based canvases that convert passive viewing into participatory discovery, adding membership tiers and digital souvenir NFTs.

Immersive theatres combine volumetric sets and live performers, offering rotating repertory that drives subscription bundles linking multiple stages. Haunted attractions intensify by layering vibration floors and micro-dosed scent bursts, attracting millennials seeking elevated thrill metrics. Exhibitions deploy temporary domes to overlay historical artifacts with CGI reconstructions, extending residency periods and capturing new sponsorship pools across the Europe immersive entertainment market.

By Technology: VR dominance gives way to MR momentum

Virtual reality still commands 54.20% of 2025 spend, equating to about USD 19.74 billion of Europe immersive entertainment market size. Tethered and mobile HMDs cover everything from zombie shooters to children’s animation, and headset subsidies by platform owners facilitate rapid refresh cycles.

Mixed reality, however, is projected to grow at 30.05% CAGR, the fastest of all stacks. Optical see-through headsets overlay historical ruins with holographic storyboards, making them ideal for UNESCO sites subject to strict preservation codes. Pilot deployments at the Colosseum and York Minster produced satisfaction scores above 90%, paving the path for scaling and shifting Europe immersive entertainment market share toward MR experiences. Augmented reality continues to proliferate in retail and tourism; projection mapping and holography deliver spectacle without headgear; while spatial-audio arrays and ambisonics elevate emotional believability, underscoring audio’s pivotal role.

By Offering: Hardware heavy yet services soar

Hardware contributed 62.35% of 2025 revenue, driven by HMDs, 4K projectors, depth-sensing cameras and motion floors. Suppliers release annual optical improvements and field-of-view gains, refreshing the Europe immersive entertainment market. Bundled trade-ins lift replacement rates, and premium lenses push ASPs higher.

Services will post a 28.1% CAGR through 2031, outpacing hardware on the back of design consulting, integration and managed operations contracts. Operators outsource calibration, content scheduling and predictive maintenance, reducing downtime and boosting gross margins. Real-time engines sold on consumption-based licenses tie costs to visitor footfall, easing cash-flow for independents and reinforcing recurring revenue architecture within the Europe immersive entertainment market.

Software tools—3-D modeling suites, virtual-production toolsets and analytics dashboards—form the connective tissue binding multi-sensor rigs. As pipelines converge on open standards, vendor lock-in risk declines, encouraging multi-studio collaboration that enriches content breadth.

By Experience Format: Social venues rule but home adoption accelerates

Location-based venues captured 71.10% of 2025 spending, underlining their primacy in the Europe immersive entertainment market. Shared rituals, cinematic scale and curated hospitality experiences keep group bookings high. Operators add themed cafés, branded retail corners and after-dark DJ sets, pushing average spend per head to USD 48.

At-home consumption will grow at 29.45% CAGR. Standalone HMD prices dropped below EUR 300 (USD 350.83) in late-2024, and cloud-rendered visuals minimize local processing. Cross-device passes let users unlock episodic chapters at home that extend storylines first tasted onsite, creating a continuous engagement loop that enlarges the Europe immersive entertainment market size for living-room formats.

By Revenue Model: Ticket sales prevail while subscriptions multiply

Ticket sales formed 66.25% of 2025 revenue—USD 24.12 billion—validating their continued centrality to the Europe immersive entertainment market. Dynamic pricing algorithms lifted peak-hour yields without cannibalizing volume. Yet subscriptions and memberships will climb at a 31.85% CAGR: multi-venue passes, queue-skip perks and exclusive digital drops boost stickiness. This recurring model stabilizes cash flow and permits content planning horizons of up to five years, a structural positive for the Europe immersive entertainment market.

In-experience purchases—avatar skins, behind-the-scenes scenes and commemorative NFTs—add incremental yield. Sponsorship and advertising slots leverage immersive dwell times that exceed 40 minutes per visitor, delivering high-impact brand recall.

Geography Analysis

The United Kingdom generated 21.60% of revenue in 2025, reflecting London’s cluster of flagship VR centres, a robust indie-studio scene and tax incentives for creative R&D. The UK entertainment and media sector is projected to surpass GBP 100 billion (USD 135.03 billion) in 2025, a trajectory that cements national leadership within the Europe immersive entertainment market. Public-private schemes offset business-rate hikes, while Bristol and Sheffield anchor 5G testbeds that feed developer ecosystems.

Germany and France together contribute more than one-third of regional revenue. Berlin’s start-up density and Bavaria’s XR Hub attract venture capital, while Paris benefits from the Fonds d’Expériences Immersives that underwrites mixed-reality storytelling. France’s cultural policy and Germany’s industrial heritage museums both deploy MR overlays, lifting overall Europe immersive entertainment market share for central Europe.

Spain is forecast to grow at 26.95% CAGR, driven by tourism-focused XR tours that illuminate Gaudí landmarks and Moorish palaces. City councils convert public squares into projection-mapping canvases for nightly shows, and football clubs bundle holographic locker-room tours into fan packages. Nordic nations and the Netherlands score high on broadband penetration and design-thinking pedagogy, ensuring swift adoption of spatial computing. Italy balances heritage preservation with cutting-edge optics; pilot holographic operas in Florence reveal crossover potential. Eastern European markets start from lower bases but court international chains with low lease costs, expanding the geographical footprint of the Europe immersive entertainment market.

Coverage of the immersive entertainment market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Latin America, Asia, and North America.

Competitive Landscape

Global tech giants Meta, Microsoft and Sony anchor the hardware and platform lattice. Their subsidies on consumer headsets build user funnels that funnel into location-based attractions, entwining device ecosystems with the Europe immersive entertainment market. Qualcomm’s chipset cadence fuels lighter optics and longer battery life, helping venues lower staffing costs through reduced headset swaps.

Regional venue chains—Merlin Entertainments, Sandbox VR, Zero Latency and Immersive Gamebox—deploy franchise and JV models to scale quickly. Sandbox VR opened nine EU sites in 2024 and targets 40 by 2027. Dreamscape Immersive differentiates with Hollywood IP narratives, while Darkfield experiments with blindfolded spatial-audio horror pods. These expansions diversify content formats and strengthen the Europe immersive entertainment market.

Boutique studios such as Felix & Paul create cinematic VR, partnering with telecoms on bandwidth-stress demos. Magic Leap supplies optical see-through headsets for guided museum tours, a niche that signals enterprise convergence. Cross-licensing and engine interoperability agreements emerge as must-have safeguards, reducing fragmentation and accelerating content throughput in the Europe immersive entertainment market.

Europe Immersive Entertainment Industry Leaders

Meta Platforms, Inc. (Meta)

Microsoft Corporation

HTC Corporation

Barco NV

Magic Leap, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Comcast NBCUniversal confirmed a Universal-branded theme park in Bedford, UK, with construction slated for 2026.

- March 2025: Samsung announced Project Moohan, a mixed-reality headset co-developed with Qualcomm and Google, scheduled for late-2025.

- February 2025: The European Commission adopted its Web 4.0 and virtual-worlds strategy to foster an open, secure XR landscape.

- January 2025: UBS Digital Art Museum partnered with teamLab to open a permanent immersive gallery in Hamburg.

Europe Immersive Entertainment Market Report Scope

Immersive Experience describes how deeply an audience connects with a narrative and its crafted reality or fictional universe. This term applies to various media, including film, video games, virtual and augmented reality, and interactive theater.

The European immersive entertainment market is segmented by application (themed entertainment, haunted attractions, and escape rooms, immersive theaters, experiential art museums, and others), by geography (United Kingdom, Germany, France, Rest of Europe). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Themed Entertainment |

| Haunted Attractions and Escape Rooms |

| Immersive Theatres |

| Experiential Art Museums |

| Exhibitions and Other Events |

| Virtual Reality (VR) |

| Augmented Reality (AR) |

| Mixed Reality (MR) |

| Projection Mapping and Holography |

| Spatial-Audio and Ambisonics |

| Hardware | Head-Mounted Displays (HMDs) |

| Projection and Display Systems | |

| Motion Capture and Tracking | |

| Haptic Interfaces | |

| Immersive-Audio Systems | |

| Software | Real-Time Engines |

| 3-D Modelling and Design Tools | |

| Experience-Management Platforms | |

| Services | Design and Consulting |

| Installation and Integration | |

| Operations and Maintenance |

| Location-Based (Out-of-Home) |

| At-Home / Personal Devices |

| Ticket Sales |

| Subscriptions and Memberships |

| In-experience Purchases |

| Sponsorship and Advertising |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| Netherlands |

| Nordics |

| Rest of Europe |

| By Application | Themed Entertainment | |

| Haunted Attractions and Escape Rooms | ||

| Immersive Theatres | ||

| Experiential Art Museums | ||

| Exhibitions and Other Events | ||

| By Technology | Virtual Reality (VR) | |

| Augmented Reality (AR) | ||

| Mixed Reality (MR) | ||

| Projection Mapping and Holography | ||

| Spatial-Audio and Ambisonics | ||

| By Offering | Hardware | Head-Mounted Displays (HMDs) |

| Projection and Display Systems | ||

| Motion Capture and Tracking | ||

| Haptic Interfaces | ||

| Immersive-Audio Systems | ||

| Software | Real-Time Engines | |

| 3-D Modelling and Design Tools | ||

| Experience-Management Platforms | ||

| Services | Design and Consulting | |

| Installation and Integration | ||

| Operations and Maintenance | ||

| By Experience Format | Location-Based (Out-of-Home) | |

| At-Home / Personal Devices | ||

| By Revenue Model | Ticket Sales | |

| Subscriptions and Memberships | ||

| In-experience Purchases | ||

| Sponsorship and Advertising | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Nordics | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe immersive entertainment market?

In 2026 the market is valued at USD 45.14 billion.

How fast will the Europe immersive entertainment market grow?

It is expected to register a 23.98% CAGR between 2026 and 2031.

Which application segment leads the Europe immersive entertainment market?

Themed entertainment leads with 37.42% revenue share in 2025, while experiential art museums are the fastest-growing.

What technology is gaining momentum after VR?

Mixed reality is projected to expand at a 30.05% CAGR through 2031, the highest among technologies.

How important are subscriptions compared with ticket sales?

Ticket sales still dominate, but subscriptions and memberships will grow at 31.85% CAGR, reshaping revenue models.

Which country shows the fastest growth outlook?

Spain is forecast to expand at a 26.95% CAGR over 2026-2031 due to strong tourism-oriented XR investments.

Page last updated on: