Europe Security Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

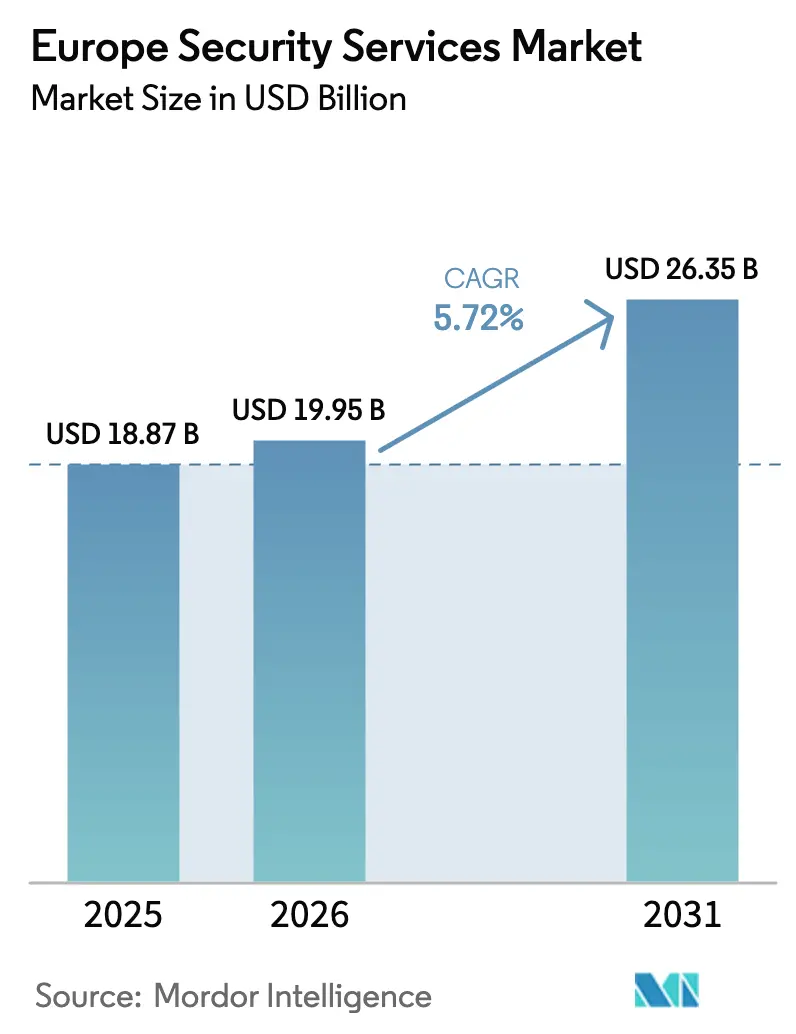

| Base Year Market Size (2025) | USD 18.87 Billion |

| Market Size (2026) | USD 19.95 Billion |

| Market Size (2031) | USD 26.35 Billion |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

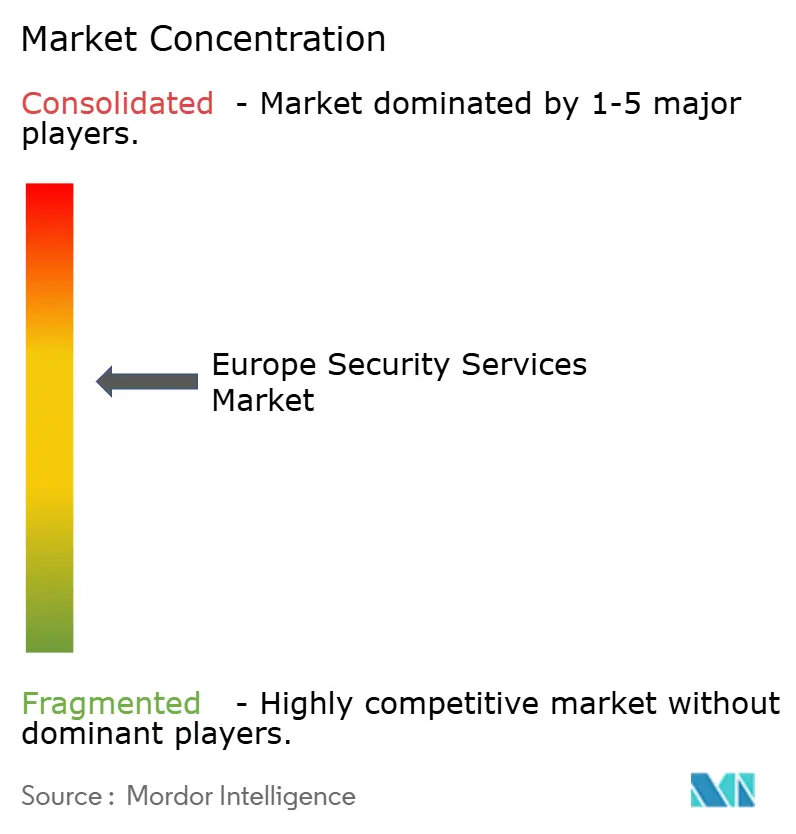

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Security Services Market Analysis by Mordor Intelligence

The Europe security services market size in 2026 is estimated at USD 19.95 billion, growing from 2025 value of USD 18.87 billion with 2031 projections showing USD 26.35 billion, growing at 5.72% CAGR over 2026-2031. Demand accelerates as the NIS2 Directive broadens mandatory cyber-risk budgets across 18 critical sectors, while NATO’s expanded cyber-defence spending pledge secures a long-term public-sector revenue stream. Organisations now treat operational technology, supply-chain assurance and post-quantum cryptography as integral elements of enterprise protection, boosting uptake of consulting, threat-intelligence and managed detection offerings. Growing cloud adoption among European SMEs, combined with persistent cyber-skills shortages, shifts preference from technology ownership to outcome-based managed security contracts. At the same time, consolidation among service providers—exemplified by Sophos’s integration of Secureworks’ XDR assets—signifies a competitive race to build scale, AI-based analytics and regulatory expertise within one platform.

Key Report Takeaways

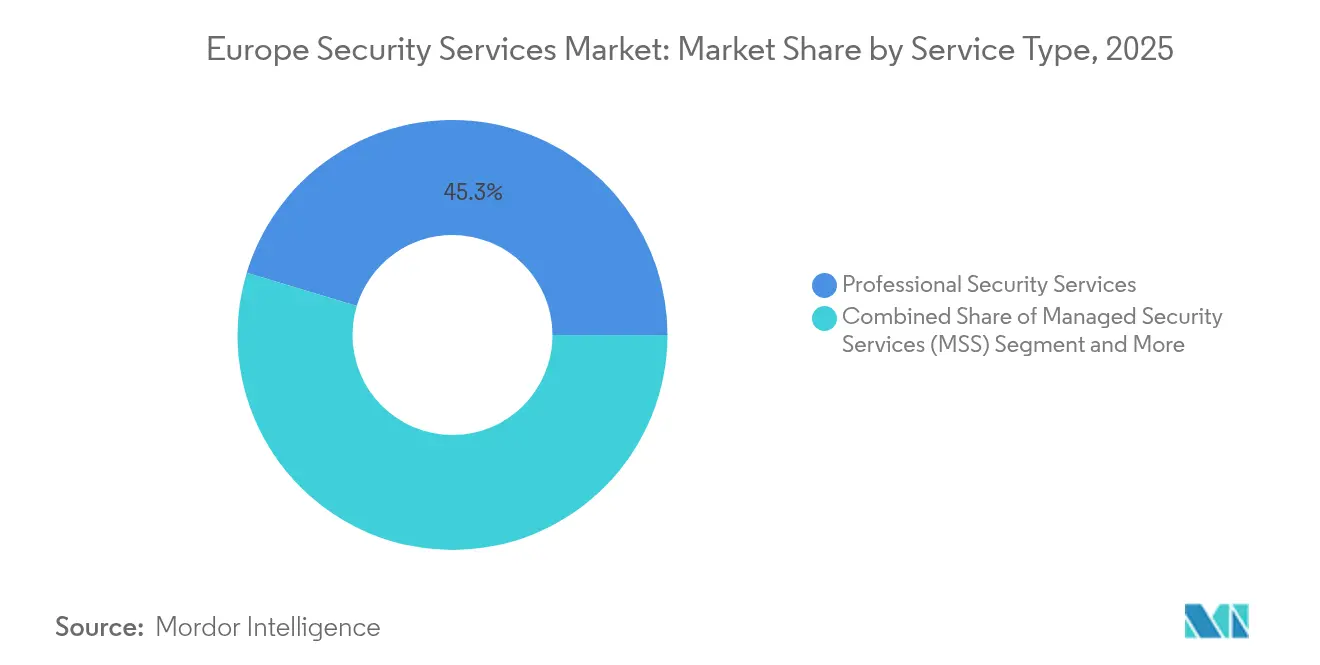

- By service type, professional security services led with 45.32% of Europe security services market share in 2025, whereas managed security services are forecast to expand at a 6.41% CAGR through 2031.

- By security domain, cyber security services accounted for 63.12% share of the Europe security services market size in 2025 and are growing at a 6.32% CAGR to 2031.

- By deployment mode, on-premise solutions held 57.25% revenue share in 2025; cloud deployment is advancing at a 6.03% CAGR on the back of SME multi-cloud adoption.

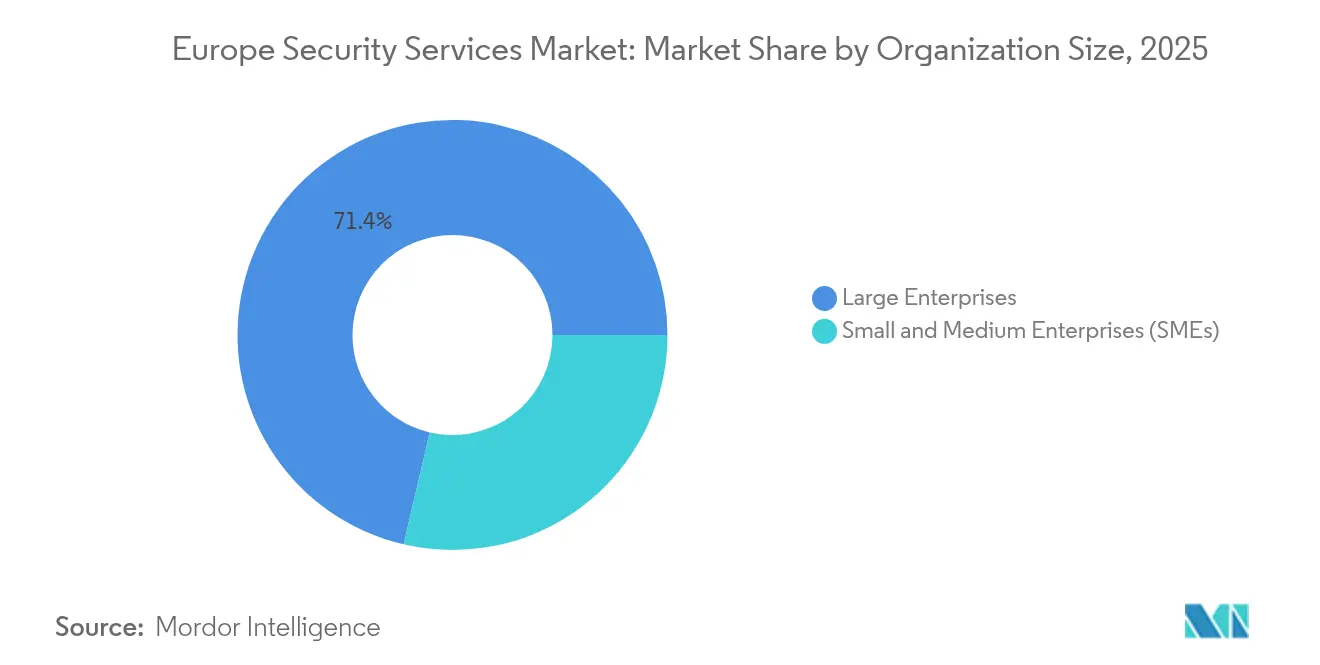

- By organisation size, large enterprises captured 71.35% share of the Europe security services market size in 2025, while SMEs post the highest CAGR at 6.22% through 2031.

- By end-user industry, BFSI dominated with 24.12% market share in 2025; healthcare is projected to record the fastest 5.82% CAGR through 2031.

- By country, the United Kingdom contributed 21.68% of 2025 revenue; France is on track for the quickest 6.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe contributes to a system defined not by any single geography but by the interaction of many. The global security services market data by Mordor Intelligence represents that combined structure.

Europe Security Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-wide NIS2 Directive Enforcing Mandatory Cyber-Risk Budgets | +1.2% | EU-wide, strongest in Germany, France, Netherlands | Medium term (2-4 years) |

| AI-Driven Attacks on European Manufacturing Supply-Chains Escalating SOC Demand | +0.8% | Germany, Italy, France manufacturing hubs | Short term (≤ 2 years) |

| State-Sponsored Breaches Targeting Energy Utilities Post-Ukraine War | +0.6% | Eastern EU, Nordic region, UK | Long term (≥ 4 years) |

| Multi-Cloud Adoption by European SMEs to Meet GDPR Enhancing MSS Uptake | +0.9% | Western EU, particularly UK, Germany, France | Medium term (2-4 years) |

| Cyber-Skills Gap Driving Outsourcing of 24/7 SOCs Across EU | +0.7% | EU-wide, concentrated in Nordics, Benelux | Long term (≥ 4 years) |

| PSD2/Open-Banking APIs Expanding Attack Surface in Digital Banking | +0.5% | EU financial centers: London, Frankfurt, Paris | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU-wide NIS2 Directive Enforcing Mandatory Cyber-Risk Budgets

NIS2’s October 2024 go-live raised average cyber spend to 9% of IT budgets and extended obligations to medium-sized firms, broadening the Europe security services market by thousands of new compliance-bound customers.[1]European Union Agency for Cybersecurity, “NIS Investments 2024,” enisa.europa.eu Fines of up to EUR 10 million (USD 10.8 million) push boards to adopt managed detection, threat-intelligence and third-party risk monitoring. German enterprises alone earmarked EUR 11.2 billion (USD 12.1 billion) for IT security in 2024, a 13.8% jump linked largely to NIS2 preparation.

AI-Driven Attacks on European Manufacturing Supply Chains Escalating SOC Demand

In 2024, 68 OT incidents with physical consequences hit factories, a 19% rise year on year, prompting manufacturers to commission 24/7 SOCs that merge IT and OT telemetry.[2]Waterfall Security Solutions, “2024 Threat Report,” waterfall-security.com Orange Cyberdefence notes hacktivists account for 25% of serious OT attacks, underscoring the need for managed detection services capable of real-time correlation between cyber and physical events.

State-Sponsored Breaches Targeting Energy Utilities Post-Ukraine War

Weekly cyber strikes on European utilities have doubled since early 2024, and 71% of sector executives expect bigger security budgets in 2025. The suspected April 2025 attack on Spain and Portugal’s grid reinforced the demand for critical infrastructure protection, threat-intel, and incident-response retainer services.

Multi-Cloud Adoption by European SMEs to Meet GDPR Enhancing MSS Uptake

SMEs 99% of EU businesses are deploying multi-cloud to balance agility and data-residency rules, yet 74% lack internal cyber-awareness programmes. Providers offering unified cloud posture management and compliance dashboards are winning new contracts, fuelling sustained growth of the Europe security services market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Data-Sovereignty Rules Inflating Pan-EU Compliance Cost | -0.8% | EU-wide, particularly affecting cross-border services | Medium term (2-4 years) |

| Public-Sector In-Country Procurement Preference Limiting Cross-Border Scale | -0.6% | National governments, strongest in France, Germany | Long term (≥ 4 years) |

| Mid-Market Budget Freezes Amid EU Slowdown Delaying Premium TI Services | -0.4% | Mid-market enterprises across EU | Short term (≤ 2 years) |

| Schrems II-Driven Cloud-Data Skepticism Slowing SECaaS Adoption | -0.5% | EU-wide, particularly affecting US cloud providers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Data-Sovereignty Rules Inflating Pan-EU Compliance Cost

Twenty-three member states missed the NIS2 transposition deadline, forcing providers to navigate divergent frameworks and sustain multiple compliance workstreams that erode economies of scale.[3]Ropes & Gray, “The EU's NIS2 Directive Is in Force – but Can It Be Enforced?” ropesgray.com This complexity especially burdens cross-border SOCs.

Public-Sector In-Country Procurement Preference Limiting Cross-Border Scale

France’s intervention to shield Atos underlines a sovereignty-first stance that fragments demand and privileges local champions over pan-European offerings. The constraint dampens uniform service rollout for large governmental contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Advisory Depth Sustains Professional Services Lead

Professional services generated the largest slice of the Europe security services market in 2025, claiming a 45.32% revenue share as enterprises sought bespoke NIS2 and post-quantum readiness audits. High-value consulting projects frequently anchor multi-year managed security contracts, allowing vendors to embed staff on-site and cross-sell threat-intelligence subscriptions. Regulatory upheaval, mergers, and the looming PQC cut-over together create a steady backlog of gap assessments and remediation roadmaps.

Managed security services, however, remain the expansion engine, growing at a 6.41% CAGR through 2031. The cyber-skills gap, coupled with a board-level appetite for measurable outcomes, propels the demand for MDR, XDR, and SOC-as-a-service bundles. Sophos’s SecureWorks absorption and Orange Cyberdefence’s EUR 1.1 billion (USD 1.2 billion) turnover illustrate how scale, AI telemetry, and 24/7 coverage underpin competitive edge. Vendors that fuse compliance content, advanced analytics, and sector-specific playbooks are best placed to monetize the European security services market.

By Security Domain: Cyber Services Outpace Physical Integration

Cybersecurity services commanded 63.12% of 2025 revenue and are advancing 6.32% annually as organizations safeguard hybrid IT-OT estates. Cloud-native firewalls, zero-trust network access and threat-intel APIs are now standard purchase bundles. The rapid digitalization of hospitals, utilities, and manufacturing elevates the demand for unified cyber-physical monitoring centers.

Physical security incumbents pivot by embedding IoT sensors, video analytics, and access-control telemetry into broader cyber threat analytics platforms. Securitas, for instance, grew its technology integration segment to 32% of group sales, signaling a structural realignment toward converged offerings. Providers who can ingest badge logs, CCTV metadata, and industrial control signals into SIEM lakes will unlock new addressable pockets within the Europe security services market.

By Deployment Mode: Cloud Momentum Challenges On-Premise Dominance

On-premise deployments still accounted for 57.25% of 2025 spending, reflecting sovereignty concerns and entrenched data-center investments, particularly among critical infrastructure operators. Yet cloud models post a 6.03% CAGR, with SMEs leveraging pay-as-you-go SOC tooling and shared threat-intel lakes to sidestep capital outlays. Schrems II compliance anxieties channel workloads into EU-based clouds, benefiting regional IaaS providers and SOCs that guarantee explicit data-residency.

Hybrid architectures emerge as the pragmatic path, allowing retention of ultra-sensitive telemetry on-site while using cloud analytics for scale-out correlation and PQC algorithm updates. Deutsche Telekom’s 10.8% order-entry growth at T-Systems underscores how hybrid cloud security projects now form a staple share of enterprise transformation roadmaps.

By Organisation Size: SME Demand Becomes Prime Growth Lever

Large enterprises delivered 71.35% of 2025 turnover, buoyed by mature security operations and compliance pressures across global footprints. Even so, SMEs are the momentum story, expanding at 6.22% CAGR as NIS2 scope widens to mid-caps. ENISA’s SME classification framework (Digital Enabler, Digitally Based, Digitally Dependent) drives segmented offers—ranging from virtual CISO retainers to turnkey MDR bundles—allowing providers to harvest latent demand cost-effectively.

The cyber-skills crunch bites harder in small firms: 82% report staffing shortages, pushing them toward subscription SOCs, automated phishing simulation and managed endpoint detection. Vendors tailoring price points to OPEX budgets, coupled with compliance dashboards that simplify reporting, are poised to capture incremental share of the Europe security services market.

By End-User Industry: Healthcare Overtakes as Growth Frontier

BFSI retained leadership with 24.12% revenue share in 2025, driven by PSD2 open-banking interfaces and stringent payment-service risk controls. Zero-trust mandates, API shielding and real-time fraud analytics remain core purchase drivers.

Healthcare, however, registers the briskest 5.82% CAGR. Ransomware assaults on EU hospitals jumped 160% in 2024, exposing life-critical systems and prompting the European Commission’s dedicated sectoral action plan. Providers that bundle incident-response retainers, medical-device penetration testing and patient-data privacy consulting command premium margins within the Europe security services market.

Geography Analysis

The United Kingdom generated 21.68% of 2025 revenues, anchored by a dense financial-services ecosystem and government backing for the National Cyber Security Centre. Its vendor landscape includes 960 software-security firms, 66 AI cyber innovators and several unicorn exits, such as Darktrace’s USD 5.32 billion buy-out. Yet the talent gap remains acute, and diverging post-Brexit data regimes inject complexity into cross-border service delivery.

Germany represents the EU’s largest national opportunity, with enterprises spending EUR 11.2 billion (USD 12.1 billion) on cyber controls in 2024. Losses linked to cyber incidents reached EUR 179 billion (USD 193.4 billion) that year, galvanising board-level attention to SOC modernisation and industrial-control-system hardening. Berlin’s research grants and a forthcoming “Cyber Dome” with Israel bolster its R&D pull.

France exhibits the fastest trajectory at a 6.98% CAGR through 2031, underpinned by the EUR 1 billion (USD 1.08 billion) France 2030 allocation and Olympic-driven security demands. ANSSI’s proactive stance accelerates adoption of managed detection, cryptography upgrades and sovereign-cloud SOCs. Italy, the Nordics and Benelux each show above-average momentum owing to new national cybersecurity laws, cross-sector incident spikes and state investment programmes, collectively broadening the Europe security services market’s geographic spread.

The security services market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for North America, Asia, and Latin America.

Competitive Landscape

Market structure is moderately concentrated. The five largest vendors jointly control an estimated 42% of 2024 revenue, leaving space for regional specialists and disruptive AI platforms. Consolidation remains a favoured playbook, as illustrated by Sophos’s USD 859 million Secureworks purchase, Orange Cyberdefence’s serial acquisitions and Thoma Bravo’s roll-up of Darktrace. Providers compete on three pillars: demonstrable NIS2 and GDPR compliance expertise, AI-driven analytics that cut mean-time-to-detect, and the ability to fuse cyber and physical telemetry for critical-infrastructure clients.

IBM’s alliance with Telefónica Tech around quantum-safe encryption positions both for the EU-mandated PQC transition, while Cisco’s zero-trust reference architectures shore up mid-market deployment velocity. Physical-security giants such as Securitas and G4S pursue technology integration to transition from guarding contracts to converged cyber-physical service bundles.

White-space opportunities persist in SME-centric MDR offerings, sector-specific threat-intel (healthcare, energy utilities) and managed PQC migration. Players that automate compliance reporting, leverage generative AI for incident triage and layer consulting around strategic roadmaps are set to gain incremental share of the Europe security services market.

Europe Security Services Industry Leaders

IBM Corporation

Atos SE (Eviden Cybersecurity)

Orange Cyberdefense (Orange S.A.)

Accenture PLC

BT Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: NATO allies pledged to spend 1.5% of GDP on cyber resilience by 2035, guaranteeing a durable public-sector revenue pipeline and reshaping five-year planning cycles.

- June 2025: The European Commission issued a coordinated post-quantum cryptography roadmap, requiring member-state transition plans by Dec 2026 and completion for high-risk use cases by 2030.

- April 2025: A suspected cyberattack on the Iberian power grid triggered nationwide outages, accelerating energy-sector security budgets and crisis-management engagements.

- March 2025: Deutsche Telekom’s FY 2024 results highlighted a 10.8% rise in T-Systems order entry, largely fuelled by hybrid-cloud security projects.

Europe Security Services Market Report Scope

Security services are processes or comprehensive services that improve an organization's protection and security against common cyberattacks, including phishing, malicious software, and ransomware. These services encompass design and integration, deployment, risk and threat analysis, and consultation. Managed and hosted security services and solutions can be supplemented using cloud services, artificial intelligence (AI), biometrics, Internet of Things (IoT), and other remote services.

The European security services market is segmented by service type (managed security services, professional security services, consulting services, and threat intelligence security services), mode of deployment (on-premise and cloud), end-user industry (IT and infrastructure, government, industrial, healthcare, transportation and logistics, banking, and other end-user industries), and country (United Kingdom, Germany, France, and Rest of Europe). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Managed Security Services (MSS) |

| Professional Security Services |

| Consulting and Advisory Services |

| Threat Intelligence Services |

| Managed Detection and Response (MDR) |

| Cyber Security Services |

| Physical Security Services |

| On-Premise |

| Cloud |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| IT and Infrastructure |

| Government and Public Sector |

| BFSI |

| Industrial and Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Retail and E-Commerce |

| Energy and Utilities |

| Telecom |

| Other Industries |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Benelux |

| Nordics |

| Rest of Europe |

| By Service Type | Managed Security Services (MSS) |

| Professional Security Services | |

| Consulting and Advisory Services | |

| Threat Intelligence Services | |

| Managed Detection and Response (MDR) | |

| By Security Domain | Cyber Security Services |

| Physical Security Services | |

| By Deployment Mode | On-Premise |

| Cloud | |

| Hybrid | |

| By Organisation Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By End-User Industry | IT and Infrastructure |

| Government and Public Sector | |

| BFSI | |

| Industrial and Manufacturing | |

| Healthcare and Life Sciences | |

| Transportation and Logistics | |

| Retail and E-Commerce | |

| Energy and Utilities | |

| Telecom | |

| Other Industries | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Benelux | |

| Nordics | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe security services market?

The Europe security services market size stood at USD 19.95 billion in 2026 and is forecast to reach USD 26.35 billion by 2031.

Which segment is growing fastest within the market?

Managed security services are projected to post a 6.41% CAGR to 2031, the highest among service categories.

How does NIS2 influence enterprise security spending?

NIS2 expands mandatory cyber-risk budgets to more sectors and medium-sized firms, lifting average security spend to 9% of IT budgets and driving demand for managed detection, advisory and compliance services.

Why is healthcare a high-growth vertical?

A 160% surge in ransomware attacks and 309 major incidents in 2024 prompted an EU action plan, elevating healthcare cyber budgets and creating rapid uptake of managed security solutions.

Page last updated on: